Tax Compliance Research using Administrative Data in Rwanda

30

Tax Compliance Research using Administra7ve Data in Rwanda UNU-Wider & ICTD Workshop 9 February 2016 Giulia Mascagni (ICTD), Denis Mukama (RRA), Christopher Nell (ICTD)

-

Upload

chevening-scholarships -

Category

Government & Nonprofit

-

view

414 -

download

1

Transcript of Tax Compliance Research using Administrative Data in Rwanda

TaxComplianceResearchusingAdministra7veDatainRwanda

UNU-Wider&ICTDWorkshop

9February2016

GiuliaMascagni(ICTD),DenisMukama(RRA),ChristopherNell(ICTD)

Agenda

1. Overviewofresearchproject

2. Experimental design, implementa<on, andlessonslearnt

3. Preliminaryresultsfromdescrip<vesta<s<cs

Part1Overviewof

ResearchProject

GeCngStartedProject7tle:TaxcomplianceusingAdministra4veDatainRwandaPrepara7onphase• Objec7ves: data availability, feasibility of research, develop

researchdesign,policyrelevance,RRA’swillingnesstopar<cipate• Outcomes:dataavailable,many ini<a<vesoncomplianceatRRA,

but liIle evalua<on of policies, knowledge gap on the drivers ofcompliance

Implementa7onphase• ATAF,ICTD,RRAcollabora<on

OverviewofProjectObjec7ve: Iden<fy drivers of compliance and testcommunica<onstrategiesthatRRAcanadopttoincreasecomplianceAc7ngasateam:• FormalapprovalfromtheCG• FundingfromICTD/ATAF• Interna<onalteamwork

– Researchers,externalreviewers,RRA• Regularfeedbackonideasanddesign• Maintainingconfiden<ality

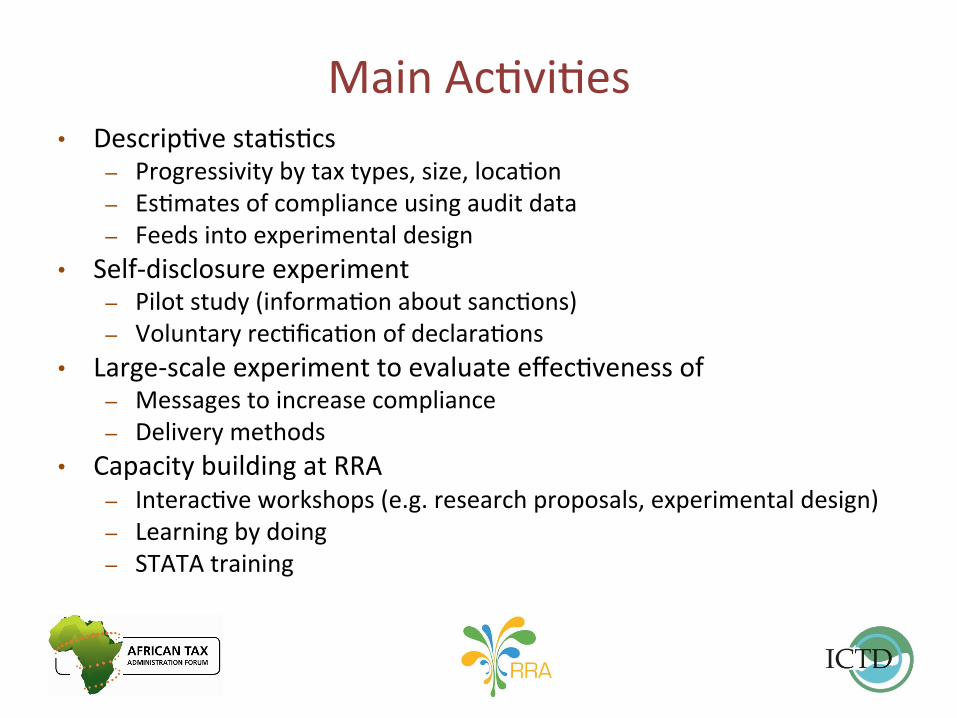

MainAc<vi<es• Descrip<vesta<s<cs

– Progressivitybytaxtypes,size,loca<on– Es<matesofcomplianceusingauditdata– Feedsintoexperimentaldesign

• Self-disclosureexperiment– Pilotstudy(informa<onaboutsanc<ons)– Voluntaryrec<fica<onofdeclara<ons

• Large-scaleexperimenttoevaluateeffec<venessof– Messagestoincreasecompliance– Deliverymethods

• CapacitybuildingatRRA– Interac<veworkshops(e.g.researchproposals,experimentaldesign)– Learningbydoing– STATAtraining

Part2ExperimentalDesign,

Implementa<on,andLessonsLearnt

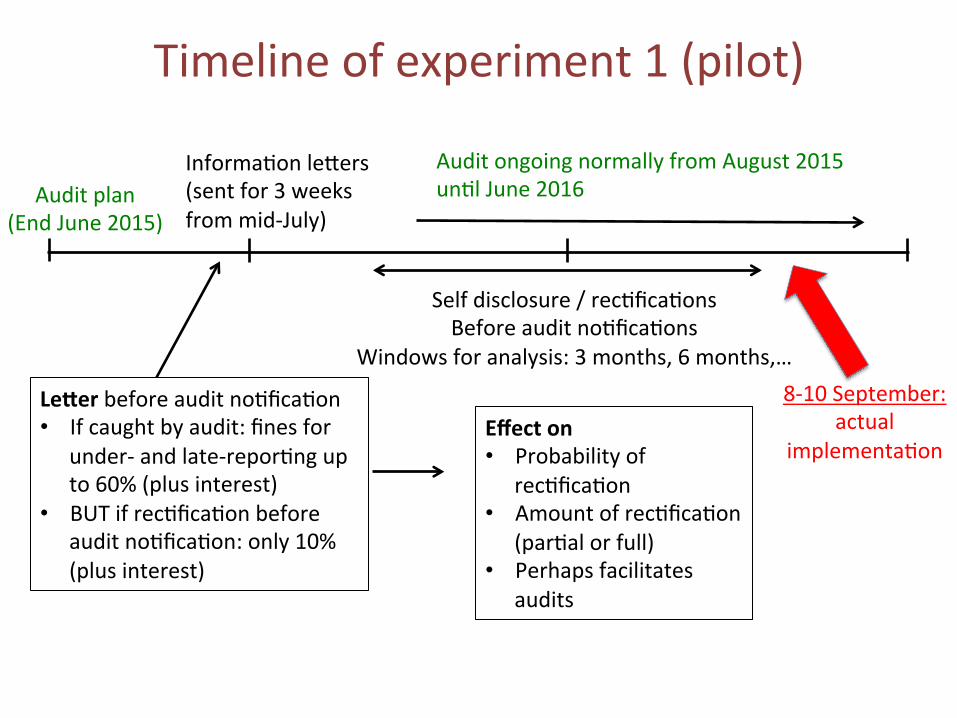

Timelineofexperiment1(pilot)

Auditplan(EndJune2015)

Selfdisclosure/rec<fica<onsBeforeauditno<fica<ons

Windowsforanalysis:3months,6months,…

LeTerbeforeauditno<fica<on• Ifcaughtbyaudit:finesfor

under-andlate-repor<ngupto60%(plusinterest)

• BUTifrec<fica<onbeforeauditno<fica<on:only10%(plusinterest)

Effecton• Probabilityof

rec<fica<on• Amountofrec<fica<on

(par<alorfull)• Perhapsfacilitates

audits

Informa<onleIers(sentfor3weeksfrommid-July)

AuditongoingnormallyfromAugust2015un<lJune2016

8-10September:actual

implementa<on

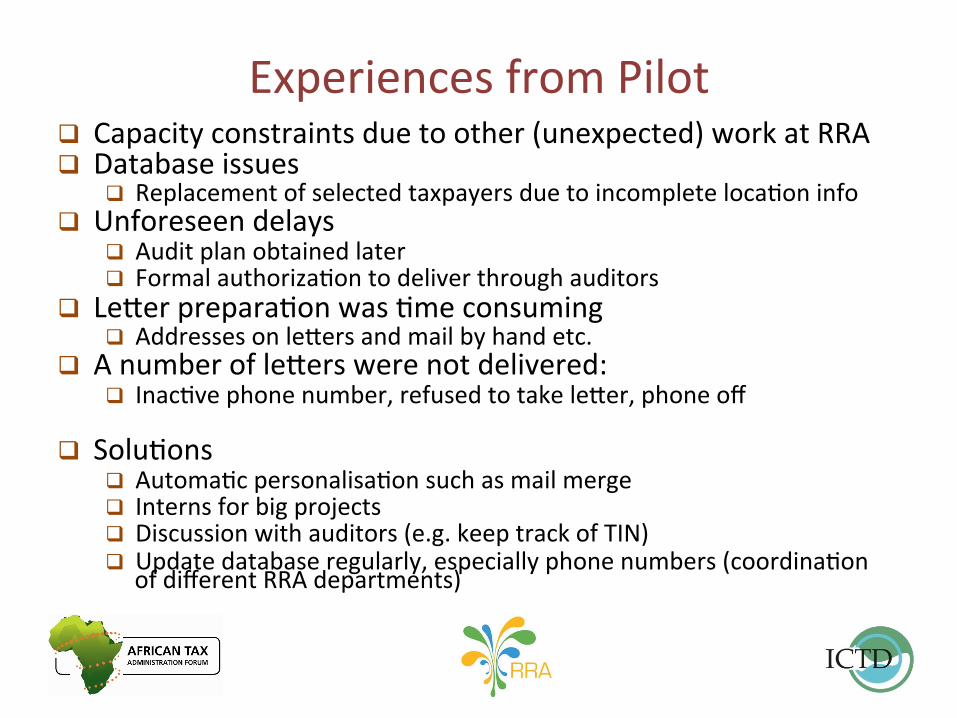

ExperiencesfromPilotq Capacityconstraintsduetoother(unexpected)workatRRAq Databaseissues

q Replacementofselectedtaxpayersduetoincompleteloca<oninfoq Unforeseendelays

q Auditplanobtainedlaterq Formalauthoriza<ontodeliverthroughauditors

q LeIerprepara<onwas<meconsumingq AddressesonleIersandmailbyhandetc.

q AnumberofleIerswerenotdelivered:q Inac<vephonenumber,refusedtotakeleIer,phoneoff

q Solu<onsq Automa<cpersonalisa<onsuchasmailmergeq Internsforbigprojectsq Discussionwithauditors(e.g.keeptrackofTIN)q Updatedatabaseregularly,especiallyphonenumbers(coordina<on

ofdifferentRRAdepartments)

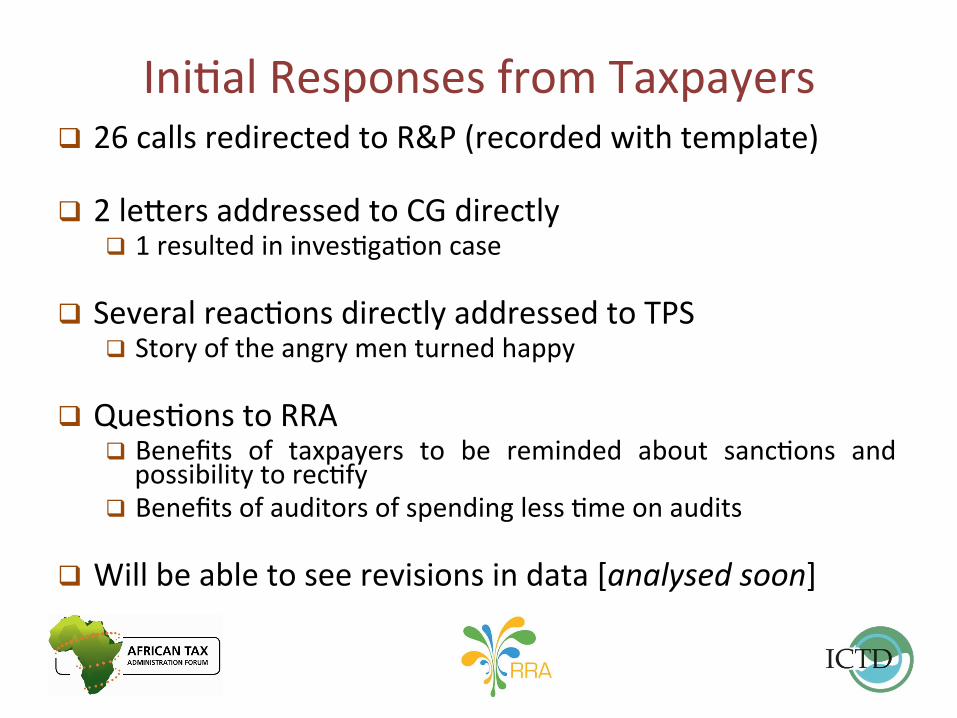

Ini<alResponsesfromTaxpayersq 26callsredirectedtoR&P(recordedwithtemplate)

q 2leIersaddressedtoCGdirectlyq 1resultedininves<ga<oncase

q Severalreac<onsdirectlyaddressedtoTPSq Storyoftheangrymenturnedhappy

q Ques<onstoRRAq Benefits of taxpayers to be reminded about sanc<ons andpossibilitytorec<fy

q Benefitsofauditorsofspendingless<meonaudits

q Willbeabletoseerevisionsindata[analysedsoon]

TimelineofExperiment2

31/122014

31/32014

31/122015

30/032016

Taxreturn1 Taxreturn2

Messages1. Importanceoftaxtofund

publicservices2. Stressenforcement3. Controlmessage

Effecton• Levelofcompliance

(e.g.paidon<me,cancelleddebts)

• Comparedeclara<onstopreviousyear…

• Compare“treatment”&“notreatment”

Sample• CITandPIT

taxpayerswithphonenumbers

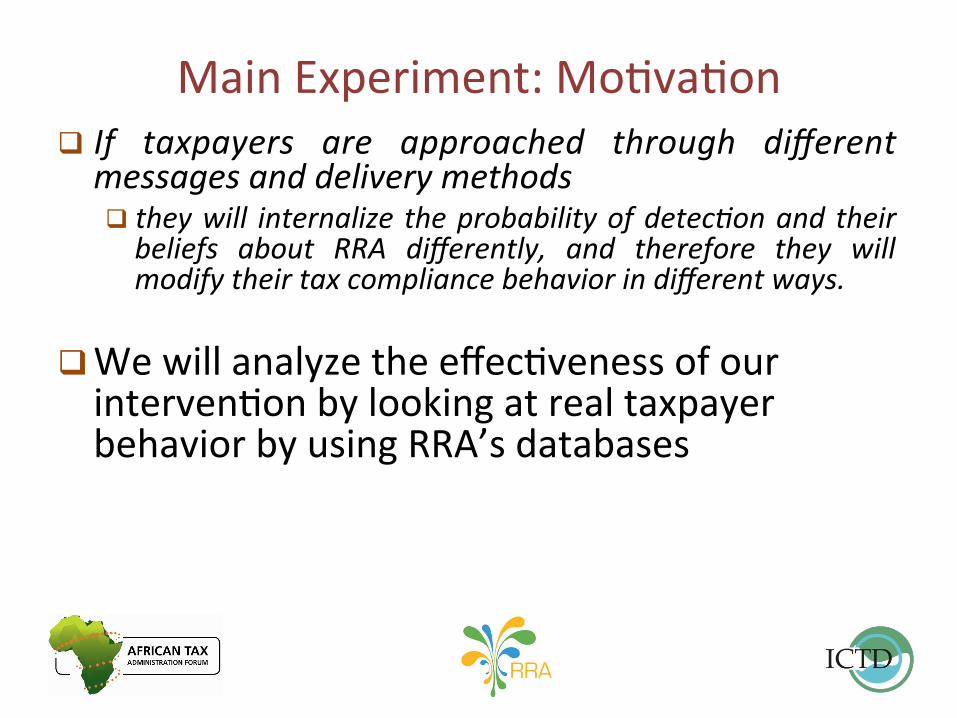

MainExperiment:Mo<va<onq If taxpayers are approached through differentmessagesanddeliverymethodsq theywill internalize theprobabilityofdetec4onandtheirbeliefs about RRA differently, and therefore they willmodifytheirtaxcompliancebehaviorindifferentways.

q Wewillanalyzetheeffec<venessofourinterven<onbylookingatrealtaxpayerbehaviorbyusingRRA’sdatabases

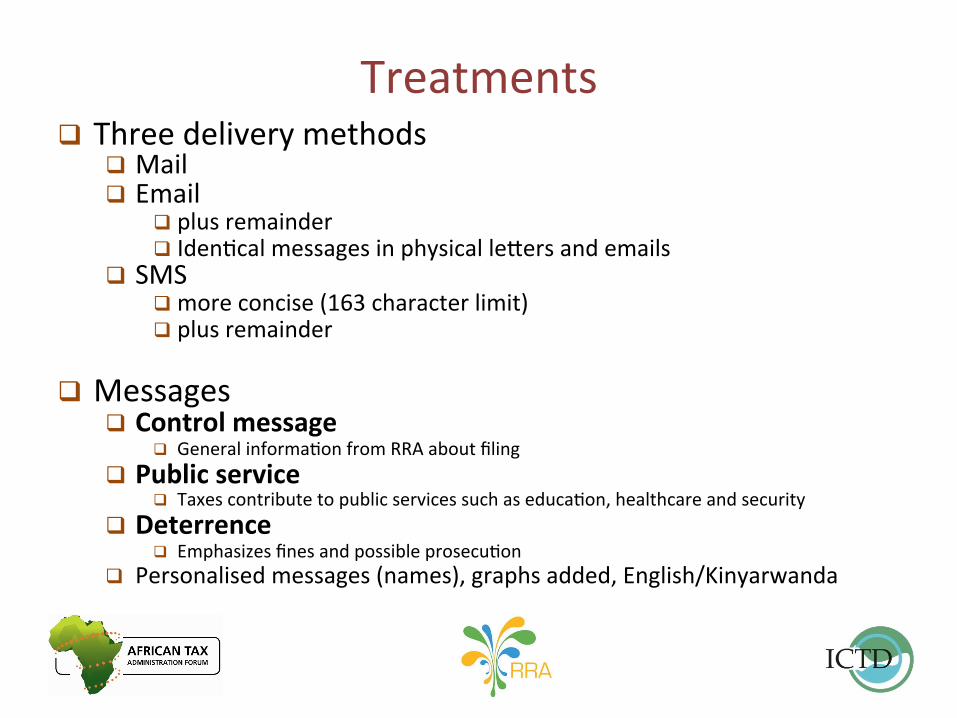

Treatmentsq Threedeliverymethods

q Mailq Email

q plusremainderq Iden<calmessagesinphysicalleIersandemails

q SMSq moreconcise(163characterlimit)q plusremainder

q Messages

q Controlmessageq Generalinforma<onfromRRAaboutfiling

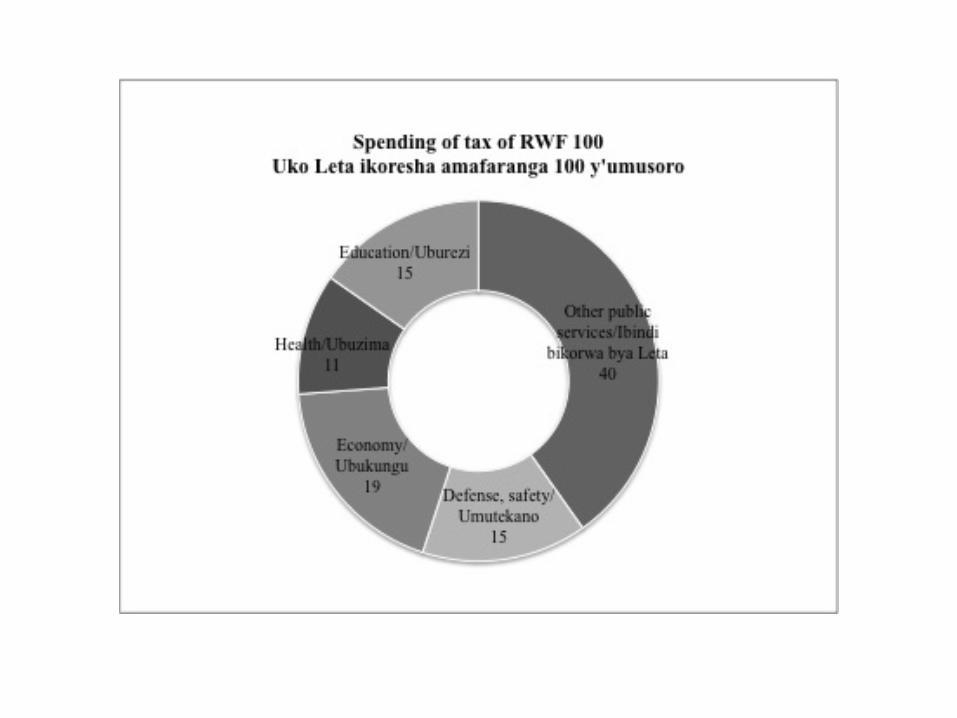

q Publicserviceq Taxescontributetopublicservicessuchaseduca<on,healthcareandsecurity

q Deterrenceq Emphasizesfinesandpossibleprosecu<on

q Personalisedmessages(names),graphsadded,English/Kinyarwanda

SampleOverviewq 45,000ac<veCITandPITtaxpayersq Experimentincludes

q E-taxfilersq Registeredin2013and2014q RegisteredinKigaliprovince

q likelytohaveup-to-datephonenumbersandemailaddresses

q CITq Phoneandemailfor94%outofe-tax/newtaxpayers–10,600q Usealldeliverymethodsandmessages(3x3treatments)+control

q PIT

q Ac<vephonesfor47%andemailsforlessthan1%q UseSMSfor2,800taxpayers,asmorefeasibleforRRA

CITTreatments

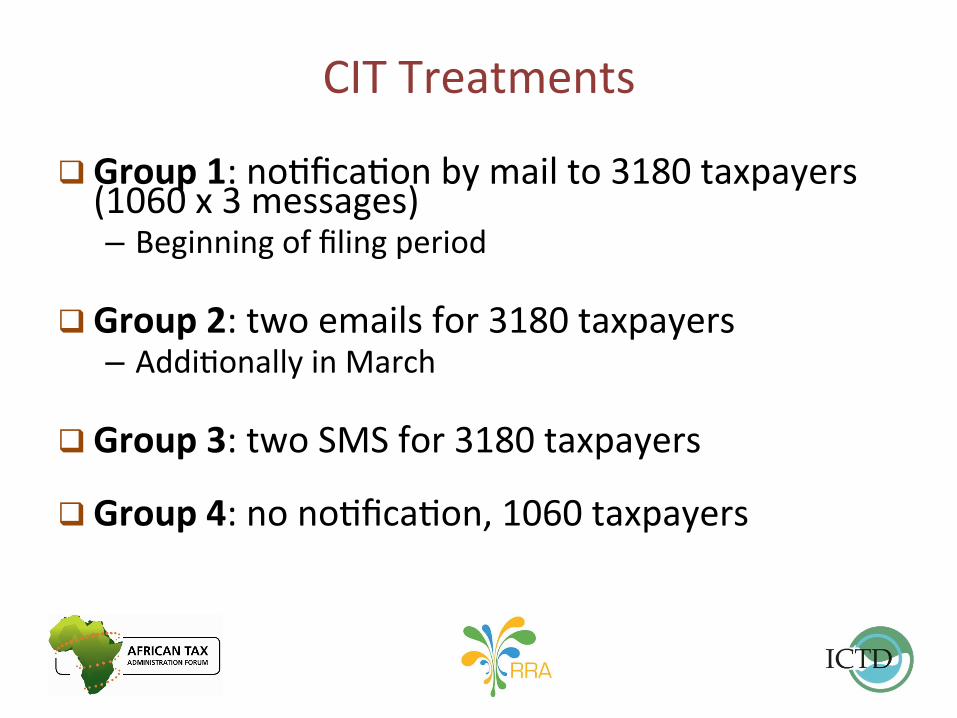

q Group1:no<fica<onbymailto3180taxpayers(1060x3messages)– Beginningoffilingperiod

q Group2:twoemailsfor3180taxpayers– Addi<onallyinMarch

q Group3:twoSMSfor3180taxpayers

q Group4:nono<fica<on,1060taxpayers

CITandPITTreatments

q Group1:no<fica<onbymailto3180taxpayers(1060x3messages)– Beginningoffilingperiod

q Group2:twoemailsfor3180taxpayers– Addi<onallyinMarch

q Group3:twoSMSfor3180taxpayers

q Group4:nono<fica<on,1060taxpayers

PITexperiment:twoSMS(2100taxpayersintotal)

Stra<fica<on

q Performrandomiza<onbasedonvariablesq forsubgroupanalysisq likelytopredictcompliance

q Nil-filersq Manytaxpayersfiledeclara<onwithzeroincomeq Reason:avoidfinefornotfiling,butnotaxliabilityq Nil-filersmayresponddifferentlytomessages

Stra<fica<on

q Regimetypeq Taxpayersinlump-sumregimehavehighertaxburden

q Maynotbeawareq Othercompensa<ngbenefitssuchaslowervisibility

q Nil-filingandregimetypemayberelatedtocompliance

OutcomeComparisons

q Differentmessages,giventhedeliverymethodq E.g.publicservicevscontrolmessageusingemail

q Deliverymethods,giventhemessage:

q E.g.publicserviceusingemail/mail/SMSrela<vetocontrolgroup

q Alsodiscussq SMSforCITandPIT

Part3PreliminaryResultsfromDescrip<veSta<s<cs

Findings

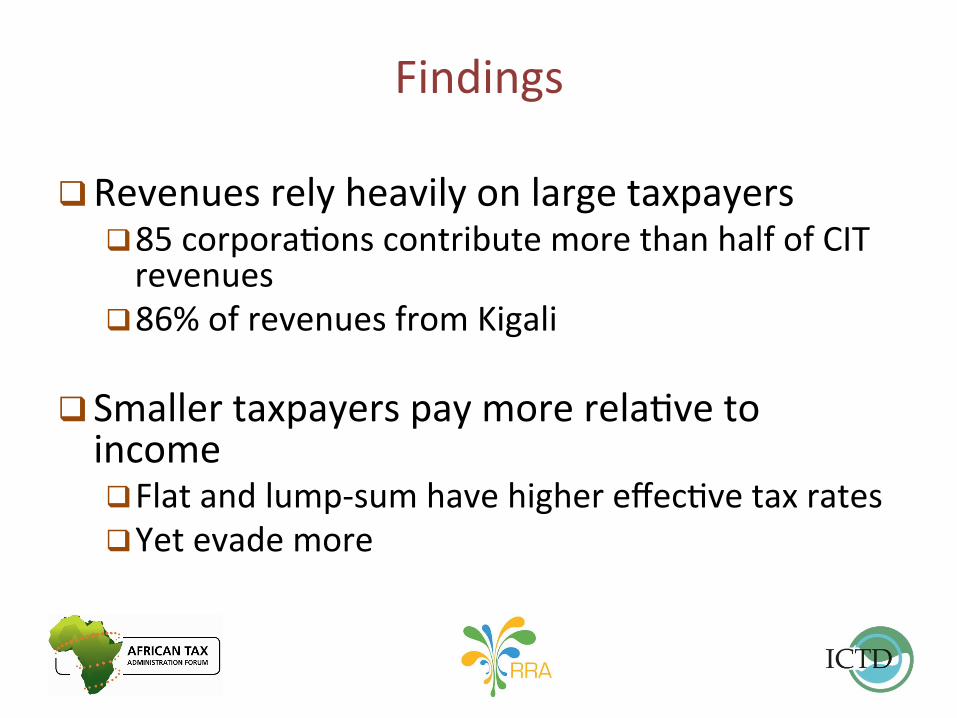

q Revenuesrelyheavilyonlargetaxpayersq 85corpora<onscontributemorethanhalfofCITrevenues

q 86%ofrevenuesfromKigali

q Smallertaxpayerspaymorerela<vetoincomeq Flatandlump-sumhavehighereffec<vetaxratesq Yetevademore

Findings

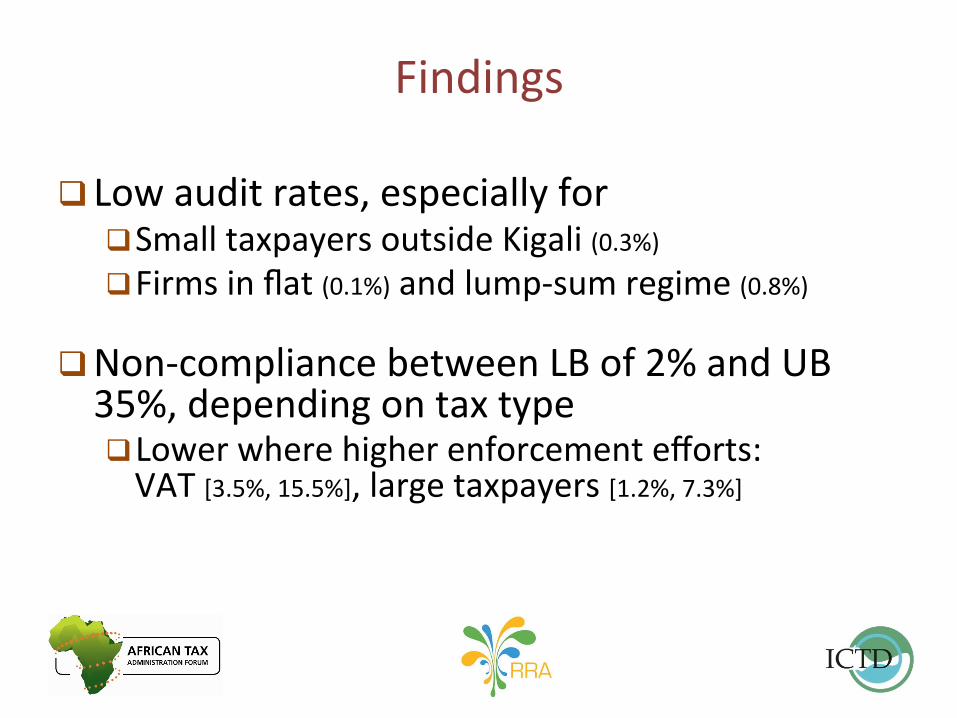

q Lowauditrates,especiallyforq SmalltaxpayersoutsideKigali(0.3%)q Firmsinflat(0.1%)andlump-sumregime(0.8%)

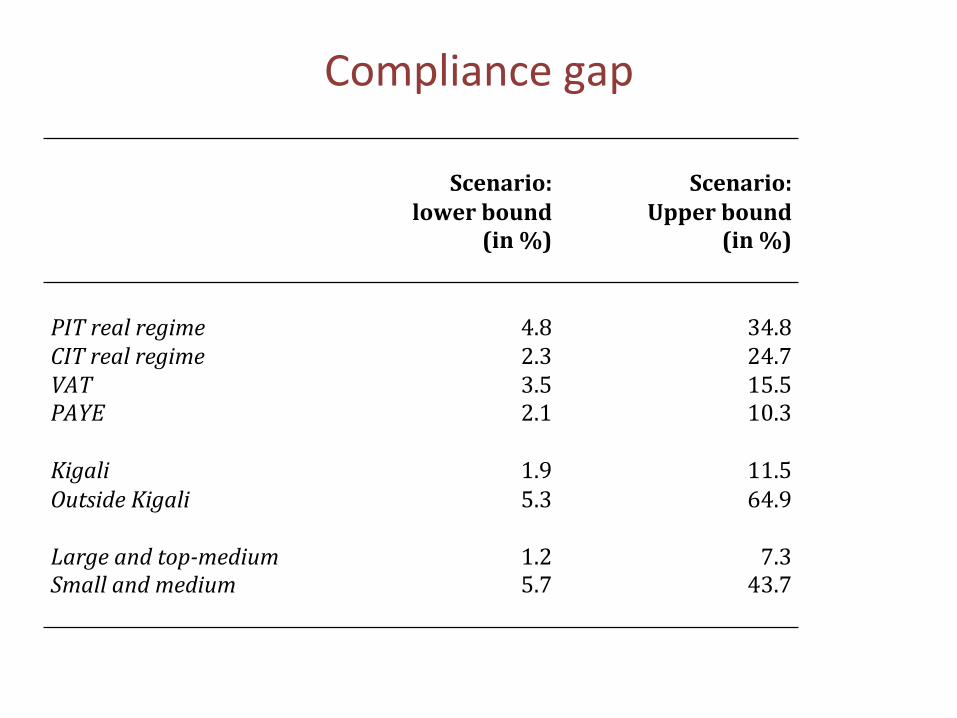

q Non-compliancebetweenLBof2%andUB35%,dependingontaxtypeq Lowerwherehigherenforcementefforts:VAT[3.5%,15.5%],largetaxpayers[1.2%,7.3%]

JointSummary

q Admindataforq Descrip<veanalysisq Experiments

q Coordina<on,teamwork,learningq Minimizedelaysq Regularupdateofdatabasesq Equalpartnershipsq FocalpointsatRA

Ques<onsandcomments?Thankyou.Pleasegetintouchwithus:Christopher:[email protected]: [email protected]: [email protected]: [email protected]

Appendix

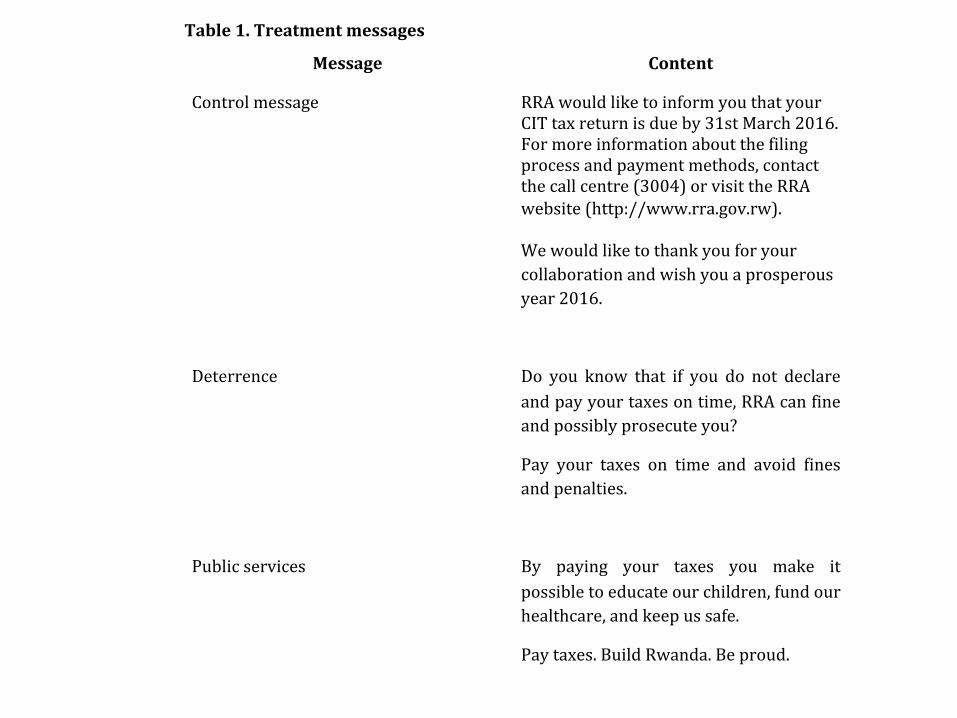

Table&1.&Treatment&messages&

Message& Content&

Control'message' RRA'would'like'to'inform'you'that'your'CIT'tax'return'is'due'by'31st'March'2016.'For'more'information'about'the'filing'process'and'payment'methods,'contact'the'call'centre'(3004)'or'visit'the'RRA'website'(http://www.rra.gov.rw).'''''We'would'like'to'thank'you'for'your'collaboration'and'wish'you'a'prosperous'year'2016.'

'

Deterrence' Do' you' know' that' if' you' do' not' declare'and'pay'your'taxes'on'time,'RRA'can'fine'and'possibly'prosecute'you?''

Pay' your' taxes' on' time' and' avoid' fines'and'penalties.'

'

Public'services' By' paying' your' taxes' you' make' it'possible'to'educate'our'children,'fund'our'healthcare,'and'keep'us'safe.'

Pay'taxes.'Build'Rwanda.'Be'proud.''

'

'

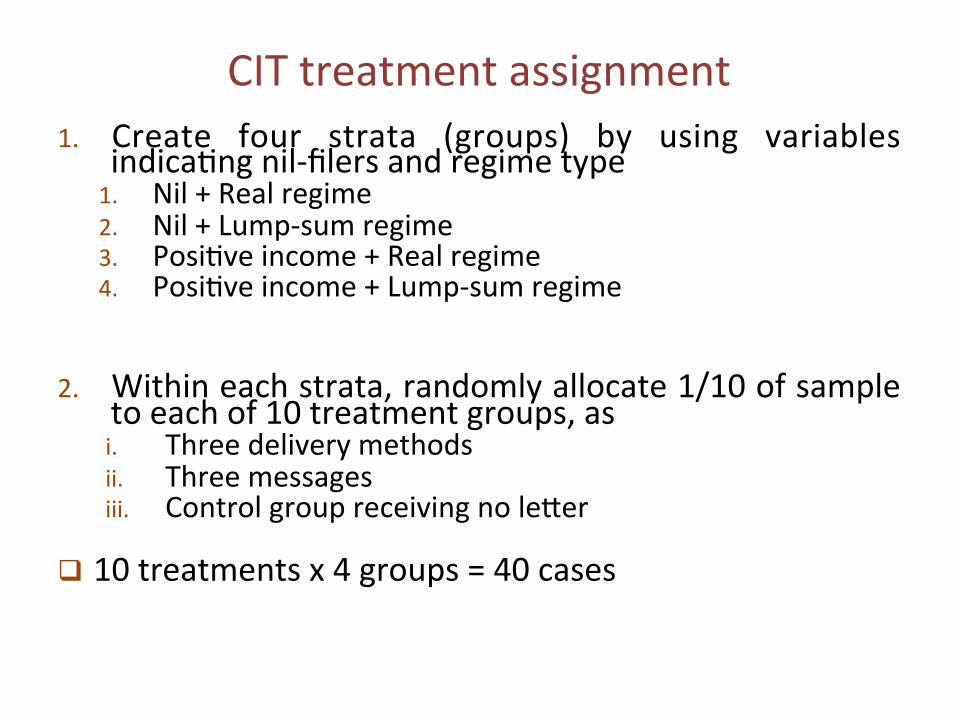

CITtreatmentassignment1. Create four strata (groups) by using variables

indica<ngnil-filersandregimetype1. Nil+Realregime2. Nil+Lump-sumregime3. Posi<veincome+Realregime4. Posi<veincome+Lump-sumregime

2. Withineachstrata,randomlyallocate1/10ofsample

toeachof10treatmentgroups,asi. Threedeliverymethodsii. Threemessagesiii. ControlgroupreceivingnoleIer

q 10treatmentsx4groups=40cases

ETRbasedonoverallincome Decile PIT

FlatPIT

Lump-sum

PITReal

CITReal

1 20.6 3 2.2 3.02 2.7 3 1.2 1.63 2.7 3 1.3 1.64 2.8 3 1.2 1.45 2.6 3 1.4 1.56 2.3 3 1.5 1.87 2.0 3 1.5 1.48 1.6 3 1.0 1.49 2.3 3 0.8 1.410 2.1 3 0.7 1.5

Compliancegap

Scenario:

lowerbound(in%)

Scenario:

Upperbound(in%)

PITrealregime 4.8 34.8CITrealregime 2.3 24.7VATPAYE

3.52.1

15.510.3

KigaliOutsideKigaliLargeandtop-mediumSmallandmedium

1.95.3

1.25.7

11.564.9

7.343.7