Tax Law Updates for FS 2011

42

1 Tax Law Updates for FS 2011 TAX LAW UPDATES FOR TAX YEAR 2010 Rev 11- 05-2010

-

Upload

roanna-cox -

Category

Documents

-

view

44 -

download

0

description

Tax Law Updates for FS 2011. TAX LAW UPDATES FOR TAX YEAR 2010. Rev 11-05-2010. Tax Law Updates for FS 2011. Personal/Dependency Exemption No increase - $3,650. Rev 11-2010. Tax Law Updates for FS 2011. Standard Deduction: Single - $5,700 Married filing separately - $5,700 - PowerPoint PPT Presentation

Transcript of Tax Law Updates for FS 2011

1

Tax Law Updates for FS 2011

TAX LAW UPDATESFOR TAX YEAR 2010

Rev 11-05-2010

2

Tax Law Updates for FS 2011

Rev 11-2010

Personal/Dependency Exemption

No increase - $3,650

Tax Law Updates for FS 2011

Standard Deduction:

• Single - $5,700• Married filing separately - $5,700• Head of household - $8,400 only increased $50• Married filing jointly/Qualifying

widow(er) - $11,400

Tax Law Updates for FS 2011

Mileage Rates:

• Business Miles - 50 cents• Medical or Moving Miles – 16.5

cents• Charitable Miles - 14 cents

Tax Law Updates for FS 2011

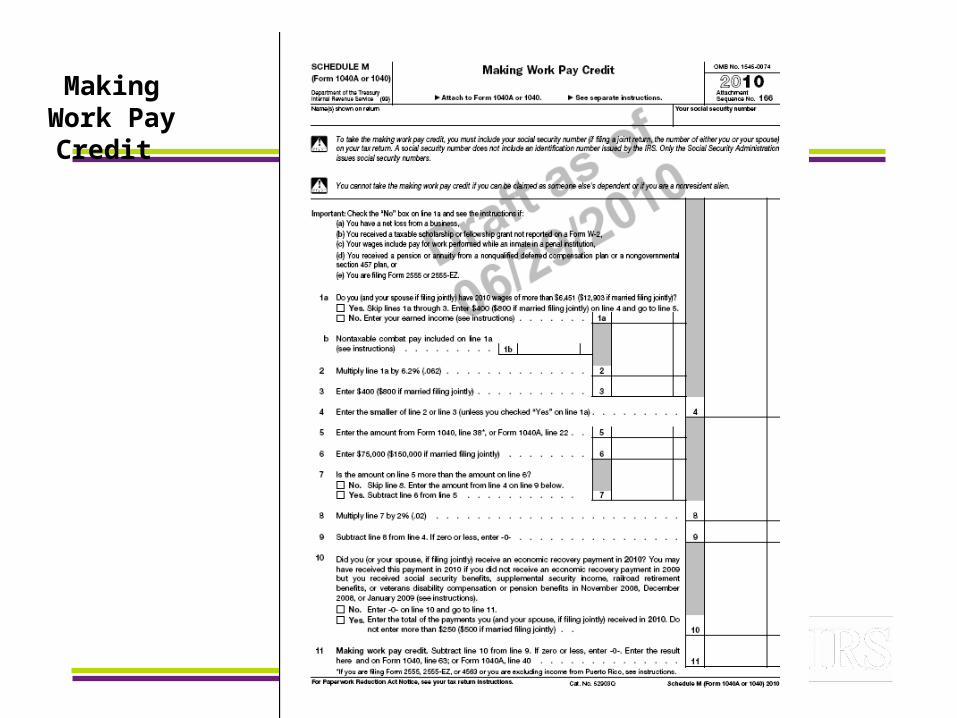

Making Work Pay Credit

Making Work Pay Credit

• Maximum credit is $400 ($800 if married filing jointly)

• Credit is refundable • Credit limited to 6.2% of earned

income• Can be employee or self-

employed• Phased out over modified AGI

range of $75,000-$95,000 ($150,000-$190,000 if married filing jointly)

• Available for tax year 2010

Making Work Pay Credit (continued)

• Taxpayer must have a social security number; if married filing jointly, at least one spouse must have SSN

• Not available to nonresident aliens, individuals who can be claimed as dependents on someone else’s tax return, or estates and trusts

1040 pg. 2Line 63

Making Work Pay Credit

Making Work Pay Credit (continued)

Any Making Work Pay Credit

must be reduced for taxpayersthat received an

Economic Recovery Paymentin 2010

Tax Law Updates for FS 2011

Temporary increase in

Earned Income Tax Credit (EITC)

Earned Income Credit

Credit percentage increases from 40% to 45% for families with 3 or more children (maximum credit is now $5,657)

Phase-out amount for married taxpayers filing jointly increases from $3,120 to $5,000

Earned Income Tax Credit (EITC) for Tax Year 2009

No. of Children Maximum Credit Earned Income/ AGI Each Less Than

0 $457 $13,460*

1 $3050 $35,535*

2 $5036 $40,363*

3 or More+ $5666 $43,352*

Taxpayers with investment income of more than $3,100 are not eligible for the credit.*Increase these amounts by $5,010 for joint return filers. And/or by the 30% additional amount for NYS credit.

EITC Awareness Day 2010

•Friday, January 28, 2011, EITC Awareness Day events

•News conferences or news releases to raise awareness of EITC and free tax preparation services

•Most volunteer return preparation sites will be open by EITC Day

•More than 60 percent of all EITC tax returns are filed during the month of February

Tax Law Updates for FS 2011

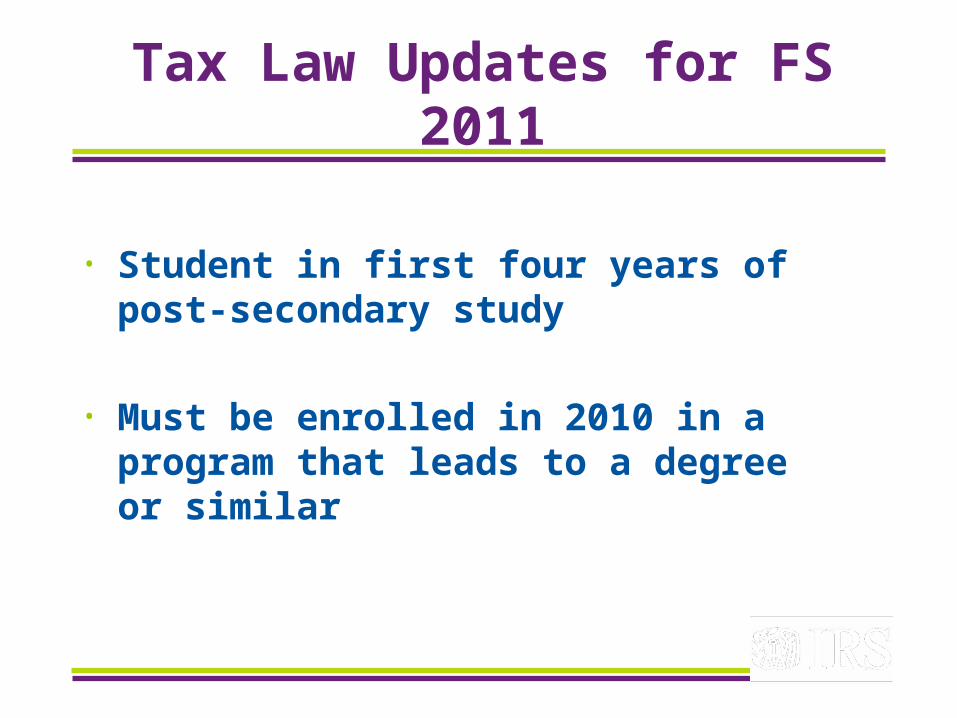

American Opportunity Credit

Tax Law Updates for FS 2011

• Student in first four years of post-secondary study

• Must be enrolled in 2010 in a program that leads to a degree or similar

Tax Law Updates for FS 2011

• Up to $2500 per student

• 100% of first $2000 and 25% of second $2000

• 40% is refundable credit (up to $1000)

1040 Page 2

Line 66

Tax Law Updates for FS 2011

Temporary increase inrefundable portion of

Child Tax Credit

Additional Child Tax Credit

The earned income threshold generally needed to qualify for the additional child tax credit decreases from $8,500 to $3,000

More people will qualify for the credit Lower threshold applies in 2009 and

2010

Tax Law Updates for FS 2011

First-TimeHomebuyer Credit

First-Time Homebuyer Credit

• Extended closing deadline from June 30, 2010 to September 30, 2010

• Purchased a qualifying home by April 30, 2010 and settle by September 30, 2010

First-Time Homebuyer Credit

(continued)

• May be eligible for a credit up to $8,000

• Documentation requirements apply

First-Time Homebuyer Credit (Continued)

• For purchases made in 2008, repayment of the credit over a 15-year period begins with the 2010 tax return.

• Minimum payment of $500

Form 5405 page 2

Tax Law Updates for FS 2011

Medicare Part D Coverage Gap

“donut hole” Rebate – $250

More information can be found on www.medicare.gov

Tax Law Updates for FS 2011

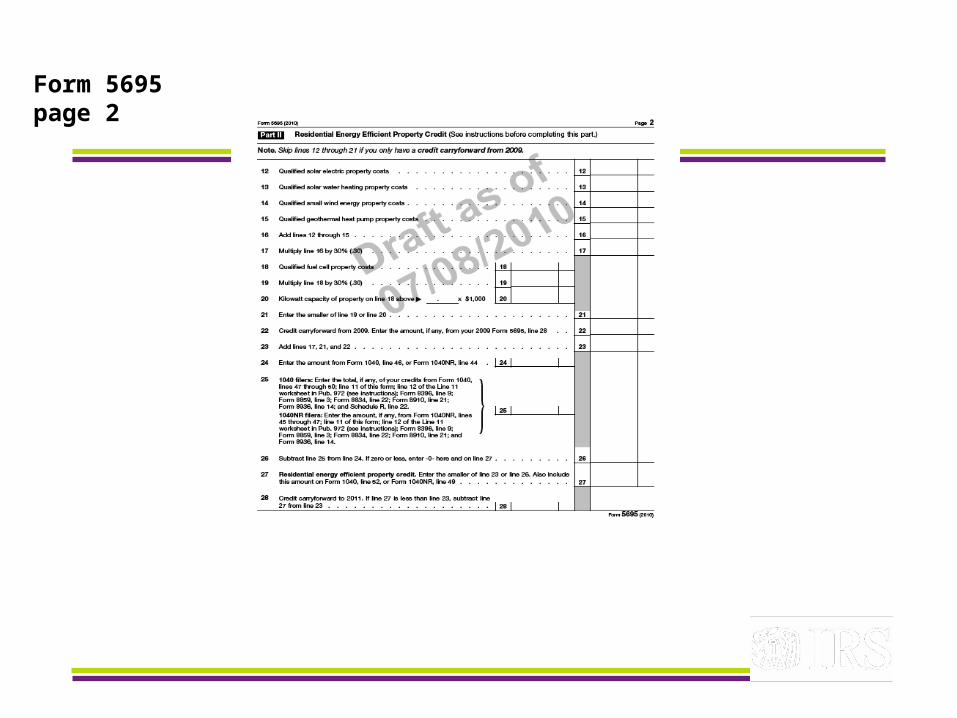

Residential Energy Credits

Residential Energy Credits

Extension and modification of credit Nonbusiness energy property: Form 5695, Part I

• Amount of credit increases from 10% to 30%• Credit limited to $1,500 for the total of all

2009 and 2010 purchases• Credit expanded to include certain asphalt

roofs and stoves that burn biomass fuel• Definition of qualifying property revised,

primarily to update energy efficiency requirements

Form 5695 page 2

Tax Law Updates for FS 2011

Basis of Inherited Property:

• No automatic increase in basis to fair market value (FMV)

• Inherited property treated as a gift

Tax Law Updates for FS 2011

Basis of Inherited Property:

• Basis of inherited property is lesser of decedent's basis or FMV

• Executor may allocate limited basis increase to some property

Tax Law Updates for FS 2011

Expiring Tax Benefits:

• Economic Recovery Payments for SSA, VA and RRB

• Special Credit for Certain

Government Retirees

Tax Law Updates for FS 2011

Expiring Tax Benefits (continued):

• Increased Standard Deduction for Real Estate taxes or net disaster loss

• Unemployment Compensation Payments

Tax Law Updates for FS 2011

Expiring Tax Benefits (continued):

• Sales Tax for Purchase of New Vehicle

• Deduction for educator expenses in figuring AGI

Tax Law Updates for FS 2011

Expiring Tax Benefits (continued):

• Itemized deduction for state and local general sales taxes

• Tuition and Fees deduction in figuring AGI

Tax Law Updates for FS 2011

Refund Option – Savings Bonds:

• Purchase Savings Bonds without a bank account

• Refund balance in paper check

• Form 8888, Allocation of Refund (including Bond Purchases)

Tax Law Updates for FS 2011

In-Scope Changes:

Schedule C, Profit or Loss from Business (Sole Proprietorship)

•Same as Schedule C-EZ•Expenses up to $10,000

Tax Law Updates for FS 2011

In-Scope Changes:

Schedule K-1 (Form 1041, Form 1065 or Form 1120S)

• Royalty income added

Tax Law Updates for FS 2011

In-Scope Changes:

Form 5329, Additional Taxes on Qualified Plans(Including IRAs) and Other Tax-Favored Accounts – Part 1

•Exceptions to additional tax on early distribution

Tax Law Updates for FS 2011

In-Scope Changes:

Cancellation of Debt (COD) – Debit Cards

Health Savings Accounts (HSAs)

Tax Law Updates for FS 2011

Form 13614-CIntake/Interview & Quality

Review Sheets

A must for preparers!

Tax Law Updates for FS 2011

QUESTIONS????

QUESTIONS???

QUESTIONS?????