Taunton - Academy Update - July 2016

74

Academy Schools Accounting and tax update seminar July 2016

-

Upload

pkf-francis-clark -

Category

Business

-

view

120 -

download

1

Transcript of Taunton - Academy Update - July 2016

Academy Schools

Accounting and tax update seminar July 2016

Welcome

Martin Lock

pkf-francisclark.co.uk

.

Housekeeping

Agenda

• Accounts Direction 2016 – Stephanie Henshaw

• New information request spreadsheet – Kate

Taylor

• Regularity – Martin Lock

• Multi Academy Trusts – Laura Waycott

• VAT Update – Liam Dushynsky

• Tax Update – Martin Lock

• Q&A - All

pkf-francisclark.co.uk

Accounts Direction 2016

Stephanie Henshaw

Academies Accounts Direction 2016

This session will cover:

• What has changed for 2016

• What this means in practice for the information

you will need to provide

• What other changes you will see in the financial

statements

pkf-francisclark.co.uk

pkf-francisclark.co.uk

.

Academies Accounts Direction 2016

FRS102

• 2015 accounts were prepared under a framework of

accounting standards which formed UK GAAP

(Generally Accepted Accounting Practice)

• Complete overhaul this year with the introduction of

FRS102

Sounds daunting but in practice the impact on the

numbers in your accounts will be minimal.

pkf-francisclark.co.uk

.

Academies Accounts Direction 2016

SORP 2015

• The SORP is the Statement of Recommended

Practice which sets out how charities should apply the

accounting standards

• New SORP for 2015 to take account of FRS102, but

includes other changes

• No major impact on the numbers reported, but lots of

changes to presentation and formats

pkf-francisclark.co.uk

.

What is ‘transition’

There will be reference at times to ‘transition date’ for

FRS102

• This is the date at the start of the comparative period

for the year in which FRS102 is adopted

• For all Academies it will be 1 September 2014

pkf-francisclark.co.uk

.

Key changes

Which areas may impact Academy Trusts?

• Trustees’ report

• Changes to the SOFA

• Balance sheet and cash flow

• Accounting policies and disclosure requirements

pkf-francisclark.co.uk

.

Key changes

Trustees’ report

• Explain arrangements and policies for setting pay and

remuneration of the academy trust’s key management

personnel, including an explanation of any benchmark

or parameters / criteria used for setting pay

Action: determine key management

personnel

pkf-francisclark.co.uk

.

Key changes

Trustees’ report

• Describe the main risks to the academy and

summarise plans and strategies in place to manage

them

Action: ensure that risk registers are

up to date and that strategies are in

place for all key risks

pkf-francisclark.co.uk

.

Key changes

Trustees’ report

• Compare actual level of reserves to policy and identify

free reserves held

Action: check reserves policy in

place and appropriate

pkf-francisclark.co.uk

.

Key changes

SoFA

• Presentational changes to headings / descriptions for

various income and expenditure, eg ‘voluntary income’

now ‘donations’

• Governance costs no longer separately disclosed, but

will be included as support costs within charitable

expenditure

Action: Normal analysis of income

and expenditure required – FC will

deal with the changes

pkf-francisclark.co.uk

.

Key changes

SoFA

• Comparatives required for all columns now, not just the

total

Action: None – FC will deal with

(major headache!)

pkf-francisclark.co.uk

.

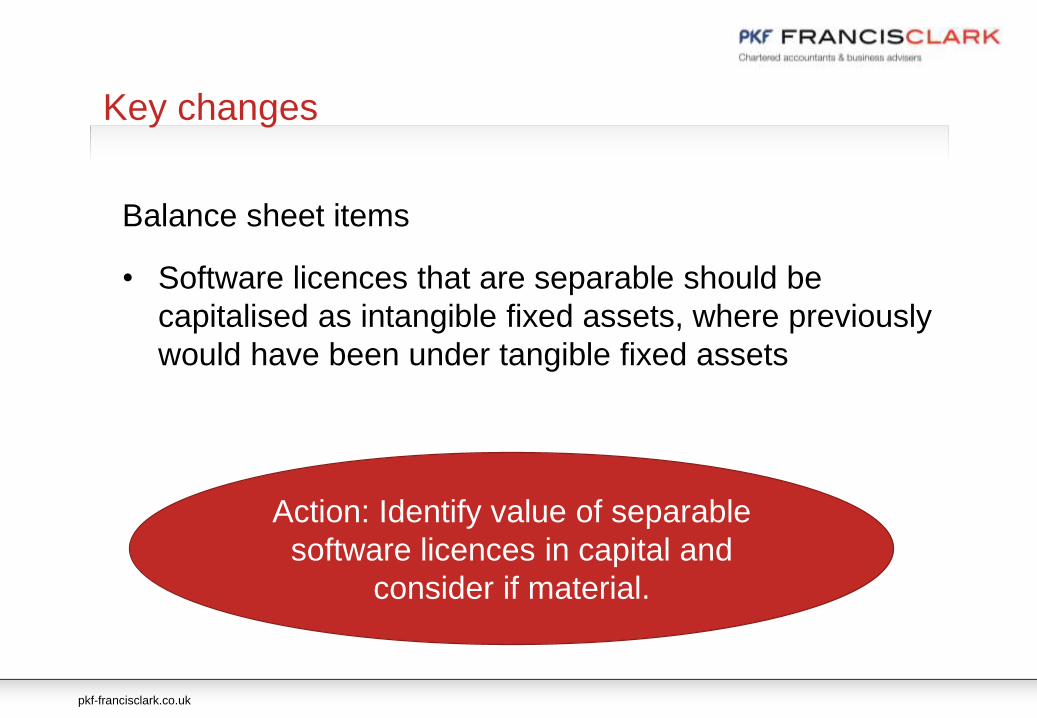

Key changes

Balance sheet items

• Software licences that are separable should be

capitalised as intangible fixed assets, where previously

would have been under tangible fixed assets

Action: Identify value of separable

software licences in capital and

consider if material.

pkf-francisclark.co.uk

.

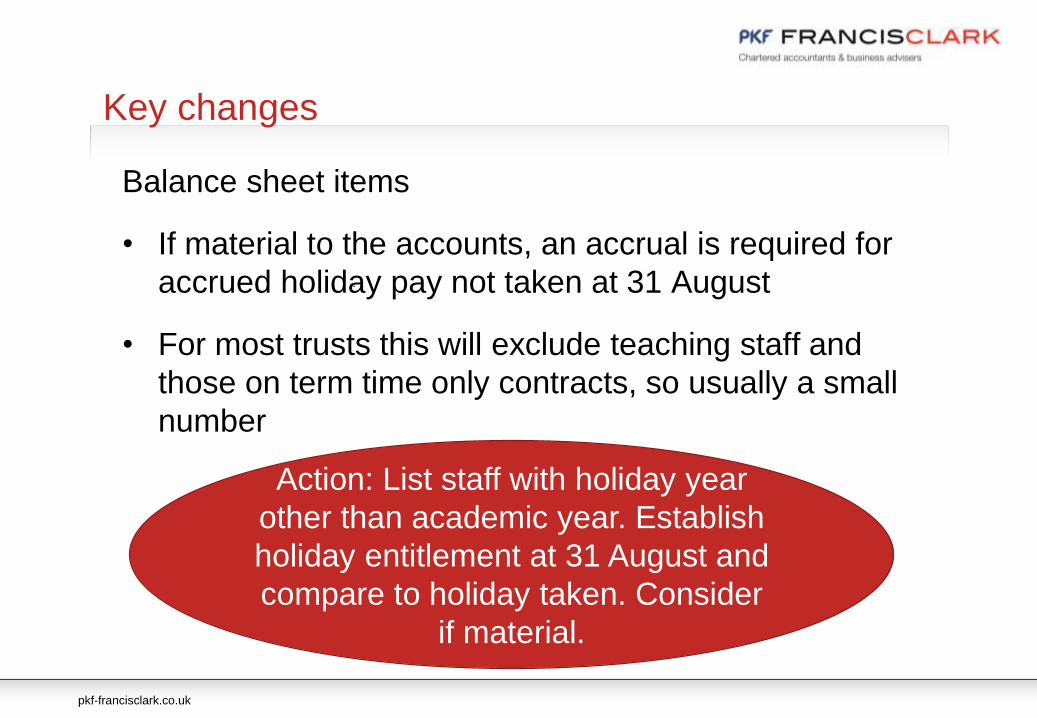

Key changes

Balance sheet items

• If material to the accounts, an accrual is required for

accrued holiday pay not taken at 31 August

• For most trusts this will exclude teaching staff and

those on term time only contracts, so usually a small

number

Action: List staff with holiday year

other than academic year. Establish

holiday entitlement at 31 August and

compare to holiday taken. Consider

if material.

pkf-francisclark.co.uk

.

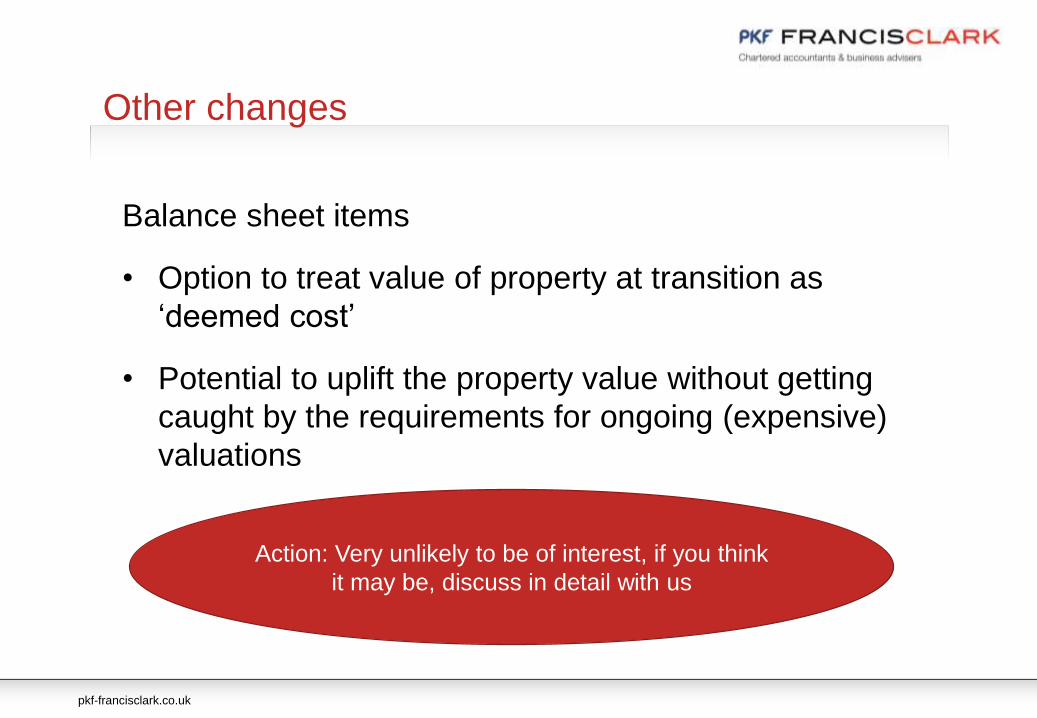

Other changes

Balance sheet items

• Option to treat value of property at transition as

‘deemed cost’

• Potential to uplift the property value without getting

caught by the requirements for ongoing (expensive)

valuations

Action: Very unlikely to be of interest, if you think

it may be, discuss in detail with us

pkf-francisclark.co.uk

.

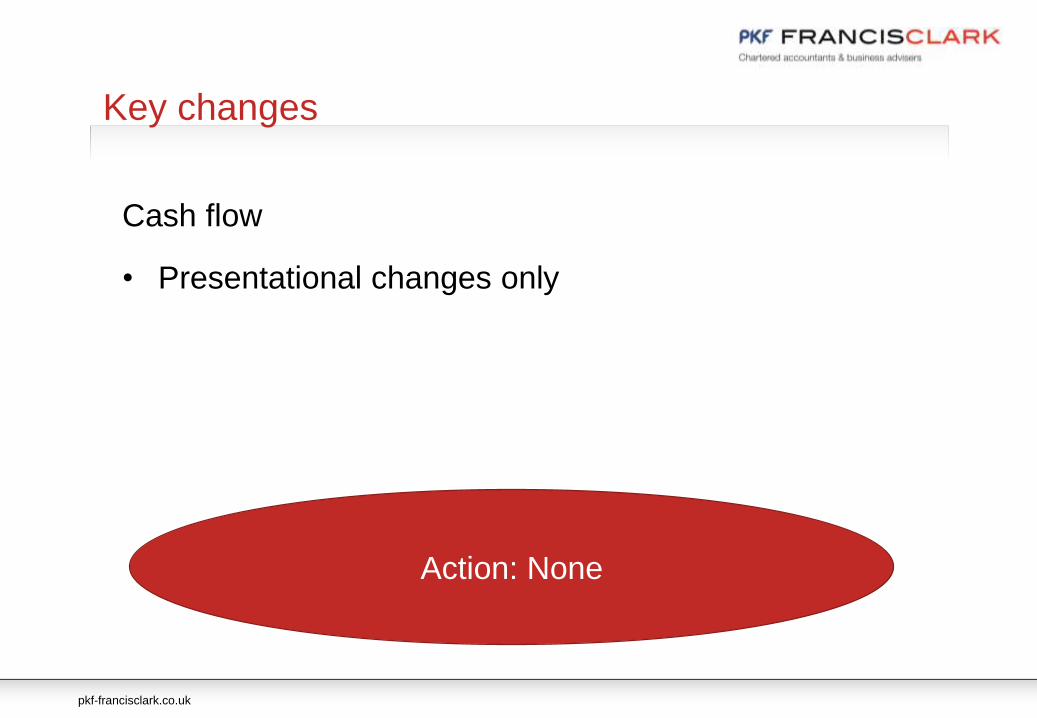

Key changes

Cash flow

• Presentational changes only

Action: None

pkf-francisclark.co.uk

.

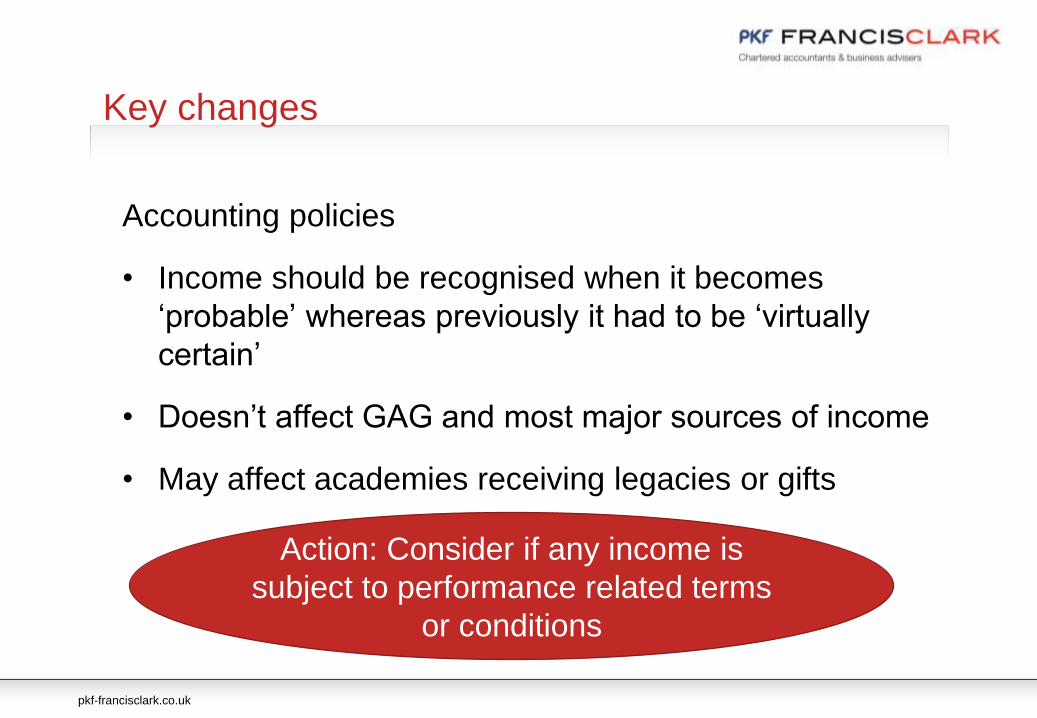

Key changes

Accounting policies

• Income should be recognised when it becomes

‘probable’ whereas previously it had to be ‘virtually

certain’

• Doesn’t affect GAG and most major sources of income

• May affect academies receiving legacies or gifts

Action: Consider if any income is

subject to performance related terms

or conditions

pkf-francisclark.co.uk

.

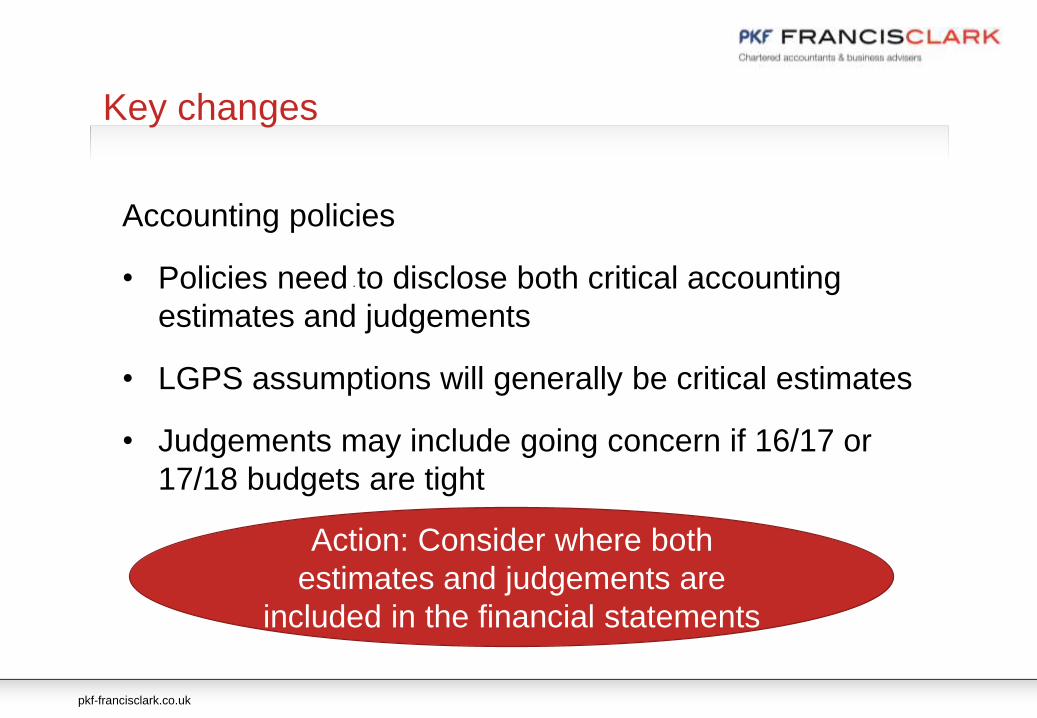

Key changes

Accounting policies

• Policies need to disclose both critical accounting

estimates and judgements

• LGPS assumptions will generally be critical estimates

• Judgements may include going concern if 16/17 or

17/18 budgets are tight

Action: Consider where both

estimates and judgements are

included in the financial statements

pkf-francisclark.co.uk

.

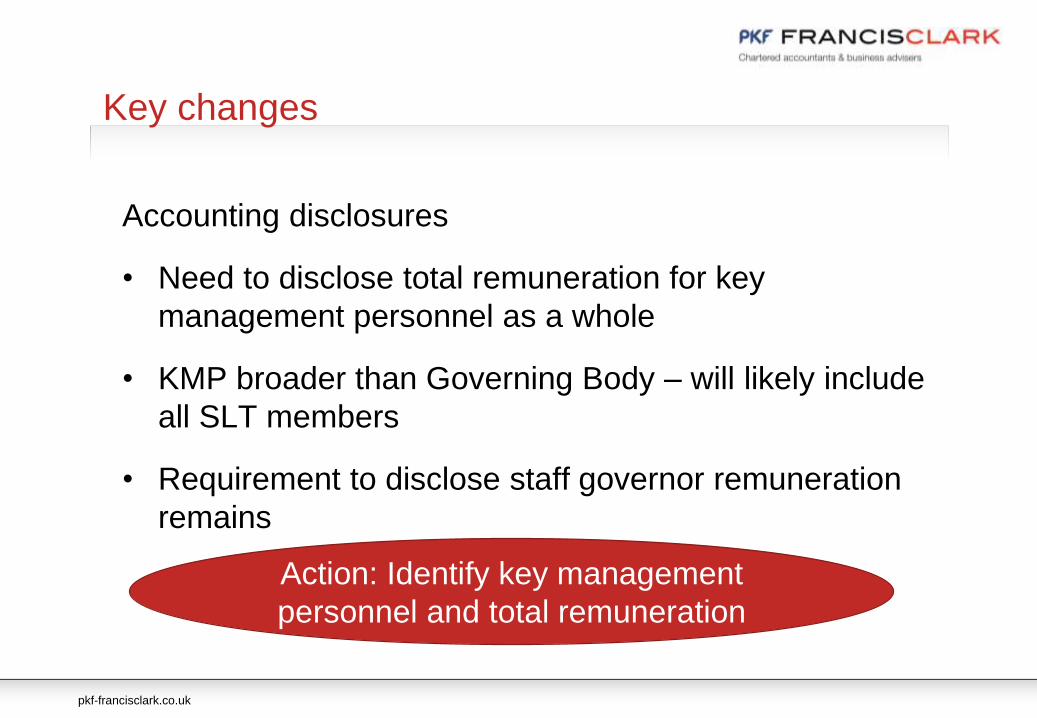

Key changes

Accounting disclosures

• Need to disclose total remuneration for key

management personnel as a whole

• KMP broader than Governing Body – will likely include

all SLT members

• Requirement to disclose staff governor remuneration

remains

Action: Identify key management

personnel and total remuneration

pkf-francisclark.co.uk

.

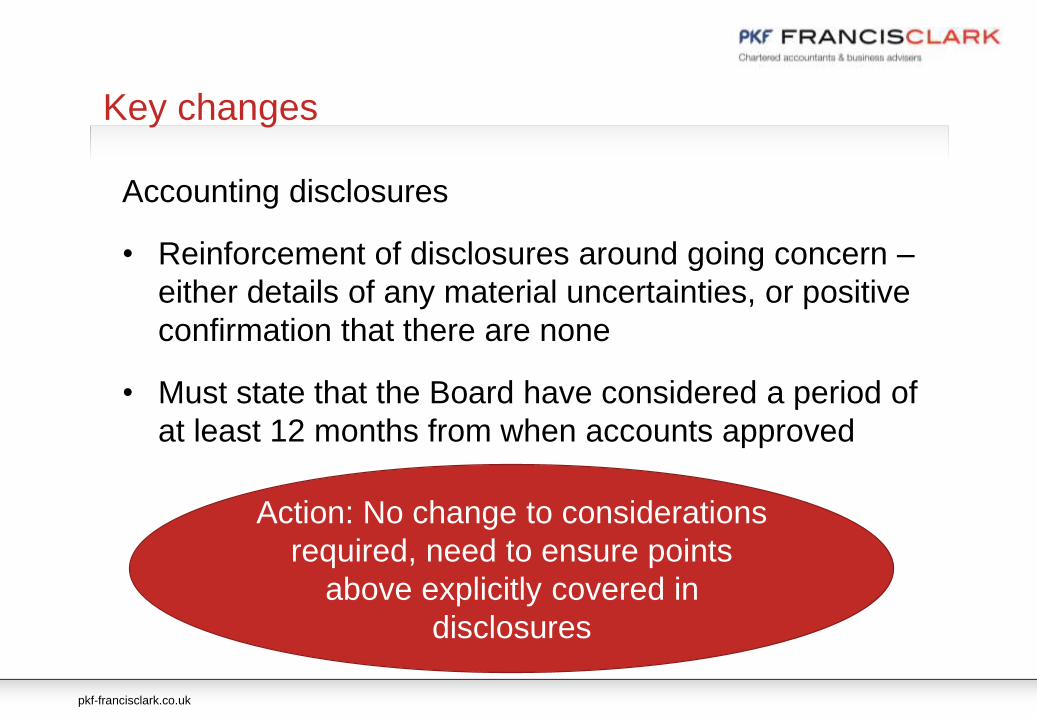

Key changes

Accounting disclosures

• Reinforcement of disclosures around going concern –

either details of any material uncertainties, or positive

confirmation that there are none

• Must state that the Board have considered a period of

at least 12 months from when accounts approved

Action: No change to considerations

required, need to ensure points

above explicitly covered in

disclosures

pkf-francisclark.co.uk

.

Key changes

Accounting disclosures

• All related party transactions must be disclosed

• Must state whether on an arm’s length basis, and must

have evidence to substantiate where this is stated

Action: Continue to identify all

related party transactions

pkf-francisclark.co.uk

.

Key changes

Accounting disclosures - LGPS

• Detailed valuation requirements have changed – will be

reflected in the report provided

• A ‘net interest charge’ will replace ‘expected return on

plan assets’ and ‘interest on pension liabilities’

• Net liability unlikely to be affected

Action: Request report under

FRS102 rather than FRS17,

including relevant comparative

disclosures for 2015

pkf-francisclark.co.uk

.

Key changes

Accounting disclosures

• Commitments under operating leases will now be the

total minimum commitment for the term of the lease,

not the annual commitment

Action: No change in the information

required, but disclosures will be

different in the accounts

pkf-francisclark.co.uk

.

Key changes

Transition

• Various notes will be included to explain the transition

to FRS102 and SORP2015

• There will be a note reconciling opening reserves. In

most cases this will only include the pension charge

adjustments, and holiday pay if this applies

Action: None, FC will deal with this

Academies Accounts Direction 2016

Summary:

• Fundamental changes to the underlying

accounting standards and framework

• Unlikely to be significant impact on numbers

reported

• The changes will mainly come through in

disclosures and formats

• Review the action points

pkf-francisclark.co.uk

New Information Request Form

Kate Taylor

pkf-francisclark.co.uk

We have developed a template to assist with the audit process. It is an alternative to the standard audit request list.

• Why have we put this together?

• Who will this apply to?

Audit Template

Academy Audit Template

Regularity

Martin Lock

pkf-francisclark.co.uk

.

Introduction

• What is Regularity?

• How is Assurance on Regularity Provided?

• What Should the Academy Trust do?

• What Work do the Auditors do on Regularity?

• Problem Areas Identified by the EFA

• Quick Reminders on Connected Party Transactions,

Leasing Transactions and Staff Severance Payments

• Academies Financial Handbook

pkf-francisclark.co.uk

.

What is Regularity?

• In simple terms the academy is handling public funds and

should use it for the purposes intended

• What are you spending it on? What should you be

spending it on?

• Are you following established delegated authorities?

• Delegated responsibility to the Academy Trust (as detailed in

the Academies Financial Handbook and funding agreement)

• Academy Trust delegates to the Accounting Officer

• Accounting Officer delegates to academy staff through the

scheme of delegation and financial procedures manual

pkf-francisclark.co.uk

.

How is Assurance on Regularity Provided?

• National Audit Office require comfort as the academy trust

accounts are consolidated into the EFA’s accounts

• Accounting officer signs off a ‘Statement of Regularity,

Propriety and Compliance’ in the annual report:

“I confirm that I and the academy trust board of trustees are able to identify any

material irregular or improper use of funds by the academy trust, or material non-

compliance with the terms and conditions of funding under the academy trust’s

funding agreement and the Academies Financial Handbook 2015.

I confirm that no instances of material irregularity, impropriety or funding non-

compliance have been discovered to date. If any instances are identified after

the date of this statement, these will be notified to the board of trustees and

EFA.”

pkf-francisclark.co.uk

.

How is Assurance on Regularity Provided?

• Auditors sign separate Reporting Accountant’s assurance

report on regularity

• ‘Limited’ (negative) opinion required

“In the course of our work, nothing has come to our attention which suggests that

in all material respects the expenditure disbursed and income received during

the period to 31 August 2016 has not been applied to purposes intended by

Parliament and the financial transactions do not confirm to the authorities which

govern them.”

pkf-francisclark.co.uk

.

What Should the Academy Trust do?

• Maintain and follow a financial procedures manual and

scheme of delegation compliant with the Academies

Financial Handbook

• We recommend a Key Financial Controls checklist to

evidence compliance (example pro-forma available)

• Ensure knowledge on the trustee board of the Academies

Financial Handbook

• The above will help enable the Accounting Officer to sign off

his/her statements on ‘Regularity, Propriety and

Compliance’, and the ‘Governance Statement’ in the

accounts

pkf-francisclark.co.uk

.

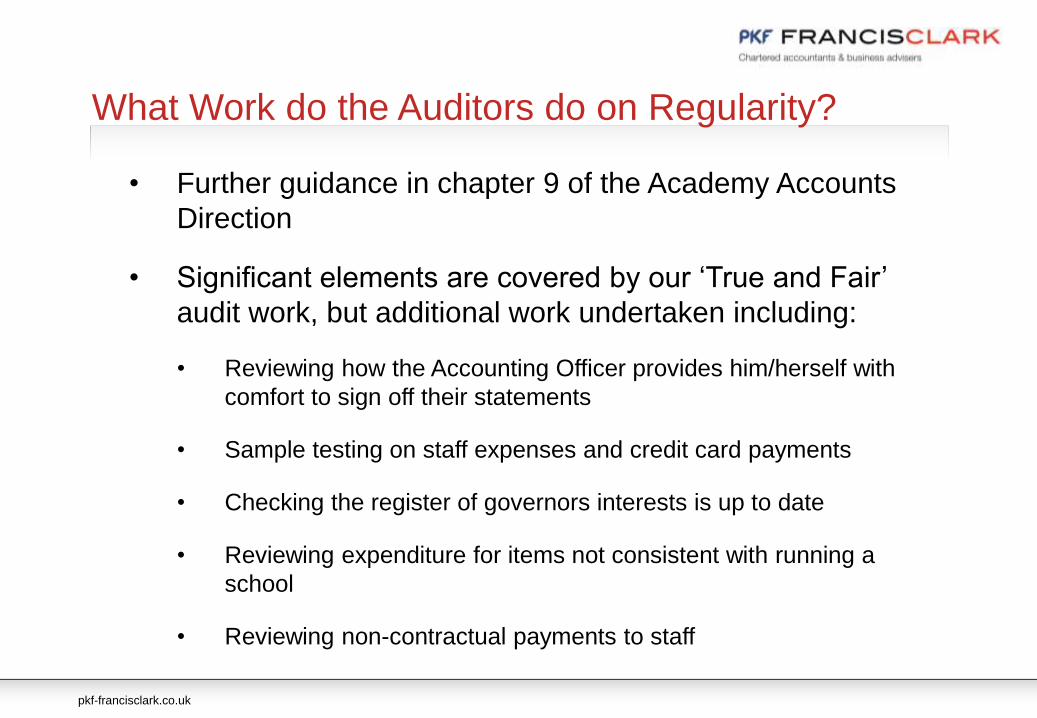

What Work do the Auditors do on Regularity?

• Further guidance in chapter 9 of the Academy Accounts

Direction

• Significant elements are covered by our ‘True and Fair’

audit work, but additional work undertaken including:

• Reviewing how the Accounting Officer provides him/herself with

comfort to sign off their statements

• Sample testing on staff expenses and credit card payments

• Checking the register of governors interests is up to date

• Reviewing expenditure for items not consistent with running a

school

• Reviewing non-contractual payments to staff

pkf-francisclark.co.uk

.

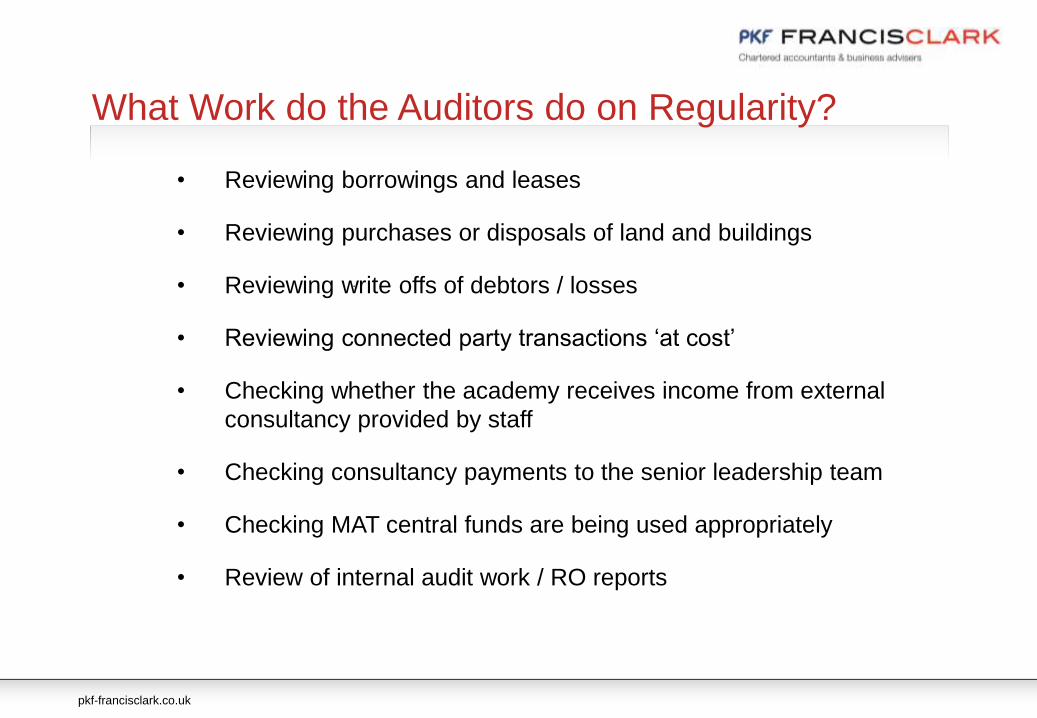

What Work do the Auditors do on Regularity?

• Reviewing borrowings and leases

• Reviewing purchases or disposals of land and buildings

• Reviewing write offs of debtors / losses

• Reviewing connected party transactions ‘at cost’

• Checking whether the academy receives income from external

consultancy provided by staff

• Checking consultancy payments to the senior leadership team

• Checking MAT central funds are being used appropriately

• Review of internal audit work / RO reports

pkf-francisclark.co.uk

.

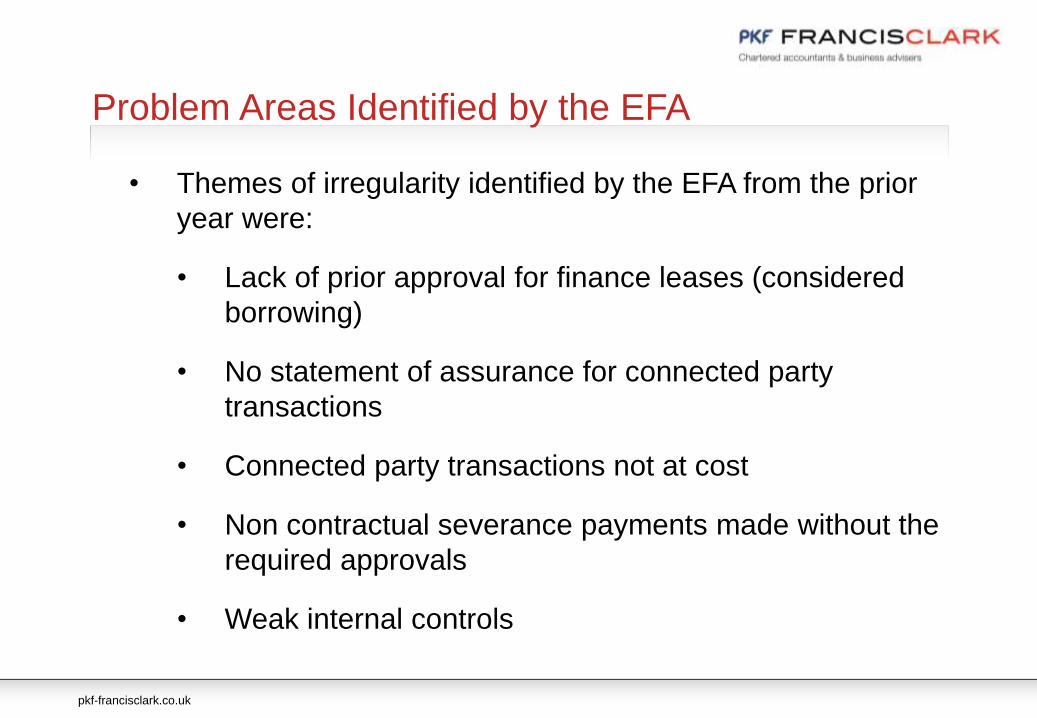

Problem Areas Identified by the EFA

• Themes of irregularity identified by the EFA from the prior

year were:

• Lack of prior approval for finance leases (considered

borrowing)

• No statement of assurance for connected party

transactions

• Connected party transactions not at cost

• Non contractual severance payments made without the

required approvals

• Weak internal controls

pkf-francisclark.co.uk

.

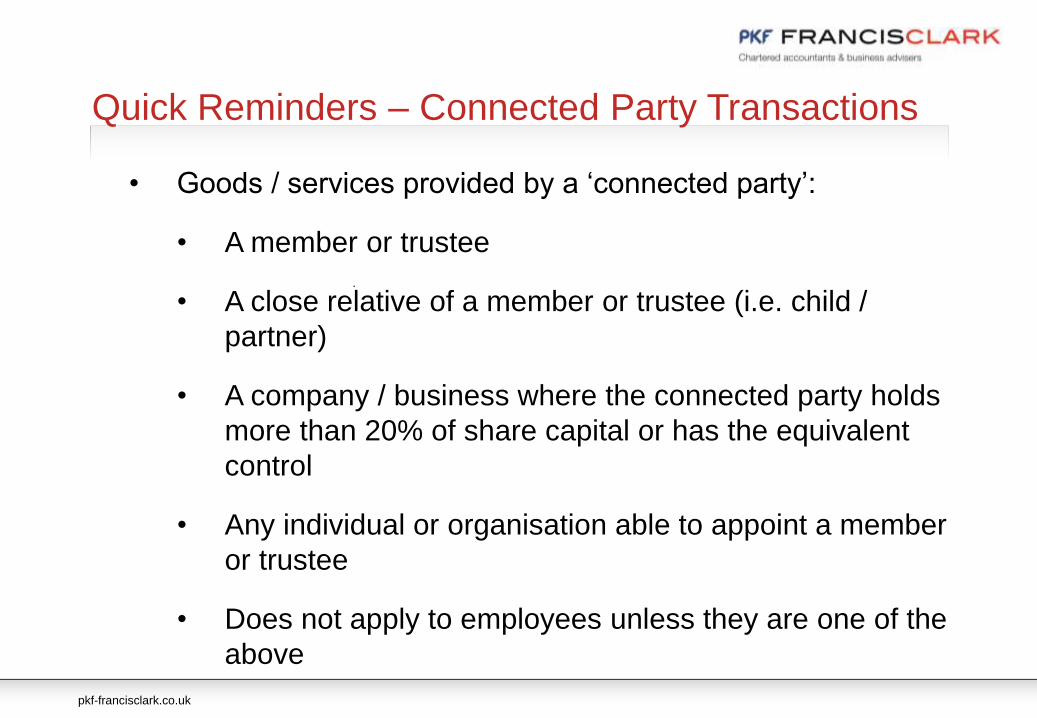

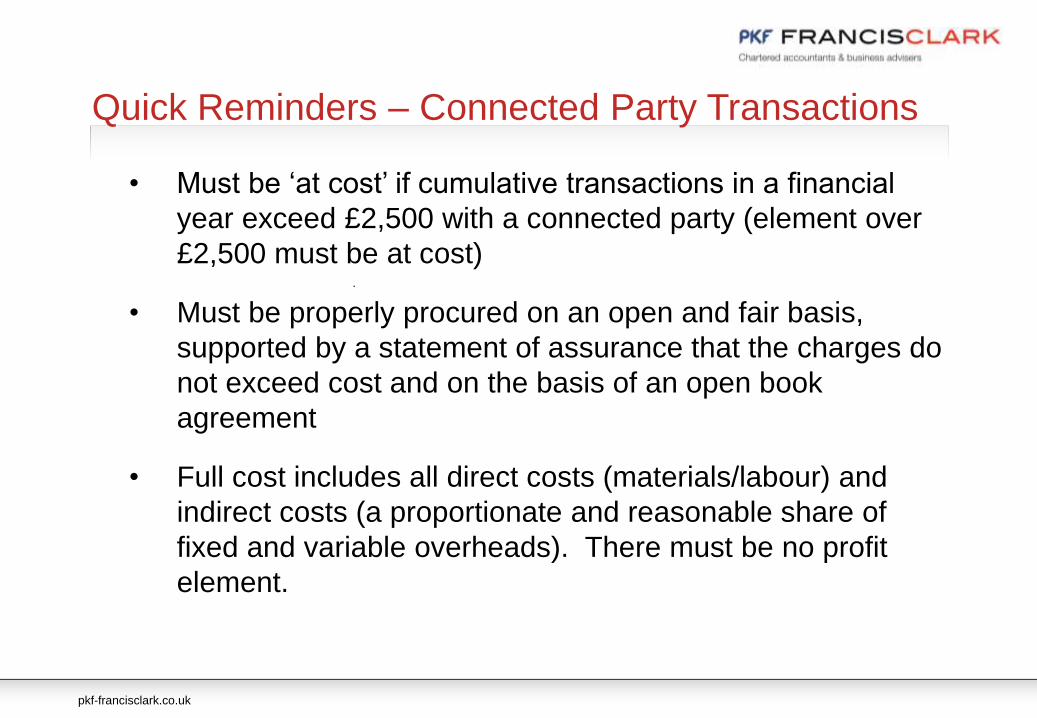

Quick Reminders – Connected Party Transactions

• Goods / services provided by a ‘connected party’:

• A member or trustee

• A close relative of a member or trustee (i.e. child /

partner)

• A company / business where the connected party holds

more than 20% of share capital or has the equivalent

control

• Any individual or organisation able to appoint a member

or trustee

• Does not apply to employees unless they are one of the

above

pkf-francisclark.co.uk

.

Quick Reminders – Connected Party Transactions

• Must be ‘at cost’ if cumulative transactions in a financial

year exceed £2,500 with a connected party (element over

£2,500 must be at cost)

• Must be properly procured on an open and fair basis,

supported by a statement of assurance that the charges do

not exceed cost and on the basis of an open book

agreement

• Full cost includes all direct costs (materials/labour) and

indirect costs (a proportionate and reasonable share of

fixed and variable overheads). There must be no profit

element.

pkf-francisclark.co.uk

.

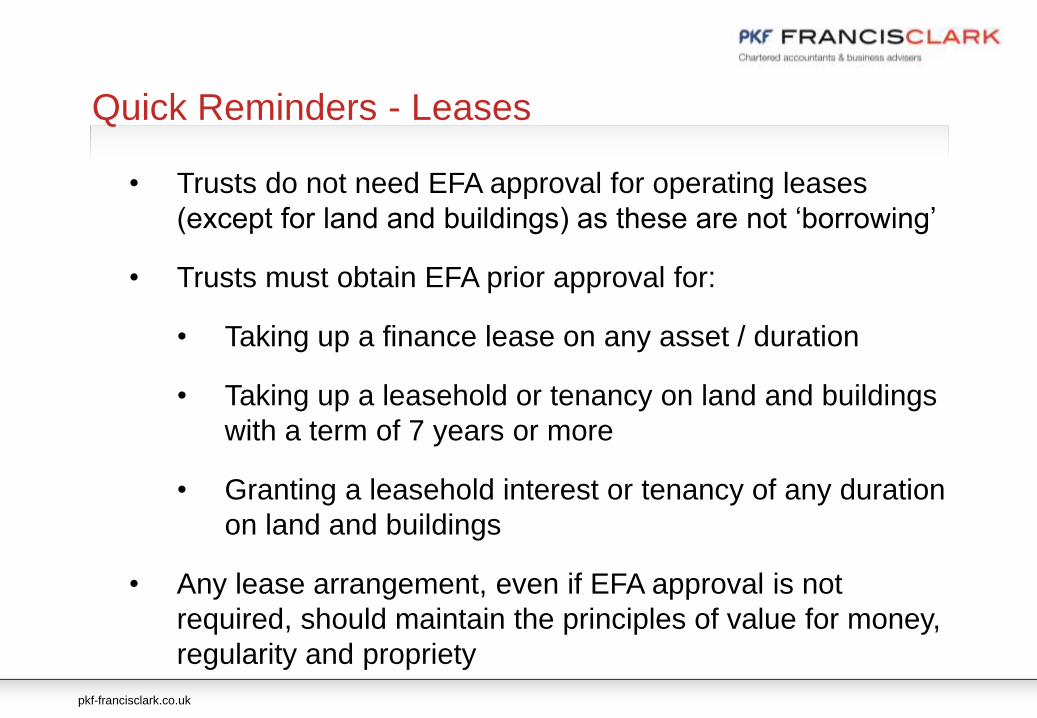

Quick Reminders - Leases

• Trusts do not need EFA approval for operating leases

(except for land and buildings) as these are not ‘borrowing’

• Trusts must obtain EFA prior approval for:

• Taking up a finance lease on any asset / duration

• Taking up a leasehold or tenancy on land and buildings

with a term of 7 years or more

• Granting a leasehold interest or tenancy of any duration

on land and buildings

• Any lease arrangement, even if EFA approval is not

required, should maintain the principles of value for money,

regularity and propriety

pkf-francisclark.co.uk

.

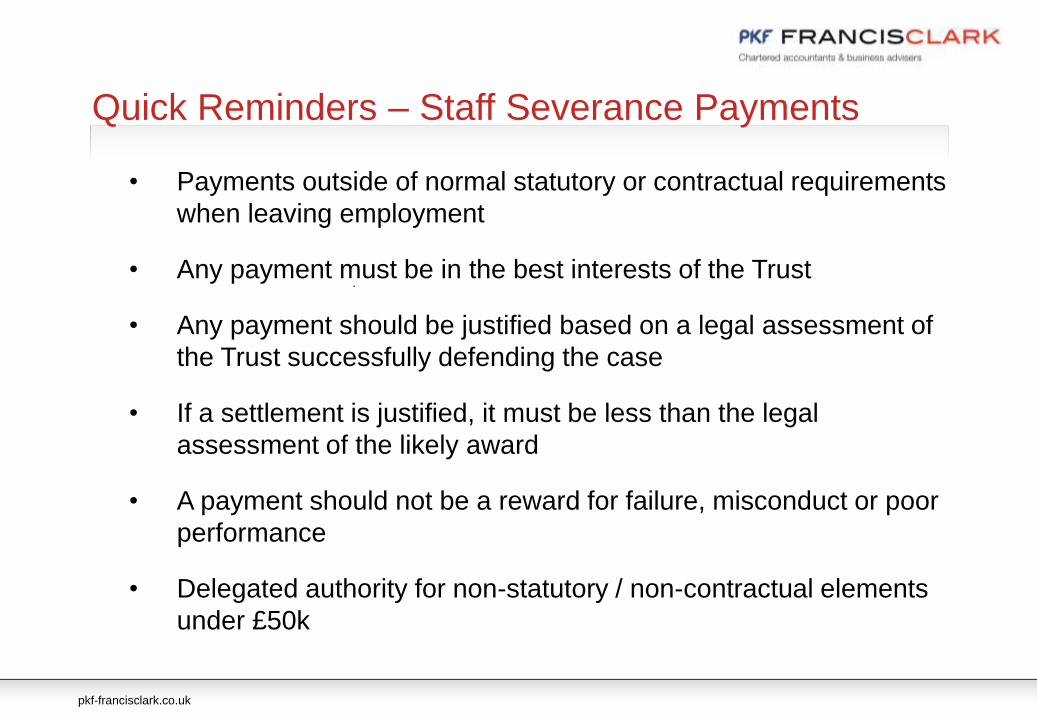

Quick Reminders – Staff Severance Payments

• Payments outside of normal statutory or contractual requirements

when leaving employment

• Any payment must be in the best interests of the Trust

• Any payment should be justified based on a legal assessment of

the Trust successfully defending the case

• If a settlement is justified, it must be less than the legal

assessment of the likely award

• A payment should not be a reward for failure, misconduct or poor

performance

• Delegated authority for non-statutory / non-contractual elements

under £50k

pkf-francisclark.co.uk

.

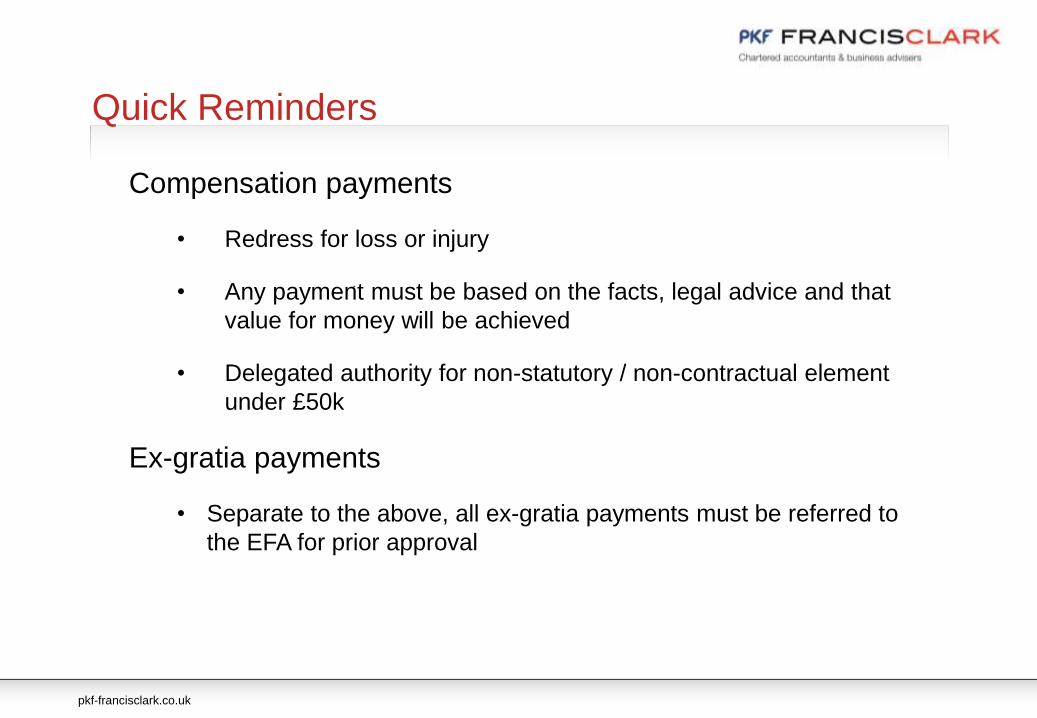

Quick Reminders

Compensation payments

• Redress for loss or injury

• Any payment must be based on the facts, legal advice and that

value for money will be achieved

• Delegated authority for non-statutory / non-contractual element

under £50k

Ex-gratia payments

• Separate to the above, all ex-gratia payments must be referred to

the EFA for prior approval

pkf-francisclark.co.uk

.

Academies Financial Handbook

• Updated annually

• The 2015 version applies to accounting periods from 1

September 2015

https://www.gov.uk/government/publications/academies-

financial-handbook-2015

• 2016 version just published (on 1 July - published 22 July

last year), and applies wef 1 September 2016. Only minimal

changes

pkf-francisclark.co.uk

.

Academies Financial Handbook

• Little change, but note:

• Board of Trustees (at all levels – so LGB’s as well) to review/identify/action the range of skills and

experience it needs. See Governance Handbook for training materials;

• In line with the Governance Handbook, the school must publish on its website its governance

arrangements (including details of the Scheme of Delegation if a MAT);

• All Trusts must have either their Principal or Chief Exec as Accounting Officer, and the role of AO must

not rotate;

• All Trusts must publish the relevant business and pecuniary interests of their AO regardless of them

being a Trustee, and also local governors (so those on LGBs) are now included in identifying relevant

interests from close family relationships;

• Schools must notify the DfE of the appointment/resignation of members, trustees, accounting officers,

chief financial officers, chairs of trustees/local governing bodies and local governors (as before) but now

must be via the Edubase, and must be notified within 14 days of the change

• The AFH2016 expressly states that variances between budget and actual income/expenditure must be

understood and addressed

pkf-francisclark.co.uk

.

Academies Financial Handbook

• Little change, but note (cont.):

• AFH2016 emphasises that exposure to investment products must be tightly

controlled and the Board has an investment policy in place – security of funds

is more important than maximising revenue!;

• Trusts are now required to have a whistleblowing procedure in place;

• Trusts must implement reasonable risk management audit recommendations

provided by their risk auditors;

• In a MAT, the audit committee’s oversight must extend to the financial

controls and risks at constituent academies;

• Oversight must include the submission of information to the DfE/EFA such as

pupil number returns and funding claims.

• So a more settled scene. But suggest read Annex B: “Schedule of

freedoms and delegations” and Annex C: “The Musts”. Otherwise,

are you demonstrating strong governance and financial

management?

pkf-francisclark.co.uk

Coffee Break

Multi Academy Trusts – some thoughts…

Laura Waycott

pkf-francisclark.co.uk

Background

• As at September 2015, about 15% of primaries and more than 60% of secondaries were academies

• There were 391 MATs in March 2011 – rose to 846 by July 2015. And of these, the number of MATs with 2-5 academies rose from 224 to 517.

• Government Agenda is clear! All schools to become Academies by 2022….?

• Local Authorities struggling to provide level of support and challenge previously offered – so how do schools get this support? And budgets are being squeezed. Particularly difficult for small Primaries.

• So Multi Academy Trusts (“MATs”) might be an answer?

Multi Academy Trusts

pkf-francisclark.co.uk

What is a Multi Academy Trust (“MAT”)?

• A group of schools governed through a single set of members

and directors

• One master funding agreement with the EFA – but a

supplemental funding agreement for each school

• One legal entity, with one Mem & Arts

• One shared ethos and culture???

Multi Academy Trusts

pkf-francisclark.co.uk

.

Multi Academy Trusts

Potential benefits:

• Improve standards in feeder schools

• Shared resources/expertise

• Economies of scale

• Leadership succession planning

BUT planning and due diligence is key. It is a daunting

process!

pkf-francisclark.co.uk

.

Multi Academy Trusts

Conversion

• Various grants potentially available, e.g.

• £25k grant available per new Academy conversion

• Sponsor Capacity grant for eligible academy trust to set

up/expand/develop – typically £50k-£100k

• Primary Academy Chain Development grant for primaries looking to

set up a MAT – keeps coming and going….

• Average time to convert over a year! Key considerations:

• Structure/roles?

• Policies?

• Ethos and culture?

pkf-francisclark.co.uk

.

Multi Academy Trusts

Financial Management considerations on conversion

• What does the Finance function(s) look like? One set of Policies

and Procedures?

• Who keeps what records? Where? Who has what authority?

• Accounting software?

• Intra-school charging

• How many bank accounts?

pkf-francisclark.co.uk

.

Multi Academy Trusts

Financial Oversight and considerations

• What does financial governance look like? Director of Finance

(and Operations?)?

• Monthly/termly reporting process?

• How is the central function to be financed?

• Top-slicing or not?

• If so, what percentage? Flat-rate or not?

• GAG pooling? So GAG income can be applied across any

academy within the MAT. Rare……

pkf-francisclark.co.uk

.

Multi Academy Trusts

What do the accounts look like?

• One set of accounts per MAT

• Statement of funds

• Costs split by school

• Central services

• Governor remuneration

• Related party transactions and connected parties

• FRS17

pkf-francisclark.co.uk

.

Multi Academy Trusts

Year-end considerations

• Are charts of accounts consistent across all schools?

• “Consolidation”

• Intra-school transactions

• Supporting schedules

pkf-francisclark.co.uk

.

Multi Academy Trusts

Conclusions?

• Planning is key!

• Impact on governance at the school level – how much influence will

existing Trustees have? Do their intended roles within the MAT suit

their skill-set?

• Is there a clear ethos and philosophy shared by all?

• Clarify and challenge the proposed governance, structure, roles and

responsibilities under the MAT before joining. Consider especially

the impact on the Finance function. What does this look like under a

MAT?

• Appoint someone to drive and manage the conversion process!

VAT Update

Liam Dushynsky

VAT Update - Agenda

Registration Limits

Recharges

Common Supplies and Pitfalls

Sports Lettings

Apportionment

pkf-francisclark.co.uk

pkf-francisclark.co.uk

VAT – Registration Limits

• Changes from 1 April 2016

Registration £82k → £83k

De-registration £80k → £81k

• Applies to all business income

• Includes all schools within a MAT

• Also includes reverse charges

• Agents fees

• Software licences

• Overseas services

pkf-francisclark.co.uk

.

VAT – Recharges

Internal

Cost Centres e.g. photocopying, meals – Outside the scope

External

Recharge of time costs for staff – Admin and Teachers

Consultancy – Failing Schools

Catering

pkf-francisclark.co.uk

.

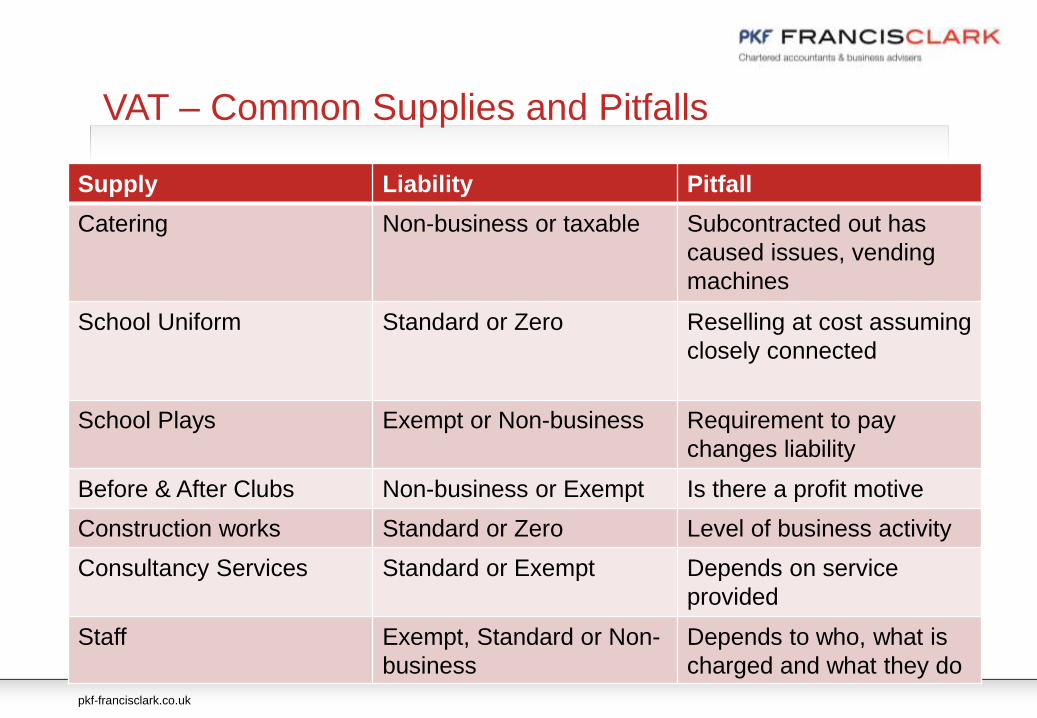

VAT – Common Supplies and Pitfalls

Supply Liability Pitfall

Catering Non-business or taxable Subcontracted out has

caused issues, vending

machines

School Uniform Standard or Zero Reselling at cost assuming

closely connected

School Plays Exempt or Non-business Requirement to pay

changes liability

Before & After Clubs Non-business or Exempt Is there a profit motive

Construction works Standard or Zero Level of business activity

Consultancy Services Standard or Exempt Depends on service

provided

Staff Exempt, Standard or Non-

business

Depends to who, what is

charged and what they do

pkf-francisclark.co.uk

.

VAT – Sports Lettings

Academy

School Use – Free – Non-Business

To public – Members / non-members – Exempt (unless OTT)

Trading Subsidiary

To public – Standard rated if one offs, Exempt if considered land

pkf-francisclark.co.uk

.

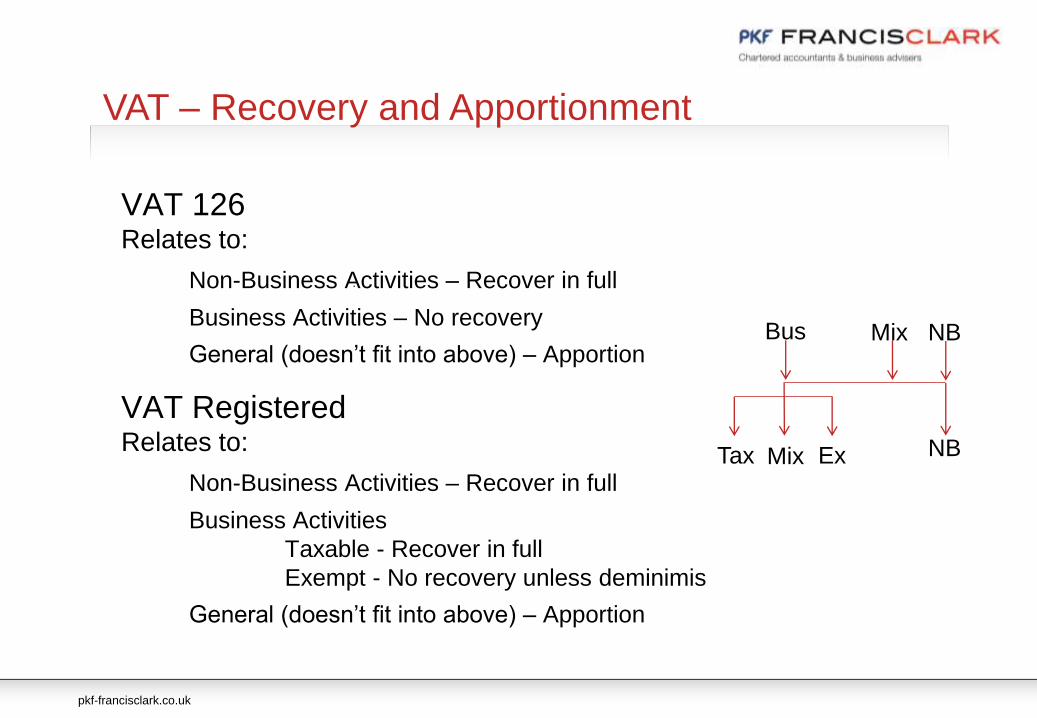

VAT – Recovery and Apportionment

VAT 126Relates to:

Non-Business Activities – Recover in full

Business Activities – No recovery

General (doesn’t fit into above) – Apportion

VAT RegisteredRelates to:

Non-Business Activities – Recover in full

Business Activities

Taxable - Recover in full

Exempt - No recovery unless deminimis

General (doesn’t fit into above) – Apportion

Bus Mix NB

NBTax Mix Ex

Topical Tax Issues

Martin Lock

Topical Tax Issues

Employment status of supply teachers and other

staff

• A matter of fact – not a question of choice!

• Teachers supplied via LA and those located through

school’s own contacts likely to be employees – with all that

entails…..

• Agency workers likely to be self-employed

• HMRC Manuals give guidance - see http://www.hmrc.gov.uk/manuals/esmmanual/esm4502.htm

• Some cases are very obvious – but many are not! Don’t

just look at the contract – look at the substance behind it.

Do actual arrangements mirror the contract?

pkf-francisclark.co.uk

pkf-francisclark.co.uk

.

Topical Tax Issues

Do I need a trading subsidiary?

• If income from trading activities more than £50k per annum,

school is liable to corporation tax

• Does not apply to “primary purpose” or “ancillary” trading

• If you are caught, then a trading subsidiary might be the answer?

• Also consider commercial risk, VAT, and practicalities of a

subsidiary – don’t let the tax tail wag the dog!

pkf-francisclark.co.uk

.

Topical Tax Issues

Income from lettings – is it taxable?

• Rental income usually exempt if profits applied for charitable

purposes

• But when does letting of a premises become a trade?

• Let on a regular basis?

• Provide additional services e.g. conference facilities, IT

equipment, support staff, catering, etc?

• Often hard to determine whether trading – each case will depend

on facts

pkf-francisclark.co.uk

.

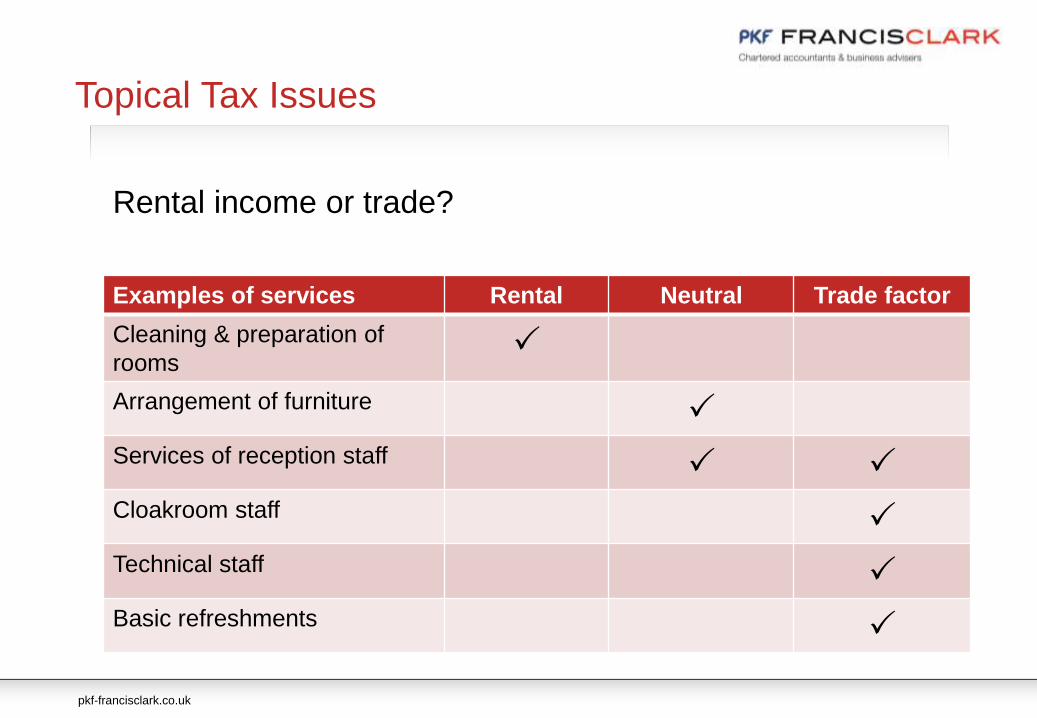

Rental income or trade?

Examples of services Rental Neutral Trade factor

Cleaning & preparation of

roomsP

Arrangement of furnitureP

Services of reception staffP P

Cloakroom staffP

Technical staffP

Basic refreshmentsP

Topical Tax Issues

pkf-francisclark.co.uk

.

Topical Tax Issues

Fundraising exemption – applies for tax and VAT

• Exempt for tax and VAT for one-off events such as Summer

Fairs, ticketed theatre performances and car boot sales

• Applies to income received – including associated sponsorship

• BUT must not be more than 15 of the same type of event in the

same location in a financial year and event must be promoted as

a fund-raiser for the school

pkf-francisclark.co.uk

.

New model Gift Aid declaration wef 6 April 2016

• Applies for both single and multiple donations

• Now must include ‘tax to cover’ statement:

“I am a UK taxpayer and understand that if I pay less Income Tax

and/or Capital Gains Tax in the current tax year than the amount

of Gift Aid claimed on all my donations it is my responsibility to

pay any difference.”

• Model forms at: https://www.gov.uk/guidance/gift-aid-

declarations-claiming-tax-back-on-donations#declaration-formats

Topical Tax Issues

Q&A

(c) copyright PKF Francis Clark, 2016

You shall not copy, make available, retransmit, reproduce, sell, disseminate, separate, licence, distribute, store electronically, publish, broadcast or otherwise

circulate either within your business or for public or commercial purposes any of (or any part of) these materials and / or any services provided by PKF Francis

Clark in any format whatsoever unless you have obtained prior written consent from PKF Francis Clark to do so and entered into a licence.

To the maximum extent permitted by applicable law PKF Francis Clark excludes all representations, warranties and conditions (including, without limitation,

the conditions implied by law) in respect of these materials and /or any services provided by PKF Francis Clark.

These materials and /or any services provided by PKF Francis Clark are designed solely for the benefit of delegates of PKF Francis Clark.

The content of these materials and / or any services provided by PKF Francis Clark does not constitute advice and whilst PKF Francis Clark endeavours to

ensure that the materials and / or any services provided by PKF Francis Clark are correct, we do not warrant the completeness or accuracy of the materials

and /or any services provided by PKF Francis Clark; nor do we commit to ensuring that these materials and / or any services provided by PKF Francis Clark

are up-to-date or error or omission-free.

Where indicated, these materials are subject to Crown copyright protection. Re-use of any such Crown copyright-protected material is subject to current law

and related regulations on the re-use of Crown copyright extracts in England and Wales.

These materials and / or any services provided by PKF Francis Clark are subject to our terms and conditions of business as amended from time to time, a

copy of which is available on request.

Our liability is limited and to the maximum extent permitted under applicable law PKF Francis Clark will not be liable for any direct, indirect or consequential

loss or damage arising in connection with these materials and / or any services provided by PKF Francis Clark, whether arising in tort, contract, or otherwise,

including, without limitation, any loss of profit, contracts, business, goodwill, data, income or revenue. Please note however, that our liability for fraud, for

death or personal injury caused by our negligence, or for any other liability is not excluded or limited.

PKF Francis Clark is a trading name of Francis Clark LLP. Francis Clark LLP is a limited liability partnership, registered in England and Wales with registered

number OC349116. The registered office is Sigma House, Oak View Close, Edginswell Park, Torquay TQ2 7FF where a list of members is available for

inspection and at www.pkf-francisclark.co.uk. The term ‘Partner’ is used to refer to a member of Francis Clark LLP or to an employee. Registered to carry on

audit work in the UK and Ireland, regulated for a range of investment business activities and licensed to carry out reserved legal activity of non-contentious

probate in England and Wales by the Institute of Chartered Accountants in England and Wales. Partners acting as insolvency practitioners are licensed in the

UK by the Institute of Chartered Accountants in England and Wales. A partner appointed as Administrator or Administrative Receiver acts only as agent of the

insolvent entity and without personal liability. Francis Clark LLP is a member firm of the PKF International Limited network of legally independent firms and

does not accept responsibility or liability for the actions or inactions on the part of any other individual member firm or firms.

Disclaimer & copyright

pkf-francisclark.co.uk