TAX & LEGAL Business Restructurings: Contract Manufacturers and Commissionaires Eugenio Graziani...

33

TAX & LEGAL Business Restructurings: Contract Manufacturers and Commissionaires Eugenio Graziani KStudio Associato - Verona

-

date post

19-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of TAX & LEGAL Business Restructurings: Contract Manufacturers and Commissionaires Eugenio Graziani...

TAX & LEGAL

Business Restructurings: Contract Manufacturers and CommissionairesEugenio GrazianiKStudio Associato - Verona

2 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

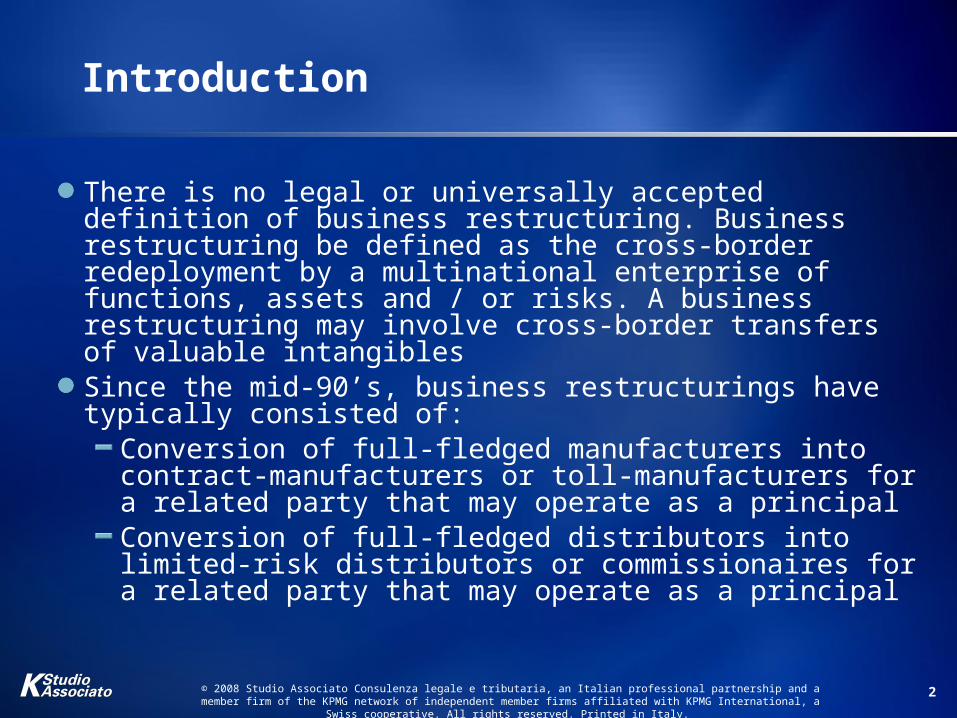

Introduction

There is no legal or universally accepted definition of business restructuring. Business restructuring be defined as the cross-border redeployment by a multinational enterprise of functions, assets and / or risks. A business restructuring may involve cross-border transfers of valuable intangiblesSince the mid-90’s, business restructurings have typically consisted of:

Conversion of full-fledged manufacturers into contract-manufacturers or toll-manufacturers for a related party that may operate as a principalConversion of full-fledged distributors into limited-risk distributors or commissionaires for a related party that may operate as a principal

3 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract ManufacturingContract Manufacturing

4 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing Base Case

PR bears economic risk of loss to raw materials, work-in-process and finished goods throughout manufacturing process; and it has requisite substance to oversee and control timing, quantity and quality of production

PR

CM

Shareholder

Z

1 buy rawmaterials or components

5 sell finished goods

2provideconversion services

$

4 sells finished goods (transferprice) Sales

CompanyX

3 cost-plusconversion fee $

Customers

Y

$

X

Drop Ship

5 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract ManufacturerOverview

Relationship between a principal (“PR”) that engages a contract manufacturer (“CM”) to provide manufacturing servicesCM bears little economic risk associated with production:

Valued intangible property rights are held by PRPlant and equipment are owned by CM (but PR compensates CM for their use)Guaranteed sales (little market risk for CM)Negligible obsolescence risk for CMLittle accounts receivable risk for CMLittle products defect risk for CM

CM transacts on a consignment or buy/sell basis with PRCM generally compensated on a cost-plus basis

6 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract ManufacturerPrincipal

No employees, property, plant or equipment to manufacture productsProvides necessary knowledge to CM (technology, sourcing, planning, material procurements, financial management, sales management, etc.)Assumes entrepreneurial risks such as economic risk of loss on raw materials, work-in-process and finished goodsConducts itself in the manner expected of a third party

7 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

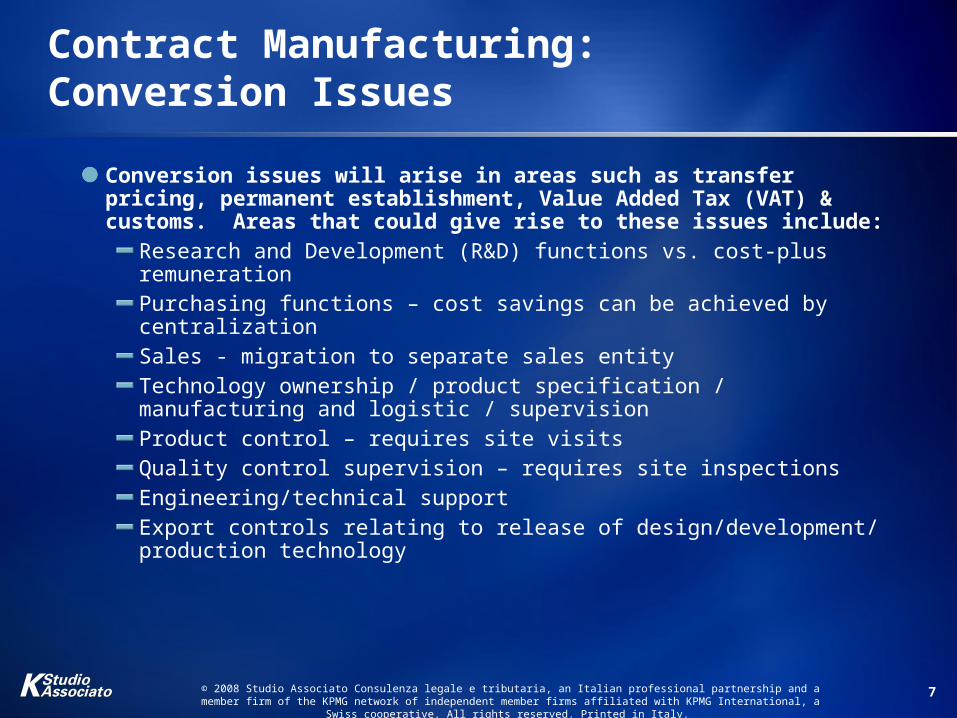

Contract Manufacturing:Conversion Issues

Conversion issues will arise in areas such as transfer pricing, permanent establishment, Value Added Tax (VAT) & customs. Areas that could give rise to these issues include:

Research and Development (R&D) functions vs. cost-plus remunerationPurchasing functions – cost savings can be achieved by centralization Sales - migration to separate sales entityTechnology ownership / product specification / manufacturing and logistic / supervisionProduct control – requires site visitsQuality control supervision – requires site inspectionsEngineering/technical support Export controls relating to release of design/development/ production technology

8 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing – Deemed Transfer of Existing IP or intangibles, or indemnity rights

Charge concerns/transfers of valued Intellectual Property (IP) or other intangibles from CM to PR, or right upon CM for an idemnity due to conversion of the business

9 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing:Transfer Pricing Issues

Issue where related party transactions are involved (provision of processing services). Concern that transfer pricing is used to reallocate profits from high tax to low tax countriesPreferred method - comparable uncontrolled price (CUP)

Likely to be most accurate but difficult to get good comparablesAlternative method - cost-plus

Endorsed by Organisation for Economic Co-operation and Development (OECD)May also be difficult due to variables like functions performed, term of contractEssentially an indirect way to determine an appropriate return on investment/assets

10 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing:Permanent Establishment Issues

Permanent Establishment (“PE”) = a taxable presence created by a fixed place of businessIncludes substantial equipment, dependent agentsPE is an issue as PR will conduct itself as a third Party and thus, may perform:

On-site InspectionReview of production and Quality Control (QC) reportsApprove/disapprove vendors lists

Some of these functions may require PR’s presence in CM’s country

11 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing:Permanent Establishment Issues (cont’d)

ExclusionsAuxiliary or preparatory type work Comments:

PR should have no physical presence locallyCM sells products locallyCM has no authority to conclude contractsCM to carry its own entrepreneurial riskPR should not physically interfere in the manufacturing process

12 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Contract Manufacturing:Value Added Tax (VAT) Issues

European Union (EU) law is based on directives implemented in the domestic legislation of each member stateVAT is more complex for consignment CMA consignment CM is supplying servicesA buy-sell CM and a PR are liable to normal VAT rules based on the place of supply of goodsIf the PR is not registered locally (VAT), CM can:

Act as importer; andRecover import VAT paid on its VAT return

13 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

CommissionaireCommissionaire

14 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Buy/Sell Distributor Commissionaire

Country A

Country B

Conventional Distribution Structure vs. Commissionaire

Principal

Buy/SellDistributor

Title

Sales Contract

Customer Invoice

Title

PurchaseContract

Commissionaire

Commission

Sales income

Customer

Title

Agency Agreement

Principal

Sales Contract

Invoice

15 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire StructureObjectives

Business enhancementMaintains local sales effortsRetains existing client tiesCentralizes functions & risksConversion entails the centralization of many functions

Considerations must be taken into account:Changes must be invisible to customersAvoidance of perception of “downsizing” operations of the sales subsidiary

16 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaires in GeneralHow They Operate

Local distributor responsible only for product salesTitle passes directly from manufacturer to customerConversion from “buy/sell” distributor to commissionaire

Risks/functions change

17 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire StructureIncome Shift

Risk/Function Shift

B U Y / S E L L C O M M I S S I O N A I R E

Distributor Principal Commissionaire1. Economic Risk (ER)

2. Inventory Risk

3. Receivable Risk

4. Currency Risk

5. Warranty Risk

6. Sales & Marketing

7. Distribution

8. Invoicing / Back Office

9. After Market Service

1. Increased ER

2. Inventory Risk

3. Receivable Risk

4. Currency Risk

5. Warranty Risk

6. Distribution

7. Invoicing / Back Office

1. Sales & Marketing

2. After Market Service (optional)

18 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaires in GeneralHow They Operate

CommissionaireActs in own name on behalf of principalMay or may not mention principal in contract with customerMay account gross or net

19 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire:Conversion IssuesCommissionaire:

Conversion Issues

20 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

CommissionaireConversion Issues

GoodwillConversion from buy/sell to commissionaire may give rise to taxable sale of goodwill or other intangiblesAssumed transfer value may be treated as a constructive dividend subject to withholding taxWith proper planning, goodwill concerns can be reducedCan taxable goodwill acquisition create amortizable asset?

21 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

CommissionaireConversion Issues

Net operating losses (NOLs)In some countries conversion may constitute a change in business/trade so as to prevent the carry-over of NOLs

22 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

CommissionaireConversion Issues

Termination compensation

Existing distribution agreement and/or local laws may require compensation be paid for terminating or modifying long-term distribution contracts

Termination compensation depends on terms of the agreement and must be on an arm's length basisIf agreement is silent then distributor would have to show it had suffered a prejudice beyond its normal business and claim damagesPayment may also be due if contractual termination clause (notice period) is not properly observedCompensation could also be due for expenses or investments made by the distributor at the request of the other party

23 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

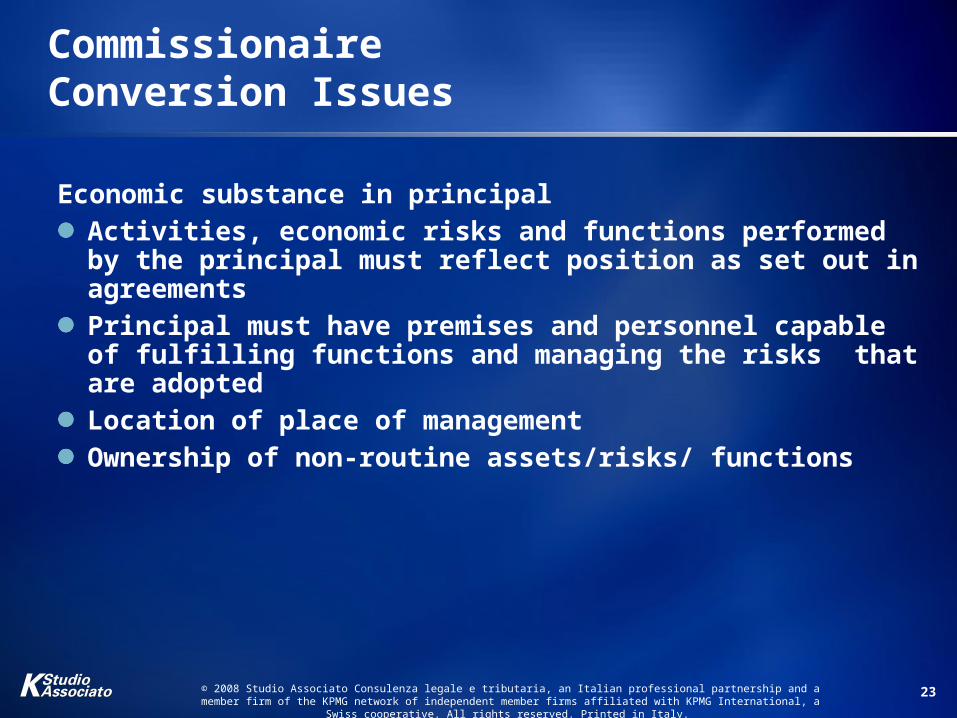

CommissionaireConversion Issues

Economic substance in principalActivities, economic risks and functions performed by the principal must reflect position as set out in agreementsPrincipal must have premises and personnel capable of fulfilling functions and managing the risks that are adoptedLocation of place of managementOwnership of non-routine assets/risks/ functions

24 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire: Maintenance and Management

Issues

Commissionaire: Maintenance and Management

Issues

25 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

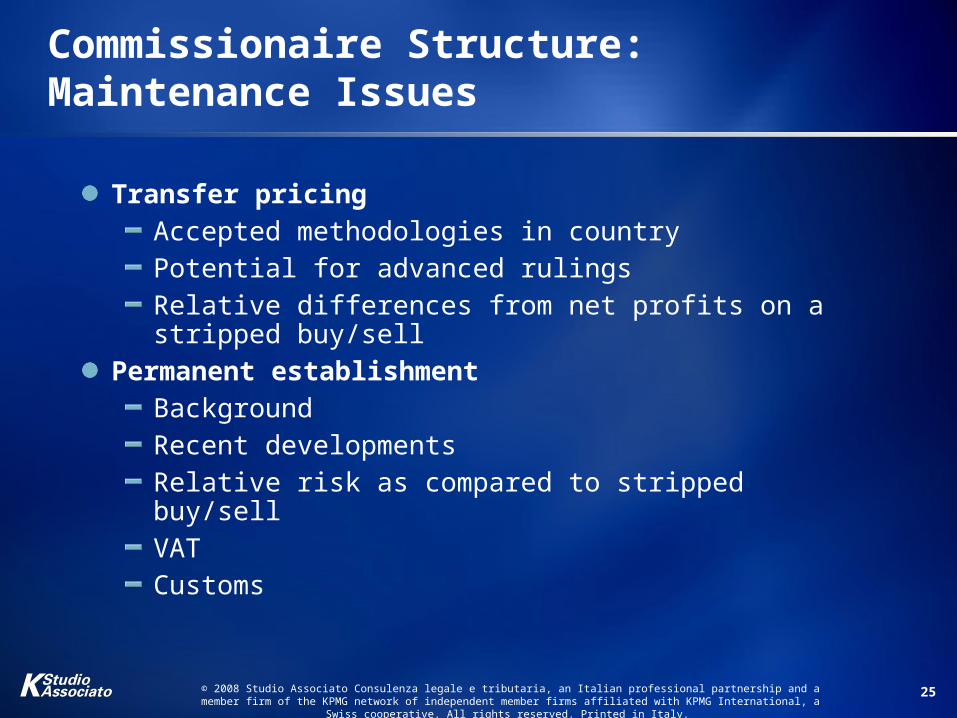

Commissionaire Structure:Maintenance Issues

Transfer pricingAccepted methodologies in countryPotential for advanced rulingsRelative differences from net profits on a stripped buy/sell

Permanent establishmentBackgroundRecent developmentsRelative risk as compared to stripped buy/sellVATCustoms

26 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire Maintenance:Transfer Pricing Considerations

Transfer pricing focus will now be on arm’s length nature of commission rate

Two most common methods cost-plusrevenue based commission

Advanced ruling possible in some countries

27 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire Maintenance:Permanent Establishment Issues

Principal could have a permanent establishment (PE) depending on

local tax law of distributor or commissionaire terms of the tax treaty

Article 5 of Model OECD TreatyPE avoided ifIndependent agentDependant agent not empowered to bind principal

28 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

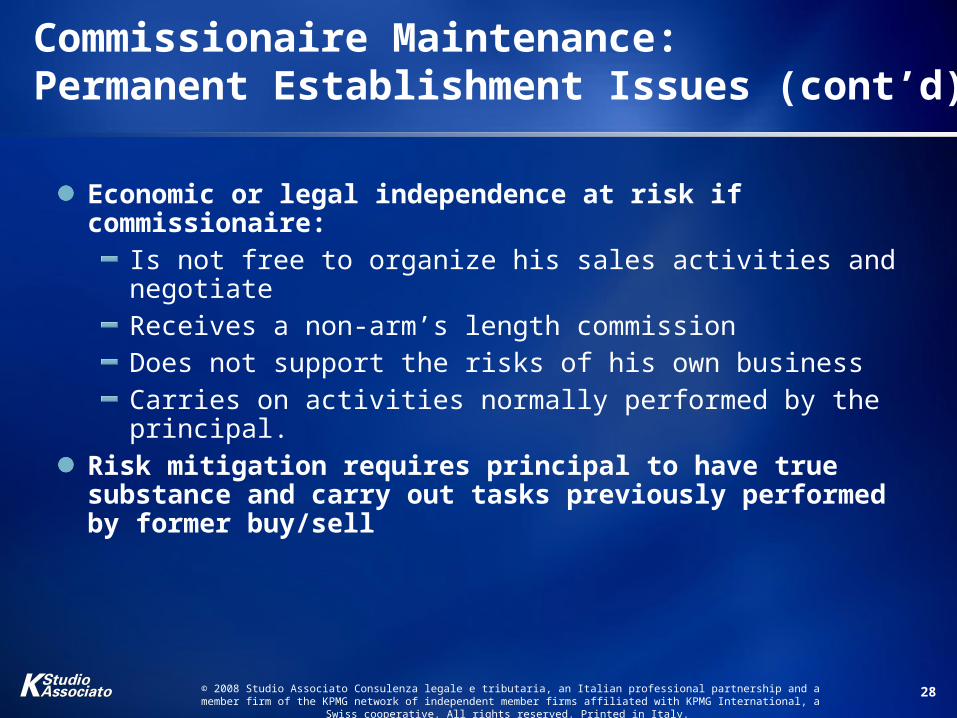

Commissionaire Maintenance:Permanent Establishment Issues (cont’d)

Economic or legal independence at risk if commissionaire:Is not free to organize his sales activities and negotiate Receives a non-arm’s length commissionDoes not support the risks of his own businessCarries on activities normally performed by the principal.

Risk mitigation requires principal to have true substance and carry out tasks previously performed by former buy/sell

29 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

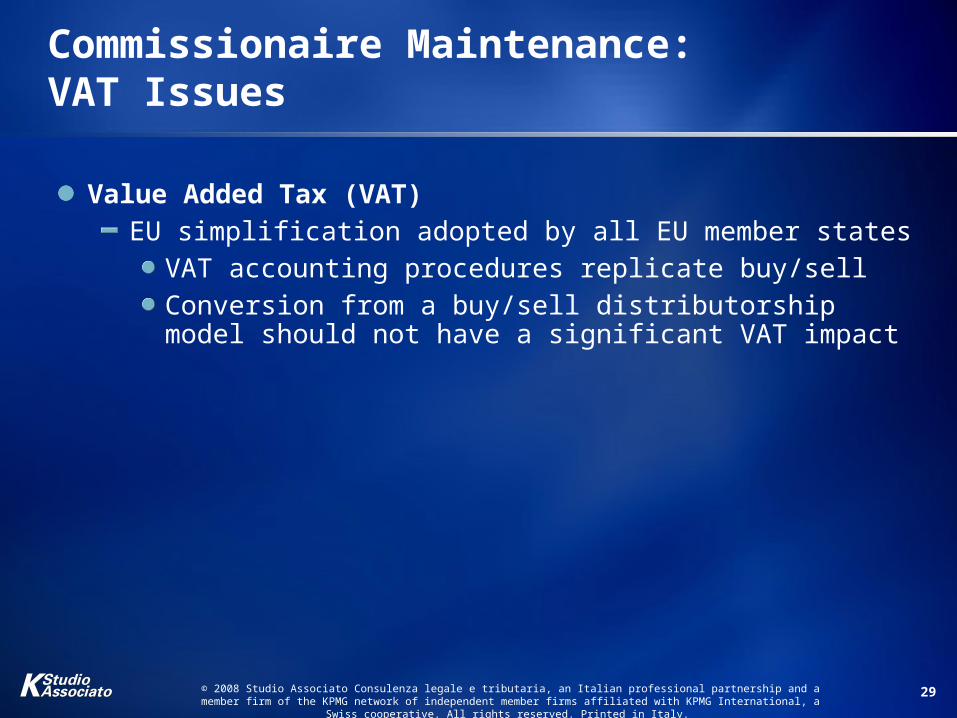

Commissionaire Maintenance:VAT Issues

Value Added Tax (VAT) EU simplification adopted by all EU member states

VAT accounting procedures replicate buy/sellConversion from a buy/sell distributorship model should not have a significant VAT impact

30 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire Maintenance:VAT Issues (cont’d)

Value Added TaxSimplified VAT accounting model

Commissionaire is deemed to buy at a price excluding their commission charge and sell at a price including their commission chargeNo VAT invoice for the commission charge should be issued by the commissionaire

European countries outside the EU may not operate a simplified structure

31 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire Maintenance: Customs Issues

Customs DutiesTriggered by the movement of goods from one customs territory to another

EU is a single customs territoryThere is no “deemed” intermediate sale from the principal to the commissionaire

This may result in the customs value (on which duties are calculated) being the full retail value

32 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Commissionaire:Customs Issues

Customs DutiesIn the buy/sell model it may be possible for the customs value to be calculated on the value attributed to the sale by the principal to the buy/sell distributorThe commissionaire structure may increase the customs duties payableThe principal may need to address registration or other customs requirements for those transactions in which the principal bears responsibility for inbound customs clearance (e.g. a delivered duty paid sale)

33 © 2008 Studio Associato Consulenza legale e tributaria, an Italian professional partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights

reserved. Printed in Italy.

Presenter’s contact details

Eugenio Graziani

KStudio Associato Consulenza

legale e tributaria

+39 045 8114111