TAX IN PRACTICE - Practising Tax · Practising Tax Pty Ltd 23 September 2013...

29

TAX IN PRACTICE MEANS TESTING THE PRIVATE HEALTH INSURANCE OFFSET

Transcript of TAX IN PRACTICE - Practising Tax · Practising Tax Pty Ltd 23 September 2013...

TAX IN PRACTICE

MEANS TESTING THE PRIVATE HEALTH

INSURANCE OFFSET

© 2013 Practising Tax Pty Ltd. Except as permitted by the Copyright Act 1968, these materials must not

be reproduced in whole or in part without the express written consent of Practising Tax Pty Ltd.

These materials are intended to be used as a guide only. They should not be relied upon as a substitute

for professional advice regarding actual facts or circumstances.

Practising Tax Pty Ltd, its employees and agents do not accept any liability for any injury, loss or damage

resulting from any person acting, or refraining to act, in reliance on all or part of these materials.

ABOUT PRACTISING TAX

Practising Tax is a specialist tax information provider. Practising Tax is a team of

passionate tax professionals with diverse experience ranging from ‘Big 4’ accounting

firms, top tier law firms, private practice, ATO and tax education providers.

Practising Tax is unrivalled in the quality, accuracy and approachability of its product.

We pride ourselves on ensuring that our clients get the most up-to-date, easy to

understand and practical tax information available.

CONTACT DETAILS

PO Box 6152

Hawthorn VIC 3122

Ph: (03) 9815 2998

Fax: (03) 8648 6808

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page i

TABLE OF CONTENTS

MEANS TESTING THE PRIVATE HEALTH INSURANCE REBATE ..................................... 1!

PRIVATE HEALTH INSURANCE INCENTIVE TIERS.............................................................................. 1!CALCULATING THE PRIVATE HEALTH INSURANCE REBATE ............................................................... 3!

CLAIMING THE PRIVATE HEALTH INSURANCE REBATE ............................................... 11!

COMPLETING THE INDIVIDUAL TAX RETURN ................................................................................. 11!

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 1

MEANS TESTING THE PRIVATE HEALTH INSURANCE REBATE

The private health insurance rebate provides a reduction in the cost of private health insurance premiums for people who are eligible for Medicare and who have a complying health insurance policy.

The Fairer Private Health Insurance Incentives Act 2012 amended various Acts to implement three private health insurance incentive tiers. The impact of the three private health insurance incentive tiers is, among other things, to reduce the amount of private health insurance rebate an eligible taxpayer with a complying private health insurance policy is entitled to when they have income for surcharge purposes above the relevant Medicare levy surcharge threshold.

Private health insurance incentive tiers

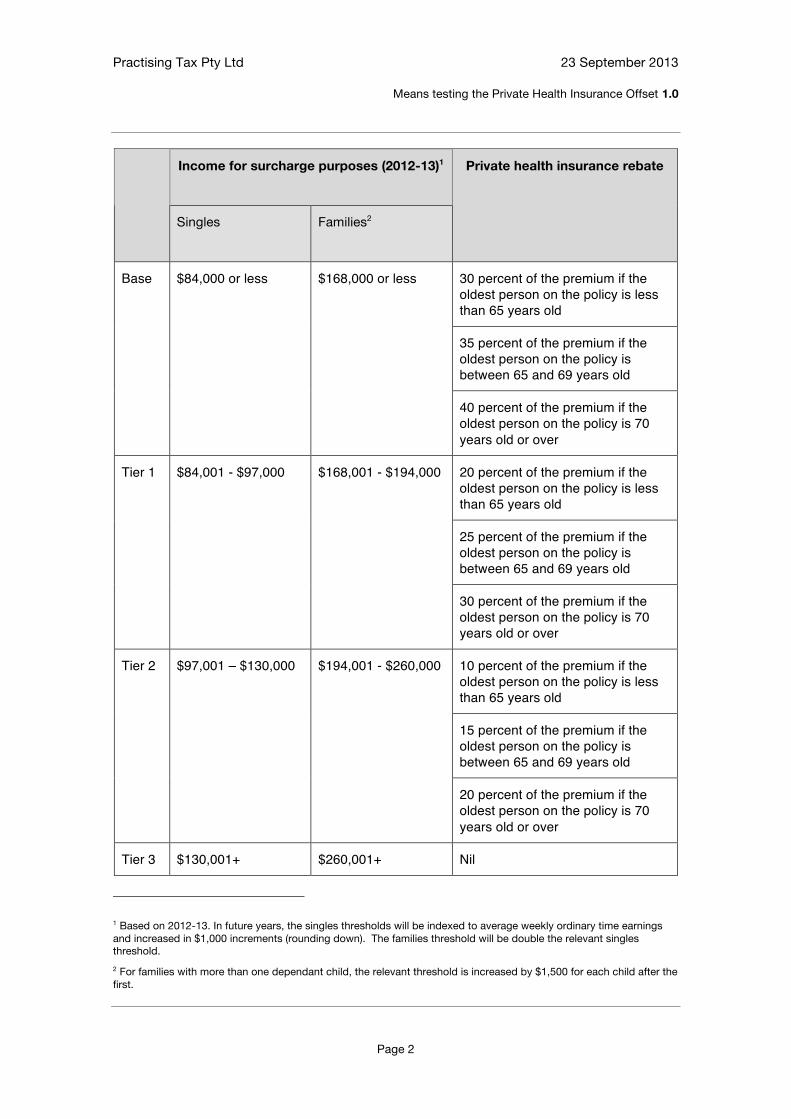

The private health insurance incentive tiers operate to means test the private health insurance rebate. The table below summaries the impact of the three private health insurance incentive tiers:

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 2

Income for surcharge purposes (2012-13)1

Singles Families2

Private health insurance rebate

30 percent of the premium if the oldest person on the policy is less than 65 years old

35 percent of the premium if the oldest person on the policy is between 65 and 69 years old

Base $84,000 or less $168,000 or less

40 percent of the premium if the oldest person on the policy is 70 years old or over

20 percent of the premium if the oldest person on the policy is less than 65 years old

25 percent of the premium if the oldest person on the policy is between 65 and 69 years old

Tier 1 $84,001 - $97,000 $168,001 - $194,000

30 percent of the premium if the oldest person on the policy is 70 years old or over

10 percent of the premium if the oldest person on the policy is less than 65 years old

15 percent of the premium if the oldest person on the policy is between 65 and 69 years old

Tier 2 $97,001 – $130,000 $194,001 - $260,000

20 percent of the premium if the oldest person on the policy is 70 years old or over

Tier 3 $130,001+ $260,001+ Nil

1 Based on 2012-13. In future years, the singles thresholds will be indexed to average weekly ordinary time earnings and increased in $1,000 increments (rounding down). The families threshold will be double the relevant singles threshold.

2 For families with more than one dependant child, the relevant threshold is increased by $1,500 for each child after the first.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 3

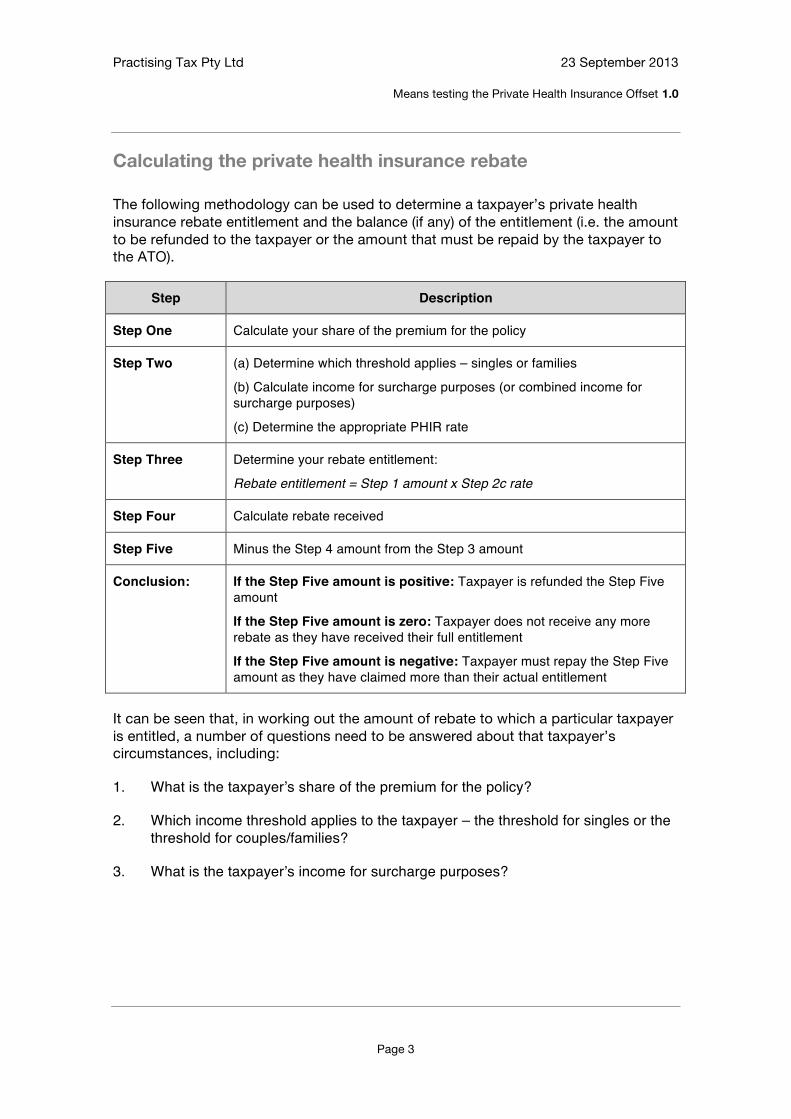

Calculating the private health insurance rebate

The following methodology can be used to determine a taxpayer’s private health insurance rebate entitlement and the balance (if any) of the entitlement (i.e. the amount to be refunded to the taxpayer or the amount that must be repaid by the taxpayer to the ATO).

Step Description

Step One Calculate your share of the premium for the policy

Step Two (a) Determine which threshold applies – singles or families

(b) Calculate income for surcharge purposes (or combined income for surcharge purposes)

(c) Determine the appropriate PHIR rate

Step Three Determine your rebate entitlement:

Rebate entitlement = Step 1 amount x Step 2c rate

Step Four Calculate rebate received

Step Five Minus the Step 4 amount from the Step 3 amount

Conclusion: If the Step Five amount is positive: Taxpayer is refunded the Step Five amount

If the Step Five amount is zero: Taxpayer does not receive any more rebate as they have received their full entitlement

If the Step Five amount is negative: Taxpayer must repay the Step Five amount as they have claimed more than their actual entitlement

It can be seen that, in working out the amount of rebate to which a particular taxpayer is entitled, a number of questions need to be answered about that taxpayer’s circumstances, including:

1. What is the taxpayer!s share of the premium for the policy?

2. Which income threshold applies to the taxpayer – the threshold for singles or the threshold for couples/families?

3. What is the taxpayer!s income for surcharge purposes?

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 4

What is the taxpayer’s share of the premium for the policy?

Important: This question effectively determines which taxpayer(s) is entitled to the

rebate, and to what extent.

The taxpayer’s share of the rebate entitlement depends on whether there is more than one adult insured under the policy:

• where there is only one adult insured under the policy – that person is entitled to apply the relevant rebate percentage to the entire premium amount;

• where there is more than one adult insured under the policy – each person is entitled to apply the relevant rebate percentage to the premium amount divided by the number of adults insured under the policy.

Singles

Where the taxpayer is the only adult insured under a singles policy, they must apply the relevant rebate percentage to the entire premium for the policy.

Couples (with or without children)

Each member of a couple insured under the same policy must apply the relevant rebate percentage to 50 percent of the premium for the policy (regardless of which member actually paid the premium).

Note: Persons that are married on the last day of the income year, and are

insured under the same policy, can elect to claim the private health

insurance tax offset on behalf of their partner, such that they will apply

the relevant rebate percentage to the entire premium for the policy

(rather than 50 percent as is the ‘normal’ rule). The choice must be

made in the person's tax return at year end.

Where such a choice is made, the other partner will not be entitled to

any rebate.

(Section 61-215)

Single parent family

The adult in a single parent family must apply the relevant rebate percentage to the entire premium for the policy.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 5

Multiple adults (not coupled)

Each adult insured under a policy must apply the relevant rebate percentage to the amount determined by dividing the premium for the policy by the number of such adults.

Dependant child only

The parents of children insured under a dependant child only policy must apply the relevant rebate percentage to 50 percent of the premium for the policy. However, if the parents of the child or children are not married, the person who pays the premium must apply the relevant rebate percentage to the entire premium.

Important: It can be seen from the above that entitlement to the rebate does not

depend on whether, and to what extent, the taxpayer has incurred an

amount in respect of the policy (with the exception of unmarried parents

in respect of a dependant child only policy).

It follows that a rebate might be available to a particular individual even if

they have not incurred any amount in respect of the policy i.e. they have

not paid any of the premiums.

Example

Felix and Jemima are divorced. They are both under 65 years old and have no children together. Felix has income of $100,000 and Jemima has income of $150,000.

They each have their own complying private health insurance policy and both nominate a 30 percent premium reduction.

It turns out that Felix is a tier 2 earner, and is therefore entitled to a private health insurance rebate of only 10 percent. As such, Felix must pay back 20 percent of the rebate entitlement he claimed as a premium reduction.

It turns out that Jemima is a tier 3 earner, and is therefore not entitled to any private health insurance rebate. As such, Jemima must pay back the entire rebate entitlement she claimed as a premium reduction.

What if Jemima pays the cost of Felix!s private health insurance policy as required under their divorce agreement?

Each adult covered by a policy is entitled to the private health insurance rebate for their share of the policy, regardless of who pays for the policy. Even if Jemima pays the cost of Felix!s policy, she can claim only a rebate for the premium paid on her policy. This also means that Felix is liable for the overpaid private health insurance rebate, notwithstanding that he did not pay for the policy.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 6

Which income threshold applies to the taxpayer – the threshold for singles or the

threshold for families?

Each adult on a private health insurance policy is income tested to determine their private health insurance entitlement rebate. An individual’s circumstances (e.g. their marital status, whether they have children etc.) will impact whether the individual is income tested under the single tier thresholds or the family tier thresholds.

Key concept – Contributing to the maintenance of a dependant child or sibling

Whether a taxpayer must look to the income thresholds for singles or the income thresholds for families depends, among other things, on whether the taxpayer has contributed to the maintenance of a dependant child or sibling at some stage during the year.

A taxpayer will have contributed to the maintenance of a dependant child or sibling for these purposes where, on any day in the financial year:

• they have contributed in a substantial way to the maintenance of that child or sibling;*

• the person being maintained is:

• a person who is under 18 years old; or

• a dependant child under the rules of the private health insurer that is not 25 years old or over, and who does not have a partner;

• the child is either:

• the taxpayer!s child (including adopted child, step-child, ex-nuptial child or a child of the person!s spouse); or

• the taxpayer!s sibling (including half brother or sister, adoptive brother or sister, step brother or sister, or foster brother or sister) who is dependant on the taxpayer for economic support

#.

According to the Explanatory Memorandum to the Fairer Private Health Insurance Incentives

Act 2011:

* An individual will be contributing to the maintenance of a child if they are providing substantial material support to that child on a regular or ongoing basis – there is no requirement that the child reside with the individual.

# To be dependent on a person for economic support, a sibling must look to that person for their care and financial wellbeing in a general sense, not merely on particular occasions. Merely looking after a sibling temporarily (e.g. while the sibling's principal care-giver is away) is not sufficient to constitute dependency. Therefore the requisite dependency relationship will rarely occur in practice, and usually will only exist where there is no-one else (for example, a parent) who has general day-to-day care of the dependent sibling.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 7

Single adults

Where a single adult meets both of the following conditions that individual’s entitlement to the private health insurance rebate will be determined based on the single tier thresholds:

• the individual is single (i.e. not married or in a de-facto relationship) as at 30 June of that income year; and

• the individual has not contributed to the maintenance of a dependant child or sibling on any day in the financial year.

Note: It can be seen that individuals who have separated from their spouses

during the year and have not contributed to the maintenance of a

dependant child or sibling at any stage during the year will compare

their income for surcharge purposes to the tiers for singles.

Couples (with or without children)

Where individuals are married or in a de-facto relationship on the last day of the year (regardless of whether they have children), their combined income for surcharge purposes will be used to determine their eligibility for the private health insurance rebate, based on the family income thresholds (increased by $1,500 for each dependant child after the first).

Single parent family

Where a single adult contributes in a substantial way to the maintenance of one or more dependant children or siblings, that individual’s entitlement to the private health insurance rebate will be determined based on the family income threshold (increased by $1,500 for each dependant child after the first).

Multiple adults (not coupled)

Each insured adult who is not otherwise married or in a de facto relationship, is income tested according to their own circumstances (either based on the single or family threshold). It follows that there may be different outcomes for each adult covered by the policy.

Dependant child only

As outlined above married (or de facto) parents of a child (or children) insured under a dependant child only policy are entitled to claim the rebate on the child (or children’s) behalf, to the extent of 50 percent each. In that case the combined income of the parents is tested against the family income threshold.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 8

Where the parents of the child are not married or in a de-facto relationship, the payer of the premium in respect of a dependant child only policy is entitled to claim the rebate (also outlined above). In that case, the payer is income tested with respect to the family tier thresholds.

What is the taxpayer’s income for surcharge purposes?

The income test for the private health insurance rebate is income for surcharge

purposes. Income for surcharge purposes is calculated as the sum of:

• taxable income (including the net amount on which family trust distribution tax has been paid);

• total reportable fringe benefits, as reported on the payment summary;

• total net investment loss (includes both net financial investment loss and net rental property loss); and

• reportable super contributions (includes both reportable employer super contributions and deductible personal super contributions),

reduced by any taxed element of a super lump sum, other than a death benefit, that does not exceed the low rate cap on super lump sum benefits (if aged 55 to 59 years).

Warning: The income test for the private health insurance rebate is not the same

as the income test for Medicare levy surcharge purposes. Unlike the

income test for Medicare levy surcharge purposes, the income test for

the private health insurance rebate does not include exempt foreign

employment income.

Single adult

A single adult simply needs to determine their own income for surcharge purposes for the financial year, to determine which tier they are in.

Single parent family

A single person who contributes to the maintenance of a dependant child or student must determine their own income for surcharge purposes to determine which tier they are in.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 9

Note: If both (separated or divorced) parents contribute to the maintenance

of the same child, each parent is income tested separately based on

the family income threshold. This is to be contrasted with the

requirement that married parents combine their income before being

assessed against the family income threshold.

Couples (with or without children)

A married or de facto couple must combine their income for surcharge purposes in order to determine which ‘family’ tier they are in.

Multiple adults (not coupled)

Where multiple adults are covered by a joint private health insurance policy, each adult must determine their income for surcharge purposes based on whether they are, independently of each other, single or a member of a couple or family.

Dependant child only

As outlined above, the individual (or individuals) entitled to the rebate in respect of a dependent child only policy depends on whether the parents of the children are married or in a de facto relationship:

• where the parents are married or in a de facto relationship and therefore each entitled to 50 percent of the rebate – their income must be combined for the purposes of determining which ‘family’ tier they are in;

• where the parents are separated or divorced such that the person who pays the premium for the policy is entitled to the rebate – that person’s income alone, or combined income if they have remarried is compared against the ‘family’ thresholds.

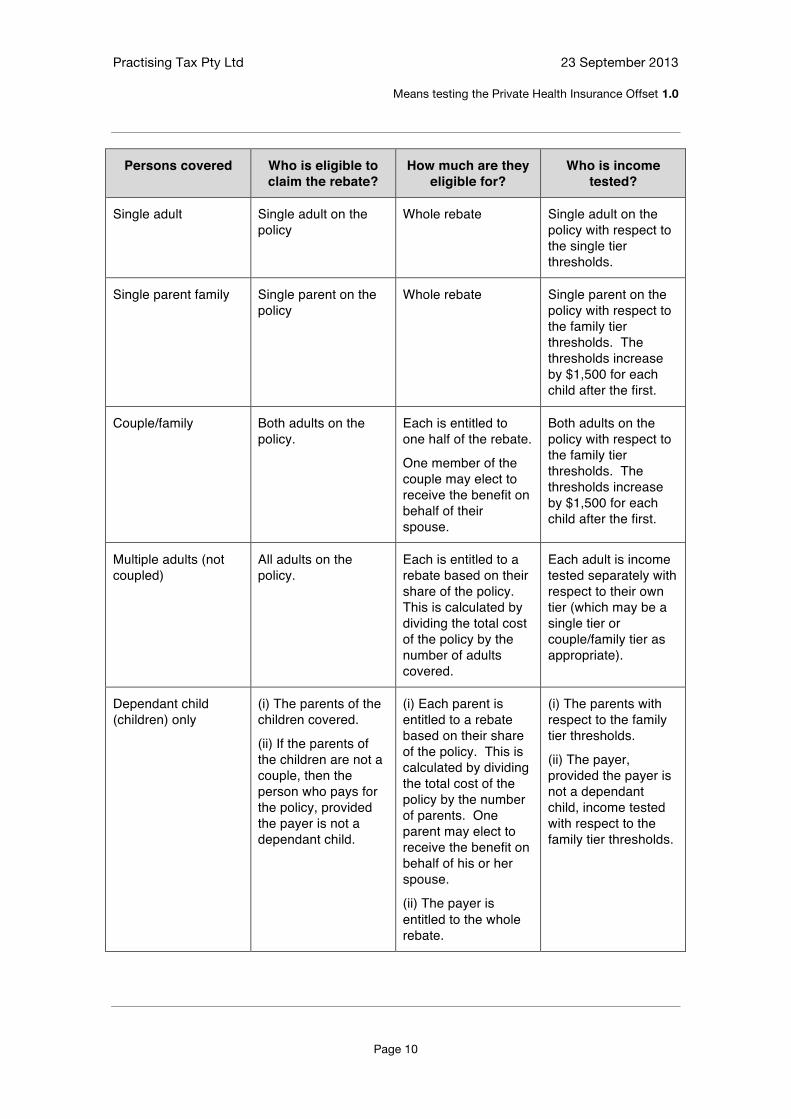

Summary

The following table (reproduced from the Explanatory Memorandum to the Fairer

Private Health Insurance Incentives Act 2011) summarises who is eligible to claim the rebate, how much they are eligible for and who is income tested.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 10

Persons covered Who is eligible to claim the rebate?

How much are they eligible for?

Who is income tested?

Single adult Single adult on the policy

Whole rebate Single adult on the policy with respect to the single tier thresholds.

Single parent family Single parent on the policy

Whole rebate Single parent on the policy with respect to the family tier thresholds. The thresholds increase by $1,500 for each child after the first.

Couple/family Both adults on the policy.

Each is entitled to one half of the rebate.

One member of the couple may elect to receive the benefit on behalf of their spouse.

Both adults on the policy with respect to the family tier thresholds. The thresholds increase by $1,500 for each child after the first.

Multiple adults (not coupled)

All adults on the policy.

Each is entitled to a rebate based on their share of the policy. This is calculated by dividing the total cost of the policy by the number of adults covered.

Each adult is income tested separately with respect to their own tier (which may be a single tier or couple/family tier as appropriate).

Dependant child (children) only

(i) The parents of the children covered.

(ii) If the parents of the children are not a couple, then the person who pays for the policy, provided the payer is not a dependant child.

(i) Each parent is entitled to a rebate based on their share of the policy. This is calculated by dividing the total cost of the policy by the number of parents. One parent may elect to receive the benefit on behalf of his or her spouse.

(ii) The payer is entitled to the whole rebate.

(i) The parents with respect to the family tier thresholds.

(ii) The payer, provided the payer is not a dependant child, income tested with respect to the family tier thresholds.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 11

CLAIMING THE PRIVATE HEALTH INSURANCE REBATE

Refundable tax offset or tax liability?

The amount of an individual’s private health insurance rebate entitlement will be determined when lodging their tax return.

A taxpayer will receive a refundable tax offset if they have not received their full private health insurance rebate as a premium reduction. The tax offset will be listed on the taxpayer’s notice of assessment.

Tip: In some circumstances it may be necessary to lodge a tax return for no

reason other than to claim the tax offset (see illustration below).

Where a taxpayer has claimed too much private health insurance rebate, the ATO will recover the amount as a tax liability. The liability will be listed on the taxpayer’s notice of assessment as Excess private health insurance refund or reduction

(rebate reduced).

Completing the individual tax return

The private health insurance policy details item of the individual tax return must be completed if at any time during the income year:

• the taxpayer was covered by a private health insurance policy; or

• the taxpayer paid for a dependant child-only policy.

A private health insurance statement is needed to complete the Private health insurance policy details item. Each adult covered by a private health insurance policy will receive their own private health insurance statement from the insurer.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 12

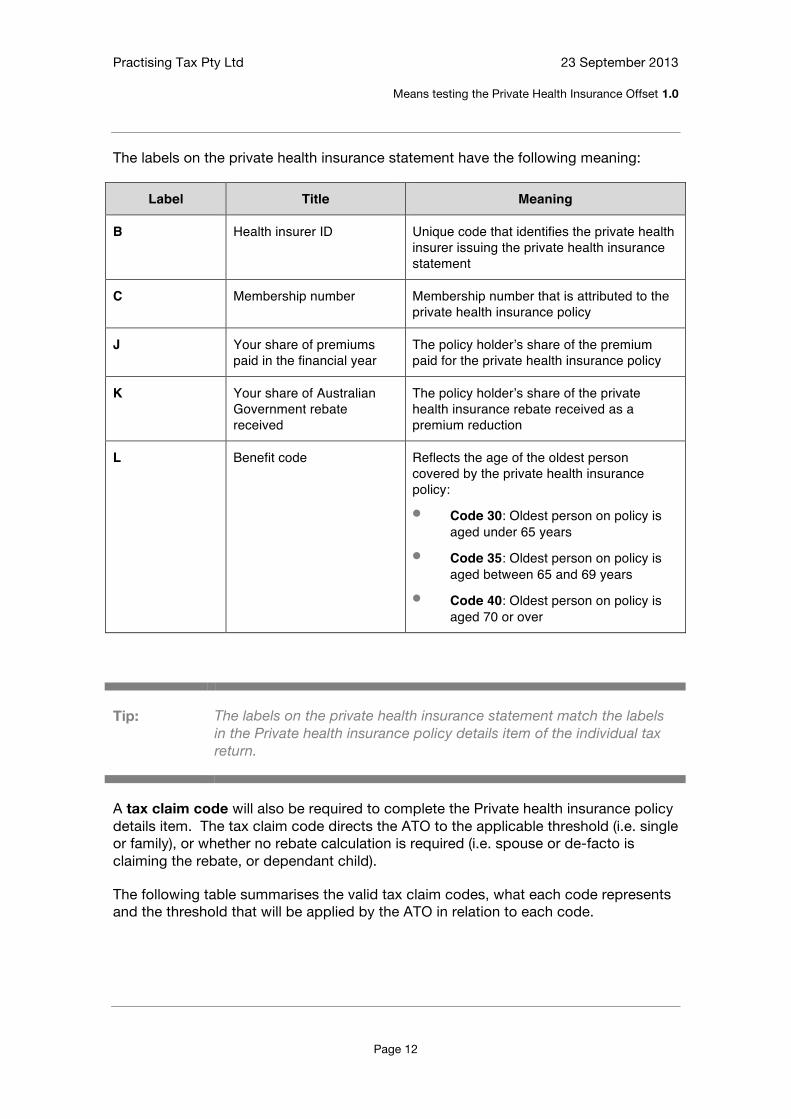

The labels on the private health insurance statement have the following meaning:

Label Title Meaning

B Health insurer ID Unique code that identifies the private health insurer issuing the private health insurance statement

C Membership number Membership number that is attributed to the private health insurance policy

J Your share of premiums paid in the financial year

The policy holder!s share of the premium paid for the private health insurance policy

K Your share of Australian Government rebate received

The policy holder!s share of the private health insurance rebate received as a premium reduction

L Benefit code Reflects the age of the oldest person covered by the private health insurance policy:

• Code 30: Oldest person on policy is aged under 65 years

• Code 35: Oldest person on policy is aged between 65 and 69 years

• Code 40: Oldest person on policy is aged 70 or over

Tip: The labels on the private health insurance statement match the labels

in the Private health insurance policy details item of the individual tax

return.

A tax claim code will also be required to complete the Private health insurance policy details item. The tax claim code directs the ATO to the applicable threshold (i.e. single or family), or whether no rebate calculation is required (i.e. spouse or de-facto is claiming the rebate, or dependant child).

The following table summarises the valid tax claim codes, what each code represents and the threshold that will be applied by the ATO in relation to each code.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 13

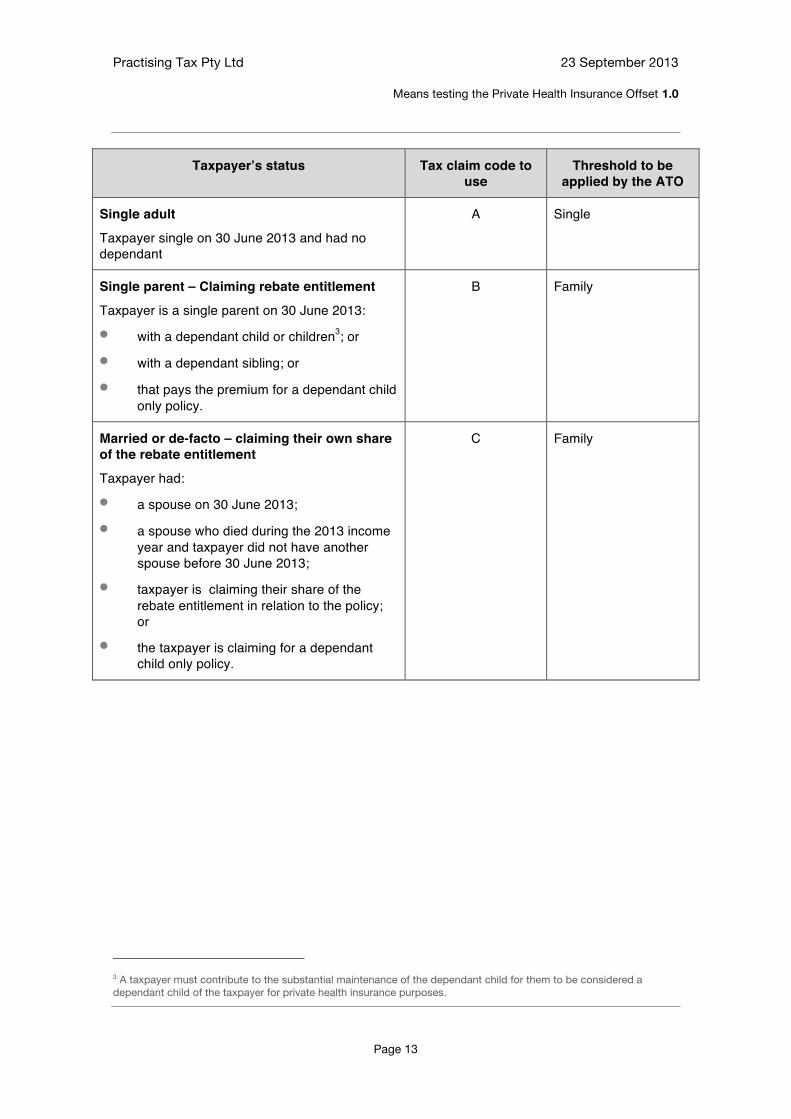

Taxpayer!s status Tax claim code to use

Threshold to be applied by the ATO

Single adult

Taxpayer single on 30 June 2013 and had no dependant

A Single

Single parent – Claiming rebate entitlement

Taxpayer is a single parent on 30 June 2013:

• with a dependant child or children3; or

• with a dependant sibling; or

• that pays the premium for a dependant child only policy.

B Family

Married or de-facto – claiming their own share of the rebate entitlement

Taxpayer had:

• a spouse on 30 June 2013;

• a spouse who died during the 2013 income year and taxpayer did not have another spouse before 30 June 2013;

• taxpayer is claiming their share of the rebate entitlement in relation to the policy; or

• the taxpayer is claiming for a dependant child only policy.

C Family

3 A taxpayer must contribute to the substantial maintenance of the dependant child for them to be considered a dependant child of the taxpayer for private health insurance purposes.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 14

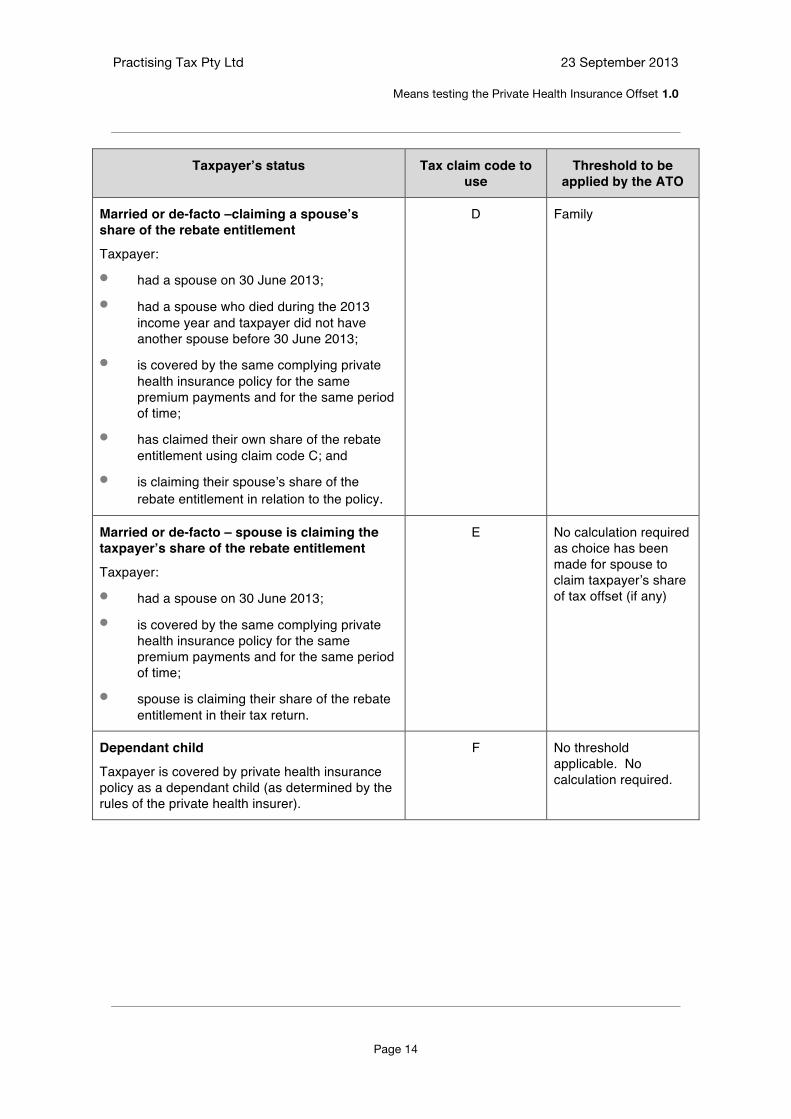

Taxpayer!s status Tax claim code to use

Threshold to be applied by the ATO

Married or de-facto –claiming a spouse!s share of the rebate entitlement

Taxpayer:

• had a spouse on 30 June 2013;

• had a spouse who died during the 2013 income year and taxpayer did not have another spouse before 30 June 2013;

• is covered by the same complying private health insurance policy for the same premium payments and for the same period of time;

• has claimed their own share of the rebate entitlement using claim code C; and

• is claiming their spouse!s share of the

rebate entitlement in relation to the policy.

D Family

Married or de-facto – spouse is claiming the taxpayer!s share of the rebate entitlement

Taxpayer:

• had a spouse on 30 June 2013;

• is covered by the same complying private health insurance policy for the same premium payments and for the same period of time;

• spouse is claiming their share of the rebate entitlement in their tax return.

E No calculation required as choice has been made for spouse to claim taxpayer!s share of tax offset (if any)

Dependant child

Taxpayer is covered by private health insurance policy as a dependant child (as determined by the rules of the private health insurer).

F No threshold applicable. No calculation required.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 15

Completing the individual tax return – Illustrations

Single adults

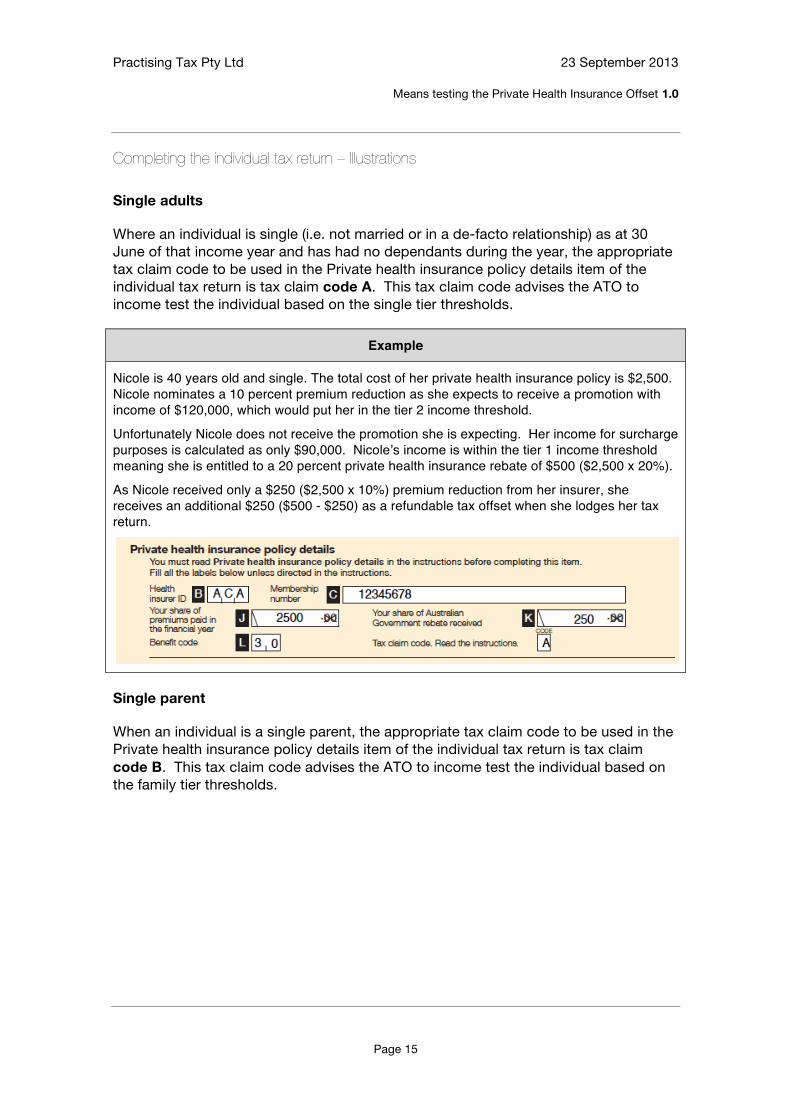

Where an individual is single (i.e. not married or in a de-facto relationship) as at 30 June of that income year and has had no dependants during the year, the appropriate tax claim code to be used in the Private health insurance policy details item of the individual tax return is tax claim code A. This tax claim code advises the ATO to income test the individual based on the single tier thresholds.

Example

Nicole is 40 years old and single. The total cost of her private health insurance policy is $2,500. Nicole nominates a 10 percent premium reduction as she expects to receive a promotion with income of $120,000, which would put her in the tier 2 income threshold.

Unfortunately Nicole does not receive the promotion she is expecting. Her income for surcharge purposes is calculated as only $90,000. Nicole!s income is within the tier 1 income threshold meaning she is entitled to a 20 percent private health insurance rebate of $500 ($2,500 x 20%).

As Nicole received only a $250 ($2,500 x 10%) premium reduction from her insurer, she receives an additional $250 ($500 - $250) as a refundable tax offset when she lodges her tax return.

Single parent

When an individual is a single parent, the appropriate tax claim code to be used in the Private health insurance policy details item of the individual tax return is tax claim

code B. This tax claim code advises the ATO to income test the individual based on the family tier thresholds.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 16

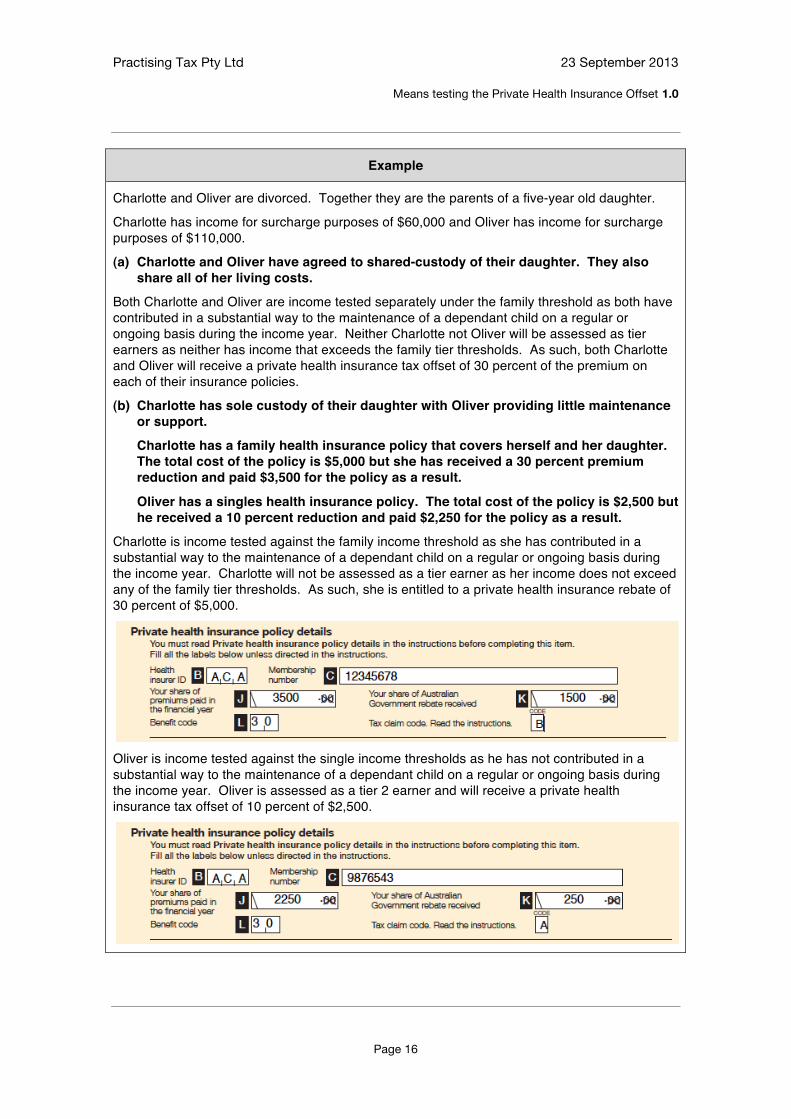

Example

Charlotte and Oliver are divorced. Together they are the parents of a five-year old daughter.

Charlotte has income for surcharge purposes of $60,000 and Oliver has income for surcharge purposes of $110,000.

(a) Charlotte and Oliver have agreed to shared-custody of their daughter. They also share all of her living costs.

Both Charlotte and Oliver are income tested separately under the family threshold as both have contributed in a substantial way to the maintenance of a dependant child on a regular or ongoing basis during the income year. Neither Charlotte not Oliver will be assessed as tier earners as neither has income that exceeds the family tier thresholds. As such, both Charlotte and Oliver will receive a private health insurance tax offset of 30 percent of the premium on each of their insurance policies.

(b) Charlotte has sole custody of their daughter with Oliver providing little maintenance or support.

Charlotte has a family health insurance policy that covers herself and her daughter. The total cost of the policy is $5,000 but she has received a 30 percent premium reduction and paid $3,500 for the policy as a result.

Oliver has a singles health insurance policy. The total cost of the policy is $2,500 but he received a 10 percent reduction and paid $2,250 for the policy as a result.

Charlotte is income tested against the family income threshold as she has contributed in a substantial way to the maintenance of a dependant child on a regular or ongoing basis during the income year. Charlotte will not be assessed as a tier earner as her income does not exceed any of the family tier thresholds. As such, she is entitled to a private health insurance rebate of 30 percent of $5,000.

Oliver is income tested against the single income thresholds as he has not contributed in a substantial way to the maintenance of a dependant child on a regular or ongoing basis during the income year. Oliver is assessed as a tier 2 earner and will receive a private health insurance tax offset of 10 percent of $2,500.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 17

Couples

Couples that are married or in a de-facto relationship on the last day of the income year, and are covered by the same health insurance policy can:

• each claim their own share of the rebate entitlement; or

• make a choice for one member of the couple to receive the offset entitlement on behalf of their partner.

Each claiming their own share of the rebate entitlement

Where individuals are married or in a de-facto relationship on the last day of the year and are each claiming their own share of the private health insurance rebate entitlement, the appropriate tax claim code to be used in the Private health insurance policy details item of the individual tax return is tax claim code C. This tax claim code advises the ATO to income test the individuals together based on the family tier thresholds.

Example

Michael and Angela are in a de-facto relationship. They are both in their thirties and have a couple!s health insurance policy.

Michael has income for surcharge purposes of $50,000 and Melanie has income for surcharge purposes of $60,000. As they are married at the end of the income year, they are assessed on the family income threshold.

Michael and Angela will not be assessed as tier earners because their combined income does not exceed the family tier thresholds.

As such, they are each entitled to receive half of a 30 percent private health insurance tax offset.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 18

Example

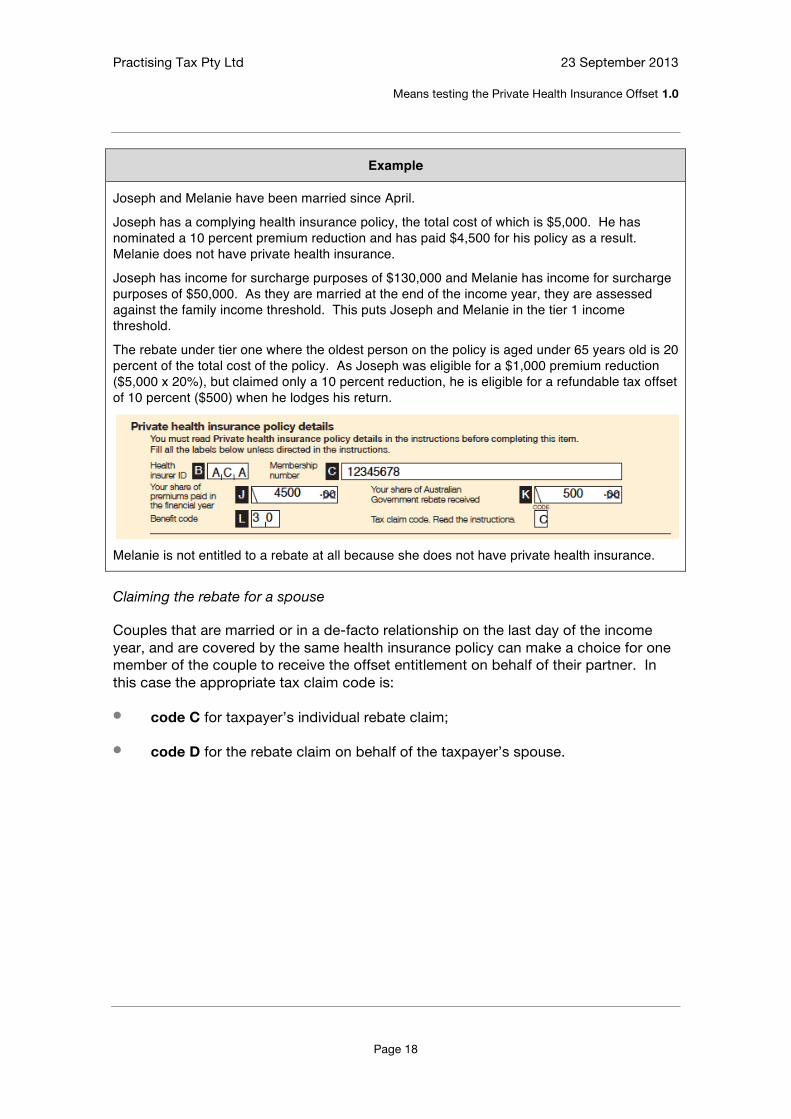

Joseph and Melanie have been married since April.

Joseph has a complying health insurance policy, the total cost of which is $5,000. He has nominated a 10 percent premium reduction and has paid $4,500 for his policy as a result. Melanie does not have private health insurance.

Joseph has income for surcharge purposes of $130,000 and Melanie has income for surcharge purposes of $50,000. As they are married at the end of the income year, they are assessed against the family income threshold. This puts Joseph and Melanie in the tier 1 income threshold.

The rebate under tier one where the oldest person on the policy is aged under 65 years old is 20 percent of the total cost of the policy. As Joseph was eligible for a $1,000 premium reduction ($5,000 x 20%), but claimed only a 10 percent reduction, he is eligible for a refundable tax offset of 10 percent ($500) when he lodges his return.

Melanie is not entitled to a rebate at all because she does not have private health insurance.

Claiming the rebate for a spouse

Couples that are married or in a de-facto relationship on the last day of the income year, and are covered by the same health insurance policy can make a choice for one member of the couple to receive the offset entitlement on behalf of their partner. In this case the appropriate tax claim code is:

• code C for taxpayer’s individual rebate claim;

• code D for the rebate claim on behalf of the taxpayer’s spouse.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 19

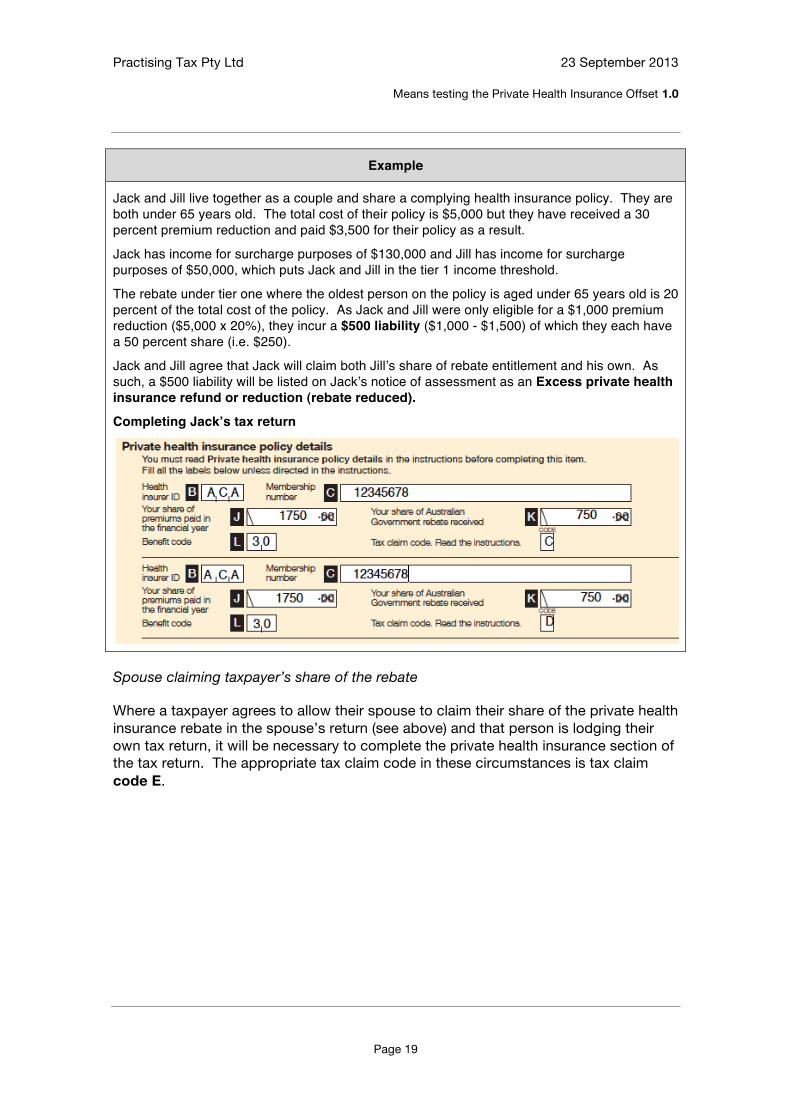

Example

Jack and Jill live together as a couple and share a complying health insurance policy. They are both under 65 years old. The total cost of their policy is $5,000 but they have received a 30 percent premium reduction and paid $3,500 for their policy as a result.

Jack has income for surcharge purposes of $130,000 and Jill has income for surcharge purposes of $50,000, which puts Jack and Jill in the tier 1 income threshold.

The rebate under tier one where the oldest person on the policy is aged under 65 years old is 20 percent of the total cost of the policy. As Jack and Jill were only eligible for a $1,000 premium reduction ($5,000 x 20%), they incur a $500 liability ($1,000 - $1,500) of which they each have a 50 percent share (i.e. $250).

Jack and Jill agree that Jack will claim both Jill!s share of rebate entitlement and his own. As such, a $500 liability will be listed on Jack!s notice of assessment as an Excess private health insurance refund or reduction (rebate reduced).

Completing Jack!s tax return

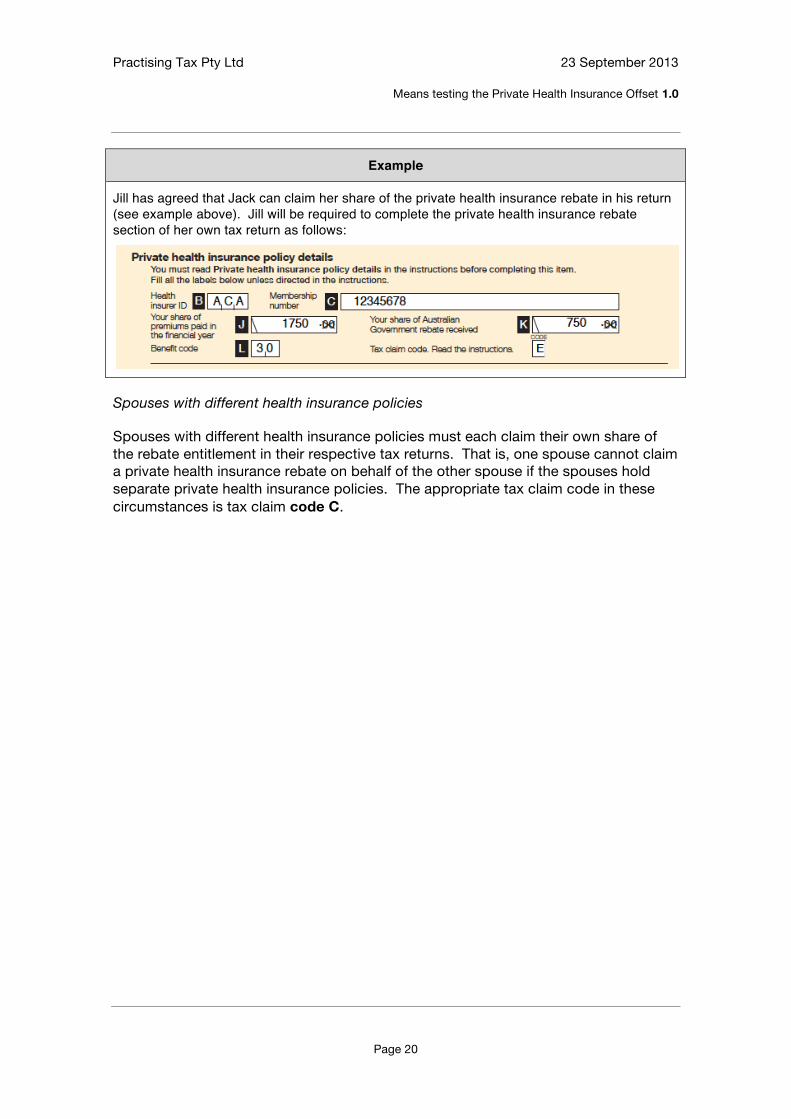

Spouse claiming taxpayer’s share of the rebate

Where a taxpayer agrees to allow their spouse to claim their share of the private health insurance rebate in the spouse’s return (see above) and that person is lodging their own tax return, it will be necessary to complete the private health insurance section of the tax return. The appropriate tax claim code in these circumstances is tax claim code E.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 20

Example

Jill has agreed that Jack can claim her share of the private health insurance rebate in his return (see example above). Jill will be required to complete the private health insurance rebate section of her own tax return as follows:

Spouses with different health insurance policies

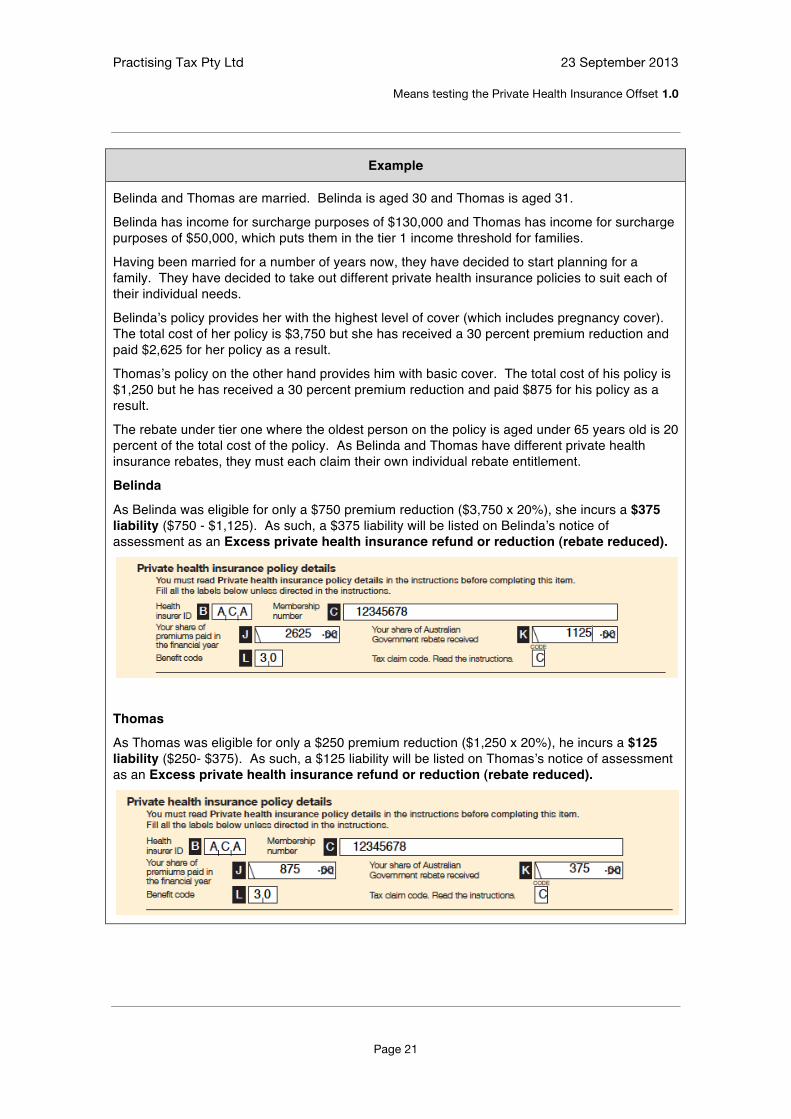

Spouses with different health insurance policies must each claim their own share of the rebate entitlement in their respective tax returns. That is, one spouse cannot claim a private health insurance rebate on behalf of the other spouse if the spouses hold separate private health insurance policies. The appropriate tax claim code in these circumstances is tax claim code C.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 21

Example

Belinda and Thomas are married. Belinda is aged 30 and Thomas is aged 31.

Belinda has income for surcharge purposes of $130,000 and Thomas has income for surcharge purposes of $50,000, which puts them in the tier 1 income threshold for families.

Having been married for a number of years now, they have decided to start planning for a family. They have decided to take out different private health insurance policies to suit each of their individual needs.

Belinda!s policy provides her with the highest level of cover (which includes pregnancy cover). The total cost of her policy is $3,750 but she has received a 30 percent premium reduction and paid $2,625 for her policy as a result.

Thomas!s policy on the other hand provides him with basic cover. The total cost of his policy is $1,250 but he has received a 30 percent premium reduction and paid $875 for his policy as a result.

The rebate under tier one where the oldest person on the policy is aged under 65 years old is 20 percent of the total cost of the policy. As Belinda and Thomas have different private health insurance rebates, they must each claim their own individual rebate entitlement.

Belinda

As Belinda was eligible for only a $750 premium reduction ($3,750 x 20%), she incurs a $375 liability ($750 - $1,125). As such, a $375 liability will be listed on Belinda!s notice of assessment as an Excess private health insurance refund or reduction (rebate reduced).

Thomas

As Thomas was eligible for only a $250 premium reduction ($1,250 x 20%), he incurs a $125 liability ($250- $375). As such, a $125 liability will be listed on Thomas!s notice of assessment as an Excess private health insurance refund or reduction (rebate reduced).

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 22

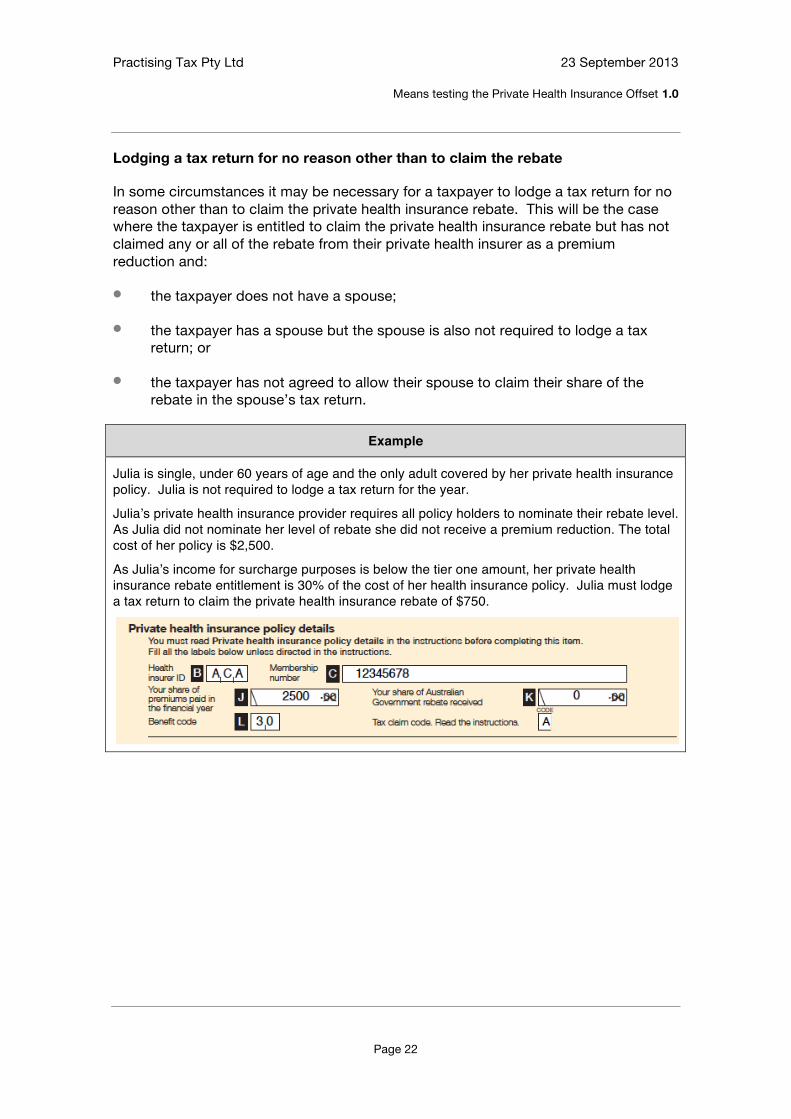

Lodging a tax return for no reason other than to claim the rebate

In some circumstances it may be necessary for a taxpayer to lodge a tax return for no reason other than to claim the private health insurance rebate. This will be the case where the taxpayer is entitled to claim the private health insurance rebate but has not claimed any or all of the rebate from their private health insurer as a premium reduction and:

• the taxpayer does not have a spouse;

• the taxpayer has a spouse but the spouse is also not required to lodge a tax return; or

• the taxpayer has not agreed to allow their spouse to claim their share of the rebate in the spouse’s tax return.

Example

Julia is single, under 60 years of age and the only adult covered by her private health insurance policy. Julia is not required to lodge a tax return for the year.

Julia!s private health insurance provider requires all policy holders to nominate their rebate level. As Julia did not nominate her level of rebate she did not receive a premium reduction. The total cost of her policy is $2,500.

As Julia!s income for surcharge purposes is below the tier one amount, her private health insurance rebate entitlement is 30% of the cost of her health insurance policy. Julia must lodge a tax return to claim the private health insurance rebate of $750.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 23

Dependant children covered by a policy

The rebate in respect of a dependant child only policy is available to the one or both of the parents of the dependant child (depending on whether they are married or in a de facto relationship).

Example

Tim and Liz are married and together have an adult child Angela (aged 21). The total cost of their family policy is $5,000 but they have received a 30 percent premium reduction and paid $3,500 for their policy as a result.

Jack has income for surcharge purposes of $100,000 and Jill has income for surcharge purposes of $60,000.

Angela is studying a Bachelor of Biomedical Science on a full-time basis and has income for surcharge purposes of $10,000 working part-time as a lab-assistant. Under the rules of their private health insurer, Angela is classified as a dependant child.

Because Angela is covered as a dependant child on the family policy, her income is not taken into consideration for the family income threshold. As such, Tim and Liz will not be assessed as tier earners as their income does not exceed any of the family tier thresholds.

The rebate for the base level where the oldest person on the policy is aged under 65 years old is 30 percent of the total cost of the policy. Tim and Liz have claimed their full rebate entitlement of 30 percent and are therefore not entitled to a further offset or liable for excess private health insurance refund or reduction.

Prepaid private health insurance

Prior to the introduction of the private health insurance tiers, high income earners who were likely to have their rebate reduced from 1 July 2012 were encouraged to prepay their 2012-13 premium before 1 July 2012 to ensure that the non-means tested rebate applied for those premiums.

Whilst there is no requirement for taxpayers who acted on this advice to repay any of the rebate, such taxpayers must nonetheless complete the private health insurance details in the individual tax return for 2013. Failure to do so may result in the taxpayer being charged Medicare levy surcharge (on the basis that an appropriate level of private hospital cover was not obtained).

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 24

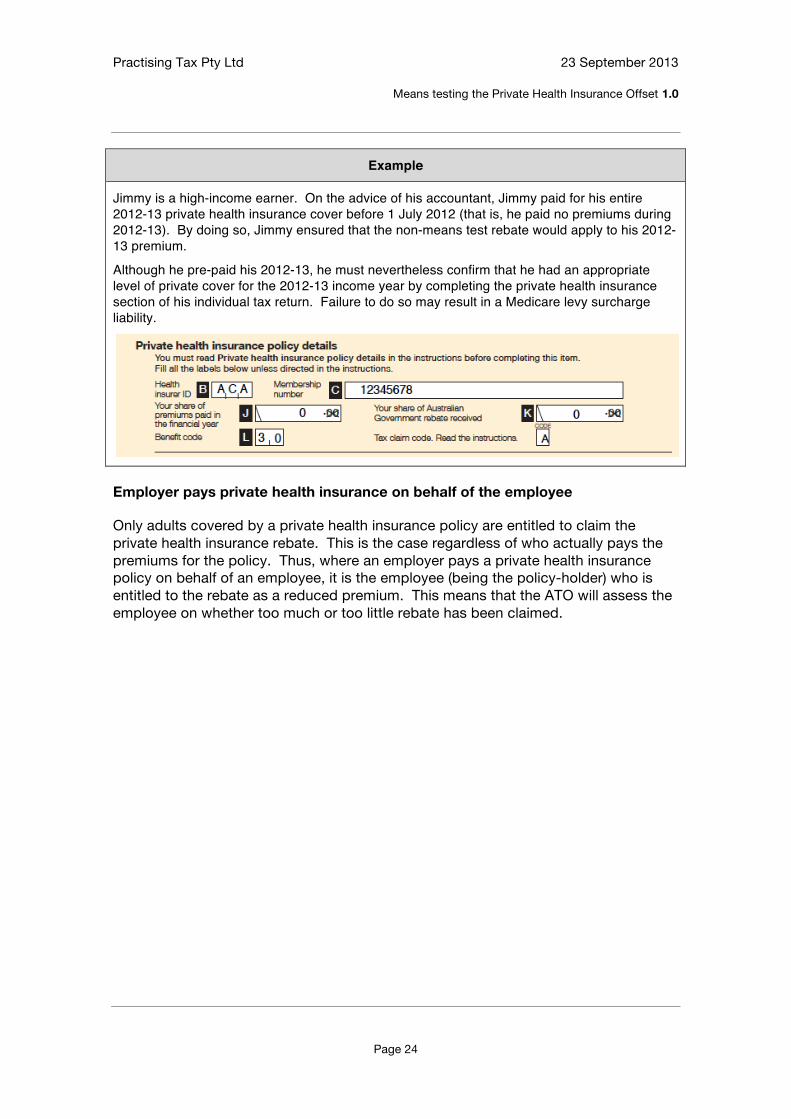

Example

Jimmy is a high-income earner. On the advice of his accountant, Jimmy paid for his entire 2012-13 private health insurance cover before 1 July 2012 (that is, he paid no premiums during 2012-13). By doing so, Jimmy ensured that the non-means test rebate would apply to his 2012-13 premium.

Although he pre-paid his 2012-13, he must nevertheless confirm that he had an appropriate level of private cover for the 2012-13 income year by completing the private health insurance section of his individual tax return. Failure to do so may result in a Medicare levy surcharge liability.

Employer pays private health insurance on behalf of the employee

Only adults covered by a private health insurance policy are entitled to claim the private health insurance rebate. This is the case regardless of who actually pays the premiums for the policy. Thus, where an employer pays a private health insurance policy on behalf of an employee, it is the employee (being the policy-holder) who is entitled to the rebate as a reduced premium. This means that the ATO will assess the employee on whether too much or too little rebate has been claimed.

Practising Tax Pty Ltd 23 September 2013

Means testing the Private Health Insurance Offset 1.0

Page 25

Example

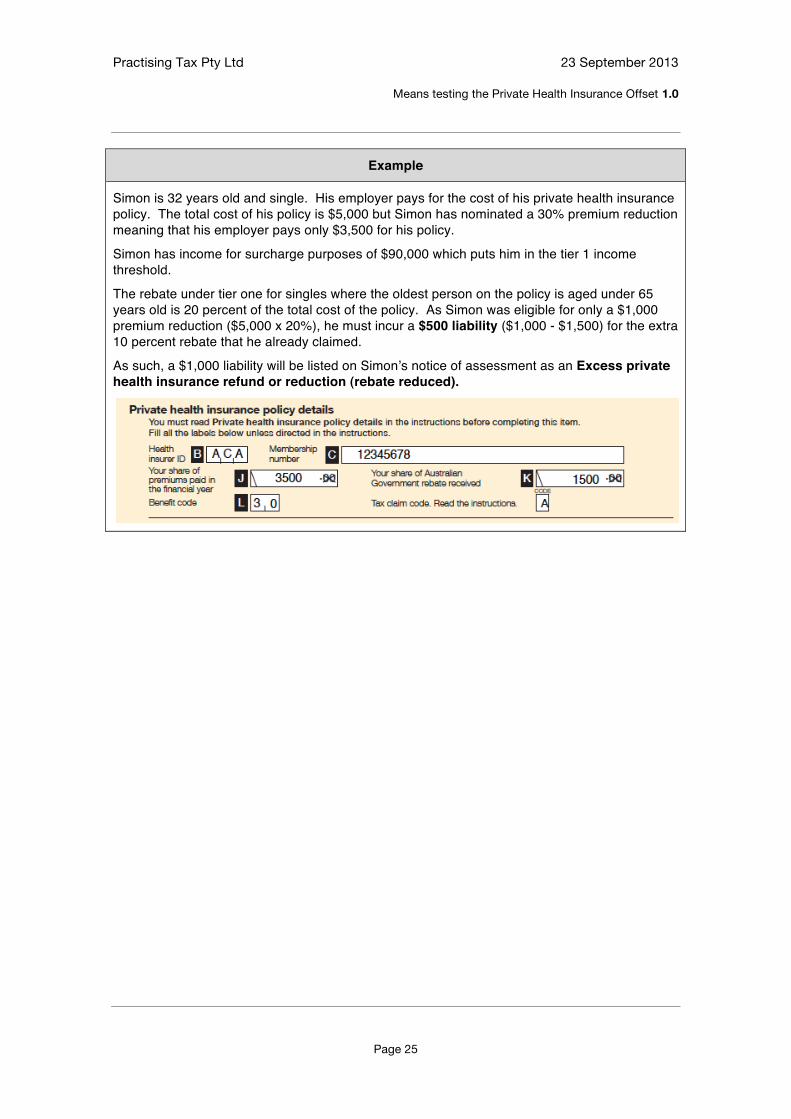

Simon is 32 years old and single. His employer pays for the cost of his private health insurance policy. The total cost of his policy is $5,000 but Simon has nominated a 30% premium reduction meaning that his employer pays only $3,500 for his policy.

Simon has income for surcharge purposes of $90,000 which puts him in the tier 1 income threshold.

The rebate under tier one for singles where the oldest person on the policy is aged under 65 years old is 20 percent of the total cost of the policy. As Simon was eligible for only a $1,000 premium reduction ($5,000 x 20%), he must incur a $500 liability ($1,000 - $1,500) for the extra 10 percent rebate that he already claimed.

As such, a $1,000 liability will be listed on Simon!s notice of assessment as an Excess private health insurance refund or reduction (rebate reduced).