taxation law

62

MANILA INTERNATIONAL AIRPORT AUTHORITY, petitioner, vs. CITY OF PASAY, SANGGUNIANG PANGLUNGSOD NG PASAY, CITY MAYOR OF PASAY, CITY TREASURER OF PASAY, and CITY ASSESSOR OF PASAY, respondents. D E C I S I O N CARPIO, J p: This is a petition for review on certiorari 1 of the Decision 2 dated 30 October 2002 and the Resolution dated 19 March 2004 of the Court of Appeals in CA-G.R. SP No. 67416. The Facts Petitioner Manila International Airport Authority (MIAA) operates and administers the Ninoy Aquino International Airport (NAIA) Complex under Executive Order No. 903 (EO 903), 3 otherwise known as the Revised Charter of the Manila International Airport Authority. EO 903 was issued on 21 July 1983 by then President Ferdinand E. Marcos. Under Sections 3 4 and 22 5 of EO 903, approximately 600 hectares of land, including the runways, the airport tower, and other airport buildings, were transferred to MIAA. The NAIA Complex is located along the border between Pasay City and Parañaque City. On 28 August 2001, MIAA received Final Notices of Real Property Tax Delinquency from the City of Pasay for the taxable years 1992 to 2001. MIAA's real property tax delinquency for its real properties located in NAIA Complex, Ninoy Aquino Avenue, Pasay City (NAIA Pasay properties) is tabulated as follows: EIcSDC

-

Upload

chuchay-hilado -

Category

Documents

-

view

213 -

download

0

description

cabanking

Transcript of taxation law

MANILA INTERNATIONAL AIRPORT AUTHORITY, petitioner, vs.

CITY OF PASAY, SANGGUNIANG PANGLUNGSOD NG PASAY, CITY

MAYOR OF PASAY, CITY TREASURER OF PASAY, and CITY

ASSESSOR OF PASAY, respondents.

D E C I S I O N

CARPIO, J p:

This is a petition for review on certiorari 1 of the Decision 2 dated 30 October 2002 and the

Resolution dated 19 March 2004 of the Court of Appeals in CA-G.R. SP No. 67416.

The Facts

Petitioner Manila International Airport Authority (MIAA) operates and administers the Ninoy

Aquino International Airport (NAIA) Complex under Executive Order No. 903 (EO

903), 3 otherwise known as the Revised Charter of the Manila International Airport

Authority. EO 903 was issued on 21 July 1983 by then President Ferdinand E. Marcos. Under

Sections 3 4 and 22 5 of EO 903, approximately 600 hectares of land, including the runways, the

airport tower, and other airport buildings, were transferred to MIAA. The NAIA Complex is

located along the border between Pasay City and Parañaque City.

On 28 August 2001, MIAA received Final Notices of Real Property Tax Delinquency from the

City of Pasay for the taxable years 1992 to 2001. MIAA's real property tax delinquency for its

real properties located in NAIA Complex, Ninoy Aquino Avenue, Pasay City (NAIA Pasay

properties) is tabulated as follows: EIcSDC

TAX TAXABLE TAX DUE PENALTY TOTAL

DECLARATION YEAR

A7-183-08346 1997-2001 243,522,855.00 123,351,728.18 366,874,583.18

A7-183-05224 1992-2001 113,582,466.00 71,159,414.98 184,741,880.98

A7-191-00843 1992-2001 54,454,800.00 34,115,932.20 88,570,732.20

A7-191-00140 1992-2001 1,632,960.00 1,023,049.44 2,656,009.44

A7-191-00139 1992-2001 6,068,448.00 3,801,882.85 9,870,330.85

A7-183-05409 1992-2001 59,129,520.00 37,044,644.28 96,174,164.28

A7-183-05410 1992-2001 20,619,720.00 12,918,254.58 33,537,974.58

A7-183-05413 1992-2001 7,908,240.00 4,954,512.36 12,862,752.36

A7-183-05412 1992-2001 18,441,981.20 11,553,901.13 29,995,882.33

A7-183-05411 1992-2001 109,946,736.00 68,881,630.13 178,828,366.13

A7-183-05245 1992-2001 7,440,000.00 4,661,160.00 12,101,160.00

——————— ——————— ———————

GRAND TOTAL P642,747,726.20 P373,466,110.13 P1,016,213,836.33

============= ============ =============

On 24 August 2001, the City of Pasay, through its City Treasurer, issued notices of levy and

warrants of levy for the NAIA Pasay properties. MIAA received the notices and warrants of levy

on 28 August 2001. Thereafter, the City Mayor of Pasay threatened to sell at public auction the

NAIA Pasay properties if the delinquent real property taxes remain unpaid.

On 29 October 2001, MIAA filed with the Court of Appeals a petition for prohibition and

injunction with prayer for preliminary injunction or temporary restraining order. The petition

sought to enjoin the City of Pasay from imposing real property taxes on, levying against, and

auctioning for public sale the NAIA Pasay properties.

On 30 October 2002, the Court of Appeals dismissed the petition and upheld the power of the

City of Pasay to impose and collect realty taxes on the NAIA Pasay properties. MIAA filed a

motion for reconsideration, which the Court of Appeals denied. Hence, this petition.

The Court of Appeals' Ruling

The Court of Appeals held that Sections 193 and 234 of Republic Act No. 7160 or the Local

Government Code, which took effect on 1 January 1992, withdrew the exemption from payment

of real property taxes granted to natural or juridical persons, including government-owned or

controlled corporations, except local water districts, cooperatives duly registered under Republic

Act No. 6938, non-stock and non-profit hospitals and educational institutions. Since MIAA is a

government-owned corporation, it follows that its tax exemption under Section 21 of EO 903 has

been withdrawn upon the effectivity of the Local Government Code.

The Issue

The issue raised in this petition is whether the NAIA Pasay properties of MIAA are exempt from

real property tax.

The Court's Ruling

The petition is meritorious.

In ruling that MIAA is not exempt from paying real property tax, the Court of Appeals cited

Sections 193 and 234 of the Local Government Code which read:

SEC. 193. Withdrawal of Tax Exemption Privileges. — Unless otherwise

provided in this Code, tax exemptions or incentives granted to, or presently

enjoyed by all persons, whether natural or juridical, including government-

owned or controlled corporations, except local water districts, cooperatives duly

registered under R.A. No. 6938, non-stock and non-profit hospitals and

educational institutions, are hereby withdrawn upon the effectivity of this Code.

SEC. 234. Exemptions from Real Property Tax. — The following are exempted

from payment of the real property tax:

(a) Real property owned by the Republic of the Philippines or any of its political

subdivisions except when the beneficial use thereof has been granted, for

consideration or otherwise to a taxable person;

(b) Charitable institutions, churches, parsonages or convents appurtenant

thereto, mosques, non-profit or religious cemeteries and all lands, buildings and

improvements actually, directly, and exclusively used for religious, charitable or

educational purposes;

(c) All machineries and equipment that are actually, directly and exclusively

used by local water districts and government owned or controlled corporations

engaged in the supply and distribution of water and/or generation and

transmission of electric power;

(d) All real property owned by duly registered cooperatives as provided for

under R.A. No. 6938; and

(e) Machinery and equipment used for pollution control and environment

protection.

Except as provided herein, any exemption from payment of real property tax

previously granted to, or presently enjoyed by, all persons, whether natural or

juridical, including all government-owned or controlled corporations are hereby

withdrawn upon the effectivity of this Code.

The Court of Appeals held that as a government-owned corporation, MIAA's tax exemption

under Section 21 of EO 903 has already been withdrawn upon the effectivity of theLocal

Government Code in 1992.

In Manila International Airport Authority v. Court of Appeals 6 (2006 MIAA case), this Court

already resolved the issue of whether the airport lands and buildings of MIAA are exempt from

tax under existing laws. The 2006 MIAA case originated from a petition for prohibition and

injunction which MIAA filed with the Court of Appeals, seeking to restrain the City of

Parañaque from imposing real property tax on, levying against, and auctioning for public sale the

airport lands and buildings located in Parañaque City. The only difference between the 2006

MIAA case and this case is that the 2006 MIAA case involved airport lands and buildings

located in Parañaque City while this case involved airport lands and buildings located in Pasay

City. The 2006 MIAA case and this case raised the same threshold issue: whether the local

government can impose real property tax on the airport lands, consisting mostly of the runways,

as well as the airport buildings, of MIAA. In the 2006 MIAA case, this Court held:

To summarize, MIAA is not a government-owned or controlled corporation

under Section 2 (13) of the Introductory Provisions of the Administrative Code

because it is not organized as a stock or non-stock corporation. Neither is MIAA

a government-owned or controlled corporation under Section 16, Article XII of

the 1987 Constitution because MIAA is not required to meet the test of

economic viability. MIAA is a government instrumentality vested with

corporate powers and performing essential public services pursuant to Section

2(10) of the Introductory Provisions of the Administrative Code. As a

government instrumentality, MIAA is not subject to any kind of tax by local

governments under Section 133(o) of the Local Government Code. The

exception to the exemption in Section 234(a) does not apply to MIAA because

MIAA is not a taxable entity under theLocal Government Code. Such exception

applies only if the beneficial use of real property owned by the Republic is

given to a taxable entity.

Finally, the Airport Lands and Buildings of MIAA are properties devoted to

public use and thus are properties of public dominion. Properties of public

dominion are owned by the State or the Republic. Article 420 of the Civil Code

provides: TSEHcA

Art. 420. The following things are property of public dominion:

(1) Those intended for public use, such as roads, canals, rivers,

torrents, ports and bridges constructed by the State, banks, shores,

roadsteads, and others of similar character;

(2) Those which belong to the State, without being for public use, and

are intended for some public service or for the development of the

national wealth.

The term "ports . . . constructed by the State" includes airports and seaports.

The Airport Lands and Buildings of MIAA are intended for public use, and at

the very least intended for public service. Whether intended for public use or

public service, the Airport Lands and Buildings are properties of public

dominion. As properties of public dominion, the Airport Lands and Buildings

are owned by the Republic and thus exempt from real estate tax under Section

234(a) of the Local Government Code. 7 (Emphasis in the original)

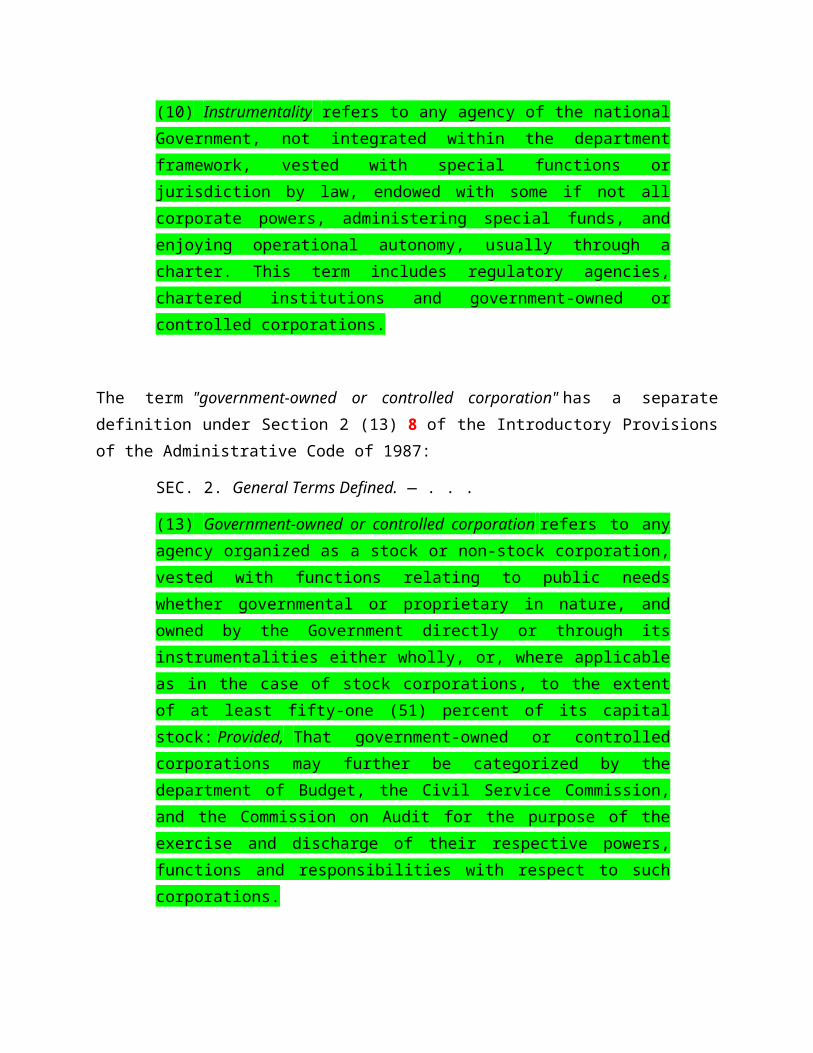

The definition of "instrumentality" under Section 2(10) of the Introductory Provisions of the

Administrative Code of 1987 uses the phrase "includes . . . government-owned or controlled

corporations" which means that a government "instrumentality" may or may not be a

"government-owned or controlled corporation". Obviously, the term government

"instrumentality" is broader than the term "government-owned or controlled corporation".

Section 2 (10) provides:

SEC. 2. General Terms Defined. — . . .

(10) Instrumentality refers to any agency of the national Government, not

integrated within the department framework, vested with special functions or

jurisdiction by law, endowed with some if not all corporate powers,

administering special funds, and enjoying operational autonomy, usually

through a charter. This term includes regulatory agencies, chartered institutions

and government-owned or controlled corporations.

The term "government-owned or controlled corporation" has a separate definition under Section

2 (13) 8 of the Introductory Provisions of the Administrative Code of 1987:

SEC. 2. General Terms Defined. — . . .

(13) Government-owned or controlled corporation refers to any agency

organized as a stock or non-stock corporation, vested with functions relating to

public needs whether governmental or proprietary in nature, and owned by the

Government directly or through its instrumentalities either wholly, or, where

applicable as in the case of stock corporations, to the extent of at least fifty-one

(51) percent of its capital stock: Provided, That government-owned or

controlled corporations may further be categorized by the department of Budget,

the Civil Service Commission, and the Commission on Audit for the purpose of

the exercise and discharge of their respective powers, functions and

responsibilities with respect to such corporations.

The fact that two terms have separate definitions means that while a government

"instrumentality" may include a "government-owned or controlled corporation", there may be

a government "instrumentality" that will not qualify as a "government-owned or controlled

corporation".

A close scrutiny of the definition of "government-owned or controlled corporation" in Section 2

(13) will show that MIAA would not fall under such definition. MIAA is a government

"instrumentality" that does not qualify as a "government-owned or controlled

corporation". As explained in the 2006 MIAA case:

A government-owned or controlled corporation must be "organized as a stock or

non-stock corporation". MIAA is not organized as a stock or non-stock

corporation. MIAA is not a stock corporation because it has no capital stock

divided into shares. MIAA has no stockholders or voting shares. . . .

Section 3 of the Corporation Code defines a stock corporation as one

whose "capital stock is divided into shares and . . . authorized to distribute to

the holders of such shares dividends . . . ." MIAA has capital but it is not

divided into shares of stock. MIAA has no stockholders or voting shares. Hence,

MIAA is not a stock corporation.

xxx xxx xxx

MIAA is also not a non-stock corporation because it has no members. Section

87 of the Corporation Code defines a non-stock corporation as "one where no

part of its income is distributable as dividends to its members, trustees or

officers". A non-stock corporation must have members. Even if we assume that

the Government is considered as the sole member of MIAA, this will not make

MIAA a non-stock corporation. Non-stock corporations cannot distribute any

part of their income to their members. Section 11 of the MIAA Charter

mandates MIAA to remit 20% of its annual gross operating income to the

National Treasury. This prevents MIAA from qualifying as a non-stock

corporation.

Section 88 of the Corporation Code provides that non-stock corporations are

"organized for charitable, religious, educational, professional, cultural,

recreational, fraternal, literary, scientific, social, civil service, or similar

purposes, like trade, industry, agriculture and like chambers". MIAA is not

organized for any of these purposes. MIAA, a public utility, is organized to

operate an international and domestic airport for public use.

Since MIAA is neither a stock nor a non-stock corporation, MIAA does not

qualify as a government-owned or controlled corporation. What then is the legal

status of MIAA within the National Government?

MIAA is a government instrumentality vested with corporate powers to

perform efficiently its governmental functions. MIAA is like any other

government instrumentality, the only difference is that MIAA is vested

with corporate powers. . . .

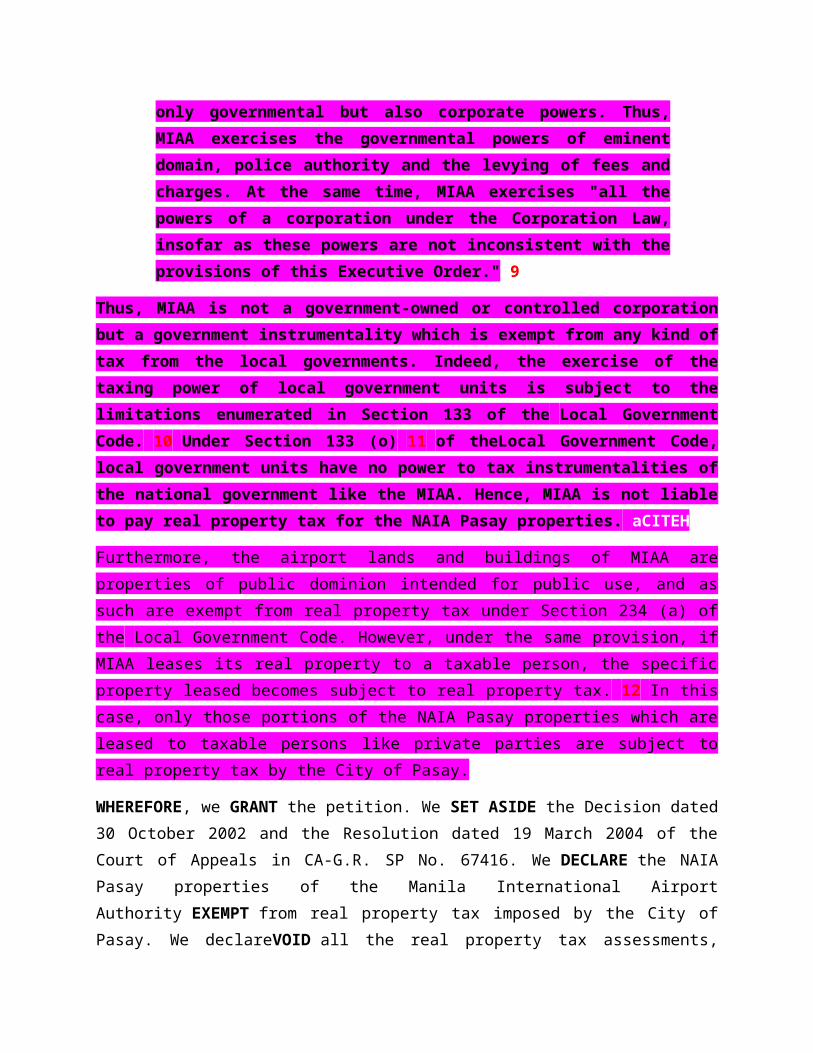

When the law vests in a government instrumentality corporate powers, the

instrumentality does not become a corporation. Unless the government

instrumentality is organized as a stock or non-stock corporation, it remains

a government instrumentality exercising not only governmental but also

corporate powers. Thus, MIAA exercises the governmental powers of

eminent domain, police authority and the levying of fees and charges. At

the same time, MIAA exercises "all the powers of a corporation under the

Corporation Law, insofar as these powers are not inconsistent with the

provisions of this Executive Order." 9

Thus, MIAA is not a government-owned or controlled corporation but a government

instrumentality which is exempt from any kind of tax from the local governments. Indeed,

the exercise of the taxing power of local government units is subject to the limitations

enumerated in Section 133 of the Local Government Code. 10 Under Section 133 (o) 11 of

theLocal Government Code, local government units have no power to tax instrumentalities

of the national government like the MIAA. Hence, MIAA is not liable to pay real property

tax for the NAIA Pasay properties. aCITEH

Furthermore, the airport lands and buildings of MIAA are properties of public dominion intended

for public use, and as such are exempt from real property tax under Section 234 (a) of the Local

Government Code. However, under the same provision, if MIAA leases its real property to a

taxable person, the specific property leased becomes subject to real property tax. 12 In this case,

only those portions of the NAIA Pasay properties which are leased to taxable persons like private

parties are subject to real property tax by the City of Pasay.

WHEREFORE, we GRANT the petition. We SET ASIDE the Decision dated 30 October 2002

and the Resolution dated 19 March 2004 of the Court of Appeals in CA-G.R. SP No. 67416.

We DECLARE the NAIA Pasay properties of the Manila International Airport

Authority EXEMPT from real property tax imposed by the City of Pasay. We declareVOID all

the real property tax assessments, including the final notices of real property tax delinquencies,

issued by the City of Pasay on the NAIA Pasay properties of the Manila International Airport

Authority, except for the portions that the Manila International Airport Authority has leased to

private parties.

No costs.

SO ORDERED.

MACTAN CEBU INTERNATIONAL AIRPORT

AUTHORITY, petitioner, vs. HON. FERDINAND J. MARCOS, in his

capacity as the Presiding Judge of the Regional Trial Court, Branch 20,

Cebu City, THE CITY OF CEBU, represented by its Mayor, HON.

TOMAS R. OSMEÑA, and EUSTAQUIO B. CESA,respondents.

The Solicitor General for petitioner.

The Office of the City Attorney for City of Cebu.

SYLLABUS

1. POLITICAL LAW; GOVERNMENT; POWER OF TAXATION; CONSTRUED. — As a

general rule, the power to tax is an incident of sovereignty and is unlimited in its range,

acknowledging in its very nature no limits, so that security against its abuse is to be found only

in the responsibility of the legislature which imposes the tax on the constituency who are to pay

it. Nevertheless, effective limitations thereon may be imposed by the people through

their Constitution. Our Constitution, for instance, provides that the rule of taxation shall be

uniform and equitable and Congress shall evolve a progressive system of taxation. So potent

indeed is the power that it was once opined that "the power to tax involves the power to destroy."

Verily, taxation is a destructive power which interferes with the personal and property rights of

the people and takes from them a portion of their property for the support of the government.

Accordingly, tax statutes must be construed strictly against the government and liberally in favor

of the taxpayer. But since taxes are what we pay for civilized society, or are the lifeblood of the

nation, the law frowns against exemptions from taxation and statutes granting the exemptions are

thus construed strictissimi juris against the taxpayer and liberally in favor of the taxing authority.

A claim of exemption from tax payments must be clearly shown and based on language in the

law too plain to be mistaken. Elsewise stated, taxation is the rule, exemption therefrom is the

exception. However, if the grantee of the exemption is a political subdivision or instrumentality,

the rigid rule of construction does not apply because the practical effect of the exemption is

merely to reduce the amount of money that has to be handled by the government in the course of

its operation.

2. ID., ID.; ID.; MAYBE EXERCISED BY THE LOCAL LEGISLATIVE BODIES. — The

power to tax is primarily vested in the Congress; however, in our jurisdictions, it may be

exercised by local legislative bodies, no longer merely by virtue of a valid delegation as before,

but pursuant to direct authority conferred by Section 5, Article X of theConstitution. Under the

latter, the exercise of the power may be subject to such guidelines and limitations as the

Congress may provide which, however, must be consistent with the basic policy of local

autonomy. The LGC, enacted pursuant to Section 3, Article X of the Constitution, provides for

the exercise by local government units of their power to tax, the scope thereof or its limitations,

and the exemptions from taxation. Section 133 of the LGC prescribes the common limitations on

the taxing powers of local government units.

3. ID.; ID .; ID.; EXEMPTION FROM PAYMENT OF TAX MAYBE WITHDRAWN AT THE

PLEASURE OF THE TAXING AUTHORITY; EXCEPTION. — There can be no question that

under Section 14 of R.A. No. 6958 the petitioner is exempt from the payment of realty taxes

imposed by the National Government or any of its political subdivisions, agencies, and

instrumentalities. Nevertheless, since taxation is the rule and exemption therefrom the exception,

the exemption may thus be withdrawn at the pleasure of the taxing authority. The only exception

to this rule is where the exemption was granted to private parties based on material consideration

of a mutual nature, which then becomes contractual and is thus covered by the non-impairment

claim of the Constitution.

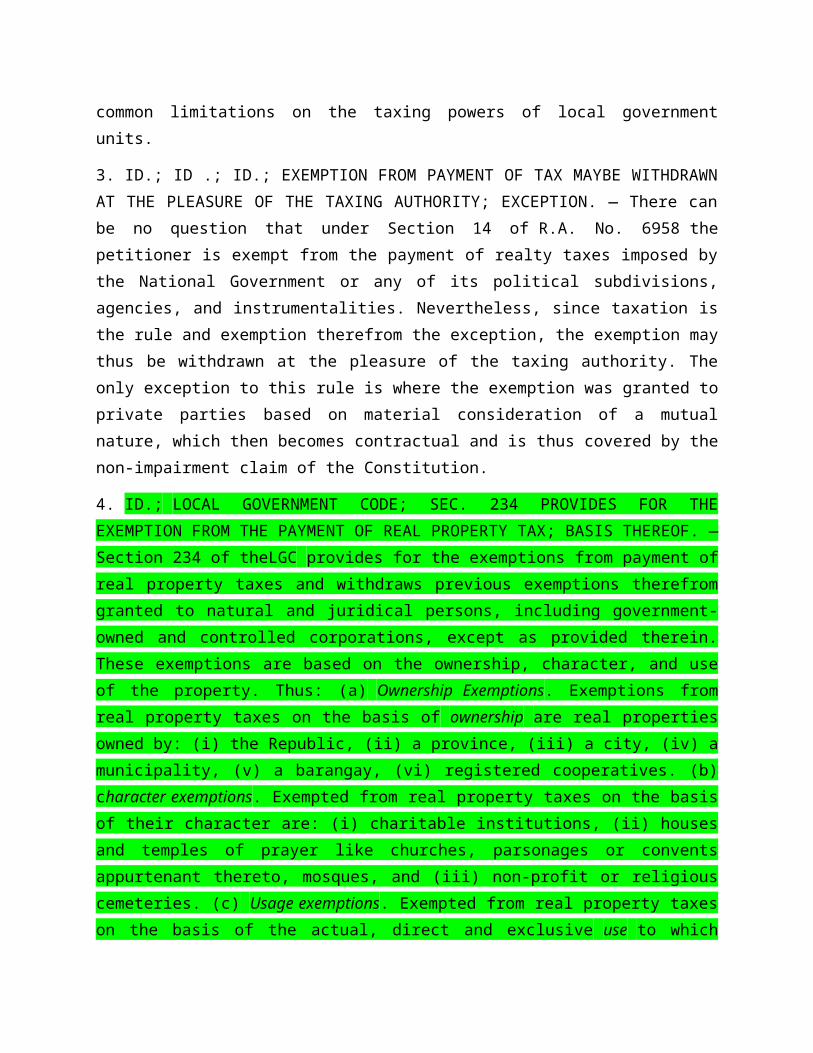

4. ID.; LOCAL GOVERNMENT CODE; SEC. 234 PROVIDES FOR THE EXEMPTION

FROM THE PAYMENT OF REAL PROPERTY TAX; BASIS THEREOF. — Section 234 of

theLGC provides for the exemptions from payment of real property taxes and withdraws

previous exemptions therefrom granted to natural and juridical persons, including government-

owned and controlled corporations, except as provided therein. These exemptions are based on

the ownership, character, and use of the property. Thus: (a) Ownership Exemptions. Exemptions

from real property taxes on the basis of ownership are real properties owned by: (i) the Republic,

(ii) a province, (iii) a city, (iv) a municipality, (v) a barangay, (vi) registered cooperatives. (b)

character exemptions. Exempted from real property taxes on the basis of their character are: (i)

charitable institutions, (ii) houses and temples of prayer like churches, parsonages or convents

appurtenant thereto, mosques, and (iii) non-profit or religious cemeteries. (c) Usage exemptions.

Exempted from real property taxes on the basis of the actual, direct and exclusive use to which

they are devoted are: (i) all lands, buildings and improvements which are actually, directly and

exclusively used for religious, charitable or educational purposes; (ii) all machineries and

equipment actually, directly and exclusively used by local water districts or by government-

owned or controlled corporations engaged in the supply and distribution of water and/or

generation and transmission of electric power; and (iii) all machinery and equipment used for

pollution control and environmental protection. To help provide a healthy environment in the

midst of the modernization of the country, all machinery and equipment for pollution control and

environmental protection may not be taxed by local governments. 2. Other Exemptions

Withdrawn. All other exemptions previously granted to natural or juridical persons including

government-owned or controlled corporations are withdrawn upon effectivity of the Code.

5. ID.; REPUBLIC OF THE PHILIPPINES AS DISTINGUISHED FROM NATIONAL

GOVERNMENT. — The terms "Republic of the Philippines" and "National Government" are

not interchangeable. The former is broader and synonymous with "Government of the Republic

of the Philippines" which the Administrative Code of 1987 defines as the "corporate

governmental entity through which the functions of government are exercised throughout the

Philippines, including, save as the contrary appears from the context, the various arms through

which political authority is made effective in the Philippines, whether pertaining to the

autonomous regions, the provincial, city, municipal or barangay subdivisions or other forms of

local government." (Section 2[1], Introductory Provisions, Administrative Code of 1987.) These

"autonomous regions, provincial, city, municipal or barangay subdivisions" are the political

subdivisions. (Section l, Article X, 1987 Constitution.) On the other hand, "National

Government" refers "to the entire machinery of the central government, as distinguished from the

different forms of local government." (Section 2[2], Introductory Provisions, Administrative

Code of 1987. The National Government then is composed of the three great departments: the

executive, the legislative and the judicial.

6. ID.; GOVERNMENT; AGENCY AS DISTINGUISHED FROM INSTRUMENTALITY. —

An "agency" of the Government refers to "any of the various units of the Government, including

a department, bureau, office, instrumentality, or government-owned or controlled corporation, or

a local government or a distinct unit therein," while an "instrumentality" refers to "any agency of

the National Government, not integrated within the department framework, vested with special

functions or jurisdiction by law, endowed with some if not all corporate powers, administering

special funds, and enjoying operational autonomy, usually, through a charter. This term includes

regulatory agencies, chartered institutions and government-owned and controlled corporations."

D E C I S I O N

DAVIDE, JR., J p:

For review under Rule 45 of the Rules of Court on a pure question of law are the decision of 22

March 1995 1 of the Regional Trial Court (RTC) of Cebu City, Branch 20, dismissing the

petition for declaratory relief in Civil Case No. CEB-16900, entitled "Mactan Cebu International

Airport Authority vs. City of Cebu," and its order of 4 May 1995 2 denying the motion to

reconsider the decision.

We resolved to give due course to this petition for it raises issues dwelling on the scope of the

taxing power of local government units and the limits of tax exemption privileges of

government-owned and controlled corporations.

The uncontradicted factual antecedents are summarized in the instant petition as follows:

Petitioner Mactan Cebu International Airport Authority (MCIAA) was created by virtue

of Republic Act No. 6958, mandated to "principally undertake the economical, efficient and

effective control, management and supervision of the Mactan International Airport in the

Province of Cebu and the Lahug Airport in Cebu City, . . . and such other airports as may be

established in the Province of Cebu . . ." (Sec. 3, RA 6958). It is also mandated to:

a) encourage, promote and develop international and domestic air traffic in the

Central Visayas and Mindanao regions as a means of making the regions

centers of international trade and tourism, and accelerating the

development of the means of transportation and communication in the

country; and,

b) upgrade the services and facilities of the airports and to formulate

internationally acceptable standards of airport accommodation and

service.

Since the time of its creation, petitioner MCIAA enjoyed the privilege of exemption from

payment of realty taxes in accordance with Section 14 of its Charter:

Sec. 14. Tax Exemptions. — The Authority shall be exempt from realty taxes

imposed by the National Government or any of its political subdivisions,

agencies and instrumentalities . . ..

On October 11, 1994, however, Mr. Eustaquio B. Cesa, Officer-in-Charge, Office of the

Treasurer of the City of Cebu, demanded payment for realty taxes on several parcels of land

belonging to the petitioner (Lot Nos. 913-G, 743, 88 SWO, 948-A, 989-A, 474, 109(931), I-M,

918, 919, 913-F, 941, 942, 947, 77 Psd., 746 and 991-A), located at Barrio Apas and Barrio

Kasambagan, Lahug, Cebu City, in the total amount of P2,229,078.79.

Petitioner objected to such demand for payment as baseless and unjustified, claiming in its favor

the aforecited Section 14 of RA 6958 which exempts it from payment of realty taxes. It was also

asserted that it is an instrumentality of the government performing governmental functions,

citing Section 133 of the Local Government Codeof 1991 which puts limitations on the taxing

powers of local government units:

Section 133. Common Limitations on the Taxing Powers of Local Government

Units. — Unless otherwise provided herein, the exercise of the taxing powers of

provinces, cities, municipalities, and barangays shall not extend to the levy of

the following:

a) . . .

xxx xxx xxx

o) Taxes, fees or charges of any kind on the National Government, its agencies

and instrumentalities, and local government units. (italics supplied)

Respondent City refused to cancel and set aside petitioner's realty tax account, insisting that the

MCIAA is a government-controlled corporation whose tax exemption privilege has been

withdrawn by virtue of Sections 193 and 234 of the Local Government Code that took effect on

January 1, 1992:

Section 193. Withdrawal of Tax Exemption Privilege. — Unless otherwise

provided in this Code, tax exemptions or incentives granted to, or presently

enjoyed by all persons whether natural or juridical, including government-

owned or controlled corporations, except local water districts, cooperatives

duly registered under RA No. 6938, non-stock and non-profit hospitals and

educational institutions, are hereby withdrawn upon the effectivity of this Code.

(italics supplied)

xxx xxx xxx

Section 234. Exemptions from Real Property Taxes. — . . .

(a) . . .

xxx xxx xxx

(e) . . .

Except as provided herein, any exemption from payment of real

property tax previously granted to, or presently enjoyed by all persons,

whether natural or juridical, including government-owned or controlled

corporations are hereby withdrawn upon the effectivity of this Code.

As the City of Cebu was about to issue a warrant of levy against the properties

of petitioner, the latter was compelled to pay its tax account "under protest" and

thereafter filed a Petition for Declaratory Relief with the Regional Trial Court of

Cebu, Branch 20, on December 29, 1994. MCIAA basically contended that the

taxing powers of local government units do not extend to the levy of taxes or

fees of any kind on an instrumentality of the national government. Petitioner

insisted that while it is indeed a government-owned corporation, it nonetheless

stands on the same footing as an agency or instrumentality of the national

government by the very nature of its powers and functions.

Respondent City, however, asserted that MCIAA is not an instrumentality of the

government but merely a government-owned corporation performing

proprietary functions. As such, all exemptions previously granted to it were

deemed withdrawn by operation of law, as provided under Sections 193 and 234

of the Local Government Code when it took effect on January 1, 1992. 3

The petition for declaratory relief was docketed as Civil Case No. CEB-16900.

In its decision of 22 March 1995, 4 the trial court dismissed the petition in light of its findings, to

wit:

A close reading of the New Local Government Code of 1991 or RA

7160 provides the express cancellation and withdrawal of exemption of taxes by

government-owned and controlled corporation per Sections after the effectivity

of said Code on January 1, 1992, to wit: [proceeds to quote Sections 193 and

234]

Petitioners claimed that its real properties assessed by respondent City

Government of Cebu are exempted from paying realty taxes in view of the

exemption granted under RA 6958 to pay the same (citing Section 14 of RA

6958).

However, RA 7160 expressly provides that "All general and special laws, acts,

city charters, decrees [sic], executive orders, proclamations and administrative

regulations, or part or parts thereof which are inconsistent with any of the

provisions of this Code are hereby repealed or modified accordingly." (/f/,

Section 534, RA 7160).

With that repealing clause in RA 7160, it is safe to infer and state that the tax

exemption provided for in RA 6958 creating petitioner had been expressly

repealed by the provisions of the New Local Government Code of 1991.

So that petitioner in this case has to pay the assessed realty tax of its properties

effective after January 1, 1992 until the present.

This Court's ruling finds expression to give impetus and meaning to the overall

objectives of the New Local Government Code of 1991, RA 7160. "It is hereby

declared the policy of the State that the territorial and political subdivisions of

the State shall enjoy genuine and meaningful local autonomy to enable them to

attain their fullest development as self-reliant communities and make them more

effective partners in the attainment of national goals. Toward this end, the State

shall provide for a more responsive and accountable local government structure

instituted through a system of decentralization whereby local government units

shall be given more powers, authority, responsibilities, and resources. The

process of decentralization shall proceed from the national government to the

local government units. . . ." 5

Its motion for reconsideration having been denied by the trial court in its 4 May 1995 order, the

petitioner filed the instant petition based on the following assignment of errors:

I. RESPONDENT JUDGE ERRED IN FAILING TO RULE THAT THE

PETITIONER IS VESTED WITH GOVERNMENT POWERS AND

FUNCTIONS WHICH PLACE IT IN THE SAME CATEGORY AS

AN INSTRUMENTALITY OR AGENCY OF THE GOVERNMENT.

II. RESPONDENT JUDGE ERRED IN RULING THAT PETITIONER IS

LIABLE TO PAY REAL PROPERTY TAXES TO THE CITY OF

CEBU.

Anent the first assigned error, the petitioner asserts that although it is a government-owned or

controlled corporation, it is mandated to perform functions in the same category as an

instrumentality of Government. An instrumentality of Government is one created to perform

governmental functions primarily to promote certain aspects of the economic life of the

people. 6 Considering its task "not merely to efficiently operate and manage the Mactan-Cebu

International Airport, but more importantly, to carry out the Government policies of promoting

and developing the Central Visayas and Mindanao regions as centers of international trade and

tourism, and accelerating the development of the means of transportation and communication in

the country," 7 and that it is an attached agency of the Department of Transportation and

Communication (DOTC), 8 the petitioner "may stand in [sic] the same footing as an agency or

instrumentality of the national government." Hence, its tax exemption privilege under Section 14

of its Charter "cannot be considered withdrawn with the passage of the Local Government

Code of 1991 (hereinafter LGC) because Section 133 thereof specifically states that the 'taxing

powers of local government units shall not extend to the levy of taxes or fees or charges of any

kind on the national government, its agencies and instrumentalities.'"

As to the second assigned error, the petitioner contends that being an instrumentality of the

National Government, respondent City of Cebu has no power nor authority to impose realty

taxes upon it in accordance with the aforesaid Section 133 of the LGC, as explained in Basco

vs. Philippine Amusement and Gaming Corporation: 9

Local governments have no power to tax instrumentalities of the National

Government. PAGCOR is a government owned or controlled corporation with

an original charter, PD 1869. All of its shares of stock are owned by the

National Government. . . .

PAGCOR has a dual role, to operate and regulate gambling casinos. The latter

role is governmental, which places it in the category of an agency or

instrumentality of the Government. Being an instrumentality of the Government,

PAGCOR should be and actually is exempt from local taxes. Otherwise, its

operation might be burdened, impeded or subjected to control by a mere Local

government. cdtai

The states have no power by taxation or otherwise, to retard, impede, burden or

in any manner control the operation of constitutional laws enacted by Congress

to carry into execution the powers vested in the federal government (McCulloch

v. Maryland, 4 Wheat 316, 4 L Ed. 579)

This doctrine emanates from the "supremacy" of the National Government over

local governments.

"Justice Holmes, speaking for the Supreme Court, made reference to the entire

absence of power on the part of the States to touch, in that way (taxation) at

least, the instrumentalities of the United States (Johnson v. Maryland, 254 USA

51) and it can be agreed that no state or political subdivision can regulate a

federal instrumentality in such a way as to prevent it from consummating its

federal responsibilities, or even to seriously burden it in the accomplishment of

them." (Antieau, Modern Constitutional Law, Vol. 2, p. 140)

Otherwise, mere creatures of the State can defeat National policies thru

extermination of what local authorities may perceive to be undesirable activities

or enterprise using the power to tax as "a tool for regulation" (U.S. v. Sanchez,

340 US 42). The power to tax which was called by Justice Marshall as the

"power to destroy" (Mc Culloch v. Maryland, supra) cannot be allowed to

defeat an instrumentality or creation of the very entity which has the inherent

power to wield it. (italics supplied)

It then concludes that the respondent Judge "cannot therefore correctly say that the questioned

provisions of the Code do not contain any distinction between a government corporation

performing governmental functions as against one performing merely proprietary ones such that

the exemption privilege withdrawn under the said Code would apply to all government

corporations." For it is clear from Section 133, in relation to Section 234, of the LGC that the

legislature meant to excludeinstrumentalities of the national government from the taxing powers

of the local government units. cdasia

In its comment, respondent City of Cebu alleges that as a local government unit and a political

subdivision, it has the power to impose, levy, assess, and collect taxes within its jurisdiction.

Such power is guaranteed by the Constitution 10 and enhanced further by the LGC. While it may

be true that under its Charter the petitioner was exempt from the payment of realty taxes, 11 this

exemption was withdrawn by Section 234 of the LGC. In response to the petitioner's claim that

such exemption was not repealed because being an instrumentality of the National Government,

Section 133 of the LGC prohibits local government units from imposing taxes, fees, or charges

of any kind on it, respondent City of Cebu points out that the petitioner is likewise a government-

owned corporation, and Section 234 thereof does not distinguish between government-owned or

controlled corporations performing governmental and purely proprietary functions. Respondent

City of Cebu urges this Court to apply by analogy its ruling that the Manila International Airport

Authority is a government-owned corporation, 12 and to reject the application of Basco because

it was "promulgated . . . before the enactment and the signing into law of R.A. No. 7160," and

was not, therefore, decided "in the light of the spirit and intention of the framers of" the said law.

As a general rule, the power to tax is an incident of sovereignty and is unlimited in its range,

acknowledging in its very nature no limits, so that security against its abuse is to be found only

in the responsibility of the legislature which imposes the tax on the constituency who are to pay

it. Nevertheless, effective limitations thereon may be imposed by the people through their

Constitutions. 13 Our Constitution, for instance, provides that the rule of taxation shall be

uniform and equitable and Congress shall evolve a progressive system of taxation. 14 So potent

indeed is the power that it was once opined that "the power to tax involves the power to

destroy." 15 Verily, taxation is a destructive power which interferes with the personal and

property rights of the people and takes from them a portion of their property for the support of

the government. Accordingly, tax statutes must be construed strictly against the government and

liberally in favor of the taxpayer. 16 But since taxes are what we pay for civilized society, 17 or

are the lifeblood of the nation, the law frowns against exemptions from taxation and statutes

granting tax exemptions are thus construedstrictissimi juris against the taxpayer and liberally in

favor of the taxing authority. 18 A claim of exemption from tax payments must be clearly shown

and based on language in the law too plain to be mistaken. 19 Elsewise stated, taxation is the

rule, exemption therefrom is the exception. 20 However, if the grantee of the exemption is a

political subdivision or instrumentality, the rigid rule of construction does not apply because the

practical effect of the exemption is merely to reduce the amount of money that has to be handled

by the government in the course of its operations. 21

The power to tax is primarily vested in the Congress; however, in our jurisdiction, it may be

exercised by local legislative bodies, no longer merely by virtue of a valid delegation as before,

but pursuant to direct authority conferred by Section 5, Article X of the Constitution. 22 Under

the latter, the exercise of the power may be subject to such guidelines and limitations as the

Congress may provide which, however, must be consistent with the basic policy of local

autonomy.

There can be no question that under Section 14 of R.A. No. 6958 the petitioner is exempt from

the payment of realty taxes imposed by the National Government or any of its political

subdivisions, agencies, and instrumentalities. Nevertheless, since taxation is the rule and

exemption therefrom the exception, the exemption may thus be withdrawn at the pleasure of the

taxing authority. The only exception to this rule is where the exemption was granted to private

parties based on material consideration of a mutual nature, which then becomes contractual and

is thus covered by the non-impairment clause of the Constitution. 23

The LGC, enacted pursuant to Section 3, Article X of the Constitution, provides for the exercise

by local government units of their power to tax, the scope thereof or its limitations, and the

exemptions from taxation.

Section 133 of the LGC prescribes the common limitations on the taxing powers of local

government units as follows:

SEC. 133. Common Limitations on the Taxing Power of Local Government

Units. — Unless otherwise provided herein, the exercise of the taxing powers of

provinces, cities, municipalities, and barangays shall not extend to the levy of

the following:

(a) Income tax, except when levied on banks and other financial

institutions;

(b) Documentary stamp tax;

(c) Taxes on estates, inheritance, gifts, legacies and other

acquisitions mortis causa, except as otherwise provided herein;

(d) Customs duties, registration fees of vessel and wharfage on wharves,

tonnage dues, and all other kinds of customs fees, charges and

dues except wharfage on wharves constructed and maintained by

the local government unit concerned;

(e) Taxes, fees and charges and other impositions upon goods carried

into or out of, or passing through, the territorial jurisdictions of

local government units in the guise of charges for wharfage, tolls

for bridges or otherwise, or other taxes, fees or charges in any

form whatsoever upon such goods or merchandise;

(f) Taxes, fees or charges on agricultural and aquatic products when sold

by marginal farmers or fishermen;

(g) Taxes on business enterprises certified to by the Board of

Investments as pioneer or non-pioneer for a period of six (6) and

four (4) years, respectively from the date of registration;

(h) Excise taxes on articles enumerated under the National Internal

Revenue Code, as amended, and taxes, fees or charges on

petroleum products;

(i) Percentage or value-added tax (VAT) on sales, barters or exchanges

or similar transactions on goods or services except as otherwise

provided herein;

(j) Taxes on the gross receipts of transportation contractors and persons

engaged in the transportation of passengers or freight by hire and

common carriers by air, land or water, except as provided in this

Code;

(k) Taxes on premiums paid by way of reinsurance or retrocession;

(l) Taxes, fees or charges for the registration of motor vehicles and for

the issuance of all kinds of licenses or permits for the driving

thereof, except, tricycles;

(m) Taxes, fees, or other charges on Philippine products actually

exported, except as otherwise provided herein;

(n) Taxes, fees, or charges, on Countryside and Barangay Business

Enterprises and cooperatives duly registered under R.A. No.

6810 and Republic Act Numbered Sixty-nine hundred thirty-

eight (R.A. No. 6938) otherwise known as the "Cooperatives

Code of the 'Philippines' respectively; and

(o) TAXES, FEES OR CHARGES OF ANY KIND ON THE NATIONAL

GOVERNMENT, ITS AGENCIES AND INSTRUMENTALITIES,

AND LOCAL GOVERNMENT UNITS. (italics supplied)

Needless to say, the last item (item o) is pertinent to this case. The "taxes, fees or charges"

referred to are "of any kind"; hence, they include all of these, unless otherwise provided by

the LGC. The term "taxes" is well understood so as to need no further elaboration, especially in

light of the above enumeration. The term "fees" means charges fixed by law or ordinance for the

regulation or inspection of business or activity, 24 while "charges" are pecuniary liabilities such

as rents or fees against persons or property. 25

Among the "taxes" enumerated in the LGC is real property tax, which is governed by Section

232. It reads as follows:

SEC. 232. Power to Levy Real Property Tax. — A province or city or a

municipality within the Metropolitan Manila Area may levy an annual ad

valorem tax on real property such as land, building, machinery, and other

improvements not hereafter specifically exempted.

Section 234 of the LGC provides for the exemptions from payment of real property taxes and

withdraws previous exemptions therefrom granted to natural and juridical persons, including

government-owned and controlled corporations, except as provided therein. It provides:

SEC. 234. Exemptions from Real Property Tax. — The following are exempted

from payment of the real property tax:

(a) Real property owned by the Republic of the Philippines or any of its

political subdivisions except when the beneficial use thereof had

been granted, for consideration or otherwise, to a taxable person;

(b) Charitable institutions, churches, parsonages or convents appurtenant

thereto, mosques, non-profit or religious cemeteries and all lands,

buildings and improvements actually, directly, and exclusively

used for religious, charitable or educational purposes;

(c) All machineries and equipment that are actually, directly and

exclusively used by local water districts and government-owned

or controlled corporations engaged in the supply and distribution

of water and/or generation and transmission of electric power;

(d) All real property owned by duly registered cooperatives as provided

for under R.A. No. 6938; and

(e) Machinery and equipment used for pollution control and

environmental protection.

Except as provided herein, any exemption from payment of real property tax

previously granted to, or presently enjoyed by, all persons, whether natural or

juridical, including all government-owned or controlled corporations are hereby

withdrawn upon the effectivity of this Code.

These exemptions are based on the ownership, character, and use of the property. Thus:

(a) Ownership Exemptions. Exemptions from real property taxes on the basis

of ownership are real properties owned by: (i) the Republic, (ii) a

province, (iii) a city, (iv) a municipality, (v) a barangay, and (vi)

registered cooperatives.

(b) Character Exemptions. Exempted from real property taxes on the basis of

their character are: (i) charitable institutions, (ii) houses and temples of

prayer like churches, parsonages or convents appurtenant thereto,

mosques, and (iii) non-profit or religious cemeteries.

(c) Usage exemptions. Exempted from real property taxes on the basis of the

actual, direct and exclusive use to which they are devoted are: (i) all

lands, buildings and improvements which are actually directly and

exclusively used for religious, charitable or educational purposes; (ii) all

machineries and equipment actually, directly and exclusively used by

local water districts or by government-owned or controlled corporations

engaged in the supply and distribution of water and/or generation and

transmission of electric power; and (iii) all machinery and equipment

used for pollution control and environmental protection.

To help provide a healthy environment in the midst of the modernization of the

country, all machinery and equipment for pollution control and environmental

protection may not be taxed by local governments.

2. Other Exemptions Withdrawn. All other exemptions previously granted to

natural or juridical persons including government-owned or controlled

corporations are withdrawn upon the effectivity of the Code. 26

Section 193 of the LGC is the general provision on withdrawal of tax exemption privileges. It

provides:

SEC. 193. Withdrawal of Tax Exemption Privileges. — Unless otherwise

provided in this Code, tax exemptions or incentives granted to, or presently

enjoyed by all persons, whether natural or juridical, including government-

owned or controlled corporations, except local water districts, cooperatives duly

registered under R.A. 6938, non-stock and non-profit hospitals and educational

institutions, are hereby withdrawn upon the effectivity of this Code.

On the other hand, the LGC authorizes local government units to grant tax exemption privileges.

Thus, Section 192 thereof provides:

SEC. 192. Authority to Grant Tax Exemption Privileges. — Local government

units may, through ordinances duly approved, grant tax exemptions, incentives

or reliefs under such terms and conditions as they may deem necessary.

The foregoing sections of the LGC speak of: (a) the limitations on the taxing powers of local

government units and the exceptions to such limitations; and (b) the rule on tax exemptions and

the exceptions thereto. The use of exceptions or provisos in these sections, as shown by the

following clauses:

(1) "unless otherwise provided herein" in the opening paragraph of Section 133;

(2) "Unless otherwise provided in this Code" in Section 193;

(3) "not hereafter specifically exempted" in Section 232; and

(4) "Except as provided herein" in the last paragraph of Section 234

initially hampers a ready understanding of the sections. Note, too, that the aforementioned

clause in Section 133 seems to be inaccurately worded. Instead of the clause "unless

otherwise provided herein," with the "herein" to mean, of course, the section, it should have

used the clause "unless otherwise provided in this Code." The former results in absurdity

since the section itself enumerates what are beyond the taxing powers of local government

units and, where exceptions were intended, the exceptions are explicitly indicated in the next.

For instance, in item (a) which excepts income taxes "when levied on banks and other

financial institutions"; item (d) which excepts "wharfage on wharves constructed and

maintained by the local government unit concerned"; and item (1) which excepts taxes, fees

and charges for the registration and issuance of licenses or permits for the driving of

"tricycles." It may also be observed that within the body itself of the section, there are

exceptions which can be found only in other parts of the LGC, but the section

interchangeably uses therein the clause, "except as otherwise provided herein" as in items (c)

and (i), or the clause "except as provided in this Code" in item (j). These clauses would be

obviously unnecessary or mere surplusages if the opening clause of the section were "Unless

otherwise provided in this Code" instead of "Unless otherwise provided herein." In any

event, even if the latter is used, since under Section 232 local government units have the

power to levy real property tax, except those exempted therefrom under Section 234, then

Section 232 must be deemed to qualify Section 133.

Thus, reading together Sections 133, 232, and 234 of the LGC, we conclude that as a general

rule, as laid down in Section 133, the taxing powers of local government units cannot extend to

the levy of, inter alia, "taxes, fees and charges of any kind on the National Government, its

agencies and instrumentalities, and local government units"; however, pursuant to Section 232,

provinces, cities, and municipalities in the Metropolitan Manila Area may impose the real

property tax except on, inter alia, "real property owned by the Republic of the Philippines or any

of its political subdivisions except when the beneficial use thereof has been granted, for

consideration or otherwise, to a taxable person," as provided in item (a) of the first paragraph of

Section 234.

As to tax exemptions or incentives granted to or presently enjoyed by natural or judicial persons,

including government-owned and controlled corporations, Section 193 of the LGC prescribes the

general rule, viz., they are withdrawn upon the effectivity of the LGC, except those granted to

local water districts, cooperatives duly registered under R.A. No. 6938, non-stock and non-profit

hospitals and educational institutions, and unless otherwise provided in the LGC. The latter

proviso could refer to Section 234 which enumerates the properties exempt from real property

tax. But the last paragraph of Section 234 further qualifies the retention of the exemption insofar

as real property taxes are concerned by limiting the retention only to those enumerated therein;

all others not included in the enumeration lost the privilege upon the effectivity of the LGC.

Moreover, even as to real property owned by the Republic of the Philippines or any of its

political subdivisions covered by item (a) of the first paragraph of Section 234, the exemption is

withdrawn if the beneficial use of such property has been granted to a taxable person for

consideration or otherwise.

Since the last paragraph of Section 234 unequivocally withdrew, upon the effectivity of the LGC,

exemptions from payment of real property taxes granted to natural or juridical persons, including

government-owned or controlled corporations, except as provided in the said section, and the

petitioner is, undoubtedly, a government-owned corporation, it necessarily follows that its

exemption from such tax granted it in Section 14 of its Charter, R.A. No. 6958, has been

withdrawn. Any claim to the contrary can only be justified if the petitioner can seek refuge under

any of the exceptions provided in Section 234, but not under Section 133, as it now asserts,

since, as shown above, the said section is qualified by Sections 232 and 234. LLphil

In short, the petitioner can no longer invoke the general rule in Section 133 that the taxing

powers of the local government units cannot extend to the levy of:

(o) taxes, fees or charges of any kind on the National Government, its agencies

or instrumentalities, and local government units.

It must show that the parcels of land in question, which are real property, are any one of those

enumerated in Section 234, either by virtue of ownership, character, or use of the property. Most

likely, it could only be the first, but not under any explicit provision of the said section, for none

exists. In light of the petitioner's theory that it is an "instrumentality of the Government," it could

only be within the first item of the first paragraph of the section by expanding the scope of the

term "Republic of the Philippines" to embrace its "instrumentalities" and "agencies." For

expediency, we quote:

(a) real property owned by the Republic of the Philippines, or any of its political

subdivisions except when the beneficial use thereof has been granted, for

consideration or otherwise, to a taxable person.

This view does not persuade us. In the first place, the petitioner's claim that it is an

instrumentality of the Government is based on Section 133(o), which expressly mentions the

word "instrumentalities"; and, in the second place, it fails to consider the fact that the legislature

used the phrase "National Government, its agencies and instrumentalities" in Section 133(o), but

only the phrase "Republic of the Philippines or any of its political subdivisions" in Section

234(a).

The terms "Republic of the Philippines" and "National Government" are not interchangeable.

The former is broader and synonymous with "Government of the Republic of the Philippines"

which the Administrative Code of 1987 defines as the "corporate governmental entity through

which the functions of government are exercised throughout the Philippines, including, save as

the contrary appears from the context, the various arms through which political authority is made

affective in the Philippines, whether pertaining to the autonomous regions, the provincial, city,

municipal or barangay subdivisions or other forms of local government." 27 These "autonomous

regions, provincial, city, municipal or barangay subdivisions" are the political subdivisions. 28

On the other hand, "National Government" refers "to the entire machinery of the central

government, as distinguished from the different forms of local governments."29 The National

Government then is composed of the three great departments: the executive, the legislative and

the judicial. 30

An "agency" of the Government refers to "any of the various units of the Government, including

a department, bureau, office, instrumentality, or government-owned or controlled corporation, or

a local government or a distinct unit therein;" 31 while an "instrumentality" refers to "any agency

of the National Government, not integrated within the department framework, vested with

special functions or jurisdiction by law, endowed with some if not all corporate powers,

administering special funds, and enjoying operational autonomy, usually through a charter. This

term includes regulatory agencies, chartered institutions and government-owned and controlled

corporations." 32

If Section 234(a) intended to extend the exception therein to the withdrawal of the exemption

from payment of real property taxes under the last sentence of the said section to the agencies

and instrumentalities of the National Government mentioned in Section 133(o), then it should

have restated the wording of the latter. Yet, it did not. Moreover, that Congress did not wish to

expand the scope of the exemption in Section 234(a) to include real property owned by other

instrumentalities or agencies of the government including government-owned and controlled

corporations is further borne out by the fact that the source of this exemption is Section 40(a)

of P.D. No. 464, otherwise known as The Real Property Tax Code, which reads:

SEC. 40. Exemptions from Real Property Tax. — The exemption shall be as

follows:

(a) Real property owned by the Republic of the Philippines or any of its political

subdivisions and any government-owned or controlled corporation so

exempt by its charter: Provided, however, That this exemption shall not

apply to real property of the above-mentioned entities the beneficial use

of which has been granted, for consideration or otherwise, to a taxable

person.

Note that as reproduced in Section 234(a), the phrase "and any government-owned or

controlled corporation so exempt by its charter" was excluded. The justification for this

restricted exemption in Section 234(a) seems obvious: to limit further tax exemption

privileges, especially in light of the general provision on withdrawal of tax exemption

privileges in Section 193 and the special provision on withdrawal of exemption from

payment of real property taxes in the last paragraph of Section 234. These policy

considerations are consistent with the State policy to ensure autonomy to local

governments 33 and the objective of the LGCthat they enjoy genuine and meaningful local

autonomy to enable them to attain their fullest development as self-reliant communities and

make them effective partners in the attainment of national goals. 34 The power to tax is the

most effective instrument to raise needed revenues to finance and support myriad activities of

local government units for the delivery of basic services essential to the promotion of the

general welfare and the enhancement of peace, progress, and prosperity of the people. It may

also be relevant to recall that the original reasons for the withdrawal of tax exemption

privileges granted to government-owned and controlled corporations and all other units of

government were that such privilege resulted in serious tax base erosion and distortions in the

tax treatment of similarly situated enterprises, and there was a need for these entities to share

in the requirements of development, fiscal or otherwise, by paying the taxes and other

charges due from them. 35

The crucial issues then to be addressed are: (a) whether the parcels of land in question belong to

the Republic of the Philippines whose beneficial use has been granted to the petitioner, and (b)

whether the petitioner is a "taxable person."

Section 15 of the petitioner's Charter provides:

Sec. 15. Transfer of Existing Facilities and Intangible Assets. — All existing

public airport facilities, runways, lands, buildings and other properties, movable

or immovable, belonging to or presently administered by the airports, and all

assets, powers, rights, interests and privileges relating on airport works or air

operations, including all equipment which are necessary for the operations of air

navigation, aerodrome control towers, crash, fire, and rescue facilities are

hereby transferred to the Authority: Provided, however, that the operations

control of all equipment necessary for the operation of radio aids to air

navigation, airways communication, the approach control office, and the area

control center shall be retained by the Air Transportation Office. No equipment,

however, shall be removed by the Air Transportation Office from Mactan

without the concurrence of the Authority. The Authority may assist in the

maintenance of the Air Transportation Office equipment.

The "airports" referred to are the "Lahug Air Port" in Cebu City and the "Mactan International

Airport in the Province of Cebu," 36 which belonged to the Republic of the Philippines, then

under the Air Transportation Office (ATO). 37

It may be reasonable to assume that the term "lands" refer to "lands" in Cebu City then

administered by the Lahug Air Port and included the parcels of land the respondent City of Cebu

seeks to levy on for real property taxes. This section involves a "transfer" of the "lands," among

other things, to the petitioner and not just the transfer of the beneficial use thereof, with the

ownership being retained by the Republic of the Philippines.

This "transfer" is actually an absolute conveyance of the ownership thereof because the

petitioner's authorized capital stock consists of, inter alia, "the value of such real estate owned

and/or administered by the airports." 38 Hence, the petitioner is now the owner of the land in

question and the exception in Section 234(c) of the LGC is inapplicable.

Moreover, the petitioner cannot claim that it was never a "taxable person" under its Charter. It

was only exempted from the payment of real property taxes. The grant of the privilege only in

respect of this tax is conclusive proof of the legislative intent to make it a taxable person subject

to all taxes, except real property tax.

Finally, even if the petitioner was originally not a taxable person for purposes of real property

tax, in light of the foregoing disquisitions, it had already become, even if it be conceded to be an

"agency" or "instrumentality" of the Government, a taxable person for such purpose in view of

the withdrawal in the last paragraph of Section 234 of exemptions from the payment of real

property taxes, which, as earlier adverted to, applies to the petitioner.

Accordingly, the position taken by the petitioner is untenable. Reliance on Basco vs. Philippine

Amusement and Gaming Corporation 39 is unavailing since it was decided before the effectivity

of the LGC. Besides, nothing can prevent Congress from decreeing that even instrumentalities or

agencies of the Government performing governmental functions may be subject to tax. Where it

is done precisely to fulfill a constitutional mandate and national policy, no one can doubt its

wisdom.

WHEREFORE, the instant petition is DENIED. The challenged decision and order of the

Regional Trial Court of Cebu, Branch 20, in Civil Case No. CEB-16900 are AFFIRMED.

No pronouncement as to costs.

SO ORDERED

PHILIPPINE LONG DISTANCE TELEPHONE COMPANY,

INC., petitioner, vs. CITY OF BACOLOD, FLORENTINO T. GUANCO, in

his capacity as the City Treasurer of Bacolod City, and ANTONIO G.

LACZI, in his capacity as the City Legal Officer of Bacolod

City, respondents.

Estelito P. Mendoza for petitioner.

Bacolod City Legal Office for respondents.

SYLLABUS

1. POLITICAL LAW; LOCAL GOVERNMENT; TAXATION; FRANCHISE

TAX; REPUBLIC ACT NO. 7925, SECTION 23 THEREOF; "MOST-FAVORED-

TREATMENT" CLAUSE, CONSTRUED. — As we see it, the only question which commends

itself for our resolution is, whether or not Section 23 of Rep. Act No. 7925, also called the

"most-favored-treatment" clause, operates to exempt petitioner PLDT from the payment of

franchise tax imposed by the respondent City of Bacolod. Contrary to petitioner's claim, the issue

thus posed is not one of "first impression" insofar as this Court is concerned. In PLDT vs. City of

Davao, this Court interpreted Section 23 of Rep. Act No. 7925 as not operating to exempt PLDT

from the payment of franchise tax imposed upon it by the City of Davao: In sum, it does not

appear that, in approving §23 ofR.A. No. 7925, Congress intended it to operate as a blanket tax

exemption to all telecommunications entities. Applying the rule of strict construction of laws

granting tax exemptions and the rule that doubts should be resolved in favor of municipal

corporations in interpreting statutory provisions on municipal taxing powers, we hold that §23

of R.A. No. 7925 cannot be considered as having amended petitioner's franchise so as to entitle it

to exemption from the imposition of local franchise taxes. Consequently, we hold that petitioner

is liable to pay local franchise taxes in the amount of P3,681,985.72 for the period covering the

first to the fourth quarter of 1999 and that it is not entitled to a refund of taxes paid by it for the

period covering the first to the third quarter of 1998.

2. ID.; ID.; ID.; ID.; ID.; GRANT OF TAX EXEMPTION TO SMART AND GLOBE DOES

NOT IPSO FACTO APPLY TO PHILIPPINE LONG DISTANCE TELEPHONE COMPANY,

INC. — As in City of Davao, supra, petitioner presently argues that because Smart

Communications, Inc. (SMART) and Globe Telecom (GLOBE) under whose respective

franchises granted after the effectivity of the Local Government Code, are exempt from franchise

tax, it follows that petitioner is likewise exempt from the franchise tax sought to be collected by

the City of Bacolod, on the reasoning that the grant of tax exemption to SMART and GLOBE

ipso facto applies to PLDT, consistent with the "most-favored-treatment" clause found in Section

23 of the Public Telecommunications Policy Act of the Philippines (Rep. Act No. 7925). Again,

there is nothing novel in petitioner's contention. In rejecting PLDT's contention, this Court ruled

in City of Davao as follows: The acceptance of petitioner's theory would result in absurd

consequences. To illustrate: In its franchise, Globe is required to pay a franchise tax of only one

and one-half percentum (1/2% [sic] ) of all gross receipts from its transactions while Smart is

required to pay a tax of three percent (3%) on all gross receipts from business transacted.

Petitioner's theory would require that, to level the playing field, any "advantage, favor, privilege,

exemption, or immunity" granted to Globe must be extended to all telecommunications

companies, including Smart. If, later, Congress again grants a franchise to another

telecommunications company imposing, say, one percent (1%) franchise tax, then all other

telecommunications franchises will have to be adjusted to "level the playing field" so to speak.

This could not have been the intent of Congress in enacting Section 23 of Rep. Act 7925.

Petitioner's theory will leave the Government with the burden of having to keep track of all

granted telecommunications franchises, lest some companies be treated unequally. It is different

if Congress enacts a law specifically granting uniform advantages, favor, privilege, exemption or

immunity to all telecommunications entities.

3. ID.; ID.; ID.; ID.; ID.; DOES NOT REFER TO TAX EXEMPTION BUT ONLY TO

EXEMPTION FROM CERTAIN REGULATIONS AND REQUIREMENTS IMPOSED BY

THE NATIONAL TELECOMMUNICATIONS COMMISSION. — On PLDT's motion for

reconsideration in City of Davao, the Court added in its en banc Resolution of March 25, 2003,

that even as it is a state policy to promote a level playing field in the communications industry,

Section 23 of Rep. Act No. 7925 does not refer to tax exemption but only to exemption from

certain regulations and requirements imposed by the National Telecommunications Commission:

. . . . The records of Congress are bereft of any discussion or even mention of tax exemption. To

the contrary, what the Chairman of the Committee on Transportation, Rep. Jerome V. Paras,

mentioned in his sponsorship of H.B. No. 14028, which became R.A. No. 7925, were 'equal

access clauses' in interconnection agreements, not tax exemptions. He said: There is also a need

to promote a level playing field in the telecommunications industry. New entities must be

granted protection against dominant carriers through the encouragement of equitable access

charges and equal access clauses in interconnection agreements and the strict policing of

predatory pricing by dominant carriers. Equal access should be granted to all operators

connecting into the interexchange network. There should be no discrimination against any carrier

in terms of priorities and/or quality of services. Nor does the term 'exemption' in §23 of R.A.

No. 7925 mean tax exemption. The term refers to exemption from certain regulations and

requirements imposed by the National Telecommunications Commission (NTC). For

instance, R.A. No. 7925, §17 provides: 'The Commission shall exempt any specific

telecommunications service from its rate or tariff regulations if the service has sufficient

competition to ensure fair and reasonable rates or tariffs.' Another exemption granted by the law

in line with its policy of deregulation is the exemption from the requirement of securing permits

from the NTC every time a telecommunications company imports equipment.

4. ID.; ID.; ID.; ID.; ID.; RULE THAT TAX EXEMPTION SHOULD BE APPLIED IN

STRICTISSIMI JURIS AGAINST THE TAXPAYER AND LIBERALLY IN FAVOR OF THE

GOVERNMENT APPLIES EQUALLY TO TAX EXCLUSIONS; TAX EXEMPTION

DISTINGUISHED FROM TAX EXCLUSION. — In the same en banc Resolution, the Court

even rejected PLDT's contention that the "in-lieu-of-all-taxes" clause does not refer to "tax

exemption" but to "tax exclusion" and hence, the strictissimi juris rule does not apply, explaining

that these two terms actually mean the same thing, such that the rule that tax exemption should

be applied in strictissimi juris against the taxpayer and liberally in favor of the government

applies equally to tax exclusions. Thus: Indeed, both in their nature and in their effect there is no

difference between tax exemption and tax exclusion. Exemption is an immunity or privilege; it is

freedom from a charge or burden to which others are subjected. Exclusion, on the other hand, is

the removal of otherwise taxable items from the reach of taxation, e.g., exclusions from gross

income and allowable deductions. Exclusion is thus also an immunity or privilege which frees a

taxpayer from a charge to which others are subjected. Consequently, the rule that tax exemption

should be applied in strictissimi juris against the taxpayer and liberally in favor of the

government applies equally to tax exclusions. To construe otherwise the 'in lieu of all taxes'

provision invoked is to be inconsistent with the theory that R.A. No. 7925, §23 grants tax

exemption because of a similar grant to Globe and Smart.

5. ID.; ID.; ID.; ID.; ID.; THE BUREAU OF LOCAL GOVERNMENT FINANCE IS NOT AN

ADMINISTRATIVE AGENCY WHOSE FINDINGS OF FACT ARE GIVEN WEIGHT AND

DEFERENCE IN COURTS. — PLDT likewise argued in said case that the RTC at Davao City

erred in not giving weight to the ruling of the BLGF which, according to petitioner, is an

administrative agency with technical expertise and mastery over the specialized matters assigned

to it. But then again, we held in Davao: To be sure, the BLGF is not an administrative agency

whose findings on questions of fact are given weight and deference in the courts. The authorities

cited by petitioner pertain to the Court of Tax Appeals, a highly specialized court which

performs judicial functions as it was created for the review of tax cases. In contrast, the BLGF

was created merely to provide consultative services and technical assistance to local

governments and the general public on local taxation, real property assessment, and other related

matters, among others. The question raised by petitioner is a legal question, to wit, the

interpretation of §23 of R.A. No. 7925. There is, therefore, no basis for claiming expertise for

the BLGF that administrative agencies are said to possess in their respective fields.

D E C I S I O N