TCS Group IFRS results - static.tinkoff.ru · March 2018 TCS Group 2017 FY IFRS results 3 2017FY...

28

TCS Group IFRS results 2017 FY

Transcript of TCS Group IFRS results - static.tinkoff.ru · March 2018 TCS Group 2017 FY IFRS results 3 2017FY...

TCS Group IFRS results2017 FY

Disclaimer

March 2018 TCS Group 2017 FY IFRS results 2

Certain statements and/or other information included in this document may not be historical facts and may

constitute “forward looking statements” within the meaning of Section 27A of the U.S. Securities Act and

Section 2(1)(e) of the U.S. Securities Exchange Act of 1934, as amended. The words “believe”, “expect”,

“anticipate”, “intend”, “estimate”, “plans”, “forecast”, “project”, “will”, “may”, “should” and similar expressions

may identify forward looking statements but are not the exclusive means of identifying such statements.

Forward looking statements include statements concerning our plans, expectations, projections, objectives,

targets, goals, strategies, future events, future revenues, operations or performance, capital expenditures,

financing needs, our plans or intentions relating to the expansion or contraction of our business as well as

specific acquisitions and dispositions, our competitive strengths and weaknesses, our plans or goals relating to

forecasted production, reserves, financial position and future operations and development, our business

strategy and the trends we anticipate in the industry and the political, economic, social and legal environment

in which we operate, and other information that is not historical information, together with the assumptions

underlying these forward looking statements. By their very nature, forward looking statements involve inherent

risks, uncertainties and other important factors that could cause our actual results, performance or

achievements to be materially different from results, performance or achievements expressed or implied by

such forward-looking statements. Such forward-looking statements are based on numerous assumptions

regarding our present and future business strategies and the political, economic, social and legal environment

in which we will operate in the future. We do not make any representation, warranty or prediction that the

results anticipated by such forward-looking statements will be achieved, and such forward-looking statements

represent, in each case, only one of many possible scenarios and should not be viewed as the most likely or

standard scenario. We expressly disclaim any obligation or undertaking to update any forward-looking

statements to reflect actual results, changes in assumptions or in any other factors affecting such statements.

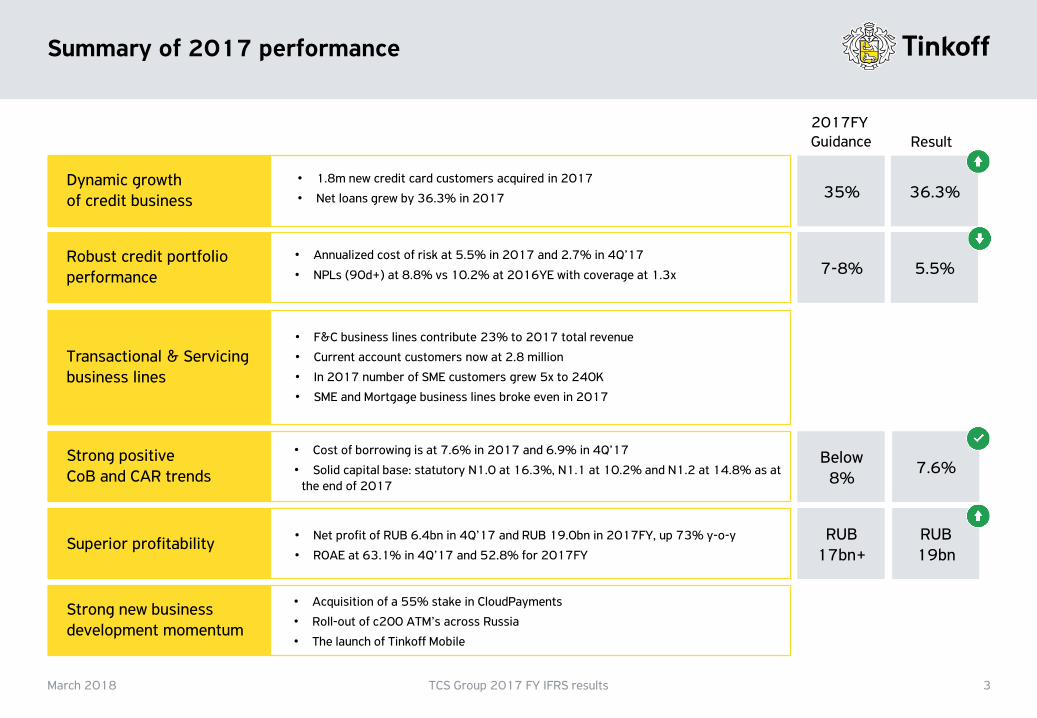

Summary of 2017 performance

March 2018 TCS Group 2017 FY IFRS results 3

2017FYGuidance Result

Dynamic growth of credit business

• 1.8m new credit card customers acquired in 2017

• Net loans grew by 36.3% in 2017 35% 36.3%

Robust credit portfolio performance

• Annualized cost of risk at 5.5% in 2017 and 2.7% in 4Q’17

• NPLs (90d+) at 8.8% vs 10.2% at 2016YE with coverage at 1.3x 7-8% 5.5%

Transactional & Servicing business lines

• F&C business lines contribute 23% to 2017 total revenue

• Current account customers now at 2.8 million

• In 2017 number of SME customers grew 5x to 240K

• SME and Mortgage business lines broke even in 2017

Strong positiveCoB and CAR trends

• Cost of borrowing is at 7.6% in 2017 and 6.9% in 4Q’17

• Solid capital base: statutory N1.0 at 16.3%, N1.1 at 10.2% and N1.2 at 14.8% as at the end of 2017

Below 8%

7.6%

Superior profitability• Net profit of RUB 6.4bn in 4Q’17 and RUB 19.0bn in 2017FY, up 73% y-o-y

• ROAE at 63.1% in 4Q’17 and 52.8% for 2017FY

RUB 17bn+

RUB 19bn

Strong new business development momentum

• Acquisition of a 55% stake in CloudPayments

• Roll-out of c200 ATM’s across Russia

• The launch of Tinkoff Mobile

Continued asset growth dynamics

March 2018 TCS Group 2017 FY IFRS results 4

23.0 19.9 21.2 25.0 32.3

102.9 111.5 121.2134.1

140.2

33.3 32.546.0

57.972.5

16.2 13.0

27.0

19.0

23.9

175.4 176.8

215.3236.0

268.8

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Cash and cash equivalents Investment securities and REPO Net loans Other

13% 11% 10% 11% 12%

59% 63%56% 57% 52%

19% 18%21% 25% 27%

9% 7% 13% 8% 9%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Cash and cash equivalents Investment securities and REPO Net loans Other

A 36%+ y-o-y growth of net loans was supplemented by doubling of

the investment securities portfolio on the back of retail and SME

current accounts growth

All currency data are in RUB bn unless otherwise stated

ASSETS ASSETS STRUCTURE

53.3%13.9%

Quality growth of credit card portfolio, ahead of the market

March 2018 TCS Group 2017 FY IFRS results 5

102.9 111.5 121.2134.1 140.2

17.517.9

18.319.3 17.5

120.4129.4

139.5153.4 157.8

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Net loans LLP

2.0% 1.9% 1.9% 1.7% 1.7%

3.3%2.4%

1.9% 1.8% 2.1%

5.0% 5.3% 5.5% 5.9%5.0%

142% 144% 140%134%

126%

155% 158% 158%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

90-180 dpd 180+ dpd Courts

LLP/NPL, IAS 39 LLP/NPL, IFRS 9

All currency data are in RUB bn unless otherwise stated

31.0%2.9%

GROSS LOANS NPL (AS % OF GROSS LOANS)

A solid 31% y-o-y growth of gross loans

is attributed to the average 200K credit

cards issuance per month, as well

as to the development of cash and POS

loans business lines

The share of non-performing

loans (NPLs) fell to 8.8%

in 2017

Loan loss provision coverage

notched down to 1.26x under

IAS 39

Funding: customer inflows remain strong

March 2018 TCS Group 2017 FY IFRS results 6

72.0 66.9 71.7 74.9 77.4

5.8 8.212.6

18.2

25.4

11.5 11.1

23.222.4

22.0

139.5 137.7

172.0186.3

212.5

8.08.3

10.8

46.7 48.155.9 62.6

76.3

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Individuals term Individuals current Legal entities

Subordinated debt Debt securities in issue Due to banks

107.2 105.8 121.7 136.4 158.3

17.3 17.418.5

19.320.8

83% 85% 86% 87% 87%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

RUB

FX

% of retailaccounts coveredby DIA*

4.8* 5.2* 5.017.3

2Q'18 … 4Q'18 … 2Q'19 … 3Q'22

Local bonds

Subordinated bond

ECP

Put option

*management estimates, unaudited

Put option Call option

* volume outstanding as of Mar 13, 2018

FUNDING CUSTOMER ACCOUNTS

WHOLESALE DEBT MATURITY PROFILE

52.3%14.0%

All currency data are in RUB bn unless otherwise stated

Customer accounts remain our primary

source of funding:

• A 29% growth of individual accounts

balances is attributed to the acquisition

of debit card customers

• A 4.4x growth of corporate accounts balances

is due to SME business line development

We leveraged strong appetite for Tinkoff risk in the wholesale debt

market to boost our capital position, diversify our funding mix and

to balance our liabilities duration position. In 2017, we

successfully completed 3 new bond transaction:

• $300m perpetual subordinated debt placement in Jun’17

• Local RUB 5bn bond placement in Apr’17

• Issuance of $48m ECP in Dec’17

We hedge our open

FX position with

long-dated Swaps

Equity – solid capital position and robust ROE underpin a new dividend policy

March 2018 TCS Group 2017 FY IFRS results 7

29.533.5

35.939.1

41.9

14.8%16.8%

24.7% 23.6%21.0%

16.3%18.0%

25.1% 23.9%21.1%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Equity Basel III Tier 1 CARBasel III Total CAR

All currency data are in RUB bn unless otherwise stated

42.1%7.2% 11.1% 12.7% 12.0%

16.0% 16.3%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

8.6% 9.4% 9.8% 9.8% 10.2%

14.4% 14.8%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

N1.1 N1.2

SHAREHOLDERS’ EQUITY N1.0 CAPITAL RATIO (STATUTORY)

N1.1, N1.2 CAPITAL RATIOS (STATUTORY)

Our equity showed a strong 42.1% y-o-y growth which ensures

healthy margins above regulatory capital requirements

N1.2 was boosted by the USD 300mn perpetual

bond placed in June

Solid capital position and strong capital generation momentum

enable out new dividend policy: up to 50% of our quarterly net

income is paid in dividends

A total $1.08/per GDR declared in dividends based on 2017 earnings

N1.0 min 9.25%

N1.2 min 7.25%

N1.1 min 5.75%

Revenue

All currency data are in RUB bn unless otherwise stated

REVENUE REVENUE STRUCTURE

84% 84% 81% 76% 71%

9% 10% 12%14% 19%

5% 4% 5% 6% 6%2% 2% 3% 4% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Credit F&C business Treasury Insurance premiums

85%77%

8%14%

5% 5%2% 3%

2016 2017

13.4 13.5 14.8 16.0 16.8

1.4 1.62.3

3.04.4

0.8 0.7

0.8

1.2

1.3

16.0 16.1

18.4

21.0

23.6

0.40.4

0.5

0.8

1.0

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Credit F&C business Treasury Insurance premiums

49.1

61.0

58.1

79.0

4.6

11.2

3.0

4.1

1.3

2.7

2016 2017

36.1% 47.3%

Group’s revenue showed a 36.1% increase

y-o-y driven by growth of core credit

business as well as development of

transactional & servicing businesses

The share of non-credit related

revenue increased from 15% in

2016 to 23% in 2017

March 2018 TCS Group 2017 FY IFRS results 8

Credit business: Interest income and expense

March 2018 TCS Group 2017 FY IFRS results 9

40.8% 39.0% 39.7% 40.0% 39.3%

8.4% 8.0% 7.3% 7.3% 7.2%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Credit portfolio Investment portfolio

40.3% 39.6%

8.8% 7.2%

2016 2017

10.0%8.5% 7.7% 7.7% 6.9%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

11.0%

7.6%

2016 2017

INTEREST INCOME YIELD

INTEREST EXPENSE COST OF BORROWING

2.7 2.5 2.4 2.6 2.6

0.60.5 0.6

0.8 0.8

3.4 3.0 3.0 3.5 3.4

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Customer accounts Wholesale / due to banks

10.9 10.1

2.7 2.7

13.6 12.8

2016 2017

12.1 12.2 13.4 14.7 15.3

0.8 0.70.8

1.2 1.312.9 12.914.2

15.8 16.6

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Credit portfolio Treasury

44.655.5

3.04.147.6

59.5

2016 2017

In 2017 interest income grew by 25%

y-o-y with gross interest yield of credit portfolio

showing a decline from 40.3% to 39.6%

Interest expense decreased by 6% y-o-y while the aggregate cost of borrowing dropped

by 340bps y-o-y as a result of declining retail deposit rates and gradual growth of the

weight of the individual and SME current accounts in the liability structure

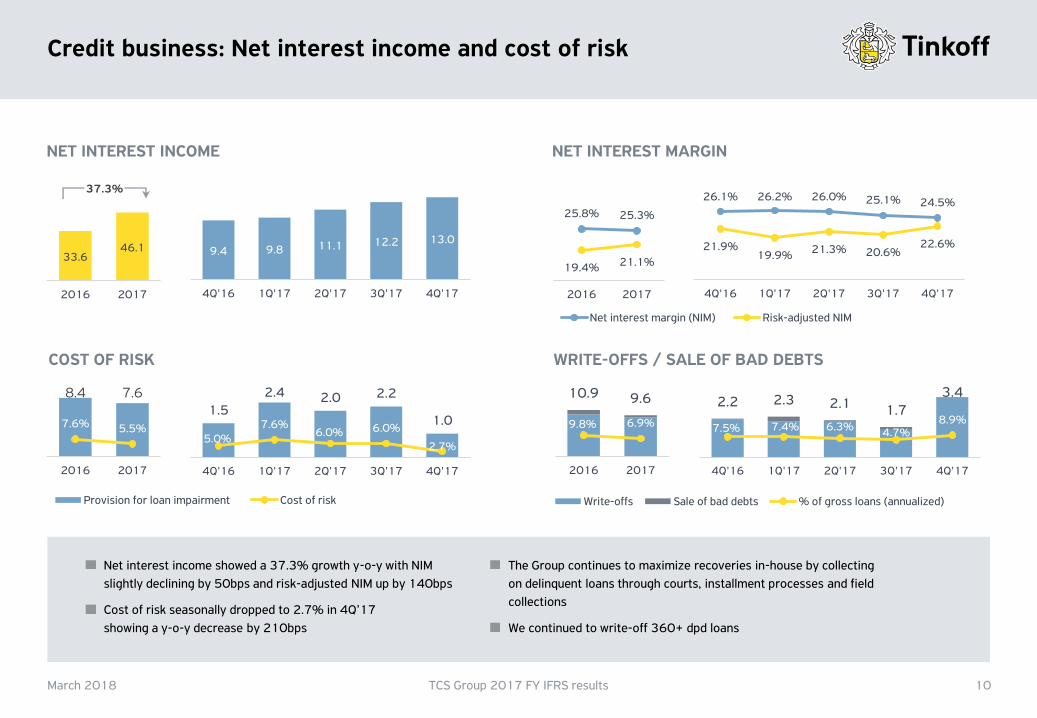

Credit business: Net interest income and cost of risk

March 2018 TCS Group 2017 FY IFRS results 10

9.4 9.8 11.1 12.2 13.0

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

33.646.1

2016 2017

NET INTEREST INCOME NET INTEREST MARGIN

26.1% 26.2% 26.0% 25.1% 24.5%

21.9%19.9%

21.3% 20.6%22.6%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Net interest margin (NIM) Risk-adjusted NIM

25.8% 25.3%

19.4% 21.1%

2016 2017

2.2 2.3 2.1 1.73.4

7.5% 7.4% 6.3% 4.7%8.9%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Write-offs Sale of bad debts % of gross loans (annualized)

1.5

2.4 2.0 2.2

1.0

5.0%7.6%

6.0% 6.0%

2.7%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Provision for loan impairment Cost of risk

8.4 7.6

7.6% 5.5%

2016 2017

10.9 9.6

9.8% 6.9%

2016 2017

COST OF RISK WRITE-OFFS / SALE OF BAD DEBTS

37.3%

Net interest income showed a 37.3% growth y-o-y with NIM

slightly declining by 50bps and risk-adjusted NIM up by 140bps

Cost of risk seasonally dropped to 2.7% in 4Q’17

showing a y-o-y decrease by 210bps

The Group continues to maximize recoveries in-house by collecting

on delinquent loans through courts, installment processes and field

collections

We continued to write-off 360+ dpd loans

Transition to IFRS 9

41.9

32.2

-9.7

IAS 39 Transitioneffect

IFRS 9

All currency data are in RUB bn unless otherwise stated

EQUITY

8.8%

11.9%

IAS 39 IFRS 9

NPL

126.0%

157.6%

IAS 39 IFRS 9

NPL COVERAGE

Introduction of unused limits provisioning

All installment loans will be recognized as a stage 3 loans

Immediate 12-month ECL recognition

Effect on gross interest yield and cost of risk is estimated at 1-2 pp

KEY CHANGES

March 2018 TCS Group 2017 FY IFRS results 11

0.1 0.1 0.2 0.30.4

0.2 0.30.3

0.6

0.7

0.4 0.40.5

0.8

1.0

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Auto Other

0.4

0.9

1.0

1.8

1.3

2.7

2016 2017

1.4 1.3 1.4 1.3 1.5

0.6 0.60.8 1.0

1.30.3 0.40.5 0.6

0.90.5

1.0

1.4

0,3 0.0

0.1

0.2

0.4

2.6 2.7

3.4

4.0

5.4

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Credit-related Debit cards Merchant acquiring SME Other

4.55.5

1.8

3.61.3

2.4

3.2

0.7

0.7

8.4

15.5

2016 2017

Transactional & Servicing business:Continued growth momentum in fee and commission income

March 2018 TCS Group 2017 FY IFRS results 12

FEE AND COMMISSION INCOME INSURANCE PREMIUMS EARNED

All currency data are in RUB bn unless otherwise stated

84.9% 2.1x 2x

Non-credit revenue

(including F&C income + insurance premiums)

steady growth continues: 23% in total revenue

Rapid growth in F&C income is due to the

development of non-credit business lines, primarily

debit cards, online acquiring and SME services

We continue to view a more

aggressive growth in the

insurance business as premature

0.3 0.3 0.4 0.40.5

0.1 0.10.1

0.2

0.2

0.1 0.1

0.10.2

0.2

0.1 0.1

0.1

0.1

0.1

0.0 0.0

0.0

0.0

0.0

0.1

0.1

0.2

0.6 0.6

0.8

1.0

1.3

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Interchange FX Cash withdrawal SMS Placement Other

Transactional business: Current accounts

March 2018 TCS Group 2017 FY IFRS results 13

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17M

illio

ns

RU

B b

n

Current accounts balance (LHS) Saving accounts balance (LHS)

Customers (RHS)

BALANCES AND CUSTOMERS* FEE AND COMMISSION INCOME

All currency data are in RUB bn unless otherwise stated

2.1x

* Management estimates, unaudited

63.3%

We see our current accounts business

as the cornerstone of our customer relationship

Our award-winning mobile and internet bank applications

ensure best-in-class customer experience

* Management estimates, unaudited

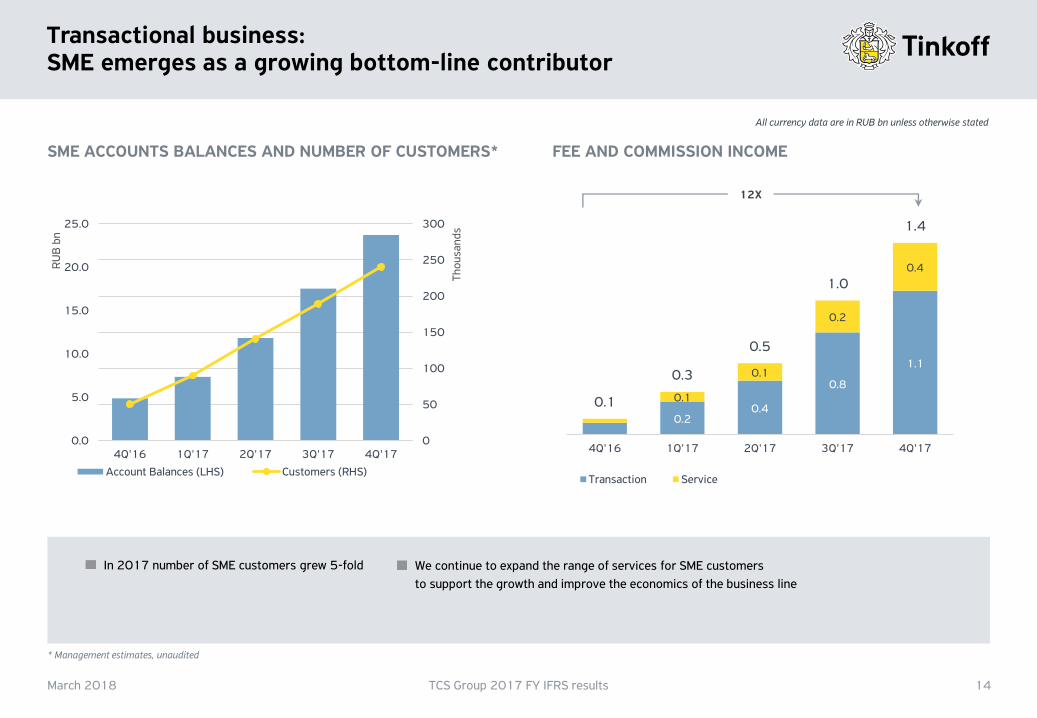

Transactional business: SME emerges as a growing bottom-line contributor

March 2018 TCS Group 2017 FY IFRS results 14

0

50

100

150

200

250

300

0.0

5.0

10.0

15.0

20.0

25.0

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17T

ho

usa

nd

s

RU

B b

n

Account Balances (LHS) Customers (RHS)

SME ACCOUNTS BALANCES AND NUMBER OF CUSTOMERS* FEE AND COMMISSION INCOME

0.20.4

0.8

1.1

0.1

0.1

0.2

0.4

0.1

0.3

0.5

1.0

1.4

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Transaction Service

All currency data are in RUB bn unless otherwise stated

12X

In 2017 number of SME customers grew 5-fold We continue to expand the range of services for SME customers

to support the growth and improve the economics of the business line

Transaction business: Mortgage broker scaling up

March 2018 TCS Group 2017 FY IFRS results 15

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

RU

B m

n

Volume (LHS) Number of mortgage loans (RHS)

MORTGAGE VOLUME ORIGINATED THROUGH TINKOFF.RU* PARTNERS

All currency data are in RUB bn unless otherwise stated

* Management estimates, unaudited

More than RUB 10bn mortgage loans were originated through

Tinkoff platform in 2017

The mortgage broker business is looking to scale up without

excessive pressure on the operating profit

Two new banks — UniCredit and Gazprombank —

joined our partners’ group

DOM.RF became our strategic partner

DeltaCredit Bank Gazprombank

Absolut Bank UniCredit Bank

URALSIB Bank AK BARS Bank

SMP Bank Metallinvestbank

Housing Finance Bank Orient Express Bank

DOM.RF

Transaction business: Tinkoff investments shows steady growth

March 2018 TCS Group 2017 FY IFRS results 16

1,123

3,424

6,099

10,057

12,441

0

10

20

30

40

50

60

70

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

RU

B'0

00

Total (RUB mn) Average (RHS)

15

13

1716

15

0%

5%

10%

15%

20%

25%

30%

35%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Accounts opened (in period) Share in new MOEX accounts (RHS)

ACCOUNTS OPENED (IN THE PERIOD) TURNOVER

All currency data are in RUB bn unless otherwise stated

We capitalize on a buoyant

growth of the Russian retail

investor market

More than 60k accounts were

opened in 2017

Tinkoff Investments is a retail securities trading platform

we launched in 3Q’16 in partnership with BCS, Russia’s

leading retail brokerage

Operating expenses

March 2018 TCS Group 2017 FY IFRS results 17

2.4 2.5 2.6 2.93.5

0.7 0.8 0.91.0

1.21.0 0.9

1.11.2

1.6

1.3 1.01.3

1.6

1.9

5.55.2

5.9

6.7

8.2

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

Administrative staff Acquisition staff Other administrative Other acquisition

7.511.4

2.6

4.03.8

4.84.0

5.8

18.0

25.9

2016 2017

All currency data are in RUB bn unless otherwise stated

STRUCTURE OF OPERATING EXPENSES* OPERATING EFFICIENCY**

47.4%

42.7% 41.9% 42.3%

45.5%

29.4%

27.7%25.9%

25.9%

28.0%30.0%

25.8% 25.5%

29.2%

27.8%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

C/I (incl. acquisition) C/I (excl. acquisition) C/I (core business)

43.9% 43.2%

27.5% 26.9%

29.1%27.1%

2016 2017

* Administrative and other operating expenses + customer acquisition expenses.** Income is stated as operating income that includes net interest income, net fee and commission income, insurance premiums earned and other operating income. Cost is stated as client acquisition expenses plus administrative and other operating expenses.

44.2%

Operating expenses were up

by 44.2% y-o-y in 2017

At the same time, cost-to-

income ratio decreased from

43.9% to 43.2%

A seasonal growth in 4Q’17 is attributed to

salary indexation and advertising expenses

51.4%42.8%

48.6% 53.7%63.1%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

8.7%7.7% 8.6% 8.9%

10.1%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

7.1%8.9%

2016 2017

42.5%52.8%

2016 2017

Net income – a set of record-high quarterly result

March 2018 TCS Group 2017 FY IFRS results 18

3.73.4

4.2

5.0

6.4

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17

11.0

19.0

2016 2017

All currency data are in RUB bn unless otherwise stated

NET INCOME RETURN ON ASSETS

RETURN ON EQUITY

72.8%

A net income of RUB 19.0bn

for 2017 with ROAE of 52.8%

Our 4Q’17 net income of RUB

6.4bn is a new quarterly record

0.17

0.20

0.22+

0.18

0.31DIVIDEND PER GDR$

$

$

$

FY2018 guidance

March 2018 TCS Group 2017 FY IFRS results 19

2017 2018F

Net loan portfolio growth 36.3% 25%+

Cost of risk (IAS 39) 5.5% Below 7%

Cost of borrowing 7.6% 6-7%

Net income RUB 19bn RUB 24bn+

Appendix

Customer profile

March 2018 TCS Group 2017 FY IFRS results 21

Platinum Credit Card

All AirlinesCredit cobrands

Tinkoff BlackDebit cobrands

TinkoffInvestments

Gender (M/F) 47/53 64/36 60/40 63/37 56/44 88/12

Average age 41 37 34 35 37 33

Monthly income (kRUB) 47 113 68 80 65 90

Geography

Moscow and Moscow Region

19% 47% 24% 39% 25% 41%

Saint-Petersburg and Leningradskaya oblast’

8% 12% 9% 13% 12% 12%

Every other region < 5% < 3% < 9% < 3% < 3% < 3%

Credit Transactional & Servicing

17.1%22.2%

25.5%

33.2% 39.4% 42.8%45.5%

0.4% 2.2% 2.5% 4.2%

5.8%

7.2%

7.5%

6.7%8.3%

10.3%

11.6%

4.6%

5.7%

7.1%7.0%

7.3%

8.3%

5.8% 10.0%10.9%

9.4%

7.2%

6.4%

6.6%7.8%

8.1%

6.9%

69.1% 55.7% 48.5%40.9%

39.6%

36.8%

35.9%

29.5%23.4% 18.9%

16.2%

25.2%31.1% 30.3%

28.1%

24.4%

22.0%

19.0%

17.0%

14.1%12.6%

11.4%

177 206 193

228

368

671

990

1,156

1,032 999

1,122

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Other consumer banks*

58% 63% 69% 72%

Credit card market: resumed growth while consolidating

March 2018 TCS Group 2017 FY IFRS results 22

* Other consumer banks include OTP Bank, Binbank credit cards, HCF Bank, Orient Express Bank, Credit Europe Bank, MTS Bank, Trust, Renaissance Credit, Sovcombank and Russian Standard BankSource: Bank’s analytics based on CBR 101 form

2017 consumer credit portfolio dynamics

• Credit cards: 12.3%

• Mortgage: 15.0%

• Other: 10.7%

Top 4 players:

RUSSIAN CREDIT CARD MARKET

All currency data are in RUB bn unless otherwise stated

Tinkoff financial supermarket: Ecosystem built around the customer

March 2018 TCS Group 2017 FY IFRS results 23

* “Under Construction”

SM

E

Cre

dit

car

ds

Insu

ran

ce

Mo

bile

an

d p

aym

ents

Broker platform Proprietary products

Car

loan

s*

Cas

h lo

ans*

Insu

ran

ce

Tra

vel

Acq

uiri

ng

Ret

ail s

ecur

itie

s

Mo

rtg

ages

MV

NO

Tinkoff ID: customer’s key for Tinkoff.ru

Cu

rren

t ac

cou

nts

Customer lands on potal

Long-term perspective – profitability

March 2018 TCS Group 2017 FY IFRS results 24

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0.0

0.8

1.6

2.4

3.2

4.0

4.8

5.6

6.4

7.2

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013 2014 2015 2016 2017

RU

B b

n

Profit (quarterly) ROE (YTD), rs

• Russian consumer finance crisis

• Macro weakness

• Low oil prices

• Geopolitics

Long-term perspective – growth

March 2018 TCS Group 2017 FY IFRS results 25

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

0

20

40

60

80

100

120

140

160

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013 2014 2015 2016 2017

RU

B b

n

Loans and advances to retail customers LTM Tinkoff portfolio growth, rs LTM market growth, rs

• Russian consumer finance crisis

• Macro weakness

• Low oil prices

• Geopolitics

Issue in lombard

74%

Issue not in lombard26% Financial

33%

Communications

4%

Industrial10%Utilities

5%

Government20%

Energy19%

Basic Materials

8%

Consumer, Non-cyclical

2%

RUB65%

FX35%

0-113%

1-327%

3-542%

5+18%

>=BBB-44%

BB+21%

BB7%

BB-7%

B+ 21%

Structure of the treasury portfolio

March 2018 TCS Group 2017 FY IFRS results 26

Note: management estimates, unaudited

BY RATING BY DURATION BY CURRENCY

IN CBR LOMBARD BY SECTOR

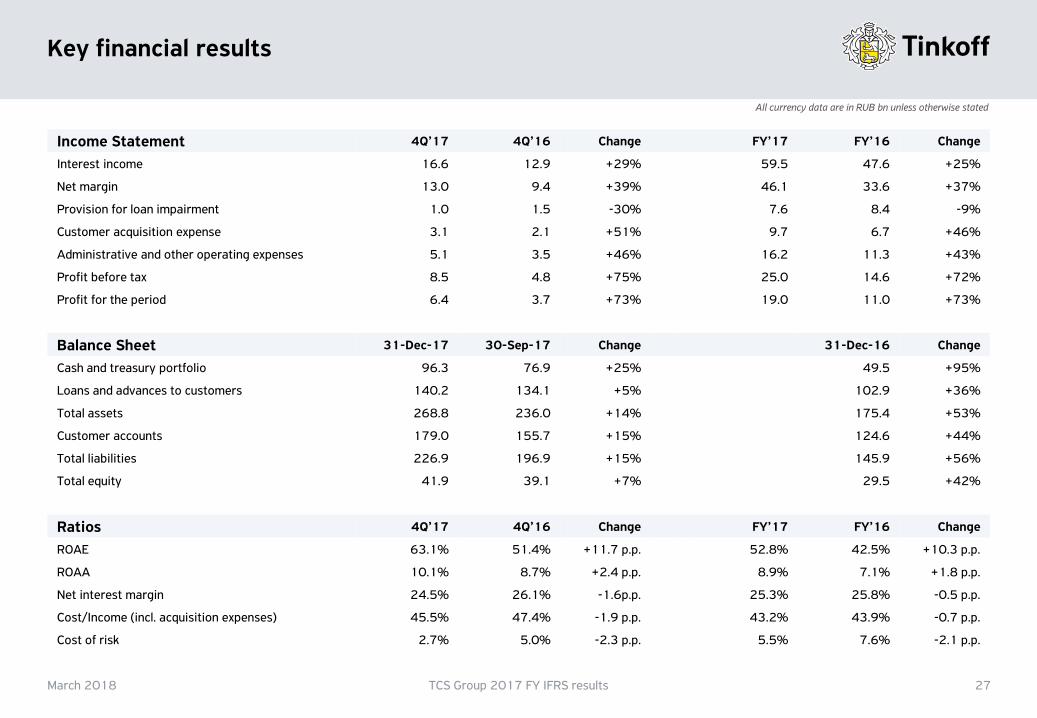

Key financial results

March 2018 TCS Group 2017 FY IFRS results 27

Income Statement 4Q’17 4Q’16 Change FY’17 FY’16 Change

Interest income 16.6 12.9 +29% 59.5 47.6 +25%

Net margin 13.0 9.4 +39% 46.1 33.6 +37%

Provision for loan impairment 1.0 1.5 -30% 7.6 8.4 -9%

Customer acquisition expense 3.1 2.1 +51% 9.7 6.7 +46%

Administrative and other operating expenses 5.1 3.5 +46% 16.2 11.3 +43%

Profit before tax 8.5 4.8 +75% 25.0 14.6 +72%

Profit for the period 6.4 3.7 +73% 19.0 11.0 +73%

Balance Sheet 31-Dec-17 30-Sep-17 Change 31-Dec-16 Change

Cash and treasury portfolio 96.3 76.9 +25% 49.5 +95%

Loans and advances to customers 140.2 134.1 +5% 102.9 +36%

Total assets 268.8 236.0 +14% 175.4 +53%

Customer accounts 179.0 155.7 +15% 124.6 +44%

Total liabilities 226.9 196.9 +15% 145.9 +56%

Total equity 41.9 39.1 +7% 29.5 +42%

Ratios 4Q’17 4Q’16 Change FY’17 FY’16 Change

ROAE 63.1% 51.4% +11.7 p.p. 52.8% 42.5% +10.3 p.p.

ROAA 10.1% 8.7% +2.4 p.p. 8.9% 7.1% +1.8 p.p.

Net interest margin 24.5% 26.1% -1.6p.p. 25.3% 25.8% -0.5 p.p.

Cost/Income (incl. acquisition expenses) 45.5% 47.4% -1.9 p.p. 43.2% 43.9% -0.7 p.p.

Cost of risk 2.7% 5.0% -2.3 p.p. 5.5% 7.6% -2.1 p.p.

All currency data are in RUB bn unless otherwise stated