TEAMSAI AND CAVOK JOIN FORCES - ARSAarsa.org/.../ARSA-CAVOK-2015MROAssessment-20150302.pdf ·...

86

-

Upload

trinhthien -

Category

Documents

-

view

214 -

download

0

Transcript of TEAMSAI AND CAVOK JOIN FORCES - ARSAarsa.org/.../ARSA-CAVOK-2015MROAssessment-20150302.pdf ·...

1 Copyright © 2015 CAVOK, a division of Oliver Wyman

TEAMSAI AND CAVOK JOIN FORCES

In 2013 the Aeronautical Repair Station Association (ARSA) announced a strategic partnership with TeamSAI,

an aviation consulting firm specializing in strategic, tactical and operational management solutions. The

relationship enabled the firms to combine ARSA’s industry knowledge and policy expertise with TeamSAI’s

betterinsight™ market intelligence service to create regular, high quality economic analyses of the global

aviation maintenance sector.

As of February 2, 2015, CAVOK, the aviation technical services and consulting division of international

consulting firm Oliver Wyman, has acquired and integrated TeamSAI into their business. The new CAVOK and

its betterinsight™ market intelligence service will continue to work with ARSA to provide critical information

to make its members more effective managers and leaders, and help lawmakers, regulators, journalists, and

voters better understand the economic consequences of policy decisions.

CONTENTS

EXECUTIVE SUMMARY ................................................................................................................................................... 3

STATE OF THE WORLD ................................................................................................................................................... 5

STATE OF THE AIRLINE INDUSTRY .................................................................................................................................. 7

GLOBAL AIR TRANSPORT FLEET FORECAST ................................................................................................................... 9

1. FLEET MIX ........................................................................................................................................................ 13

2. AIRCRAFT ORDERS IN 2014 ............................................................................................................................. 15

3. ORDER BACKLOG ............................................................................................................................................ 17

4. DELIVERIES AND RETIREMENTS ...................................................................................................................... 18

5. CARGO FLEET .................................................................................................................................................. 20

6. REGIONAL FLEET CHARACTERISTICS .............................................................................................................. 23

GLOBAL AIR TRANSPORT MRO MARKET FORECAST ..................................................................................................... 27

1. TOTAL MRO BY CLASS ..................................................................................................................................... 28

2. TOTAL MRO BY REGION .................................................................................................................................. 29

3. TOTAL MRO BY OEM ....................................................................................................................................... 31

4. TOTAL MRO BY AIRCRAFT FAMILY/MODEL ..................................................................................................... 33

5. IMPLICATIONS FOR MROS .............................................................................................................................. 35

AIRFRAME MAINTENANCE MARKET FORECAST AND STRUCTURE ............................................................................... 37

1. MARKET STRUCTURE ...................................................................................................................................... 39

2. COST STRUCTURE ........................................................................................................................................... 41

3. SUPPLY CHAIN ................................................................................................................................................ 42

Copyright © 2015 CAVOK, a division of Oliver Wyman 2

ENGINE MAINTENANCE MARKET FORECAST AND STRUCTURE ................................................................................... 43

1. MARKET STRUCTURE ...................................................................................................................................... 47

2. COST STRUCTURE ........................................................................................................................................... 49

3. SUPPLY CHAIN ................................................................................................................................................ 50

COMPONENT MAINTENANCE FORECAST AND STRUCTURE ........................................................................................ 51

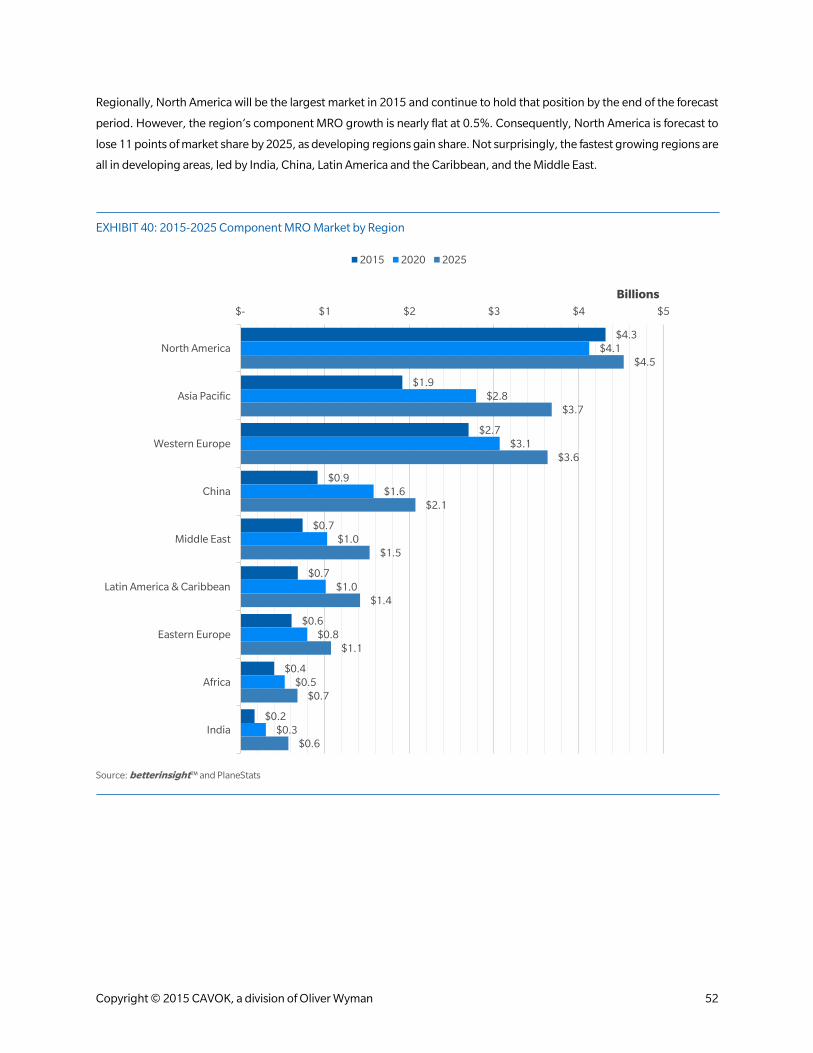

1. MARKET STRUCTURE ...................................................................................................................................... 53

2. COST STRUCTURE ........................................................................................................................................... 55

3. SUPPLY CHAIN ................................................................................................................................................ 56

LINE MAINTENANCE MARKET FORECAST AND STRUCTURE ........................................................................................ 57

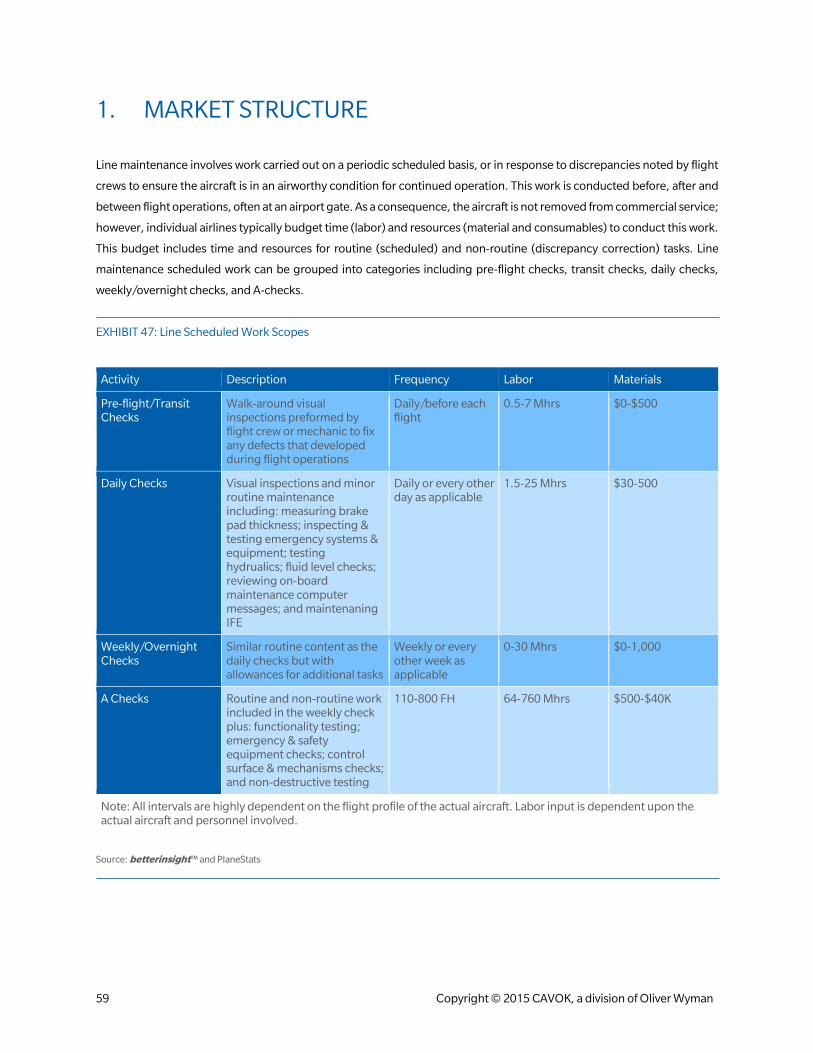

1. MARKET STRUCTURE ...................................................................................................................................... 59

2. COST STRUCTURE ........................................................................................................................................... 61

3. SUPPLY CHAIN ................................................................................................................................................ 62

GLOBAL MRO BALANCE OF TRADE .............................................................................................................................. 63

1. AIRFRAME MAINTENANCE (excluding modifications) ...................................................................................... 63

2. ENGINE MAINTENANCE .................................................................................................................................. 66

3. COMPONENT MAINTENANCE ........................................................................................................................ 68

GLOBAL BUSINESS AVIATION OUTLOOK FOR 2015 ..................................................................................................... 70

AVIATION MAINTENANCE INDUSTRY EMPLOYMENT & ECONOMIC IMPACT ............................................................... 74

1. AIRFRAME & LINE MAINTENANCE ................................................................................................................... 75

2. ENGINE MAINTENANCE .................................................................................................................................. 76

3. COMPONENT MAINTENANCE ........................................................................................................................ 77

4. U.S. EMPLOYMENT AND ECONOMIC IMPACT................................................................................................. 78

CONCLUSION .............................................................................................................................................................. 81

3 Copyright © 2015 CAVOK, a division of Oliver Wyman

EXECUTIVE SUMMARY

This report details CAVOK’s 2015 assessment and ten-year outlook of the air transport maintenance, repair, and overhaul

(MRO) market and a one year out look of the business aviation MRO market, starting with a review of global economic

conditions, a key driver for the health of the industry. The global economy is expected to improve in the coming years, but

concerns remain over the strength of the recovery. Generally, airlines operate with very thin margins with major cost

drivers such as labor, maintenance, and fuel, greatly influencing financial performance. Operators are increasingly

relentless in managing costs; with limited leverage over labor and fuel, airlines focus significant attention on managing

maintenance expenses.

The global commercial air transport fleet stands at nearly 24,000 aircraft. Approximately one-third is domiciled in North

America. Twenty percent is in Western Europe while Eastern Europe has five percent. Asia Pacific, China, and India

combined have slightly more than a quarter of the world’s fleet; however, the composition will be changing over the next

ten years. The North American share is expected to experience a decline of seven percent; any net growth is limited by the

large operators’ significant re-fleeting efforts. The Asian markets anticipate the highest growth rates, representing

opportunities for the MRO industry.

Globally, the 2015 air transport jet and turboprop MRO markets are expected to be $67.1B, piercing the $100B milestone

by 2025. This represents a healthy 4.1% compound annual growth rate (CAGR). The airframe, engine, component, and

line MRO market segments each have a different growth profile:

Airframe MRO 2015 forecast is $14.5B, increasing to $16.7B by 2025. This represents a 1.4% growth

rate, the slowest MRO segment during the forecast period. Airlines and their affiliated maintenance

providers maintain a solid hold on this market. The airframe MRO market is considered a low-margin,

labor intensive segment.

Engine MRO is expected to be $27.9B in 2015; growing at 5.3% annually it will reach $46.8B by 2025.

Unlike airframe MRO, the engine segment is largely contracted with the engine original equipment

manufacturers (OEMs) having a large share of the market. Engine MROs, recognizing the value of the

aftermarket, typically enjoy higher margin work.

Component MRO is forecast to be $12.4B in 2015, growing to $19.2B by 2025, representing a 4.4%

annual growth rate. Like the engine MRO business, much of the component segment is contracted,

though it varies greatly from one component type to the next. Similarly, the labor and material mix can

vary.

Line MRO is pegged at $12.3B in 2015 and forecast to grow at 3.7% annually to $17.8B by 2025. The

nature of line maintenance is less prone to contracting, and because the work is labor-intensive and

subject to limited ground times in a scheduled operation, the opportunities to take advantage of

economies of scale are limited.

Copyright © 2015 CAVOK, a division of Oliver Wyman 4

An examination of the flow of maintenance work among and between regions reveals that North America contracts more

airframe maintenance to the rest of the world than it provides to other regions. Engine maintenance, on the other hand, is

just the opposite. North America supports other regions with more capacity and throughput than its region demands.

Structural characteristics in the global economy such as labor rate differentials and complex supply chains have led to these

trends; however, as the differentiators between developed and developing regions narrow, North America will be ripe to

repatriate airframe maintenance currently contracted to other regions.

The business aviation fleet currently consists of nearly 31,400 aircraft requiring roughly $8.8B in MRO market activity in

2015. Nearly 67% (17,814) of the business aviation fleet is domiciled in North America.

In terms of economic activity, MRO plays a significant role. In the United States, approximately 4,023 firms with more than

218,000 employees operate in the civil MRO market (including airline employees). Small and medium-sized enterprises

(SME) account for 84% of these U.S. firms and 20% of all employees. There are 141,707 technicians in the U.S. and

approximately 37% are certificated.

5 Copyright © 2015 CAVOK, a division of Oliver Wyman

STATE OF THE WORLD

Seven years have passed since the last global financial crisis. Global recovery is weak and uneven, but economic

predictions for 2015 anticipate quickening economic growth. Emerging market and developing economies will continue

to be the largest portion of global growth, but output will remain below the levels seen in the 2010-2011 rebound. Led by

the United States and the United Kingdom, advanced economies are expected to pick up steam in 2015; however, the

spread between the growth rates of developed and developing economies is expected to widen slightly due to weakening

conditions that continue to linger in the advanced economies.

EXHIBIT 1: IMF World Economic Outlook Projections

Source: IMF World Economic Outlook – October 2014

World gross domestic product (GDP) is expected to grow by 3.8% in 2015 according to the October 2014 International

Monetary Fund (IMF) World Economic Outlook with the factors underlying global economic activity continuing to improve.

Significant risks, including spillover effects of central bank policies, and escalating geopolitical tensions in Eastern Europe

still remain.

Advanced economies are expected to see a 2.3% increase in GDP for 2015, a half a point increase over 2014 and nearly a

full point over the growth experienced in 2013. Drivers of the predicted growth acceleration are efforts to stabilize debt to

GDP ratios by reducing deficit spending, and enduring loose credit monetary policies that will keep interest rates at or near

record lows.

The U.S. is forecast to experience 3.1% GDP growth in 2015 driven by an accommodative monetary policy, strengthened

household balance sheets, and a healthy housing market. Across the Pacific, with the Japanese economic revival remaining

problematic, expected growth in 2015 is only 1.5%.

The euro zone, moving slowly out of recession, is expected to grow by 1.3% in 2015; however, considerable financial,

economic, and political challenges remain. Unexpected weakness in Germany and worsening conditions in France creates

1.2% 1.4%1.8%

2.3%

5.1%4.7%

4.4%5.0%

3.4% 3.3% 3.3%3.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2012 2013 2014 2015

Advanced Economies Emerging & Developing Economies World Output

Copyright © 2015 CAVOK, a division of Oliver Wyman 6

concern. Policymakers face significant challenges in restoring confidence in the financial sector; high levels of private and

public debt and unemployment create political instability risks. The euro zone priority is to achieve strong growth and

increase inflation, which implies that the euro zone will continue to loosen monetary policy, and may go as far as

purchasing sovereign assets if economic conditions do not improve.

Emerging and developing economies, including China, are expected to grow at 5.0% in 2015. Exports – driven by stronger

growth in advanced economies and stronger domestic demand encouraged by low levels of unemployment – are expected

to support this growth. While the emerging and developing economies are expected to experience the strongest growth

since 2012, their output will remain below the growth rates achieved during the 2010-2011 rebound. This reflects the long

lasting structural factors affecting all economies. Even as residential investment continues to slow in China, GDP is

projected to sustain its high growth at 7.1% in 2015, down just 0.3% from 2014. China’s growth in both 2014 and 2015 is

primarily the result of new tax relief policies adopted in the first half of 2014, increased infrastructure spending, and cuts

in required reserve ratios.

Growth in India is expected to increase substantially to 6.4% as demand for exports and investments continue.

In contrast to the two aforementioned high growth countries, the Commonwealth of Independent States is projected to

grow a mere 1.6%, reflecting the region’s deteriorating economic and geopolitical conditions. The low growth is due in

part to the situation in Ukraine, resultant sanctions placed upon Russia, and currently low oil prices.

The weak and uneven growth in GDP along with rising geopolitical tensions also negatively impact trade. In 2015, the

World Trade Organization projects global trade growth at 4.0%. Exports are projected to increase by 3.8% in developed

economies and 4.5% in developing economies while imports are expected to rise by 3.7%% in developed economies and

4.5% in developing economies.

There are signs that growth is picking up in both developed and developing countries, but the world continues to face a

fragile recovery. Economic issues have significant impact on the airline and MRO industries. Business environments

become increasingly challenging when conditions worsen.

A bright spot that has developed in recent months is the price of crude oil. The price of oil went into free fall during the last

quarter of 2014 and it is not expected to recover in 2015. While the increased supply and reduced cost of oil has a positive

impact on the world’s regions, except the Middle East, in 2015, the World Bank is forecasting that oil prices will break $100

per barrel again within the decade. With this in mind, market participants should carefully consider hedging options once

the price of oil has stabilized and begins to trend higher.

7 Copyright © 2015 CAVOK, a division of Oliver Wyman

STATE OF THE AIRLINE INDUSTRY

The graph below depicts IATA’s estimate that 3.3 billion passengers and 51.3 million metric tons of cargo were carried in

2014. The growth in traffic together with airline capacity discipline created first-time passenger load factors of 80%,

allowing the industry to record an estimated $19.9 billion in post-tax profits.

EXHIBIT 2: IATA Global Passenger and Freight Traffic Growth Forecasts

Source: IATA Industry Financial Forecast – June 2014

IATA believes the key elements for the best financial performance since 2010 are the development of ancillary revenue

sources, industry restructuring, falling fuel prices and the strong cyclical economic upturn. IATA also understands that the

upturn in advanced economies is a result of loose monetary policies, reduced budgetary tightening, and improving

balance sheets for households and banking.

Despite the presence of adverse developments in Ukraine, the stuttering euro area recovery, and growing terrorist and

militant actions in the Middle East, with low fuel prices expected throughout the year, the industry is forecast to improve

upon last year’s performance.

In 2015, passenger traffic is expected to be up 7.0%, well above the 20 year average of 5%, and cargo volumes are expected

to grow by 4.5%. The anticipated 7.3% passenger capacity growth will slightly exceed traffic growth, pushing the expected

load factor down a few tenths.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

$-

$5

$10

$15

$20

$25

$30

2013 2014 2015F

TRA

FFIC

GR

OW

TH R

ATE

S

PO

ST T

AX

PR

OFI

TS

BIL

LIO

NS

Post-Tax Profits Passenger Traffic Freight Traffic

Copyright © 2015 CAVOK, a division of Oliver Wyman 8

In addition to the strong traffic growth, airlines are expected to return a net profit of $25.0B in 2015, creating back-to-back

years of record profits. This increase in financial performance will be driven by marginally higher economic growth

expected in 2015, continued increases in revenue from ancillary services, improvements to industry structure and

efficiency, and substantially lower fuel prices.

EXHIBIT 3: Spot Prices of Crude Oil and Jet Fuel per Gallon

Source: U.S. Energy Information Administration

IATA is forecasting the price of jet fuel to average $2.38 per gallon in 2015, down from $2.78 per gallon in 2014, and thus

fuel costs are expected to decrease in 2015 as a percentage of airline operating costs to 26%. For the past several years,

fuel costs as a percent of total airline expenses have been hovering around 30%. Notwithstanding current low fuel prices,

improving fuel efficiency will continue to be a priority for airlines in 2015, and for the foreseeable future.

IATA’s 2015 forecast represents the most upbeat outlook the industry has seen in several years as traffic and profitability

are forecast to continue to improve; however, the airline industry remains a comparatively low margin business, and the

balance between profit and loss remains delicate. Net margins are expected to remain weak at 3.2% in 2015, and as such,

the industry remains highly susceptible to negative shocks.

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Jan

-04

Ap

r-0

4Ju

l-0

4O

ct-0

4Ja

n-0

5A

pr-

05

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6Ju

l-0

6O

ct-0

6Ja

n-0

7A

pr-

07

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8Ju

l-0

8O

ct-0

8Ja

n-0

9A

pr-

09

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0Ju

l-1

0O

ct-1

0Ja

n-1

1A

pr-

11

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2Ju

l-1

2O

ct-1

2Ja

n-1

3A

pr-

13

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4Ju

l-1

4O

ct-1

4

WTI Crude Oil Brent Crude Oil Kerosene-Type Jet Fuel

9 Copyright © 2015 CAVOK, a division of Oliver Wyman

GLOBAL AIR TRANSPORT FLEET FORECAST

The global commercial air transport fleet currently stands at nearly 24,000 aircraft and is expected to grow 3.9% annually

from 2015-2020 to 29,003 aircraft. Growth is expected to slow to 3.5% per year during the second five year period, bring

the total number of in service aircraft up to 34,408 by 2025.

EXHIBIT 4: 2015-2025 Global Fleet Forecast by Aircraft Class

Source: betterinsight™ and PlaneStats

13,124

16,949

21,089

4,686

5,753

7,181

3,396

3,222

2,906

2,721

3,079

3,232

23,927

29,003

34,408

5.2%

4.5%4.2%

4.5%

-1.0%

-2.0%

2.5%

1.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2015 2015-2020CAGR

2020 2020-2025CAGR

2025

Narrowbody Widebody Regional Jet Turboprop

Copyright © 2015 CAVOK, a division of Oliver Wyman 10

EXHIBIT 5: 2015-2025 Global Fleet Forecast by Aircraft Usage

Source: betterinsight™ and PlaneStats

Over the entire ten-year forecast, CAVOK predicts the global fleet will grow on average by 3.7% annually. The passenger

fleet is expected to grow at 3.8% annually and the cargo fleet by 2.3% annually.

22,056

26,947

32,062

1,871

2,056

2,346

23,927

29,003

34,408

4.1%

3.5%

1.9%

2.7%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2015 2015-2020CAGR

2020 2020-2025CAGR

2025

Passenger Cargo

11 Copyright © 2015 CAVOK, a division of Oliver Wyman

EXHIBIT 6: 2015-2025 Global Aircraft Demand

Source: betterinsight™ and PlaneStats

Fueling the 3.7% annual growth rate, CAVOK forecasts the delivery of 18,068 new passenger aircraft and 423 new cargo

aircraft over the next ten years, and the retirement of 7,346 passenger aircraft and 664 cargo aircraft over the same period.

In other words, 43% of the new deliveries over the forecast period are replacement aircraft while 57% are for growth. In

addition to deliveries of new aircraft and the retirement of current in-service aircraft, the 716 passenger to freighter

conversions of current in-service aircraft will play an integral role in the size and growth of the global cargo fleet, which is

discussed further in section five of this fleet forecast.

Copyright © 2015 CAVOK, a division of Oliver Wyman 12

EXHIBIT 7: 2015-2025 In-service Fleet Growth by Region

Source: betterinsight™ and PlaneStats

Just as the economic growth outlook varies widely from region to region, so too does the in-service fleet growth outlook.

At one extreme of the regional fleet growth outlook, North American airlines have created the highest demand for new

aircraft. Over 4,100 new aircraft are forecast to be delivered to the region over the next ten years with 78% of the deliveries

slotted as replacements for older aircraft. China, on the other hand, is experiencing just the opposite phenomenon where

2,548 deliveries will mostly support net growth. The systematic elimination and replacement of older, less fuel efficient

aircraft is expected to improve the bottom line of airlines by reducing fuel and maintenance costs over the life of the aircraft.

22%922

69%2,219

48%1,452

89%2,264

63%920 73%

96850%565

96%800

45%371

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

NorthAmerica

Asia Pacific WesternEurope

China LatinAmerica &Caribbean

Middle East EasternEurope

India Africa

Deliveries Retirements Net Growth

13 Copyright © 2015 CAVOK, a division of Oliver Wyman

1. FLEET MIX

Today, the global commercial airline fleet of western built jets and turboprops is made up of 13,124 narrowbodies, 4,686

widebodies, 3,396 regional jets, and 2,721 turboprops. While the airline fleet expected to grow by nearly 10,500 aircraft

by 2025, the complexion of the global fleet is not expected to experience drastic change.

The narrowbody (NB) fleet currently comprises nearly 55% of the total fleet with some 13,124 in-service aircraft. Over the

next ten-year period, its share will rise to 61%, growing to 21,089. The narrowbody is the fastest growing aircraft class and

is expected to achieve a 4.9% CAGR over the next ten years.

EXHIBIT 8: 2015-2025 Narrowbody Fleet Characteristics

2015 2020 2025

Fleet Size 13,124 16,949 21,089

CAGR N/A 5.2% 4.9%

Market Share 55% 58% 61%

Source: betterinsight™ and PlaneStats

Widebodies (WB) presently account for 20% of the total fleet. The in-service fleet will grow from 4,686 to 5,753 over five

years, and to 7,181 in ten years. Widebody market share will remain fairly constant over the forecast period. The widebody

fleet is also expected to achieve a robust CAGR of 4.4% over the forecast period.

EXHIBIT 9: 2015-2025 Widebody Fleet Characteristics

2015 2020 2025

Fleet Size 4,686 5,753 7,181

CAGR N/A 4.2% 4.4%

Market Share 20% 20% 21%

Source: betterinsight™ and PlaneStats

Copyright © 2015 CAVOK, a division of Oliver Wyman 14

Regional jets (RJ) currently make up roughly 14% of the total fleet, but that share will decline to 8% by 2025 as the fleet of

RJs shrinks from 3,396 to 2,906 in-service aircraft. This shrinking of the regional jet fleet is evidence of the up-gaging trend

that has been prevalent in recent forecasts as part of an industry wide effort to improve cost structure and profitability amid

volatile fuel prices.

EXHIBIT 10: 2015-2025 Regional Jet Fleet Characteristics

2015 2020 2025

Fleet Size 3,396 3,222 2,906

CAGR N/A -1.0% -1.5%

Market Share 14% 11% 8%

Source: betterinsight™ and PlaneStats

Turboprops (TP) account for 11% of the total fleet or 2,721 aircraft. Over the next five years, the in-service commercial

turboprop fleet will grow by 358 aircraft to 3,079. The fleet in 2025 is predicted to be 3,232 and make up 9% of the global

fleet.

EXHIBIT 11: 2015-2025 Turboprop Fleet Characteristics

2015 2020 2025

Fleet Size 2,721 3,079 3,232

CAGR N/A 2.5% 1.7%

Market Share 11% 11% 9%

Source: betterinsight™ and PlaneStats

15 Copyright © 2015 CAVOK, a division of Oliver Wyman

2. AIRCRAFT ORDERS IN 2014

Orders of typical usage types (passenger, freighter, combi, and quick-change) to commercial customers (airlines; airline

holding companies; banks; special purpose corporations; and financial lessors; and operating lease companies) during

2014 were as follows:

Gross orders from commercial customers in 2014 totaled 3,282, and net orders totaled 2,847.

Boeing won the orders battle by recording 1,296 net orders over Airbus’ 1,099.

EXHIBIT 12: 2014 Aircraft Orders by Aircraft Family/Series and Aircraft Class

Aircraft Class Aircraft Family/Series

NB WB RJ TP

Airbus A320CEO/NEO Family 967 49%

Airbus A330 Family 150 34%

Airbus A350 Family -32 -7%

Airbus A380 14 3%

ATR 42/72 155 82%

Boeing 737NG/MAX Series 992 51%

Boeing 747 Series 0 0%

Boeing 767 Series 4 1%

Boeing 777/777X Series 276 63%

Boeing 787 Series 24 6%

Bombardier CRJ Series 45 17%

Bombardier CSeries 59 22%

Bombardier QSeries 34 18%

Embraer E-Jet/E2 115 44%

Mitsubishi MRJ 24 9%

Sukhoi Superjet 100 20 8%

Total Net Orders 2,018 71% 436 15% 204 7% 189 7%

Source: betterinsight™ and PlaneStats

Copyright © 2015 CAVOK, a division of Oliver Wyman 16

An important factor in the 2014 order total relative to previous years was the significant drop in orders for widebody and

regional jet aircraft (namely A350, 787, and E-175/E-175 E2 aircraft), while A320CEO/NEO family and 737NG/MAX series

aircraft continued to dominate narrowbody orders with 97% of net narrowbody orders and 69% of net total orders.

Overall, 2,018 net narrowbody orders were placed by commercial customers. The 737NG/MAX series led narrowbody

orders with 992 net orders, while the A320 family and C-Series followed with 967 and 59 net orders, respectively.

Widebodies represented roughly 15% of net orders. Orders for widebodies in 2014 decreased substantially over the

previous year’s orders. The 2014 net total of 436 widebody orders was down from 607 net orders in 2013. The top-selling

widebody was the 777 with 276 net orders. The 787 received 24 net orders. The A350 received -32 net orders. Airbus

received 150 net orders for the A330, and 14 net orders for the A380. The 747 series received 2 orders and 2 cancellations

in 2014 resulting in 0 net orders.

Regional jet orders constituted 9% of net orders with 204 net orders. The E-Jet family led regional orders with 115 net

orders in 2014. Bombardier’s CRJ program received 45 net orders, and Sukhoi took 20 net orders. Mitsubishi’s MRJ took

24 new orders.

Turboprops orders also represented roughly 7% of net orders with 189 net orders. ATR received 155 net orders for ATR-

72/42 aircraft, and Bombardier received 34 net orders for Q400 aircraft.

17 Copyright © 2015 CAVOK, a division of Oliver Wyman

3. ORDER BACKLOG

The strong orders intake during the last few years has pushed the firm backlog to a record total of over 13,600 aircraft;

9,643 are narrowbodies (71%), 2,614 are widebodies (20%), 960 are regional jets (7%), and 344 are turboprops (3%). This

backlog is equal to 57% of the current in-service fleet.

Airbus has the largest share of the order backlog with 6,032 on order, while Boeing follows with 5,639 on order. All other

manufacturers account for the remaining 15% of aircraft on order.

This high level of backlog is equivalent to 8.5 years of production based on the 2014 delivery total. Production rates are

expected to increase for the 737 and 787, and several new aircraft programs are expected to launch in coming years. New

market entrants (A320NEO, 737MAX, CSeries, 787-10, 777-X, A350, C919, ARJ21, Embraer E2, MRJ, and MC-21)

represent 62% of the backlog.

EXHIBIT 13: 2015 Order Backlog by Aircraft Manufacturer and Aircraft Class

Source: betterinsight™ and PlaneStats

Copyright © 2015 CAVOK, a division of Oliver Wyman 18

4. DELIVERIES AND RETIREMENTS

As the world continues to recover from the global financial crisis, commercial aircraft manufacturers have never seen a

better market. In the face of historically high - although recently softening - fuel costs in combination with low interest rates

and a drive to reduce costs and increase profits, the airlines have generated unprecedented demand on the manufacturers

for more efficient and more reliable aircraft.

EXHIBIT 14: 2015-2025 Deliveries by Aircraft Class

Source: betterinsight™ and PlaneStats

During 2014, delivery of 1,575 new aircraft to operators made for another historic year. Boeing led with 692 deliveries

(44%) followed by Airbus with 611 (39%). Embraer delivered 90 (5%), ATR 76, Bombardier 77 (5%), and Sukhoi delivered

29 (2%).

The level of deliveries in the next few years is expected to remain high due to a strong backlog as well as expected

production rate increases by Airbus and Boeing. 8,865 aircraft are forecast to be delivered in the next five years, of which

64% will be narrowbodies, 22% widebodies, 8% regional jets, and 6% turboprops. Offsetting these deliveries will be nearly

3,800 retirements of current in-service aircraft, resulting in a net growth of 5,076 aircraft.

5,693

6,142

11,835 1,911

2,192

4,103

728

611 1,339

533

681 1,214

18,491

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2015-2020 2020-2025 2015-2025

Narrowbody Widebody Regional Jet Turboprop

19 Copyright © 2015 CAVOK, a division of Oliver Wyman

In the second five-year period, sustained traffic growth due to continued worldwide GDP growth, increasing need to

replace older generation aircraft with more fuel efficient and less maintenance intensive aircraft, and the build-up of

production rates for 737MAX, A320NEO, 787, A350, and other new market entrants will drive a forecast for a higher level

of deliveries—some 9,626. However, more than 4,200 retirements of current in-service aircraft are forecasted in the same

period, resulting in a net growth of 5,405 aircraft.

Over the ten years, overall deliveries will total 18,491. Roughly 44% of deliveries will be for replacement and 8,010 aircraft,

or roughly 33% of the current in-service fleet, will be retired.

EXHIBIT 15: 2015-2025 Retirements by Aircraft Class

Source: betterinsight™ and PlaneStats

Delivery financing is expected to be a key factor in upcoming years given the high levels of forecast deliveries and

anticipated increases in the cost of financing, due to expected interest rate increases in advanced economies. Lessors are

likely to take a larger role in the commercial aviation market with nearly 50% of the global commercial aircraft fleet

expected to be under an operating lease by the end of the forecast period.

(1,868)

(2,002)

(3,870)(844)

(764)

(1,608)

(902)

(927)

(1,829)

(175)

(528) (703)

(8,010)

(9,000)

(8,000)

(7,000)

(6,000)

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

02015-2020 2020-2025 2015-2025

Narrowbody Widebody Regional Jet Turboprop

Copyright © 2015 CAVOK, a division of Oliver Wyman 20

5. CARGO FLEET

The current cargo fleet of 1,871 in-service aircraft is forecast to grow an average of 2.3% a year to 2,346 by 2025. With short

haul and domestic traffic subject to strong competition by trucks in the U.S. and Europe, long haul traffic is the key to the

cargo market; however this market is being threatened by large bellied passenger aircraft such as the 777 which has 25%

more capacity under the floor than a 747-8. Over 35% of the existing active fleet will be retired over the next ten years,

reflecting the high average age of the freighter fleet which is 21.6 today and will be 21.4 in 2025.

EXHIBIT 16: 2015-2025 Cargo Fleet by Aircraft Class

Source: betterinsight™ and PlaneStats

All 423 of the new deliveries over the 10 year period are forecast to be widebodies, contributing to a slight reduction of the

cargo fleet age. New build freighter deliveries are destined to the larger carriers as longer range models, where their higher

utilization make them economically viable.

564 618 626

966

1,056

1,336

27

27

34

314

355

350

1,871

2,056

2,346

1.8% 0.3%

1.8%

4.8%0.0%

4.7%2.5%

-0.3%

0

500

1,000

1,500

2,000

2,500

2015 2015-2020CAGR

2020 2020-2025CAGR

2025

Narrowbody Widebody Regional Jet Turboprop

21 Copyright © 2015 CAVOK, a division of Oliver Wyman

EXHIBIT 17: 2015-2025 Cargo Aircraft Deliveries, Conversions, and Retirements

2015-2020 2020-2025

Deliveries 154 269

Conversions 324 392

Retirements 293 371

Source: betterinsight™ and PlaneStats

Some 716 conversions will account for 63% of the aircraft being added to the cargo fleet. The lower capital cost of

acquisition and conversion is critical to the economics for lower utilization markets. Reduced demand due to increased

competition from trucking and rail has led to fewer conversions being forecast.

EXHIBIT 18: 2015-2025 Conversions by Aircraft Class

Source: betterinsight™ and PlaneStats

187

148

335 50

113

163

9

22

31

78

109

187

716

0

100

200

300

400

500

600

700

800

2015-2020 2020-2025 2015-2025

Narrowbody Widebody Regional Jet Turboprop

Copyright © 2015 CAVOK, a division of Oliver Wyman 22

CAVOK forecasts that roughly 46% of the conversions during the forecast period will be narrowbody aircraft. Turboprop

aircraft will make up 26% of conversions over the next ten years, widebody aircraft will make up 23%, and regional jet

aircraft will make up the remaining 4% of conversions.

Interesting developments to watch in the future include conversion programs for the A320/321, A330, 737NG, 777,

CRJ100/200 aircraft and the success of the MD-80 program.

To date, the narrowbody passenger to freighter conversion market has been dominated by Boeing models, namely the

737-400. Airbus has not yet been able to develop an economical narrowbody freighter for several reasons, but chief among

them being technical issues related to the placement of the A320 family’s fly-by-wire system as it runs through the area

where the cargo door would typically be placed. Recently, however, PacAvi Group, in partnership with AeroTurbine, has

announced that it is launching a new program for conversion of A320/A321 aircraft and expects deliveries to begin in 2017

or earlier. It will be interesting to watch this program progress, especially since the A320 family passenger to freighter

conversion joint venture between Airbus and Irkut was shuttered due to technical challenges and costs.

The 737-800, much like its predecessor, the 737-400, will be a popular conversion candidate in the coming years. The

aircraft is capable of transporting one additional pallet over the 737-400 and is a proven, reliable airframe with much newer

technology.

The first MD-80 passenger to freighter supplemental type certificate was issued in 2013. This aircraft is considerably more

expensive to operate on an hourly basis than the slightly smaller Boeing 737-400 which burns about 12% less fuel;

however, the significantly lower ownership costs make this an attractive niche aircraft for low utilization cargo operators

whose aircraft spend a significant amount of time on the ground. Aeronautical Engineers estimates that a 737-400 can cost

between $3.3 million and $4.0 million where was an MD-80 will go for $750,000 to $800,000.

For some time now, Boeing has been promoting the 777 passenger to freighter conversion alongside the new build 777F

with little success. Technical design and cost issues related to replacing the composite floor beams are a major drawback

to the program and the widebody dedicated freighter market in general has been suffering in the past few years as the

airlines have been moving more cargo in the bellies of large passenger aircraft amidst high fuel prices and soft demand for

expedited cargo shipments. This shift away from dedicated freighters to the bellies of passenger aircraft has also affected

the success of the A330 passenger to freighter conversion program as well as the new build A330 new build freighter.

Lastly, the CRJ passenger to freighter conversion program was launched in 2013 by Miami based Aeronautical Engineers,

Inc., but it remains to be seen whether or not there is a market for these small freighters, especially since the CRJs will have

to compete against the lower cost turboprop freighters such as the ATR72. CAVOK forecasts more than 120 ATR

conversions over the next ten years and only 30 CRJ conversions over the same period.

23 Copyright © 2015 CAVOK, a division of Oliver Wyman

6. REGIONAL FLEET CHARACTERISTICS

The global commercial air transport fleet currently stands at nearly 24,000 aircraft. Approximately one-third of the fleet is

domiciled in North America. Twenty percent of the fleet is in Western Europe; Eastern Europe adds another 5%. Asia

Pacific, China, and India combined have slightly more than a quarter of the world’s fleet. However, the fleet composition is

changing. North America, which is experiencing significant re-fleeting, is expected to see its share decline by 7%, as its net

growth is very limited. Emerging markets in Asia are expected to see a greater share of the market, and therefore represent

the MRO growth engines for the industry.

EXHIBIT 19: 2015-2025 Fleet Share Change by Region

Source: betterinsight™ and PlaneStats

-7%

-3%

1%

1%

1%

1%

2%

2%

3%

-8% -6% -4% -2% 0% 2% 4%

North America

Western Europe

Africa

Latin America & Caribbean

Eastern Europe

Middle East

Asia Pacific

India

China

Copyright © 2015 CAVOK, a division of Oliver Wyman 24

EXHIBIT 20: 2015-2025 Fleet Growth by Region

Source: betterinsight™ and PlaneStats

The African fleet of 1,030 aircraft is forecast to grow 3.6% annually in the first five-year period to 1,228 aircraft by 2020

and 6.3% in the second-five year period to 1,670 aircraft by 2025.

Over the forecast period, 821 aircraft are forecast to be delivered while 450 currently in-service aircraft are forecast to be

retired. Africa is expected to receive over 270 net migrations over the forecast period, the majority of which are expected

to migrate from Western Europe.

The North American commercial fleet of 7,420 aircraft is, and will continue to be, the largest fleet throughout the ten-

year forecast period, although its share of the fleet declines from 31% to 24% of the in-service fleet.

CAVOK views North America as a mature market that will experience minimal fleet growth over the forecast period. The

North American commercial fleet is forecast to grow 1.2% annually to 7,874 aircraft by 2020 and by 0.7% to 8,142 aircraft

by 2025.

North America is forecast to receive 22% of the worldwide total deliveries over the next ten years (4,112 aircraft).

1,287

726

772

507

373

453

306

454

198

1,032

1,377

332

490

549

408

507

268

442

0 500 1,000 1,500 2,000 2,500

Asia Pacific

China

Western Europe

Latin America & Caribbean

Middle East

Eastern Europe

India

North America

Africa

2020 2025

25 Copyright © 2015 CAVOK, a division of Oliver Wyman

The current commercial fleet in India of 385 aircraft is forecast to grow 12.4% annually in the first five-year period to 691

aircraft by 2020 and by 11.6% per year in the second-five year period to 1,198 aircraft in 2025. Despite the high growth

rate, India will still have the smallest fleet in 2025 (3% share of global fleet) as limited infrastructure and significant

competition from rail continue to limit India’s aviation potential.

Over the forecast period, 832 aircraft are forecast to be delivered and very few aircraft currently in-service are forecast to

be retired in India due to the already young age of the country’s fleet.

The Eastern European fleet of 1,294 aircraft is forecast to grow 6.2% annually in the first five-year period to 1,747 aircraft

by 2020 and by 4.3% in the second-five year period to 2,155 aircraft in 2025.

Over the forecast period, 1,123 aircraft are forecast to be delivered, while 558 aircraft currently in-service are forecast to

be retired in the region. Eastern Europe is expected to receive over 280 net migrations over the forecast period, a large

portion of which are expected to come from Western Europe.

The fleet in the Middle East of 1,174 aircraft is forecast to grow 5.7% annually in the first five-year period to 1,547 aircraft

by 2020 and by 6.3% in the second-five year period to 2,096 aircraft in 2025.

Over the forecast period, 1,327 aircraft are forecast to be delivered and 359 aircraft currently in-service are expected to be

retired in the region.

The commercial fleet in Latin America and the Caribbean of 1,720 aircraft is forecast to grow 5.3% annually in the first

five-year period to 2,227 aircraft by 2020 and by 4.1% in the second-five year period to 2,717 aircraft in 2025.

Over the forecast period, 1,462 aircraft are forecast to be delivered while 542 currently in-service aircraft are expected to

be retired in the region. Latin America is forecast to receive over 70 net migrations over the forecast period, mostly from

Western Europe and North America.

Western Europe has the second largest commercial fleet (4,837 in-service aircraft). While Western Europe is a mature

market in most respects, it also has some characteristics of a growth market when considering the prominence of low-cost

carriers in the region. Currently, the Western European fleet comprises 20% of the global commercial fleet, and, in ten

years’ time, Western Europe’s share of the global fleet is expected to decrease to 17% by 2025.

The commercial fleet is forecast to grow 3.0% annually in the first five-year period to 5,609 aircraft by 2020 and by 1.2%

annually in the second five-year period to 5,941 aircraft in 2025.

Western Europe is forecast to receive 16% of the worldwide total deliveries in the next ten years (3,051 aircraft), while 1,599

of the current in-service fleet in Western Europe is expected to retire over the next ten years.

More than 300 net migrations out of the region are forecast over ten years.

Copyright © 2015 CAVOK, a division of Oliver Wyman 26

China is a key economic market and a major driver of global fleet growth. The current in-service fleet of 2,232 aircraft is

forecast to grow 5.8% annually in the first five-year period to 2,958 aircraft by 2020 and by 7.9% annually in the second

five-year period to 4,335 aircraft in 2025. Over the ten year period, the Chinese fleet is forecast to grow 6.9% annually,

nearly doubling in size. China’s share of the global fleet is expected to increase from 9% in 2015 to 13% in 2025.

China will account for 14% of the worldwide total deliveries over the next ten years (2,548 aircraft). An overwhelming

majority, 89%, are for fleet expansion verus fleet replacement.

Only 284 in-service aircraft are forecast to retire over the period. This low level of retirements can be attributed to the young

average age of the Chinese fleet. Approximately 150 net migrations out of the region are forecast over ten years (mostly

older A320 and 737 aircraft).

Asia Pacific is currently the third largest region in terms of fleet size with a 16% share of the baseline fleet (3,835 in-service

aircraft). Asia Pacific’s share of the global fleet is expected to increase to 18% by 2025. Like China, Asia Pacific is one of the

key growth markets in the fleet forecast.

The commercial fleet in Asia Pacific is forecast to grow 6.0% annually over the first five-year period to 5,122 aircraft by 2020

and by 3.7% annually in the second five-year period to 6,154 aircraft in 2025.

Asia Pacific is expected to receive 17% of the deliveries in the next ten years (3,215 aircraft). Over 69% forecast deliveries

are for expansion purposes (vs. fleet replacement). 996 currently in-service aircraft are forecast to retire over the next ten

years.

27 Copyright © 2015 CAVOK, a division of Oliver Wyman

GLOBAL AIR TRANSPORT MRO MARKET FORECAST

The fleet forecast as previously discussed drives demand for MRO work. The global air transport MRO spend in 2015 is

expected to be $67.1B. This will rise to $83.2B by 2020, representing a solid 4.4% CAGR over the 5 year period. The growth

rate will decline modestly to 3.8% annually in the second half of the forecast period (2020-2025). Over the full 10 year

forecast period, the global air transport MRO spend will average 4.1% CAGR, rising to $100.4B by 2025.

Airframe maintenance will continue to lose market share in deference to increased engine MRO spend over the next ten

years, while little is expected to change in the relative mix of component and line MRO spend over the forecast period.

EXHIBIT 21: 2015-2025 Global MRO Forecast by MRO Segment

Source: betterinsight™ and PlaneStats

$14.5 $15.9 $16.7

$27.9

$37.1

$46.8

$12.4

$15.2

$19.2

$12.3

$15.0

$17.8

$67.1

$83.2

$100.4

1.9% 1.0%

5.9%

4.8%4.1%

4.7%4.0%

3.5%

$-

$20

$40

$60

$80

$100

$120

2015 2015-2020CAGR

2020 2020-2025CAGR

2025

Bil

lio

ns

Airframe Engine Component Line

Copyright © 2015 CAVOK, a division of Oliver Wyman 28

1. TOTAL MRO BY CLASS

On the whole, very little change is expected in the total MRO market mix by aircraft class (NB, WB, RJ, or TP) over the period.

Narrowbodies will continue to hold a commanding overall share (upwards of 49-54%) in contrast to the widebodies’ 38-

40%, the regional jets’ declining 7%, and the turboprops’ 4-5%.

Globally, MRO related to narrowbody aircraft dominates the budget. The MRO share mirrors that of the fleet itself—that is,

the narrowbody fleet constitutes roughly 55% of the total fleet, and the narrowbody MRO constitutes approximately 49%

of the global MRO. Widebody MRO, on the other hand, makes up just 20% of the global fleet but represents roughly 40%

of the market over the forecast period, because each aircraft is much more maintenance intensive. As the global regional

jet fleet size declines, regional jet MRO and its share of the total MRO market are expected to also decline. The turboprop

fleet is expected to grow modestly (1.7% CAGR 2015-2025), which translates into a total MRO market size growing at 3.5%

CAGR in the first half of the forecast period, then just 0.4% for the second half as more maintenance-efficient turboprops

assume a larger share of the fleet.

EXHIBIT 22: 2015-2025 Global MRO Forecast by Aircraft Class

Source: betterinsight™ and PlaneStats

$32.7 B $41.7 B$54.1 B

$26.4 B $33.1 B$38.1 B

$4.8 B $4.6 B $4.4 B$3.2 B $3.8 B $3.9 B

5.0%5.3%

4.6% 2.9%-0.9% -0.9%3.5% 0.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2015-2020CAGR

2020 2020-2025CAGR

2025

Narrowbody Widebody Regional Jet Turboprop

29 Copyright © 2015 CAVOK, a division of Oliver Wyman

2. TOTAL MRO BY REGION

Regionally, as the fleet distribution changes, so too will MRO follow. For the first time, North America will not remain the

largest single region for total MRO value throughout the forecast period. CAVOK is expecting North America to shrink from

$20.0B in 2015 to $19.2B by 2020, then rebounding a bit to $21.3B by 2025; overall, relatively flat growth for the period

with 0.6% CAGR. Latin America and the Caribbean, which currently represents 5% of the total MRO market, is expected to

more than double over the period (growing from $3.2B to $6.5B) and increasing its market share by one point.

EXHIBIT 23: 2015-2025 Global MRO Forecast by Region

Source: betterinsight™ and PlaneStats

$20.0

$12.4

$14.7

$5.1

$5.5

$3.2

$3.2

$2.1

$0.8

$19.2

$17.3

$18.2

$7.5

$8.0

$4.8

$4.0

$2.3

$1.8

$21.3

$20.5

$19.9

$11.7

$9.8

$6.5

$5.1

$3.0

$2.6

$- $5 $10 $15 $20 $25

North America

Asia Pacific

Western Europe

China

Middle East

Latin America & Caribbean

Eastern Europe

Africa

India

Billions

2015 2020 2025

Copyright © 2015 CAVOK, a division of Oliver Wyman 30

Europe is expected to see solid growth, however, Western Europe will lose a couple points of market share, even as it grows

at 3.0% annually and adds $5.1B to its current $14.7B MRO demand. Eastern Europe, while relatively small at just 5% of

the market, is forecast to grow much faster, at 4.6% annually over the forecast period.

Asia, as has been the case for some years now, remains the growth engine for MRO. Asia Pacific countries should grow at

a healthy 5.2%, rising to the same levels as that of Western Europe and North America. China, which is expected to more

than double in market size, is forecast to grow at 8.6% CAGR. India is forecast to grow 12.1% annually during the forecast

period, but should remain a relatively small share of the total market (1-3%).

Together, the Americas, Europe, and Asia represent nearly 90% of the total MRO market. As CAVOK has pointed out in the

past, however, the Americas and Europe are expected to lose market share to Asia. By 2019, greater Asia (including Asia

Pacific, China, and India) is expected to be the largest of the combined regional areas.

The Middle East is anticipated to nearly double in market size, growing at a 6.0% annual rate and constitute 10% of the

global MRO market by 2025. Africa too is expected to enjoy healthy growth at 3.9% per year, but will only maintain its 3%

market share.

31 Copyright © 2015 CAVOK, a division of Oliver Wyman

3. TOTAL MRO BY OEM

Boeing and Airbus will remain the two dominant players in the air transport aircraft manufacturing market with a combined

three-quarters or more of the worldwide fleet. Boeing aircraft are expected to maintain the largest share of the global fleet

over the forecast period; however, it will lose share as Airbus’ share approaches that of Boeing. Combined, today these two

OEMs’ aircraft drive 88% of the MRO, and by 2025 they are expected to expand this share to 90%.

EXHIBIT 24: 2015-2025 Global MRO Forecast by Aircraft Manufacturer

Source: betterinsight™ and PlaneStats

$25.3 B

$36.8 B $44.6 B

$.9 B

$1.4 B $1.8 B

$33.8 B

$37.7 B $45.5 B

$3.2 B$3.3 B $3.7 B

$2.4 B $2.5 B $2.3 B

$1.4 B $1.5 B $2.4 B

7.8%

3.9%9.1%

4.9%

2.2% 3.8%

0.5% 2.3%0.8% -1.5%0.1% 10.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2015-2020 CAGR 2020 2020-2025 CAGR 2025

Airbus ATR Boeing Bombardier Embraer Other

Copyright © 2015 CAVOK, a division of Oliver Wyman 32

Bombardier and Embraer aircraft are both expected to lose MRO market share over the forecast period. Some of this loss

will be to new entrants to the regional jet market space, while the rest of the loss will come from operators favoring

narrowbodies over regional jets. This is true despite the fact that Bombardier’s narrowbody CSeries will be introduced

during the forecast period. The total MRO value driven by the CSeries is limited compared to the MRO value already

delivered Bombardier regional jets will shed as they are phased out of service (especially its CRJ fleet).

Within the regional jet space, Embraer aircraft are anticipated to maintain the top ranking for global MRO, even as its fleets’

MRO value declines by -0.3% annually through 2025. Bombardier’s regional jet MRO share will fall more than 40% as its

existing aircraft’s market potential declines over the forecast period. Despite the positive press for new regional jets, none

of the new entrants in this MRO market space (SuperJet, Mitsubishi, etc.) will come close to rivaling either Bombardier or

Embraer over the forecast period.

As for turboprop MRO, ATR aircraft are almost single handedly driving the growth for this aircraft class. ATR aircraft are

expected to take over the top ranking from Bombardier within the next five years, and the fleets’ MRO value will grow by

6.9% annually during the forecast period. Bombardier’s turboprop MRO value will grow just 0.7% annually throughout the

forecast period, while Embraer’s turboprop MRO value will shrink 6.3% annually over the next 10 years. Turboprop MRO

from all other OEMs is expected to decline 0.6% annually from 2015 to 2020 and then deteriorate rapidly at a rate of -4.6%

per year between 2020 and 2025.

33 Copyright © 2015 CAVOK, a division of Oliver Wyman

4. TOTAL MRO BY AIRCRAFT FAMILY/MODEL

Airbus A320 family (including the NEO in later years) and the Boeing 737 family (excluding Classics and including the MAX

version in later years) will dominate MRO demand throughout the forecast period. The A320 family has a larger share, but

Boeing’s 737 family should begin to close that gap by 2025. Both will approximately double in market size by 2025.

EXHIBIT 25: 2015-2025 Top Aircraft Fleets by Total MRO Spend

Aircraft Family/Model 2015 2020 2025

A320 $16.2B 1 $22.8B 1 $27.9B 1

737NG/MAX $9.5B 2 $15.0B 2 $22.7B 2

777 $9.0B 3 $10.7B 3 $10.8B 3

A330 $5.1B 4 $7.2B 4 $7.2B 4

787 $0.1B $2.5B 6 $5.9B 5

A350 $0.0B $1.2B $4.5B 6

A380 $0.8B $2.5B 7 $3.0B 7

747 $4.2B 5 $3.5B 5 $2.8B 8

E-Jet $1.4B $1.9B 10 $2.1B 9

ATR $0.9B $1.4B $1.8B 10

A340 $2.1B 10 $2.4B 8 $1.5B

767 $3.0B 7 $1.8B $1.4B

CRJ $2.1B 9 $1.9B 9 $1.3B

757 $3.1B 6 $1.6B $0.6B

737CLASSICS $2.4B 8 $1.0B $0.3B

Other $7.1B $5.6B $6.6B

Note: Top ten rankings for each year are displayed to the right of the MRO spend dollar value.

Source: betterinsight™ and PlaneStats

To put this growth in perspective, the 2015 MRO spend of the 737 fleet is currently comparable to that of the third largest

fleet (777), yet by 2025 the 737 MRO spend will be nearly double the 777 despite relative rankings remaining unchanged.

Copyright © 2015 CAVOK, a division of Oliver Wyman 34

In fact, by 2025, the A320 family and 737 series combined are forecast to constitute a greater share of the combined MRO

market all other fleet types.

The A330 and 747 are the two other fleets that will remain in the 2025 top ten. New entrants to the 2025 top ten include

the 787, A350, A380, Embraer’s E-Jets and ATR.

While the global fleet’s MRO demand will grow 4.1% over the next ten years, the change in the mix by type variants shows

some interesting developments. The entrance of the NEO and the MAX will push their respective families’ annual growth

rates to 5.6% and 9.1%, respectively. Six of the top ten fleets in 2015 are forecast to decline in total MRO value by 2025.

These declining fleets will give way to other aircraft types.

The fastest growing families/models in terms of MRO demand over the forecast period are the MRJ-70/90, Irkut MC-21,

A350, CSeries, COMAC C919, 787, and ARJ21. As the fleets of MD-90s, AvroRJ, BAE 146, DC-8/9/10, Fokker50/70/100,

and classic series of the Boeing 737 and 747 models retire, demand for related MRO will dissolve. These fleets currently

represent just a small share (less than 10%) of the global market though, so their retirement will have little impact on the

overall market. More significantly, however, the 757 and 767, with their combined 9% of the global MRO demand in 2015,

are expected to fall to roughly one third of that by 2025 while shedding 7% of their MRO market share.

The 787, small in terms of MRO demand today, is expected to grow 47% year over year through 2025. This will drive it from

26th to 5th in terms of MRO rank as its MRO consumption grows to nearly $6B. Its Airbus counterpart, the A350 which is

just entering service, is expected to grow to over $4.4B by 2025.

ATR is also expected to double its MRO market value over the ten-year period; however, in total by 2025, it should fall just

short of the $2B threshold mark.

35 Copyright © 2015 CAVOK, a division of Oliver Wyman

5. IMPLICATIONS FOR MROS

Globally, the total MRO market is expected to become increasingly top heavy. In 2015, the top ten airframes comprise 85%

of the total MRO market. By 2025 the top ten airframes will represent 88%, picking up three percentage points of market

share.

Given the transition to newer generational aircraft mentioned above, it is clear that MROs must be prepared to handle the

type of activities associated with this changing mix, or focus their strategy to capture end-of-life markets. From an airframe

MRO perspective, providers must be able to address the demands of new composite and metal matrix airframe materials

that are present in the newest generation of aircraft such as the 787 and A350. At the other end of the spectrum, the

757/767 fleet will still account for over 2% of the global MRO market in 2025, meaning those with proven 757/767

capabilities and competencies should be well positioned to capitalize on the extended life of these aircraft.

New aircraft can enjoy a significant honeymoon period, particularly during the four year warranty period after delivery.

Aircraft of the 2010 and late 2000’s vintage will experience increased MRO demands in the latter half of the forecast period.

The 2000’s and 2010’s vintage fleets will grow from 6% in 2015 to more than a third of the market by 2025. This makes the

combined 2000’s and 2010’s vintage second only to the 1990’s vintage dominated by the A320 Family and 737NG Series.

As the fleets continue to age beyond the forecast period, MROs with capabilities to service this growing segment will be

well positioned for success.

The obvious targets on the narrowbody side are 737NG/MAX and A320CEO/NEO. These two families are expected to drive

a combined 38% of the MRO market in 2015. More importantly, these same two families are forecast to drive slightly more

than 50% of the market by 2025.

While all widebodies combined are not expected to come close to the MRO these two top narrowbodies demand, over half

of the top ten families in 2025 in terms of MRO value are widebody aircraft. Moreover, CAVOK estimates that operators

currently are sending just over 20% of their widebody heavy maintenance to regions other than their own, namely Asia

Pacific and China.

MROs in North America and Western Europe can open a broad market for themselves by targeting repatriated widebody

maintenance work with the introduction of new capacity and the development of the necessary skills. Recognizing that the

regional labor rates are continuing to move towards parity, MROs that build widebody capabilities could be in a position

to capture this market from operators in their own region that have been sending that work abroad.

Capturing market share from Asia Pacific and China will not be a simple task, however. Even if labor rate parity is reached,

or nearly reached, Asian MROs have the demonstrated capacity and skills in place today. While MROs in the other regions

of the world do have widebody capability, investment will be needed for training, tooling and equipment. There will be a

high cost of capital for such expansion, but it will be a necessary investment to compete with the Asian MROs.

Copyright © 2015 CAVOK, a division of Oliver Wyman 36

While repatriating widebody work is a good strategy for growing the otherwise stagnate markets of North America and

Western Europe, the global focus needs to be on meeting the demand by the growth being generated in Asia/Pacific,

China, and India.

MROs, such as Lufthansa Technik, are already beginning to expand their presence in Asia by expanding existing facilities

to increase capacity and opening new facilities be closer to their customers, but adding and improving facilities alone will

not adequately address the needs created by the Asian regions. MROs will need to better utilize advanced process analysis

efforts, such as Lean, to reduce turnaround times and expedite material delivery to increase competitiveness and

productivity while simultaneously reducing costs. And, in addition to increasing efficiency of operations, MROs will also

need to begin looking at forming partnerships with technical schools near their facilities to develop a skilled workforce that

is capable of keeping up with MRO growth in Asia.

37 Copyright © 2015 CAVOK, a division of Oliver Wyman

AIRFRAME MAINTENANCE MARKET FORECAST AND STRUCTURE

Air transport’s labor intensive airframe heavy maintenance and modifications MRO market is expected to be $14.5B in

2015, representing 22% of the total MRO spend for the year.

The total airframe market is forecast to increase at a rate of 1.9% CAGR through 2020. The growth will be notably slower

(1.0% CAGR) in the following five years, however, as the elevated retirement rate will continue unabated while the spend

from a high number of early 2000 vintage aircraft heavy checks dissipates.

In 2015, and through the full forecast period, the global airframe MRO market will be dominated by narrowbody spend.

Widebody and turboprop airframe MRO market share will remain effectively unchanged at 36% and 7%, respectively.

Airframe MRO spend for regional jets is expected to shrink by 10% and lose market share over the next ten years.

EXHIBIT 26: 2015 and 2025 Airframe MRO Market Share by Aircraft Class

Source: betterinsight™ and PlaneStats

The impact of new regional jet programs on the airframe MRO market is beyond the timeframe of this ten-year forecast;

once these deliveries begin to age, however, related maintenance events for these newer generational aircraft are

anticipated in the future. Thus, for the time being, the regional jet airframe market is expected to decline.

Copyright © 2015 CAVOK, a division of Oliver Wyman 38

Regionally, North America will be the largest market in 2015 and in 2025; however, it will lose 6 points of market share by

2025, slipping from the number one spot during the forecast period and replaced by Western Europe. The fastest growing

regions are all in developing areas, led by India, China, Latin America & Caribbean, and Asia Pacific.

EXHIBIT 27: 2015-2025 Airframe MRO Market by Region

Source: betterinsight™ and PlaneStats

The influence of improved technology and increased check intervals in new generation aircraft, particularly the heavy use

of composites and the maturing of software laden smart electronics, will influence the heavy maintenance and

modifications spend in the latter half of the forecast period. The 787 technology, for example, is anticipated to save some

30-35% over a similar sized, older technology, aircraft.

$4.3

$3.8

$2.3

$1.0

$1.0

$0.6

$0.8

$0.5

$0.2

$3.7

$4.0

$2.9

$1.4

$1.4

$0.8

$0.9

$0.5

$0.2

$3.9

$3.7

$3.1

$2.0

$1.1

$1.0

$1.0

$0.6

$0.4

$- $1 $2 $3 $4 $5

North America

Western Europe

Asia Pacific

China

Middle East

Latin America & Caribbean

Eastern Europe

Africa

India

Billions

2015 2020 2025

39 Copyright © 2015 CAVOK, a division of Oliver Wyman

1. MARKET STRUCTURE

Airframe maintenance involves work carried out on a regular, scheduled basis to inspect, maintain, repair, and conduct

preventive maintenance of the airframe’s structure and cabin interior. As a consequence, the aircraft is removed from

commercial service for a generally predetermined period of time and at specified intervals. Individual operators are

responsible for conducting this maintenance (either by themselves or through a qualified provider) in compliance with the

applicable aviation safety regulations (e.g., the Federal Aviation Administration (FAA), the European Aviation Safety

Administration (EASA), etc.). As such, these individual operators develop schedules for airframe maintenance that satisfy

safety and operational requirements.

Such scheduled work scopes are typically based on calendar time, a fixed number of flight hours, or a fixed number of flight

cycles. While some operators and aircraft types have highly-customized maintenance programs such as “phase checks”

and “overnight C checks,” the vast majority fit into a traditional model of a light C check and a heavy maintenance visit

(HMV). Each aircraft model is different, but for illustrative purposes, an average light C check occurs typically every 18-24

months while the HMV (often also called a “D check,” “4C Check,” or “Structural C Check”) usually occurs every 60-84

months. However, the C check interval can range from 12 to 36 months. HMV checks can range from 60 to 144 months.

Newer generation aircraft often have longer intervals; turboprops and older aircraft have the shortest intervals.

EXHIBIT 28: Airframe Scheduled Work Scopes

Activity Description Frequency Manhours Required

C Check Detailed inspection 12-36 Months 2,000-12,000 FH 1,000-15,000 FC

1,000-15,000 Mhrs 3,800 Weighted Average

HMV D Check 4C Check

Major reconditioning 48-144 months 8,000-36,000 FH 6,000-24,000 FC

2,000-70,000 Mhrs 11,600 Weighted Average

Note: All intervals are highly dependent on the flight profile of the actual aircraft.

Source: betterinsight™ and PlaneStats

Airframe maintenance providers can be classified into five categories.

Airline: Commercial air transport operators that perform maintenance utilizing in-house airframe maintenance

capabilities.

Airline Third Party: Maintenance subsidiaries of airlines, often operating with varying degrees of autonomy and

performing maintenance for other operators and possibly their own parent. These organizations leverage

maintenance capabilities at scale to offer competitive pricing to the marketplace.

Copyright © 2015 CAVOK, a division of Oliver Wyman 40

Independent: Dedicated maintenance providers with no relation to either OEMs or airlines. From large to small,

these maintenance providers often have lowest labor costs.

Joint Venture: Airframe maintenance providers that are formed by (typically) joining the resources of OEMs and

in-country capabilities to build indigenous capacity (e.g., Ameco Taikoo, GAMECO, etc.).

OEM: Airframe manufacturers, such as Airbus, Embraer, Bombardier, Sukhoi, ATR, etc., offering maintenance

capabilities for their respective aircraft types utilizing company owned facilities.

Based on known MRO contract information it is possible to estimate the market share that each market category enjoys.

Interestingly, for all the media and political discussion related to contracting work out, globally, the air transport market

still keeps nearly half of its airframe maintenance in-house (49% when combining work performed by the airline on its own

aircraft and the work performed by airline affiliated third party providers). Those airline providers that choose to pursue

the maintenance work of other airlines’ airframes capture an additional 10%. Independent maintenance providers carryout

nearly a third of the demand, while joint ventures (JVs) represent roughly 8% of the market. Finally, OEMs, recognizing the

value that the MRO aftermarket holds in the lifecycle of their products, have moved aggressively to capture a portion of

that work for themselves. Currently, OEMs hold a negligible share of the airframe MRO market; however, as new

generation aircraft begin to demand maintenance, the efforts of OEMs to sell those aircraft with maintenance packages

are expected to add to their share.

EXHIBIT 29: 2015 Airframe MRO Market Share by Maintenance Provider Classification

Source: betterinsight™ and PlaneStats

Airline28%

Airline Third Party - In House

22%

Airline Third Party -Contracted

10%

Independent31%

Joint Venture8%

OEM1%

41 Copyright © 2015 CAVOK, a division of Oliver Wyman

2. COST STRUCTURE

Airframe spend can be divided into labor and material elements.

Labor: Labor is the larger element of airframe work and accounts for 55% of the segment spend. This includes

labor for licensed technicians (mechanics or engineers) as well as the cost of benefits and overhead. When

differentiating the labor component between airframe and modifications work, labor represents 69% and 38%,

respectively.

Material: Material is the smaller element of airframe MRO, accounting for 45% of the segment spend. This

includes all required materials, hardware and consumables. When differentiating between airframe and

modifications activity, material represents 31% and 62%, respectively. Clearly, the nature of modifications work

drives a higher emphasis on materials.

Little change in this mix is expected over the forecast period.

EXHIBIT 30: 2015 Airframe MRO Market Labor and Material Mix

Source: betterinsight™ and PlaneStats

$5.4

$2.5

$7.9

$2.5

$4.1

$6.6

$14.5

$-

$2

$4

$6

$8

$10

$12

$14

$16

HMV MODS Airframe

Bil

lio

ns

Labor Materials

Copyright © 2015 CAVOK, a division of Oliver Wyman 42

3. SUPPLY CHAIN

The airframe maintenance material supply chain consists of four main sources: OEMs, PMA providers, distributors, and

surplus (used serviceable material) providers.

OEMs: Direct purchases from original equipment manufacturers represent more than 60% of the airframe

maintenance material parts demand.

PMA providers: PMA providers, despite significant barriers, have made some inroads into the airframe

maintenance market, providing some 8% of the material. Looking to the future, while PMA currently represents

the smallest share, several large PMA providers have implemented strategies which are expected to improve

PMA’s market share because of their attractiveness to airline customers focused on cost reductions.

Distributors: As intermediaries between the original equipment manufacturers and maintenance providers,

distributors provide about one-fifth of the material parts demand.

Surplus providers: Surplus providers, which purchase new and used material from other surplus providers, MROs,

operators, and/or directly from parted-out aircraft, provide 10% of the airframe maintenance parts demand.

EXHIBIT 31: 2015 Airframe Materials Market Share by Source

Source: betterinsight™ and PlaneStats

43 Copyright © 2015 CAVOK, a division of Oliver Wyman

ENGINE MAINTENANCE MARKET FORECAST AND STRUCTURE