TAX RETURNS FOR NON US CITIZENS (FOREIGN … · Topics Covered 1. Types of returns –regular 1040...

40

TAX RETURNS FOR NON US CITIZENS (FOREIGN STUDENTS AND IMMIGRANTS) Monica Ibarra and Mary Lepper Center for Great Neighborhoods VITA

Transcript of TAX RETURNS FOR NON US CITIZENS (FOREIGN … · Topics Covered 1. Types of returns –regular 1040...

TAX RETURNS FOR NON US

CITIZENS (FOREIGN STUDENTS

AND IMMIGRANTS)

Monica Ibarra and Mary Lepper

Center for Great Neighborhoods VITA

Topics Covered

1. Types of returns – regular 1040 or 1040NR

2. Steps to determine return type to file

3. Resident Alien Taxpayer

4. Nonresident Alien Taxpayer

5. Dual-Status Taxpayer

6. Individual Tax Identification Number (ITIN)

7. Tax Credit Eligibility

8. Start of 1040NR return in Taxslayer

2

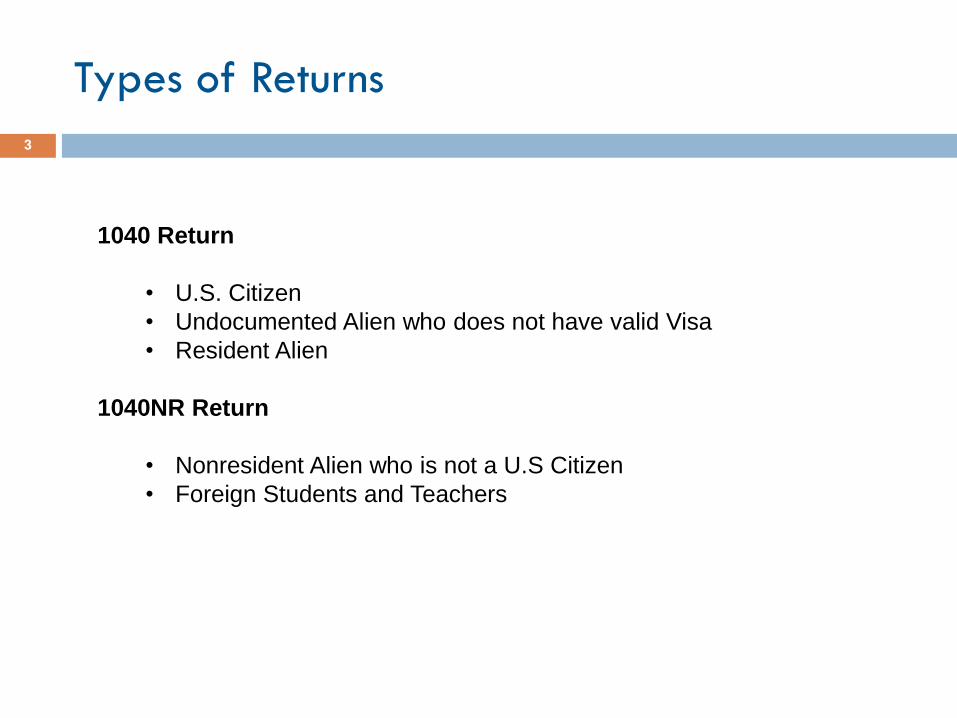

Types of Returns

1040 Return

• U.S. Citizen

• Undocumented Alien who does not have valid Visa

• Resident Alien

1040NR Return

• Nonresident Alien who is not a U.S Citizen

• Foreign Students and Teachers

3

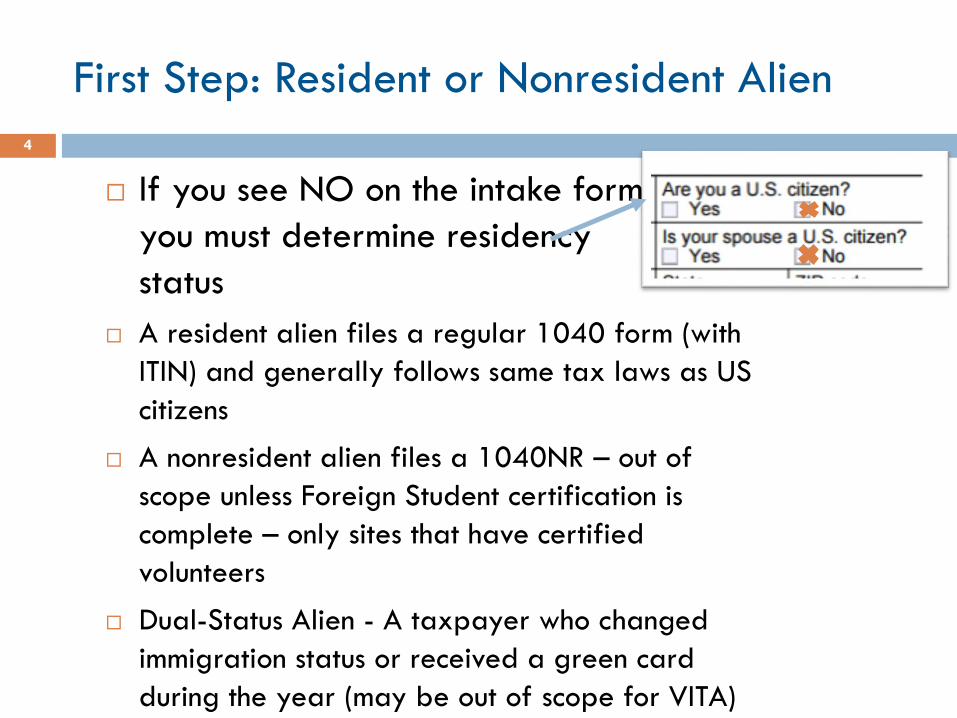

First Step: Resident or Nonresident Alien

If you see NO on the intake form

you must determine residency

status

A resident alien files a regular 1040 form (with

ITIN) and generally follows same tax laws as US

citizens

A nonresident alien files a 1040NR – out of

scope unless Foreign Student certification is

complete – only sites that have certified

volunteers

Dual-Status Alien - A taxpayer who changed

immigration status or received a green card

during the year (may be out of scope for VITA)

4

Resident Alien

Must meet one of two tests:

Green Card Test

Taxpayer was lawful permanent resident at any time during

the year (had a “green card”) OR

Substantial Presence Test

Physically present in the US for at least 31 days during

2016 AND physically present in the US for at least 183

days during the past 3 years counting all days in 2017,

1/3 of the days present in 2016 and 1/6 of the days

present in 2015.

See Decision Tree in Pub 4012 for full details

5

Sample Permanent Resident cards

Current version

Older, still valid version

6

Substantial Presence Test Example

Victor first arrived in the US on July 1st, 2016. He

returned to Syria to care for his sick mother on

December 20, 2016. After his mother’s death in May,

2017, Victor returned to Pittsburgh on August 31,

2017. He has a SSN but is not a citizen.

Victor was present in the US for 123 days in 2017

and 173 days in 2016.

123 days in 2017 + 57 (1/3 of 173) days in 2016

= 180 days

He does not meet the substantial presence test of 183

days and is a Nonresident alien for tax purposes.

7

Substantial Presence Test Example

Januka is a refugee and arrived in the US on March

1st, 2017. This is her first time in the US and she

hasn’t left the country since her arrival. She

received a Social Security number and card shortly

after she arrived.

Januka was in the US for 306 days in 2017.

Januka meets the substantial presence test and is a

resident alien for tax purposes. She files a regular

1040 return.

8

Substantial Presence Test: Students and Teachers

Foreign Students

Do not count the days present during the first 5 calendar years

will be considered nonresident for first 5 years of presence, can be

resident if here longer than 5 years

Teachers or Trainee

Do not count the days present during the first 2 calendar years

Will be considered nonresident for first 2 years of presence, can be

resident if here longer than 2 years

Question – are any of your sites preparing 1040NR returns for

nonresident students and teachers?

9

Screening Question to Help Determine Return

Type Status

Are you a citizen or resident of the US?

You are a resident of the US if you have a green

card (for all or part of the year) OR meet

the substantial presence test. If yes, continue with

preparing the regular1040 return.

If no, Check with local sites that are preparing

1040NR returns and direct taxpayer to site. Out of

scope at most local sites.

10

Identification Needed for Return Preparation

11

Social Security Card

• Issued to U.S Citizens and Immigrants with valid immigration

documentation

Individual Tax Identification Number (ITIN)

• United States tax processing number issued by the Internal Revenue

Service (IRS).

• The IRS issues ITINs to individuals who are required to have a U.S.

taxpayer identification number but who do not have, and are not

eligible to obtain, a Social Security number (SSN) from the Social

Security Administration (SSA).

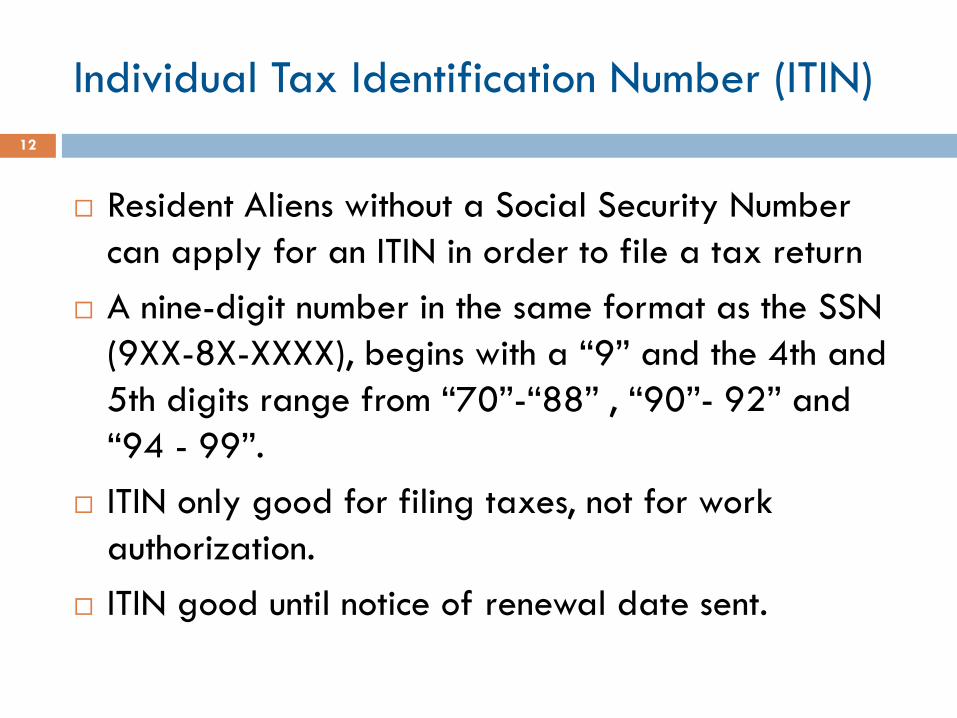

Individual Tax Identification Number (ITIN)

Resident Aliens without a Social Security Number

can apply for an ITIN in order to file a tax return

A nine-digit number in the same format as the SSN

(9XX-8X-XXXX), begins with a “9” and the 4th and

5th digits range from “70”-“88” , “90”- 92” and

“94 - 99”.

ITIN only good for filing taxes, not for work

authorization.

ITIN good until notice of renewal date sent.

12

Purpose of ITINs

IRS assigned numbers issued only for federal tax

administration purposes

Provide a means to efficiently process and account

for tax returns and payments for those not eligible

for Social Security Numbers.

Assist the IRS with collection of taxes from foreign

nationals, nonresident aliens and others who have

filing or payment obligations under U.S. tax law

13

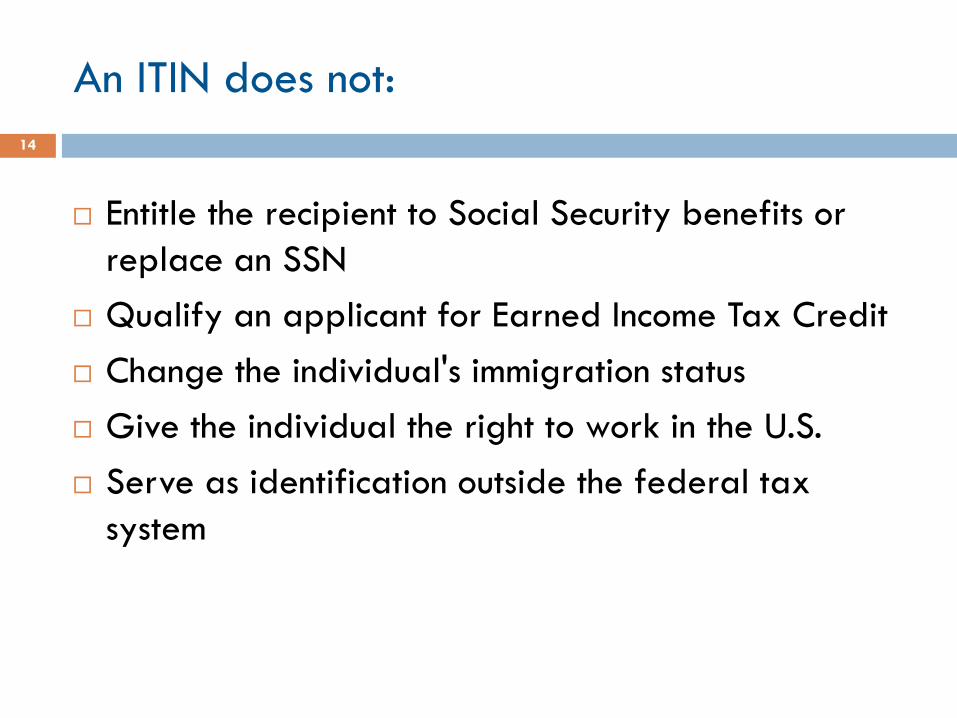

An ITIN does not:

Entitle the recipient to Social Security benefits or

replace an SSN

Qualify an applicant for Earned Income Tax Credit

Change the individual's immigration status

Give the individual the right to work in the U.S.

Serve as identification outside the federal tax

system

14

Who needs an ITIN?

A resident alien (taxpayer) filing a U.S. federal tax return who

does not have social security number.

A dependent or spouse of a U.S. citizen or taxpayer who does

not have valid social security number.

A nonresident alien required to file a return to obtain a refund

of tax withheld under the provisions of an income tax treaty.

Foreign nationals and others who have a federal income tax

reporting or filing requirement.

A nonresident alien student, professor, or researcher filing a

U.S. federal tax return or claiming an exception.

A dependent or spouse of a nonresident alien holding a U.S.

visa

15

Who is not eligible for ITIN?

U.S. citizens

Aliens with work visas that qualify them for a SSN

Permanent legal resident of the U.S. (Green card

holder, also known as Permanent Resident Card)

Any individual with a valid SSN

Applicant not meeting the criteria for residency

and/or ID documentation (who failed to prove

identity and foreign status)

16

Why should a resident alien file a tax return at

all?

If you make over a certain amount of money or owe

taxes, you have a legal obligation to file a tax return.

Filing taxes is evidence of good moral character and

continuous presence in the United States.

You could get a cash refund if your employer

withheld excess taxes during the year or if you have

a dependent or dependents that qualify for the Child

Tax Credit.

Some immigration applications require you to present

your tax returns.

17

Will the IRS share my information with

immigration if I file return with ITIN?

No. The IRS does not share information with other

departments of the US Federal government. The IRS

cannot report you to immigration for having applied

or received an ITIN.

However, the courts can request information about

you from the IRS if you have an open deportation

order or if you are suspected of terrorist activities.

18

Tax Credit Eligibility

Eligible if

dependent has

ITIN (not SSN)

Citizenship

EITC NO Child and TP must be US citizen or a legal resident

of the US with SSN valid for work – TIP: Check to

see if SSN is marked “not valid for work” if so not

valid for EIC

Dependent YES Dependent must be US citizen or a resident of the

US, Canada or Mexico (no other country)

Child Tax Credit YES Child must be US citizen or a resident of the US

(lived in US) for more than six months of the year

Head of Household YES Dependent must be US citizen or a resident of the

US, Canada or Mexico

Child Care Credit YES Child must be US citizen or a resident of the US,

Canada or Mexico

American Opportunity and

Lifetime Learning CreditsYES Child must be US citizen or a resident of the US,

Canada or Mexico

19

Special Circumstances:

US Citizen or Resident Alien married to Nonresident Alien

3 filing status options

Married filing separately

May still be able to claim exemption for spouse

Married filing joint

Wordwide income of both must be included

Must include declaration signed by both agreeing to choose resident

alien status

Head of Household

Possible even if they live together. If resident alien is unmarried or considered

unmarried on the last day of the year and they pay more than half the cost of keeping up

a home for you and a qualifying person, claim HOH. Must be a resident alien for the entire

tax year. You are considered unmarried for this purpose. Spouse can be nonresident at

any time during the year.

See details in Publication 4491

20

Special Circumstances:

Exemptions

Dependency Exemption for adopted foreign-born

child

Child must be resident of taxpayer’s household for entire

year

Dependency Exemption for a child born overseas

If at least one parent is a citizen, child is a US citizen for tax

purposes. Must have SSN.

See details in Pub 4491

21

Nonresident VISA Types

22

Student VISA – F-1

• Temporarily in US

• Does not count days in US toward Substantial Presence Test for five

years

• File return as nonresident if worked in US

Nonresident working in US – H-1

• Temporarily in US

• Days in US count toward Substantial Presence Test

• If more than 183, file regular 1040, if not 1040NR

Teacher or Researcher – J-1

• For people who wish to take part in work-and-study-based exchange

and visitor programs in the U.S. These programs are sponsored by

Universities or Corporations

Dual-Status Taxpayer

23

Dual-Status Taxpayer

• Both a resident alien and a nonresident alien in the same year

• Does not refer to Citizenship only to resident status in US

• Most common dual-status tax years are the years of arrival and

departure.

• For part of year a nonresident, taxes on income from US sources and

on certain income effectively connected with a U.S. trade or business.

• Out of Scope for VITA sites

Taxslayer – First Step to Start Nonresident

Return24

Taxslayer – Filing Status

25

Required to Answer Health Care Questions

26

Questions to Answer on Non Resident Return

27

Questions to Answer on Non Resident Return

28

Additional Resources

ITIN tab in Pub 4012

Chapter 8 in Pub 4491

Publication 1915: Understanding your IRS ITIN

Publication 519: US Tax Guide for Aliens

Publication 4757: ITIN Power Point Presentation

29

Individual Taxpayer Identification Number

31

What is an ITIN?

It was created for tax purposes. The ITIN program was created by

the IRS in July 1996 so that foreign nationals and other individuals

who are not eligible for a Social Security number (SSN) can pay the

taxes they are legally required to pay.

ITINs are not SSNs. The ITIN is a nine-digit number that always

begins with the number 9 and has a 7 or 8 in the fourth digit, for

example 9XX-7X-XXXX.

Individual Taxpayer Identification Number

32

Many immigrants have ITINs.

People who do not have a lawful status in the United States may obtain

an ITIN.

In addition, the following people are lawfully in the country and must pay

taxes but may not be eligible for a SSN and may obtain an ITIN:

A non-resident foreign national who owns or invests in a U.S.

business and receives taxable income from that U.S. business, but

lives in another country.

A foreign national student who qualifies as a resident of the United

States (based on days present in the United States).

A dependent or spouse of a U.S. citizen or lawful permanent resident.

A dependent or spouse of a foreign national on a temporary visa.

Individual Taxpayer Identification Number

33

ITINs do NOT provide legal status or work authorization.

An ITIN does not provide legal immigration status and cannot be used to prove

legal presence in the United States.

An ITIN does not provide work authorization and cannot be used to prove work

authorization on an I-9 form.

ITIN holders pay taxes.

ITINs let more people pay into the system, which builds the tax base.

ITIN holders are not eligible for all of the tax benefits and public benefits that

U.S. citizens and other taxpayers can receive. For example, an ITIN holder is

not eligible for Social Security benefits or the Earned Income Tax Credit (EITC).

However, if that person becomes eligible for Social Security in the future

(for example, by becoming a lawful permanent resident), the earnings reported

with an ITIN may be counted toward the amount he or she is eligible to receive.

ITIN holders are eligible for the Child Tax Credit (CTC).

What other purposes can an ITIN serve?

Opening an interest-bearing bank account. Individuals who do not have a SNN

but do have an ITIN can open interest-bearing accounts.

Providing proof of residency..

Applying for an ITIN

Each person who applies for an ITIN must file a

separate Form W-7 and provide their own supporting

identification documentation.

One 1040 might include 2 or more W-7s for taxpayer,

spouse and dependent(s)

Form W-7 must be completed and attached to a U.S.

federal income tax return.

34

ITIN application procedures

Appointments will be scheduled via 859.547.5542 at the Centro de

Amistad or Center for Great Neighborhoods sites

Taxpayers can complete Spanish intake form if helpful

Preparer should ensure taxpayer has required documentation before

starting return

Bilingual preparer can complete return(s) and Form W-7 if necessary

Bilingual preparer will translate for review when necessary

Reviewer should review return and Form W-7

35

Documentation Required

Unexpired Passport (If you have a passport, this is the ONLY

document required.) OR

If you do not have a passport, you must present 2 of the

following documents:

If adult, one document must include photo

If dependent, one document must be birth certificate

All documents must be original and unexpired

National Identification Card (for

example, Mexico’s Matricula Consular)

Foreign Voter ID Card

Medical records (Only for dependents

under 6 years old)

School Report Card (Only for students

under 18)

Foreign Military ID Card

Visa issued by the United States

Photo ID from the U.S. Citizenship and

Immigration Services (USCIS)

U.S. Driver’s License

Foreign Driver’s License

U.S. State Photo ID

U.S. Military ID Card

36

Form W-7

Select reason C,

D or E (resident

alien or their

spouse or

dependent)

If D or E is selected and the taxpayer is mailing in a

W-7 also, write their name and “applying for an ITIN”

on the dotted line

37

Form W-7

The applicantʼs name must be listed on the Form W-7 as it appears on the

tax return.

Form W-2 must have the same name that appears on the federal tax

return submitted with Form W-7.

If you no longer have a foreign address, list only your country of last

residence on line 3

38

Form W-7

See form instructions for specific questions

39

Return with ITIN in TaxSlayer

Complete regular 1040 form for resident aliens

Electronic filing of return with valid ITIN and

different SSN shown on W-2.

See instructions in Pub 4012 for

Starting a return for someone applying for an ITIN

Creating a temporary TIN for spouse or dependent

applying for ITIN

42