TAX CUTS & JOBS ACT - bkd.com · Repeal of Alternative Minimum Tax (AMT) ... Limitation on...

21

PRESENTED BY: THOMAS WHEELAND, BRANDY SHY & LEON LANGLITZ TAX CUTS & JOBS ACT Provisions of Interest to Insurers

Transcript of TAX CUTS & JOBS ACT - bkd.com · Repeal of Alternative Minimum Tax (AMT) ... Limitation on...

P R E S E N T E D B Y : T H O M A S W H E E L A N D , B R A N D Y S H Y & L E O N L A N G L I T Z

TAX CUTS & JOBS ACTProvisions of Interest to Insurers

2

INTRODUCTIONS Tom WheelandPartnerBKD CPAs & Advisors

Brandy ShyDirectorBKD CPAs & Advisors

Leon Langlitz, FSA, MAAASenior Vice President & PrincipalLewis & Ellis Inc.

3

OUR GOALS FOR TODAY

1 Outline Basic Provisions Applicable to All Corporations

Discuss Insurance-Specific Provisions

Summarize the Income Tax Accounting Impact of Act

Highlight Tax Planning Opportunities

2

3

4

4

GENERAL CORPORATE PROVISIONSSome good news for corporations

The View From 30,000 FeetReduction in Federal Corporate Income Tax Rate to 21%

Repeal of Alternative Minimum Tax (AMT)

Offset of Regular Tax with AMT Credits

Net Operating Losses (NOLs) • Unlimited Carryforward• No Carrybacks• Limited to 80% of Regular Taxable Income• P&C Company NOL Rules Unchanged

100% Bonus Depreciation & Expanded §179 Expensing

Limitation on Deductibility of Business Interest

Income Inclusion

Modifications to §162(m)

5

CORPORATE TAX RATEOne federal tax rate for all C corporations

Federal Tax Rate Reduced to Flat 21%

Former Top Tax Rate of 35% was Highest in the Industrialized WorldTrump Proposed a 15% Tax Rate Initial Drafts of Bill Included 20% Rate Represents a 40% Reduction in Top RateApplies to Tax Years Beginning After 12/31/17Consider Deferring Income & Accelerating Expenses

• Prepaid Expenses• Accrued Bonuses• Pension Funding• Policyholder Dividends

6

AMT REPEALThis trap for the unwary particularly affected P&C & small life insurers

Goodbye AMT in 2018!

Considered a Prepaid Tax by Most CompaniesCorporations Allowed a Credit for AMT –Used to Offset Regular Tax to Extent it Exceeded Tentative AMT in Future YearsSmall Life Insurers – Many Paid AMT with Limited Ability to Claim Credit (See Slide on SLICD)A Benefit for P&C Companies in Poor Underwriting Years Makes Certain Investment Decisions Less Complex

7

AMT CREDITSEasier to use credits from pre-law periods, including a refund mechanism

Utilization of Existing AMT Credits

Use AMT Credits to Offset Regular TaxExcess Credits are Refundable (over an established period)

• 50% of Excess Refundable in 2018 – 2020

• 100% of Excess Refundable in 2021

8

AMT CREDITSEasier to use credits from pre-law periods, including a refund mechanism

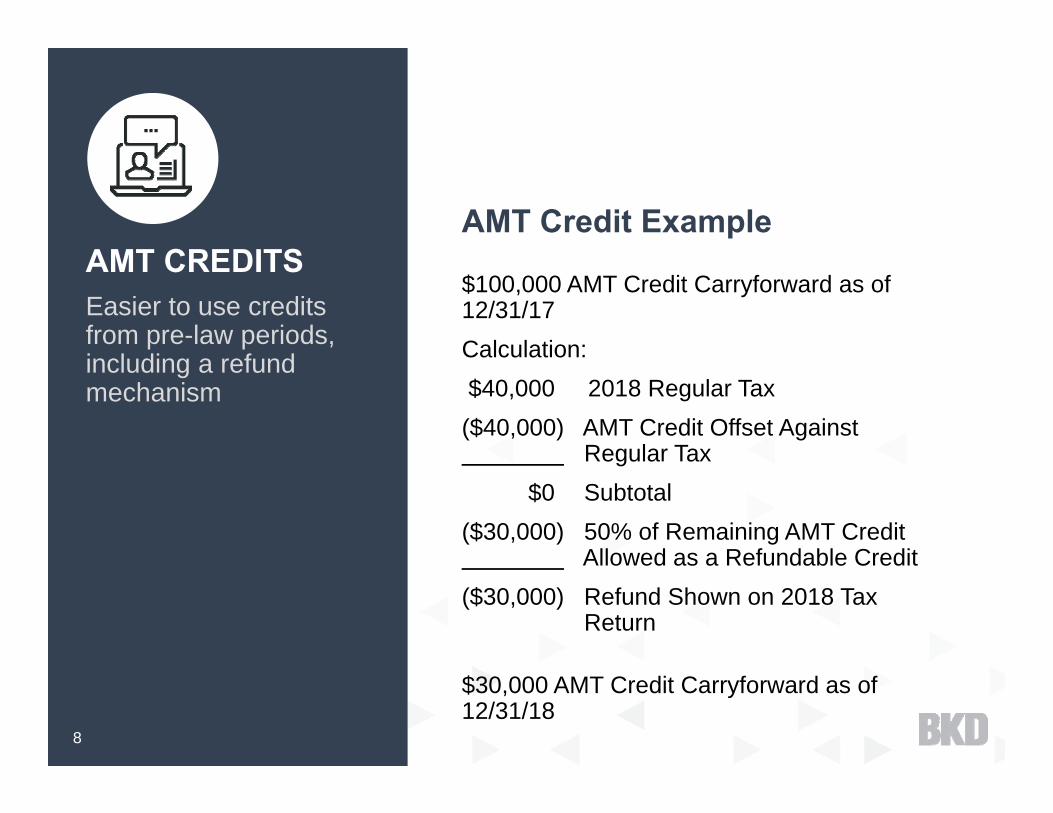

AMT Credit Example

$100,000 AMT Credit Carryforward as of 12/31/17Calculation:$40,000 2018 Regular Tax ($40,000) AMT Credit Offset Against

Regular Tax$0 Subtotal

($30,000) 50% of Remaining AMT Credit Allowed as a Refundable Credit

($30,000) Refund Shown on 2018 Tax Return

$30,000 AMT Credit Carryforward as of 12/31/18

9

NET OPERATING LOSSESThe Lord Giveth, the Lord Taketh Away …

Net Operating Losses (NOLs)

Conforms Life Operations Loss Deduction (OLD) Rules to NOLsNo Carryback of NOLsIndefinite CarryforwardAnnual Limitation of 80% of Regular Taxable Income for Post-2017 NOLsP&C NOLs Unchanged

• 2-Year Carryback• 20-Year Carryforward• 100% Offset of Regular Taxable

IncomeCapital Loss Carryback & Carryforward Rules Unchanged

TAX REFORMNOL Comparison Chart

OLD LAW Years Carryback

Years Carryforward % Offset

C-Corporations 2 20 100Non-Life Insurers 2 20 100

Life Insurers 3 15 100

NEW LAW Years Carryback

Years Carryforward % Offset

C-Corporations 0 ∞ 80

Non-Life Insurers 2 20 100

Life Insurers 0 ∞ 80

11

LIBERALIZING FIXED ASSET EXPENSINGBonus depreciation & §179

Good News …

Bonus Depreciation Increased to 100% for Assets Placed in Service After September 27, 2017 & Before January 1, 2023§179 Expensing

• Expanded to $1 million (from $500K) with Phase-Out Beginning at $2.5 million (from $2 million)

• Property Placed in Service After December 31, 2017

12

YEAR OF INCLUSION More guidance is needed to determine effect on market discount deferral

Other Items of Note

Year of Inclusion• Income Inclusion – No Later than

Inclusion for Financial Reporting Purposes

• Some Exceptions• Questionable Application to Market

Discount & Accrued Dividends§174 Amortization of Research & Experimentation Expenses

• 5-Year Amortization Period• For Expenses Incurred After

12/31/21• No Change to R&E Credit

13

BUSINESS INTEREST Is insurance company interest income considered trade or business interest?

Other Items of Note

Limitation on Business Interest Expense• Limits Net Business Interest

Expense• 30% of Adjusted Taxable Income• Excess Carried Forward

Meals & Entertainment• All Meals Subject to 50%

Disallowance• No Deduction for Entertainment

Expenses

14

NON-LIFE COMPANIESFocused on reserves & proration

Non-Life Insurance Company Provisions

Loss Reserves• Changes in Interest Rate & Payment

Pattern – Reduce Tax Loss Reserves

• No Company Election• Repeal of §847

Proration Percentage Increased from 15% to 25%

• Keeps the After-Tax Yield of Tax-Exempt Bonds Constant

• Narrows the Spread Between Taxable & Tax-Exempt Bonds

Retention of NOL Rules

15

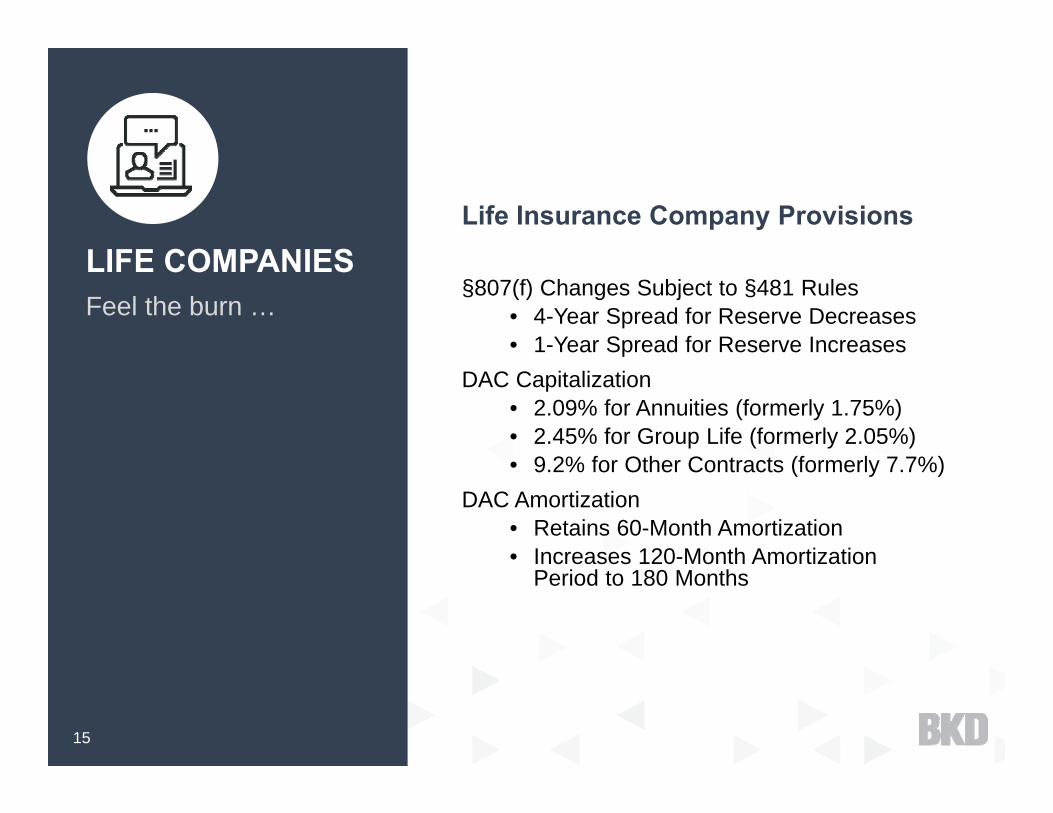

LIFE COMPANIESFeel the burn …

Life Insurance Company Provisions

§807(f) Changes Subject to §481 Rules• 4-Year Spread for Reserve Decreases• 1-Year Spread for Reserve Increases

DAC Capitalization• 2.09% for Annuities (formerly 1.75%)• 2.45% for Group Life (formerly 2.05%)• 9.2% for Other Contracts (formerly 7.7%)

DAC Amortization• Retains 60-Month Amortization• Increases 120-Month Amortization

Period to 180 Months

16

LIFE COMPANIES… but it could have been worse

Life Insurance Company ProvisionsLife Reserves Capped at Greater of Net Surrender Value or 92.81% of NAIC Prescribed Reserves (8-Year Phase-In)70% Company Share/30% Policyholder ShareInclusion of Policyholder Surplus Account Balance in Income over 8 YearsNOL/OLD ConformityElimination of Small Life Insurance Company Deduction (SLICD)

17

GAAP & SAPReduction in Current Federal Taxes with Short-Term Effect of DTA Reduction

Income Tax Accounting Impact

Reduction in DTAs• Increase 2017 GAAP Effective Tax

Rate (ETR) in P&L Regardless of Source

• Increase 2017 SAP ETR in SurplusElimination of NOL Carryback for Ordinary DTAs of Life Companies

• Removes a Source of Income for GAAP

• Makes SSAP 101, ¶11.a., Effectively Moot

Increases in Current Taxes (Caused by Reserves & DAC) Increase Deductible Temporary Differences – Reversal Patterns are Key

18

CHANGE IS HERE!Though most changes are effective in 2018, there are strategies you can implement in 2017 to help maximize the benefits of tax reform

Planning Opportunities

Look for Opportunities to Accelerate Deductions & Defer Income

• Prepaid Expenses• Pension Funding• Compensation Accruals• Bonus Depreciation• Policyholder Dividends

Analyze Portfolio for Effect of Proration & Company Share Changes

19

QUESTIONS? Tom [email protected]

Susan [email protected]

Brandy [email protected]

Kara CramerBKDSenior [email protected]

Leon LanglitzLewis & EllisSenior Vice President & [email protected]

Thank You!

20

TH10