Tech, Trade Tensions, and Tightening: Key Market Topics ... · As of December 31, 2017 for...

26

Tech, Trade Tensions, and Tightening: Key Market Topics for Spring April 19, 2018 Rebecca Patterson Chief Investment Officer Alex Christie Portfolio Manager

Transcript of Tech, Trade Tensions, and Tightening: Key Market Topics ... · As of December 31, 2017 for...

Tech, Trade Tensions, and Tightening: Key Market Topics for Spring

April 19, 2018

Rebecca PattersonChief Investment Officer

Alex ChristiePortfolio Manager

This summary is for your general information. The discussion of any tax, charitable giving, or estate planning alternatives and other observations herein are not intended as legal or tax advice and do not take into account the particular estate planning objectives, financial situation or needs of individual clients. This summary is based upon information obtained from various sources that Bessemer believes to be reliable, but Bessemer makes no representation or warranty with respect to the accuracy or completeness of such information. Views expressed herein are current only as of the date indicated and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in law, regulation, interest rates, and inflation.

Past performance is no guarantee of future results. This material is provided for your general information. It does not take into account the particular investment objectives, financial situation, or needs of individual clients. This material has been prepared based on information that Bessemer Trust believes to be reliable, but Bessemer Trust makes no representation or warranty with respect to the accuracy or completeness of such information. This presentation does not include a complete description of any fund or portfolio mentioned herein and is not an offer to sell any securities. Investors should carefully consider the investment objectives, risks, charges, and expenses of each fund or portfolio before investing.

Views expressed herein are current only as of the date indicated, and are subject to change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopolitical conditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, and our view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Index information is included herein to show the general trend in the securities markets during the periods indicated and is not intended to imply that any referenced portfolio is similar to the indices in either composition or volatility. Index returns are not an exact representation of any particular investment, as you cannot invest directly in an index.

2

Agenda

§ Technology: Sector in the Spotlight and How Bessemer Is Positioned

§ Trade Tensions: Putting in Context and Looking Ahead

§ Tightening: How the Federal Reserve Views the Economic Outlook and What It Means for Portfolios

§ Key Takeaways and Current Portfolio Positioning

3

Technology is … Massive

4

Left as of April 17, 2018. Right as of December 31, 2017. Source: FactSet, Bureau of Economic Analysis

S&P 500 Sector Weights Capital Spending as a Share of GDP

Information Technology 25.0%

Health Care13.7%

Financials 14.6%Industrials 10.1%

Consumer Discretionary

12.6%

Consumer Staples7.6%

Energy 6.1%Materials 2.9%

Utilities 2.8%

Telecom Services1.9% Real Estate 2.8%

IT Equipment, Software and R&D

42%

Other58%

Technology is … Accelerating

5

Cloud

Digital

Big Data

IoT AI

SaaS

Mobile

Social Media e-commerce

Automation

Cyber Security

Block Chain

0%

10%

20%

30%

40%

50%

Apr 17 Jul 17 Oct 17 Jan 18 Apr 18

The Technology Sector Has Performed Well

6

S&P Tech Sector

S&P 500

Average Return 33%

One-Year Total ReturnIndexed to 0 on April 13, 2017

One-Year Total Return, Tech Sector Constituents

As of April 17, 2018. Source: FactSet

-20% 20% 60% 100% 140%Advanced Micro Device

SymantecWestern Union Company

CorningQUALCOMM

CAKLA-Tencor

FacebookCadence Design Systems

Fidelity National Information ServicesFiserv

Alphabet (Class C)Hewlett Packard Enterprise

Motorola SolutionsCisco Systems

Activision BlizzardCognizant Technology Solutions

MicrosoftFLIR Systems

Applied MaterialsLam Research

NetAppRed HatNVIDIA

Bessemer Technology Exposure

We like many attributes of technology stocks, and portfolios have benefited from being overweight§ High gross margins and returns on investments

§ Solid growth prospects

§ Competitive advantages

§ Low use of debt

§ Reduced cyclicality

Tech themes in Bessemer equity portfolios§ Cloud

§ Digitalization/software/SaaS

§ Payment technologies

§ e-commerce platforms

§ Artificial intelligence

7

Bitcoin Interest and Prices Skyrocketed in 2017

8

As of March 21, 2018. Google search numbers represent search interest relative to the highest point on the chart for the given region and time. A value of 100 is the peak popularity for the term. A value of 50 means that the term is half as popular. A score of 0 means there was not enough data for this term.Source: Bloomberg, Google

0

10

20

30

40

50

60

70

80

90

100

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2013 2014 2015 2016 2017 2018

Bitcoin per U.S. Dollar (L)Google Searches: Bitcoin (R)

Bitcoin Per Dollar and Worldwide Google Searches for Bitcoin

Crypto Not Ready to Replace Mainstream Currencies or Gold Anytime Soon

Attribute Fiat Money Gold Crypto Currencies

Store of value Yes Yes Sometimes

Easy to hold/exchange Yes Sometimes Usually

Universally accepted Yes Yes No

Stability of value Usually Usually No

Legal oversight Yes Yes No

Anonymity No No Yes

9

Central Banks Around the World Working on Sovereign Cryptocurrencies

10

As of January 2018. CBCC stands for Central Bank Crypto Currency. Source: Bank for International Settlements, Bessemer Trust

Agenda

§ Technology: Sector in the Spotlight and How Bessemer Is Positioned

§ Trade Tensions: Putting in Context and Looking Ahead

§ Tightening: How the Federal Reserve Views the Economic Outlook and What It Means for Portfolios

§ Key Takeaways and Current Portfolio Positioning

11

Key U.S. Trade Developments

12

As of April 6, 2018. Unfilled bars represent as-yet-unimplemented tariffs.

Source: J.P. Morgan

Tariffs on U.S. Tariffs on China

Announced Tariffs by China and U.S.

Billions

$2.2

-$0.8

$3

-$3

$50

-$50

$150

-$100 $0 $100 $200

U.S. Wash Mach/Solar Panels (Jan 22)

CH Retaliation on Sorguhm (Feb 4)

U.S. Steel & Ali (Mar 18)

CH Steel & Ali Retaliation (Apr 2)

U.S. Section 301 (Apr 3)

CH Retaliation to Section 301 (Apr 4)

U.S. Revised Section 301 (April 5)

As-Yet-Unimplemented

Tariffs

Potential Next Steps?

§ CFIUS legislation§ China technology and

“reciprocity”§ Comment window for Section

301 proposals§ Outlines of NAFTA deal§ TPP???

Key U.S. Fiscal Developments

December 2017: Tax Cuts and Jobs Act§ Includes provisions to lower corporate tax rate, as well as change international taxes, taxation of

domestic business activity, individual income taxes, estate and gift taxes

– Top individual tax rate lowered from 39.6% to 37%; maximum deduction for state/local real estate, personal property and either income or sales taxes capped at $10,000 (previously no limit)

– Top corporate tax rate lowered from 35% to 21%; one-time deemed repatriation tax on accumulated foreign earnings at 8% for active business and 15.5% for liquid assets (“cash”), to be paid over eight years

February 2018: Spending Package§ Two-year plan to increase both defense and non-defense spending by a total of roughly $300 billion

§ Federal debt ceiling raised through March 2019

CBO’s Take:§ Stimulus should boost GDP over next few years but longer-term potential growth is likely to remain

around 2%

§ Budget deficit rising toward 5% of GDP while federal debt on track to rise from 76.5% of GDP in 2017 to 96.2% by 2028

13

As of April 9, 2018. Source: Congressional Budget Office, Capital Economics

1968 1978 1988 1998 2008 2018 2028-10%-8%-6%-4%-2%0%2%4%

U.S. Fiscal Developments: Visual ImplicationsFederal Budget Balance

Percent of GDP

14

14%

17%

20%

23%

26%

1968 1978 1988 1998 2008 2018 2028

Revenue

Outlays

0%

1%

2%

3%

4%

1968 1978 1988 1998 2008 2018 20280.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2010 2013 2016 2019 2022 2025 2028

April 2018

June 2017

Federal Interest CostsPercent of GDP

Federal Outlays & RevenuePercent of GDP

Real Potential GDPYoY

CBO Projections

CBO ProjectionsCBO

Projections

CBO Projections

Equity Tug of War with Fiscal and Trade Policies

15

As of April 16, 2018. Equity Market is measured using the S&P 500. Source: Bloomberg

Equity Market Lows Holding as Trade Policy Remains in Focus

2300

2400

2500

2600

2700

2800

2900

Mar 17 May 17 Jul 17 Sep 17 Nov 17 Jan 18 Mar 18

"Conciliatory" Xi Speech

Metal Tariffs

Inflation Fear+Vol Sell-Off

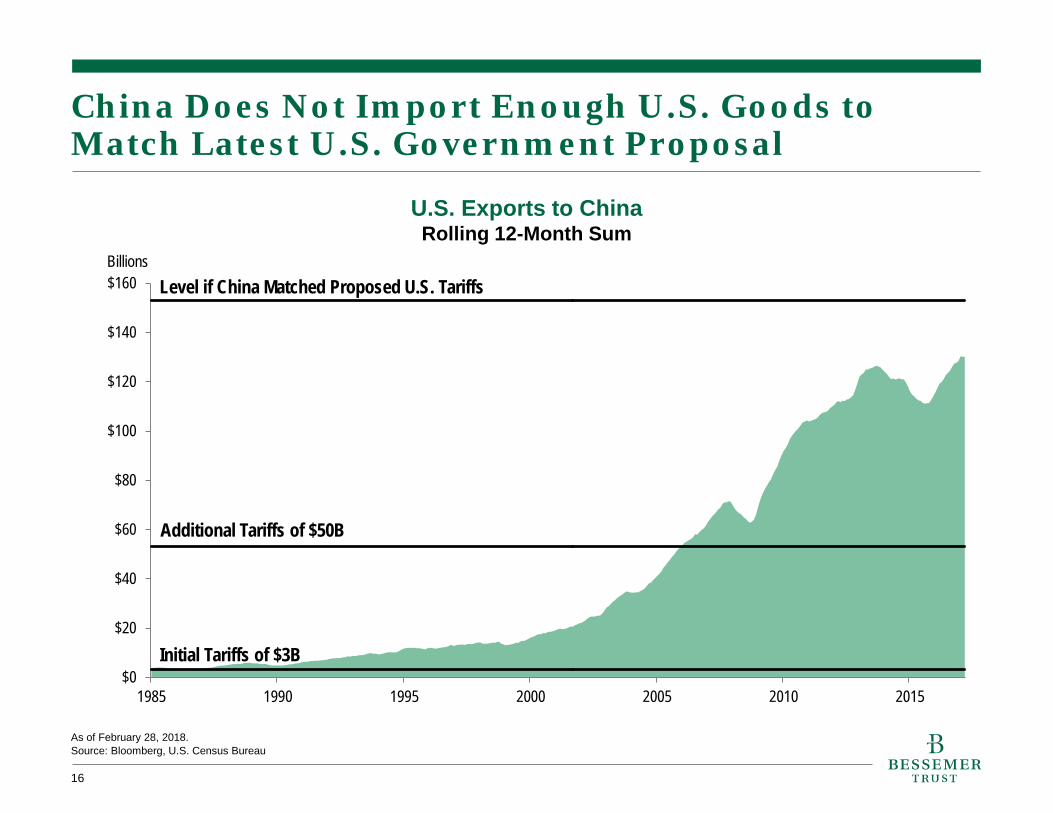

China Does Not Import Enough U.S. Goods to Match Latest U.S. Government Proposal

16

As of February 28, 2018. Source: Bloomberg, U.S. Census Bureau

$0

$20

$40

$60

$80

$100

$120

$140

$160

1985 1990 1995 2000 2005 2010 2015

U.S. Exports to ChinaRolling 12-Month Sum

Initial Tariffs of $3B

Additional Tariffs of $50B

Level if China Matched Proposed U.S. Tariffs Billions

6.0

6.1

6.2

6.3

6.4

6.5

6.6

6.7

6.8

6.9

7.0

Apr 13 Dec 13 Aug 14 Apr 15 Dec 15 Aug 16 Apr 17 Dec 17

China Has Other Options for Trade Retaliation

17

As of April 16, 2018. Source: Bloomberg

August 2015 Devaluation

Chinese Renminbi Has Room for Depreciation/Devaluation If NeededChinese Renminbi per U.S. Dollar

-40%

-30%

-20%

-10%

0%

10%

20%

30%

-30

-20

-10

0

10

20

30

40

2004 2006 2008 2010 2012 2014 2016 2018

Equipment Spending (Right)Composite Capex Plans Index (Left)

YoY, SAAR

What Will Matter Most to Corporate Decision-Makers: Fiscal Policy or Trade?

As of December 31, 2017 for equipment spending. As of March 31, 2018 for composite capex plans index. Composite capex plans index is the average of planned capex series from the Dallas Fed, Kansas City Fed, NY Fed, Philly Fed, and Richmond Fed Manufacturing Surveys. Source: Strategas, Federal Reserve, U.S. Bureau of Economic Analysis

Capex Plans vs. Actual Capex

18

Agenda

§ Technology: Sector in the Spotlight and How Bessemer Is Positioned

§ Trade Tensions: Putting in Context and Looking Ahead

§ Tightening: How the Federal Reserve Views the Economic Outlook and What It Means for Portfolios

§ Key Takeaways and Current Portfolio Positioning

19

U.S. Expansion Mature, but Recession Not Imminent

As of March 31, 2018. Recession colors indicate: green (positive economic growth momentum), yellow (neutral momentum) and red (weakening momentum). Source: Bloomberg, National Bureau of Economic Research

Yield Curve Not Yet InvertedDifference Between 10-Year and 2-Year Yields

Key Recession Indicators

20

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1977 1985 1993 2001 2009 2017

Recession Jobless claims

ISM services

ISM manufacturing

Consumer confidence

Personal consumption

Existing home sales

Single family housing permits

Yield curve

Vehicle sales

Investment grade bond spreads

Will Higher U.S. Bond Yields Attract Enough Buyers?

21

As of December 31, 2017.Source: Bloomberg, U.S. Treasury

Foreign Official Holdings of U.S. Securities Percent of Reserves

50%

52%

54%

56%

58%

60%

2001 2005 2009 2013 2017

-120

-100

-80

-60

-40

-20

0

20

40

60

80

100

-35

-30

-25

-20

-15

-10

-5

0

5

1985 1990 1995 2000 2005 2010 2015

Europe Attracting and Keeping More Capital as Economy Recovers, Bond Yields Rise

Left as of February 28, 2018. ZEW data is based on surveys of up to 300 financial market experts. Consumer confidence and ZEW Eurozone Assessment of Current Situation are diffusion indices, meaning a reading above (below) 0 indicates that more (fewer) surveyed individuals reported a positive view on a scale of -100 to 100. Source: Bloomberg, Eurostat, ZEW Zentrum fuer Europaeische Wirtschaftsforschung GmbH

Consumer Confidence and Assessment of the Current Economy Near All-Time Highs

ZEW Eurozone Assessment of Current Situation (R)

Consumer Confidence (L)

German Bond Yields Rise on Improved OutlookGerman 10-Year Government Bond Yield

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

Jan 16 Jul 16 Jan 17 Jul 17 Jan 18

22

Higher Interest Rates Don’t Guarantee Strong USD

23

As of January 31, 2018. U.S. dollar is measured using the Federal Reserve Trade-Weighted Major Currencies Index.Source: Bloomberg, Federal Reserve

85

90

95

100

105

110

115

-6 0 6 12 18 24 30 36Months Relative to First Hike

Mar 83 Feb 88Feb 94 Jun 99Jun 04 Dec 15

Start of Rate Hikes

Trade-Weighted U.S. Dollar Performance During Fed Tightening Cycles

Indexed to 100 the Month of the First Rate Hike

± Higher interest rates± Corporate repatriation± Strong U.S. growth/earnings

attracting capital flows

± Widening current-account deficit± Stronger overseas growth and

relatively attractive equity valuations pulling capital out of U.S.

± Central banks potentially shifting reserves at margin

Starting Month of Rate Hikes

Agenda

§ Technology: Sector in the Spotlight and How Bessemer Is Positioned

§ Trade Tensions: Putting in Context and Looking Ahead

§ Tightening: How the Federal Reserve Views the Economic Outlook and What It Means for Portfolios

§ Key Takeaways and Current Portfolio Positioning

24

Key Takeaways and Current Portfolio Positioning

25

Core Views Portfolio Implications

Global economy moderating into spring but still robust; central banks moving gradually

Hold equity exposure and modest underweight to fixed income

Late-cycle dynamics increasingly apparent; volatility likely to persist in coming quarters

Maintain defensive exposures within equity mandates as well as broader commodity exposure

Balance of payments dynamics offset rising interest rates; dollar range-bound to modestly weaker

Supportive for emerging market equities at the margin; commodities offer partial hedge for dollar

Political and policy uncertainty a risk for business and consumer confidence

Portfolio changes more likely if uncertainty starts to weigh on confidence indicators