TCIOceania16 The Defence Teaming Centre’s role in South Australia

Upload

tci-networkCategory

view

338download

1

Upgrading Australia’s Competitiveness: The Role of Cluster-based Economic Development

Christian H. M. Ketels

3rd TCI Oceania Cluster Conference, Adelaide, 1-3 June 2016 "Driving (Regional) Competitiveness through Innovative Clusters to Bolster National Prosperity"

Upgrading Australia’s Competitiveness: The Role of Cluster-based Economic Development

Dr. Christian H. M. KetelsInstitute for Strategy and Competitiveness, Harvard Business School

President, The TCI Network

Adelaide, Australia2 June 2016

2 Copyright 2013 © Christian Ketels

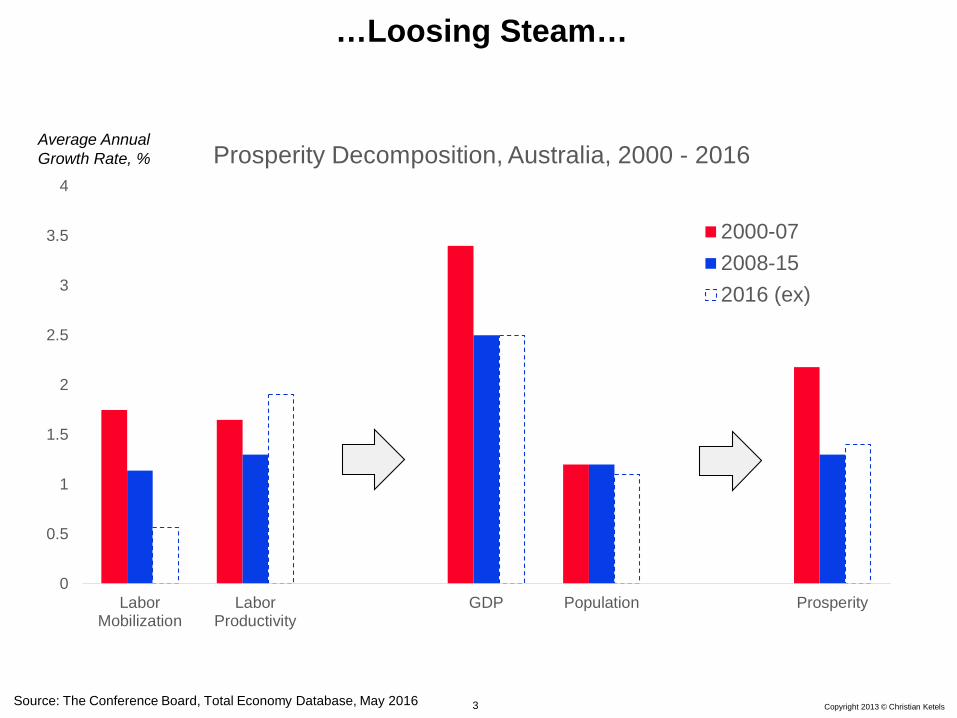

The Lucky Country…

Australia outperforming its peers, fueled by..• Past policy reforms• China-driven natural resource-boom• (Partial) isolation from US/European crises

Source: IMF, 2016

3 Copyright 2013 © Christian Ketels

…Loosing Steam…

0

0.5

1

1.5

2

2.5

3

3.5

4

LaborMobilization

LaborProductivity

GDP Population Prosperity

Prosperity Decomposition, Australia, 2000 - 2016

2000-072008-152016 (ex)

Source: The Conference Board, Total Economy Database, May 2016

Average Annual Growth Rate, %

4 Copyright 2013 © Christian Ketels

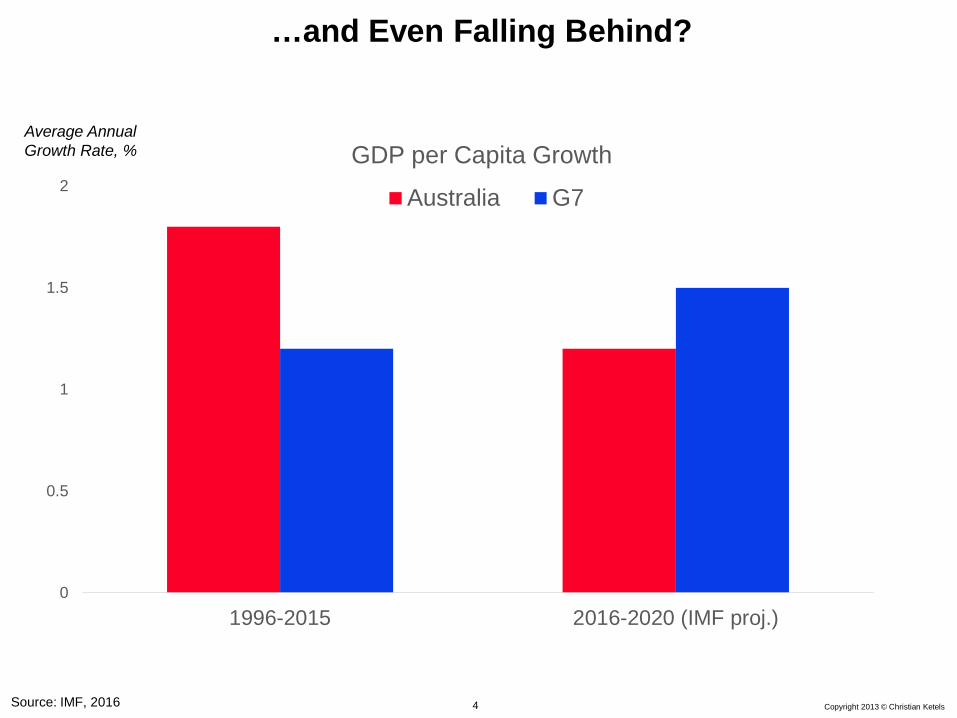

…and Even Falling Behind?

0

0.5

1

1.5

2

1996-2015 2016-2020 (IMF proj.)

GDP per Capita Growth

Australia G7

Average Annual Growth Rate, %

Source: IMF, 2016

5 Copyright 2013 © Christian Ketels

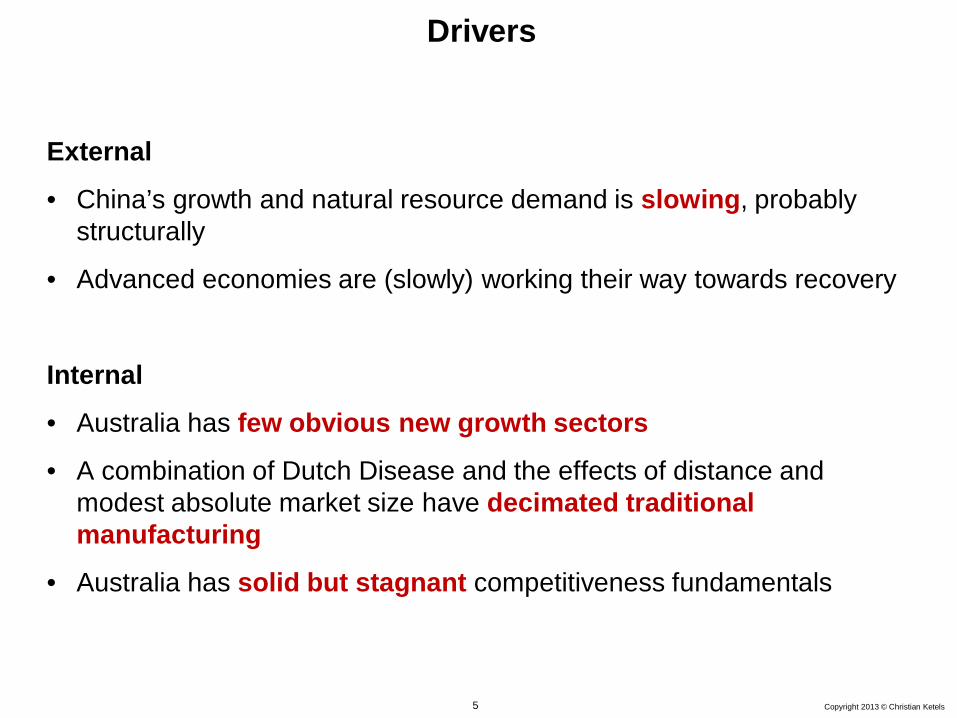

Drivers

External

• China’s growth and natural resource demand is slowing, probably structurally

• Advanced economies are (slowly) working their way towards recovery

Internal

• Australia has few obvious new growth sectors

• A combination of Dutch Disease and the effects of distance and modest absolute market size have decimated traditional manufacturing

• Australia has solid but stagnant competitiveness fundamentals

6 Copyright 2013 © Christian Ketels

Australia’s Competitiveness Fundamentals over Time

Openness ofProduct Markets

Cost of Doing Business

Overall Competitiveness

• 2008: Rank 13 • 2013: Rank 8

• 2010: 81% • 2016: 80%

• 2010: Rank 15 • 2015: Rank 22

7 Copyright 2013 © Christian Ketels

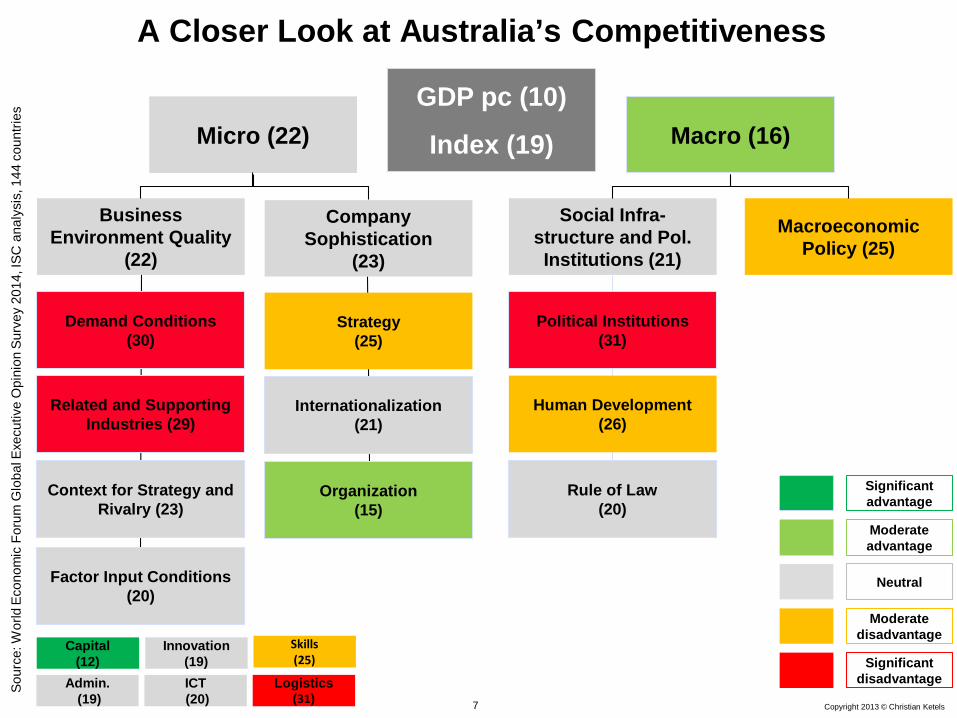

A Closer Look at Australia’s Competitiveness

Macro (16)

Political Institutions (31)

Human Development (26)

Rule of Law(20)

Demand Conditions (30)

Related and Supporting Industries (29)

Context for Strategy and Rivalry (23)

Factor Input Conditions (20)

Micro (22)

Capital (12)

Admin.(19)

Logistics (31)

ICT(20)

Innovation(19)

GDP pc (10)

Index (19)

Social Infra-structure and Pol. Institutions (21)

Macroeconomic Policy (25)

Business Environment Quality

(22)

Company Sophistication

(23)

Sour

ce: W

orld

Eco

nom

ic F

orum

Glo

bal E

xecu

tive

Opi

nion

Sur

vey

2014

, ISC

ana

lysi

s, 1

44 c

ount

ries

Strategy(25)

Internationalization (21)

Organization(15)

Skills(25)

Significant advantage

Moderateadvantage

Neutral

Moderate disadvantage

Significant disadvantage

8 Copyright 2013 © Christian Ketels

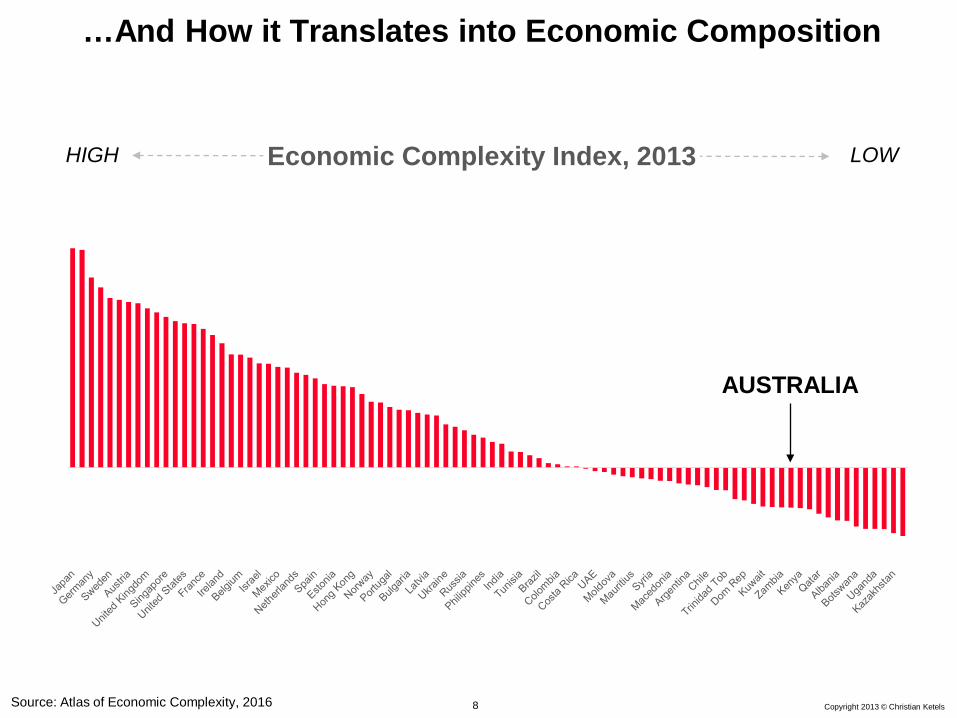

…And How it Translates into Economic Composition

Economic Complexity Index, 2013

AUSTRALIA

Source: Atlas of Economic Complexity, 2016

HIGH LOW

9 Copyright 2013 © Christian Ketels

Australia’s Competitiveness Challenge 2016

• What will be Australia’s positioning in the Asian/Oceanic and global economy in the future?

• In what sectors and markets will companies from Australia be able to successfully compete?

• What policies can help Australia build sustainable competitive advantages in specific areas?

• What role can cluster-based economic development approaches play in addressing these questions?

10 Copyright 2016 © Christian Ketels

Clusters: An Established Concept….

11 Copyright 2016 © Christian Ketels

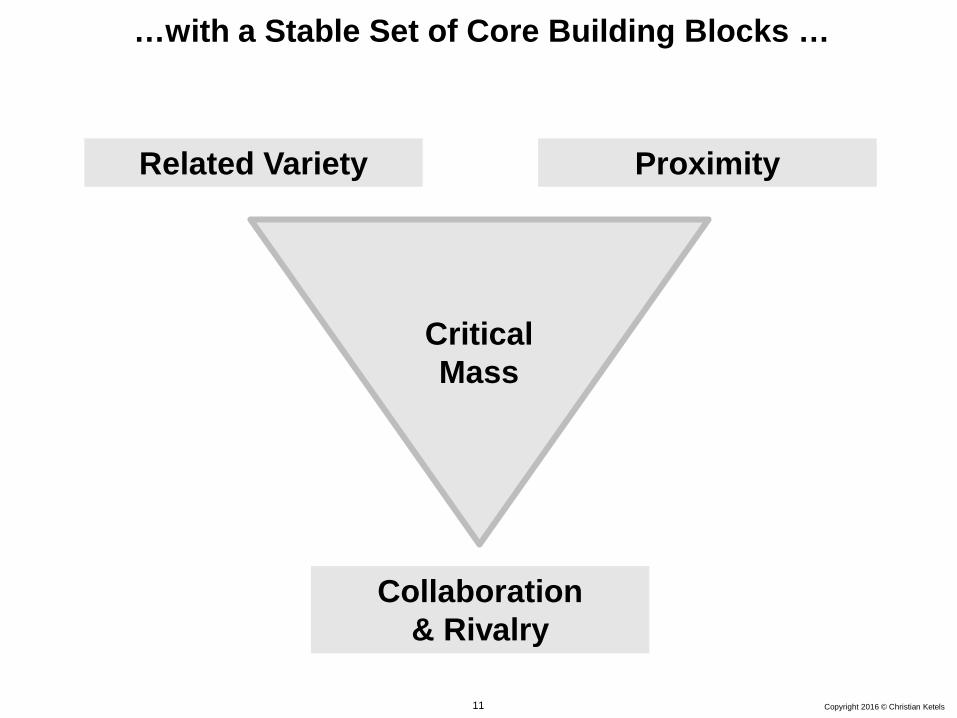

…with a Stable Set of Core Building Blocks …

Collaboration & Rivalry

Related Variety

Critical Mass

Proximity

12 Copyright 2015 © Christian Ketels

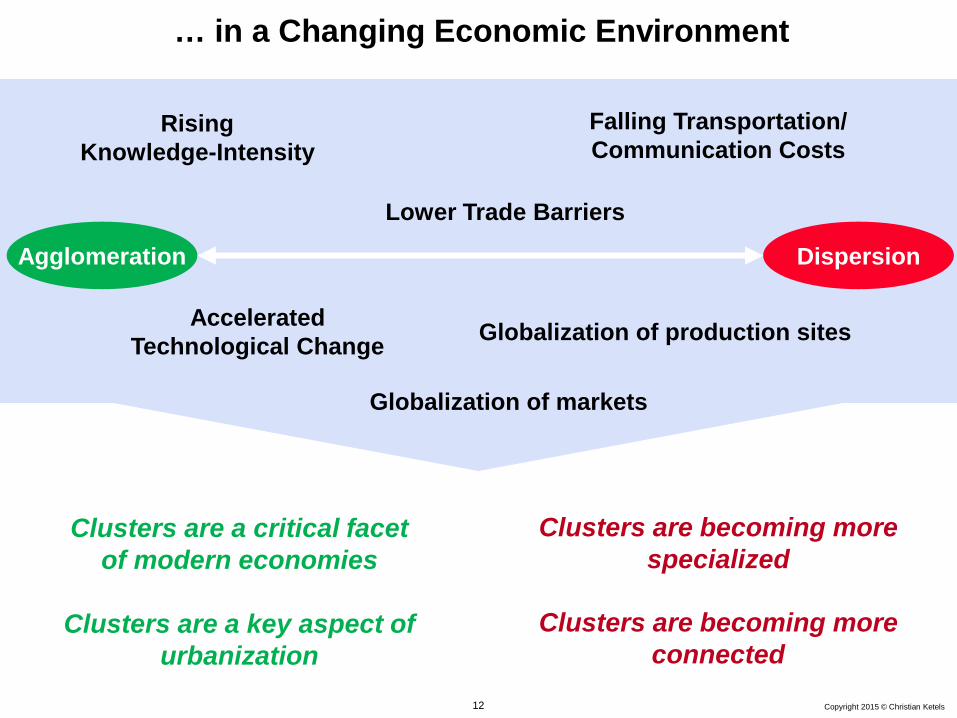

… in a Changing Economic Environment

Rising Knowledge-Intensity

Lower Trade Barriers

Globalization of production sites

Falling Transportation/Communication Costs

Accelerated Technological Change

Clusters are a critical facet of modern economies

Clusters are a key aspect of urbanization

Clusters are becoming more specialized

Clusters are becoming more connected

Agglomeration Dispersion

Globalization of markets

13 Copyright 2015 © Christian Ketels

14 Copyright 2015 © Christian Ketels

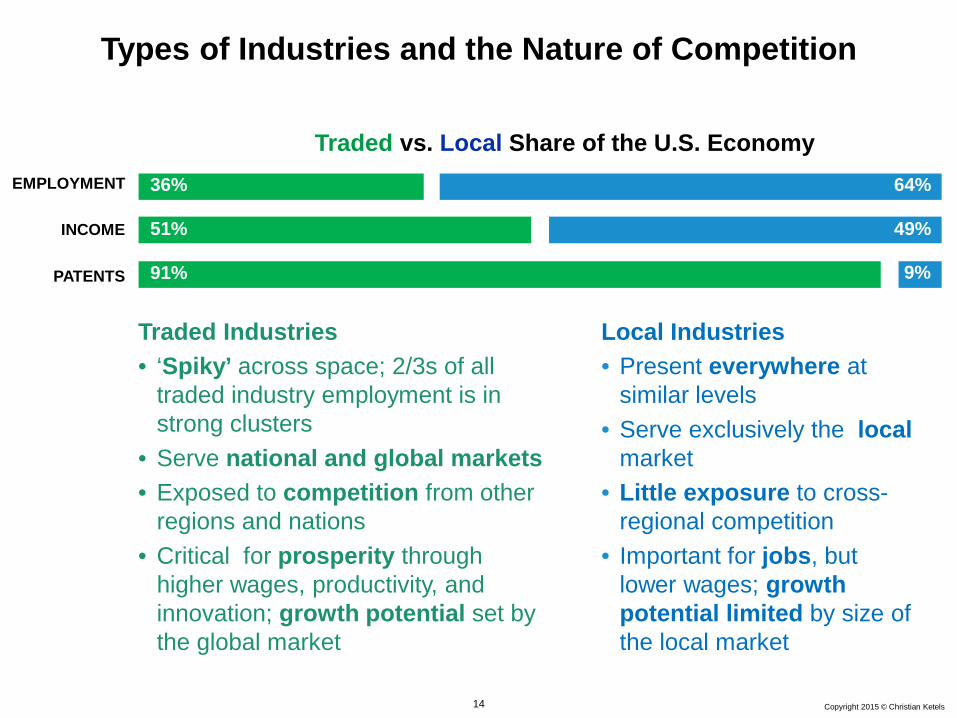

Types of Industries and the Nature of Competition

EMPLOYMENT

INCOME

PATENTS

36% 64%

51% 49%

91% 9%

Local Industries• Present everywhere at

similar levels• Serve exclusively the local

market• Little exposure to cross-

regional competition • Important for jobs, but

lower wages; growth potential limited by size of the local market

Traded Industries• ‘Spiky’ across space; 2/3s of all

traded industry employment is in strong clusters

• Serve national and global markets• Exposed to competition from other

regions and nations• Critical for prosperity through

higher wages, productivity, and innovation; growth potential set by the global market

Traded vs. Local Share of the U.S. Economy

15

Employees 50,000 =

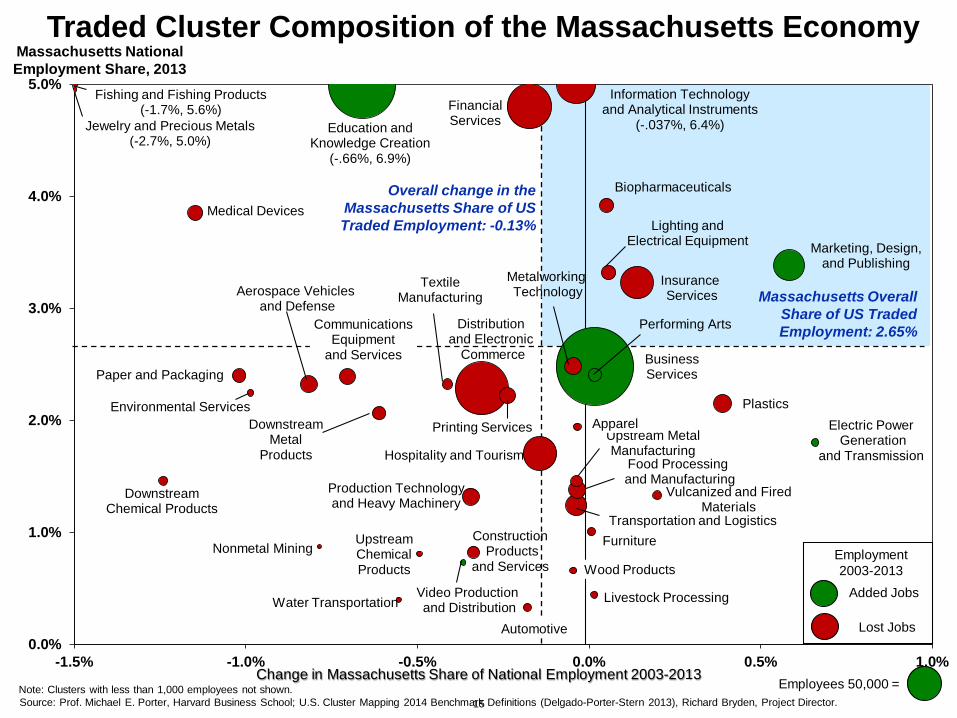

Traded Cluster Composition of the Massachusetts Economy

Note: Clusters with less than 1,000 employees not shown.Source: Prof. Michael E. Porter, Harvard Business School; U.S. Cluster Mapping 2014 Benchmark Definitions (Delgado-Porter-Stern 2013), Richard Bryden, Project Director.

Overall change in the Massachusetts Share of US Traded Employment: -0.13%

Massachusetts Overall Share of US Traded Employment: 2.65%

Added Jobs

Lost Jobs

Employment 2003-2013

Massachusetts National Employment Share, 2013

Change in Massachusetts Share of National Employment 2003-2013

Business Services

Education and Knowledge Creation

(-.66%, 6.9%)

Marketing, Design, and Publishing

Performing Arts

Electric PowerGeneration

and Transmission

Video Productionand Distribution

Distribution and Electronic

Commerce

Financial Services

Information Technology and Analytical Instruments

(-.037%, 6.4%)

Hospitality and Tourism

InsuranceServices

Transportation and Logistics

Plastics

Food Processingand Manufacturing

Production Technology and Heavy Machinery

Aerospace Vehiclesand Defense

MetalworkingTechnology

Communications Equipment

and Services

Printing Services

Medical DevicesLighting and

Electrical Equipment

Biopharmaceuticals

Paper and Packaging

Downstream Metal

Products

ConstructionProducts

and Services

Upstream Metal Manufacturing

Textile Manufacturing

Downstream Chemical Products

Furniture

Vulcanized and Fired Materials

Automotive

Apparel

Wood Products

Livestock Processing

Fishing and Fishing Products(-1.7%, 5.6%)

Environmental Services

Upstream Chemical Products

Jewelry and Precious Metals(-2.7%, 5.0%)

Water Transportation

Nonmetal Mining

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0%

16

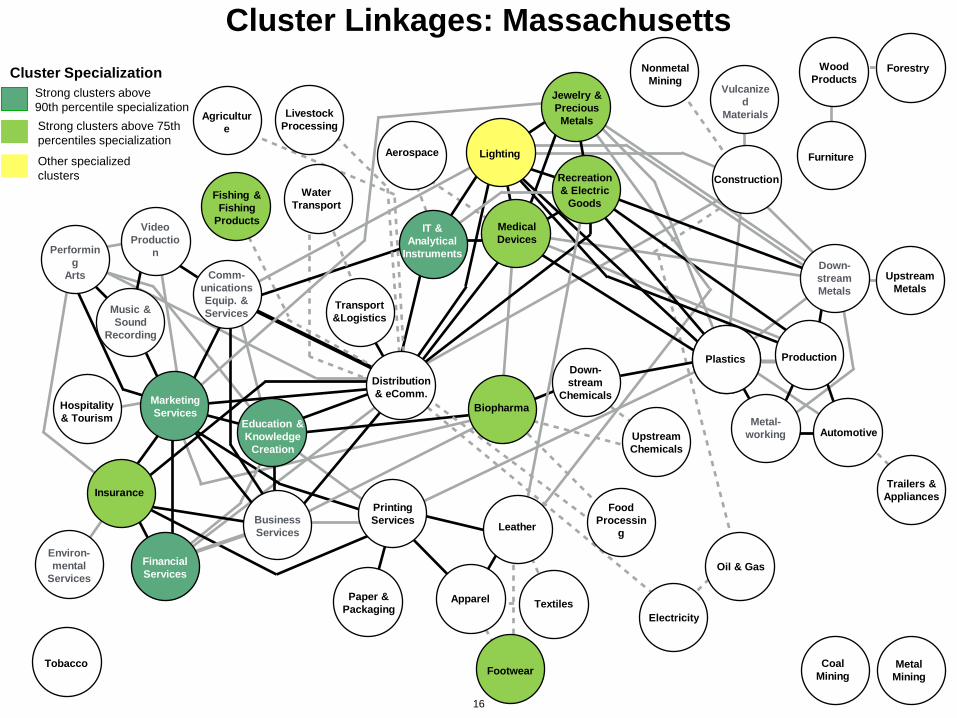

Cluster Linkages: Massachusetts

Metal-working

Food Processin

g

Lighting

IT & Analytical

Instruments

Comm-unicationsEquip. & Services

Down-stream

ChemicalsBiopharma

Leather

Apparel

PrintingServices

FinancialServices

Insurance

Environ-mental

Services

BusinessServices

Education & Knowledge

Creation

MarketingServices

Music & Sound

Recording

Performing

Arts

VideoProductio

n

Hospitality& Tourism

Metal Mining

CoalMining

UpstreamMetals

Wood Products

Furniture

Tobacco

Aerospace

UpstreamChemicals

Trailers & Appliances

Textiles

Footwear

Forestry

Agriculture

PlasticsPlastics

Distribution& eComm.

LivestockProcessing

Fishing &Fishing

Products

Water Transport

Transport &Logistics

Vulcanized

Materials

Construction

NonmetalMining

Oil & Gas

Electricity

Down-streamMetals

Production

Metal-working Automotive

Paper &Packaging

Recreation& Electric

Goods

Jewelry & Precious Metals

Strong clusters above 90th percentile specialization

Other specialized clusters

Strong clusters above 75th percentiles specialization

Cluster Specialization

MedicalDevices

17 Copyright 2013 © Christian Ketels

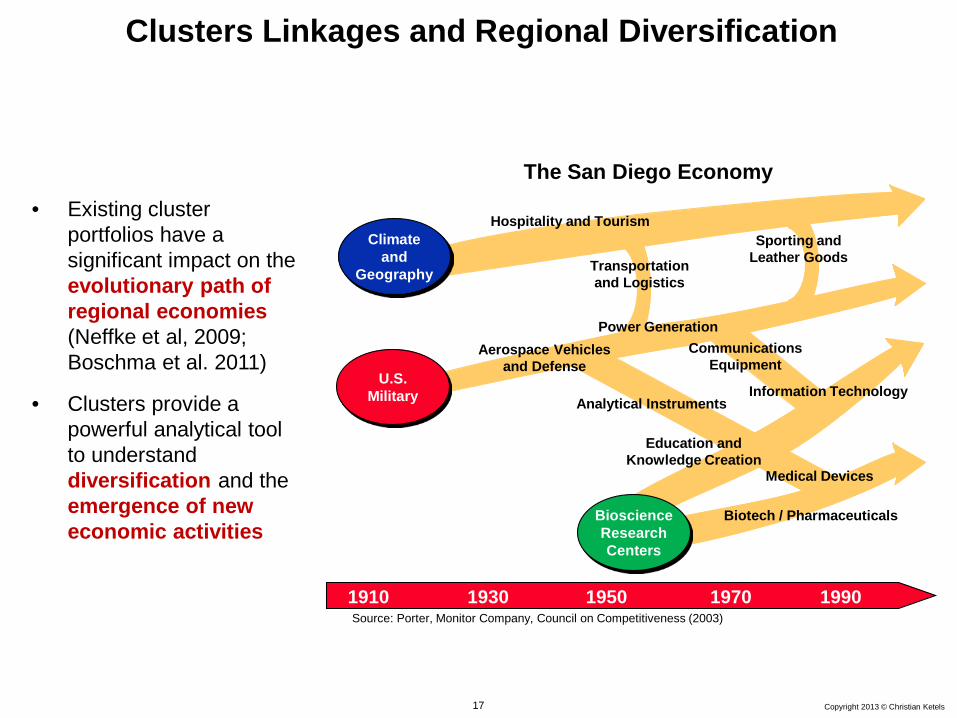

Clusters Linkages and Regional Diversification

U.S. Military

CommunicationsEquipment

Sporting andLeather Goods

Analytical Instruments

Power GenerationAerospace Vehicles

and Defense

Transportationand Logistics

Information Technology

1910 1930 1950 19901970

Bioscience Research Centers

Climate and

Geography

Hospitality and Tourism

Medical Devices

Biotech / Pharmaceuticals

Education andKnowledge Creation

• Existing cluster portfolios have a significant impact on the evolutionary path of regional economies (Neffke et al, 2009; Boschma et al. 2011)

• Clusters provide a powerful analytical tool to understand diversification and the emergence of new economic activities

The San Diego Economy

Source: Porter, Monitor Company, Council on Competitiveness (2003)

18 Copyright 2015 © Christian Ketels

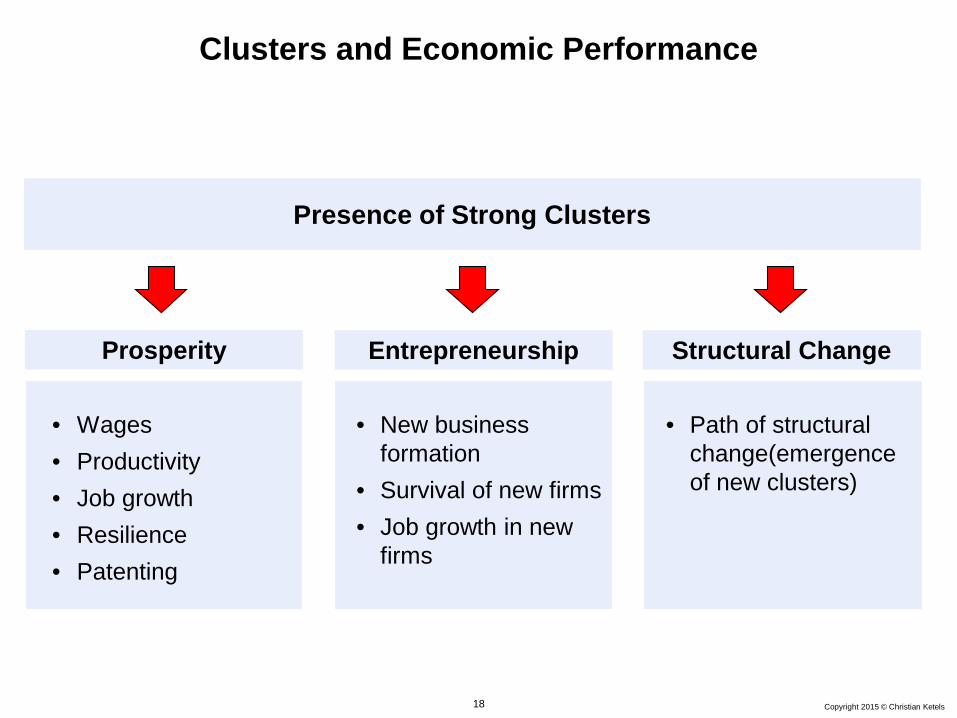

Clusters and Economic Performance

Prosperity Entrepreneurship Structural Change

• Wages• Productivity• Job growth• Resilience• Patenting

• New business formation

• Survival of new firms• Job growth in new

firms

• Path of structural change(emergence of new clusters)

Presence of Strong Clusters

19 Copyright 2015 © Christian Ketels

Putting Clusters into Context

(Creative) Skills

ComplexitySocial Capital

Innovation Systems

Entrepreneurial Ecosystems

Framework Conditions

Clusters

Urbanization

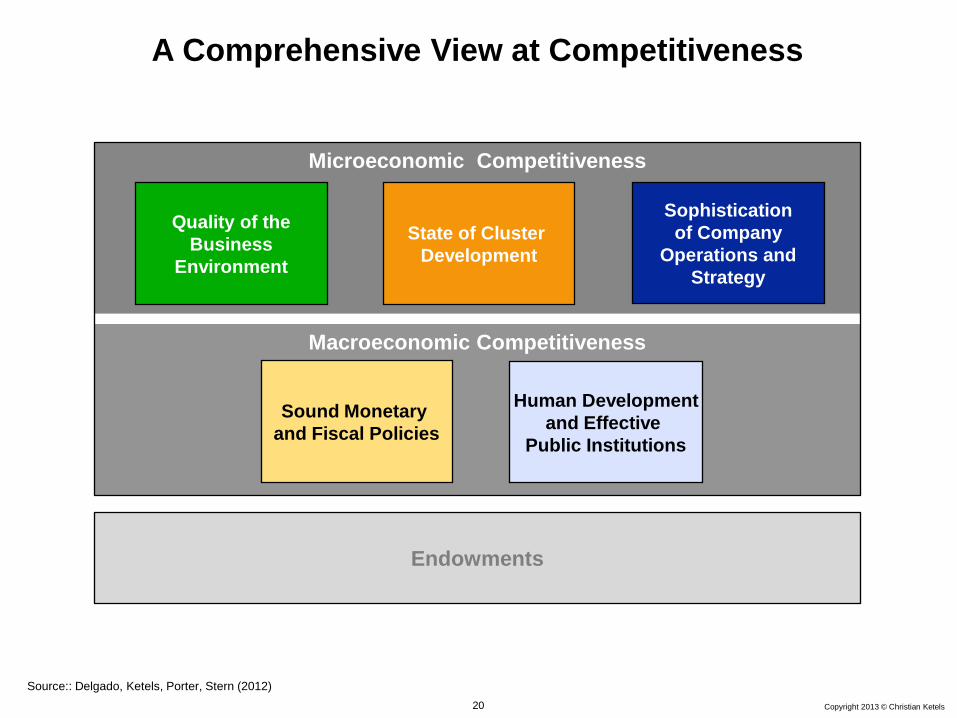

20 Copyright 2013 © Christian Ketels

Macroeconomic Competitiveness

Microeconomic Competitiveness

Sophisticationof Company

Operations andStrategy

Quality of the Business

Environment

State of Cluster Development

Endowments

Human Development and Effective

Public Institutions

Sound Monetary and Fiscal Policies

A Comprehensive View at Competitiveness

Source:: Delgado, Ketels, Porter, Stern (2012)

21 Copyright 2013 © Christian Ketels

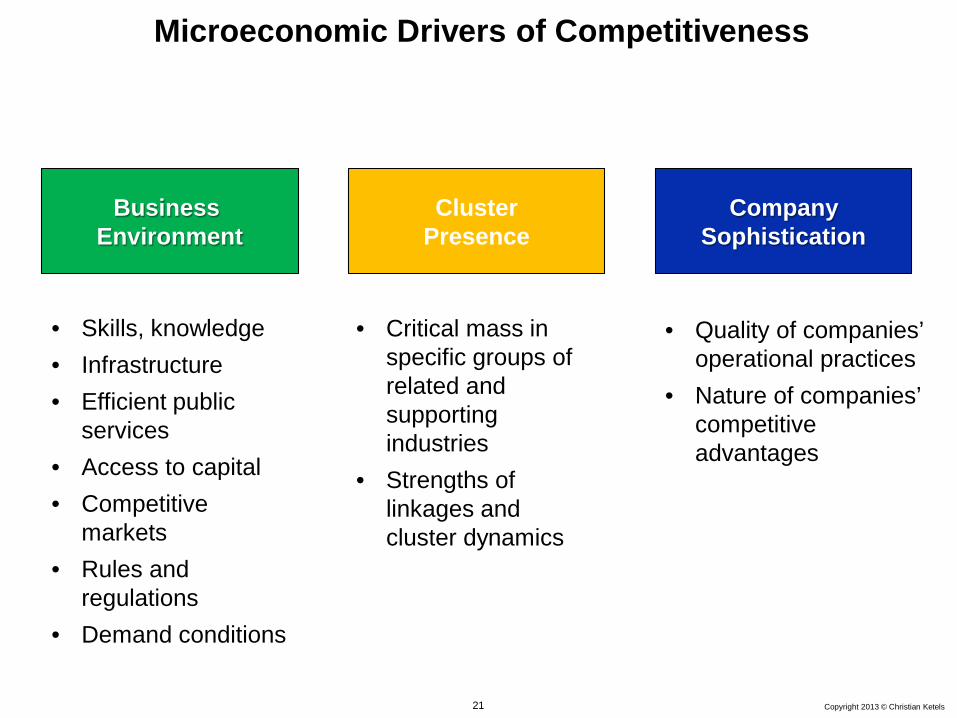

Microeconomic Drivers of Competitiveness

Business Environment

• Skills, knowledge• Infrastructure• Efficient public

services• Access to capital• Competitive

markets• Rules and

regulations• Demand conditions

ClusterPresence

• Critical mass in specific groups of related and supporting industries

• Strengths of linkages and cluster dynamics

CompanySophistication

• Quality of companies’ operational practices

• Nature of companies’ competitive advantages

22 Copyright 2013 © Christian Ketels

Upgrading Competitiveness: Principles

• There is no silver bullet

• Many things matter

• What matters most depends on what you already have

• Every location is different, but all adhere to the same economic principles and dynamics

• You can’t change everything at once, even if all has to change eventually

• Change requires action by many

23 Copyright 2013 © Christian Ketels

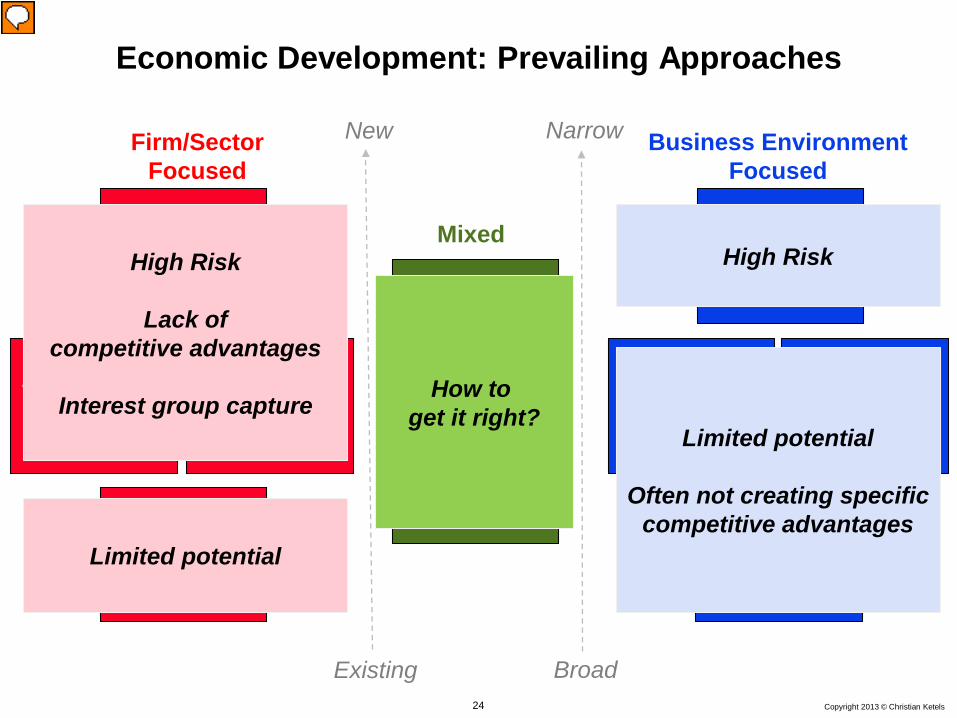

Economic Development: Prevailing Approaches

Entrepr.Eco-

systems

Clusters

Mixed

Economic Gardening

Big Game Hunting

The Next Big Thing

Picking Winners

Firm/Sector Focused

New

Existing

Framework Conditions

Build it and They Will

Come

Place Making

Open for Business

Business Environment Focused

Narrow

Broad

24 Copyright 2013 © Christian Ketels

Economic Development: Prevailing Approaches

Framework Conditions

Economic Gardening

Big Game Hunting

Build it and They Will

Come

The Next Big Thing

Picking Winners

Place Making

Open for Business

Firm/Sector Focused

Business Environment Focused

Entrepr.Eco-

systems

Clusters

Mixed

New

Existing

Narrow

Broad

High Risk

Lack ofcompetitive advantages

Interest group capture

Limited potential

Limited potential

Often not creating specificcompetitive advantages

High Risk

How to get it right?

25 Copyright 2015 © Christian Ketels

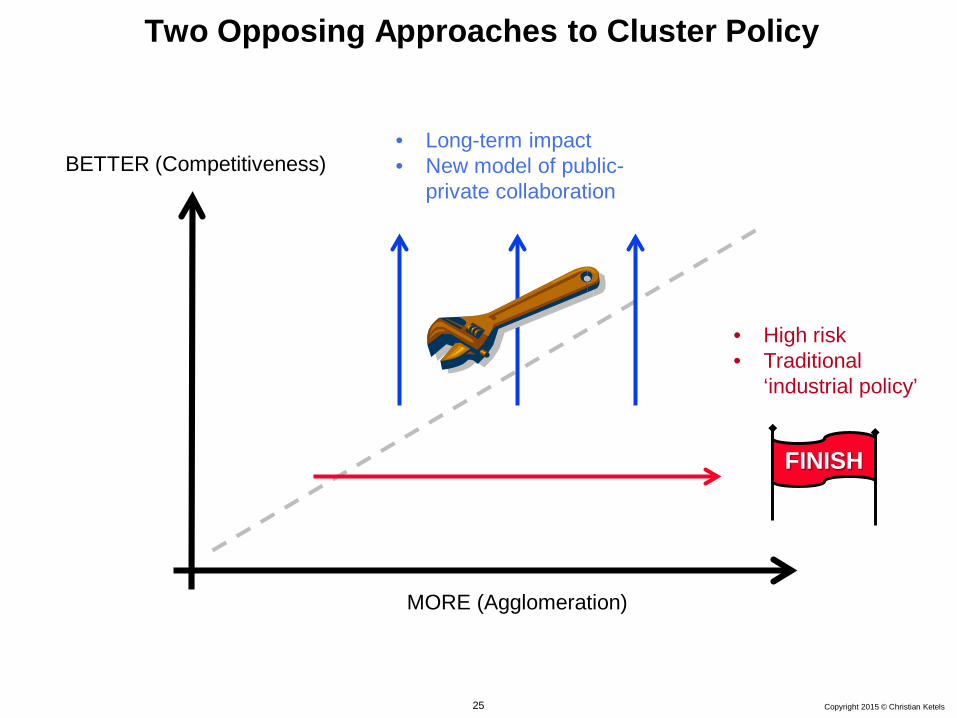

Two Opposing Approaches to Cluster Policy

MORE (Agglomeration)

BETTER (Competitiveness)

FINISH

• High risk• Traditional

‘industrial policy’

• Long-term impact• New model of public-

private collaboration

20150204 – MOC 2015 – Session 2 Copyright 2015 © Christian Ketels26

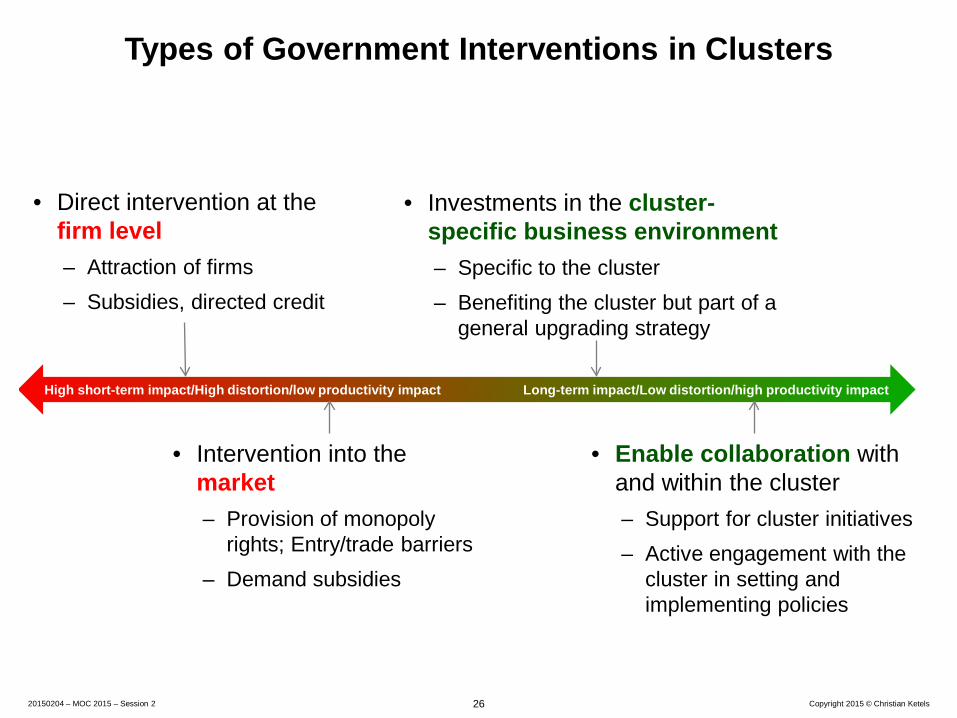

Types of Government Interventions in Clusters

• Direct intervention at the firm level– Attraction of firms– Subsidies, directed credit

High short-term impact/High distortion/low productivity impact Long-term impact/Low distortion/high productivity impact

• Intervention into the market– Provision of monopoly

rights; Entry/trade barriers– Demand subsidies

• Investments in the cluster-specific business environment– Specific to the cluster– Benefiting the cluster but part of a

general upgrading strategy

• Enable collaboration with and within the cluster– Support for cluster initiatives– Active engagement with the

cluster in setting and implementing policies

27 Copyright 2013 © Christian Ketels

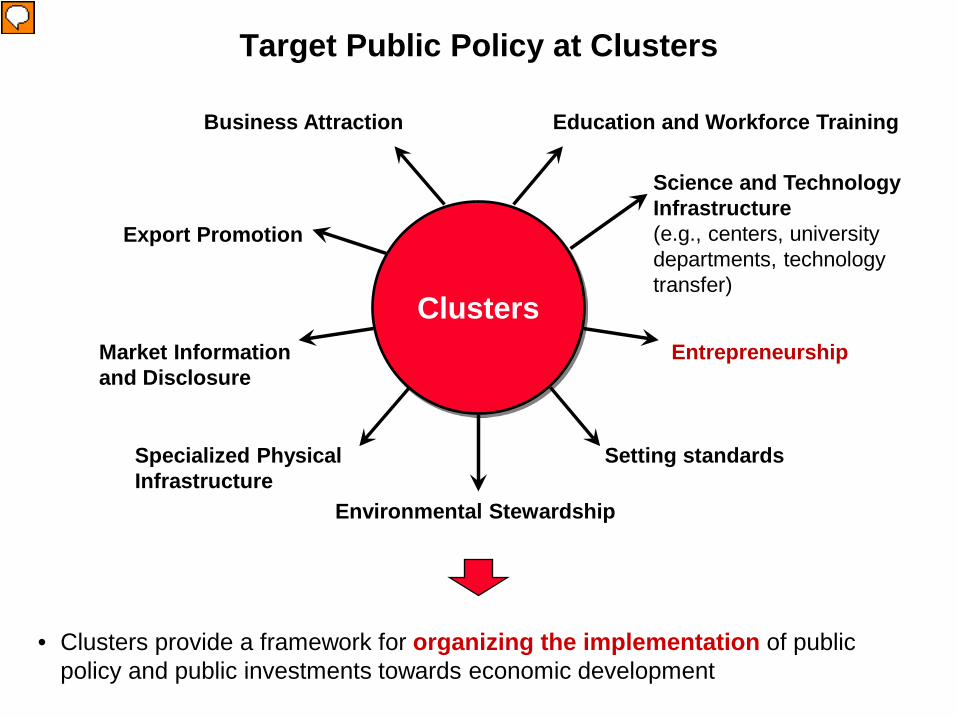

Target Public Policy at Clusters

Clusters

Specialized Physical Infrastructure

Environmental Stewardship

Setting standards

Science and TechnologyInfrastructure (e.g., centers, university departments, technology transfer)

Education and Workforce TrainingBusiness Attraction

Export Promotion

• Clusters provide a framework for organizing the implementation of public policy and public investments towards economic development

EntrepreneurshipMarket Information and Disclosure

28 Copyright 2016 © Christian Ketels

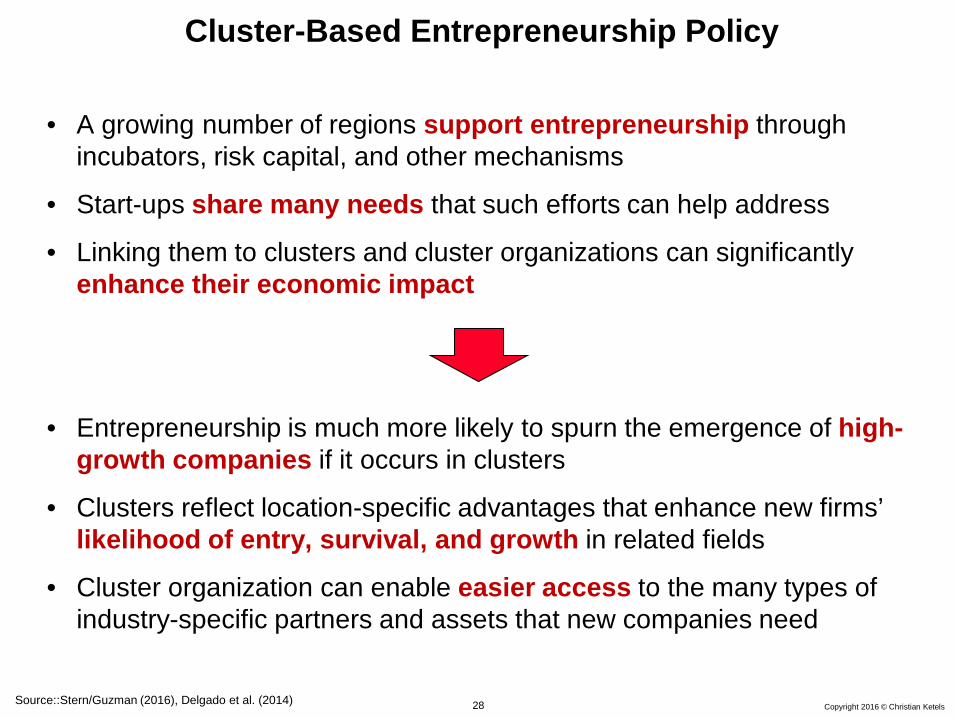

Cluster-Based Entrepreneurship Policy

• A growing number of regions support entrepreneurship through incubators, risk capital, and other mechanisms

• Start-ups share many needs that such efforts can help address

• Linking them to clusters and cluster organizations can significantly enhance their economic impact

• Entrepreneurship is much more likely to spurn the emergence of high-growth companies if it occurs in clusters

• Clusters reflect location-specific advantages that enhance new firms’ likelihood of entry, survival, and growth in related fields

• Cluster organization can enable easier access to the many types of industry-specific partners and assets that new companies need

Source::Stern/Guzman (2016), Delgado et al. (2014)

29 Copyright 2015 © Christian Ketels

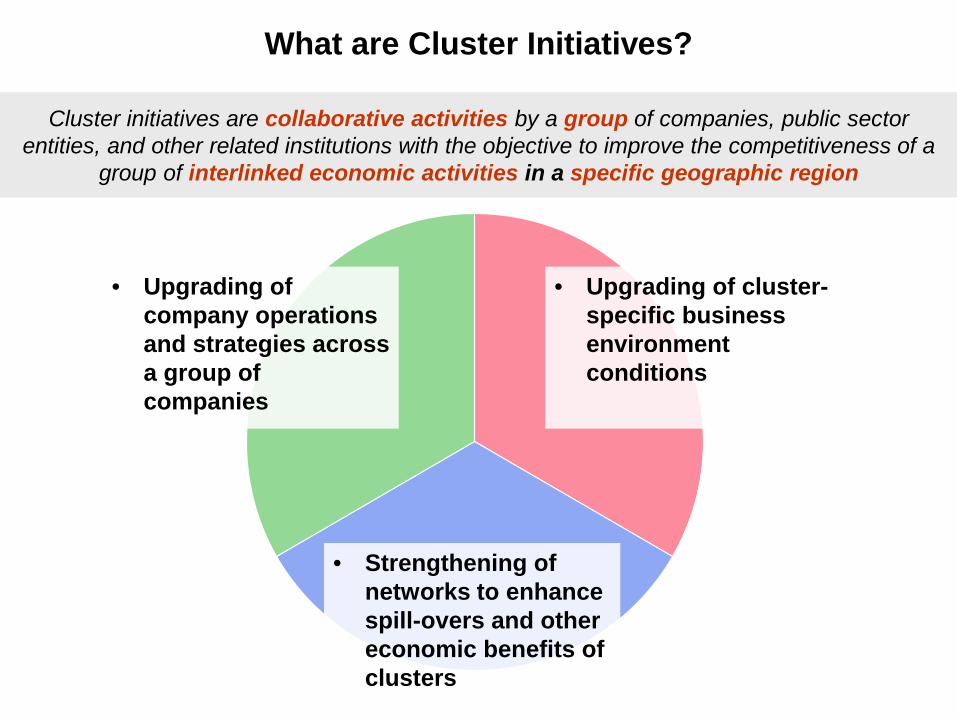

What are Cluster Initiatives?

• Upgrading of company operations and strategies across a group of companies

• Strengthening of networks to enhance spill-overs and other economic benefits of clusters

• Upgrading of cluster-specific business environment conditions

Cluster initiatives are collaborative activities by a group of companies, public sector entities, and other related institutions with the objective to improve the competitiveness of a

group of interlinked economic activities in a specific geographic region

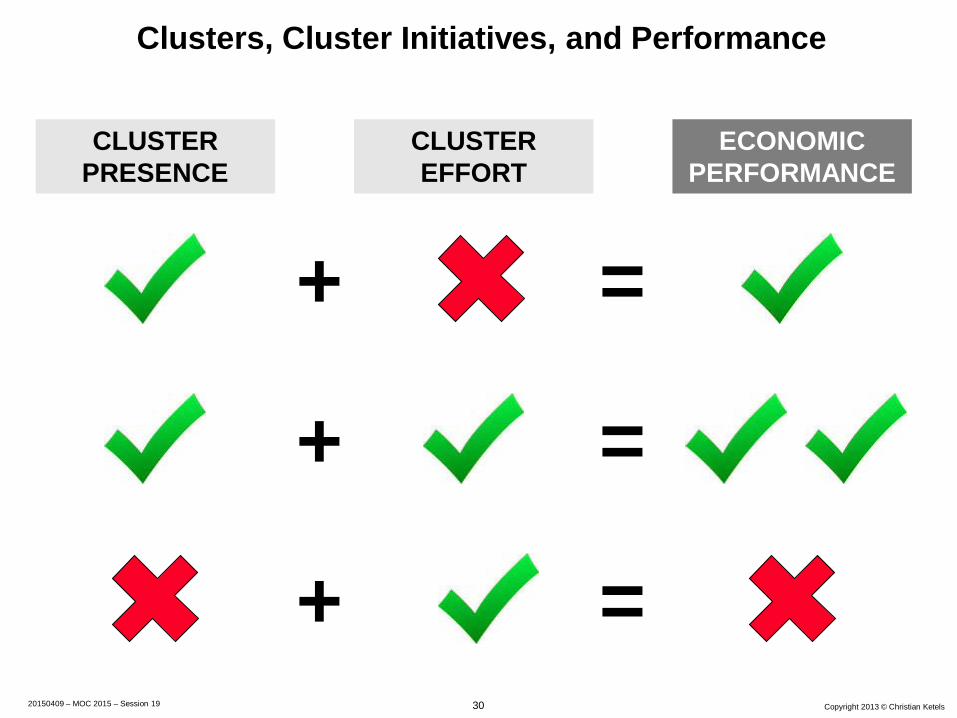

30 Copyright 2013 © Christian Ketels

Clusters, Cluster Initiatives, and Performance

CLUSTERPRESENCE

CLUSTEREFFORT

ECONOMICPERFORMANCE

+ =

+ =

+ =

20150409 – MOC 2015 – Session 19

31 Copyright 2015 © Christian Ketels

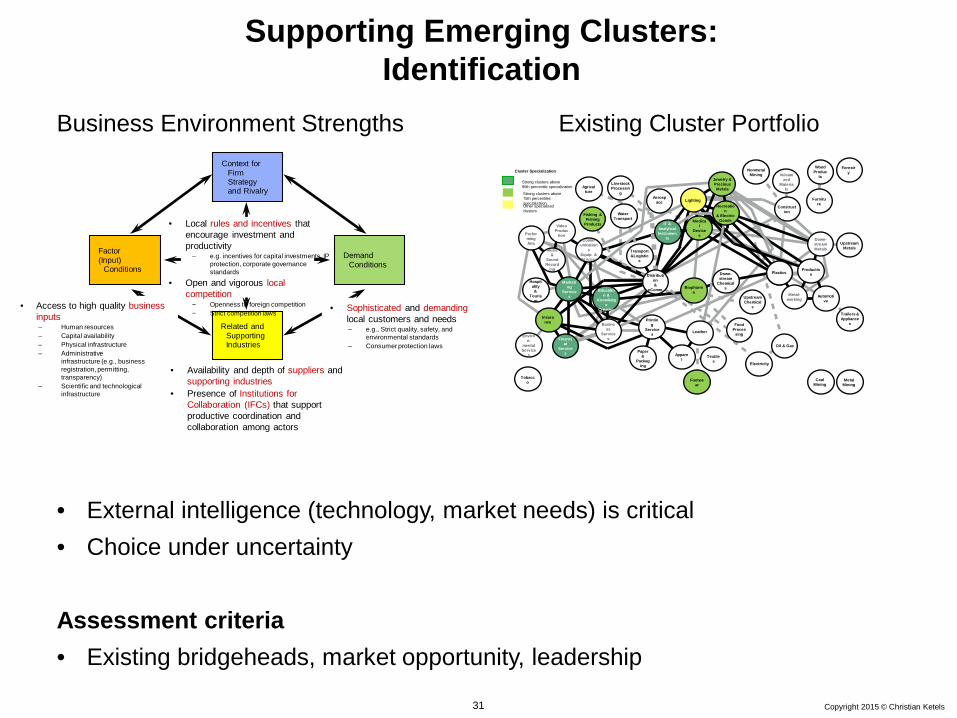

Supporting Emerging Clusters: Identification

Context for Firm Strategy and Rivalry

Related and Supporting Industries

Factor(Input)

Conditions

Demand Conditions

• Sophisticated and demandinglocal customers and needs– e.g., Strict quality, safety, and

environmental standards– Consumer protection laws

• Local rules and incentives that encourage investment and productivity

– e.g. incentives for capital investments, IP protection, corporate governance standards

• Open and vigorous local competition− Openness to foreign competition− Strict competition laws

• Access to high quality business inputs– Human resources– Capital availability– Physical infrastructure– Administrative

infrastructure (e.g., business registration, permitting, transparency)

– Scientific and technological infrastructure

• Availability and depth of suppliers and supporting industries

• Presence of Institutions for Collaboration (IFCs) that support productive coordination and collaboration among actors

Business Environment Strengths Existing Cluster Portfolio

• External intelligence (technology, market needs) is critical• Choice under uncertainty

Assessment criteria• Existing bridgeheads, market opportunity, leadership

Metal-working

Food Proces

sing

Lighting

IT & AnalyticalInstrumen

tsComm-unication

sEquip. & Services

Down-stream

ChemicalsBiopharm

a

Leather

Apparel

Printing

Services

Financial

Services

Insurance

Environ-

mental Service

s

Business

Services

Education &

Knowledge

Creation

Marketing

Services

Music &

SoundRecord

ing

PerformingArts

VideoProduc

tion

Hospitality&

Tourism

Metal Mining

CoalMining

UpstreamMetals

Wood Produc

ts

Furniture

Tobacco

Aerospace

UpstreamChemical

s

Trailers & Appliance

s

Textiles

Footwear

Forestry

Agriculture

PlasticsPlasticsDistribution&

eComm.

LivestockProcessin

g

Fishing &Fishing

Products

Water Transport

Transport &Logistic

s

Vulcanized

Materials

Construction

NonmetalMining

Oil & Gas

Electricity

Down-streamMetals

Production

Metal-working

Automotive

Paper &

Packaging

Recreation

& Electric Goods

Jewelry & Precious Metals

Strong clusters above 90th percentile specialization

Other specialized clusters

Strong clusters above 75th percentiles specialization

Cluster Specialization

Medical

Devices

32 Copyright 2015 © Christian Ketels

Current Status of Cluster Policies and Programs

• Many countries and regions, especially within the OECD, have cluster-related policy programs

• Spending on cluster-related programs is meaningful, but only a modest percentage of total spending per policy area

• Funding is tilted towards existing strengths, but many efforts exist without established critical mass

• Cluster programs are often run by a range of ministries or agencies; there is limited coordination between programs

• Funding for strengthening collaboration is always a part; other elements differ significantly

• Design principles differ widely across many dimensions

20150204 – MOC 2015 – Session 2 Copyright 2015 © Christian Ketels33

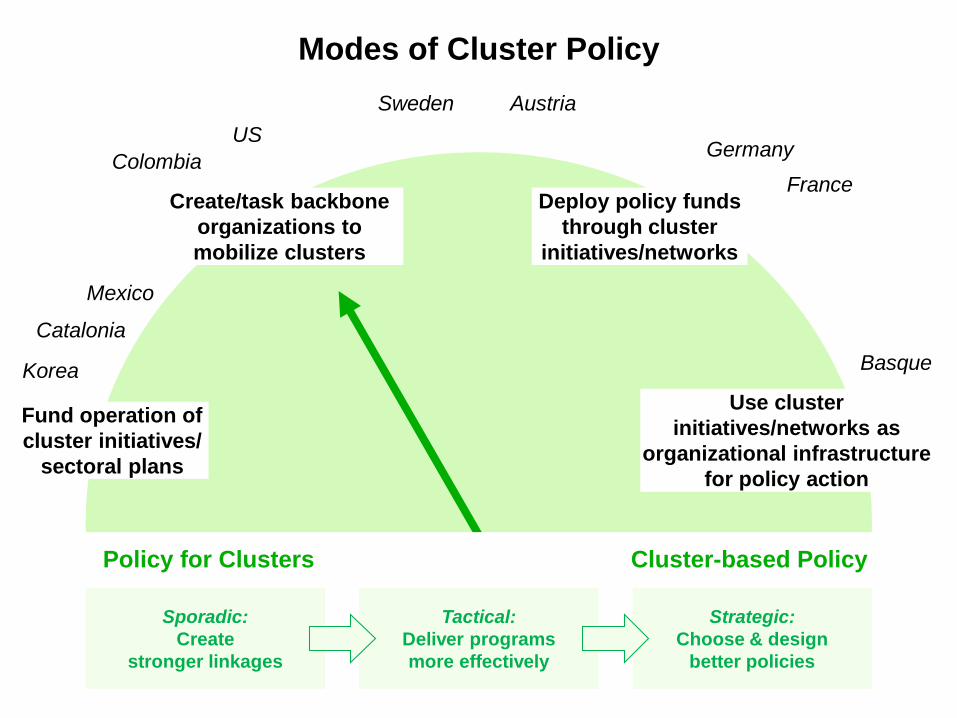

Modes of Cluster Policy

Fund operation of cluster initiatives/

sectoral plans

Create/task backbone organizations to mobilize clusters

Deploy policy funds through cluster

initiatives/networks

Use cluster initiatives/networks as

organizational infrastructure for policy action

Policy for Clusters Cluster-based Policy

Basque

GermanyFrance

SwedenUS

Catalonia

Korea

Austria

Mexico

Colombia

Sporadic: Create

stronger linkages

Tactical: Deliver programs more effectively

Strategic: Choose & design

better policies

34 Copyright 2016 © Christian Ketels

Resources &Capabilities

• Quality of staff• Budget and tools• Governance

Narrow model• Focus on networking• Limited resources• Limited impact

Systemic model• Cluster initiatives as

key channel for delivering policy action

• Moderate operational resources, strong influence on other investment streams

• High impact possible

What Drives the Success of Cluster Initiatives?

Context

Activities

• Cluster strength• Business

environment conditions

• Firm sophistication• Collaboration

culture, trust

IMPACT

• Activities aligned with the needs of firms• Activities aligned with actions of partners• Effectiveness of implementation

35 Copyright 2014 © Christian Ketels

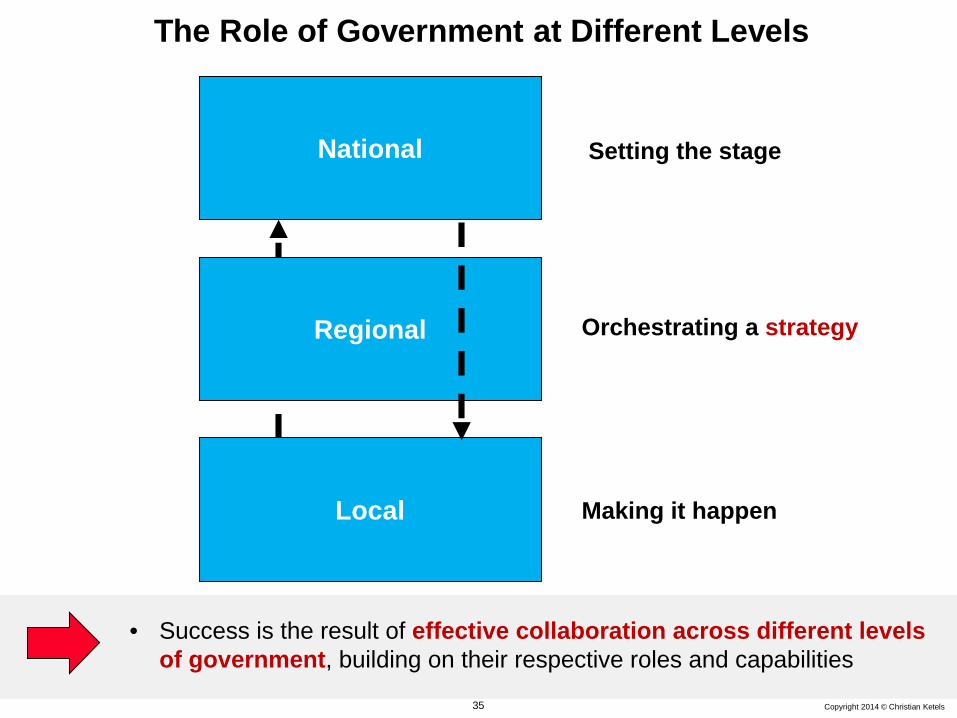

The Role of Government at Different Levels

National

Regional

Local Making it happen

Orchestrating a strategy

Setting the stage

• Success is the result of effective collaboration across different levels of government, building on their respective roles and capabilities

36 Copyright 2013 © Christian Ketels

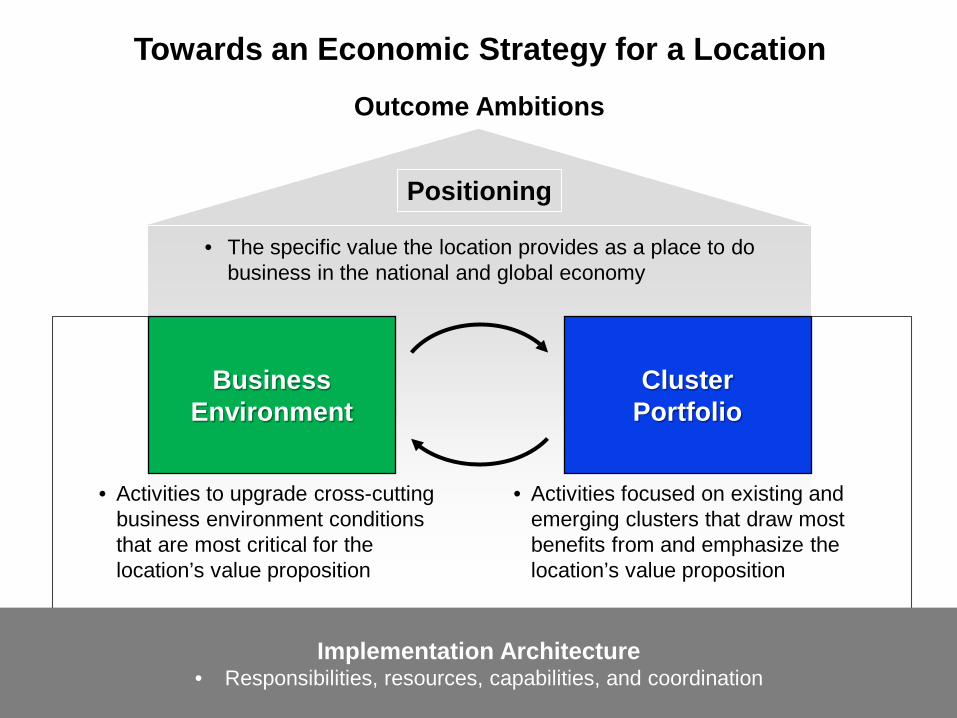

Towards an Economic Strategy for a Location

BusinessEnvironment

ClusterPortfolio

Positioning

• The specific value the location provides as a place to do business in the national and global economy

• Activities focused on existing and emerging clusters that draw most benefits from and emphasize the location’s value proposition

• Activities to upgrade cross-cutting business environment conditions that are most critical for the location’s value proposition

Outcome Ambitions

Implementation Architecture• Responsibilities, resources, capabilities, and coordination

37 Copyright 2013 © Christian Ketels

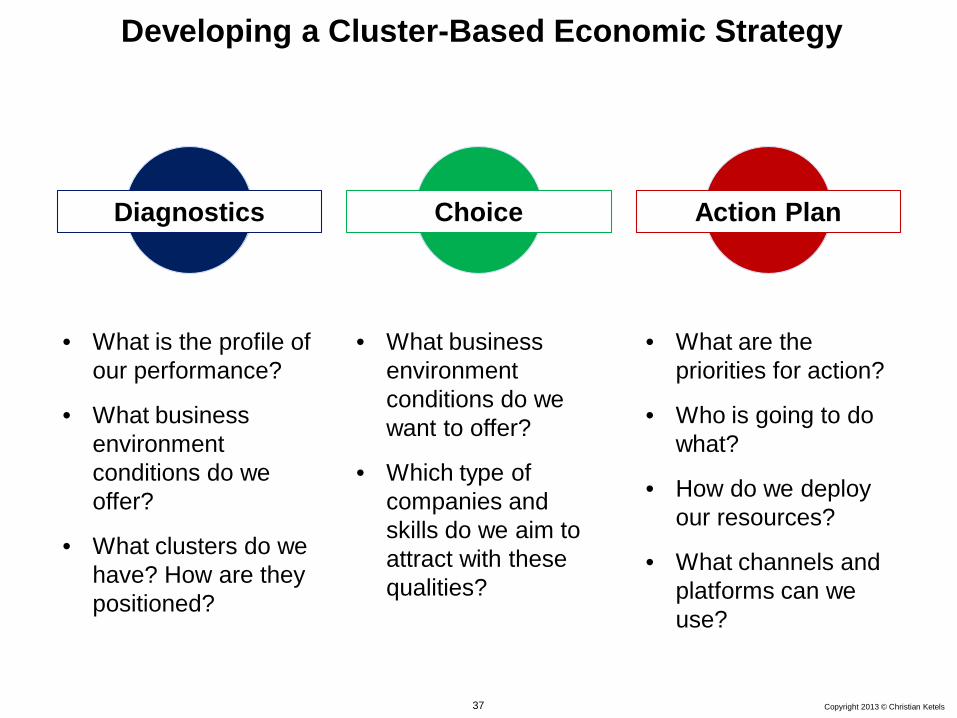

Developing a Cluster-Based Economic Strategy

Diagnostics Choice Action Plan

• What is the profile of our performance?

• What business environment conditions do we offer?

• What clusters do we have? How are they positioned?

• What business environment conditions do we want to offer?

• Which type of companies and skills do we aim to attract with these qualities?

• What are the priorities for action?

• Who is going to do what?

• How do we deploy our resources?

• What channels and platforms can we use?

38 Copyright 2013 © Christian Ketels

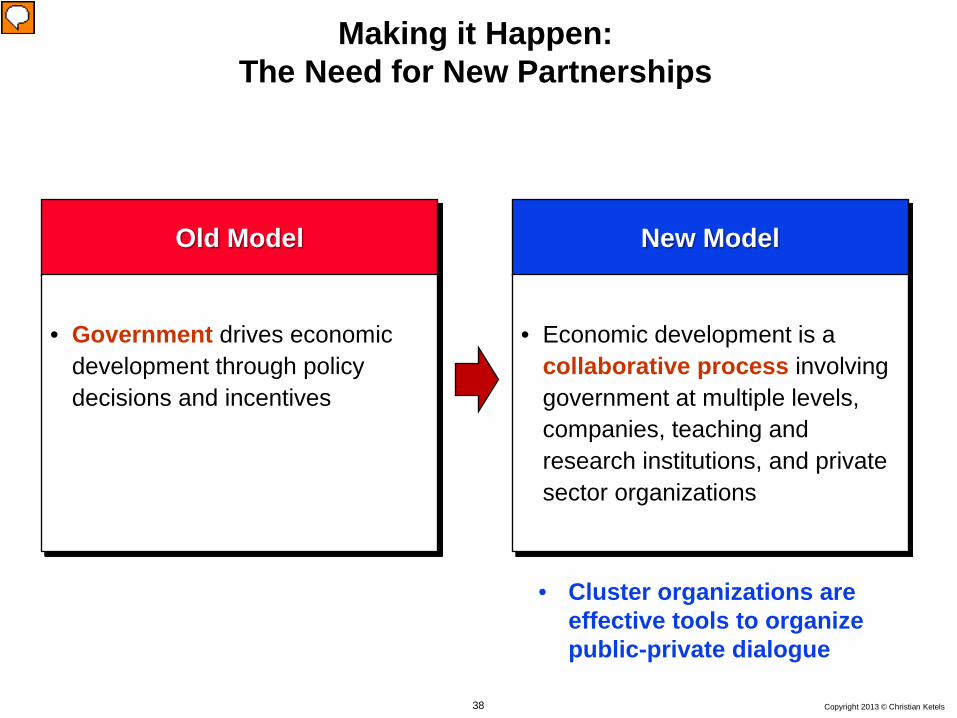

Making it Happen:The Need for New Partnerships

Old Model

• Government drives economic development through policy decisions and incentives

New Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and private sector organizations

• Cluster organizations are effective tools to organize public-private dialogue

39 Copyright 2013 © Christian Ketels

Implications for Australia

• Australia has a strong economy, rooted in robust underlying competitiveness

• The combination of strong demand for Australian natural resources and a policy focus on cross-cutting framework conditions, especially the openness of markets, has left the country with few competitive advantages and clusters outside a narrow range of areas

• The country would benefit from shifting towards the exploration and systematic development of positions in a broader range of fields

• A cluster-based approach is a powerful way for Australia to identify and implement such a strategy, based on a new model of public-private collaboration