Tax information reporting The growing need for compliance ...

9

Tax information reporting The growing need for compliance technology

Transcript of Tax information reporting The growing need for compliance ...

Tax information reportingThe growing need for compliance technology

2

The Internal Revenue Service (IRS) is expanding information reporting and withholding requirements, including an increased focus on U.S. source income for foreign persons — now a Tier 1 tax examination issue. How can technology support the increasingly complex compliance process?

Deloitte hosted a Dbriefs webcast to discuss the evolving tax information and reporting landscape. Presenters reviewed the current compliance environment and common compliance issues. They also shared practical tips for addressing these issues and reviewed processes and technologies that exist to help manage compliance. More than 2,200 participants shared their own views through responses to polling questions posed during the webcast.

We cannot emphasize this point strongly enough — the information reporting compliance environment has changedIn the past, IRS enforcement efforts focused less on information reporting compliance than on income tax compliance. Accordingly, many companies did not devote

As used in this document, “Deloitte” means Deloitte Tax LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

extensive resources to compliance in the information reporting area. This has changed. The IRS and Treasury Department are now firmly focused on the payment and reporting of income paid by companies to U.S. recipients on a worldwide basis. Recent legislation has increased the types of payments to be reported from both a domestic and global perspective. Payments subject to reporting and for which companies become liable for withholding (at 28 percent or 30 percent) are “above the line” and can be collected regardless of a company’s net taxable income position.

Concurrent with these changes, the IRS is moving from reliance on taxpayer self-reporting to independent verification via third-party reporting. It also has increased enforcement through hiring and training of additional audit staff and elevating Internal Revenue Code (IRC) Section 1441 (see below) to a Tier 1 audit examination issue. And, it is automating data collection through the various information reporting regimes, enabling it to expand its reach by exchanging information with taxing authorities across borders.

Primary information reporting requirements

Commonalities: AP/treasury interface, tax department responsibilities, IT systems

Operational/training/communication/coordination requirements

Effective dates

Payment card and third-party payments (6050W)

ü Global Currently effective and 1/1/2013

Payments to Nonresident aliens (NRAs) (1441)

ü Global Currently effective

1042/1042S Reporting ü Global Currently effective

Foreign Account Tax Compliance Act (FATCA)

ü Global Generally 1/1/2013

1099 reporting ü United States Currently effective

Withholding calculations, deposits, reporting

ü United States Currently effective

Taxpayer Identification Number (TIN) documentation/collection

ü Global Currently effective

Foreign Bank and Financial Accounts (FBAR)

ü United States Currently effective

Other: Non-U.S., Multistate ü Global/United States Various – Non-U.S. countries seeking to implement U.S.-type regimes

The exhibit lists the primary reporting regimes and requirements of which you should be aware.

Tax information reporting The growing need for compliance technology 3

Some of the U.S. information reporting regimes will be familiar. The Form 1042 series, which deals with information reporting of payments to NRAs under IRC Section 1441 and the Form 1099 series, which reports a variety of payments such as miscellaneous income or dividends, have been in place for decades. There may be withholding obligations that arise in connection with these payments.

Some of the other regimes may be a little less familiar. For example, requirements for cost-basis reporting may impact companies other than financial institutions; for example, organizations that undergo stock splits may need to file Form 8937, Report of Organizational Actions Affecting Securities Basis. IRC Section 6050W, newly effective in 2011, requires reporting of payments by merchant banks that make credit card settlements and transaction settlements that are made by what is termed “third-party settlement organizations.” Many Internet sites are using this business model and had a 1099-K reporting responsibility under 6050W for 2011.

Another new legislative item with information reporting implications is the FATCA. FATCA requires companies to document the status of foreign financial institutions (FFIs) and the underlying substantial U.S. owners of non-financial foreign entities (NFFEs). In addition, it financially compels foreign financial intermediaries to identify and report specified U.S. account holders to the U.S. Treasury through the use of withholding taxes. Withholding agents must withhold 30 percent of payments to undocumented/non-compliant FFIs/NFFEs.

Information reporting compliance challengesOne of the greatest challenges to improving compliance efforts is the collection, review, and retention of appropriate documentation. This includes processes for collecting Forms W-9 and W-8 and sometimes Form 8233. It also includes the type of support gathered for income type and source, such as contracts, internal memoranda, accounting entries, invoices, and affidavits. For many organizations, this is still very much a manual effort.

Other challenges include identification, calculation, and deposit of appropriate withholding taxes by taxing jurisdictions — an area where noncompliance can put a company at risk for penalties as well as for withholding liabilities. In addition, most states require information reporting and sometimes withholding. In many cases, state requirements track federal requirements, but not always.

Perhaps the biggest challenge, though, is simply keeping up with changing requirements. For example, the IRS released final Forms 1065, U.S. Return of Partnership Income, and 1120, U.S. Corporation Income Tax Return for 2011. The revised forms include the addition of new line items requiring taxpayers to answer whether they filed all required Form(s) 1099. In addition, payments made with a credit card, payment card, and certain other types of payment (third-party network transactions) are now reported by the payment settlement entity on Form 1099-K rather than on Form 1099-MISC. And, the revised Form 1065 and Form 1120, as well as revised Form 1040 Schedules C, E, and F, indicate that the IRS will require the inclusion of information from the new Form 1099-K.

These are some steps you can take to reinforce up-to-date compliance efforts:•Develop and maintain good policies and procedures

•Train key personnel and accounts payable staff

•Follow IRS guidelines for form validation and retention

•Maintain an appropriate level of audit readiness

•Consider automating internal reports and templates for filings, as well as processes around W-8s and W-9s

4

An end-to-end view of the tax information reporting and withholding process

On the front end (at left), it is important to collect and validate documentation from customers, vendors, investors, and creditors and set up proper vendor and customer records. The second step (middle) is calculation of withholding on payments to vendors. For foreign vendors, the withholding tax determination can be at a transaction level. This requires line item detail from invoices — and given the sheer volume of transactions for most companies, it can be a very onerous process. The third step (upper right) is remitting withholding tax to the IRS, and the final step (right) is annual 1099, 1042, and 1042-S reporting responsibility. In addition, concurrent with all these steps can be activities to re-solicit up-to-date documentation, recertify that forms are current, and remediate any inaccurate payments and documentation.

Within this end-to-end process, there are six areas that should receive particular focus:•Onboarding/procurement — collecting and confirming

proper withholding certificates.

•Maintenance/recertification — identifying expired certificates or changes in customer information and initiating recertification procedures.

•Remediation — reviewing prior-year payments and forms and remediating past discrepancies and oversights.

•Payment/withholding — identifying sources of income and payment type; determining withholding rates, treaty rates, or exemptions; applying presumptions in absence of adequate data; executing timely withholding and depositing tax with the proper authority; and remitting payment to the payee, less withholding tax.

•Reporting — collecting payment/withholding data and preparing information returns.

•Validation — analyzing payments and payee data to determine compliance and analyzing invoices and other information for adequacy to support withholding determinations.

Having processes and designated responsibilities around each of these areas is critically important. At the same time, you also need to have processes in place to notify tax leadership of any issues, be aware of any past audit issues in these areas, and understand and embed any requirements for your company’s quality controls and management reporting.

The diagram below provides a high-level view of an end-to-end tax information reporting process.

Customers

Vendors

Investors

Creditors

Tax form collection and

validation

Vendor/ customer

maintenance

Re-solicitation, remediation, and recertification

Internal audit

IRSRemittance

Payee documentation (W-8/W-9/CA 592)

Tax reporting: 1099/1042

Identify invalid payment documentation

Procurement/Onboarding

Re-solicit valid documentation

TaxPayments

Invoices

Payment/withholding Tax reporting

Tax information reporting The growing need for compliance technology 5

Technologies to facilitate end-to-end tax information reporting processes

Customers

Vendors

Investors

Creditors

Tax form collection and

validation

Vendor/ customer

maintenance

Recertification

Policies and procedures / training / controls

Remediation

Management reporting

Internal audit

IRS

Tax reporting: 1099/1042

Procurement/onboarding Payments

ERP Extended withholding, third-party withholding calculators

Tax reporting tools or services

(1099 and 1042)

Data analysis

tool

ERP, flow-through entity

hierarchy management

Electronic withholding certificate collection

Invoices

Invoice receipt/withholding

Auto procedures

Tax reportingPayment

Manual intervention Remittance

In summary, there are many challenges, many rules, and many moving parts facing companies today. The rules for each jurisdiction are broad and designed to capture a large universe of payments. These rules are complex and use unforgiving presumptions; a slight foot fault can lead to unexpected withholding liability on a given payment. Moreover, disparate functions often manage the data required to determine withholding for a given payment, and it is understandable that such functions may not be aware of the intricate tax rules that could apply to each payment.

Managing the challenges of information reporting is not a problem the tax department can solve alone. While income tax reporting regimes may primarily impact the tax function and tax resources, information reporting impacts companies across the board. This area requires a holistic,

cross-functional approach that includes representatives from tax, information technology, accounts payable, vendor onboarding, treasury, compliance and risk management, and other functions. Companies that have been successful in this area have developed proactive, well-defined, and well-enforced processes that cross the business. By doing so, they have been able to reduce error rates and potential exposures. The good news is there are many scalable effective practices and newly developed technology approaches available to support this need.

Technologies to facilitate end-to-end tax information reporting processesThe end-to-end process described above provides a good foundation for looking at the technology and processes that can potentially improve compliance — and potentially improve efficiencies at the same time.

6

W-8/W-9 systems. Proper documentation is a critical first step in compliance. The W-8BEN is a highly prescriptive form with only about 20 fields, but there are many places that issues can occur. Electronic W-8 and W-9 systems collect tax forms and establish rules engines that validate the documents so that you can see where you stand at any moment. The structured nature of electronic tools — with messages, drop-down lists, and help features — have the potential to reduce error rates. For organizations with significant flow-through to intermediaries and that receive W-8IMYs, there are also tools on the market to manage hierarchies and underlying subaccount status and withholding statements.

Technology considerations may include buy-versus-build options, vendor selection, implementation implications, change management, and product support. One key consideration is to select a vendor that has previously received a Memorandum of Understanding (MOU) from the IRS, deeming the tool a valid way to collect forms online.

Enterprise resource planning (ERP) solutions for withholding. For determining withholding at the transaction level, one option available is configurations in an ERP system, such as SAP’s® extended withholding modules. ERP solutions do not fully automate withholding calculations, but leading ERPs do offer ways to configure a framework that allows you to determine the appropriate rate and apply the tables that you configure and populate — it’s just not automated. There are also bolt-on third-party calculators and solutions that can be tied into your existing payment solution to help classify income type and withholding rates, but it is important to work with vendors to confirm that invoices identify where goods and services are performed. This approach may take a bit of configuration, but it is a way to leverage ERP systems and withholding calculators to address compliance objectives.

Reporting. There are technologies and services to assist with 1099 and 1042S filings, as well as ERP system configurations that can produce the filings. A key to using these tools effectively is to collect the proper data, such as 1042S income codes, downstream.

Data analysis. The information and withholding process typically involves large amounts of data. There are numerous tools available that enable analysis of data from disparate data sources, linking various data sets for a more complete picture and reconciling data for greater accuracy. In addition, they offer capabilities for customizing numerous tests, based on needs for discovering anomalies in data, such as payment and contract information. These tools can be customized for specific tasks — for example, all payments to vendors out of the United States that are services — and configured to analyze vendor data to review withholding and reporting compliance. It also is possible to integrate analytical tools into withholding analyses to assist in categorizing payment types, income sourcing, etc.

In summary, these types of tools can help you turn static information into data that can flow from one system to the next. For example, you can gather tax documentation from an electronic W-8/W-9 tool that could then feed a payment system with the status of the vendor, treaty rates, and applicable withholding. The payment system, in turn, can produce the information needed to feed into a 1099/1042S processing system.

However, there is no perfect end-to-end solution. There are technologies available that can be pieced together to help improve compliance, efficiencies, reporting, and other areas. Whether you are implementing one technology or looking at the process as a whole, an important first step is conducting an assessment to understand your current compliance position. From that, you can consider the specific process improvements, technology tools, and remediation steps necessary to comply with tax information reporting and withholding requirements.

Tax information reporting The growing need for compliance technology 7

which of these regimes included such requirements, just over 70 percent of webcast participants correctly indicated “all of the above.”

A variety of information reporting regimes pose implications for U.S. companies. Of those, webcast participants were split with respect to the one most important to their own 2012/2013 planning. Just over 18 percent indicated they were most concerned about compliance with Form 1099 reporting, another 14 percent cited FATCA implementation, and about 8 percent stated that IRS audits for Section 1441 issues were their primary concern. About a quarter, 26 percent, said they need an overall information reporting assessment.

Tax executives’ perspectivesDeloitte hosted a Dbriefs webcast to discuss the evolving tax information and reporting landscape. Presenters reviewed the current compliance environment and common compliance issues. They also shared practical tips for addressing these issues and reviewed processes and technologies that exist to help manage compliance. More than 2,200 participants shared their own views through responses to polling questions posed during the webcast.

Several U.S. tax information reporting regimes — including IRC Section 1441, FATCA, and IRC Section 6050W — require identification and/or documentation of foreign payees by U.S. withholding agents. When quizzed about

Source: Deloitte’s Tax Operations Dbriefs webcast, “Tax Information Reporting: The Growing Need for Compliance Technology,” held on April 19, 2012.Polling results presented herein are solely the thoughts and opinions of survey participants and are not necessarily representative of the total population.

12%

14%

3.5%

70.5%

Which of the following U.S. tax information reporting regimes will require identification and/or documentation of foreign payees by U.S. withholding agents?

IRC Section 1441

FATCA

IRC Section 6050W

All of the above

26%33.2%

7.9%

14.3%

18.6%

Which of the following are most important for your planning for 2012/2013 compliance efforts?

Need for an overall information reporting assessment

Concerns regarding FATCA implementation

IRS audit for Section 1441 issues

Compliance with Forms 1099 reporting

Unsure/not applicable

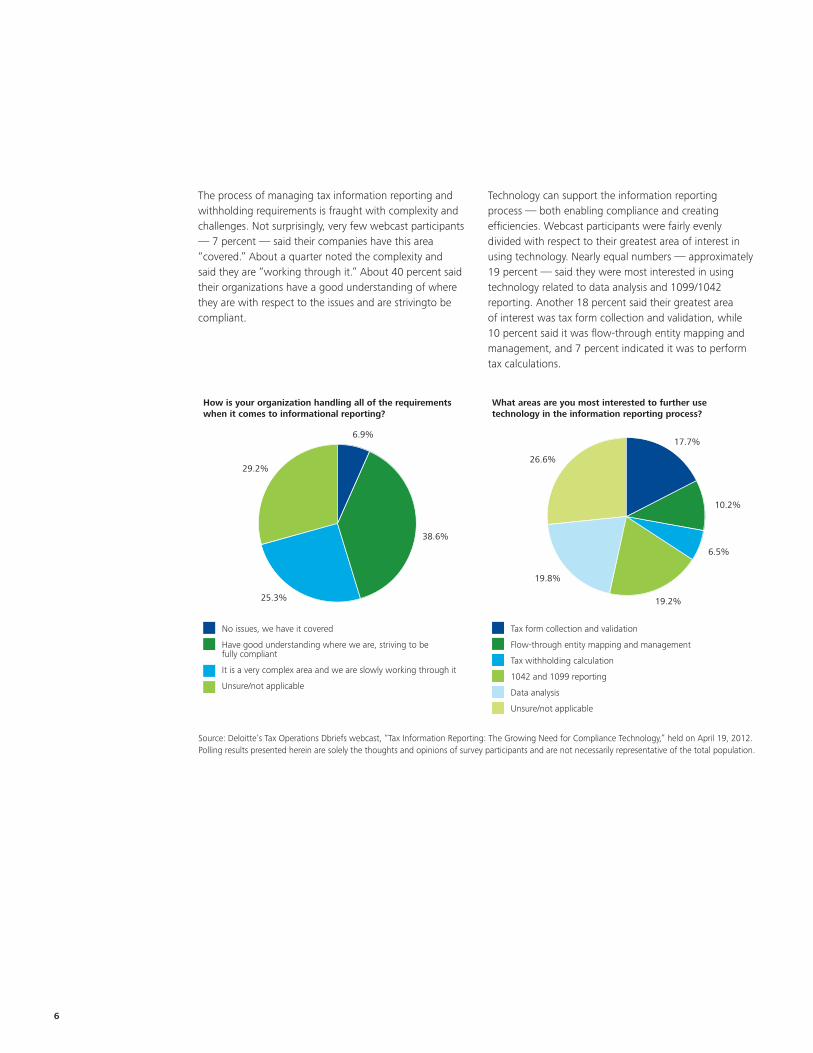

The process of managing tax information reporting and withholding requirements is fraught with complexity and challenges. Not surprisingly, very few webcast participants — 7 percent — said their companies have this area “covered.” About a quarter noted the complexity and said they are “working through it.” About 40 percent said their organizations have a good understanding of where they are with respect to the issues and are strivingto be compliant.

Technology can support the information reporting process — both enabling compliance and creating efficiencies. Webcast participants were fairly evenly divided with respect to their greatest area of interest in using technology. Nearly equal numbers — approximately 19 percent — said they were most interested in using technology related to data analysis and 1099/1042 reporting. Another 18 percent said their greatest area of interest was tax form collection and validation, while 10 percent said it was flow-through entity mapping and management, and 7 percent indicated it was to perform tax calculations.

6.9%

38.6%

25.3%

29.2%

How is your organization handling all of the requirements when it comes to informational reporting?

No issues, we have it covered

Have good understanding where we are, striving to be fully compliant

It is a very complex area and we are slowly working through it

Unsure/not applicable

17.7%

26.6%

19.2%

6.5%

10.2%

19.8%

What areas are you most interested to further use technology in the information reporting process?

Tax form collection and validation

Flow-through entity mapping and management

Tax withholding calculation

1042 and 1099 reporting

Data analysis

Unsure/not applicable

Source: Deloitte’s Tax Operations Dbriefs webcast, “Tax Information Reporting: The Growing Need for Compliance Technology,” held on April 19, 2012.Polling results presented herein are solely the thoughts and opinions of survey participants and are not necessarily representative of the total population.

6

This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering business, financial, investment, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this publication.

Copyright © 2013 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited

ContactsFor more information on technology as it relates to tax information reporting or Deloitte’s Global Information Reporting and Withholding Services, contact your Deloitte adviser or one of the individuals below:

Patty FlornessPartnerDeloitte Tax LLP+1 212 436 [email protected]

Faye TannenbaumTax PartnerDeloitte Tax LLP+1 212 436 [email protected]

Denise HintzkeDirectorDeloitte Tax LLP+1 212 436 [email protected]

David BolnerSenior ManagerDeloitte Tax LLP+1 203 708 [email protected]

Regina AriesSenior Manager Deloitte Tax LLP+1 617 437 [email protected]

Terence CoppingerDirectorDeloitte Tax LLP+1 212 436 [email protected]

Anthony MartiranoDirectorDeloitte Tax LLP+1 973 602 [email protected]