TAX INFORMATION FOR 2009 - middlefield.commiddlefield.com/pdf/reports/mrftaxguide2009.pdf ·...

28

TAX INFORMATION FOR 2009

Transcript of TAX INFORMATION FOR 2009 - middlefield.commiddlefield.com/pdf/reports/mrftaxguide2009.pdf ·...

TAX INFORMATION FOR 2009

T5013A-SAMPLE

Fiscal period end / Exercice se terminant le

Renounced Canadian exploration and development expenses - Frais d'exploration et d'aménagement au Canada ayant fait l'objet d'une renonciation Renounced Canadian exploration expenses

Renounced Canadian development expenses

Assistance for Canadian exploration expenses

Assistance for Canadian development expenses

Portion subject to an interest-free period - CEE

Expenses qualifying for an ITC

Portion subect to an interest-free period - ITC

Partie donnant lieu à une périodesans intérêt - FEC

Frais admissibles aux fins du CIIPartie donnant lieu à une périodesans intérêt - CII

129128

Number of units acquired Cost per unit Total cost of units

Amount / DetailsMontant / Détails

Tax shelter information - Renseignements sur l'abri fiscal150 151 152 153 Limited-recourse amounts

Frais renoncés d'explorationau Canada

Frais renoncés d'aménagementau Canada

Montant d'aide pour fraisd'exploration au Canada

Montant d'aide pour fraisd'aménagement au Canada

Amount / DetailsMontant / Détails

Box /Case

Amount / DetailsMontant / Détails

Pour des renseignements en français, lisez les instructions en annexe.

Gains (pertes) en capital Provision relative aux gains encapital

Déduction pour amortissement

For information in English, see attachment.

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Box /Case

Box /Case

Frais financiers

Capital gains (losses) Capital gains reserves Capital cost allowance85 Box /Case

71

Business investment loss

Intérêts de source canadienne Revenu étranger en dividendeset en intérêts

Perte au titre d'un placementd'entreprise

55 56

Other amounts and information - Montants et renseignements additionnelsBox /Case

70

Farming income (loss) Fishing income (loss)43

Revenu (perte) de profession libérale

Revenu (perte) d'agriculture Revenu (perte) de pêche

37 41

Box /Case

Canadian and foreign net business income (loss) - Revenu net (perte nette) d'entreprise canadien et étranger

Perte comme commanditairedisponible à reporter

Remboursement de capitalPerte d'années antérieuresadmissables pour l'année courante

24 25 27

Revenu brut total de la société de personnes

Other income Partnership's total gross income

Autre revenu

3430

Amount / DetailsMontant / Détails

Limited partnership lossavailable for carryforward

Previous loss carryforwardeligible in the current year

Return of capital Box /Case

Box /Case

Box /Case

Box /Case

Amount / DetailsMontant / Détails

Box /Case

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Box /Case

Amount / DetailsMontant / Détails

Box /Case

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Box /Case

Box /Case

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Actual amount of dividends (other than eligible dividends)

Taxable amount of dividends (other than eligible dividends)

Dividend tax credit for dividends other than eligible dividends

Montant imposable des dividendes (autres que des dividendes déterminés)

Crédit d'impôt pour dividendes autres que des dividendes déterminés

51-1 52-2

59

Actual amount of eligible dividends

51-2

Box /Case

Box /Case

Crédit d'impôt pour dividendesdéterminés

Montant réel des dividendesdéterminés

52-1

Box /Case

52

Montant imposable desdividendes déterminés

Carrying charges

Revenu net (perte nette) delocation canadien et étranger

Montant réel des dividendes (autres que des dividendes déterminés)

50 Interest from Canadian sources

Foreign dividend and interest income

Amount / DetailsMontant / Détails

Box /Case

Type of slip

T

Partnership code

Code du genre de société de personnes

06 07

02 Partnership's Business Number Tax shelter identification number

S

Identification

Member code08

01

Numéro d'identification de la société de personnesY - A

Number of partnership units held09

Code de l'associé

Country code

Is this a publicly traded partnership?

MS'agit-il d'une société de personnes cotée à la bourse?

05

10

03 04

11

Nombre d'unités détenues de la société de personnes

Amount / DetailsMontant / Détails

BC

Partnership's name and address - Raison sociale et adresse de la société de personnes

12

Partner's share (%) of partnership income (loss)

Numéro d'inscription de l'abri fiscal

_

T5013A (06) XXXX

121 130

Privacy Act personal information bank number CRA/P-PU-005 - Loi sur la protection des renseignements personnels, Fichier de renseignements personnels numéro CRA/P-PU-005

35

143

Business income (loss) Professional income (loss)

51

Amount / DetailsMontant / Détails

Canadian and foreign investments and carrying charges - Investissements canadiens et étrangers et frais financiers

Revenu (perte) d'entreprise

Taxable amount of eligible dividends

Dividend tax credit for eligible dividends

Canadian and foreign net rental income (loss)

26

120 124 125

Box /Case 141

Box /Case 144 MBSK

STATEMENT OF PARTNERSHIP INCOME FOR TAX SHELTERS AND RENOUNCED RESOURCE EXPENSESÉTAT DES REVENUS D'UNE SOCIÉTÉ DE PERSONNES POUR LES ABRIS FISCAUX ET

LES FRAIS DE RESSOURCES AYANT FAIT L'OBJET D'UNE RENONCIATION

Part (%) de l'associé dans les revenus (pertes) de la société de personnes

Recipient's identification number - Numéro d'identification du bénéficiaire

Code du pays

Genre de feuillet

Complex sharing arrangements - Part des revenus ne pouvant pas être exprimée

ON

Amount / DetailsMontant / Détails

Box /Case145

Box /Case

Revenu (perte) d'entreprise ducommanditaire

22 Limited partnership business income (loss)

22-1

Fraction à risques de laparticipation du commanditaire

Limited partner's at-risk amount

Amount / DetailsMontant / Détails

Amount / DetailsMontant / Détails

Box /Case

At-risk adjustment

Revenu (perte) d'agriculture ducommanditaire

Stabilisation du revenu agricole(PCSRA)

Revenu (perte) de pêche ducommanditaire

Limited partnership farming income (loss)

20-1 Agricultural income stabilization (CAIS)

21

Fraction à risques rajustée de laparticipation du commanditaire

Revenu (perte) de location ducommanditaire

Limited partnership rental income (loss)

22-2 Limited partner's adjusted at-risk amount

Nombre d'unités acquises Coût par unité Coût total des unités Montant à recours limité

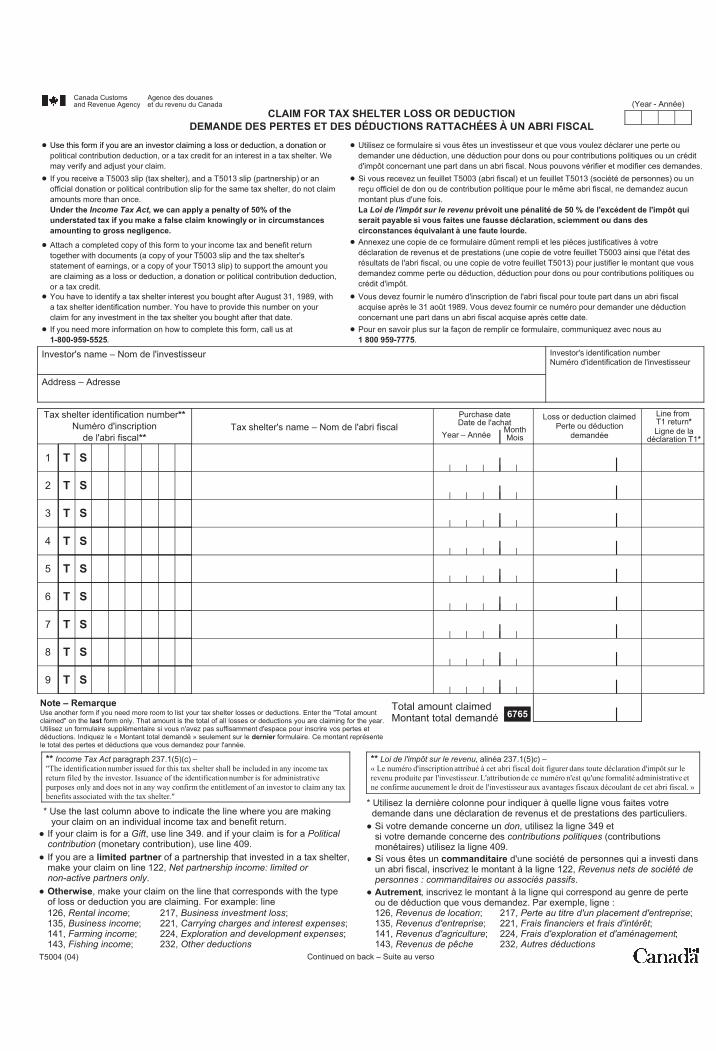

investor to claim any tax benefits associated with the tax shelter."

Income Tax Act

doit figurer dans toute déclaration d'impôt sur le revenu produite par l'investisseur. L'attribution de

ce numéro n'est qu'une formalité administrative et ne confirme aucunement le droit de

20 Limited partnership fishing income (loss)

alinéa 237.1(5)(c) - « Le numéro d'inscription attribué à cet abri fiscal

be included in any income tax return filed by the investor. Issuance of the identification number

is for administrative purposes only and does not in any way confirm the entitlement of an

Limited partnership net income (loss) - Revenue net (perte nette) du commanditaire23

l'investisseur aux avantages fiscaux découlant de cet abri fiscal. »

Loi de l'impôt sur le revenuparagraph 237.1(5)(c)-"The identification number issued for this tax shelter shall

Box /Case

Other indirect reductions

Partner's name and address - Nom et adresse de l'associé

Autres réductions indirectesAmount / DetailsMontant / DétailsMontant de rajustement à risque

154 155

Enter this amount on Schedule 4 Line 122

and Form T5004

Enter this amount on Schedule 4 Line 121

Enter this amount on Schedule 4 Line 221 and

Form T5004

Enter this amount on Schedule 4 Line 120

Enter this amount on Schedule 1 Line 425

Enter this amount on Schedule 3 Line 174

Enter this amount on Form T1229. Enter the resultant

CEE on Line 224 and on Form T5004

Enter this amount on Form T1229. Enter the resultant CDE on Line 224 and on Form T5004

Enter this amount on Form T1229. Enter the resultant qualifying

expenses on Form T2038 Box 6717. (Individuals only)

Do not record this amount on your tax return.

For CRA information only

Enter this amount on Form BC T1231. Enter the resultant tax

credit on Form BC 428 and Form T1229. (British Columbia resident

individuals only)

Enter this amount on Form MB T1241. Enter the resultant tax

credit on Form MB 428 and Form T1229. (Manitoba resident

individuals only)

Enter this amout on Form ON T1221 and Line 6266 of Form ON 479.

Enter the resultant credit on Form T1229. (Ontario resident individuals

only)

TAX GUIDE FOR PREPARING YOUR 2009 INCOME TAX RETURN

MRF 2008 RESOURCE LIMITED PARTNERSHIP DISCOVERY 2008 FLOW-THROUGH LIMITED PARTNERSHIP

MRF 2009 RESOURCE LIMITED PARTNERSHIP DISCOVERY 2009 FLOW-THROUGH LIMITED PARTNERSHIP

March 2010

Dear Investor:

The purpose of this booklet is to provide you with information to assist you in filing your income tax return for 2009. The taxslips necessary to file your return will be mailed separately by your investment advisor.

Enclosed in this booklet please find the following tax information for 2009:

(i) Sample T5013A located opposite this page, including instructions.(ii) Middlefield Tax Guide to assist you with the preparation of your 2009 income tax return.

(iii) Federal tax forms you will require to file your income tax return (T1229, T2038, T5004).

We have enclosed only the Federal tax forms you will require to file your income tax return. Any Provincial tax forms that

you may require can be obtained directly from your local tax office.

MRF 2009 Resource Limited Partnership (“MRF 2009”), Discovery 2009 Flow-Through Limited Partnership (“Discovery2009”)MRF 2009 raised $37.0 million in early 2009 and the proceeds were fully invested by the 2009 year end in a portfolio of 44companies balanced between the oil and gas and mining sectors. Discovery 2009 raised $23.0 million in the fall of 2009 and

investments were made in a portfolio of 45 companies predominantly focussed on the mining sector.

MRF 2008 Resource Limited Partnership (“MRF 2008”), Discovery 2008 Flow-Through Resource Limited Partnership(“Discovery”)MRF 2008 was launched in the spring of 2008 and Discovery was launched in the fall of 2008. The proceeds of each

Partnership were fully invested by their 2008 year ends. Please refer to our website for updated information.

For the 2010 taxation year, investors may wish to consider investing in our new partnership, MRF 2010 ResourceLimited Partnership, which is currently available. Please contact your Investment Advisor for more information onthis new offering.

The information contained in this guide is strictly for information purposes and should not be regarded as tax advice. Wesuggest you consult with your tax advisor to determine the optimal use of your share of the federal/provincial

deductions/credits, as well as the impact, if any, on your liability for alternative minimum tax. If you have any difficultiescompleting your income tax return or claiming any deductions/credits which appear on your T5013A/Relevé 15, you should

consult your tax advisor. Additionally, if you are a corporation or trust and require assistance, please consult with your taxadvisor as this guide is for individual taxpayers only.

We hope the enclosed information will be useful to you in completing your 2009 income tax return. Please visit our website

at www.middlefield.com for more information on all our Partnerships, including month-end net asset values.

Yours truly,

Nancy ThamSenior Vice President

416-847-5349

c.c.: Investment Advisor

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

2

TABLE OF CONTENTS

Page

Filing Instructions for Form T5013A

A. Business Income (Loss), Capital Gains (Losses), Eligible Dividends, Interest Income and

Carrying Charges from a Partnership 3B. Claiming Canadian Exploration Expenses (CEE) , Canadian Development Expenses (CDE) 4

C. Claiming the Federal Investment Tax Credit 5

D. Claiming a Deduction for Issue Costs (for dissolved partnerships only) 6

For Ontario Residents OnlyE. Claming the Ontario Focused Flow-Through Share Tax Credit 6

For British Columbia Filers OnlyF. Claiming the British Columbia Mining Flow-Through Share Tax Credit 7

For Manitoba Filers OnlyG. Claiming the Manitoba Mineral Exploration Tax Credit 7

Filing Instructions for Saskatchewan Filers Only

H. Claiming the Saskatchewan Mineral Exploration Tax Credit 8

Filing Instructions for Form Relevé 15

For Québec Filers OnlyI. Business Income (Loss), Capital Gains (Losses), Eligible Dividends, Interest Income and

Carrying Charges from a Partnership 8

J. Claiming Canadian Exploration Expenses 10K. Claiming Québec Exploration Expenses 11

L. Claiming a Deduction for Issue Costs (for dissolved partnerships only) 12

Preparation Instructions for Tax Shelter Forms

M. Form T5004 – For All Investors 12

N. Form TP-1079.6 – For Québec Filers Only 13

Filing of Tax Forms

O. For All Investors 13

P. For Québec Filers Only 13

Exhibit A: Relevé 15 Memo Supplementary 14

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

3

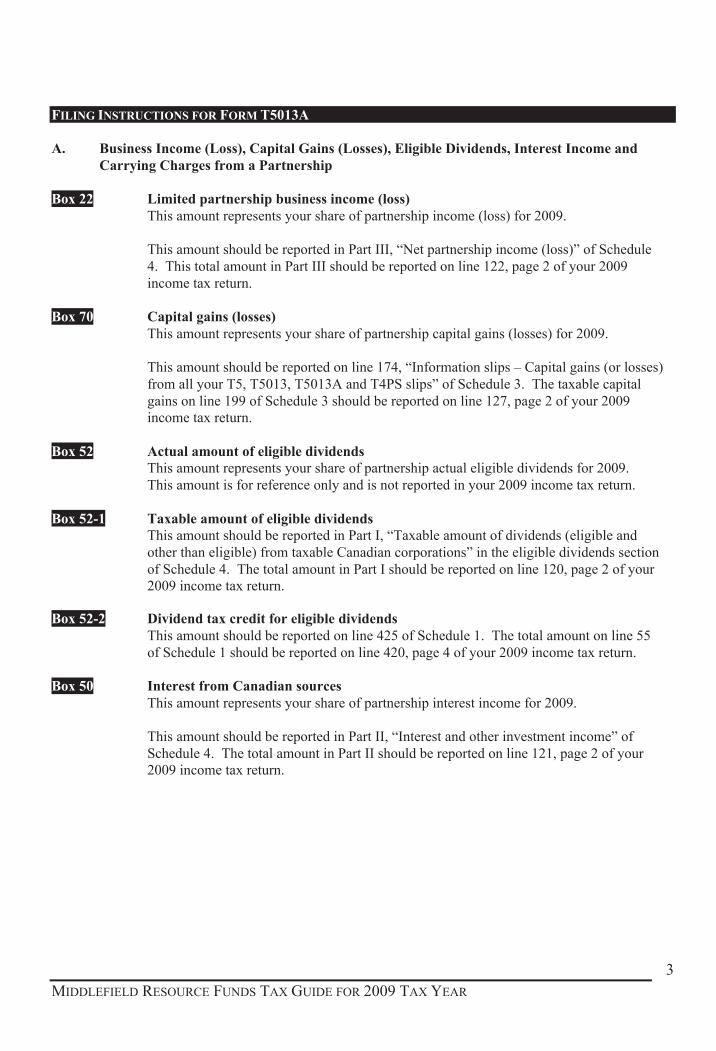

FILING INSTRUCTIONS FOR FORM T5013A

A. Business Income (Loss), Capital Gains (Losses), Eligible Dividends, Interest Income andCarrying Charges from a Partnership

Box 22 Limited partnership business income (loss)This amount represents your share of partnership income (loss) for 2009.

This amount should be reported in Part III, “Net partnership income (loss)” of Schedule

4. This total amount in Part III should be reported on line 122, page 2 of your 2009

income tax return.

Box 70 Capital gains (losses)This amount represents your share of partnership capital gains (losses) for 2009.

This amount should be reported on line 174, “Information slips – Capital gains (or losses)

from all your T5, T5013, T5013A and T4PS slips” of Schedule 3. The taxable capital

gains on line 199 of Schedule 3 should be reported on line 127, page 2 of your 2009income tax return.

Box 52 Actual amount of eligible dividendsThis amount represents your share of partnership actual eligible dividends for 2009.

This amount is for reference only and is not reported in your 2009 income tax return.

Box 52-1 Taxable amount of eligible dividendsThis amount should be reported in Part I, “Taxable amount of dividends (eligible and

other than eligible) from taxable Canadian corporations” in the eligible dividends section

of Schedule 4. The total amount in Part I should be reported on line 120, page 2 of your2009 income tax return.

Box 52-2 Dividend tax credit for eligible dividendsThis amount should be reported on line 425 of Schedule 1. The total amount on line 55

of Schedule 1 should be reported on line 420, page 4 of your 2009 income tax return.

Box 50 Interest from Canadian sourcesThis amount represents your share of partnership interest income for 2009.

This amount should be reported in Part II, “Interest and other investment income” of

Schedule 4. The total amount in Part II should be reported on line 121, page 2 of your2009 income tax return.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

4

FILING INSTRUCTIONS FOR FORM T5013A (CONTINUED)

Box 59 Carrying chargesThis amount represents your share of partnership carrying charges related to borrowings

of the partnership.

This amount should be reported in Part IV, “Carrying charges and interest expenses” of

Schedule 4. The total amount in Part IV should be reported on line 221, page 3 of your2009 income tax return.

The amount of any deductible interest expense you incurred in the year on a borrowing tofinance your limited partnership units should be treated as outlined above for Box 59

amounts.

FILING INSTRUCTIONS FOR FORM T5013 (CONTINUED)Box 24 Limited partnership loss available for carryforward

This amount represents your share of the current year limited partnership loss that cannot

be deducted.

Note: You can only deduct this amount from future partnership income allocations if youhave a positive at-risk amount. You can carry forward this amount indefinitely.

Box 22-1 Limited partner’s at-risk amountThis amount represents a partner’s original cost of partnership interest plus or minus

certain adjustments. A limited partner cannot deduct partnership losses, resource

expenses and investment tax credits in excess of the at-risk amount.

This amount is for reference only and is not reported in your 2009 income tax return.

Box 34 Partnership’s total gross incomeThis amount represents the total 2009 gross income of the partnership.

This amount is for reference only and is not reported in your 2009 income tax return.

Box 152 Total cost of unitsThis amount represents a partner’s original cost of partnership interest.

This amount is for reference only and is not reported in your 2009 income tax return.

B. Claiming Canadian Exploration Expenses (CEE), Canadian Development Expenses (CDE)

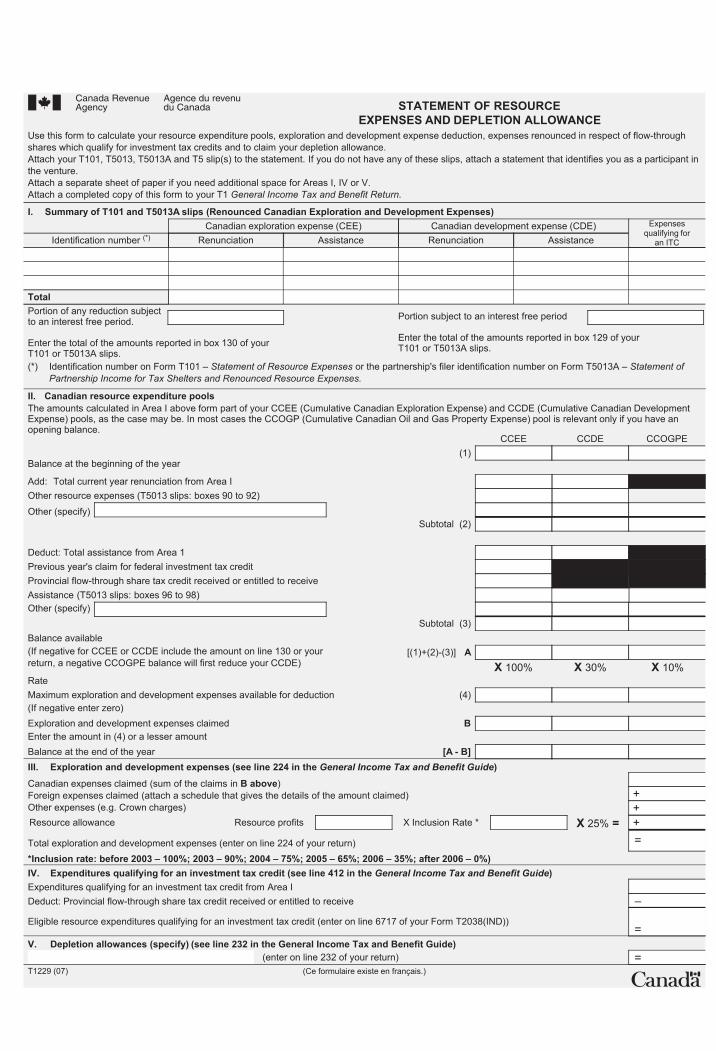

Box 120 and 121 Renounced Canadian exploration and development expensesThis amount represents your share of Canadian exploration and development expenses

for 2009.

This amount should be reported in Form T1229 – Statement of Exploration and

Development Expenses and Depletion Allowance for calculating the maximum CEE andCDE deduction available in 2009 to reduce your federal taxable income for the year, or

for a future year.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

5

FILING INSTRUCTIONS FOR FORM T5013A (CONTINUED)

Box 120 and 121 Renounced Canadian exploration and development expenses(i) Report any carry forward balance of Cumulative CEE (CCEE) and Cumulative

CDE (CCDE) from the prior year to Area II box (1) of your 2009 Form T1229.A carry forward would arise if you had any undeducted CEE or CDE from

previous years.

(ii) Report the amount from box 120 and box 121 of the T5013A slip to Area I andArea II of Form T1229.

(iii) Report previous year’s claim for the federal investment tax credit and current

year’s claim for the provincial flow-through share tax credit to Area II of FormT1229.

(iv) Calculate box A by adding box (1) to box (2) and subtracting box (3).

(v) If the amount in box A of Form T1229 is negative, report this amount as other

income on line 130, page 2 of your 2009 income tax return.(vi) For CEE, calculate box (4) by multiplying box A by 100%. For CDE, calculate

box (4) by multiplying box A by 30%.

(vii) Report your desired CEE and CDE claim for the current year in box B, Area II ofForm T1229.

Note: You may claim any amount of CEE and CDE deduction up to a maximum

of box (4).(viii) Calculate box [A-B] by subtracting box B from box A. Box [A-B] will be the

amount carried forward to the 2010 taxation year.

Note: Any unused balance of the CEE and CDE pool at the end of the year can

be carried forward indefinitely.(ix) Report Area II, box B to Area III. The total amount in Area III should be

reported on line 224, page 3 of your 2009 income tax return.

C. Claiming the Federal Investment Tax Credit

Box 128 Expenses qualifying for an Investment Tax Credit (ITC)This amount represents the renounced Canadian exploration expenses that qualify for theInvestment Tax Credit in 2009.

This amount should be reported on Form T1229 – Statement of Resource Expenses andDepletion Allowance and T2038 – Investment Tax Credit (Individuals) for calculating

the investment tax credit available in 2009 to reduce your federal tax payable for the year,

for a previous year, or for a future year.(i) Report the amount from box 128 on the T5013A slip to Area I & IV of Form

T1229.

(ii) Report the provincial flow-through share tax credit available in the year to Area

IV of Form T1229.(iii) Calculate the eligible expenditure qualifying for an investment tax credit in Area

IV of Form T1229 and enter the amount on line 6717, Part A of Form T2038.

(iv) Calculate line B in Part A Code 5 of Form T2038 by multiplying line 6717 by15% and enter the amount in column 3 on page 6 of Form T2038.

(v) Report any carry forward balance of federal investment tax credits from the prior

year in column 1, page 6 of your 2009 Form T2038.(vi) Calculate column 5 by adding column 1, 2 and 3 and subtracting column 4.

(vii) Report the amount from column 5 on line C of Form T2038.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

6

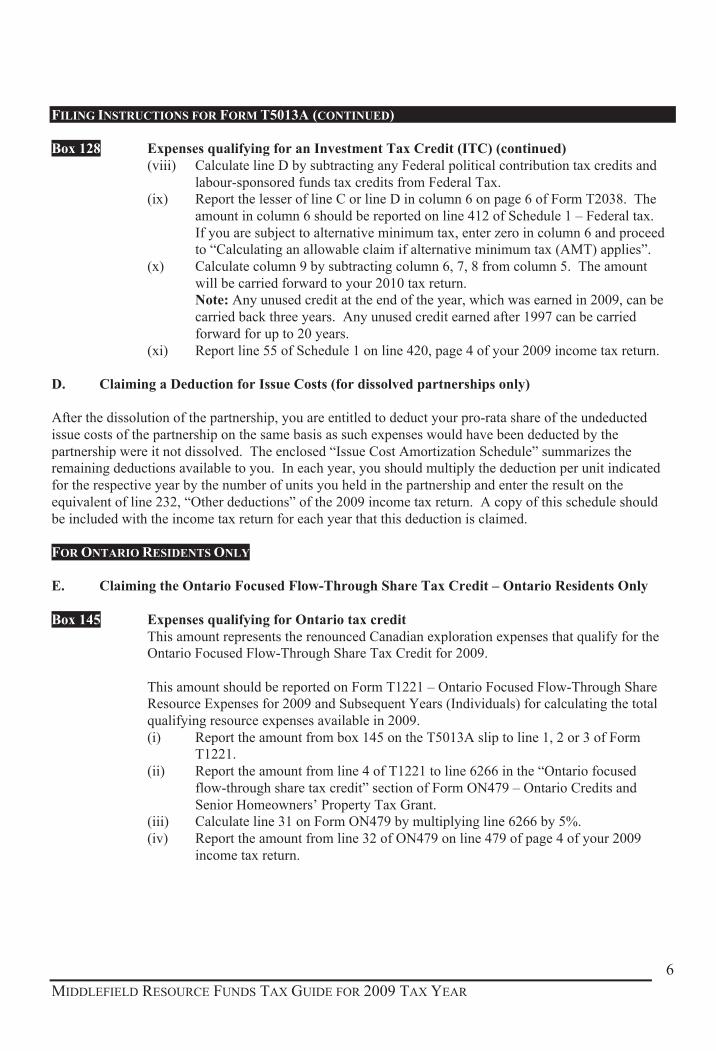

FILING INSTRUCTIONS FOR FORM T5013A (CONTINUED)

Box 128 Expenses qualifying for an Investment Tax Credit (ITC) (continued)(viii) Calculate line D by subtracting any Federal political contribution tax credits and

labour-sponsored funds tax credits from Federal Tax.(ix) Report the lesser of line C or line D in column 6 on page 6 of Form T2038. The

amount in column 6 should be reported on line 412 of Schedule 1 – Federal tax.

If you are subject to alternative minimum tax, enter zero in column 6 and proceedto “Calculating an allowable claim if alternative minimum tax (AMT) applies”.

(x) Calculate column 9 by subtracting column 6, 7, 8 from column 5. The amount

will be carried forward to your 2010 tax return.Note: Any unused credit at the end of the year, which was earned in 2009, can be

carried back three years. Any unused credit earned after 1997 can be carried

forward for up to 20 years.

(xi) Report line 55 of Schedule 1 on line 420, page 4 of your 2009 income tax return.

D. Claiming a Deduction for Issue Costs (for dissolved partnerships only)

After the dissolution of the partnership, you are entitled to deduct your pro-rata share of the undeducted

issue costs of the partnership on the same basis as such expenses would have been deducted by the

partnership were it not dissolved. The enclosed “Issue Cost Amortization Schedule” summarizes theremaining deductions available to you. In each year, you should multiply the deduction per unit indicated

for the respective year by the number of units you held in the partnership and enter the result on the

equivalent of line 232, “Other deductions” of the 2009 income tax return. A copy of this schedule should

be included with the income tax return for each year that this deduction is claimed.

FOR ONTARIO RESIDENTS ONLY

E. Claiming the Ontario Focused Flow-Through Share Tax Credit – Ontario Residents Only

Box 145 Expenses qualifying for Ontario tax creditThis amount represents the renounced Canadian exploration expenses that qualify for theOntario Focused Flow-Through Share Tax Credit for 2009.

This amount should be reported on Form T1221 – Ontario Focused Flow-Through ShareResource Expenses for 2009 and Subsequent Years (Individuals) for calculating the total

qualifying resource expenses available in 2009.

(i) Report the amount from box 145 on the T5013A slip to line 1, 2 or 3 of FormT1221.

(ii) Report the amount from line 4 of T1221 to line 6266 in the “Ontario focused

flow-through share tax credit” section of Form ON479 – Ontario Credits and

Senior Homeowners’ Property Tax Grant.(iii) Calculate line 31 on Form ON479 by multiplying line 6266 by 5%.

(iv) Report the amount from line 32 of ON479 on line 479 of page 4 of your 2009

income tax return.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

7

FILING INSTRUCTIONS FOR FORM T5013A (CONTINUED)

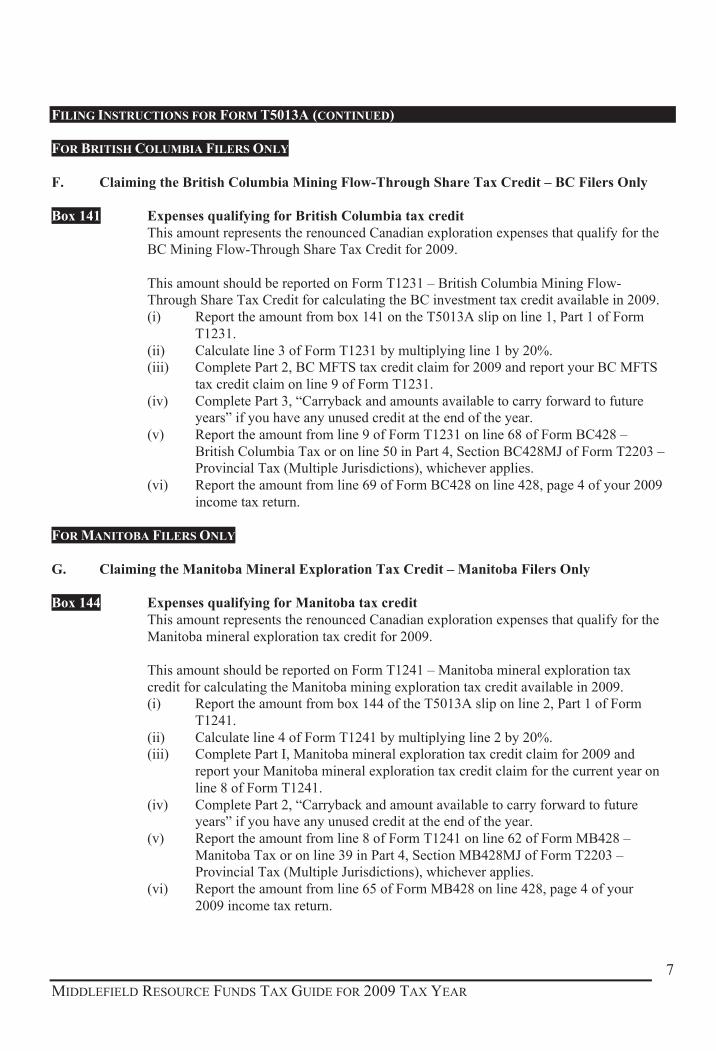

FOR BRITISH COLUMBIA FILERS ONLY

F. Claiming the British Columbia Mining Flow-Through Share Tax Credit – BC Filers Only

Box 141 Expenses qualifying for British Columbia tax creditThis amount represents the renounced Canadian exploration expenses that qualify for theBC Mining Flow-Through Share Tax Credit for 2009.

This amount should be reported on Form T1231 – British Columbia Mining Flow-Through Share Tax Credit for calculating the BC investment tax credit available in 2009.

(i) Report the amount from box 141 on the T5013A slip on line 1, Part 1 of Form

T1231.

(ii) Calculate line 3 of Form T1231 by multiplying line 1 by 20%.(iii) Complete Part 2, BC MFTS tax credit claim for 2009 and report your BC MFTS

tax credit claim on line 9 of Form T1231.

(iv) Complete Part 3, “Carryback and amounts available to carry forward to futureyears” if you have any unused credit at the end of the year.

(v) Report the amount from line 9 of Form T1231 on line 68 of Form BC428 –

British Columbia Tax or on line 50 in Part 4, Section BC428MJ of Form T2203 –Provincial Tax (Multiple Jurisdictions), whichever applies.

(vi) Report the amount from line 69 of Form BC428 on line 428, page 4 of your 2009

income tax return.

FOR MANITOBA FILERS ONLY

G. Claiming the Manitoba Mineral Exploration Tax Credit – Manitoba Filers Only

Box 144 Expenses qualifying for Manitoba tax creditThis amount represents the renounced Canadian exploration expenses that qualify for the

Manitoba mineral exploration tax credit for 2009.

This amount should be reported on Form T1241 – Manitoba mineral exploration tax

credit for calculating the Manitoba mining exploration tax credit available in 2009.(i) Report the amount from box 144 of the T5013A slip on line 2, Part 1 of Form

T1241.

(ii) Calculate line 4 of Form T1241 by multiplying line 2 by 20%.(iii) Complete Part I, Manitoba mineral exploration tax credit claim for 2009 and

report your Manitoba mineral exploration tax credit claim for the current year on

line 8 of Form T1241.

(iv) Complete Part 2, “Carryback and amount available to carry forward to futureyears” if you have any unused credit at the end of the year.

(v) Report the amount from line 8 of Form T1241 on line 62 of Form MB428 –

Manitoba Tax or on line 39 in Part 4, Section MB428MJ of Form T2203 –Provincial Tax (Multiple Jurisdictions), whichever applies.

(vi) Report the amount from line 65 of Form MB428 on line 428, page 4 of your

2009 income tax return.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

8

FILING INSTRUCTIONS FOR SASKATCHEWAN FILERS ONLY

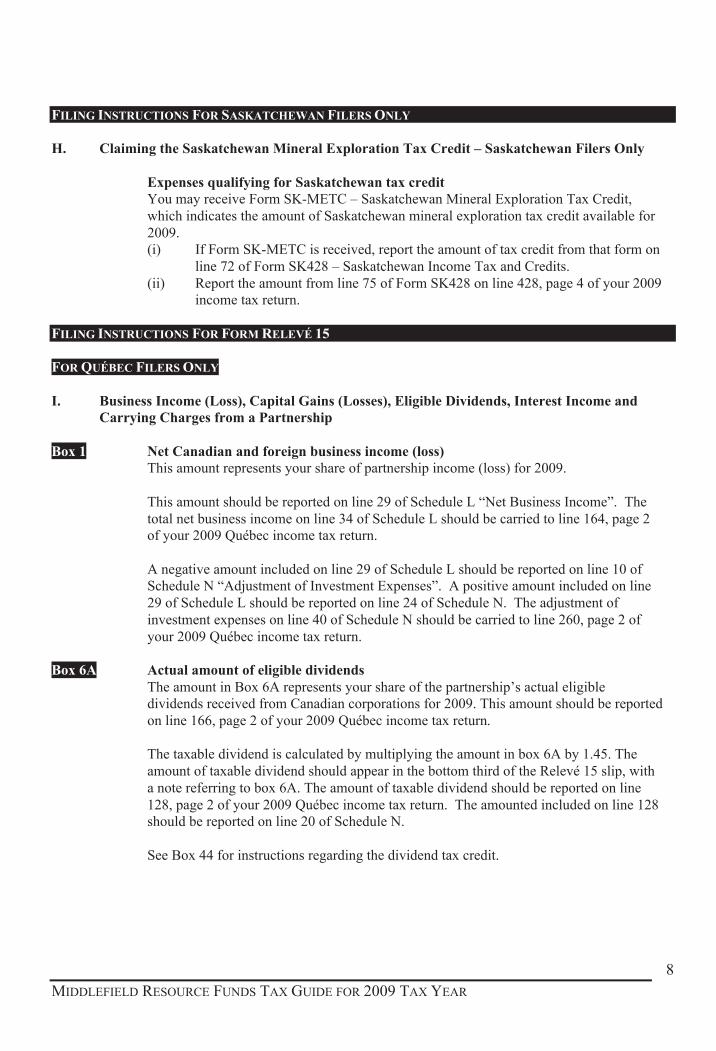

H. Claiming the Saskatchewan Mineral Exploration Tax Credit – Saskatchewan Filers Only

Expenses qualifying for Saskatchewan tax creditYou may receive Form SK-METC – Saskatchewan Mineral Exploration Tax Credit,

which indicates the amount of Saskatchewan mineral exploration tax credit available for

2009.(i) If Form SK-METC is received, report the amount of tax credit from that form on

line 72 of Form SK428 – Saskatchewan Income Tax and Credits.

(ii) Report the amount from line 75 of Form SK428 on line 428, page 4 of your 2009income tax return.

FILING INSTRUCTIONS FOR FORM RELEVÉ 15

FOR QUÉBEC FILERS ONLY

I. Business Income (Loss), Capital Gains (Losses), Eligible Dividends, Interest Income andCarrying Charges from a Partnership

Box 1 Net Canadian and foreign business income (loss)This amount represents your share of partnership income (loss) for 2009.

This amount should be reported on line 29 of Schedule L “Net Business Income”. The

total net business income on line 34 of Schedule L should be carried to line 164, page 2of your 2009 Québec income tax return.

A negative amount included on line 29 of Schedule L should be reported on line 10 ofSchedule N “Adjustment of Investment Expenses”. A positive amount included on line

29 of Schedule L should be reported on line 24 of Schedule N. The adjustment of

investment expenses on line 40 of Schedule N should be carried to line 260, page 2 of

your 2009 Québec income tax return.

Box 6A Actual amount of eligible dividendsThe amount in Box 6A represents your share of the partnership’s actual eligibledividends received from Canadian corporations for 2009. This amount should be reported

on line 166, page 2 of your 2009 Québec income tax return.

The taxable dividend is calculated by multiplying the amount in box 6A by 1.45. The

amount of taxable dividend should appear in the bottom third of the Relevé 15 slip, with

a note referring to box 6A. The amount of taxable dividend should be reported on line

128, page 2 of your 2009 Québec income tax return. The amounted included on line 128should be reported on line 20 of Schedule N.

See Box 44 for instructions regarding the dividend tax credit.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

9

FILING INSTRUCTIONS FOR FORM RELEVÉ 15 (CONTINUED)

FOR QUÉBEC FILERS ONLY

Box 7 Interest and other investment income from Canadian sourcesThis amount represents your share of partnership interest income for 2009.

This amount should be reported on line 130, page 2 of your 2009 Québec income tax

return. The amount included on line 130 should be reported on line 22 of Schedule N.

Box 12 Capital gains (or capital losses)This amount represents your share of partnership capital gains (losses) for 2009 from

resource property.

This amount should be reported on line 47 of Schedule G "Capital Gains and Losses".

The total taxable capital gain from line 98 of Schedule G should be reported on line 139,page 2 of your 2009 Québec income tax return. If none of the property you disposed of

entitles you to the capital gains deduction (see line 292, page 3 your 2009 Québec income

tax return and Section 260 of the Revenu Québec Guide to your 2009 return), enter theamount indicated on line 139 of your return on line 34 of Schedule N.

Note: You are advised to consult with your tax advisor to determine your eligibility for

exemption on gains realized from the disposition of resource property.

Box 14 Gross income (or gross loss) of the partnershipThis amount represents the total 2009 gross income of the partnership.

You are not required to report this amount on your 2009 Québec income tax return.

Box 15A Carrying charges and interest expensesThis amount represents your share of partnership carrying charges related to borrowings

of the partnership.

This amount should be reported on line 231, page 2 of your 2009 Québec income tax

return and on line 12 of Schedule N.

The amount of any deductible interest expense you incurred in the year on a borrowing to

finance your limited partnership units should be treated as outlined above for Box 15A

amounts.

Box 26 At-risk amountThis amount represents a partner’s original cost of partnership interest plus or minus

certain adjustments. A limited partner cannot deduct partnership losses and resourceexpenses in excess of the “at-risk” amount. This amount is for reference only and is not

reported in your 2009 Québec income tax return.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

10

FILING INSTRUCTIONS FOR FORM RELEVÉ 15 (CONTINUED)

FOR QUÉBEC FILERS ONLY

Box 27 Limited partnership lossThis amount represents your share of the current year limited partnership loss that cannot

be deducted.

Note: You can only deduct this amount from future partnership income allocations if you

have a positive at-risk amount. When deducted, this amount will also be taken intoaccount in computing your adjustment of investment expenses for the year. You can

carry forward this amount indefinitely.

Box 44 Dividend Tax CreditThis amount represents your share of the dividend tax credit.

This amount should be reported on line 415, page 3 of your 2009 Québec income taxreturn.

Box 52 Total cost of unitsThis amount represents a partner’s original cost of partnership interest.

This amount is for reference only and is not reported in your 2009 Québec income tax

return.

J. Claiming Canadian Exploration Expenses

Box 60 Canadian exploration expensesThis amount represents your share of Canadian exploration expenses for 2009.

This amount should be added to the Cumulative Canadian Exploration Expenses pool todetermine the maximum available resource deduction. This deduction is claimed at line

241, page 2 of your 2009 Québec income tax return. We have enclosed a blank Relevé 15

memo supplementary (see Exhibit A) to assist you with the calculations.

(i) Report any carryforward balance of Cumulative CEE (CCEE) from the prior year

in column A on the Relevé 15 memo supplementary schedule.(ii) Report the amount from box 60 of the RL15 slip in column B of the Relevé 15

memo supplementary schedule.

(iii) Report the aggregate amount from box 62 and the corresponding amount in box

66, item 62, of the RL15 slip, in column F of the Relevé 15 memo supplementaryschedule.

(iv) Calculate column H by adding column A to column B and subtracting column C,

D, E, F and G.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

11

FILING INSTRUCTIONS FOR FORM RELEVÉ 15 (CONTINUED)

FOR QUÉBEC FILERS ONLY

Box 60 Canadian exploration expenses (continued)(v) Report your desired CEE claim for the current year in column I.

Note: You may claim any amount of CEE deduction up to a maximum of 100%

of box H.(vi) Calculate column J by subtracting column I from column H. Column J will be

carried forward to your 2010 Québec income tax return.

(vii) Report the amount in column I of Relevé 15 memo supplementary schedule toline 241, page 2 of your 2009 Québec income tax return.

(viii) Report an amount equal to 50% of the deduction claimed at line 241 (Resource

deductions) on line 14 of Schedule N.

K. Claiming Québec Exploration Expenses

Box 62 Québec exploration expensesThis amount represents your share of Québec exploration expenses for 2009.

This amount should be reported on line 250, page 2 of your 2009 Québec income taxreturn. Also, enter code “09” “Deduction for exploration expenses incurred in Québec”

on line 249, page 2 of your 2009 Québec income tax return.

Box 62 and 63 Québec exploration expenses, Québec surface mining and oil and gas explorationexpensesThis amount represents your share of Québec exploration expenses, surface mining and

oil and gas exploration expenses.(i) For each of boxes 62 and 63 of the RL15 slip there may be a corresponding item

in box 66 below it. From each of the amounts in boxes 62 and 63 subtract the

corresponding amount, if any, in item 62 or 63 of box 66. Report 25% of the

eligible amount relating to box 62 and 25% of the eligible amount relating tobox 63 of the RL15 slip on line 287, page 3 of your 2009 Québec income tax

return.

(ii) Enter the corresponding number “04”, “Additional Deduction for QuebecResources” in box 286. If you are entitled to more than one type of deduction on

line 287, enter the number “80” in box 286.

Box 64 Exploration expenses incurred in northern QuébecThis amount represents your share of exploration expenses incurred in northern Québec.

Only corporations are entitled to an additional deduction with respect to exploration

expenses incurred in northern Québec.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

12

FILING INSTRUCTIONS FOR FORM RELEVÉ 15 (CONTINUED)

FOR QUÉBEC FILERS ONLY

L. Claiming a Deduction for Issue Costs (for dissolved partnerships only)

After the dissolution of the partnership, you are entitled to deduct your pro-rata share of the undeducted

issue costs of the partnership on the same basis as such expenses would have been deducted by thepartnership were it not dissolved. The enclosed “Issue Cost Amortization Schedule” summarizes the

remaining deductions available to you. In each year, you should multiply the deduction per unit indicated

for the respective year by the number of units you held in the partnership and enter the result on theequivalent of line 250, “Other deductions” of the 2009 Québec income tax return. Enter the

corresponding number “16”, “Other Deductions” in box 249. A copy of this schedule should be included

with the income tax return for each year that this deduction is claimed.

PREPARATION INSTRUCTIONS FOR TAX SHELTER FORMS

M. Form T5004 – For All Investors

A statement of Tax Shelter Loss or Deduction (T5004) must be completed in order to claim deductions

related to your Middlefield Resource Fund.

(i) Form T5004 requires the Tax Shelter Identification Number, which is located in Box 3 of

Form T5013A.

(ii) The tax shelter name is whichever specific Middlefield Resource Fund you have invested in.(iii) Purchase date is the date of purchase of your Middlefield investment(s).

(iv) In the column marked “loss or deduction claimed”, enter the following amounts and indicate

the corresponding line from your 2009 income tax return (enter each amount on a separateline):

Amount of loss or deduction claimed Line from 2009 income tax return

1) Net Partnership Income (Loss) Line 122

2) Carrying Charges Line 221

3) Exploration and Development Expenses Line 224

Note that if you own more than one flow-through limited partnership or tax-sheltered investment, these

amounts must be calculated individually and reported on Form T5004 for each partnership or investment.

The amounts on the 2009 income tax return may be aggregated.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

13

PREPARATION INSTRUCTIONS FOR TAX SHELTER FORMS

PREPARATION INSTRUCTIONS FOR TAX SHELTER FORMS (CONTINUED)

N. Form TP-1079.6 – For Québec Filers Only

A statement of Losses, Deductions and Tax Credits Respecting a Tax Shelter (TP-1079.6) must be

completed in order to claim deductions related to your Middlefield Resource Fund.

(i) Form TP-1079.6 requires the Tax Shelter Identification Number, which is located in the top

right box of Form RL15.

(ii) The tax shelter name is whichever specific Middlefield Resource Fund you have invested in.(iii) Purchase date is the date of purchase of your Middlefield investment(s).

(iv) In the column marked “loss, deduction or tax credit”, enter the following amounts and

indicate the line from your 2009 Québec income tax return (enter each amount on a separate

line):

Amount of loss or deduction claimed Line from 2009 Québec income tax return

1) Business Income (Loss) Line 164

2) Carrying Charges Line 231

3) Resource Deduction Line 241

Note that if you own more than one flow-through limited partnership or tax-sheltered investment, these

amounts must be calculated individually and reported on Form TP-1079.6 for each partnership or

investment. The amounts on the 2009 Québec income tax return may be aggregated.

FILING OF TAX FORMS

O. For All Investors

File your completed 2009 income tax return along with the following:

(i) Schedules 1, 3 and 4.

(ii) Copy 2 of Form T5013A. Copy 3 should be retained in your files.

(iii) Form T1229, Form T2038 and Form T5004.

(iv) Any provincial tax forms that were completed.

File the Issue Cost Amortization Schedule for Future Years (blue form) (for dissolved partnerships only)

with your completed income tax returns for the relevant years.

Please retain a copy of all tax forms, including copy 3 of Form T5013A, for your files.

P. For Québec Filers Only

File your completed 2009 Québec income tax return along with the following:

(i) Schedules G, L and N.

(ii) Copy 2 of Form RL15. Copy 3 should be retained in your files.

(iii) Form TP-1079.6.

Please retain a copy of all tax forms, including Copy 3 of Form RL15, for your files.

MIDDLEFIELD RESOURCE FUNDS TAX GUIDE FOR 2009 TAX YEAR

14

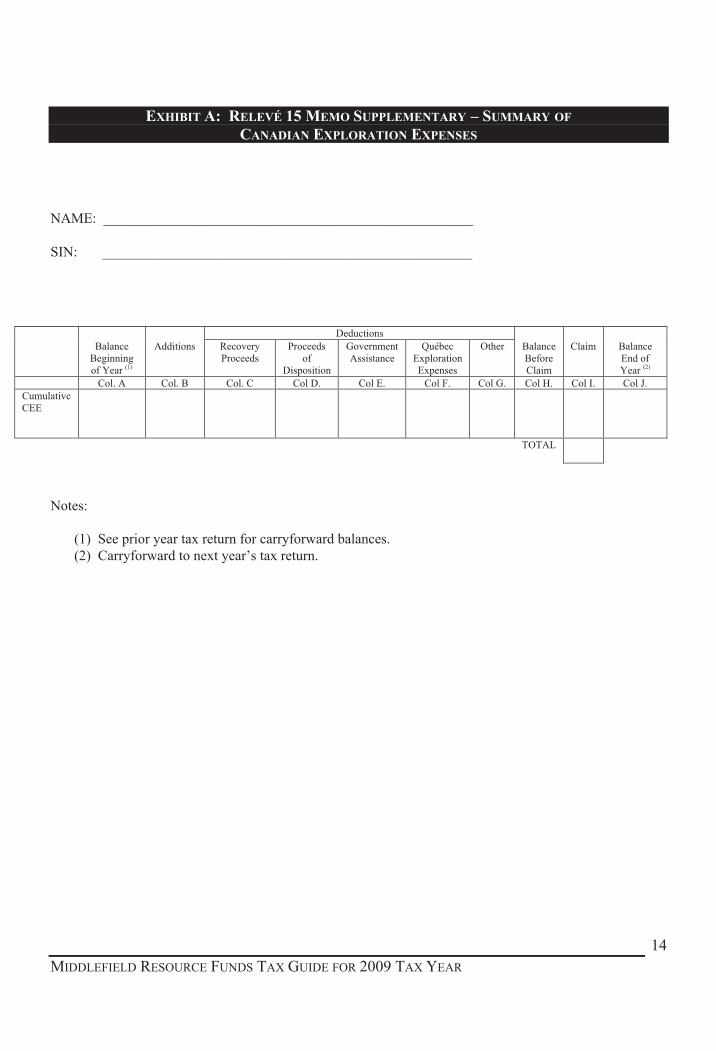

EXHIBIT A: RELEVÉ 15 MEMO SUPPLEMENTARY – SUMMARY OF

CANADIAN EXPLORATION EXPENSES

NAME: ____________________________________________________

SIN: ____________________________________________________

Deductions

BalanceBeginningof Year (1)

Additions RecoveryProceeds

Proceedsof

Disposition

GovernmentAssistance

QuébecExplorationExpenses

Other BalanceBeforeClaim

Claim BalanceEnd ofYear (2)

Col. A Col. B Col. C Col D. Col E. Col F. Col G. Col H. Col I. Col J.

CumulativeCEE

TOTAL

Notes:

(1) See prior year tax return for carryforward balances.

(2) Carryforward to next year’s tax return.

STATEMENT OF RESOURCE

EXPENSES AND DEPLETION ALLOWANCE

Use this form to calculate your resource expenditure pools, exploration and development expense deduction, expenses renounced in respect of flow-through

shares which qualify for investment tax credits and to claim your depletion allowance.

Attach your T101, T5013, T5013A and T5 slip(s) to the statement. If you do not have any of these slips, attach a statement that identifies you as a participant in

the venture.

Attach a separate sheet of paper if you need additional space for Areas I, IV or V.

Attach a completed copy of this form to your T1 General Income Tax and Benefit Return.

T1229 (07) (Ce formulaire existe en français.)

I. Summary of T101 and T5013A slips (Renounced Canadian Exploration and Development Expenses)

Canadian exploration expense (CEE) Canadian development expense (CDE)

Renunciation Assistance Renunciation AssistanceIdentification number (*)

Total

Expensesqualifying for

an ITC

Portion of any reduction subjectto an interest free period.

Enter the total of the amounts reported in box 130 of yourT101 or T5013A slips.

Portion subject to an interest free period

Enter the total of the amounts reported in box 129 of yourT101 or T5013A slips.

Canadian expenses claimed (sum of the claims in B above)

Foreign expenses claimed (attach a schedule that gives the details of the amount claimed)

Other expenses (e.g. Crown charges)

Total exploration and development expenses (enter on line 224 of your return)

IV. Expenditures qualifying for an investment tax credit (see line 412 in the General Income Tax and Benefit Guide)

Expenditures qualifying for an investment tax credit from Area I

Deduct: Provincial flow-through share tax credit received or entitled to receive –

=

=

V. Depletion allowances (specify) (see line 232 in the General Income Tax and Benefit Guide)

(enter on line 232 of your return)

*Inclusion rate: before 2003 – 100%; 2003 – 90%; 2004 – 75%; 2005 – 65%; 2006 – 35%; after 2006 – 0%)

Eligible resource expenditures qualifying for an investment tax credit (enter on line 6717 of your Form T2038(IND))

II. Canadian resource expenditure pools

The amounts calculated in Area I above form part of your CCEE (Cumulative Canadian Exploration Expense) and CCDE (Cumulative Canadian DevelopmentExpense) pools, as the case may be. In most cases the CCOGP (Cumulative Canadian Oil and Gas Property Expense) pool is relevant only if you have anopening balance.

CCEE CCDE CCOGPE

III. Exploration and development expenses (see line 224 in the General Income Tax and Benefit Guide)

(1)Balance at the beginning of the year

Add: Total current year renunciation from Area I

Subtotal (2)

Deduct: Total assistance from Area 1

Previous year's claim for federal investment tax credit

Provincial flow-through share tax credit received or entitled to receive

Assistance (T5013 slips: boxes 96 to 98)

Other resource expenses (T5013 slips: boxes 90 to 92)

Other (specify)

Other (specify)

Identification number on Form T101 – Statement of Resource Expenses or the partnership's filer identification number on Form T5013A – Statement of

Partnership Income for Tax Shelters and Renounced Resource Expenses.

(*)

Subtotal (3)

A

Balance available

(If negative for CCEE or CCDE include the amount on line 130 or your

return, a negative CCOGPE balance will first reduce your CCDE)

Rate

(4)Maximum exploration and development expenses available for deduction

(If negative enter zero)

Exploration and development expenses claimed

Enter the amount in (4) or a lesser amount

B

Balance at the end of the year [A - B]

X 100%

[(1)+(2)-(3)]

X 30% X 10%

+

+

=

+X Inclusion Rate * X 25% =Resource profitsResource allowance

ÉTAT DE FRAIS DE RESSOURCESET DE DÉDUCTIONS POUR ÉPUISEMENT

T1229 (07)

Remplissez et joignez une copie de ce formulaire à votre déclaration de revenus et de prestations pour calculer vos comptes de ressources au Canada, votredéduction de frais d'exploration et d'aménagement, vos dépenses renoncées concernant des actions accréditives qui sont admissibles aux fins du crédit d'impôtà l'investissement, et pour réclamer votre déduction pour épuisement.Joignez vos feuillets T101, T5013, T5013A et T5 à l'état. Si vous n'avez reçu aucun de ces feuillets, joignez une copie de l'état qui vous désigne comme ayantune participation dans l'entreprise.Si vous avez besoin de plus d'espace pour les parties I, IV ou V, prière de joindre une annexe.Joignez une copie complétée de ce formulaire à votre déclaration générale d'impôt et de prestations.

II. Comptes de frais de ressources au Canada

Les montants calculés à la partie I ci-dessus font partis de vos FCEC (Frais cumulatifs d'exploration au Canada) et FCAC (Frais cumulatifs d'aménagement auCanada) suivant le cas. Dans la majorité des cas, les FCBCPG (Frais cumulatifs à l'égard de biens canadiens relatifs au pétrole et au gaz) sont pertinentsseulement si vous avez un solde d'ouverture.

I. Sommaire des feuillets T101 et T5013A (Frais d'exploration et d'aménagement au Canada ayant fait l'objet d'une renonciation)

Frais d'exploration au Canada (FEC) Frais d'aménagement au Canada (FAC)

Renonciation Montant d'aide Renonciation Montant d'aideN° d'identification (*)

Total

Frais admissiblesaux fins du CII

Partie d'une réduction donnantlieu à une période sans intérêt

Inscrivez le total des montants reportés à la case 130 devos feuillets T101 ou T5013A

Partie donnant lieu à une période sans intérêt

Inscrivez le total des montants reportés à la case 129 de vos feuillets T101ou T5013A.

Numéro d'identification sur le formulaire T101 – État des frais de ressources ou le numéro d'identification de la société de personnes dans le formulaire

T5013 – État des revenus d'une société de personnes pour les abris fiscaux et les frais de ressources ayant fait l'objet d'une renonciation.(*)

(1)Solde au début de l'année

Ajoutez : Total des renonciations de l'année courante calculé à la partie I

Total partiel (2)

Déduire : Total du montant d'aide à la partie I

Crédit d'impôt à l'investissement fédéral demandé de l'année précédente

Crédit d'impôt provincial lié aux actions accréditives reçu ou en droit de recevoir

Montant d'aide (feuillet T5013 : cases 96 à 98)

Autre frais de ressources (feuillet T5013 : cases 90 à 92)

Autre (précisez)

FCEC FCAC FCBCPG

Autre (précisez)

Total partiel (3)

Frais d'exploration et d'aménagement au Canada demandé (somme des montants demandés à la ligne B ci-dessus)

Frais d'exploration et d'aménagement à l'étranger demandé (annexez une cédule pour le montant demandé)

Autre frais (p. ex. droits à la Couronne)

Déduction relative aux ressources

Frais d'exploration et aménagement total (inscrivez ce montant à la ligne 224 de votre déclaration)

+

IV. Frais admissibles aux fins du crédit d'impôt à l'investissement (lisez la ligne 412 du guide général d'impôt et de prestations)

Frais admissibles aux fins du crédit d'impôt à l'investissement calculé à la partie I

Déduire : Crédit d'impôt provincial lié aux actions accréditives reçu ou en droit de recevoir –

=

=

V. Déductions pour épuisement (précisez) (lisez la ligne 232 du guide général d'impôt et de prestations)(inscrivez le montant à la ligne 232 de votre déclaration)

*Taux d'inclusion : avant 2003 – 100 %; 2003 – 90 %; 2004 – 75 %; 2005 – 65 %; 2006 – 35 %; après 2006 – 0 %)

Frais admissibles aux fins du crédit d'impôt à l'investissement

(Inscrivez ce montant à la ligne 6717 de votre formulaire T2038(IND))

=

Bénéfices relatifs aux ressources X taux d'inclusion * X 25 % =

(This form is available in English.)

Taux

(4)Frais d'exploration et d'aménagement maximum disponible pour déduction

(Si négatif, inscrivez zéro)

Frais d'exploration et d'aménagement demandé

Inscrivez le montant calculé à la ligne (4) ou un montant moindre

B

Solde à la fin de l'année [A - B]

Solde disponible

(Si négatif pour FCEC ou FCAC, inscrivez ce montant à la ligne 130 de votre

déclaration, un solde de FCBCPG négatif réduit votre FCAC en premier)A[(1)+(2)-(3)]

III. Frais d'exploration et aménagement (lisez la ligne 224 du guide général d'impôt et de prestations)

X 100 % X 30 % X 10 %

+

+

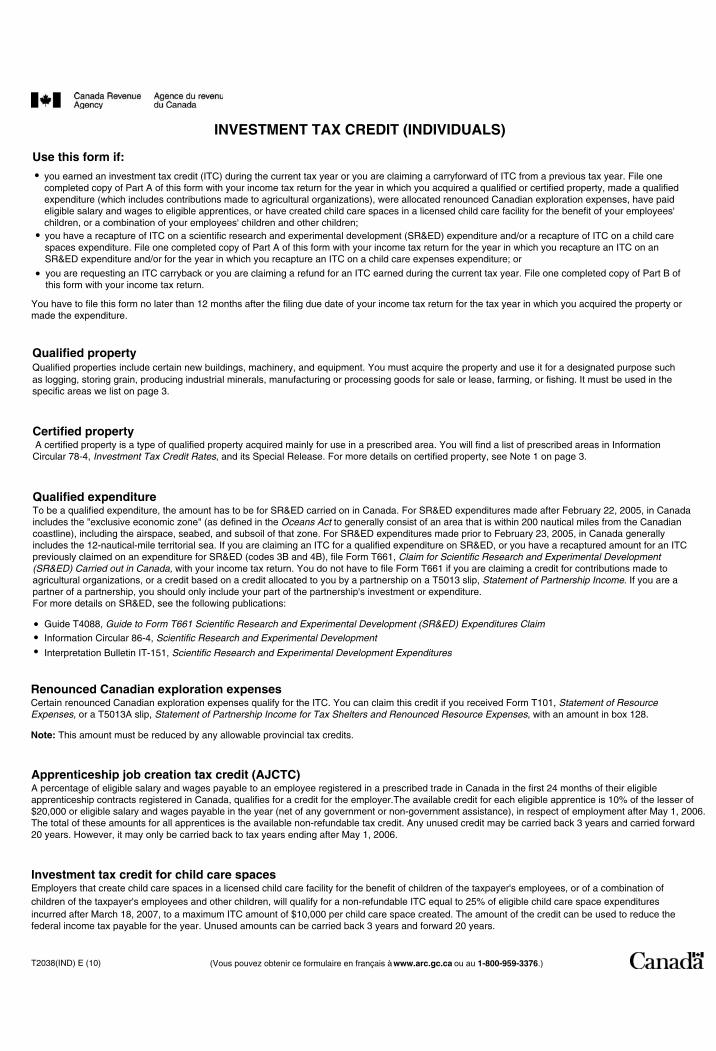

Investment tax credit for child care spacesEmployers that create child care spaces in a licensed child care facility for the benefit of children of the taxpayer's employees, or of a combination ofchildren of the taxpayer's employees and other children, will qualify for a non-refundable ITC equal to 25% of eligible child care space expendituresincurred after March 18, 2007, to a maximum ITC amount of $10,000 per child care space created. The amount of the credit can be used to reduce thefederal income tax payable for the year. Unused amounts can be carried back 3 years and forward 20 years.

Apprenticeship job creation tax credit (AJCTC)A percentage of eligible salary and wages payable to an employee registered in a prescribed trade in Canada in the first 24 months of their eligibleapprenticeship contracts registered in Canada, qualifies for a credit for the employer.The available credit for each eligible apprentice is 10% of the lesser of$20,000 or eligible salary and wages payable in the year (net of any government or non-government assistance), in respect of employment after May 1, 2006.The total of these amounts for all apprentices is the available non-refundable tax credit. Any unused credit may be carried back 3 years and carried forward20 years. However, it may only be carried back to tax years ending after May 1, 2006.

(Vous pouvez obtenir ce formulaire en français à www.arc.gc.ca ou au 1-800-959-3376.)

You have to file this form no later than 12 months after the filing due date of your income tax return for the tax year in which you acquired the property ormade the expenditure.

T2038(IND) E (10)

INVESTMENT TAX CREDIT (INDIVIDUALS)

Use this form if:

Guide T4088, Guide to Form T661 Scientific Research and Experimental Development (SR&ED) Expenditures Claim

Information Circular 86-4, Scientific Research and Experimental Development

Interpretation Bulletin IT-151, Scientific Research and Experimental Development Expenditures

you earned an investment tax credit (ITC) during the current tax year or you are claiming a carryforward of ITC from a previous tax year. File onecompleted copy of Part A of this form with your income tax return for the year in which you acquired a qualified or certified property, made a qualifiedexpenditure (which includes contributions made to agricultural organizations), were allocated renounced Canadian exploration expenses, have paideligible salary and wages to eligible apprentices, or have created child care spaces in a licensed child care facility for the benefit of your employees'children, or a combination of your employees' children and other children;you have a recapture of ITC on a scientific research and experimental development (SR&ED) expenditure and/or a recapture of ITC on a child carespaces expenditure. File one completed copy of Part A of this form with your income tax return for the year in which you recapture an ITC on anSR&ED expenditure and/or for the year in which you recapture an ITC on a child care expenses expenditure; or

you are requesting an ITC carryback or you are claiming a refund for an ITC earned during the current tax year. File one completed copy of Part B ofthis form with your income tax return.

�

�

�

�

��

Certified property A certified property is a type of qualified property acquired mainly for use in a prescribed area. You will find a list of prescribed areas in InformationCircular 78-4, Investment Tax Credit Rates, and its Special Release. For more details on certified property, see Note 1 on page 3.

Qualified propertyQualified properties include certain new buildings, machinery, and equipment. You must acquire the property and use it for a designated purpose suchas logging, storing grain, producing industrial minerals, manufacturing or processing goods for sale or lease, farming, or fishing. It must be used in thespecific areas we list on page 3.

Qualified expenditureTo be a qualified expenditure, the amount has to be for SR&ED carried on in Canada. For SR&ED expenditures made after February 22, 2005, in Canadaincludes the "exclusive economic zone" (as defined in the Oceans Act to generally consist of an area that is within 200 nautical miles from the Canadiancoastline), including the airspace, seabed, and subsoil of that zone. For SR&ED expenditures made prior to February 23, 2005, in Canada generallyincludes the 12-nautical-mile territorial sea. If you are claiming an ITC for a qualified expenditure on SR&ED, or you have a recaptured amount for an ITCpreviously claimed on an expenditure for SR&ED (codes 3B and 4B), file Form T661, Claim for Scientific Research and Experimental Development(SR&ED) Carried out in Canada, with your income tax return. You do not have to file Form T661 if you are claiming a credit for contributions made toagricultural organizations, or a credit based on a credit allocated to you by a partnership on a T5013 slip, Statement of Partnership Income. If you are apartner of a partnership, you should only include your part of the partnership's investment or expenditure.For more details on SR&ED, see the following publications:

Note: This amount must be reduced by any allowable provincial tax credits.

Renounced Canadian exploration expensesCertain renounced Canadian exploration expenses qualify for the ITC. You can claim this credit if you received Form T101, Statement of ResourceExpenses, or a T5013A slip, Statement of Partnership Income for Tax Shelters and Renounced Resource Expenses, with an amount in box 128.

Page 2

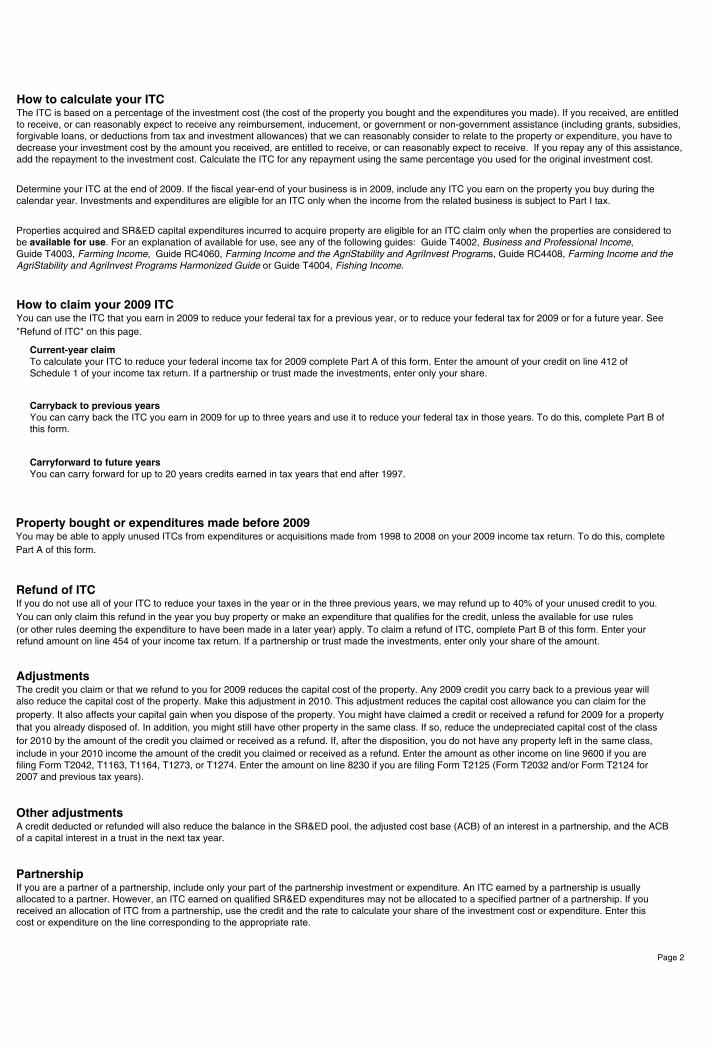

Other adjustmentsA credit deducted or refunded will also reduce the balance in the SR&ED pool, the adjusted cost base (ACB) of an interest in a partnership, and the ACBof a capital interest in a trust in the next tax year.

AdjustmentsThe credit you claim or that we refund to you for 2009 reduces the capital cost of the property. Any 2009 credit you carry back to a previous year willalso reduce the capital cost of the property. Make this adjustment in 2010. This adjustment reduces the capital cost allowance you can claim for theproperty. It also affects your capital gain when you dispose of the property. You might have claimed a credit or received a refund for 2009 for a propertythat you already disposed of. In addition, you might still have other property in the same class. If so, reduce the undepreciated capital cost of the classfor 2010 by the amount of the credit you claimed or received as a refund. If, after the disposition, you do not have any property left in the same class,include in your 2010 income the amount of the credit you claimed or received as a refund. Enter the amount as other income on line 9600 if you arefiling Form T2042, T1163, T1164, T1273, or T1274. Enter the amount on line 8230 if you are filing Form T2125 (Form T2032 and/or Form T2124 for2007 and previous tax years).

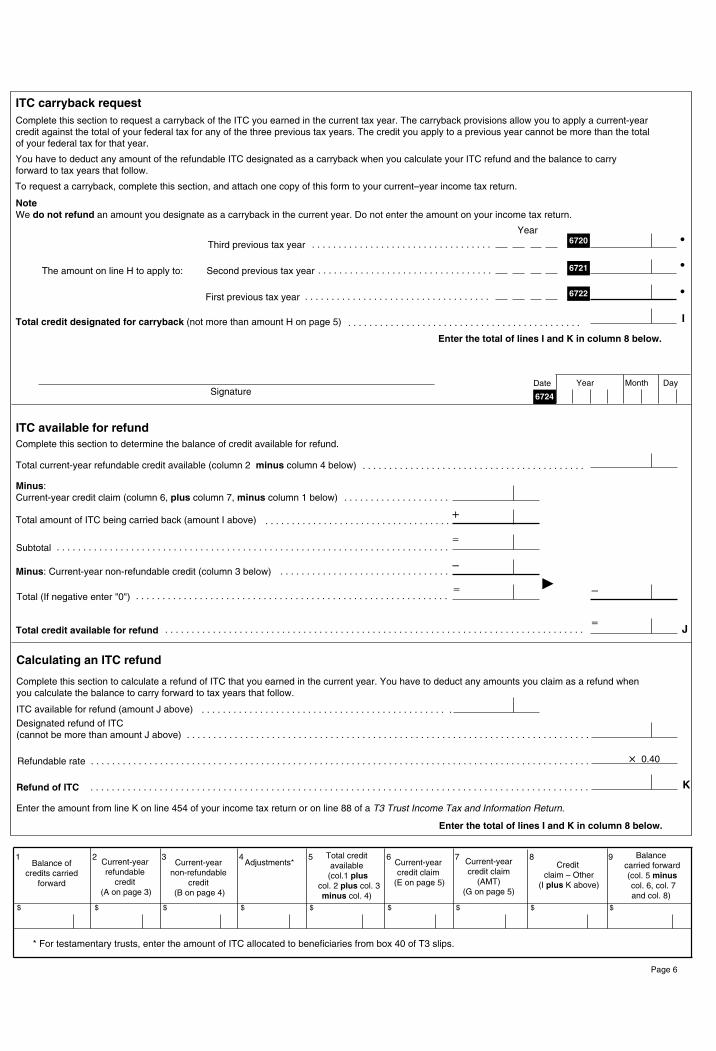

Refund of ITCIf you do not use all of your ITC to reduce your taxes in the year or in the three previous years, we may refund up to 40% of your unused credit to you.You can only claim this refund in the year you buy property or make an expenditure that qualifies for the credit, unless the available for use rules(or other rules deeming the expenditure to have been made in a later year) apply. To claim a refund of ITC, complete Part B of this form. Enter yourrefund amount on line 454 of your income tax return. If a partnership or trust made the investments, enter only your share of the amount.

PartnershipIf you are a partner of a partnership, include only your part of the partnership investment or expenditure. An ITC earned by a partnership is usuallyallocated to a partner. However, an ITC earned on qualified SR&ED expenditures may not be allocated to a specified partner of a partnership. If youreceived an allocation of ITC from a partnership, use the credit and the rate to calculate your share of the investment cost or expenditure. Enter thiscost or expenditure on the line corresponding to the appropriate rate.

Property bought or expenditures made before 2009You may be able to apply unused ITCs from expenditures or acquisitions made from 1998 to 2008 on your 2009 income tax return. To do this, completePart A of this form.

Carryback to previous yearsYou can carry back the ITC you earn in 2009 for up to three years and use it to reduce your federal tax in those years. To do this, complete Part B ofthis form.

Properties acquired and SR&ED capital expenditures incurred to acquire property are eligible for an ITC claim only when the properties are considered tobe available for use. For an explanation of available for use, see any of the following guides: Guide T4002, Business and Professional Income,Guide T4003, Farming Income, Guide RC4060, Farming Income and the AgriStability and AgriInvest Programs, Guide RC4408, Farming Income and theAgriStability and AgriInvest Programs Harmonized Guide or Guide T4004, Fishing Income.

How to claim your 2009 ITCYou can use the ITC that you earn in 2009 to reduce your federal tax for a previous year, or to reduce your federal tax for 2009 or for a future year. See"Refund of ITC" on this page.

Determine your ITC at the end of 2009. If the fiscal year-end of your business is in 2009, include any ITC you earn on the property you buy during thecalendar year. Investments and expenditures are eligible for an ITC only when the income from the related business is subject to Part I tax.

Carryforward to future yearsYou can carry forward for up to 20 years credits earned in tax years that end after 1997.

Current-year claimTo calculate your ITC to reduce your federal income tax for 2009 complete Part A of this form. Enter the amount of your credit on line 412 ofSchedule 1 of your income tax return. If a partnership or trust made the investments, enter only your share.

How to calculate your ITCThe ITC is based on a percentage of the investment cost (the cost of the property you bought and the expenditures you made). If you received, are entitledto receive, or can reasonably expect to receive any reimbursement, inducement, or government or non-government assistance (including grants, subsidies,forgivable loans, or deductions from tax and investment allowances) that we can reasonably consider to relate to the property or expenditure, you have todecrease your investment cost by the amount you received, are entitled to receive, or can reasonably expect to receive. If you repay any of this assistance,add the repayment to the investment cost. Calculate the ITC for any repayment using the same percentage you used for the original investment cost.

Part A – Calculating an investment tax credit (ITC)

Calculating the current–year refundable credits – Tick the appropriate box.

}Code 3B

�

Page 3

Total expenditure

Total expenditureCode 4B

Code 3B

(Note 2 on this page)

Incurred after 1994(Note 2 on this page)

. . . . . . . . . . . . . . . . .

Code 4CIncurred after 2000(Note 5 on this page) . . . . . . . . . . . . . . . . . . . . .

Code 12 Acquired after 1994 . . . . . . . . . . . . . . . . . . . . .

Code 12 Total investment(Note 3 on this page) . . . . . . . . . . . . . . . . . . . . .

Enter the total from line A in column 2 on page 6.Total current–year refundable credits – . . . . . . . . . . . . . . . . . . . . . . . . . . .

} . . . . . . . . . . . . . . . . .Total investmentCode 3A

(Note 2 on this page) Total expenditure

(Note 1 on this page)

A

6710

6712

6715

6714

6716

� 0.30 �

� 0.20 �

� 0.20 �

� 0.10 �

� 0.15 �

Total expenditure

Total investment

�

�

�

�

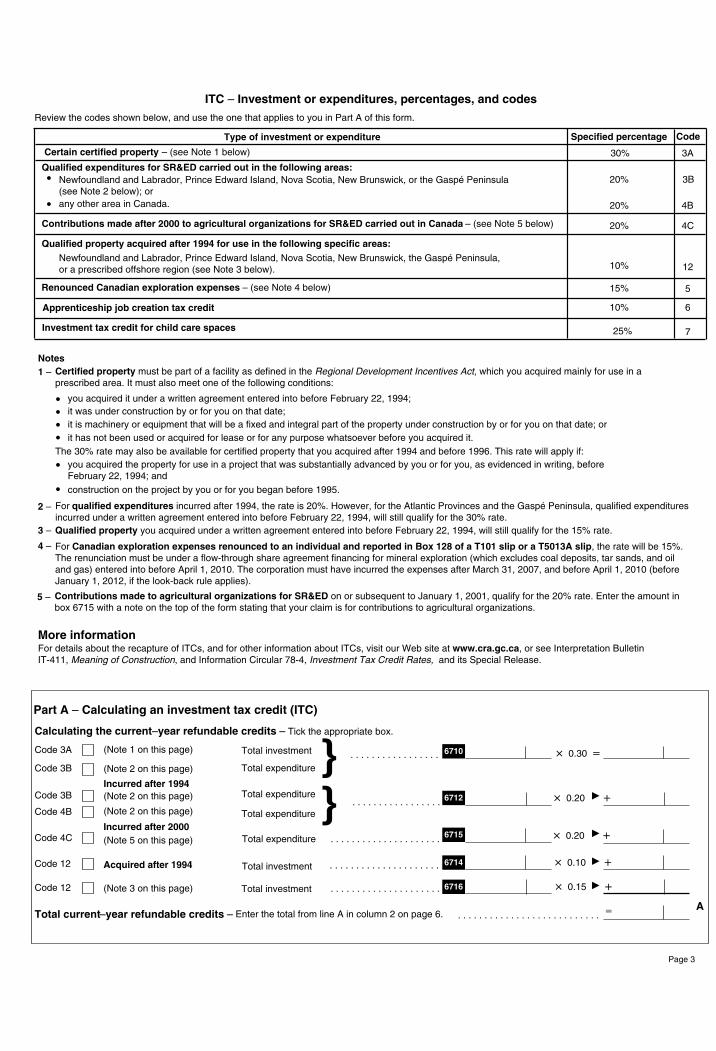

construction on the project by you or for you began before 1995.

Notes

More informationFor details about the recapture of ITCs, and for other information about ITCs, visit our Web site at www.cra.gc.ca, or see Interpretation BulletinIT-411, Meaning of Construction, and Information Circular 78-4, Investment Tax Credit Rates, and its Special Release.

Contributions made to agricultural organizations for SR&ED on or subsequent to January 1, 2001, qualify for the 20% rate. Enter the amount inbox 6715 with a note on the top of the form stating that your claim is for contributions to agricultural organizations.

Certified property must be part of a facility as defined in the Regional Development Incentives Act, which you acquired mainly for use in aprescribed area. It must also meet one of the following conditions:

1 –

For qualified expenditures incurred after 1994, the rate is 20%. However, for the Atlantic Provinces and the Gaspé Peninsula, qualified expendituresincurred under a written agreement entered into before February 22, 1994, will still qualify for the 30% rate.

2 –

Qualified property you acquired under a written agreement entered into before February 22, 1994, will still qualify for the 15% rate.3 –

For Canadian exploration expenses renounced to an individual and reported in Box 128 of a T101 slip or a T5013A slip, the rate will be 15%.The renunciation must be under a flow-through share agreement financing for mineral exploration (which excludes coal deposits, tar sands, and oiland gas) entered into before April 1, 2010. The corporation must have incurred the expenses after March 31, 2007, and before April 1, 2010 (beforeJanuary 1, 2012, if the look-back rule applies).

4 –

you acquired it under a written agreement entered into before February 22, 1994;

it has not been used or acquired for lease or for any purpose whatsoever before you acquired it.

����

5 –

it is machinery or equipment that will be a fixed and integral part of the property under construction by or for you on that date; orit was under construction by or for you on that date;

you acquired the property for use in a project that was substantially advanced by you or for you, as evidenced in writing, beforeFebruary 22, 1994; and

The 30% rate may also be available for certified property that you acquired after 1994 and before 1996. This rate will apply if:

�

�

10%

5

10%

3B

Newfoundland and Labrador, Prince Edward Island, Nova Scotia, New Brunswick, the Gaspé Peninsula,or a prescribed offshore region (see Note 3 below).

Newfoundland and Labrador, Prince Edward Island, Nova Scotia, New Brunswick, or the Gaspé Peninsula(see Note 2 below); or

Review the codes shown below, and use the one that applies to you in Part A of this form.

ITC – Investment or expenditures, percentages, and codes

Qualified expenditures for SR&ED carried out in the following areas:

CodeSpecified percentage

3A30%

12

20%

4B20%

Type of investment or expenditure

15%

6

20% 4C

any other area in Canada.

Contributions made after 2000 to agricultural organizations for SR&ED carried out in Canada – (see Note 5 below)

Qualified property acquired after 1994 for use in the following specific areas:

25% 7

�

�

Renounced Canadian exploration expenses – (see Note 4 below)

Certain certified property – (see Note 1 below)

Apprenticeship job creation tax credit

Investment tax credit for child care spaces

Page 4

Amount of expenditure on which ITC is recaptured at 30% (see "Qualified expenditure" on thefirst page). Do not enter more than the amount of the original expenditure (i)

Recapture of ITC on SR&ED expenditures

(ii)Amount of expenditure on which ITC is recaptured at 20% (see "Qualified expenditure" on thefirst page). Do not enter more than the amount of the original expenditure

Add the amount on line (7) to the amount on line 406 of Schedule 1 of your income tax return.

�Total recaptured credits – Amount from line 6730, plus line (i), plus line (ii)

6713

6711

� 0.20 �

� 0.30 � . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . .

�

�

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Enter the amount from line 6730 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Recapture – ITC for child care spacesIf, at any time within 60 months of the day that you create a new child care space, that space is no longer available, or if the property acquired for a childcare space is leased for any purpose or converted to another use, we will recover the ITC for that space or property.

The amount of the recovery will be:

25% of the proceeds of disposition of the eligible property (or 25% of fairmarket value if disposed of to a non-arm's length party)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total recapture of investment tax credit for child care spaces (add line 3 and line 6)

3

4

6730

If only child care spaces are disposed of, the amount originally claimed for those child care spaces . . . . . . . . . . . . . . . . . . . . . . . .

If property other than child care spaces is disposed of:

Amount originally claimed for ITC for the property disposed of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5

6The lesser of line 4 and line 5

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

�

�

Enter the lesser of line 1 and line 2

B

Total amount of current year expenditures

Investment tax credit for child care spaces

Total number of child care spaces created

Eligible child care space expenditures include the cost of depreciable property, and the amount of specified child care start–up expenditures acquired orincurred solely for the purpose of the creation of the new child care spaces at a licensed child care facility.

Code 7

– Enter the total from line B in column 3 on page 6.Total current-year non-refundable credits

. . . . . . . . . . . . . . . . .

$40,000

. . . . . . . . . . . . . . . . . . . . . . . . . 6719

1

2� �

� 0.25 �

�

�

For each apprentice in their first 24 months of the apprenticeship, enter the apprenticeship contract number registered with Canada, or a province or territoryof Canada, under an apprenticeship program designed to certify or license individuals in the trade. If there is no contract number, enter the SIN or the nameof the eligible apprentice. Then, enter the name of the eligible trade and the eligible salary and wages ** payable in the year in respect of employment afterMay 1, 2006. The credit is 10% of the total of the amounts in column C. Attach a note if more space is required.

1.

2.

3.

Name of eligible trade

BEligible salary and wages ** payable

in the year, or $20,000, whichever is less

Contract number(SIN or name of apprentice)

A

Total of amounts in column C

** Net of any government or non-government assistance received or to be received in respect of eligible salary and wages.

Code 6 Apprenticeship job creation tax credit

6718

C

� 0.10 ��

If your apprentice works for you and also works for a related employer as defined under subsection 251(2), all related employers have to agree in writing thatyou are the only employer who will be claiming the apprenticeship job creation tax credit for this tax year for each apprentice whose contract number, socialinsurance number (SIN), or name appears below.

Calculating the current-year non-refundable credits – Tick the appropriate box.

Code 5 (Note 4 on page 3) . . . . . . . . . . . . . . . . . . . . . . .Total expense 6717 � 0.15 *

* This credit will reduce your Canadian exploration expense pool in the year following the year in which you claim the credit.

�

. . . . . . . . . . . . . . . . . . . . . . . .

7

Page 5

Part B – Calculating a carryback and refund of ITC

* To arrive at the amount available to carry back, you first have to apply your credit to the fullest extent in the current year, whether you claimed all of it or not. This means that, before determining the amount available to carry back, you first have to reduce your federal tax for the current year by the maximum amounts you could have claimed in columns 6 and 7, whether you claimed the maximum or not.

ITC available for carryback

Complete this section to determine the balance of credit available for carryback to previous tax years.

HTotal credit available for carryback

Minus: Current-year credit applicable*

Total current-year credit available (column 5 minus column 1 on page 6)

The maximum amounts you could have claimed in column 6, plus column 7, minus column 1 on page 6(if negative, enter 0)

�

�. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Enter the amount from line G on line 412 of Schedule 1 of your income tax return, or on line 37 of T3 Schedule 11. Also enter the amount from line G incolumn 7 on page 6.

Calculating an allowable claim if alternative minimum tax (AMT) appliesComplete this section only if you calculate an amount greater than zero on line 94 of Form T691.

Enter the amount from line D

F

GYou can claim an ITC amount up to, but not more than, line C or F, whichever is less.Enter your claim on this line

Plus: Federal foreign tax credit (from line 405 on Schedule 1 of your income tax return)

Subtotal – if negative, enter 0

Minus: "Minimum amount" from line 58 of Form T691

�

�

�

�

�. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Subtotal

If you do not have to complete Form T691, Alternative Minimum Tax (AMT), (see your guide for information) or if the amount you calculate on line 94 ofForm T691 is zero, enter the amount from line E on line 412 of Schedule 1 of your income tax return, or on line 37 of T3 Schedule 11. If AMT does notapply, enter the amount from line E in column 6 on page 6 of this form.

Calculating an allowable claim

Otherwise, complete the following section to determine your ITC claim and enter "0" in column 6 on page 6 of this form.

Enter the total credit available from column 5 on page 6 of the form C

Minus: Labour–sponsored funds tax credit (from line 414 of Schedule 1 of your income tax return)

EYou can claim an ITC amount up to, but not more than, line C or D, whichever is less. Enter your claim on this line

Federal tax (from line 406 of Schedule 1 of your income tax return)

Minus: Federal political contribution tax credit (from line 410 of Schedule 1 of your income tax return)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

D��

�

�

�. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Subtotal

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Subtotal

. . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . .

Page 6

� 0.40

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Refundable rate

Enter the amount from line K on line 454 of your income tax return or on line 88 of a T3 Trust Income Tax and Information Return.

Enter the total of lines I and K in column 8 below.

ITC available for refund (amount J above)

Refund of ITC

Designated refund of ITC(cannot be more than amount J above)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

K

Calculating an ITC refund

Complete this section to calculate a refund of ITC that you earned in the current year. You have to deduct any amounts you claim as a refund whenyou calculate the balance to carry forward to tax years that follow.

Adjustments*

* For testamentary trusts, enter the amount of ITC allocated to beneficiaries from box 40 of T3 slips.

$

Balance ofcredits carried

forward

Current-yearrefundable

credit (A on page 3)

Balance carried forward (col. 5 minus col. 6, col. 7

and col. 8)

Total creditavailable

(col.1 plus col. 2 plus col. 3

minus col. 4)

Credit claim – Other

(I plus K above)

Current-yearcredit claim

(AMT)(G on page 5)

1Current-yearcredit claim

(E on page 5)

4Current-year

non-refundablecredit

(B on page 4)

$

2 3 5 6 7 8 9

$$ $$ $ $ $

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

�

�

�

�

�

�

�

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . .

Complete this section to determine the balance of credit available for refund.

Current-year credit claim (column 6, plus column 7, minus column 1 below)

Total current-year refundable credit available (column 2 minus column 4 below)

ITC available for refund

Total credit available for refund

Minus:

Total amount of ITC being carried back (amount I above)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Minus: Current-year non-refundable credit (column 3 below)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

J

Subtotal

Total (If negative enter "0")

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6720

�

First previous tax year