Taxing Times - Budget 2008 - December...

15

TaxingTimes December 2007 Budget 2008 & Current Tax Developments

Transcript of Taxing Times - Budget 2008 - December...

TaxingTimesDecember 2007

Budget 2008 & Current Tax Developments

KPMG is Ireland’s leading Tax practice withover 500 tax professionals based in Dublin,Belfast, Cork and Galway. Our clients rangefrom dynamic and fast growing familybusinesses to individuals, partnerships andpublicly quoted companies.

KPMG tax professionals have an unrivalledunderstanding of business and industry issues,adding real value to tax based decision making.

KPMG's Tax services include:

� Corporate Tax

� Private Client Services

� International Executive Services

� VAT

� International and Cross Border Tax

For further information on Budget 2008 log ontokpmg.ie/budget2008

Introduction

Budget 2008

Personal TaxCredits Raised 2

Business Tax Matters –Minister Makes FewChanges 4

Minister CutsStamp Duty 5

New VAT System ForCommercial Property 6

Minister Improves R&DIncentive 8

CO2 and VRT 9

Financial Services,Farming and Fishing 10

Tax rates andcredits 2008 11

Personal Tax Scenarios 12

Mike FarrellHead of Tax and Legal Services

This was the first unified BudgetStatement that announced all newspending and income raising measurestogether. This is a positive developmentwhich allows greater transparency inviewing the planned income andexpenditure for the year ahead.

The minister adopted a prudentapproach in forming his BudgetStatement. His decision to run abudget deficit and to continue to rollout the National Development Planshould position Ireland well forcompetitive advantage in the comingyears. The deficit will be funded byborrowings, thereby allowing theminister not to increase taxes.

The minister’s proposals in socialwelfare will be welcomed as will theincome tax changes which are aimedprimarily at those on lower incomes.

The changes in the stamp duty areawill also be welcomed. Together withchanges in mortgage interest relief,these should put some life back intothe residential property market.However, the top 9% stamp duty rateremains too high by internationalstandards. The commercial propertysector will be disappointed that theminister did not take the opportunity toreduce that rate with a view tostimulating activity in that sector.

The minister’s decision to bringforward the new rules for VAT onproperty transactions with effect from1 July 2008 is significant. This followsan extensive consultation processduring which several anomalies thatwere identified in the original proposalshave been corrected.

Reflecting the composition of thegovernment, the Budget Statementincludes a considerable number ofmeasures that are aimed at improvingthe environment.

Business will be largely unaffected bythis Budget Statement. No changeshave been introduced that would resultin increased employment costs andthis is welcomed.

This Budget edition of Taxing Timesprovides a summary of the keychanges announced today in all areas,including personal and business taxes,property and indirect taxes. Thesubstantive changes that will giveeffect to the Budget Statement will becontained in Finance Bill 2008. This isdue for publication in early February.

This publication seeks only tosummarise the minister’s Budgetmeasures. Your KPMG tax contact isbest placed to discuss with you theimpact of these changes on yourbusiness and personal affairs.

Minister Brian Cowen delivered his fourth Budget Statementtoday – the first Budget Statement of the new government.He did so at a time of change in the economy and against abackground of a recent slowdown in tax revenues.

Mike FarrellPartner

TaxingTimes Budget 2008 1

TaxingTimes Budget 2008 2

The Standard Rate Bands have beenwidened from:

� €34,000 to €35,400 for single people

� €43,000 to €44,400 for marriedcouples with one income

� €68,000 to €70,800 for marriedcouples with two incomes.

The single person’s tax credit hasincreased by €70 to €1,830, while themarried couple’s credit has increasedby €140 to €3,660. The EmployeeTax Credit is now €1,830, an increaseof €70.

There are have also been increases incertain tax credits for widowed

persons, widowed parents for the firstfive years after bereavement, the blindperson’s allowances, the incapacitatedchild credit (which has been increasedto €3,660) and the age credit (up to€325 for a single person and €650 fora married couple). The Home CarerCredit has been raised by €130 to€900.

The Age Exemption Limits have beenraised, rising by €1,000 (to €20,000)for a single person and by €2,000 (to€40,000) for a married couple.

The credit for rent paid by certaintenants will increase for 2008. Forthose aged under 55, it is beingincreased from €360 to €400 per

annum for a single person and from€720 to €800 per annum for widowedand married persons. For those agedover 55, the credit rises to €800 perannum for a single person and €1,600for a widowed or married person.

The standard-rate tax allowance fortrade union subscriptions paid bymembers is to be increased from €300to €350 per annum. This equates to atax credit of €70 per annum.

In addition to the stamp duty changes,the minister raised the ceiling formortgage interest relief for first timebuyers from €8,000 to €10,000 forsingle people and from €16,000 to€20,000 for married couples. The

Personal Tax Credits RaisedThe minister has widened the Standard Rate Bands andraised tax credits.

Robert DowleyPartner

TaxingTimes Budget 2008 3

additional relief will be available for thefirst seven years for which there is anentitlement to mortgage interest relief.

PRSI and health levychangesThe PRSI ceiling for employees risesfrom €48,800 to €50,700. The PRSIthreshold will also increase from €339to €352 per week.

The Health Levy thresholds for theindividual rises from €480 to €500 perweek and from €24,960 to €26,000per annum.

Preferential loansThe specified interest rate on preferentialloans from an employer to an employeehas increased from 4.5% to 5.5% inrespect of home loans, and from 12% to13% in respect of other loans.

Rent-a-Room limit raisedThis relief provides an exemption fromincome tax where people rent out a

room or rooms in their principal privateresidence. The limit of the exemptionrises from €7,620 to €10,000.

Remittance basis extendedto UK incomeThe remittance basis of taxation (whichapplies to individuals who are notdomiciled in Ireland or who are Irishresidents but not ordinarily resident)did not extend previously to incomearising from UK sources. With effectfrom 1 January 2008, this taxtreatment will extend to investmentincome and foreign employmentincome which has its source in the UK.This amendment follows queries fromthe EU Commission on whether theexclusion of UK source income fromthe remittance of tax wasdiscriminatory.

The remittance basis also extends tocapital gains tax in the case ofnon–domiciled individuals. In suchcases, the legislation provides that the

remittance basis does not apply to UKsource gains. Interestingly, themeasures published do not removethis tax on gains (unlike incomeabove), and it remains to be seenwhether this will also be amended inthe Finance Bill.

Capital gains tax on sitetransferThere is currently an exemption fromcapital gains tax on the transfer of asite from a parent to a child, wherethat site is transferred for the purposesof constructing the child’s principalprivate residence.

In conjunction with the changesannounced on stamp duty, theexemption limit on the value of the sitehas been increased from €254,000 to€500,000. The change will take effectin respect of disposals made on orafter Budget Day.

TaxingTimes Budget 2008 4

Preliminary tax thresholdraisedSmall companies can pay preliminarytax at 90% of their expected final taxliability or 100% of the previous year’stax liability. Last year, this thresholdwas increased to €150,000. This yearthe minister further increased thethreshold to €200,000.

The threshold for startup companieswas also increased, to €200,000.Start-ups will not be required to paypreliminary tax in respect of their firstaccounting period where their taxliability is expected to be less than thisamount.

Both changes are effective in relationto preliminary tax payment datesarising after 5 December 2007.

While these changes are welcome,large businesses will be disappointedthat the minister did not extend theprior-year option to them.

VAT alterationsFrom 1 May 2008 the VAT registrationthresholds will be increased to€37,500 for services and €75,000 forgoods.

The minister announced proposals tointroduce a "reverse-charge" for VATon supplies made by a subcontractorto a principal contractor in theconstruction sector, from 1September 2008. The measure isbeing introduced to protect Revenueagainst subcontractors charging VATon invoices and failing to pay over theVAT.

Capital allowances andexpenses for business cars

In line with the minister’s “green”agenda, he has essentially reduced theavailability of capital allowances and

tax deductions for leasing expenses onbusiness cars which emit more than155g/km of CO2. These changes willbecome effective from 1 July 2008.

Where cars have CO2 emission levelsof less than 155 g/km, capitalallowances can be claimed on thelower of cost or €24,000. Capitalallowances are available on €12,000(or 50% of the cost of the car if lower)where CO2 emission levels arebetween 156 and 190 g/km. There areno capital allowances available on carswith CO2 emission levels of over191g/km.

Under the existing scheme, leasingcharges were restricted proportionately

for cars costing in excess of €24,000.From 1 July 2008, the leasing chargesfor cars with CO2 emission levels ofless than 155 g/km will continue to berestricted by reference to €24,000. Forcars emitting between 156 and 190

g/km of CO2, only 50% of the actualor restricted leasing charges will bedeductible. No tax deduction will beavailable for cars with CO2 emissionlevels of over 191g/km.

Section 481 film reliefThe minister confirmed that he wasextending the film relief on the currentbasis until 2012. He has commissioneda report to review the relief and anychanges arising from this study will beannounced in the Finance Bill.

Unfortunately, this extension to therelief is unlikely to have the desiredeffect of re-energising the film industryin Ireland, given the package ofincentives on offer in the UK.

Business Tax Matters –Minister Makes Few ChangesRelatively few corporate tax changes were announced in thisyear’s budget. Anna Scally

Partner

CO2 emission levels

< 155 g/km 156 – 190 g/km >191 g/km

Capital allowances €24,000(or cost if lower)

€12,000(or 50% of costif lower)

Nil

Deductible leasing charges no restriction forcars costing lessthan €24,000orrestriction byreference to€24,000

50% of leasecharges wherecar costs lessthan €24,000or50% of restrictedlease charges

Nil

TaxingTimes Budget 2008 5

Suggestions ranged from theintroduction of a six-year exemption forfirst-time buyers to a reduction in thetop rate of stamp duty from 9% to5%. Until the minister delivered hisbudget speech, it appeared as if thesesubmissions were falling on deaf ears.

System simplified to tworatesThe minister announced theintroduction of a simplified system,incorporating an exemption of€125,000 with two progressive ratesinstead of the existing six-rate bandsfor residential property. The changeswill apply both to owner occupiers andinvestors in residential property. Thiswelcome reform is directed towardsimproving the efficiency of the housingmarket and boosting overall economicactivity.

Residential property transactions whichdo not exceed the €125,000exemption level will not attract stampduty. For amounts not exceeding €1million, stamp duty at a rate of 7% willbe chargeable on the excess over€125,000. Where the transactionexceeds €1 million, the first €125,000will be exempt, the next €875,000 willattract stamp duty at a rate of 7% andthe amount in excess of €1 million willattract stamp duty at a rate of 9%.

In addition, residential properties witha value in excess of €125,000 but notexceeding €127,000 will not be liablefor stamp duty.

For example, an investor purchasing ahouse for €850,000 will pay stamp dutyof €50,750, just over €25,750 less thanunder the old regime, a 34% saving.

ExemptionsThe stamp duty exemptions currentlyavailable to first-time purchasers andpurchasers of new homes willcontinue to apply. First-time owner-occupying purchasers of residentialproperty and other owner-occupyingpurchasers of new residential propertywith a floor area of under 125m² areexempt from stamp duty. Otherowner-occupying purchasers of newresidential property with a floor area ofover 125m² incur stamp duty on thegreater of the site value or 25% of theproperty value (excluding VAT).

These changes will apply toinstruments which are required to bepresented to the RevenueCommissioners for stamping no laterthan 5 December 2007. Accordingly,instruments which were executed inthe 30-day period prior to 5 December2007 should benefit from this change.

Claw-back of stamp dutyreliefAs outlined above, an exemption fromstamp duty is generally available forfirst-time owner-occupying purchasersof residential property and otherowner-occupying purchasers of newresidential property with a floor area ofunder 125m². In addition, partial reliefis available to owner-occupyingpurchasers of new residential propertywith a floor area of over 125m².Currently, these exemptions/reliefs area clawback where the purchaser rentsout the residential property, other thanunder rent-a-room arrangement, withinfive years of the date of the deed oftransfer relating to the purchase.

The minister has decided to recognisethe need to relax the clawbackprovisions to better reflect theincreased career and residentialmobility of house buyers and the needto provide them with greater flexibilityand certainty in their choices.

He announced a reduction in the claw-back period for all three reliefs fromfive years to two years for deeds oftransfer executed on, or after, 5December 2007. For deeds of transferexecuted before 5 December 2007, tothe extent that residential property isrented out on, or after, 5 December2007, a clawback of relief will not arisewhere the letting occurs in the third,fourth or fifth year of ownership.

Transfer of a site to a childThe exemption threshold applicable tothe conveyance, transfer or lease of a siteby a parent to a child for the purposes ofconstructing the child’s principal privateresidence has been increased.

With effect from 5 December 2007,the exemption will apply to sites with amarket value not exceeding €500,000(previously €254,000).

Similar changes have been made tothe equivalent capital gains taxexemption.

Minister Cuts Stamp DutyFollowing a deceleration of the residential property market inrecent months, the minister was inundated with pre-budgetsubmissions urging stamp duty reform to help re-ignite themarket.

Colm RogersPartner

TaxingTimes Budget 2008 6

The implementation date for the newrules will be 1 July 2008. This will bethe most significant change to IrishVAT law on property since itsintroduction in 1972. The new systemaffects the VAT treatment of allcommercial property transactions.

Why is the system beingchanged?The Revenue Commissioners carriedout a review of the existing systemand published their report in December2006. The existing system, they said,was too complex and not secure froman Exchequer perspective.

Three key featuresBroadly speaking, the VAT treatment ofresidential property will remain thesame. The main changes relate tocommercial property and there arethree key elements.

� First, the VAT treatment of the saleof property will no longer bedetermined by reference to whetherthe property has been developedsince 1972. Under the newsystem, VAT will apply to the sale of“new” properties.

"New" will mean the first sale of aproperty within five years ofcompletion, or any further salewithin five years of completionwhere the building has beenoccupied for less than two years.The sale of old properties (i.e. thosethat are not “new” under thedefinition), will be exempt from VAT,with an option to apply VAT to thesale. The option will be exercisablejointly by the vendor and purchaser,and VAT will be chargeable at13.5% on the sales price (this is achange from the original proposals).

New VAT System forCommercial PropertyThe minister announced that the Finance Bill 2008 willintroduce a completely new system of VAT on property.This follows a public consultation process.

John McGlonePartner

Terry O’NeillPartner

TaxingTimes Budget 2008 7

� Secondly, the current VAT treatmentof long leases will be abolished.Under the new system, all leases(with the exception of very longleases akin to a freehold) will betreated as exempt from VAT unlessthe landlord elects to charge VAT onthe lease rents at 21%. An electionwill not be possible where thelandlord and tenant are connectedparties. This is a worrying aspect ofthe proposals given the level ofsubletting between members of agroup which can arise in everydaysituations.

Although the budget announcementwas not clear on the point, it appearsthat the election will be property-specific. There will be provisions toallow for cancellation of the electionbut the proposals indicate that therewill be potential consequences wherea cancellation occurs within 20 yearsof the commencement of the lease.The original proposal - to allow anelection only where the tenant hasgreater than 90% VAT recovery - hasbeen dropped.

� The third key feature of the newsystem is a “Capitals GoodsScheme”. This is likely to be acomplex mechanism for adjustingthe initial VAT deduction arising on aproperty transaction. Depending onthe use to which the property is putover the 20 years from acquisition,a party acquiring or developing aproperty may be required to adjustthe initial deduction claimed.

Worrying clawbackThe budget announcement containedan overview of transitional measuresbut more detail will be needed toproperly assess their impact. Oneworrying retrospective measureenvisages a clawback of VAT deductedin the last 20 years under the existingrules, where the use of the propertyhas changed since then.

Many issues remainIn May 2007, in its response to thepublic consultation process, KPMGoutlined significant concerns aboutaspects of the proposals. Theseincluded concerns relating to thetransitional regime, the potentialcomplexity of the new system and themarket impact of the proposedlargescale changes. In addition togeneral concerns, KPMG also raised anumber of specific points in respect ofthe draft legislation.

Whilst the budget proposals addresssome of these concerns, many issuesremain. It is not yet clear whether theRevenue’s ambition of simplifying thesystem of VAT on property will beachieved.

Other measuresFrom 1 May 2008 the VAT registrationthresholds will be increased to€37,500 for services and €75,000 forgoods.

The minister announced proposals tointroduce a "reverse-charge" for VAT onsupplies made by a subcontractor to aprincipal contractor in the constructionsector, from 1 September 2008. Themeasure is being introduced to protect

Revenue against subcontractorscharging VAT on invoices and failing topay over the VAT to Revenue.

TaxingTimes Budget 2008 8

Given the current economic climateand the Government’s efforts topromote Ireland as a knowledgeeconomy, it is reassuring that theminister is listening to the needs ofindustry.

Further freezing of baseyearLast year’s budget saw the rollingthree-year base year “frozen” at 2003for relevant periods commencingbefore 1 January 2010. This year theminister went further and announcedthat the base year which is used tocalculate incremental qualifyingexpenditure is being fixed for a furtherfour years, to 2013. This improvementreflects the reality of the average lifecycle of R&D activities carried out bycompanies in Ireland. The longer theperiod between the base year and the

relevant period, the more likely it isthat a company will have incrementalexpenditure in excess of that expectedfrom inflation alone.

This improvement is welcome. TheIrish R&D tax credit needs to be keptunder regular review, particularly inlight of competing jurisdictions’ recentenhancements of their R&Dinvestment incentives.

The fixing of the base year at 2003 isalso good news for start upcompanies, or multinational companieswhich did not have a presence inIreland in 2003 - all their expenditurecould be incremental.

It will be necessary to inform theEuropean Commission about thesechanges from a State Aid perspective.

Minister ImprovesR&D IncentiveThis was the minister’s fourth budget, and the fourth timehe will amend the R&D tax credit regime he introduced inhis first budget in 2004.

Ken HardyPartner

TaxingTimes Budget 2008 9

Recycling BESHe will amend the Business ExpansionScheme (BES) so that recyclingcompanies can have easier access toBES financing. As the BES is anapproved State aid, it is necessary toadvise the European Commission ofthe proposed change.

Electricity taxUnder the EU Energy Tax Directive allmember states are required tointroduce an excise tax on electricity.From 1 October 2008, the rates will be50 cent per megawatt hour for businessuse and €1 per megawatt hour for non-business use. However, electricity usedby households will be exempt from thenew charge as will electricity producedfrom renewables and combined heatand power generation.

The introduction of a carbon tax,expected to be on a revenue-neutralbasis, will be part of the terms ofreference of the forthcomingCommission on Taxation.

Cutting CO2

There are changes to the capitalallowances and leasing expensededuction for motor cars and to theVRT regime, both aimed at supportingreduced CO2 emission levels. Tocomplement the changes in the VRTsystem, the government also intendsto bring forward proposals that will linkmotor tax to CO2 emissions for newcars from 1 July 2008.

‘Greener vehicles’This year’s “green budget” takesanother step towards addressingIreland’s commitment to the Kyoto

protocol under which we must reduceemissions over the next few years to13% of 1990 levels.

To reflect the necessity to reduce ourlevel of carbon emissions the budgetaims to incentivise us to purchase anduse “greener ” low-emission vehiclesand alternative fuel sources. Oneaspect of the Government’s strategy isto make those choosing higher-emissionvehicles pay more by increasing the VRTchargeable on these vehicles.Conversely, those using “greener”,lower carbon-emitting vehicles will berewarded with lower rates of VRT.

The basis for calculating VRT will shiftfrom a system based on enginecapacity to one based on the level ofcarbon dioxide emissions produced bythe vehicle. The changes will not beretrospective, and will come into forcefrom 1 July 2008 generally. The Julycommencement date should allow carimporters to adjust their purchaseorders to reflect a perceived decreasein future sales of higher carbon-emitting vehicles.

Current systemUnder the current system, the enginesize of vehicles dictates the rate atwhich VRT is paid – currently cars withan engine size of 1,400cc or lowerattract a 22.5% rate, those between1,401cc and 1,900cc a 25% rate, andvehicles above 1,901cc attract a 30%rate. These rates are applied to theopen market selling price of the vehicle

Proposed systemUnder the minister’s proposals, newbands of VRT rates ranging from 14%to 36% will apply to new vehicles from

1 July 2008. The VRT to be chargedwill depend on the amount of CO2emitted per kilometre. For example, acar emitting up to 120g will have VRTcharged at 14%, those emitting up to140g will have VRT charged at 16%anda top rate of 36% will apply to carsemitting more than 226g per ilometre.

The result of these proposed changeswill probably be twofold - we will seethe price of some lower-emissionvehicles fall (e.g. diesel-poweredvehicles), while some larger petrolmodels will rise in price.

Free trade issuesAs the law is not retrospective,vehicles that are purchased abroad,and brought into Ireland, will be liableto the new VRT system whenenacted, whereas secondhand carspurchased in Ireland will not.

VRT tax take may fall

Last year’s revenue from VRT was ofthe order of €1.3 billion. If theGovernment succeeds in reducingcarbon emissions from vehicles byrewarding people who buy greenercars, the tax take from VRT will, bynecessity, fall.

So, if this tax succeeds in changing carbuyer’s preferences, and given thecurrent economic climate in which theExchequer tax returns are falling, howdoes the Government plan to make upa shortfall, should it arise? Theproposed changes could make VRT aself-defeating tax.

CO2 and VRTThe minister announced a number of initiatives to encouragebehaviour that would reduce greenhouse gas emissions. Hedescribed the initiatives as forward-looking and pro-active. Shaun Murphy

PartnerKen HardyPartner

Electronic payment boostTo support the trend away from apaper-based payment system, theminister has substantially reduced thestamp duty on the variouscash/debit/credit cards.

The stamp duty on credit cards will bereduced by 25% while the stamp dutyon all other cards will be reduced by50%. The reduction in this penal dutywill be welcomed by consumers.

The cost of this measure will in part befinanced by a doubling of the stampduty on cheques and other bills ofexchange. If this latter measuresucceeds in reducing cheque usage itshould be welcomed by banks, giventhe high cost of administering thispaper-based system.

Card stamp dutyIn a now familiar manoeuvre toproduce a once-off current year cash-flow benefit to the Exchequer, theminister has accelerated the paymentdates of stamp duty on credit and cashcards for banks.

In December 2008 and in subsequentyears banks will be obliged to make a

payment on account of this duty forthe current year based on 80% of theactual payment for the previous year.This change should have no impact forcustomers of the banks.

Farm partnershipsThe dissolution of a farm partnershipcan give rise to deemed disposals ofchargeable assets for capital gains taxpurposes. Liability to capital gains taxcould arise, for example, in respect offarm land which was a partnershipasset owned by all the partners prior tothe dissolution but is taken by one ofthe partners on the dissolution of thepartnership.

The minister stated that he intends tointroduce a new relief from capitalgains tax to cover exposures to capitalgains tax arising on the dissolution offarm partnerships. The relief will runfor a period of five years.

Sugar beet growersFinance Act 2007 introduced arelieving provision for payments madeto farmers in respect of restructuringaid under the EU Sugar BeetCompensation Package. In broadterms, the relief provides for thetaxation of the payments to be spreadover six years.

The minister stated that a similarrelieving provision will be introduced inrespect of payments under thediversification aid element of the EUCompensation Package.

Milk partnershipsProvisions will be included in theFinance Bill to remove the clawback ofincome tax that would occur for

farmers who have opted to avail of thespecial income tax averagingarrangements and subsequently enterinto a milk production partnership.

VAT – flat rate farmers

The farmers’ flat rate addition is beingretained at 5.2% for 2008.

Farm consolidationIn Finance Act 2007, the ministerintroduced a new stamp duty relief forfarmers consolidating their holdings.The relief applied on land exchangesbetween two farmers consolidatingtheir holdings and to each farmerwhere only one farmer is consolidatinghis holding. The relief was to beimplemented by ministerial order. Theminister, having obtained thenecessary EU State Aid approval, hasnow signed the order to commencethe relief.

Vessel decommissioningThe minister has announced proposalsto help the restructuring of the fishingindustry. Provision will be made in theFinance Bill to amend the tax code toassist the take-up of decommissioningpayments to be made under theFishing Vessel DecommissioningScheme.

Paul McGowanPartner

TaxingTimes Budget 2008 10

Financial Services,Farming and Fishing

Pat McDaidPartner

Description Current New

Charge cards & credit cardaccounts

€40 €30

ATM cards €10 €5

Debit cards €10 €5

Combined ATM/Debit cards €20 €10

Cheques/Bills of Exchange €0.15 €0.30

TaxingTimes Budget 2008 11

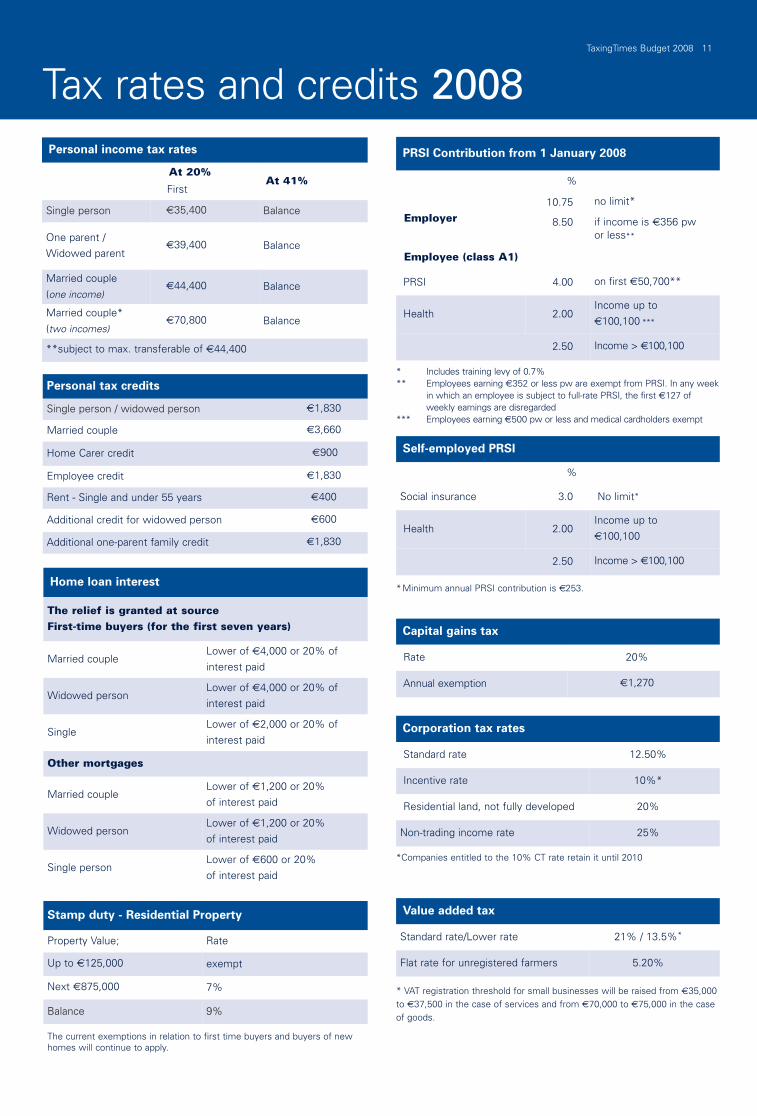

Tax rates and credits 2008Personal income tax rates

At 20%

FirstAt 41%

Single person €35,400 Balance

One parent /Widowed parent

€39,400 Balance

Married couple(one income)

€44,400 Balance

Married couple*(two incomes)

€70,800 Balance

**subject to max. transferable of €44,400

Personal tax credits

Single person / widowed person €1,830

Married couple €3,660

Home Carer credit €900

Employee credit €1,830

Rent - Single and under 55 years €400

Additional credit for widowed person €600

Additional one-parent family credit €1,830

Home loan interest

The relief is granted at sourceFirst-time buyers (for the first seven years)

Married coupleLower of €4,000 or 20% ofinterest paid

Widowed personLower of €4,000 or 20% ofinterest paid

SingleLower of €2,000 or 20% ofinterest paid

Other mortgages

Married coupleLower of €1,200 or 20%of interest paid

Widowed personLower of €1,200 or 20%of interest paid

Single personLower of €600 or 20%of interest paid

Stamp duty - Residential Property

Property Value; Rate

Up to €125,000 exempt

Next €875,000 7%

Balance 9%

The current exemptions in relation to first time buyers and buyers of newhomes will continue to apply.

PRSI Contribution from 1 January 2008

%

Employer10.75

8.50

no limit*

if income is €356 pwor less**

Employee (class A1)

PRSI 4.00 on first €50,700**

Health 2.00Income up to€100,100 ***

2.50 Income > €100,100

* Includes training levy of 0.7%** Employees earning €352 or less pw are exempt from PRSI. In any week

in which an employee is subject to full-rate PRSI, the first €127 ofweekly earnings are disregarded

*** Employees earning €500 pw or less and medical cardholders exempt

*Minimum annual PRSI contribution is €253.

*Companies entitled to the 10% CT rate retain it until 2010

Self-employed PRSI

%

Social insurance 3.0 No limit*

Health 2.00Income up to€100,100

2.50 Income > €100,100

Capital gains tax

Rate 20%

Annual exemption €1,270

Corporation tax rates

Standard rate 12.50%

Incentive rate 10%*

Residential land, not fully developed 20%

Non-trading income rate 25%

Value added tax

Standard rate/Lower rate 21% / 13.5%*

Flat rate for unregistered farmers 5.20%

* VAT registration threshold for small businesses will be raised from €35,000to €37,500 in the case of services and from €70,000 to €75,000 in the caseof goods.

Personal Tax Scenarios

TaxingTimes Budget 2008 12

kpmg.ie/budget2008

1 Stokes PlaceSt. Stephen’s GreenDublin 2Telephone +353 1 410 1000Fax +353 1 412 1122

1 Harbourmaster PlaceIFSCDublin 1Telephone +353 1 410 1000Fax +353 1 412 1122

90 South MallCorkTelephone +353 21 425 4500Fax +353 21 425 4525

Odeon HouseEyre SquareGalwayTelephone +353 91 534600Fax +353 91 565567

Stokes House17 - 25 College Sq. EastBelfast BT1 6DHTelephone +44 28 9024 3377Fax +44 28 9089 3893

The information contained herein is of a general nature and is not intended to addressthe circumstances of any particular individual or entity. Although we endeavour toprovide accurate and timely information, there can be no guarantee that suchinformation is accurate as of the date it is received or that it will continue to beaccurate in the future. No one should act on such information without appropriateprofessional advice after a thorough examination of the particular situation.

If you've received this publication directly from KPMG, it is because we hold yourname and company details for the purpose of keeping you informed on a range ofbusiness issues and the services we provide. If you would like us to delete thisinformation from our records and would prefer not to receive any further updatesfrom us please contact us at (01) 700 4017.

© 2007 KPMG, an Irish partnership and a member firm of the KPMG network ofindependent member firms affiliated with KPMG International, a Swiss cooperative.All rights reserved. Printed in Ireland.

KPMG and the KPMG logo are registered trademarks of KPMG International,a Swiss cooperative.

Produced by: KPMG’s Marketing Department.

Publication Date: December 2007.