Tax issues in cross border secondment of personnel ... - H... · Tax issues in cross border...

80

1 Tax issues in cross border secondment of personnel – including Service PE, ESOP Planning, Tax equalization, Hypo tax etc. H Padamchand Khincha B.com,L.L.B,FCA

Transcript of Tax issues in cross border secondment of personnel ... - H... · Tax issues in cross border...

1

Tax issues in cross border secondment of personnel – including Service PE, ESOP Planning, Tax equalization, Hypo tax etc.

H Padamchand Khincha B.com,L.L.B,FCA

2

Contents

I. ‘Secondment of Personnel’ – An Introduction II. Tax implications under domestic law

• Residential status • Incidence of tax • Short stay exemption

III. Tax implications under Treaty law • Applicability of a Treaty • Taxation rules

3

Contents…

IV. TDS consequences V. Specific issues

• Transfer pricing implications • Treatment of per diem expenses • Treatment of Social security and other statutory

deductions in home country • Treatment of ESOPs to seconded employees • Tax equalization and Hypo tax

4

Secondment of Personnel – An Introduction

• Secondment of personnel means movement of employees from one organization to another for a definite period.

• Seconded personnel are known as “expatriates”. • Deputation as per Shorter Oxford Dictionary means appointment,

assignment to an office. • Dictionary meanings of ‘deputation’ and ‘secondment’ are different.

However, in common practice, both these terms are used interchangeably [See Cholamandalam MS General Insurance Co In re 309 ITR 356].

Reasons/Causes of secondment • Globalization • Business considerations • Requirement of specialized skill and expertise • Growth Prospects

5

II. Tax Implications under domestic law

• Residential Status • Incidence of Tax • Short stay exemption

6

Residential status under domestic law

• Scope of taxation under the IT Act depends upon residential status of an assessee.

• Physical presence in a previous year in India determines the residential status of the seconded employee.

Residential status of a seconded personnel

Non-Resident (NR) Resident

Section 6(1)

Resident but not Ordinarily resident

(RNOR)

Section 6(6)

Section 2(30) Resident and Ordinarily resident

(ROR)

Classification

7

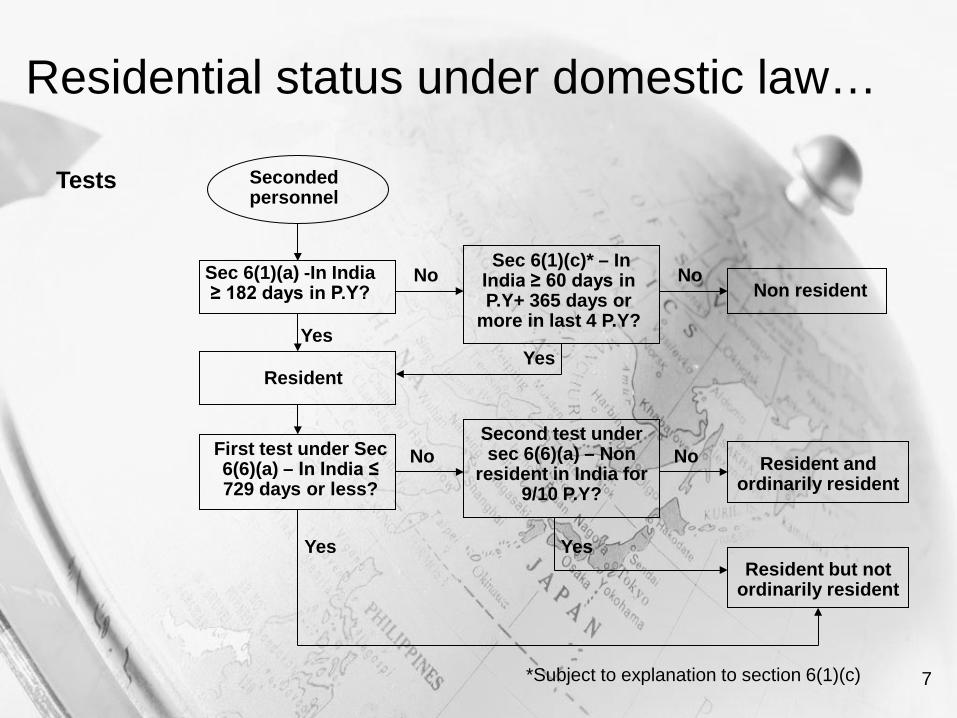

Residential status under domestic law…

Seconded personnel

Sec 6(1)(a) -In India ≥ 182 days in P.Y?

Yes

Resident

No Sec 6(1)(c)* – In India ≥ 60 days in P.Y+ 365 days or

more in last 4 P.Y?

No Non resident

First test under Sec 6(6)(a) – In India ≤ 729 days or less?

No

Yes

Second test under sec 6(6)(a) – Non

resident in India for 9/10 P.Y?

Resident and ordinarily resident

No

Yes Resident but not

ordinarily resident

Yes

Tests

*Subject to explanation to section 6(1)(c)

8

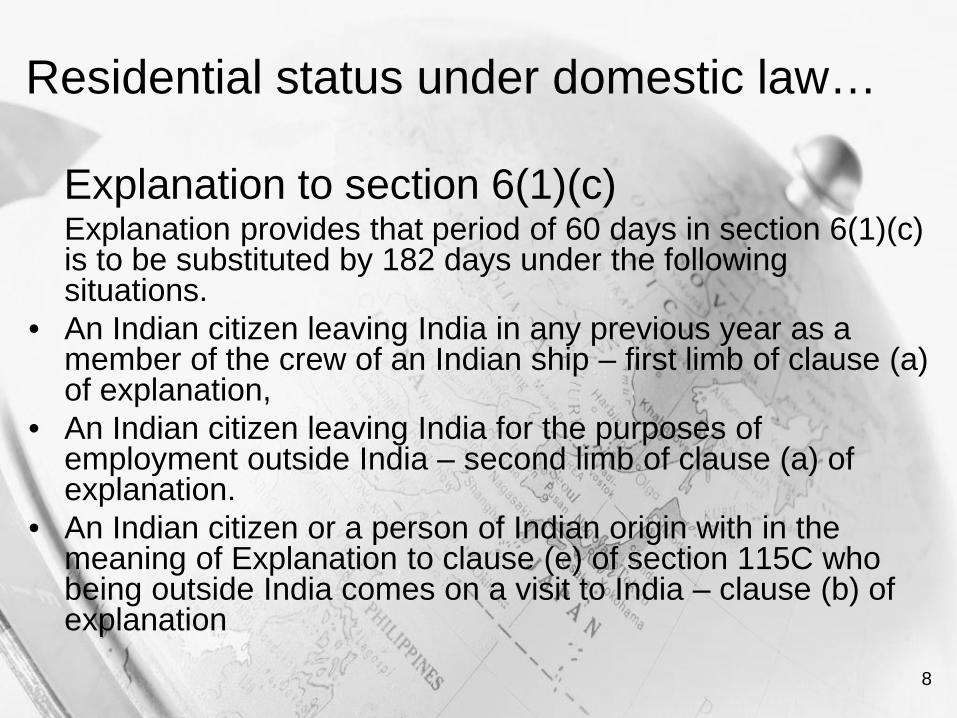

Residential status under domestic law…

Explanation to section 6(1)(c) Explanation provides that period of 60 days in section 6(1)(c)

is to be substituted by 182 days under the following situations.

• An Indian citizen leaving India in any previous year as a member of the crew of an Indian ship – first limb of clause (a) of explanation,

• An Indian citizen leaving India for the purposes of employment outside India – second limb of clause (a) of explanation.

• An Indian citizen or a person of Indian origin with in the meaning of Explanation to clause (e) of section 115C who being outside India comes on a visit to India – clause (b) of explanation

9

Residential status under domestic law…

Meaning of the expression ‘for the purposes of employment outside India’

– Dictionary meaning of the term ‘employment’ is an activity in which a person is engaged, a special errand or task.

– Considering the dictionary meaning of the term employment, an employee who renders service abroad, under a contract of service, could fall with in the meaning of the expression ‘for the purposes of employment outside India’.

– Special Bench of Mumbai Tribunal in ITO v. Abbott Industries 31 ITD 183 (Mum)(SB) held that “employment outside India” refers to “posting” outside India permanently or temporarily. A foreign tour does not imply employment outside India.

10

Residential status under domestic law…

– AAR ruling in British India Pvt Ltd In re 285 ITR 218 supports the view that a employee leaving India under deputation would be regarded as a person who leaves India for the purpose of employment under explanation (a) to section 6(1)(c). It is not required that a person would have to unemployed for getting covered under the explanation.

– Bangalore Tribunal in Ramsagar Choudhary’s case 31 ITD 21 held that explanation is attracted even when the employee has been sent on deputation.

Contrary view – The expression ‘for the purposes of employment outside India’ means

leaving India for taking up an employment. It does not apply to a person who is sent abroad by his employer for taking up an assignment. This view is forthcoming from the decision of the Bangalore Tribunal in ITO v. Dr. M.P. Konanhalli 55 ITD 266.

Meaning of the expression ‘person of Indian origin’ – Either of parents or grand parents born in undivided India [Circular No

554 dated 13/02/1990: 183 ITR St 130]

11

Residential status under domestic law…

• Computation of number of days presence in India • No Specific rules in the IT Act

Days to be included Days to be excluded

• Part of a day • Day of arrival and day of departure - Advance Ruling in P. No 1995 In re (1997) 223 ITR 462 • Contrary decisions in – ITO v. Fausta C Cordeiro ITA No 4933/Mum/2011 (Mum), ITO v. Gautam Banerjee ITA No 2374/Mum/2011 and CIT v. Manoj Kumar Reddy 245 CTR 350 (Kar)

• Transit between two different point outside the State of activity if the individual is present in the State of activity for less than 24 hours – OECD guidelines

12

Residential status under domestic law…

Decision of Karnataka High Court in CIT v. Manoj Kumar Reddy case (2011) 245 CTR 350

• High Court approved the decision of Bangalore Tribunal reported in 34 SOT 180 • The Tribunal findings were:

– Clause (b) of Explanation to section 6(1)(c) is not applicable in cases where an Indian citizen comes to India in a previous year after completing deputation outside India. Under such circumstances, one has to see whether the said employee satisfies the tests prescribed in section 6(1)(a) or section 6(1)(c).

– For the purpose of computing the period of 60 days as mentioned in section 6(1)(c), the period of any prior visits to India in the same previous year is to be excluded.

– Two views are possible with regard to the issues whether fraction of a day has to be considered while determining the physical presence in India.

– Day of arrival to be ignored while computing physical presence in India.

13

Residential status under domestic law…

Determination of residential status – Case studies (1) Mr Mohit, an Indian citizen deputed by XYZ Ltd to USA.

During previous year 2012-13, he comes to visit his family on 04-07-2012. He leaves back to USA on 20-09-2012.

(2) Mr Mohit comes back to India permanently after completing his deputation on 31-01-2013. He lands in India at 11.30 PM.

14

Incidence of Tax under IT Act

Residential Status Income liable to tax in India

Resident and ordinarily resident • Global income during the previous year – section 5(1)

Resident but not ordinarily resident

• Income received or deemed to be received in India during the previous year – sec 5(1)(a) • Income accrued or deemed to accrue or arise in India during the previous year – section 5(1)(b) • Income accruing or arising outside India during the previous year – taxable only if income accrues or arises outside India from a business controlled from India or a profession set up in India as per proviso to section 5(1)(c).

Non Resident • Income received or deemed to received in India during the previous year – section 5(2)(a) • Income accrued or deemed to accrue or arise in India during the previous year – section 5(2)(b)

15

Incidence of Tax under IT Act….

• Section 9 defines Income deemed to accrue or arise in India • Income falling under the head ‘salary’ is deemed to accrue or

arise in India if it is earned in India- Section 9(1)(ii) • Salary is ‘earned in India’ if the services have been rendered

in India – clause (a) of explanation to section 9(1)(ii) • Payment for rest period or leave preceded and succeeded by

services rendered in India if forms part of the service contract of employment would also constitute income earned in India – clause (b) of explanation to section 9(1)(ii)

16

Incidence of Tax under IT Act…

• Place of execution of employment contract, place of receipt of salary are irrelevant if services have been rendered in India.

• Supreme Court in Sedco Forex International Drill Inc 279 ITR 310 observed “Therefore with this Explanation, irrespective of where the contract was entered into or where the liability to pay arose or where the payment was actually received, if the service was rendered in India, the salary for such service was exigible to tax as income under the Act”

• Home salary of an expatriate in connection with rendition of services in India deemed to accrue or arise in India – Hindustan Power Plus Ltd In re 271 ITR 433 (AAR), CIT v. Eli Lilly and Co (India) P. Ltd. (SC) 312 ITR 225

17

Short Stay Exemption

• Section 10(6)(vi) grants an exemption from taxation in India to a foreign citizen rendering services in India.

Cumulative Conditions: – He should be an employee of foreign enterprise – Remuneration should be received from a foreign enterprise – Foreign enterprise is not engaged in any trade or business in India – Stay in India ≤ 90 days in aggregate in any previous year – Remuneration paid should not be liable to be deducted from the

income of the employer chargeable under IT Act. Amount paid to employees of a foreign co by an Indian co for meeting incidental expenses while rendering services to it in India constitutes remuneration exempt under section 10(6)(iv) - CIT v. Bharat Heavy

Electricals 252 ITR 218 (Del)

18

Tax implications under Treaty law

• Applicability of a Treaty • Taxation Rules under the Treaty

19

Applicability of a Treaty

• Resort to Treaty provisions only if it is more beneficial to the assessee – Section 90(2)

• Production of tax residence certificate is must for availing benefit of Treaty provisions – Section 90(4)

• Seconded personnel must be a resident of any of the contracting States.

20

Applicability of a Treaty Determination of Residence • Residential status is determined in accordance with the domestic law of

the contracting States. The treaties generally prescribe the determination of residential status with reference to domicile, residence, citizenship, place of incorporation, place of management or any other criterion of similar nature.

• Article 4 (1) of the OECD Model Reads as under– “Resident of Contracting State means any person who under the laws of

that State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature, and also includes that State and any political subdivision or local authority thereof. This term, however, does not include any person who is liable to tax in that State in respect only of income from sources in that State or capital situated therein.”

• If the seconded personnel turns out to be a resident of both the contracting States, apply tie breaker rules.

21

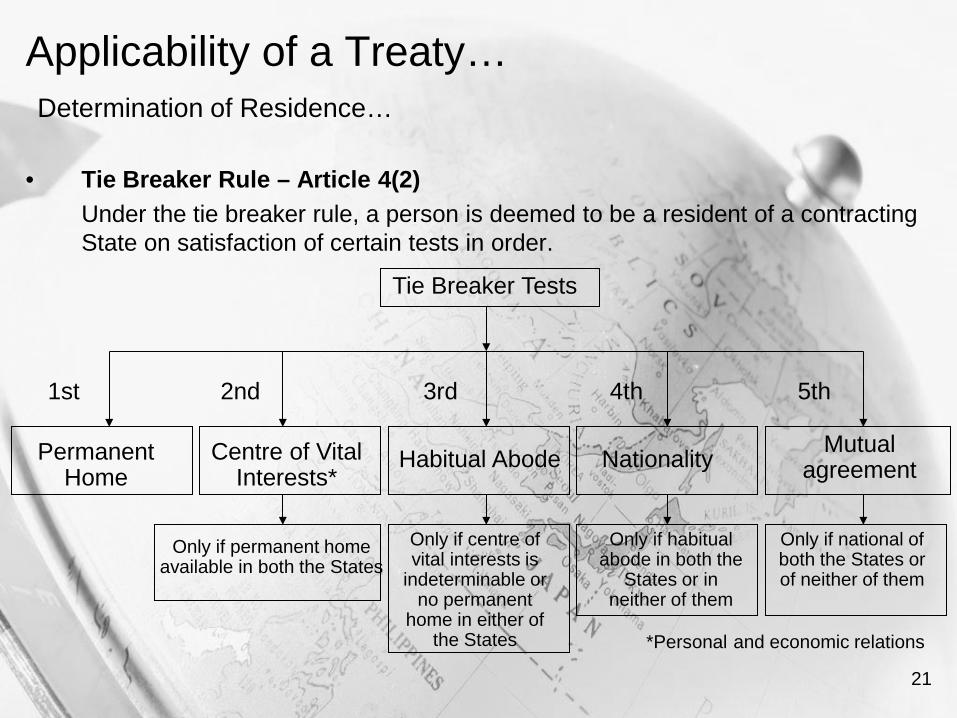

Applicability of a Treaty… Determination of Residence…

• Tie Breaker Rule – Article 4(2) Under the tie breaker rule, a person is deemed to be a resident of a contracting

State on satisfaction of certain tests in order.

Tie Breaker Tests

Permanent Home

Centre of Vital Interests*

Habitual Abode Nationality Mutual agreement

1st 2nd 3rd 4th 5th

*Personal and economic relations

Only if permanent home available in both the States

Only if centre of vital interests is

indeterminable or no permanent

home in either of the States

Only if habitual abode in both the

States or in neither of them

Only if national of both the States or of neither of them

22

Applicability of a Treaty… Determination of Residence…

• ‘Permanent home available to the Individual’ – OECD Views: ‘As regards the concept of home, it should be observed that

any form of home may be taken into account (house or apartment belonging to or rented b the individual, rented furnished room). But the permanence of the home is essential; this means that the individual has arranged to have the dwelling available to him at all times continuously, and not occasionally for the purposes of a stay which, owing to reasons for it, is necessary for short duration (travel for pleasure, business travel, educational travel, attending a course at a school, etc.)’

– Length of stay not relevant for determining permanence aspect. – Ruling of AAR in Rajnikant Bhatt 222 ITR 562 - House provided by foreign

employer in the country of deputation can be claimed as a permanent home as the same is available to him continuously.

23

Applicability of a Treaty… Determination of Residence…

• Centre of Vital interests – Center of vital interest are linked to the individual’s personal and economic

interest as demonstrated by his personal, social, family, cultural connections. – OECD View: ‘If the individual has a permanent home in both Contracting

States, it is necessary to look at the facts in order to ascertain with which of the two States his personal and economic relations are closer. Thus, regard will be had to his family and social relations, his occupations, his political, cultural or other activities, his place of business, the place from which he administers his property, etc. The circumstances must be examined as a whole, but it is nevertheless obvious that considerations based on the personal acts of the individual must receive special attention. If a person who has a home in one State sets up a second in the other State while retaining the first, the fact that he retains the first in the environment where he has always lived, where he has worked, and where he has his family and possessions, can, together with other elements, go to demonstrate that he has retained his centre of vital interests in the first State.”

– AAR in Mohsinally Alimohammed Rafik, In Re 213 ITR 317 held that the centre of vital interest was in Dubai, where Mr. Rafik had been carrying out his economic activities and had been staying with his wife and children.

24

Taxation Rules under the Treaty

25

Taxation Rules Article 15(1)

• General Rule – Article 15(1) of OECD Model Convention - Taxability in the State where employment is exercised

• Article 15(1) of the OECD Model Convention – Right of taxation of salary, wages and other similar remuneration derived by a resident of a Contracting State in respect of an employment rests with State of residence unless the employment is exercised in the other State. If the employment is exercised in the other State then the said State has the right of taxation.

• Critical expressions ‘in respect of an employment’ and ‘exercise of employment’.

• The expression ‘In respect of an employment’ denotes that only remuneration arising out of employer-employee relationship would be covered under this Article.

26

Taxation Rules… Article 15(1)…

“Employment is exercised” – Connotation • OECD Model Commentary - Employment is exercised at the

place where the employee is physically present when performing the activities for which the employment income is paid.

• US Model Commentary – Employment exercised means services performed

• Time or place of payment of Salary, wages or other similar remuneration is irrelevant as long as the remuneration pertains to employment exercised in the Other State.

• The place where the results of the work are exploited is irrelevant

27

Taxation Rules… Article 15(2)

• Specific Rule – Article 15(2) of OECD Model Convention - Taxability arises only in State of residence even if employment is exercised in the other State.

• Article 15(2) facilitates short term secondment. • Conditions:

– the recipient is present in the other State for a period or periods not exceeding in the aggregate 183 days in any 12 month period* commencing or ending in the fiscal year concerned;

– the remuneration is paid by, or on behalf of, an employer who is not a resident of the other State; and

– the remuneration is not borne by a permanent establishment or a fixed base which the employer has in the other State.

*This period of stay is only indicative. The Contracting States are not bound to adopt the same.

28

Taxation Rules… Article 15(2)…

First condition – present for 183 days or more: OECD Model – “days of physical presence” method Inclusions – part of a day; day of arrival/ departure; – all other days spent inside the State of activity such as Saturdays and

Sundays, national holidays, holidays before, during and after the activity, short breaks (training, strikes, lockout, delays in supplies), days of sickness and death or sickness in the family

Exclusions: – Days in transit – Any entire day spent outside the State of Source, whether for

holidays, business trips, or any other reason, should not be taken into account

29

Taxation Rules… Article 15(2)…

• Case Study – Mr Rohit was in India from 01-04-2012 to 10-01-2013. On 11-01-2013, he was hired by XYZ Inc who is a resident of USA. On the same day he moved to USA. On 15-02-2013, Mr Mohit was sent to India on a deputation.

• Issue – whether the period of stay in India during 01-04-2012 to 10-01-2013 is to be considered for determining the period of stay in terms of Article 16(2)(a) of the India-USA Treaty?

• OECD view: “Days during which the taxpayer is a resident of the source State should not,

however be taken into account in the calculation. Subparagraph a) has to be read in the context of the first part of paragraph 2, which refers to “remuneration derived by a resident of a Contracting State in respect of an employment exercised in the other Contracting State”, which does not apply to a person who resides and works in the same State. The words “recipient is present”, found in subparagraph a), refer to the recipient of such remuneration and, during a period of residence in the source State, a person cannot be said to be the recipient of remuneration derived by a resident of a Contracting State in respect of an employment exercised in the other Contracting State.”

30

Taxation Rules… Article 15(2)…

Second Condition – the remuneration is paid by, or on behalf of, an employer who is not a resident of the other State*.

• Meaning of the term ‘employer’ is critical as there are occasions when seconded employees are on the rolls of a non-resident employer but in essence work as per the directions and under the supervision of an enterprise to whom he has been seconded and yet claims short stay exemption. – Short stay exemption under Article 15(2) available for remuneration for

‘contract of service’ and not for ‘contract for service’. – Klaus Vogel on Double Taxation Conventions [3rd edition observations at page

899] “..an employer is someone to whom an employee is committed to supply his capacity to work and under whose direction the latter engages in his activities and whose instructions he is bound to obey. This definition is also in accordance with the international understanding of the term employer.”

– ‘Control and command’ are important features of an employer - CIT v. Dalmia 207 ITR 267 (Cal), Ram Prasad v. CIT 86 ITR 122 (SC), Dharmangadha Commercial Works v. State of Saurashtra 1957 SCR 152

*The language employed may not be same in all the treaties. For instance, Article 16(2)(b) of India – Norway DTAA reads as “the remuneration is paid by, or on behalf of, an employer who is a resident of the State of which the recipient is a resident.”

31

Taxation Rules… Article 15(2)…

– Bangalore Tribunal in Abbey Business Services (P.) Ltd v. DCIT (2012) 6 TaxCorp (A.T.) 28944 (BANGALORE) observed

“..it is necessary to discuss and evaluate as to who can be regarded as an employer, employee and the relation between employer and employee. As per Shorter Oxford English dictionary, 'employer' means 'a person who employs or makes use of a person or an organization that pays someone to do work on a regular or contractual basis' and the term 'employee' means 'a person who works for an employer.' An employee is a person who works under the direct control, supervision and direction of another person called an employer who exercises such authority over the employee. The employee not only receives instructions from his employer but is also subject to the right of the employer to control the manner in which he should carry out such instructions. A significant feature of employer-employee relationship being 'control and command’.”

32

Taxation Rules… Article 15(2)…

– Factors suggested by OECD in Commentary to determine whether seconded employee actually renders services to his formal employer or whether the enterprise to which services are provided in host country is the real employer:

(i) who has the authority to instruct the individual regarding the manner in which the work has to be performed;

(ii) who controls and has responsibility for the place at which the work is performed;

(iii) the remuneration of the individual is directly charged by the formal employer to

the enterprise to which the services are provided (see paragraph 8.15 below); (iv) who puts the tools and materials necessary for the work at the individual’s

disposal; (v) who determines the number and qualifications of the individuals performing

the work; (vi)who has the right to select the individual who will perform the work and to

terminate the contractual arrangements entered into with that individual for that purpose;

(vii) who has the right to impose disciplinary sanctions related to the work of that individual;

(viii) who determines the holidays and work schedule of that individual

33

Taxation Rules… Article 15(2)…

• Examples in OECD commentary where seconded employee is not regarded as employee of enterprise to whom he has been seconded

1. A co, a company resident of State A, concludes a contract with B co, a

company resident of State B, for the provision of training services. A co is specialised in training people in the use of various computer software and B co wishes to train its personnel to use recently acquired software. X, an employee of A co who is a resident of State A, is sent to B co’s offices in State B to provide training courses as part of the contract.

2. C co, a company resident of State C, is the parent company of a group of

companies that includes D co, a company resident of State D. C co has developed a new worldwide marketing strategy for the products of the group. In order to ensure that the strategy is well understood and followed by D co, which sells the group’s products, C co sends X, one of its employees who has worked on the development of the strategy, to work in D co’s headquarters for four months in order to advise D co with respect to its marketing and to ensure that D co’s communications department understands and complies with the worldwide marketing strategy.

34

Taxation Rules… Article 15(2)…

• Examples in OECD commentary where seconded employee is regarded as employee of enterprise to whom he has been seconded 1. A multinational owns and operates hotels worldwide through a number of

subsidiaries. Eco, one of these subsidiaries, is a resident of State E where it owns and operates a hotel. X is an employee of Eco who works in this hotel. F co, another subsidiary of the group, owns and operates a hotel in State F where there is a shortage of employees with foreign language skills. For that reason, X is sent to work for five months at the reception desk of F co’s hotel. F co pays the travel expenses of X, who remains formally employed and paid by Eco, and pays Eco a management fee based on X’s remuneration, social contributions and other employment benefits for the relevant period.

2. I co is a company resident of State I specialised in providing engineering services. I co employs a number of engineers on a full time basis. J co, a smaller engineering firm resident of State J, needs the temporary services of an engineer to complete a contract on a construction site in State J. I co agrees with J co that one of I co’s engineers, who is a resident of State I momentarily not assigned to any contract concluded by I co, will work for four months on J co’s contract under the direct supervision and control of one of J co’s senior engineers. J co will pay I co an amount equal to the remuneration, social contributions, travel expenses and other employment benefits of that engineer for the relevant period, together with a 5 percent commission. J co also agrees to indemnify I co for any eventual claims related to the engineer’s work during that period of time

35

Taxation Rules… Article 15(2)…

Decisions where it has been held that the host country entity constitute real and economic employer of seconded employees for the reason that the said entity had the control and command over the seconded employees: – HCL Info systems Ltd. vs. DCIT : 76 TTJ 505 (Del) (affirmed by the Delhi High

Court in 274 ITR 261), IDS Software Solutions India Pvt. Ltd. v. ITO: 122 TTJ 410 (Bang.), Cholamandalam MS, In re: (2009) 178 Taxman 100 (AAR), Abbey Business Services (P.) Ltd v. DCIT (2012) 6 TaxCorp (A.T.) 28944 (Bang)

Contrary view: – Supreme Court in DIT v. Morgan Stanley 292 ITR 416 held that in case of

deputation, the entity to whom the employees have been deputed cannot be regarded as employer of such employees as the employees continue to have lien on his employment with the entity which deputes him.

– Entity seconding the employee is the employer as it retained the right over seconded employee – AT & S India Pvt Ltd 287 ITR 421

36

Taxation Rules… Article 15(2)…

Third Condition - “The remuneration is not borne by a permanent establishment which the employer has in the other State.” – The word ‘borne by’ is not defined in the DTA. – Whether this refers to the commercial aspects (i.e., bearing the cash flow /

liability) or the tax aspects (i.e., claim of such expenditure as an allowable deduction).

– Para 2 of Article 3 - Any term not defined therein shall, unless the context otherwise requires, have the meaning which it has under the laws of that State.

– As per Supreme Court in CIT v. Dalhousie Properties Ltd. [1984] 149 ITR 708 (SC) “The expression ‘borne’ may refer to either the liability which a person is liable to discharge or the actual sum paid by him in discharge of that liability.”

– Going by the meaning of the term ‘borne by’ as propounded by the Supreme Court, one may state that the exemption from taxation under this Article may not be available to the employee in the source State if the liability to pay remuneration of the said employee rests on the permanent establishment of the employer.

37

Taxation Rules… Article 15(2)…

• However, OECD commentary on Article 15 suggests that the term ‘borne by’ refers to the aspect of deduction of remuneration as an expense. If the Permanent establishment of the employer claims the remuneration as a deduction then the employee would not be eligible for exemption under Article 15(2).

• OECD observations – “…The phrase “borne by” must be interpreted in the light of the underlying purpose of sub-paragraph c) of the Article, which is to ensure that the exception provided for in paragraph 2 does not apply to remuneration that could give rise to a deduction, having regard to the principles of Article 7 and the nature of the remuneration, in computing the profits of a permanent establishment situated in the State in which the employment is exercised.”

38

Taxation Rules…

• India’s reservations on Article 15(2) of the OECD Model Convention: – India reserves the right to decide the period of stay

through bilateral negotiations. – Disagrees with the interpretation set out in paragraph 6.2

of the commentary on Article 15(2) of the OECD Model convention wherein a partner is recognized as an employer in the case of fiscally transparent entities.

39

TDS Consequences

40

TDS consequences

(A) Payments to seconded employees – Obligation u/s 192 – Payment received by seconded employees from his employer constitute

salary – TDS obligation under section 192(1) if payment is chargeable under the

head ‘salaries’ in India. – Obligation to deduct tax at source (TAS) is on any person responsible to

make payment chargeable under the head ‘salaries’. – Significance of the word ‘any’? ‘Any’ includes all [G. Narsingh Das

Agarwal v. UOI, [1967] 1 MLJ 197] – ‘Employer’ is the ‘person responsible for paying’ - section 204(i) – Any employer – would include formal as well as real employer. – Liability arises at the time of payment of salary. No payment, no liability

to deduct tax at source.

41

TDS consequences… Obligation u/s 192…

– Non resident / Foreign employer also covered - P. No. 13 of 1995, In re, [1997] 228 ITR 487 (AAR)

– Home salary received for rendering services in India, employer making the payment, liable to deduct tax under section 192(1).

Dual employment: – Dual employment covered in section 192(2). If information is furnished to

chosen employer, then the said employer is under an obligation to consider the information while discharging the obligation under section 192(1).

– As per the Supreme Court decision in CIT v. Morgan Stanley 292 ITR 416, an employee seconded / deputed to foreign entity continues to have a lien over the employment with the employer in the home country. If the foreign entity commands and supervises the work of the seconded employee then it would be regarded as the economic employer of the said employee. As a result the seconded employee would be considered as a person having dual employment.

42

TDS consequences… Obligation u/s 192…

– Receipt of salary from formal employer in home country - Entity to whom employees are seconded would be liable to deduct TAS if information pertaining to home salary is furnished by employees - [ Refer Circular No 8/2012, CIT v. Woodward Governor 295 ITR 1 (Del)]

Decision in Eli Lily case In CIT v. Eli Lily (Company) Pvt Ltd 312 ITR 225, the Supreme Court

held that entity to whom employees are seconded are under an obligation to deduct TAS from salaries paid in home country by the formal employer.

Points not considered in the decision: (i) No information regarding home salary was furnished by the

seconded employees. (ii) Decision purely based on import of section 192(1) read with section

9(1)(ii).

43

TDS consequences… Obligation u/s 192…

(iii) Stipulations of section 192(2) and section 204(i) not considered. Interesting development: Subsequent to Eli Lily decision, Supreme Court dismissed the special

leave petition of the revenue against the decision of the Delhi High Court in CIT v. Kinetics Technology ITA No. 541 of 2005 [Refer 321 ITR (St.) 167]. The Delhi High Court in the said decision had affirmed the order of Delhi Tribunal (reported in 94 TTJ 1). The Tribunal in its order had cancelled the penalty under 271C(1)(a) by holding that the present employer cannot be held responsible for not deducting tax on salaries received from the other employer by expatriates in their home country if the details of such salary were not furnished to the present employer under section 192(2).

44

TDS consequences…

(B)Payments to enterprise seconding employees – Obligation u/s 195 – Liability under section 195 only if sum paid is chargeable

to tax in India – Payment of salaries not covered under section 195. – Situations where question of TDS liability arises:

(i) Payment of fees by an enterprise (Indian entity) to foreign entity for seconding employees

(ii) Reimbursement of salaries to the entity seconding the employees (foreign entity) from the entity to whom employees have been seconded (Indian entity).

45

TDS consequences… Obligation u/s 195…

(i) Payment of a fees by an enterprise (Indian entity) to foreign company for seconding employees: – Fees may constitute technical services under section 9(1)(vii). – Definition of ‘fees for technical services’ under explanation 2 to section

9(1)(vii) of IT Act reads as under: “For the purposes of this clause, "fees for technical services" means

any consideration (including any lump sum consideration) for the rendering of any managerial, technical or consultancy services (including the provision of services of technical or other personnel) but does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head "Salaries".

– Expressions ‘managerial’, ‘technical’ and ‘consultancy’ not defined in the Act.

46

TDS consequences… Obligation u/s 195…

Expressions Dictionary Meanings and Judicial Interpretations

Managerial I. Shorter Oxford Dictionary- “pertaining to, or characteristic of a manager, esp. a professional manager of or within an organization, business, establishment, etc”.

II. “management” includes the act of managing by direction, or regulation or superintendence – CIT v. R Dalmia 106 ITR 895

Technical I. Shorter Oxford Dictionary – “Pertaining to, involving, or characteristic of a particular art, science, profession, or occupation, or the applied arts and sciences generally”

Consultancy I. Shorter Oxford Dictionary- “the work or position

of a consultant”; “a department of consultants” II. Word Web - “The practice of giving expert advice

within a particular field”.

47

TDS consequences… Obligation u/s 195…

– Nature of service rendered by foreign entity - supply of skilled manpower.

– Payment for supplying skilled manpower cannot be regarded as payment towards managerial, technical and consultancy services as per dictionary meanings of these terms.

Whether payment is towards “provision of services of technical or other personnel”?

– Expression should not be read as a standalone category. – Expression does not cover mere provision of technical or other

personnel as it happens in case of secondment of personnel. – Expression ‘services of’ contemplates rendering of services by the

technical or other personnel. – What is meant is that some sort of work is assumed through the act of

the provision of the services of the technical or other personnel. – Work in turn should answer the description of managerial, technical or

consultancy services.

48

TDS consequences… Obligation u/s 195…

• Observations of AAR in Cholamandalam MS General Insurance Co. Ltd 309 ITR 356:

“It is debatable whether the bracketted words - "including provision of services of technical or other personnel" is independent of preceding terminology - "managerial, technical or consultancy services" or whether the bracketted words are to be regarded as integral part of managerial, technical or consultancy services undertaken by the payee of fee. In other words, is the bracketted clause a stand alone provision or is it inextricably connected with the said services? HMFICL itself does not render any service of the nature of managerial, technical or consultancy to the applicant and it has not deputed its employee to carry out such services on its behalf. There is no agreement for rendering such services. In this factual situation, it is possible to contend that merely providing the service of a technical person for a specified period in mutual business interest not as a part of technical or consultancy service package but independent of it, does not fall within the ambit of S.9(1)(vii).”

49

TDS consequences… Obligation u/s 195…

– Taxability under the Treaty as ‘fees for technical service’. » Definition of ‘fees for technical services’ in different treaties. » Satisfaction of ‘make available’ condition (if applicable).

– Taxability under the Treaty as ‘business income’ » Article dealing with taxability of business income » Payment to foreign co for seconding its employees would be

taxable in the other Contracting State only if the payment is attributable to permanent establishment (PE) situated in the other Contracting State.

» What constitutes a PE is defined in the Treaty. » Generally a PE is defined to mean as a fixed place of business. » Concept of ‘Service PE’ relevant for this discussion.

50

TDS consequences…Obligation u/s 195… Concept of Service PE

When secondment of employees results in establishment of a service PE

• Rationale of a Service PE clause – to tax the enterprise of home State for its economic activities in the source State beyond a threshold limit.

• Article 5(3) of the UN Model contains the following provision as regards service PE:

“(a)… (b) The furnishing of services, including consultancy services, by an

enterprise through employees or other personnel engaged by the enterprise for such purpose, but only if activities of that nature continues (for the same or a connected project) within the country for a period or periods aggregating more than six months within any twelve month period.”

• Threshold in OECD Model – 183 days or more as against 6 months in UN model.

51

TDS consequences…Obligation u/s 195… Concept of Service PE

Conditions – Existence of ‘service provider’ and ‘recipient of services’ – Services should be furnished by an enterprise through

employees or other personnel engaged by enterprise. » Enterprise rendering services should be

responsible for the services rendered by the employees or engaged personnel.

– Services should be furnished for a period specified in treaties.

» Different threshold periods in treaties signed by India.

52

TDS consequences…Obligation u/s 195… Concept of Service PE

India-Srilanka 183 days within any 12 months period

India-Norway 6 months within any 12 months period

India-Singapore 90 days in any fiscal year

India-Australia, India-UK, India-USA 90 days within any 12 months period

India-Indonesia 91 days in any 12 months period

India-China, India-Thailand period or periods aggregating more than 183 days

Examples of threshold period in different treaties signed by India

53

TDS consequences…Obligation u/s 195… Concept of Service PE

Decision of Supreme Court in DIT v. Morgan Stanley 292 ITR 416: Background Morgan Stanley and Co. Inc (MSCo) was a US-based entity and was obtaining

services from its Indian group entity Morgan Stanley Advantages Services Pvt. Ltd (MSAS). MSCo proposed to second two types of employees to MSAS viz., stewards and deputationists.

Supreme Court held:

– Secondment for stewardship does not result in a Service PE in India in terms of Article 5 of India-USA DTAA as they are not involved in day to day management or in any specific services to be undertaken by MSAS. Stewards merely protected the interest of MSCo. MSCo does not render any services to MSAS by deputing stewards to it.

– Presence of deputationist would create a Service PE in India as MSCo was responsible for the work of the deputationist and they continued to be in the payroll of MSCo or they continue to have their lien on their jobs with MSCo.

54

TDS consequences…Obligation u/s 195… Concept of Service PE

Outcome of Morgan Stanley case: Satisfaction of following two conditions is necessary to have

a Service PE in India: (i) The foreign company is responsible for the activities

performed by the deputed employees. (ii) The employees continue to be on the payroll of the

foreign company or continue to have lien on their jobs with the foreign company.

AAR in Centrica India offshore Private Ltd In re 348 ITR 45 held that foreign co would have a Service PE in India if the deputed personnel continue to be the employee of foreign co. Reliance was placed on Morgan stanley’s

case.

55

TDS consequences…Obligation u/s 195… Reimbursement of salary

(ii) Reimbursements of salary cost incurred by foreign co: – Reimbursement refills or replaces the quantum of disbursement. – Reimbursement of a necessary disbursement is not income [Own v Pook 74 ITR 147] – Tendency of department to contend that the reimbursement represents fees for

technical services or income from business. Decisions till date are not uniform. – Arguments why reimbursement of salary does not constitute fees for technical service

or income from business and thus deduction of TAS by Indian Co is not required {Refer, inter alia, IDS Software Solutions v. ITO 122 TTJ 410, Abbey Business Services (P.) Ltd v. DCIT (2012) 6 TaxCorp (A.T.) 28944 (Bang)]: • Expats are deputed to work under the control and supervision of the Indian

Co. Foreign Co is not responsible for the actions of the expats. Thus, Foreign Co does not render any technical service to the Indian Co.

• Since payment by Indian Co is towards reimbursement of salary cost borne by Foreign Co, no income can be said to accrue to Foreign Co in India.

• Referring to Klaus Vogel’s commentary and the relevant facts, Indian Co could be regarded as an ‘economic employer’ of the secondees. Secondment agreement constitutes an independent contract of service.

• Since the deputed employees were not subject to the control and supervision of the Foreign Co, there would be no Service PE and thus question of taxability of the reimbursement as business income would also not arise.

56

TDS consequences…Obligation u/s 195… Reimbursement of salary…

– Arguments supporting deduction of TAS by Indian Co [Refer AT&S India Pvt Ltd 287 ITR 421 (AAR), Verizon Data Services India P ltd In re 337 ITR 192 (AAR)]

• Foreign Co is the real employer of the secondees as it retains right over the employees and has power to remove/replace them

• Pursuant to foreign collaboration agreement, Foreign Co had undertaken to render the services to Indian Co and hence, lent the services of its seconded employees on payment of compensation by Indian Co.

• The recipient of the compensation was Foreign Co and not the seconded employees. Further, the payment was not merely reimbursement of salary, it also included other costs

• Thus, compensation referred to in the secondment agreement was for rendering ‘services of technical or other personnel’ —hence taxable as FTS and liable to withholding of tax u/s.195.

Decision in AT&S India Pvt Ltd have been distinguished by Bangalore Tribunal in IDS software solution case and Abbey Business services case.

57

TDS consequences…Obligation u/s 195… Reimbursement of salary…

Recent decisions: – Decision of Madras High Court in Verizon Data Services India (P) Ltd.

v. Authority for Advance Rulings and Ors. 346 ITR 489: • The High Court upheld the ruling of AAR wherein it held that the

reimbursement of salary of expatriates to foreign co by Indian co results in taxable income in the hands of the foreign co. The High Court also upheld the observations of AAR wherein it characterised the secondment of personnel as provision of managerial services.

• However, the High Court set aside the ruling of AAR wherein it held that the reimbursement of salary of expatriates constitutes fees for included services in terms of Article 12(4) of India-USA Treaty*.

– Decision of AAR in Centrica India Offshore Pvt Ltd In re 348 ITR 45: AAR has reiterated that reimbursement of salary under Secondment agreement results in taxable income in the hands of foreign co.

*The definition of fees for included services under Article 12(4) of India-USA Treaty does not deploy

the term ‘managerial services’.

58

Specific Issues

59

Transfer Pricing Implications

Secondment of personnel

To an associated enterprise* in India

No TP Provisions not applicable

Yes

Whether an International transaction** No TP Provisions not applicable

Yes

Liability to pay tax in India? TP Provisions not applicableˆ

No

Yes

TP Provisions applicable

*Associated Enterprise defined in section 92A **International Transaction defined in section 92B

ˆVanenburg In re 289 ITR 464 (AAR), Praxair Pacific Ltd In re 326 ITR 276

60

Transfer Pricing Implications…

AAR Ruling in Castleton Investment Ltd In re (2012) 348 ITR 537: – Transfer pricing provision applicable even if there is no

liability to pay tax in India. – Applicability of TP provisions not dependent upon

chargeability under the Act. Applicability of TP provisions totally depends upon satisfaction of requirements of section 92.

– Distinguished rulings in Vanenburg In re 289 ITR 464 (AAR), Dana Corporation In re 321 ITR 178, Praxair Pacific Ltd In re 326 ITR 276.

61

Treatment of per diem allowance

• Per diem allowance is granted to an employee to take care of its daily needs.

• Also known as ‘living’ or ‘daily’ allowance. • Exemption under section 10(14)(i) - any special allowance

specifically granted to meet expenses wholly, necessarily and exclusively incurred for the purpose of the duties of an office or employment is exempt from tax to the extent such expenses are actually incurred for that purpose.

• Daily allowance by way of reimbursement to an employee of a foreign co on secondment satisfy the requirements of section 10(14)(i) – CIT v. Goslino Mario (2000) 241 ITR 314 (Gau) approved by Supreme Court in 241 ITR 312.

62

Treatment of Social security and other statutory deductions in home country • Social security contributions are statutory contributions required to be

made by individuals towards a common fund. • Contributions are generally deducted from the salary of an individual

employee and deposited with the Government by the employer. • Whether Social security contribution in home country is to be treated as

part of taxable salary of an expatriate exercising employment in India? • Income tax authorities tend to argue that the social security contribution is

akin to PF contribution prevalent in India. • Mumbai Tribunal in Gallotti Raoul v. CIT 61 ITD 453 rejecting the above

argument held that the social security payments made outside India by the expatriate employee were under an overriding title, being diversion of income at source. Accordingly, such social security contributions are to be deducted from the salary for the purposes of determining the taxable salary in India.

63

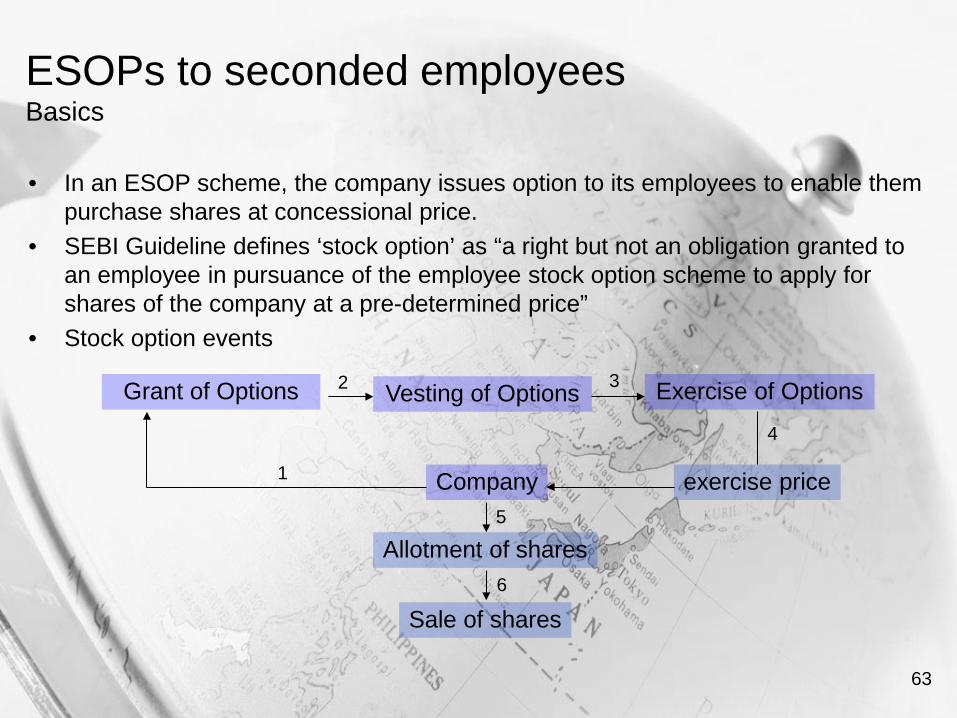

ESOPs to seconded employees Basics • In an ESOP scheme, the company issues option to its employees to enable them

purchase shares at concessional price. • SEBI Guideline defines ‘stock option’ as “a right but not an obligation granted to

an employee in pursuance of the employee stock option scheme to apply for shares of the company at a pre-determined price”

• Stock option events

Company

Grant of Options Vesting of Options Exercise of Options

exercise price

Allotment of shares

Sale of shares

1

2 3

4

5

6

64

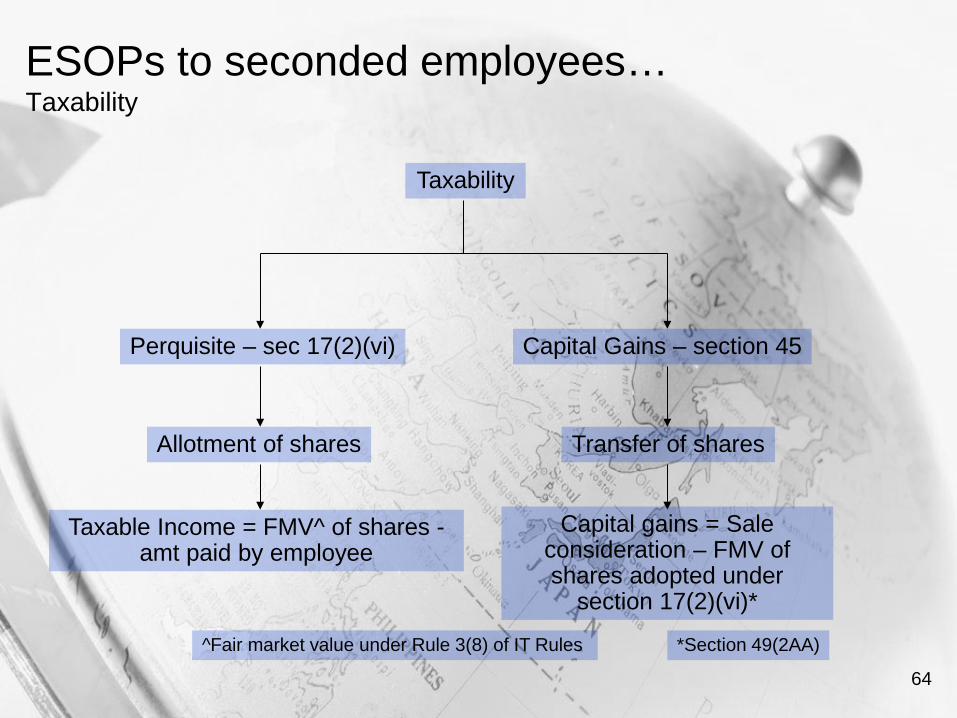

ESOPs to seconded employees… Taxability

Taxability

Perquisite – sec 17(2)(vi) Capital Gains – section 45

Allotment of shares Transfer of shares

Taxable Income = FMV^ of shares - amt paid by employee

Capital gains = Sale consideration – FMV of shares adopted under

section 17(2)(vi)*

*Section 49(2AA) ^Fair market value under Rule 3(8) of IT Rules

65

ESOPs to seconded employees… Determination of FMV of shares allotted under ESOP

FMV under Rule 3(8) of IT Rules

Equity shares listed in a recognized stock exchange and shares are traded

Equity shares not listed in a recognized stock exchange

Determined by a merchant banker on a specified date*

FMV= Avg of opening and closing price on the date of exercise of options

Equity shares listed in more than one recognized stock exchange and shares

are traded

FMV= Avg of opening and closing price on the date of exercise of options on the

recogized stock exchange which records highest volume of trading *Rule 3(8)(iv)(e)

66

ESOPs to seconded employees… Specified date under Rule 3(8)(iv)(e)

• Rule 3(8)(iv)(e) reads as: “Specified date means, (i) the date of exercising of the option; or (ii) any date earlier than the date of the exercising of the option, not

being a date which is more than 180 days earlier than the date of the exercising.”

• Clause (ii) permits an anterior date (up to a maximum of 180 days) for computing the value of shares.

• Section 17(2)(vi) specifically states that the value of perquisite should be determined on the date of exercise of options.

• Whether inconsistency between the section 17(2)(vi) and Rule 3(8)(iv)(e)? • If yes, How to resolve inconsistency between Section 17(2)(vi) and Rule

3(8)(iv)(e)?

67

ESOPs to seconded employees… Secondee receiving shares under ESOP from an Indian Co

• Circular 382 dated 04-05-1984 states as under: “Where shares in Indian companies are allotted in consideration for the machinery

and plant, the income embedded in the payments would be received in India as the shares in the Indian companies are located in India and would accordingly attract liability to income-tax as income received in India.”

• Applying the above analogy, an employee [whether resident or non-resident] receiving shares under an ESOP Scheme from its employer being an Indian Co at a concessional price would be regarded to have income received in India. As a result, he would be liable to pay tax on the same.

• Argument that the employees were rendering services outside India would be of no avail so far as taxability under the Act. However under the same may escape taxation in India by virtue of Treaty provisions if the non-resident employee is able to demonstrate that ESOP has been granted to it for rendering services outside India.

• Case study - Facts: X ltd is a company incorporated in India. It seconds its employees A and B for 11 months to its subsidiary X Inc incorporated in USA. X Ltd allots its shares at a concessional price to A and B under an ESOP scheme. Issue – whether A and B would be liable to pay tax in India on the value of perquisite?

68

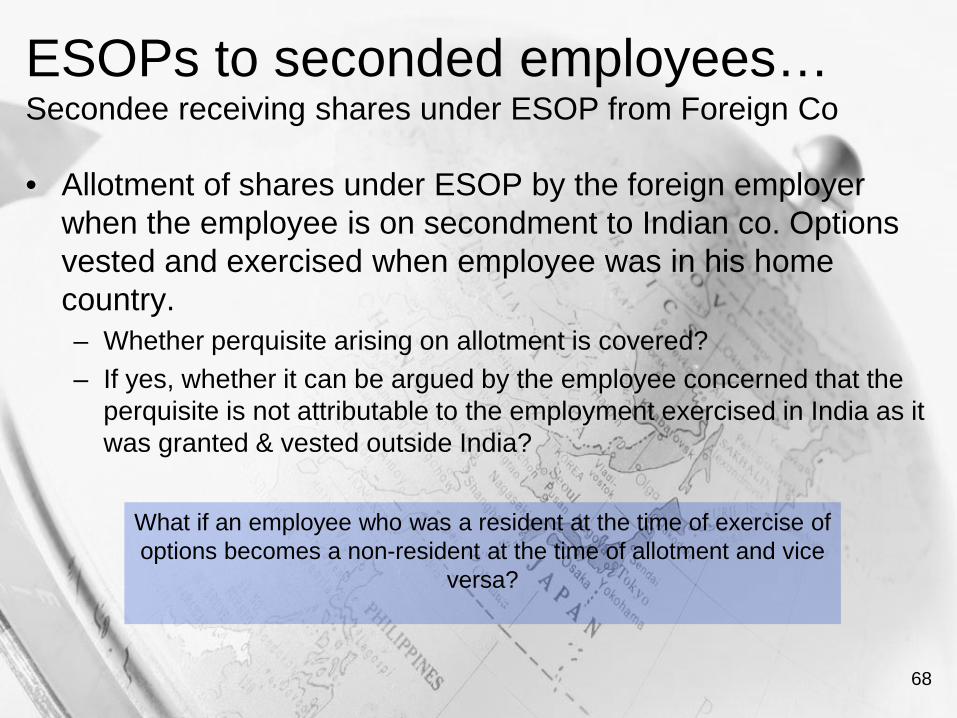

ESOPs to seconded employees… Secondee receiving shares under ESOP from Foreign Co

• Allotment of shares under ESOP by the foreign employer when the employee is on secondment to Indian co. Options vested and exercised when employee was in his home country. – Whether perquisite arising on allotment is covered? – If yes, whether it can be argued by the employee concerned that the

perquisite is not attributable to the employment exercised in India as it was granted & vested outside India?

What if an employee who was a resident at the time of exercise of options becomes a non-resident at the time of allotment and vice

versa?

69

ESOPs to seconded employees… Problems / Issues

• Stages of tax in different countries may not be uniform.

• Different characterization of benefit arising from ESOP in different countries.

• Problems in grant of credit of TDS if stage of tax or characterization does not match.

70

Hypothetical tax and tax equalization Concept

• When an employee moves to a different country under secondment agreement, their taxes are usually affected – either positively or negatively.

• Employer in home country formulates a policy where in tax liability arising out of secondment assignment in the other country is borne by the employer in home country. This policy is known as tax equalization policy.

• Objective is to ensure that the secondment assignment is tax neutral. In other words expatriate would only pay as much tax as he/she would have paid if he/she had not gone on assignment.

71

Hypothetical tax and tax equalization Concept…

• Hypothetical tax is the tax which employee would have paid on the same level of income in the home country. This would also be the amount of tax that the employer would consider for the purpose of withholding tax from the compensation paid to the employee.

• However, it may be noted that this tax is not the actual tax payable by the employee in the host country; hence the name ‘hypothetical tax’.

• The actual tax liability in the host country is discharged by the employer.

• The difference between hypothetical tax and actual tax results in ‘tax perquisite’.

72

Hypothetical tax and tax equalization Mechanics of tax equalization

• Perquisite in India and referable to tax obligation is taxable as a part of salary of the employee under section 17(2)(iv).

• The employer would thus have to gross up the salary factoring in the tax perquisite and tax rate in the host country in such a manner that the net take home salary of the employee is the same as he would have received in his home country.

73

Hypothetical tax and tax equalization Illustration

• Mr A, resident of USA, employed with ABC Inc.

• He is being deputed to an Indian Co, an AE of ABC Inc on the same salary. His net take home salary in USA is 80% of salary.

• He would be liable to pay tax in India at 30%.

Particulars Amt (INR) Salary 100 Less: tax payable In USA @ 20 % 20 Net take home salary In USA 80 Actual Tax in India@30% 30 Hypothetical tax 20

Issue – How ABC Inc would ensure that that Mr A’s take take home salary

continues to be at 80%?

74

Hypothetical tax and tax equalization Illustration…

Tax equalization working by ABC Inc: • ABC Inc would have to gross up the salary of Mr A in such a

manner that his take home salary in India remains at 80 after paying 30% of tax on salary income in India. It would be possible only if take home salary viz., Rs 80 is divided by 70%. This would result in gross salary of Mr A to 114.

• Tax to be borne by ABC Inc in India would be Rs 34 [114 * 30%]

• Net take home salary of Mr A would remain at Rs 80 [114 – 34]

• One can note that tax perquisite of Rs 14 [Actual tax (34) – hypothetical tax (20)], being taxable under section 17(2)(iv), has also been factored in this computation.

75

Hypothetical tax and tax equalization… Decisions

• Decision of Special Bench of ITAT Delhi in RBF Rig Corpn LIC (RBFRC) v ACIT 109 ITD 141: – As per secondment agreement in this case, taxes on salary were to be borne

by the employer. Accordingly in the returns of the employees filed by employer company in the representative capacity, tax borne by the employer on the salary paid was added as a perquisite and tax was calculated on the resultant figure. However, no further tax on tax was claimed to be payable in the light of provision of section 10(10CC) of the Income-tax Act. The employer company also paid tax collected in terms of provisions of section 192(1A) of the Income-tax Act (hereinafter referred to as the Act) which did not include tax on tax.

– The Assessing Officer however did not allowed the claim of the assessee. He held that tax borne by the employer was a monetary perquisite and thus further tax thereon should also be added to the salary by multiple stage grossing up process. In other words he wanted tax on tax to be added to salary. It was the contention of the Assessing Officer that since as per terms of employment, tax has to be borne by the employer, all taxes calculated by multiple stage grossing up are to be borne by the employer resulting into further tax perquisite.

76

Hypothetical tax and tax equalization… Decisions…

– The Special Bench accepting the contention of assessee held as under: “We, therefore, hold that the taxes paid by the employer on behalf of the

employee is a perquisite within the meaning of section 17(2) of the Income-tax Act, which is not provided by way of monetary payment. Therefore, there is no reason not to exclude such payment of taxes from the total income of the assessee. In other words, taxes paid by the employer can be added only once in the salary of the employee. Thereafter, tax on such perquisite is not to be added again. We, therefore, find substance in the contention advanced on behalf of teamed counsel for the assesses and the Interveners.”

• Decision in Jaydev H Raja v. DCIT ITA No. 2021/Mum/98 – The respondent-assessee was an employee of Coca-Cola Inc. USA and had

income under the head “Salalries”. Under the Tax Equalization Policy framed by the said company, the assessee's tax liability arising out of his foreign assignment was to be borne by the company but restricted only to the extent of liability arising out of such foreign assignment.

77

Hypothetical tax and tax equalization… Decisions…

– Since the assessee had received Rs.77.00 lakhs in India and the tax payable thereon was Rs.35.00 lakhs which was to be reimbursed by the employer, the assessee had included Rs.35.00 lakhs to the salary income of Rs.77.00 lakhs and offered Rs.113.00 lakhs (round figure) to tax. Though tax on Rs.113.00 lakhs at Rs.50.00 lakhs was paid, the assessee claimed that out of Rs.50.00 lakhs only Rs.35.00 lakhs was includible in the total income and not the balance amount of Rs.15.00 lakhs. The assessee contended that RS 15 lakhs was not borne by him and not the employer. The Assessing officer however rejected the contention of the assessee and held that entire Rs 50 lakhs is to be added to the salary inocme. The appeal filed by the assessee was dismissed by the CIT(A).

– The appeal filed by the assessee against the CIT(A) order was accepted by the Mumbai Tribunal. The tribunal held that the revenue authorities failed to understood that Rs 15 lakhs were not reimbursed by the assessee’s employer. It is the assessee who has borne that tax out of salary received in India.

– The decision on the Mumbai Tribunal has been recently confirmed by the Bombay High Court in CIT v. Jaydev H Raja ITA No 87 of 2000.

78

Hypothetical tax and tax equalization… Decisions…

• ITO v. Lucas Fole 124 TTJ 965 (Pune) – The assessee claimed deduction of hypothetical tax figure from the basic

salary. Tribunal held that the figure of hypothetical tax is to be deducted from perquisite and not from basic salary. While holding so it observed as under:

“It is important to understand the nature of deduction on account of hypothetical tax. This deduction on account of hypothetical tax liability is made under tax equalization policy, which, in substance, restricts the tax liability of an employee in India to the tax liability which the employee would have incurred in home country. For example, in case tax rate in the home country works out to 20% of salary income, and the assessee has to pay 30% of salary as tax in India, the assessee will be liable to pay only 20% of salary as tax and the balance 10% will be borne by the employer. This simple example would show that what is deducted on account of hypothetical tax is not a reduction of basic salary, but it is only restricting the tax liability of the employee as borne by the employer. The hypothetical tax liability thus only reduces the tax perquisite of the employee and not his income. This aspect of the matter will be relevant in computation of perquisites when the same are to be computed with reference to the salary of the employee. The deduction, therefore, should be made at the stage of computing the tax perquisite and not the basic salary.”

79

Hypothetical tax and tax equalization… Decisions…

– Issues not discussed in this case: • How the figure of hypothetical tax has been arrived at? • Why the tax borne by the employer is not to be added as a perquisite

under section 17(2)(iv)? • Other decisions rendered in context of hypothetical tax and tax

equalization concept: – CIT v. Dr Percy Batlivala – Delhi High Court ITA 1308/2008 – DCIT Mumbai v Mihir Jagadish Doshi - ITA No. 6798/Mum/2007) – Roy Marshal v. ACIT– 2008-TIOL-567- ITAT-Mum

80

Thank you