Taxlab 2017 Four Faces of Tax - Deloitte · 2020-02-11 · Taxlab 2017 Four Faces of Tax March 2017...

14

Taxlab 2017 Four Faces of Tax March 2017 Maarten de Haas and Martin Krivinskas Taxlab 2017 Four Faces of Tax Value Chain Analysis

Transcript of Taxlab 2017 Four Faces of Tax - Deloitte · 2020-02-11 · Taxlab 2017 Four Faces of Tax March 2017...

Taxlab 2017

Four Faces of TaxMarch 2017

Maarten de Haas and Martin Krivinskas

Taxlab 2017

Four Faces of Tax

Value Chain Analysis

Agenda

• Why a value chain analysis?

• What is a value chain analysis?

• Changes in transfer pricing world

• Value chain defined

• Global Tax Reset impact on value chains

• Value chain analysis as part of transfer pricing documentation

• Process for analysis

• Value Chain Analytics Tool

Today’s transfer pricing environment requires an understanding of your value chain

One of the objectives of the OECD’s Base Erosion and Profit Shifting (BEPS) project is to develop transfer pricing guidelines that align transfer pricing outcomes with value creation.

This requirement increases the need for multinational companies to holistically review how profits and functions are mapped to the organisation’s overall value chain.

A value chain analysis creates a context for the pricing of transactions between entities by assessing the relative

contributions made by each entity to the overall business.

What is a Value Chain Analysis?

Why is it helpful?

BEPS Actions 8 – 10 require the consideration of the overall value chain to contextualise the transfer price of transactions.

A value chain analysis separates a business into a series of value generating functions.

To assess a value chain, productspass through each level of value chain functions and at each level gain some value.

The revised interpretation of the arm’s length principle requires a

more granular analysis of the functions, assets and risks controlled

by a business.

A value chain analysis can provide a foundation from which to identify the

functions, assets and risks, helping to understand activities that create

value.

Once the activities that create value are identified, the relative

contribution of each entity/country to these value creating activities can

be further analysed.

What is a Value Chain Analysis and why is it helpful?

Assets

Risks

People functions

10

The New transfer pricing…

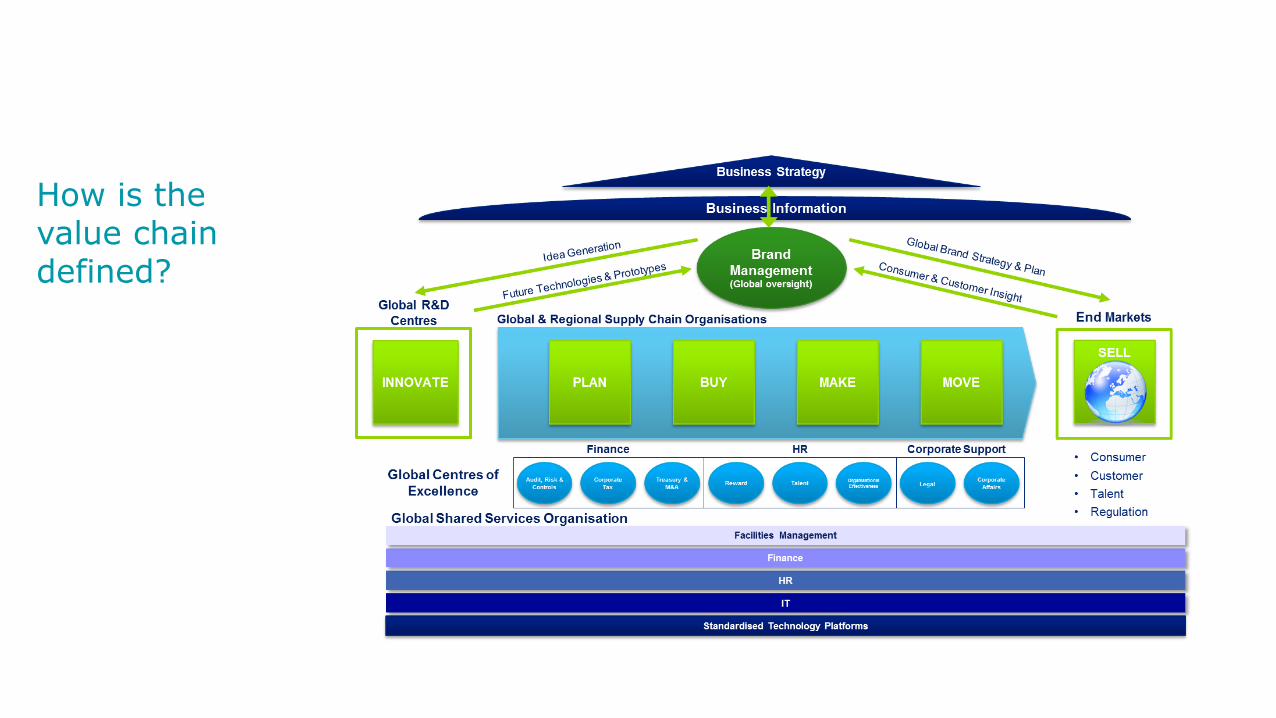

How is the value chain defined?

Senior management /

strategyProduction/

Content/Manufacturing

Intra-group services

Intellectual Property

(IP)

Procurement

Sales and Marketing

12

Business profits – global value chain

Value chain

People

Control and financial

capacity to assume

risk

Road map

Value chain analysis

Determine where business profits sit

Key people locations

Current transfer pricing outcome

Gap and opportunity analysis

Reset

13

Assessing the impact of GTR on the value chain

Example - Part of TP documentation process

Identification of Value Drivers

Key elements of the business that generate value and whose features, activities, strategies etc. provide a competitive advantage.

Identification of Value Chain

End to end value chain for the business.

Functional analysis

Detailed analysis of the functions performed, risks managed and assets owned for each element of the value chains where performed (e.g. R&D, Manufacturing, Sales and Marketing etc.).

The detailed functional analysis identifies the concentration of activity, management of risk and ownership of assets around the group.

Value Driver mapping

Mapping of identified key value drivers across the detailed value chain functional analysis toreconcile where value is created, focusing on:• nature and location of

key value generating activities,

• management of risks, and• ownership of assets

Selection of TP

method

Value Chain Analysis

/ Functional Analysis

Proposed business

model/ transactions

CUP

(where comparables with similar ‘local value’)

TNMM(no local material value

drivers)

Profit Split

(central / local both

contribute material value

drivers)

Document, embed,

manage

Deloitte’s value chain analysis provides the foundation for the transfer pricing work that is needed to comply with the evolving transfer pricing compliance landscape.

9

1

4

• Division/supply chain/operational structure – will vary by business?

• Which geographies?

• Who are the key stakeholders (typically generates C-Suite level interest)?

• Relevant profit/loss account?

• SWOT

• Will not only identify risk

• Stakeholder management

• Prioritise

• Previous analysis undertaken/ planning

• Possible areas of weakness re operation and BEPS

• Hypothesise value drivers

Define

Gather

3

• Allocate margin to simpler functions in post BEPS world

• What reward should be where?

• Comparison to expectation

Analyze

2

Document5

Understand

Analyze

Define area of review

Understand expected

result

Information gathering

Document

• What is actually happening, and where?

• Who sets strategy?

• Legal vs economic - owners of IP, contractual terms?

• Understand key functions, assets and risks

• Interview key stakeholders – where is the value generated? Why is money made?

• Key people functions - location and costs

• DEMPE re intangibles

Value chain analysis process

Value chain analytics

Taxlab 2017Four Faces of Tax

Value Chain analysis

• Operating profits by country/function

• Employee organisation chart by country/ function/grade level

Required Data• Profit & Loss by country/function/legal entity

• Balance sheet by country/function/legal entity

• Country-by-country reporting data

Additional Data

• Understanding of the Profits Drivers

• Understanding of the Industry

• Understanding of the Financials

• Understanding of the Executives’ Functions/Roles

• Deliverable summarising workshop results

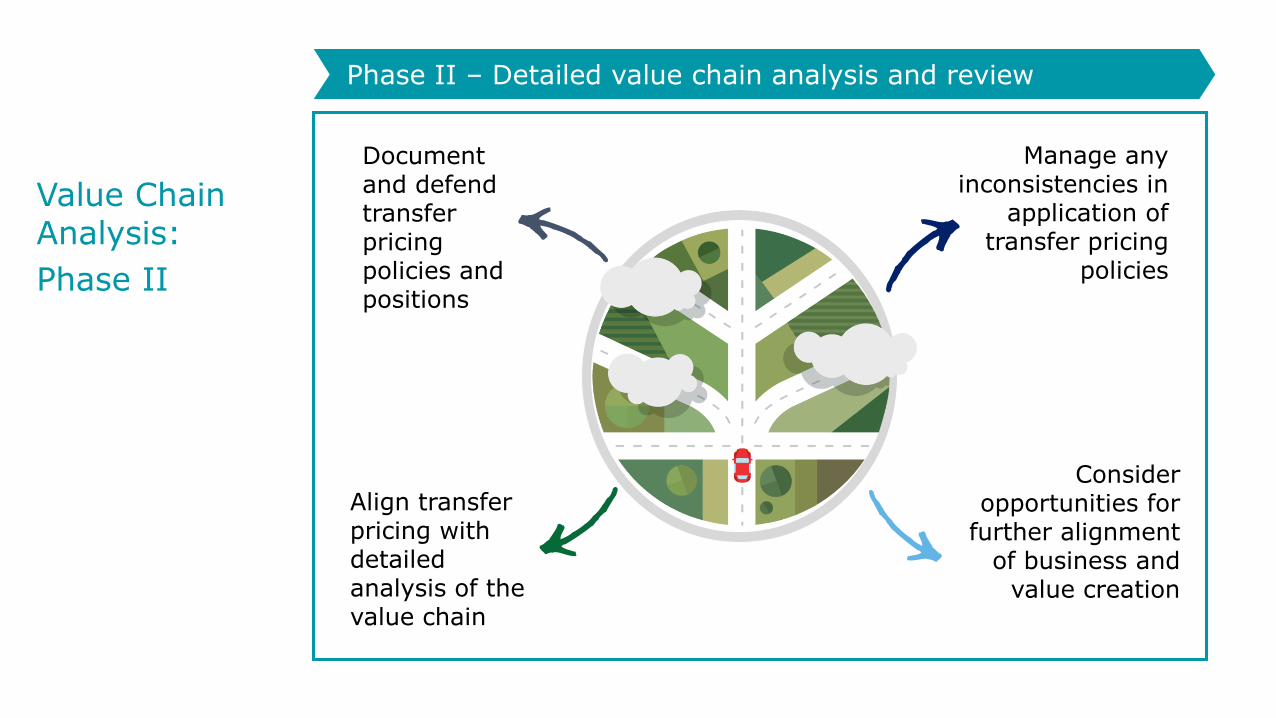

Value Chain Analysis:

Phase I

Document and defend transfer pricing policies and positions

Align transfer pricing with detailed analysis of the value chain

Manage any inconsistencies in

application of transfer pricing

policies

Consider opportunities for

further alignment of business and

value creation

Value Chain Analysis:

Phase II

Phase II – Detailed value chain analysis and review

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firmsare legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its memberfirms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500®companies through a globally connected network of member firms in more than 150 countries bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges.To learn more about how Deloitte’s approximately 225,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of thiscommunication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entityin the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2017 Deloitte The Netherlands