Tax Certainty - EBF – European Banking Federation Certainty EBF TAX CONFERENCE 2017 Brussels, 22...

29

Tax Certainty EBF TAX CONFERENCE 2017 Brussels, 22 November 2017 Giorgia Maffini OECD’s Centre for Tax Policy and Administration

Transcript of Tax Certainty - EBF – European Banking Federation Certainty EBF TAX CONFERENCE 2017 Brussels, 22...

Tax CertaintyEBF TAX CONFERENCE 2017

Brussels, 22 November 2017

Giorgia Maffini

OECD’s Centre for Tax Policy and Administration

Tax certainty

• “We welcome the … work on tax certainty conducted by the OECD andthe IMF. We acknowledge the report on Tax Certainty submitted to usand encourage jurisdictions to consider voluntarily the practical toolsfor enhanced tax certainty as proposed in that report, including withrespect to dispute prevention and dispute resolution to beimplemented within domestic legal frameworks and international taxtreaties.”

• “We ask the OECD and the IMF to assess progress in enhancing taxcertainty in 2018”

1. www.oecd.org/tax/g20-report-on-tax-certainty.htm

Tax certainty report 1 delivered to G20 Finance Ministers with IMF, March 2017

Chair of the Inclusive Framework has written to all subsidiary bodies

2

The business survey

The OECD Business Tax Certainty Survey

• Between 18 October and 16 December 2016

• 724 completed responses

• From firms with global HQ in 62 different jurisdictions

• And regional HQs in 105 different jurisdictions

Wide consultation

• Survey was developed on basis of Tax Survey developed by OUCBT and ETPF

• Consultation with business, governments/tax administrations, civil society, academia

3

Global Headquarters

Business survey – global HQs

4

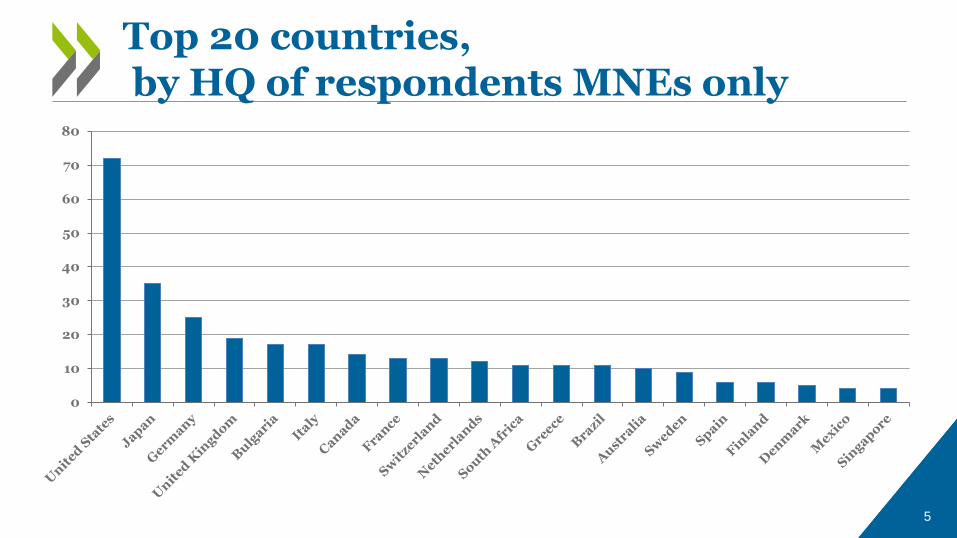

Top 20 countries,by HQ of respondents MNEs only

0

10

20

30

40

50

60

70

80

5

Business survey - regional HQs

Regional Headquarters

6

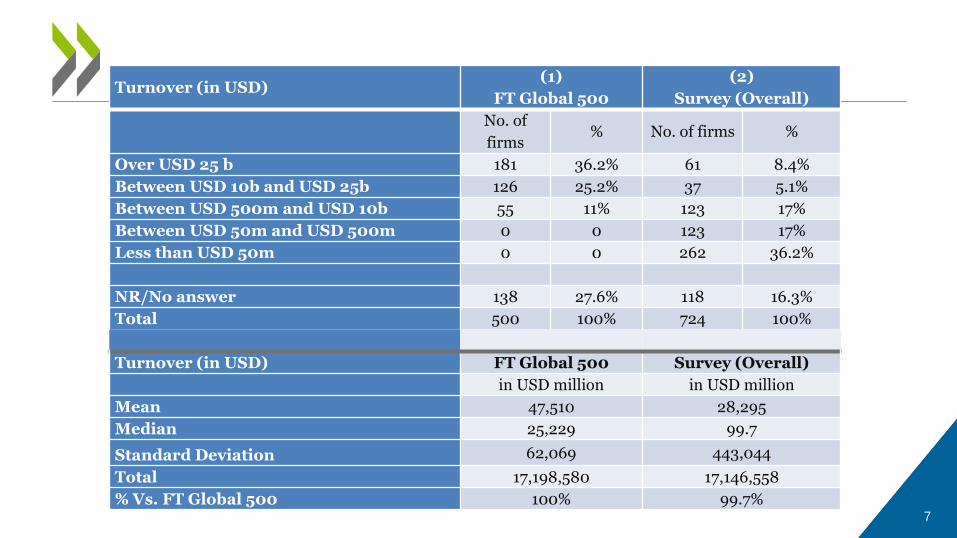

Turnover (in USD)(1)

FT Global 500

(2)

Survey (Overall)

No. of

firms% No. of firms %

Over USD 25 b 181 36.2% 61 8.4%

Between USD 10b and USD 25b 126 25.2% 37 5.1%

Between USD 500m and USD 10b 55 11% 123 17%

Between USD 50m and USD 500m 0 0 123 17%

Less than USD 50m 0 0 262 36.2%

NR/No answer 138 27.6% 118 16.3%

Total 500 100% 724 100%

Turnover (in USD) FT Global 500 Survey (Overall)

in USD million in USD million

Mean 47,510 28,295

Median 25,229 99.7

Standard Deviation 62,069 443,044

Total 17,198,580 17,146,558

% Vs. FT Global 500 100% 99.7%7

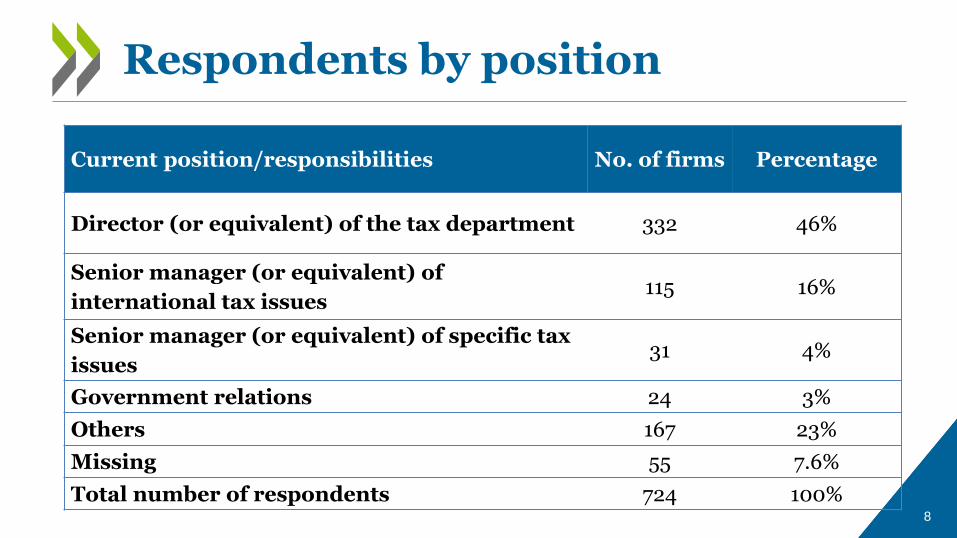

Current position/responsibilities No. of firms Percentage

Director (or equivalent) of the tax department 332 46%

Senior manager (or equivalent) of

international tax issues115 16%

Senior manager (or equivalent) of specific tax

issues 31 4%

Government relations 24 3%

Others 167 23%

Missing 55 7.6%

Total number of respondents 724 100%

Respondents by position

8

9

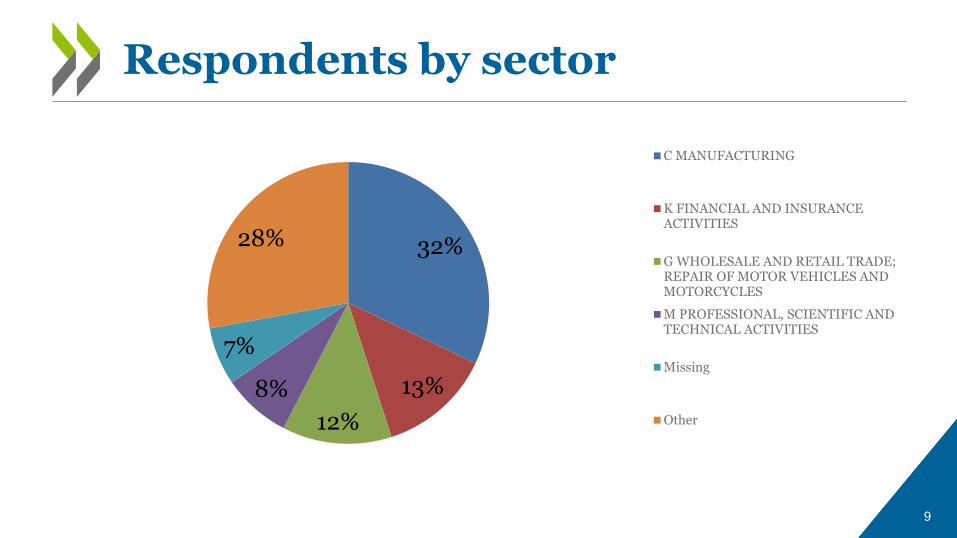

Respondents by sector

32%

13%

12%

8%

7%

28%

C MANUFACTURING

K FINANCIAL AND INSURANCEACTIVITIES

G WHOLESALE AND RETAIL TRADE;REPAIR OF MOTOR VEHICLES ANDMOTORCYCLES

M PROFESSIONAL, SCIENTIFIC ANDTECHNICAL ACTIVITIES

Missing

Other

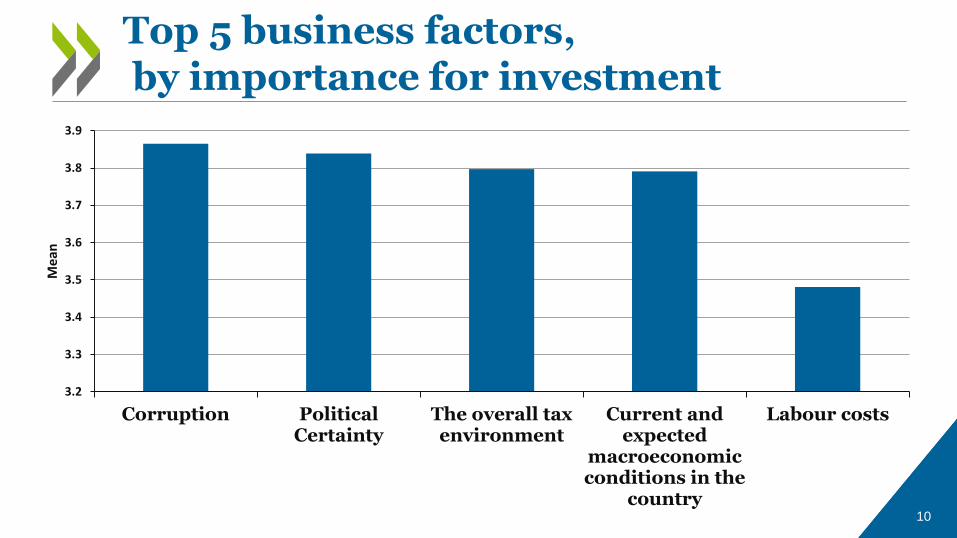

Top 5 business factors,by importance for investment

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

Corruption PoliticalCertainty

The overall taxenvironment

Current andexpected

macroeconomicconditions in the

country

Labour costs

Mea

n

10

11

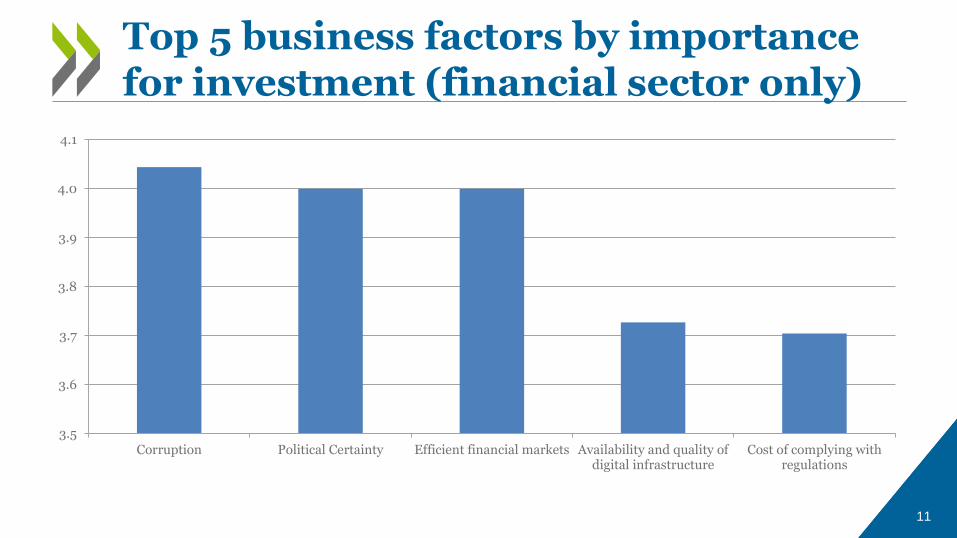

Top 5 business factors by importance for investment (financial sector only)

3.5

3.6

3.7

3.8

3.9

4.0

4.1

Corruption Political Certainty Efficient financial markets Availability and quality ofdigital infrastructure

Cost of complying withregulations

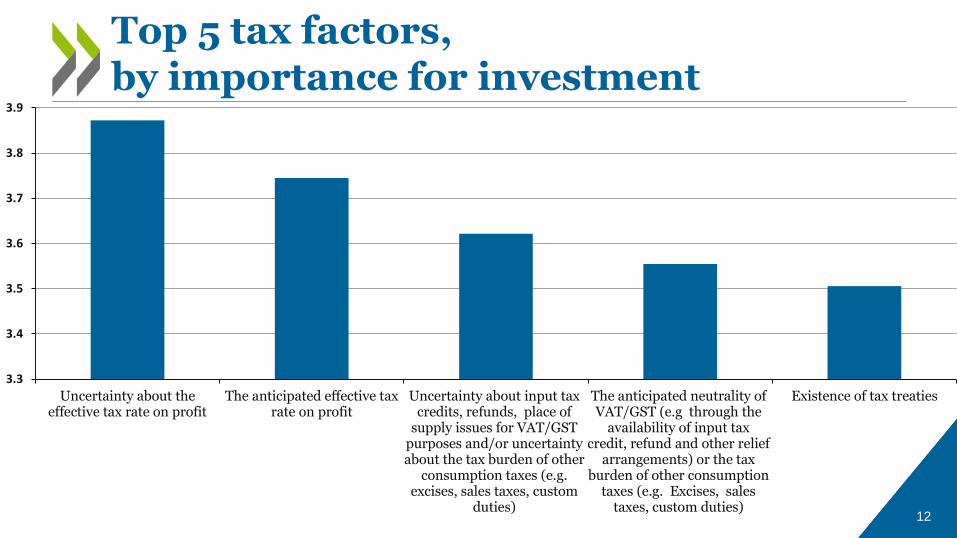

Top 5 tax factors,by importance for investment

3.3

3.4

3.5

3.6

3.7

3.8

3.9

Uncertainty about theeffective tax rate on profit

The anticipated effective taxrate on profit

Uncertainty about input taxcredits, refunds, place of

supply issues for VAT/GSTpurposes and/or uncertaintyabout the tax burden of other

consumption taxes (e.g.excises, sales taxes, custom

duties)

The anticipated neutrality ofVAT/GST (e.g through the

availability of input taxcredit, refund and other relief

arrangements) or the taxburden of other consumption

taxes (e.g. Excises, salestaxes, custom duties)

Existence of tax treaties

12

13

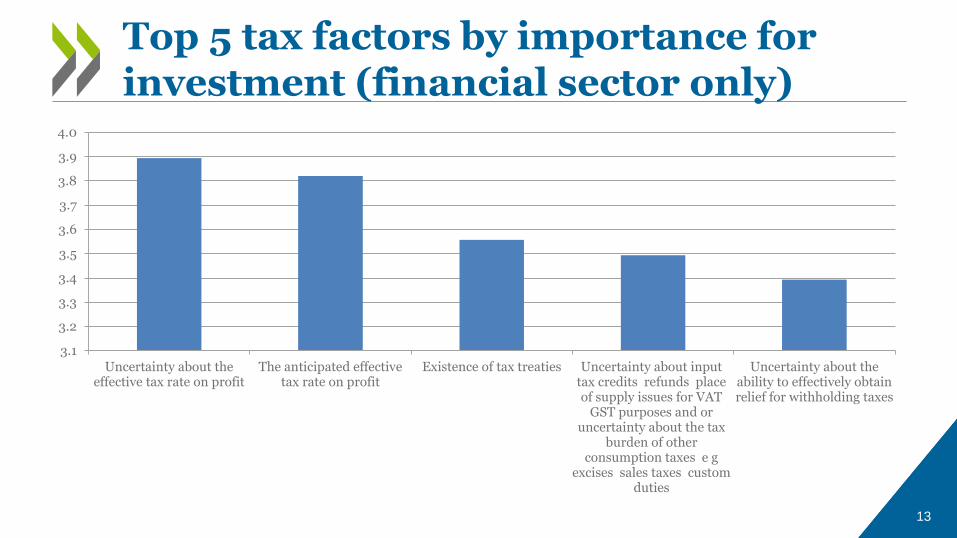

Top 5 tax factors by importance for investment (financial sector only)

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

4.0

Uncertainty about theeffective tax rate on profit

The anticipated effectivetax rate on profit

Existence of tax treaties Uncertainty about inputtax credits refunds placeof supply issues for VAT

GST purposes and oruncertainty about the tax

burden of otherconsumption taxes e g

excises sales taxes customduties

Uncertainty about theability to effectively obtainrelief for withholding taxes

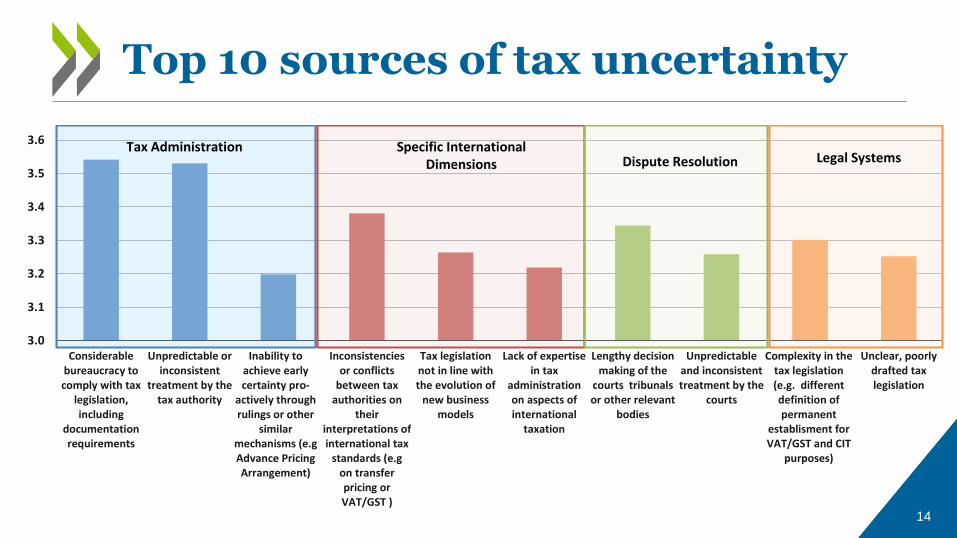

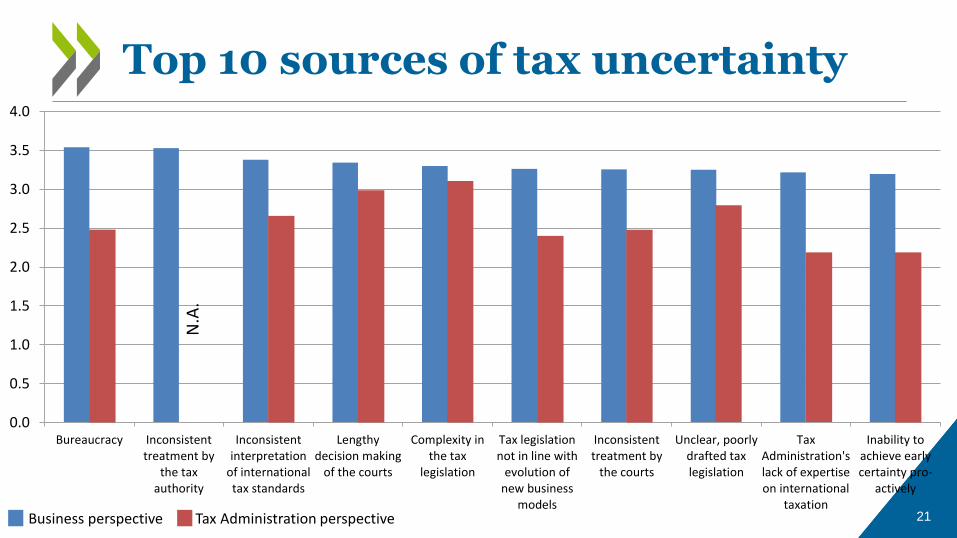

Top 10 sources of tax uncertainty

3.0

3.1

3.2

3.3

3.4

3.5

3.6

Considerablebureaucracy tocomply with tax

legislation,including

documentationrequirements

Unpredictable orinconsistent

treatment by thetax authority

Inability toachieve earlycertainty pro-

actively throughrulings or other

similarmechanisms (e.gAdvance PricingArrangement)

Inconsistenciesor conflicts

between taxauthorities on

theirinterpretations ofinternational tax

standards (e.gon transferpricing orVAT/GST )

Tax legislationnot in line withthe evolution of

new businessmodels

Lack of expertisein tax

administrationon aspects ofinternational

taxation

Lengthy decisionmaking of the

courts tribunalsor other relevant

bodies

Unpredictableand inconsistenttreatment by the

courts

Complexity in thetax legislation(e.g. differentdefinition ofpermanent

establisment forVAT/GST and CIT

purposes)

Unclear, poorlydrafted taxlegislation

Tax Administration Specific International Dimensions Dispute Resolution Legal Systems

14

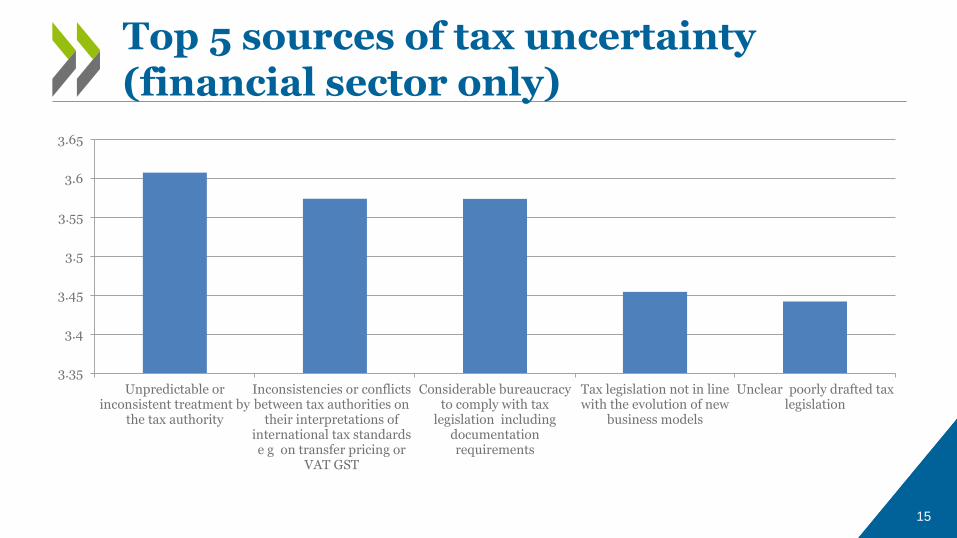

15

Top 5 sources of tax uncertainty (financial sector only)

3.35

3.4

3.45

3.5

3.55

3.6

3.65

Unpredictable orinconsistent treatment by

the tax authority

Inconsistencies or conflictsbetween tax authorities on

their interpretations ofinternational tax standardse g on transfer pricing or

VAT GST

Considerable bureaucracyto comply with tax

legislation includingdocumentationrequirements

Tax legislation not in linewith the evolution of new

business models

Unclear poorly drafted taxlegislation

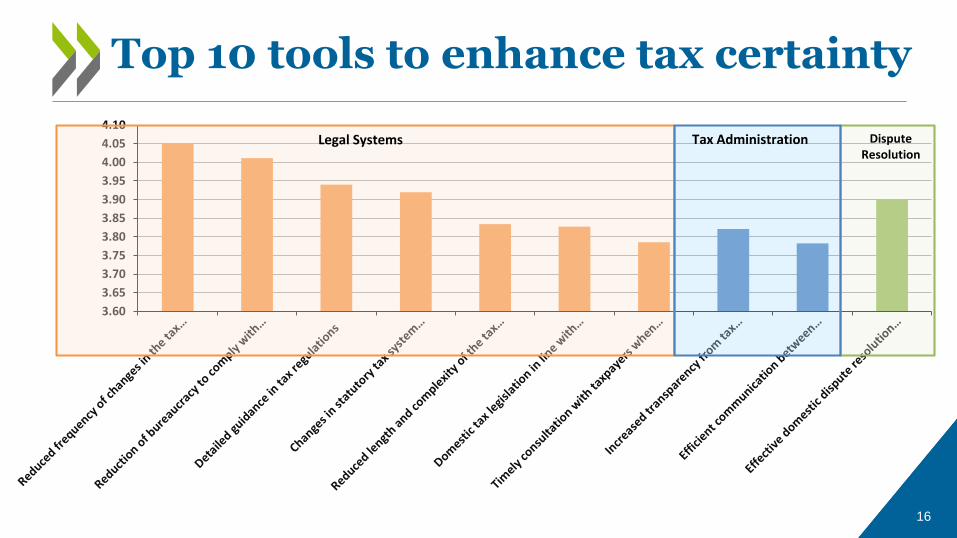

Top 10 tools to enhance tax certainty

3.60

3.65

3.70

3.75

3.80

3.85

3.90

3.95

4.00

4.05

4.10Legal Systems Dispute

ResolutionTax Administration

16

17

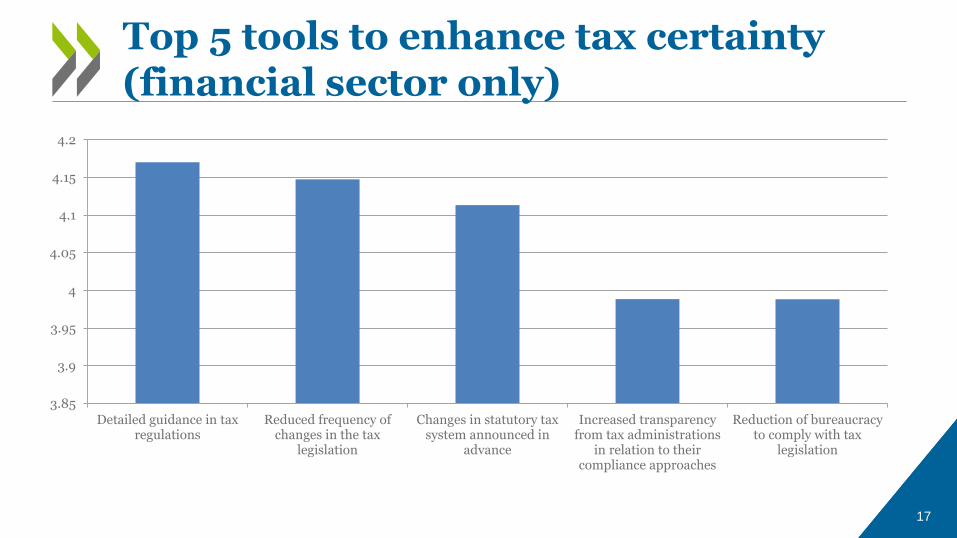

Top 5 tools to enhance tax certainty (financial sector only)

3.85

3.9

3.95

4

4.05

4.1

4.15

4.2

Detailed guidance in taxregulations

Reduced frequency ofchanges in the tax

legislation

Changes in statutory taxsystem announced in

advance

Increased transparencyfrom tax administrations

in relation to theircompliance approaches

Reduction of bureaucracyto comply with tax

legislation

• Multilateral Advance Pricing Agreements (APAs )

– 36% of respondents say very important and extremely important

– This figure is 44% when we only consider MNEs

• Multilateral audits

– 25% of respondents say very important and extremely important

• Multilateral cooperative compliance programmes

– 31% of respondents say very important and extremely important

– This figure is 36% when we only consider MNEs

Tools to support certainty in international tax

Some innovative options received strong support

18

The tax administration survey (1)

• Conducted with members of the Forum on Tax Administration (FTA)

• Allow tax administrations to respond to results of business survey

– Is tax certainty a priority for tax administrations?

– What creates uncertainty for tax administrations?

– Which measures effective in increasing certainty?

– 25 OECD and G20 countries

The OECD/FTA Tax Certainty Survey of Tax Administrations

19

The tax administration survey (2)

• Tax certainty is a high priority for tax administrations too

• Over 80% of respondents: very high/extremely high priority for tax administration

• Tax administrations recognise tax uncertainty important concern for business

• For tax administration, an important source of tax uncertainty is taxpayers’ behaviour, especially when involving aggressive tax planning

The OECD/FTA Tax Certainty Survey of Tax Administrations

20

Top 10 sources of tax uncertainty

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Bureaucracy Inconsistenttreatment by

the taxauthority

Inconsistentinterpretation

of internationaltax standards

Lengthydecision making

of the courts

Complexity inthe tax

legislation

Tax legislationnot in line with

evolution ofnew business

models

Inconsistenttreatment by

the courts

Unclear, poorlydrafted taxlegislation

TaxAdministration'slack of expertiseon international

taxation

Inability toachieve earlycertainty pro-

actively

Business perspective Tax Administration perspective

N.A

.

21

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Reduction ofbureaucracy

Efficientcommunicationwith taxpayers

Increasedtransparency in

relation tocompliance /

risk assessment

Mutualagreementprocedures

Timelycommunication

during taxaudits

Simplifiedapproaches fortax compliance

MultilateralAPAs

Domestic co-operative

complianceprogrammes

Unilateral APAs Multilateral co-operative

complianceprogrammes

Top 10 tools to enhance tax certainty controlled by the tax administration

Business perspective Tax Administration perspective22

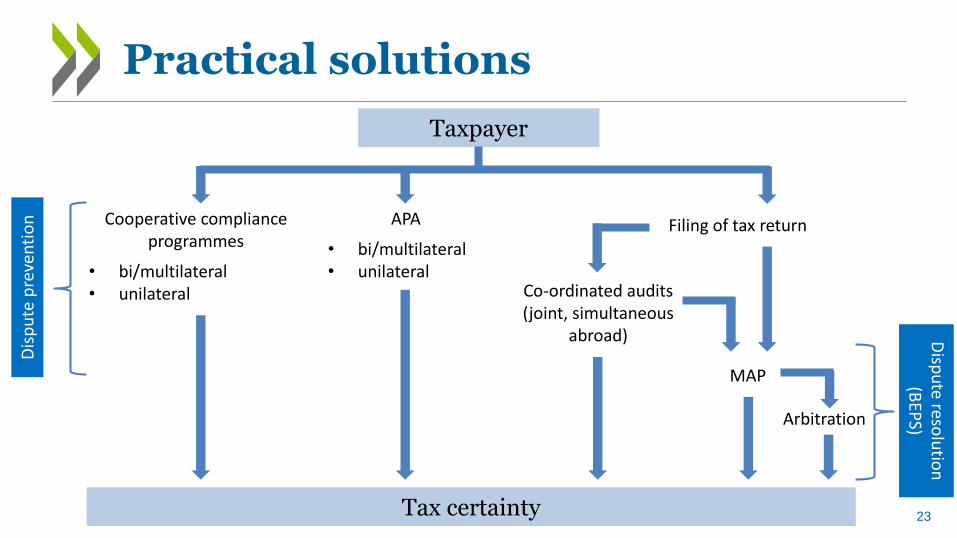

Cooperative compliance programmes

• bi/multilateral • unilateral

APA

• bi/multilateral• unilateral

Filing of tax return

Co-ordinated audits (joint, simultaneous

abroad)

MAP

Arbitration

Taxpayer

Tax certainty

Dis

pu

te p

reve

nti

on

Disp

ute reso

lutio

n(B

EPS)

Practical solutions

23

• Standardised system for claiming withholding tax relief at source on portfolio investments

• Developed jointly with business and adopted in January 2013 and subsequently aligned to Common Reporting Standard (CRS) in 2015

• Based on CRS infrastructure and technical solutions

TRACE: common standard for source country taxation

24

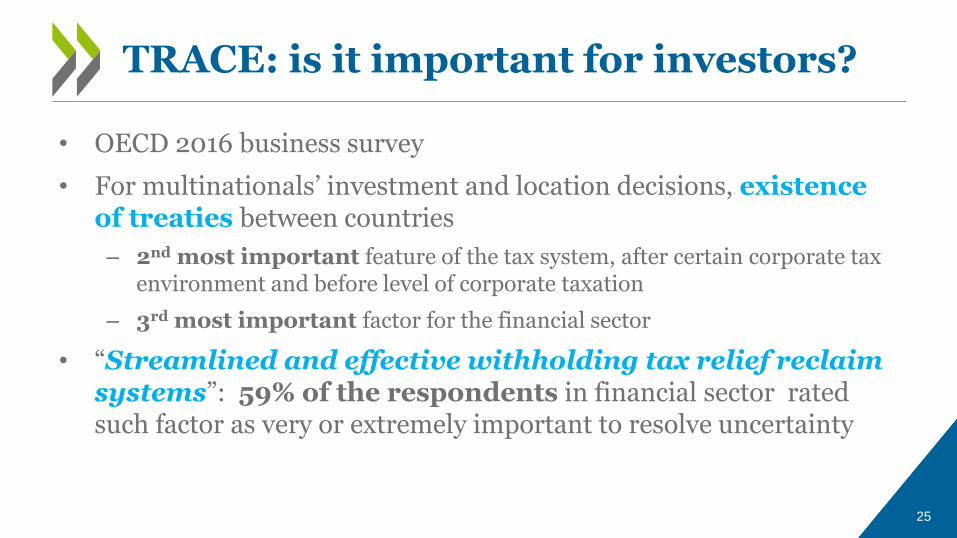

• OECD 2016 business survey

• For multinationals’ investment and location decisions, existence of treaties between countries

– 2nd most important feature of the tax system, after certain corporate tax environment and before level of corporate taxation

– 3rd most important factor for the financial sector

• “Streamlined and effective withholding tax relief reclaim systems”: 59% of the respondents in financial sector rated such factor as very or extremely important to resolve uncertainty

TRACE: is it important for investors?

25

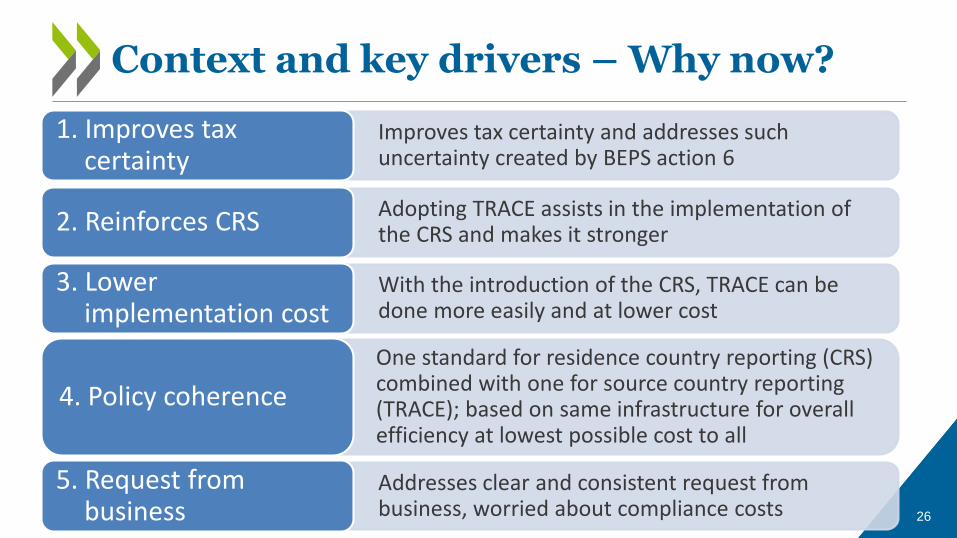

One standard for residence country reporting (CRS) combined with one for source country reporting (TRACE); based on same infrastructure for overall efficiency at lowest possible cost to all

Addresses clear and consistent request from business, worried about compliance costs

With the introduction of the CRS, TRACE can be done more easily and at lower cost

Improves tax certainty and addresses such uncertainty created by BEPS action 6

26

Context and key drivers – Why now?

4. Policy coherence

Adopting TRACE assists in the implementation of the CRS and makes it stronger2. Reinforces CRS

3. Lower implementation cost

1. Improves tax certainty

5. Request from business

• OECD working on its technical implementation

• Until recently, actual country implementation on

hold: both governments and business busy

implementing CRS and FATCA

TRACE: where are we?

27

Contact details on TRACE

Philip KERFS

Centre for Tax Policy and Administration

2, rue André Pascal - 75775 Paris Cedex 16 Tel: + 33 (01) 45 24 93 52

[email protected] || www.oecd.org/tax

28

Contact details

Giorgia Maffini

Deputy Head of the Tax Policy and Statistics DivisionCentre for Tax Policy and Administration

2, rue André Pascal - 75775 Paris Cedex 16 Tel: +33 1 45 24 15 14

[email protected] || www.oecd.org/tax29