TDS on payments to Non-Residents - vasai-icai.org Jambusaria PPT page 2 [Compatibility... ·...

27

NIHAR JAMBUSARIA, BDO India 15 th June,2011 Page 1 TDS on payments to Non-Residents

Transcript of TDS on payments to Non-Residents - vasai-icai.org Jambusaria PPT page 2 [Compatibility... ·...

NIHAR JAMBUSARIA, BDO India

15th June,2011

Page 1

TDS on payments to Non-Residents

TDS on Payments to Non-Residents & Residents

Page 2Page 2

OBJECTIVE OF SECTION 195 OF THE OBJECTIVE OF SECTION 195 OF THE OBJECTIVE OF SECTION 195 OF THE OBJECTIVE OF SECTION 195 OF THE ACTACTACTACT

TDS on Payments to Non-Residents & Residents

Page 3

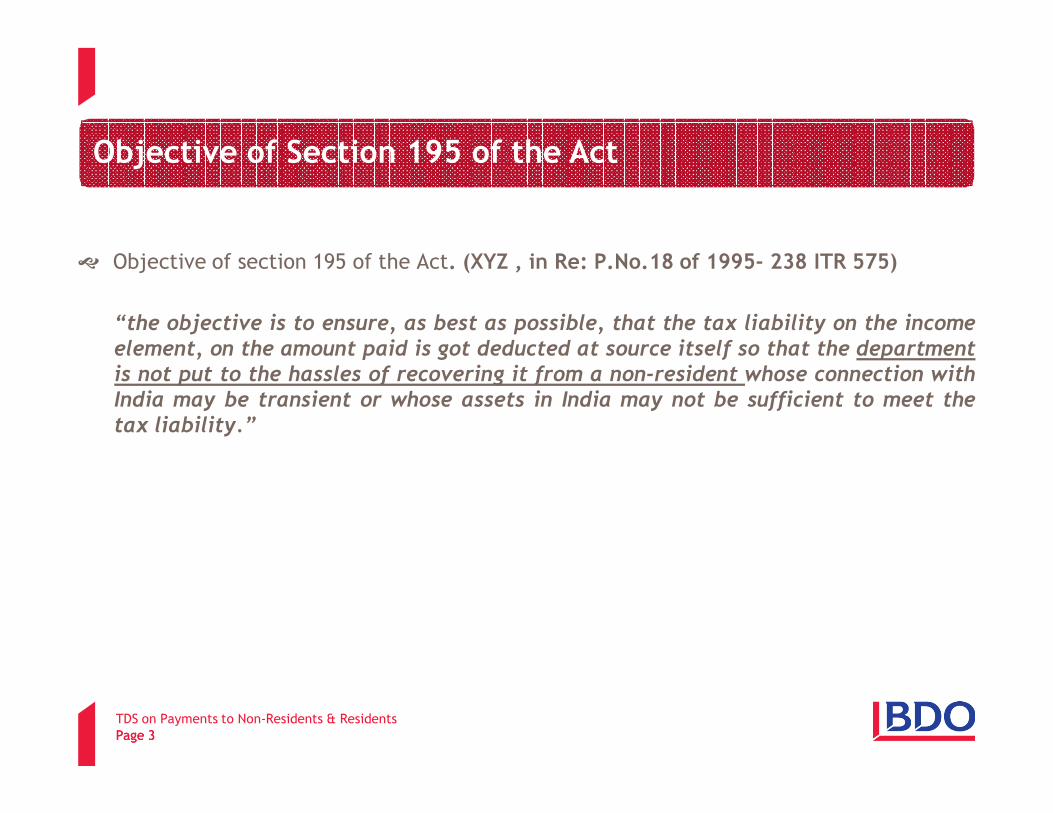

� Objective of section 195 of the Act. (XYZ , in Re: P.No.18 of 1995- 238 ITR 575)

“the objective is to ensure, as best as possible, that the tax liability on the incomeelement, on the amount paid is got deducted at source itself so that the departmentis not put to the hassles of recovering it from a non-resident whose connection withIndia may be transient or whose assets in India may not be sufficient to meet thetax liability.”

Page 3

Objective of Section 195 of the Act

TDS on Payments to Non-Residents & Residents

Page 4Page 4

OVERVIEW OF S.195 OF THE ACTOVERVIEW OF S.195 OF THE ACTOVERVIEW OF S.195 OF THE ACTOVERVIEW OF S.195 OF THE ACT

TDS on Payments to Non-Residents & Residents

Page 5

“Any Person responsible for paying to a non-resident, not being a company, or to a

foreign company, any interest or any other sum chargeable under the provisions of this Act (not being income chargeable under the head “Salaries”) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct income tax thereon at the rates in force…………….”

“Provided further that no such deduction shall be made in respect of any dividendsreferred to in section 115-O”

Page 5

Provision of section 195 of the Act

TDS on Payments to Non-Residents & Residents

Page 6Page 6

Overview of S.195 of the Act

S.195

S.195(1) S.195(5)S.195(4)S.195(3)S.195(2)

Scope and Conditions for Applicability

Application by payer for lower

or nil withholding certificate

Application by payee for lower or nil withholding certificate

Validity period of the

Certificate

Power of the CBDT to issue notifications

TDS on Payments to Non-Residents & Residents

Page 7Page 7

S.195(1)S.195(1)S.195(1)S.195(1)---- SCOPE & CONDITIONS FOR SCOPE & CONDITIONS FOR SCOPE & CONDITIONS FOR SCOPE & CONDITIONS FOR

APPLICABILITY APPLICABILITY APPLICABILITY APPLICABILITY

TDS on Payments to Non-Residents & Residents

Page 8

� Who is responsible to deduct tax at source?

- Any person – Person as defined in section 2(31)

- Includes non-residents and foreign companies

• Satellite Television Asia Region Ltd (99 ITD 92 – Mum ITAT)

• Vodafone B.V. (SC)

• E-trade Mauritius Ltd (Mum HC)

� On Payments made to non residents

- Includes all non residents having presence in India or not

- It does not include RNOR

Page 8

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 9

� What are the payments covered?

- Any sum chargeable under the Act

- Except Salary and dividends referred to in section 115-O

- Income not taxable in India (Exempt Income)

• Hyderabad Industries Ltd (188 ITR 749 – Kar HC)

� When to deduct tax

- At the time of payment or credit whichever is earlier

� What rate to apply?

- Lower of the two rates

• Relevant rates in force; or

• Rates under the Tax Treaty – sec 2(37A)(iii) – Circular No. 728 dt. 30-10-1995

Page 9

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 10

� Points to remember

• No limit has been provided unlike other sections dealing with tax required to be

deducted while making payment to residents (section 194 to 194L)

• CBDT has issued a number of circulars relating to taxability of non residents

• Tax required to be deducted on sum chargeable to tax – Section 5 and section 9

Page 10

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 11

Issues:

�Whether payment made by Branch to HO / other branch is subject to TDS?

�Circular No. 740 dt 17-4-996/Dresdner Bank-108 ITD375/ABN Amro 97 ITD89

�Whether tax required to be deducted where -

- Payment has been made to the representative assessee or agent of a non resident

- Payment made by Representative assessee or Agent of a Non Resident to a Non

resident

- Payment made to agent of a Non Resident on his instructions – 35 ITR 134 (Bom)-

Narsee Nagsee v/s CIT

- Assessee treating himself as agent of Non Resident – 200 ITR 441 (Cal) – Grindlays

bank Ltd v/s. CIT

�Are the rates that are being prescribed under the DTAA being required to be increasedby surcharge and education cess?

Page 11

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 12

� Whether tax under section 195 is required to be deducted in following situations

- On void agreements – Erricsson Communications Ltd (81 ITD 77)

� What about payments made to non resident partner?

� What about payments made in kind?

- Kanchanganga Sea Foods Ltd (265 ITR 644)

� What about payments pending FERA/FEMA approval?

- United Breweries (211 ITR 256)

- Motor Industries Co (249 ITR 141)

- Pfizer Corporation (259 ITR 391)

� On adjustment against dues?

- Raymond Ltd (80 TTJ 120) / (86 ITD 179)

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 13

� What happens if a particular source of income is chargeable to tax under the Act,but not under the DTAA? Is tax required to be deducted?

� Is tax required to be deducted from reimbursement of expenses?

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 14

S.195(1)- Scope & Conditions for applicability

Nature of Expense Case Laws in Favor of assessee Case laws against the assessee

Reimbursement of cost of services of a third party engaged by Non resident

Wallace Pharmaceuticals P. Ltd (278 ITR 97)

Reimbursement of allocated cost (ie. cost sharing arrangements)

Dunlop Rubber Co (142 ITR 493) Danfoss Industries (India) Ltd (268 ITR 1)

Payment for services rendered at cost

Timkin India Ltd (273 ITR 67)

Reimbursement of incidental expenses in addition to payments of FTS? royalty

Telco Ltd (245 ITR 823)

Industries Engg. Project (P) Ltd (202 ITR 1014)

Clifford Chance (82 ITD 106)

Mahindra and Mahindra Ltd (1 SOT 896)

Cochin Refineries Ltd (222 ITR 354)

SRK Consulting (230 ITR 206)

Hindalco Industries Ltd (278 ITR (AT) 125)

Reimbursement of living allowance, etc of a person deputed to India by the non-resident

BHEL (252 ITR 218)

Morgenstern Werner (233 ITR 751)

Goslino Mario (241 ITR 312)

Hyderabad Industries Ltd (188 ITR 749)

HCL Infosystems Ltd (274 ITR 261)

TDS on Payments to Non-Residents & Residents

Page 15

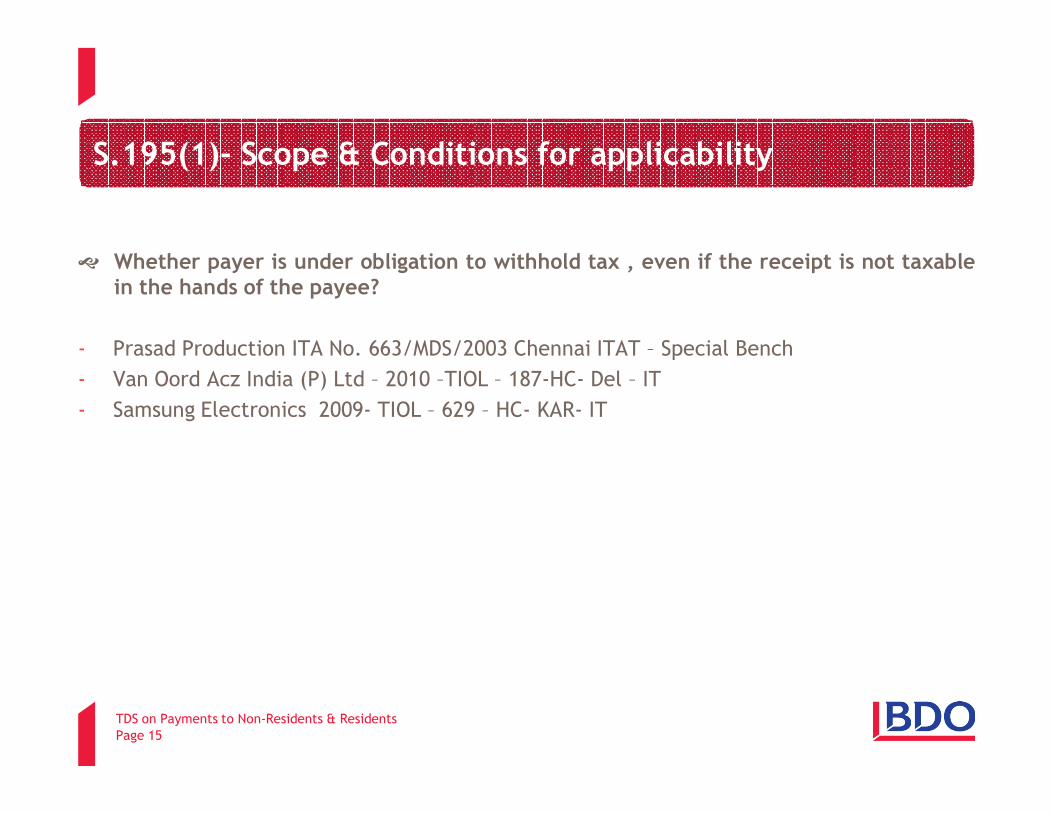

� Whether payer is under obligation to withhold tax , even if the receipt is not taxablein the hands of the payee?

- Prasad Production ITA No. 663/MDS/2003 Chennai ITAT – Special Bench

- Van Oord Acz India (P) Ltd – 2010 –TIOL – 187-HC- Del – IT

- Samsung Electronics 2009- TIOL – 629 – HC- KAR- IT

S.195(1)- Scope & Conditions for applicability

TDS on Payments to Non-Residents & Residents

Page 16Page 16

S.195(2)S.195(2)S.195(2)S.195(2)---- APPLICATION BY PAYERAPPLICATION BY PAYERAPPLICATION BY PAYERAPPLICATION BY PAYER

TDS on Payments to Non-Residents & Residents

Page 17

� Deals with a scenario where payer makes an application for an order

� No prescribed format for an application

Page 17

S.195(2)- Application by Payer

TDS on Payments to Non-Residents & Residents

Page 18

Issues:

� Where a work involves multiple phases, in such scenario, Is it sufficient if orderunder section 195(2) is obtained for phase I of the work or whether order is to beobtained for all the phases of the work?

� Whether order passed under section 195(2) is appealable?

� Whether order under section 195(2) of the Act is subject to revision under section263 of the Act?

Page 18

S.195(2)- Application by Payer

TDS on Payments to Non-Residents & Residents

Page 19Page 19

S.195(3)S.195(3)S.195(3)S.195(3)---- APPLICATION BY PAYEEAPPLICATION BY PAYEEAPPLICATION BY PAYEEAPPLICATION BY PAYEE

TDS on Payments to Non-Residents & Residents

Page 20

� Payee can make an application for a certificate

� Application can be made in prescribed format:

o Form No. 15C in the Case of Banking Company

o Form No. 15D in any other case

� Condition for issue of Certificate under section 195(3) of the Act (Rule 29B)

� Validity of Certificate

� Whether “certificate under section 195(3) of the Act is appealable?

Page 20

S.195(3)- Application by Payee

TDS on Payments to Non-Residents & Residents

Page 21

Bird eye view of Section 195 of the Act

Payment made to non resident

Deduct TDS

Taxable under the Act

DTAA accessibleDTAA not-accessible

Remittance of payment to Non-Resident

NoTDS

No

Income not exempt under DTAA

Income exempt under DTAA

Not Taxable under the Act

TDS on Payments to Non-Residents & Residents

Page 22Page 22

REFUNDREFUNDREFUNDREFUND

TDS on Payments to Non-Residents & Residents

Page 23Page 23

Refund of sum deducted- under different scenario

Sr.no

Scenario Criteria

a Contract is cancelled No remittance is made to the non-resident

b Remittance is duly made tothe non-resident, butcontract is cancelled

Remitted amount is duly refunded tothe payer by the payee

c Contract cancelled afterpartial execution

No remittance is made to the non-resident for the non executed part

d The contract is cancelledafter partial execution andremittance related to non-executed part is made to thenon-resident

Amount refunded to the payer or noremittance was made but tax wasdeducted and deposited when amountwas credited to the account of the non-resident

TDS on Payments to Non-Residents & Residents

Page 24Page 24

Refund of sum deducted- under different scenario

Sr.no

Scenario Criteria

e Amendment in law or bynotification under the Act

There occurs exemption of theremitted amount from tax

f Order passed under section154 or 248 or 264 of the Act

Tax deduction liability of the payer isreduced

g Double deduction of taxamount

Same amount deducted twice bymistake

h Other than discussed above Grossing up not required or paymentof tax at higher rate under domesticlaw while a lower rate is prescribedunder DTAA

TDS on Payments to Non-Residents & Residents

Page 25Page 25

Comparison between S.195(2),195(3) & 197 of the Act

S. 195(2) S. 195(3) S. 197

Payer applies to determineappropriate portion of sumchargeable to tax andliability for withholding tax

Nil withholding- payeeapplies to the AO

Lower or Nil withholding-Payee applies to the Ao

No Prescribed format for anapplication

Prescribed format for anapplication (Form No. 15Cor 15D as the case may be)

Prescribed format for anapplication (i.e Form No. 13)

Order appealable under section 248 of the Act

Order not appealable- Writpetition to High Court

Order not appealable-Writpetition to High Court

TDS on Payments to Non-Residents & Residents

Page 26Page 26Page 26

TDS on Payments to Non-Residents & Residents

Page 27Page 27Page 27

Thank YouThank YouThank YouThank You