TARGET’S STATEMENT For personal use only · 2013. 11. 15. · Letter from the Chairman Dear...

92

EMERALD OIL & GAS NL ACN 009 795 046 TARGET’S STATEMENT IN RELATION TO THE PROPORTIONAL TAKEOVER OFFER BY CONFEDERATE CAPITAL PTY LTD FOR 30% OF THE SHARES IN EMERALD OIL AND GAS NL FOR 1.4 CENTS PER EMERALD SHARE YOUR INDEPENDENT DIRECTORS’ RECOMMEND THAT YOU DO NOT ACCEPT THE OFFER AND THEIR REASONS FOR THIS RECOMMENDATION ARE SET OUT IN SECTION 1.2 OF THIS TARGET’S STATEMENT THE INDEPENDENT EXPERT ENGAGED BY EMERALD HAS DETERMINED A PREFERRED VALUE OF 1.62 CENTS PER EMERALD SHARE AND CONCLUDED THAT THE OFFER IS NOT FAIR AND NOT REASONABLE THIS IS AN IMPORTANT DOCUMENT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in doubt as to how to deal with this document, you should consult your legal, financial or other professional adviser as soon as possible Jeremy Shervington Barrister & Solicitor 52 Ord Street WEST PERTH WA 6005 Telephone : (08) 9481 8760 Facsimile : (08) 9481 5142 Solicitors for Emerald Oil & Gas NL For personal use only

Transcript of TARGET’S STATEMENT For personal use only · 2013. 11. 15. · Letter from the Chairman Dear...

EMERALD OIL & GAS NL

ACN 009 795 046

TARGET’S STATEMENT

IN RELATION TO THE PROPORTIONAL TAKEOVER OFFER BY CONFEDERATE

CAPITAL PTY LTD FOR 30% OF THE SHARES IN EMERALD OIL AND GAS NL FOR

1.4 CENTS PER EMERALD SHARE

YOUR INDEPENDENT DIRECTORS’ RECOMMEND THAT YOU DO NOT ACCEPT

THE OFFER AND THEIR REASONS FOR THIS RECOMMENDATION ARE SET OUT

IN SECTION 1.2 OF THIS TARGET’S STATEMENT

THE INDEPENDENT EXPERT ENGAGED BY EMERALD HAS DETERMINED A

PREFERRED VALUE OF 1.62 CENTS PER EMERALD SHARE AND CONCLUDED

THAT THE OFFER IS NOT FAIR AND NOT REASONABLE

THIS IS AN IMPORTANT DOCUMENT AND REQUIRES YOUR IMMEDIATE ATTENTION

If you are in doubt as to how to deal with this document, you should consult your legal, financial or

other professional adviser as soon as possible

Jeremy Shervington Barrister & Solicitor 52 Ord Street WEST PERTH WA 6005 Telephone : (08) 9481 8760 Facsimile : (08) 9481 5142 Solicitors for Emerald Oil & Gas NL

For

per

sona

l use

onl

y

i

Table of contents

Important Notices ii

Corporate Directory iii

Letter from the Chairman iv

What should you do? v

Advantages associated with accepting the Offer vi

Disadvantages associated with accepting the Offer vii

Frequently asked questions about the Offer viii

1 Directors’ recommendations 1

2 Key Terms of the Offer 3

3 Profile of Emerald 8

4 Profile of Confederate 16

5 Your choices as an Emerald Shareholder 19

6 Tax considerations 21

7 Directors’ interests 23

8 Additional information 25

9 Approval of Target’s Statement 27

10 Definitions and interpretation 28

Annexure 1 Independent Expert’s Report

Annexure 2 Emerald announcements to ASX since 1 November 2012

For

per

sona

l use

onl

y

ii

Important Notices

This document is a Target’s Statement issued by Emerald under part 6.5 division 3 of the Corporations Act in

response to the Bidder’s Statement issued by Confederate. This Target’s Statement is dated 15 November

2013.

A copy of this Target’s Statement was lodged with ASIC and sent to ASX on 15 November 2013. None of ASIC,

ASX nor any of their officers take any responsibility for the content of this Target’s Statement.

This Target’s Statement and the Bidder’s Statement contain important information. You should read these

documents carefully and in their entirety.

Investment decision

This Target’s Statement does not take into consideration your individual investment objectives, financial

situation or particular needs. You may wish to seek independent financial and taxation advice before deciding

whether or not to accept the Offer by Confederate to acquire 30% of your Emerald Shares.

Shareholder information

If you have any questions in relation to the Offer, please call Emerald’s company secretary, Mr Graeme Smith,

on (+61 8) 9389 2111 on weekdays between 9.00am and 5.00pm (WST).

The Directors are committed to ensuring Emerald Shareholders are kept informed of developments.

Important developments under the control of Emerald will be notified to Emerald Shareholders.

Forward looking statements

This Target’s Statement contains forward looking statements and statements of current intentions. The

forward looking statements in this Target’s Statement reflect views held at the date of this Target’s Statement.

You should be aware that such statements involve inherent risks and uncertainties. Actual events or results

may differ materially from the events or results expressed or implied in any forward looking statement and

those deviations are both normal and to be expected.

None of Emerald, its officers or any person named in this Target’s Statement with their consent or involved in

the preparation of this Target’s Statement makes any representation or warranty as to the accuracy or

likelihood or fulfilment of any forward looking statement. You should not place undue reliance on those

statements.

Defined terms

A number of defined terms are used in this Target’s Statement. These terms are explained in the definitions in

section 10.1.

Privacy statement

Emerald has collected your information from the register of Emerald Shareholders. The Corporations Act

permits that information to be made available to certain persons, including Confederate. Your information

may also be disclosed on a confidential basis to Emerald’s related bodies corporate and external service

providers and may be required to be disclosed to regulatory bodies such as ASIC. You can contact us for

details of information held by us about you.

For

per

sona

l use

onl

y

iii

Corporate Directory

Directors:

Registered & Principal Office:

Jeremy Shervington – Non-Executive Chairman Ross Williams – Non-Executive Director

Ground Floor 20 Kings Park Road

Tim Kestell - Non-Executive Director Peter Pynes - Non-Executive Director

WEST PERTH, WA, 6005 Telephone: +61 8 9389 2111 Facsimile: +61 8 9389 2199

Company Secretary: Graeme Smith

Postal Address: P.O. Box 902 WEST PERTH, WA, 6872

Auditors: Home Securities Exchange:

HLB Mann Judd ASX Ltd Level 4, 130 Stirling Street PERTH, WA, 6000

Exchange Plaza 2 The Esplanade

PERTH, WA, 6000 Solicitors:

ASX Code – EMR

Jeremy Shervington 52 Ord Street Share Registry: WEST PERTH, WA, 6005 Security Transfer Registrars Pty Ltd PO Box 535 APPLECROSS, WA, 6953 Telephone +618 9315 2333

For

per

sona

l use

onl

y

iv

Letter from the Chairman

Dear Shareholder,

This letter forms part of a Target’s Statement in response to a Bidder’s Statement lodged by Confederate

Capital Pty Ltd whereby Confederate Capital is offering 1.4 cents in cash for 30% of the Emerald Shares held by

each Emerald Shareholder.

Please read the contents of this Target’s Statement and the Bidder’s Statement carefully.

You will see that the Independent Directors being Ross Williams and I each recommend as follows in relation

to how you should deal with the Offer in respect of your Emerald Shares. A full statement of our

recommendations and the reasons for them are set out in section 1.2.

Jeremy Shervington and Ross Williams each recommend that YOU DO NOT ACCEPT THE OFFER. However, if

you have a particular need or desire to liquidate part of your investment in Emerald, the Offer provides you

with a liquidity event for that purpose in respect of 30% of your Emerald Shares. However, in the absence of

such a need or desire it is noted that the value underlying each Emerald Share as attributed by the

Independent Expert is greater than the 1.4 cents offered under the Offer and that this combined with potential

future value through future transactions/investments by Emerald may lead to a higher share price being

attainable in the medium to longer term.

Mr Shervington DOES NOT INTEND TO ACCEPT THE OFFER in relation to the Emerald Shares he controls (being

8,311,915 Emerald Shares).

Mr Williams does not hold or control any Emerald Shares.

Yours faithfully,

_______________________

Jeremy Shervington

For

per

sona

l use

onl

y

v

What should you do?

You should read the Bidder’s Statement and this Target’s Statement, which contains your Independent

Directors’ recommendations as to how to deal with the Offer in the absence of a superior proposal, and their

reasons for their recommendations in section 1.2.

As an Emerald Shareholder, you have the following choices in respect of the Offer:

(a) You may ACCEPT the Offer, in which case you should complete the acceptance form in the Bidder’s

Statement and return it in accordance with the instructions on the acceptance form.

(b) You may choose to REJECT the Offer, in which case you do not need to take any action.

(c) You may sell you Emerald Shares on market, unless you have previously accepted the Offer and you have

not validly withdrawn your acceptance.

If you have any questions in relation to the Offer, please call Emerald’s company secretary, Mr Graeme Smith,

on (+61 8) 9389 2111 on weekdays between 9.00am and 5.00pm (WST).

Key Dates

Bidder’s Statement lodged with ASIC 11 October 2013

Supplementary Bidder’s Statement lodged with ASIC

29 October 2013

Date of Offer 29 October 2013

Notice Freeing Offer from Defeating Conditions 5 November 2013

Date of Target’s Statement 15 November 2013

Close of Offer Period (unless extended) 30 November 2013

For

per

sona

l use

onl

y

vi

Advantages associated with accepting the Offer

The following is a summary of the key advantages associated with accepting the Offer. These key advantages

are also set out in section 13.1 of the Independent Expert’s Report.

(a) Shareholders can dispose part of their investment in Emerald with no transaction costs

The Offer is made to acquire 30% of the Emerald Shares held by each Emerald Shareholder for a cash price of

1.4 cents per Emerald Share. Emerald Shareholders will be able to dispose part of their investment in Emerald

with no brokerage costs or other associated selling costs for their Emerald Shares. The absence of the need to

incur transaction costs increases the cash received by Emerald Shareholders who accept the Offer.

(b) Shareholders can receive a higher price than what they can sell in the market

Based on BDO’s QMP analysis, the Offer allows Emerald Shareholders to receive a higher price, for 30% of their

Emerald Shares, than they are able to individually sell their Emerald Shares on the market.

(c) Shareholders will retain the opportunity to participate in the potential upside of Emerald

Emerald Shareholders will be able to obtain cash for a partial exit of their investment and still retain the

opportunity to participate in any potential upside of Emerald in respect of their remaining Emerald

Shareholding.

The Bidder’s Statement sets out the current intentions of Confederate upon it gaining effective control of

Emerald but where Confederate is not entitled to proceed to compulsory acquisition in accordance with Part

6A.1 of the Corporations Act.

The key intentions of Confederate are summarised as follows:

i. to appoint additional nominees to the Emerald Board, depending on the extent of success of the

Offer and to maintain Emerald’s listing on the ASX;

ii. to consider the potential disposal of the Emerald Oil Inc. shares held by Emerald but review and

continue current exploration programmes and budgets for Emerald’s Appalachian Project;

iii. to review Emerald’s operations on a strategic, operational and financial level to evaluate

Emerald’s performance and corporate direction; and

iv. to review potential cost savings by reducing staff numbers and/or consolidating back office work.

Depending on the outcome of the above reviews and the strategies concluded therefrom, the future business

of Emerald may not be a passive holding of a listed company’s shares, which currently constitutes Emerald’s

main asset. Any potential upside is likely to come from undertaking active operations in the oil and gas sector,

albeit that this will entail some risks. For

per

sona

l use

onl

y

vii

Disadvantages associated with accepting the Offer

The following is a summary of the key disadvantages associated with accepting the Offer. Some of these key

disadvantages are also set out in section 13.2 of the Independent Expert’s Report.

(a) Emerald Shareholders will have their Emerald Shareholding diluted

Shareholders will have their collective Emerald Shareholdings diluted from 80.01% to 56.01% if all Emerald Shareholders accept the Offer. Emerald Shareholders will be passing a substantial amount of control to Confederate and its associates, as a

result of an increase in Confederate and its associates’ shareholding from the current 19.99% up to 43.99%.

(b) Reduction in liquidity

If Emerald Shareholders accept the Offer, trading in Emerald Shares may be negatively affected by the

presence of a major Emerald Shareholder with approximately 44% ownership. The existing Emerald Shares will

therefore have a materially lower free float on a proportional basis which may reduce liquidity.

(c) Decreases the likelihood of a full takeover offer

If all Emerald Shareholders accept the Offer, Confederate and its associates will hold approximately 44% of the

issued capital of Emerald. This may discourage any other potential bidder from making a takeover bid in the

future as Confederate and its associates will have significant control over Emerald. This may have an adverse

effect on the Emerald Share price of Emerald and may reduce the opportunity for Emerald Shareholders to

receive a takeover premium in the future.

(d) Emerald Shareholders may be giving up the opportunity to realise the fair value of their Emerald Shares

through a better potential offer

Based on BDO’s QMP analysis, the Offer allows Emerald Shareholders to receive a higher price, for 30% of their shares, than they are able to individually sell their Emerald Shares on the market. Additionally, Emerald Shareholders would not incur transaction costs associated with selling those Emerald Shares. Whilst this may suggest that it would be logical for Emerald Shareholders to accept the Offer on this basis, Emerald Shareholders may be giving up the opportunity to receive a potentially better offer that could enable them to realise the higher net asset value for their Emerald Shares on a collective basis. As the Emerald Shares are trading at lower than its net asset value per Emerald Share, Emerald Shareholders are unable to realise the fair value of their Emerald Shares of their own accord by selling them individually on the market.

However, they may be able to achieve this on a collective basis if a potentially better offer or takeover bid is

received.

For

per

sona

l use

onl

y

viii

Frequently asked questions about the Offer

This section of the Target’s Statement is designed to help you understand the Offer by answering some

commonly asked questions. It is not intended to address all relevant issues for Emerald Shareholders. This

section should be read in conjunction with all other sections of this Target’s Statement.

Question Answer Further Information

Who is the bidder? The Offer is made by Confederate Capital Pty Ltd. Information about Confederate can be obtained from section 3 of the Bidder’s Statement or section 4 of this Target’s Statement.

Section 4

What is the Offer? Confederate has made an offer to acquire 30% of your Emerald Shares for 1.4 cents cash per Emerald Share. If you accept the Offer, you will: (a) receive 1.4 cents cash for each Emerald

Share comprising 30% of your Emerald Shareholding; and

(b) retain 70% of your Emerald Shares. You may only accept the Offer for 30% of the Emerald Shares held by you and not a lesser or greater amount unless by accepting the Offer, the 70% of your Emerald Shareholding that you retain has a market value of less than $500 based on the price of Emerald Shares on the day that your acceptance is received (or the most recent Business Day if your acceptance is not received on a Business Day), in which case the Offer will extend to 100% of your Emerald Shares. In this case (subject to the position described in the next two questions), Emerald Shareholders may elect to accept the Offer for either 30% or 100% of their Emerald Shares. Accepting Emerald Shareholders will only participate in 30% of any control premium pursuant to the Offer, and the balance of any Emerald Shares held after the Offer closes will not be able to be subsequently accepted into the Offer.

Section 2

What if I accept the Offer and I am left with an unmarketable parcel of Emerald Shares?

If you accept the Offer and the Emerald Shares you are left holding are worth less than $500, then the Offer will extend to all of your Emerald Shares (subject to the following question). In this case, Emerald Shareholders may elect to accept the Offer for either 30% or 100% of their Emerald Shares.

For

per

sona

l use

onl

y

ix

If you are unsure whether you would be left with a Emerald Shareholding that is worth less than $500, please contact your broker or financial adviser.

Can I create, or increase the size of, an unmarketable parcel of Emerald Shares after the Offer was publicly proposed so that all of my Emerald Shares can be acquired under the Offer?

NO. ASIC class order 13/521 modifies subsection 618(2) of the Corporations Act so that it does not apply to a parcel of Emerald Shares (whether held beneficially or otherwise) worth less than $500 that has come into existence, or increased in size, because of a transaction (including the creating of one of more trusts) after the date that the Offer was publicly proposed (that date being 1 October 2013).

Section 2.14

What is a ‘proportional’ takeover bid?

A proportional takeover bid (such as the Offer) is a takeover bid for a specified proportion of the securities in a class of securities. Under the Corporations Act, the specified proportion must be the same for all holders of securities in that class. The specified proportion for the Offer is 30% of the Emerald Shares held by you.

What choices do I have as an Emerald Shareholder?

As an Emerald Shareholder, you have the following choices: (a) you can accept the Offer in the absence

of a superior proposal;

(b) you can reject the Offer; or

(c) you can sell your Emerald Shares on market (unless you have previously accepted the Offer and have not validly withdrawn your acceptance).

When deciding what to do, you should carefully consider the Independent Directors’ recommendations and other important considerations set out in this Target’s Statement.

Section 5

What do your Independent Directors recommend?

Jeremy Shervington and Ross Williams both recommend (in summary) that you DO NOT ACCEPT THE OFFER. The Independent Directors’ full recommendations and reasons are set out in section 1.2.

Section 1.2

How do I accept the Offer? Details of how to accept the Offer are set out in section 2.7 of the Bidder’s Statement and section 5.1 of this Target’s Statement.

Section 5.1

For

per

sona

l use

onl

y

x

How do I reject the Offer? To reject the Offer, you do not need to do anything.

Section 5.3

Can Confederate vary the Offer? Yes, Confederate can vary the Offer by extending the Offer Period or increasing the Offer Price.

Section 2.12

When does the Offer close? The Offer will close at 5.00pm (WST) on 30 November 2013, unless it is extended or withdrawn.

Section 2.3

What happens if Confederate increases the consideration payable under the Offer?

If Confederate increases the consideration payable under the Offer, you will receive the higher consideration even if you have already accepted the Offer.

Section 2.12

What was the effect of the Notice Freeing Offer From Defeating Conditions?

Pursuant to the Notice Freeing Offer From Defeating Conditions, Confederate declared the Offer free of all Defeating Conditions, and the Offer is now unconditional.

Is the Offer conditional? No. The Offer is unconditional, pursuant to the Notice Freeing Offer From Defeating Conditions dated 5 November 2013, whereby Confederate declared that the Offers, and each contract formed pursuant to the acceptances of the Offer, are free from all Defeating Conditions.

Section 2.7

What are the consequences of accepting the Offer now?

If you accept the Offer, unless withdrawal rights are available, you will not be able to sell your Emerald Shares accepted under the Offer on the ASX or to any other bidder that may make a takeover offer, or otherwise deal with your Emerald Shares accepted under the Offer while the Offer remains open.

See section entitled “Disadvantages associated with accepting the Offer”

What if I want to sell my Emerald Shares on market?

During the Offer Period, you may sell your Emerald Shares on ASX, provided you have not accepted the Offer for those Emerald Shares. You should contact your Broker for information on how to sell your Emerald Shares on ASX and your tax adviser to determine your tax implications of such a sale. If you accept the Offer in respect of 30% of your Emerald Shares, you are not entitled to accept the Offer for your remaining Emerald Shares (“Remaining Shares”), nor can a transferee of your Remaining Shares. You may sell your Remaining Shares on a “ex-Offer” basis and a separate ASX code will be established for these ex-Offer Emerald Shares.

Section 5.2

For

per

sona

l use

onl

y

xi

Ex-Offer Emerald Shares cannot be accepted into the Offer and will trade separately to Emerald Shares which can be accepted into the Offer during the Offer Period. The market price of the ex-Offer Emerald Shares may be lower than the market price of the Emerald Shares which may be accepted into the Offer. Settlement of trades on ex-Offer Emerald Shares will be deferred until after completion of the Offer. If you do not accept the Offer in respect of 30% of your Emerald Shares, you may sell your Emerald Shares on market and the transferee will be entitled to accept the Offer in respect of 30% of the Emerald Shares.

If I accept the Offer, can I withdraw my acceptance?

Given that Confederate has provided Emerald with the Notice Freeing Offer From Defeating Conditions, and therefore, the Offer is unconditional, there is no right to withdraw an acceptance of the Offer.

Section 2.6

What happens if I do nothing? You will remain an Emerald Shareholder. However, as a result of the Offer, Confederate may obtain an Emerald Shareholding of approximately 43.99% increasing its ability to control Emerald, resulting in other Emerald Shareholders retaining only minority shareholdings. The maximum Emerald Shareholding that Confederate can acquire under the Offer (i.e. if all Emerald Shareholder accept the Offer) is approximately 30% of all Emerald Shares on issue.

See section entitled “Disadvantages associated with accepting the Offer” and section 5.3

Can I be forced to sell my Emerald Shares?

You cannot be forced to sell your Emerald Shares unless Confederate acquires a relevant interest of at least 90% of all Emerald Shares. Due to the proportional nature of the Offer, it will not be possible for Confederate to become entitled to proceed to compulsory acquisition of the remaining Emerald Shares under the Corporations Act as a result of the Offer.

When will I receive my consideration if I accept the Offer?

If you accept the Offer, you will receive your consideration by the earlier of: (a) one month after the later of:

i. the date you accept the Offer;

and

ii. the date the Offer becomes

Section 2.11

For

per

sona

l use

onl

y

xii

unconditional (which was 5 November 2013) ; and

(b) 21 days after the end of the Offer Period provided that the Offer has become unconditional (which it did on 5 November 2013).

What are the tax implications of accepting the Offer?

A general outline of the tax implications of accepting the Offer is set out in section 8 of the Bidder’s Statement and also in section 6 of this Target’s Statement. You should consult your financial or taxation adviser for advice on the taxation implications applicable to your financial circumstances.

Section 6

Why have the Directors obtained an independent expert’s report?

Confederate and Emerald have two common directors (namely Tim Kestell and Peter Pynes) and as such, pursuant to section 640 of the Corporations Act, this Target’s Statement must be accompanied by an expert’s report that states whether the Offer is fair and reasonable and gives reasons for forming that opinion. BDO have formed the opinion that the Offer is NOT FAIR and NOT REASONABLE and their reasons for forming this opinion are set out in the Expert’s Report attached as Annexure 1.

What if I have questions about the Offer?

If you have any questions in relation to the Offer, please call Emerald’s company secretary, Mr Graeme Smith, on (+61 8) 9389 2111 on weekdays between 9.00am and 5.00pm (WST). Announcements made to the ASX by Emerald and other information relating to the Offer can be obtained from Emerald’s website (www.emeraldoilandgas.com) and the ASX’s website (www.asx.com.au).

For

per

sona

l use

onl

y

1

1. Directors’ recommendations

1.1. Summary of the Offer

Confederate is offering to acquire 30% of your Emerald Shares for 1.4 cents for each Emerald Share acquired

by Confederate under the Offer. The Offer, as from 5 November 2013, pursuant to the Notice Freeing Offer

From Defeating Conditions became unconditional.

1.2. Directors’ recommendations

After taking into account the terms of the Offer, and the matters in this Target’s Statement, the

recommendations of Emerald’s Independent Directors, Jeremy Shervington and Ross Williams, in relation to

the Offer are set out below:

Mr Shervington and Mr Williams both recommend that you DO NOT ACCEPT THE OFFER. However, Mr

Shervington and Mr Williams both note that if you have a need or desire to liquidate part of your investment

in Emerald then the Offer provides a liquidity event that will enable you to do so in respect of 30% of your

Emerald Shares, perhaps more readily and with more certainty than by selling those shares on market. Apart

from that consideration, Mr Shervington and Mr Williams note that the Independent Expert has ascribed a

preferred value of 1.62 cents for each Emerald Share and on the basis of that conclusion they both

recommend that you DO NOT ACCEPT THE OFFER. However it should be noted that there is a risk that shares

in Emerald will trade at below 1.4 cents.

Mr Williams also notes that he was suggested as a Director by Peter Pynes and Tim Kestell (the directors of

Confederate), but is nonetheless an Independent Director.

As outlined elsewhere in this Target’s Statement:

Mr Tim Kestell is a non-executive director of Emerald and a director of Confederate; and

Mr Peter Pynes is a non-executive director of Emerald and a director of Confederate.

Both Mr Kestell and Mr Pynes have refrained from making a recommendation in relation to the Offer due to

their interests as directors of Confederate, and their controlled entities’ (Desertfox and P & L respectively)

shareholdings in Confederate.

1.3. Directors’ acceptance of the Offer

At the date of this Target’s Statement, none of the Directors have accepted the Offer for the relevant portion

of Emerald Shares held or controlled by them.

Details of the relevant interests of each Director in Emerald Shares are set out in section 7.1.

1.4. Directors’ intentions

As at the date of this Target’s Statement, the Directors’ intentions in relation to the Offer for the Emerald

Shares held or controlled by them are as follows:

For

per

sona

l use

onl

y

2

Jeremy Shervington:

Mr Shervington DOES NOT intend to accept the Offer in relation to the Emerald Shares he controls (being

8,311,915 Emerald Shares).

Ross Williams:

At the date of this Target’s Statement Mr Williams does not hold or control any Emerald Shares.

Tim Kestell:

At the date of this Target’s Statement, Mr Kestell’s interest in Emerald Shares (other than those Emerald

Shares which have been accepted into the Offer at the date of this Target’s Statement) is held via Desertfox

which is an associate of Confederate, and as such, will not be accepted into the Offer.

Peter Pynes:

At the date of this Target’s Statement, Mr Pynes’ interest in Emerald Shares (other than those Emerald Shares

which have been accepted into the Offer at the date of this Target’s Statement) is held via P & L which is an

associate of Confederate, and as such, will not be accepted into the Offer.

For

per

sona

l use

onl

y

3

2. Key terms of the Offer

2.1. Background

On 1 October 2013, it was announced that Confederate intended to make an off-market proportional takeover

bid for 30% of the issued Emerald Shares. On 11 October 2013, Confederate lodged its Bidder’s Statement

with ASIC and gave a copy to Emerald. On 29 October 2013, Confederate lodged its Supplementary Bidder’s

Statement with ASIC and gave a copy to Emerald. On 5 November 2013, Confederate lodged the Notice

Freeing Takeover Offer From Defeating Conditions with ASIC and gave a copy to Emerald.

The Bidder’s Statement contains the Offer.

2.2. Summary of the Offer

The Offer is a proportional offer whereby Confederate has made offers to purchase a percentage of each

Emerald Shareholding.

The Offer is to acquire 30% of your Emerald Shares and any rights attaching to those Emerald Shares for 1.4

cents cash per Share.

This means if you accept the Offer, you will retain 70% of your Emerald Shares and receive 1.4 cents cash per

Share for the 30% of your Emerald Shares accepted into the Offer. The Offer extends to all Emerald Shares on

issue on or before the end of the Offer Period, other than those Emerald Shares already held by Confederate

and its associates.

2.3. Offer Period

The Offer will remain open for acceptance until 5.00pm (WST), 30 November 2013, unless extended or

withdrawn in accordance with the Corporations Act.

Confederate may extend the Offer Period before the end of the Offer Period in accordance with the

Corporations Act. To extend the Offer Period, Confederate must lodge a notice of variation with ASIC and give

notice to Emerald and each Emerald Shareholder to whom an offer was made under the Offer.

In addition, there will be an automatic extension of the Offer Period if, within the last 7 days of the Offer

Period:

(a) Confederate improves the consideration under the Offer; or

(b) Confederate’s voting power in Emerald Shares increases to more than 50%.

If either of these events occurs, the Offer Period is automatically extended so that it ends 14 days after the

relevant event occurs.

For

per

sona

l use

onl

y

4

2.4. Withdrawal of the Offer

Confederate may not withdraw its Offer if you have already accepted it. Before you accept the Offer,

Confederate may withdraw its Offer with the written consent of ASIC and subject to the conditions (if any)

specified in that consent.

2.5. Effect of acceptances

If you accept the Offer, you will give up your right to sell 30% of your Emerald Shares that you have accepted

into the Offer on ASX or to any competing bidder or to deal with them in any other manner. The agreement

that results from acceptance of the Offer is set out in detail in section 7 of the Annexure to the Bidder’s

Statement. Section 7 of the Annexure to the Bidder’s Statement describes the rights attached to your Emerald

Shares that you will be giving up, the representations and warranties that you will be making and the

irrevocable authorities and appointments that you will be giving Confederate if you accept the Offer. Please

note that the Directors do not take any responsibility for the contents of the Bidder’s Statement and are not

endorsing any of the statements contained in it.

The remaining 70% of your Emerald Shares that are not able to be accepted into the Offer can be dealt with in

any manner. However, if you sell these Emerald Shares, they will trade on ASX on an ‘ex-Offer’ basis, meaning

that purchasers of those Emerald Shares will not be entitled to accept the Offer and settlement of these

Emerald Shares will be deferred until the end of the Offer Period.

2.6. No right to withdraw your acceptance

Given that, pursuant to the Notice Freeing Takeover Offer From Defeating Conditions, the Offer became

unconditional, if you accept the Offer, there will be not right to withdraw your acceptance of the Offer if you

do accept.

2.7. Unconditional Offer – Notice Freeing Takeover Offer From Defeating Conditions

The Offer was subject to those Defeating Conditions set out in full in section 6.1 of the Annexure to the

Bidder’s Statement, which are summarised below:

(a) a majority of the Emerald Board being made up of Confederate Nominees;

(b) Emerald not proceeding with an alternative proposal from a third party;

(c) there is no Prescribed Occurrence;

(d) there is no Material Adverse Change; and

(e) no change to the capital structure of Emerald and its subsidiaries.

Confederate, pursuant to the Notice Freeing Takeover Offer From Defeating Conditions, waived all of these

Defeating Conditions under the Corporations Act, thereby making the Offer unconditional.

2.8. Notice of Status of Conditions

The Bidder’s Statement states that Confederate will give its Notice of Status of Conditions to ASX and Emerald

as required by section 630(1) of the Corporations Act (being not more than 14 days and not less than 7 days

For

per

sona

l use

onl

y

5

before the end of the Offer Period). If the offer Period is extended by a period before the time by which

Notice of Status of Conditions is to be given, the date for giving the Notice of Status of Conditions will be taken

to be postponed for the same period. If there is such an extension, Confederate is required, as soon as

possible after the extension, to give notice to ASX and Emerald that states the new date for giving of the

Notice of Status of Conditions.

Confederate is required to set out in its Notice of Status of Conditions:

(a) whether the Offer is free of any or all Defeating Conditions;

(b) whether, so far as Confederate knows, and of the Defeating Conditions have been fulfilled; and

(c) Confederate’s voting power in Emerald.

Given that, pursuant to the Notice Freeing Takeover Offer From Defeating Conditions, the Offer became

unconditional, the only new information that will be provided in the Notice of Status of Conditions will be

Confederate’s voting power in Emerald.

2.9. Sources of Consideration for the Offer

As set out in Section 6 of the Bidder’s Statement, the consideration for the acquisition of the Emerald Shares

to which the Offer relates will be satisfied wholly in cash.

The maximum amount of cash that Confederate would be required to pay under the Offer if acceptances are

received in respect of all Emerald Shares on issue at the date of this Target’s Statement (other than those

Emerald Shares held by Confederate and its associates) would be approximately $3,171,215.48.

Confederate does not currently have existing cash reserves available to pay the consideration under the Offer.

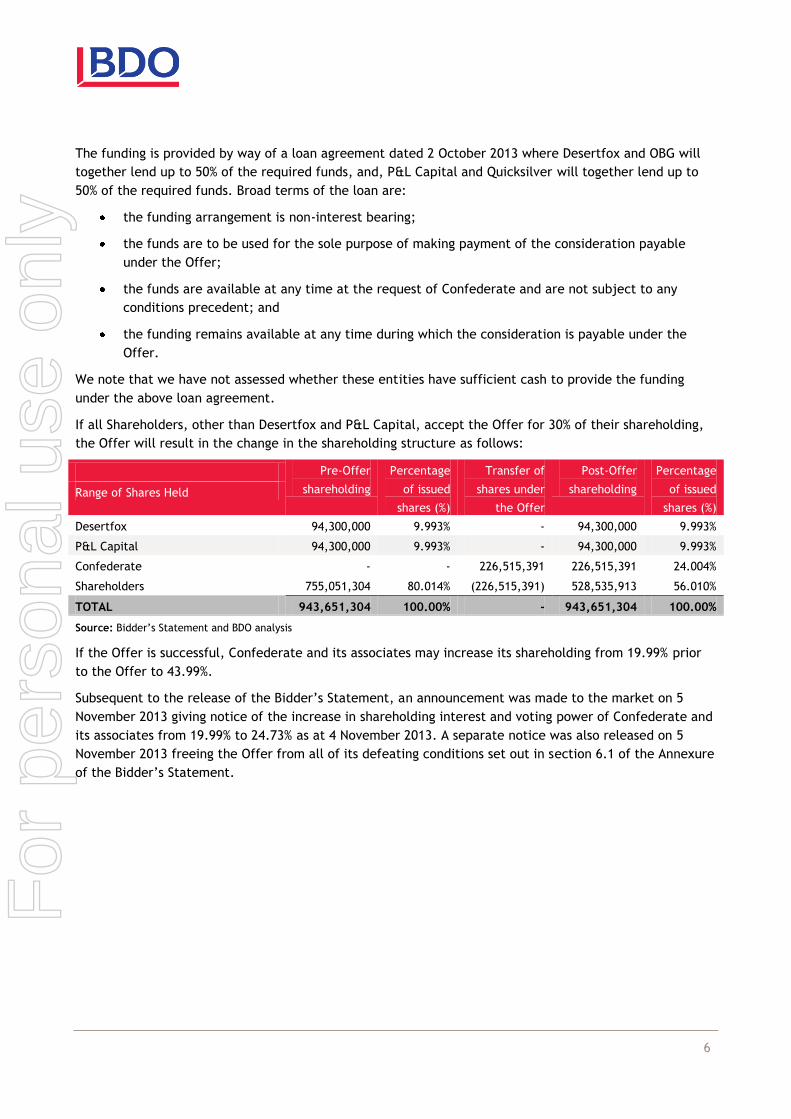

Confederate will fund the cash payable under the Offer using cash provided by the following entities:

(a) Desertfox – an entity controlled by Mr Tim Kestell (a director of both Emerald and Confederate);

(b) OBG – an entity controlled by Mr Tim Kestell (a director of both Emerald and Confederate);

(c) P & L – an entity controlled by Mr Peter Pynes (a director of both Emerald and Confederate) and his wife,

Lara Pynes; and

(d) Quicksilver – an entity controlled by Lara Pynes,

(together the Lenders) pursuant to a loan agreement dated 2 October 2013 (Loan Agreement).

Pursuant to the Loan Agreement, the Lenders have irrevocably and unconditionally agreed to advance to

Confederate such amounts as are required to satisfy Confederate’s obligations under the Offer, together with

amounts required to cover all transaction costs associated with the Offer, on the following terms:

(a) the funding arrangement is non-interest bearing;

(b) the funds may be used for the sole purpose of making payment of the consideration payable under the

Offer;

For

per

sona

l use

onl

y

6

(c) the funds are available at any time and the right to request an advance is not subject to any conditions

precedent; and

(d) the funding remains available at any time during which consideration is payable under the Offer.

Under the terms of the Loan Agreement, the proportions of funding the Offer between the Lenders has been

agreed to be as follows:

(a) Desertfox and OBG together will lend up to 50% of the required funds in such proportions between them

as Desertfox determines; and

(b) P & L and Quicksilver together will lend up to 50% of the required funds in such proportions between

them as P & L determines.

The events of default under the Loan Agreement are Confederate failing to use funds advanced for the

purpose of making payment of consideration under the Offer, Confederate becoming insolvent or Confederate

failing to repay any amounts to the Lenders when they are due and payable.

In the event that an event of default occurs under the Loan Agreement, a Lender may issue a default notice to Confederate and Confederate shall have a period of 7 days to remedy the default. If Confederate fails to remedy the default, the Lenders may seek to terminate the Loan Agreement, in which case, Confederate must repay the moneys owing under the Loan Agreement within 12 months of termination. The Offer is not subject to any financing conditions.

Emerald makes no representation whatsoever in relation to Confederate’s ability (whether pursuant to the

Loan Agreement or otherwise) to pay the consideration required for the acquisition of Emerald Shares

pursuant to the Offer to satisfy its obligation under the Offer.

2.10. Effect of acceptance

The effect of acceptance of the Offer is set out in section 7 of the Annexure to the Bidder’s Statement.

Read that section in full to understand the effect that acceptance will have on your ability to exercise the rights

attaching to your Emerald Shares and the representations and warranties which you give by accepting the

Offer. In particular, if you accept the Offer, you may forfeit the opportunity to benefit from any superior offer

made by another bidder for your Emerald Shares, if such an offer were to eventuate. If you accept the Offer

you will not be able to sell your Emerald Shares the subject of that acceptance on ASX.

Emerald Shareholders should read section 7 of the Annexure to the Bidder’s Statement in light of the Notice

Freeing Takeover Offer From Defeating Conditions, which made the Offer unconditional.

2.11. Payment of consideration

Confederate has set out in section 5 of the Annexure to the Bidder’s Statement, the timing of the payment of

consideration to holders of Emerald Shares who accept the Offer. In general terms, you will receive the

consideration to which you are entitled under the Offer by the earlier of:

(a) a month after the later of:

i. the date you accept the Offer; and

For

per

sona

l use

onl

y

7

ii. the date the Offer becomes unconditional (which was 5 November 2013); and

(b) 21 days after the end of the Offer Period.

2.12. Changes to the Offer

Confederate can vary the Offer by:

(a) extending the Offer Period; or

(b) increasing the consideration offered under the Offer.

If you accept the Offer and Confederate subsequently increases its Offer Price, you are entitled to receive the

higher price.

2.13. Emerald Options

Emerald Option holders whose Options are exercised into Emerald Shares during the Offer Period will not be

able to accept the Offer in respect of those Emerald Shares issued. Confederate is not making a separate offer

to holders of Emerald Options.

2.14. Unmarketable Parcels

As set out in section 1.3 of the Annexure to the Bidder’s Statement (which was modified by the Supplementary

Bidder’s Statement), if accepting the Offer would leave an Emerald Shareholder with a parcel of Emerald

Shares that has a value of less than $500 (based on the closing price of Emerald Shares on ASX the day before

the Emerald Shareholder accepts the Offer) (“Small Parcel”) the Offer extends to that Small Parcel.

ASIC Class Order 13/521 modifies section 618(2) of the Corporations Act so that it does not extend to Small

Parcels (whether held beneficially or otherwise) that have come into existence, or increased in size, because of

a transaction (including the creation of one or more trusts) entered into after the Offer was publicly proposed.

As such, Small Parcels created by (for example):

(a) splitting large holdings into smaller parcels and then seeking to accept the Offer for all of your Emerald

Shares; or

(b) repeatedly purchasing and accepting into the Offer holdings that are Small Parcels;

are not able to be accepted into the Offer.

Full details on the treatment of Small Parcel’s under the Offer is set out in section 1.3 of the Annexure to the

Bidder’s Statement as amended by the new section 1.3 set out in the Supplementary Bidder’s Statement.

For

per

sona

l use

onl

y

8

3. Profile of Emerald

3.1. Overview of Emerald and its Principal Activities

(a) History and operations

Emerald is a petroleum exploration and production company, listed on ASX. Emerald’s head

office is located in West Perth, Australia.

Emerald’s major asset is a substantial equity interest in Emerald Oil Inc. (NYSE:EOX), an active

Williston Basin operating company listed on the New York Stock Exchange. In addition, Emerald

holds exploration and production interests in the Appalachian Gas Project located in Magoffin

County, Kentucky.

At the date of this Target’s Statement, Emerald has 943,651,304 Emerald Shares on issue,

comprising approximately 1500 Shareholders including Confederate which has a relevant interest

in approximately 24.73% of the Emerald Shares on issue (including those Emerald Shares

accepted into the Offer). Details of the substantial shareholders of Emerald are set out in section

3.8.

i. Emerald Oil Inc.

On 26 July 2012, Emerald completed a transaction whereby Voyager Oil and Gas Inc.

(AMEX:VOG) (Voyager), a publicly listed company in the United States, acquired Emerald Oil

Inc. (Emerald’s then wholly owned subsidiary) for 11,635,217 shares in Voyager. Voyager

subsequently changed its trading name to Emerald Oil Inc. (EOX), retaining its listing on the

New York Stock Exchange (NYSE:EOX) and implemented a 7 for 1 share split, consolidating

Emerald’s holding in EOX to 1,662,174 shares.

In May 2013, a meeting of Emerald Shareholders was held to consider distributing the EOX

shares in specie to Emerald Shareholders. Shareholder approval was not obtained for the in

specie distribution at that meeting.

On 8 October 2013, OGH sought to requisition a meeting for the in specie distribution of

Emerald’s interest in EOX. This requisition request was formally withdrawn as announced to

ASX on 18 October 2013.

Further information about EOX and Emerald’s interest therein is contained in section 5.2 of

the Independent Expert’s Report and the Independent Expert’s valuation thereof is

contained in section 10.1 of the Independent Expert’s Report.

ii. Canning Basin Project

As announced to ASX on 29 July 2013, Emerald entered into an agreement with Key

Petroleum Limited (ASX:KEY) to sell all of Emerald’s interest in the Canning Basin Project for 4

million shares in the capital of Key, and $50,000 cash. Emerald has provided to Key the

required transfer documentation and has received the $50,000 cash consideration

component, and will be issued the 4 million shares in the capital of KEY following KEY’s

annual general meeting, which is scheduled to be held on 13 November 2013.

For

per

sona

l use

onl

y

9

iii. Appalachian Gas Project

Emerald’s Appalachian gas operations are operated through Kentucky Energy Partners, a

company 75% owned by Emerald. KEP currently holds 2,5000 lease acres with 29 existing

wells potentially capable of gas production, as well as an 8 mile long gas gathering pipeline

and gas conditioning/compression facilities.

Further information about the Appalachian Gas Project is contained in section 5.3 of the

Independent Expert’s Report and the Independent Expert’s valuation thereof is contained in

section 10.2 of the Independent Expert’s Report.

iv. Cash Position

Emerald’s cash position at the date of this Target’s Statement has reduced from the position

set out in Emerald’s quarterly report for the period ended 30 September 2013. Given this

relatively modest cash position, the Company may, in the near term be required to raise

further cash. This could be achieved in a variety of ways, including by a capital raising (which

could be take place by placement, rights issue or otherwise), by liquidating a portion of

Emerald’s investment in EOX, or by borrowings.

(b) Ochre Scheme of Arrangement and In Specie Distribution Proposal

As announced on 2 August 2013, Emerald entered into a scheme implementation deed with

Ochre Group Holdings Limited. The implementation deed set out the steps in implementation a

scheme of arrangement under which Emerald Shareholders would receive 1 fully paid ordinary

share in OGH in exchange for every 2.75 Emerald Shares held.

As announced on 8 October 2013, Emerald and OGH mutually agreed to terminate the scheme

implementation deed, with no break fee payable to either party. Subsequently, as announced on

8 October 2013, OGH sought to requisition a meeting of Emerald Shareholders seeking a

resolution for a reduction of capital and in specie distribution of Emerald’s interest in EOX. This

requisition request was formally withdrawn as announced to ASX on 18 October 2013.

According to its latest substantial shareholder notice given to ASX, OGH (via its wholly owned

subsidiary, Ochre Petroleum Pty Ltd) has a relevant interest in 155,650,000 Emerald Shares.

3.2. Directors

The Directors of Emerald at the date of this Target’s Statement are set out below.

Jeremy Shervington – Non Executive Chairman

Mr Shervington operates a legal practice in Western Australia. He specialises in the laws regulating companies

and the securities industry in Australia. Mr Shervington has over 30 years’ experience as a lawyer, gained since

admission as a Barrister and Solicitor of the Supreme Court of Western Australia. Mr Shervington has since

1983 served as a Director of various ASX listed companies as well as a number of unlisted public and private

companies.

For

per

sona

l use

onl

y

10

Ross Williams – Non Executive Director

Mr Williams is a founding shareholder of MACA Limited (ASX: MLD) and continues to fulfil the role of Financial

Director. Mr Williams also has 16 years banking experience having held executive positions with a major

Australian Bank. Mr Williams is a past fellow of the Australian Institute of Banking and Finance and holds a

Post Graduate Diploma in Financial Services Management.

Tim Kestell - Non Executive Director

Mr Kestell has over 15 years’ experience in equity markets, including working for Australian stockbrokers Euroz Securities and Patersons. In the past decade, Mr Kestell has played a key role in forming and/or recapitalising publicly listed companies, and raising more than $70,000,000 in the process as well as being involved in numerous takeovers, including Barrick Gold Limited's offer for Tusker Gold Limited. Mr Kestell holds a Bachelor of Commerce degree and is currently a non executive director of ASX listed

company Emmerson Resources Limited and Blue Capital Limited.

Mr Kestell is also a director of Confederate and controls 50% of the shares in Confederate.

Peter Pynes – Non Executive Director

My Pynes has in excess of 20 years’ experience in Australia and overseas capital markets. He previously worked at Deutsche Bank as a director, global markets where he gained extensive knowledge of global structured debt products as well as capital raising and syndication. In this role Mr Pynes established relationships with leading Australian investment institutions, which included his involvement in $350m of ASX listed structured debt transactions and in excess of $3.8 billion of ASX listed hybrid and convertible investments. In the past decade, Mr Pynes has played a key role in forming and capitalising both public listed and unlisted companies. Mr Pynes has been involved in both initial public offerings and takeovers, including the listing on the ASX of Tusker Gold Limited and its successful cash takeover by Barrick Gold Limited. Mr Pynes is a director of MPC Funding Limited, a specialist financing company providing in excess of $450m of loan funds for the development of the Melbourne Convention Centre, Nexus Bonds Limited and Blue Capital Limited. Mr Pynes is a Fellow of the Australian Institute of Company Directors (FAICD) and a Senior Associate of

Financial Services Institute of Australia (SA FIN).

Mr Pynes is also a director of Confederate and controls 50% of the shares in Confederate.

3.3. Summary of historical financial information

The summary historical financial information below has been extracted from Emerald’s audited financial

statements for the year ended 30 June 2013 and does not take into account the effects of the Offer.

Copies of Emerald’s annual report from which the financial information contained in this Target’s Statement

was extracted can be found on Emerald’s website at www.emeraldoilandgas.com. These reports also contain

details of Emerald’s accounting policies and the notes and assumptions that accompany the financial

statements. If you would like to receive a copy of any of these documents, please contact Emerald’s company

secretary on (+618) 9389 2111 between 9.00am to 5.00pm (WST) Monday to Friday.

For

per

sona

l use

onl

y

11

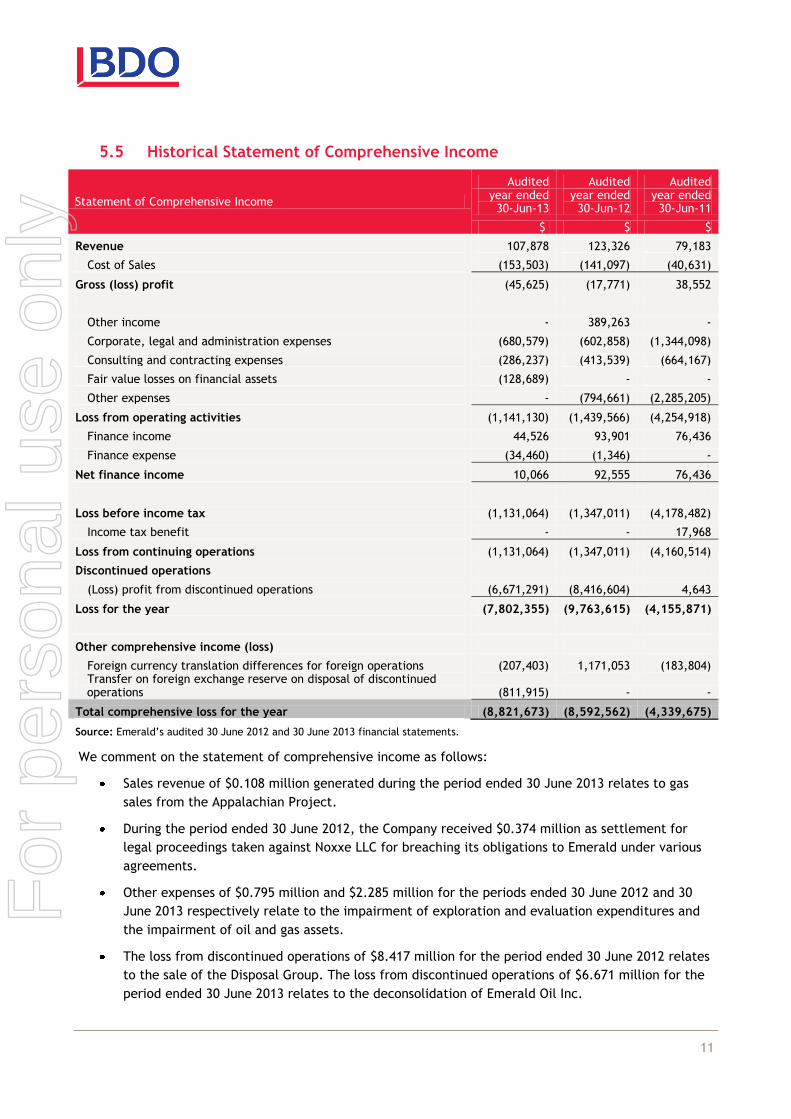

Consolidated Statement of Comprehensive Income for the year ended 30 June 2013

2013

2012

$ $ Revenue 107,878 123,326 Cost of Sales (153,503) (141,097)

Gross loss (45,625) (17,771) Other income - 389,263 Corporate, legal and administration expenses (680,579) (602,858) Consulting and contracting expenses (286,237) (413,539) Fair value losses on financial assets (128,689) - Other expenses - (794,661)

Loss from operating activities (1,141,130) (1,439,566) Finance income 44,526 93,901 Finance expense (34,460) (1,346)

Net finance income 10,066 92,555

Loss before income tax (1,131,064) (1,347,011) Income tax benefit - -

Loss from continuing operations (1,131,064) (1,347,011) Loss from discontinued operations (6,671,291) (8,416,604)

Loss for the year (7,802,355) (9,763,615)

Other comprehensive (loss) income Items that may be reclassified to profit or loss Exchange differences on translation of foreign operations (207,403) 1,171,053 Reclassification adjustments Transfer of foreign exchange reserve on disposal of discontinued operations (811,915) -

Other comprehensive (loss) income for the year (1,019,318) 1,171,053

Total comprehensive loss for the year (8,821,673) (8,592,562)

Loss for the year is attributable to: Owners of the parent (7,736,915) (9,695,166) Non-controlling interest (65,440) (68,449)

(7,802,355) (9,763,615)

Total comprehensive loss for the year is attributable to: Owners of the parent (8,774,397) (8,526,570) Non-controlling interest (47,276) (65,992)

(8,821,673) (8,592,562)

Basic loss per share for loss from continuing operations attributable to owners of the parent (cents)

(0.113) (0.155)

Basic loss per share for loss attributable to owners of the parent (cents)

(0.822) (1.175)

For

per

sona

l use

onl

y

12

Consolidated Statement of Financial Position as at 30 June 2013

2013 2012 $ $ CURRENT ASSETS Cash and cash equivalents 403,672 504,457 Trade and other receivables 40,242 22,073 Financial assets at fair value through profit or loss 12,485,233 - Assets classified as held for sale - 39,737,682

Total current assets 12,929,147 40,264,212 NON-CURRENT ASSETS Property, plant and equipment 182,037 191,563 Exploration and evaluation expenditure 389,068 339,902 Oil and gas assets 530,149 569,684

Total non-current assets 1,101,254 1,101,149

TOTAL ASSETS 14,030,401 41,365,361

CURRENT LIABILITIES Trade and other payables 64,024 172,465 Loans and borrowings - 363,065 Other creditors - 1,076,391 Liabilities classified as held for sale - 17,693,803

Total current liabilities 64,024 19,305,724

TOTAL LIABILITIES 64,024 19,305,724

NET ASSETS 13,966,377 22,059,637

EQUITY Issued capital 46,356,181 45,627,768 Reserves 1,059,713 2,070,580 Accumulated losses (33,539,990) (25,803,075)

Total equity attributable to owners of the parent 13,875,904 21,895,273 Non-controlling interest 90,473 164,364

TOTAL EQUITY 13,966,377 22,059,637

For

per

sona

l use

onl

y

13

Consolidated Statement of Cash Flows for the year ended 30 June 2013

2013 2012 $ $

Receipts from customers 99,931 343,765 Interest received 44,526 93,901 Interest paid (35,806) - Payments to suppliers and employees (1,304,580) (4,332,663)

Net cash used in operating activities (1,195,929) (3,894,997)

CASH FLOWS FROM INVESTING ACTIVITIES Purchase of property, plant and equipment - (38,465) Exploration and evaluation expenditure (1,684,200) (20,680,951) Proceeds on sale of subsidiary, net of cash disposed 1,657,328 - Payment for equity investments - (276,315) Purchase of oil and gas assets - (1,173,631) Settlement of Noxxe litigation - 373,762

Net cash used in investing activities (26,872) (21,795,600)

Proceeds from borrowings 1,875,354 15,021,047 Repayment of borrowings (363,065) - Proceeds from issue of shares 569 3,085,795 Capital raising costs (103,017) (236,944)

Net cash provided by financing activities 1,409,841 17,869,898

Net increase/(decrease) in cash and cash equivalents 187,040 (7,820,699) Cash and cash equivalents at the beginning of the year 565,742 8,385,274 Effect of exchange rates on cash holding in foreign currencies (349,110) 1,167

Cash and cash equivalents at the end of the year 403,672 565,742

For

per

sona

l use

onl

y

14

3.4. Recent share price performance

Emerald Shares are quoted on ASX under the code EMR. The graph below shows the price at which Emerald

Shares have traded in the 12 months up to close of market on 11 November 2013.

Since the announcement to ASX of Confederate’s intention to make the Offer on 1 October 2013 to 11

November 2013, Emerald Shares have traded on ASX within the range of $0.012 to $0.014.

3.5. Publicly available information

Emerald is a company listed on ASX and is subject to the periodic and continuous disclosure requirements of

the Listing Rules and the Corporations Act. A substantial amount of information on Emerald is publicly

available and may be accessed by referring to Emerald on www.asx.com.au.

A list of announcements made by Emerald between 1 November 2012 and the date of this Target’s Statement

is set out in Annexure 2. This information may be relevant to your assessment of the Offer. Copies of the

announcements are available from the ASX.

Further announcements regarding developments in relation to the Offer will continue to be made available on

Emerald’s website at www.emeraldoilandgas.com and www.asx.com.au after the date of this Target’s

Statement.

3.6. Further information

Further information about Emerald can be found on Emerald’s website at www.emeraldoilandgas.com.

3.7. Issued capital

(a) Shares

As at the date of this Target’s Statement, Emerald had 943,651,304 fully paid ordinary shares on issue and

quoted on ASX.

(b) Options

As at the date of this Target’s Statement, Emerald had 167,600,000 Options on issue as follows:

i. 117,600,000 Options exercisable for $0.05 on or before 30 April 2014; and

ii. 50,000,000 Options exercisable for $0.05 on or before 28 June 2014.

The Offer does not extend to Shares issued on any exercise of Options.

For

per

sona

l use

onl

y

15

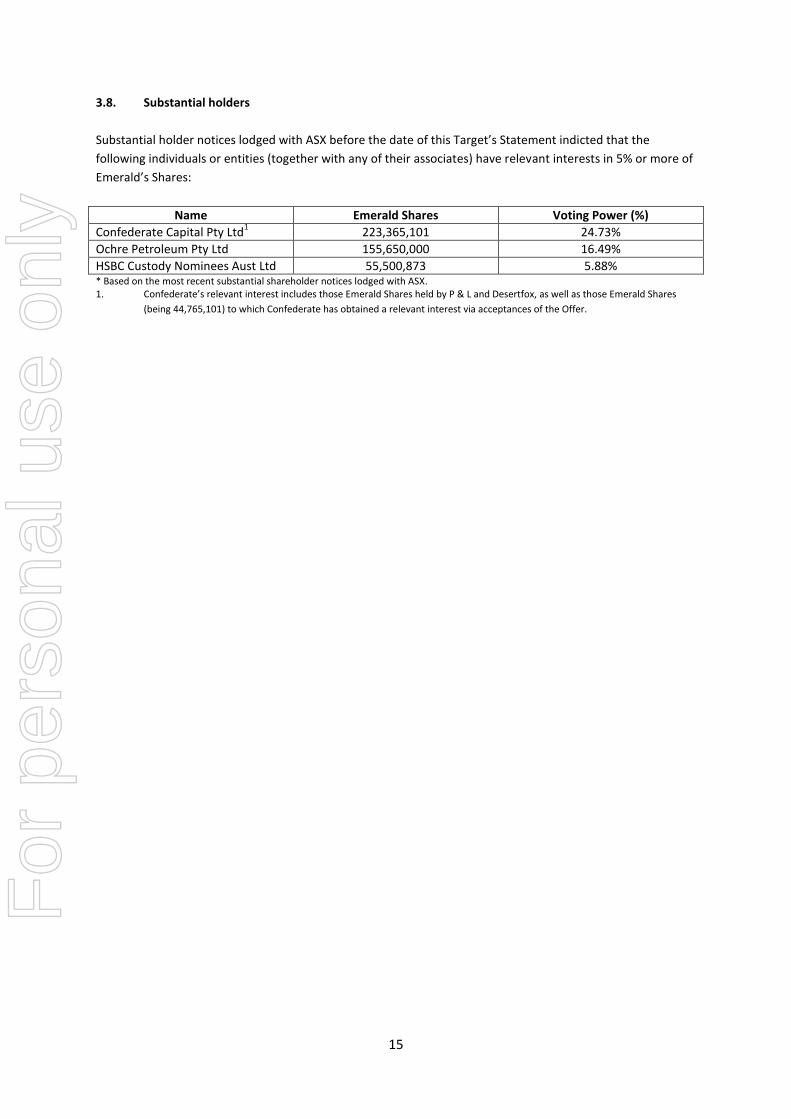

3.8. Substantial holders

Substantial holder notices lodged with ASX before the date of this Target’s Statement indicted that the

following individuals or entities (together with any of their associates) have relevant interests in 5% or more of

Emerald’s Shares:

Name Emerald Shares Voting Power (%)

Confederate Capital Pty Ltd1 223,365,101 24.73%

Ochre Petroleum Pty Ltd 155,650,000 16.49%

HSBC Custody Nominees Aust Ltd 55,500,873 5.88% * Based on the most recent substantial shareholder notices lodged with ASX. 1. Confederate’s relevant interest includes those Emerald Shares held by P & L and Desertfox, as well as those Emerald Shares

(being 44,765,101) to which Confederate has obtained a relevant interest via acceptances of the Offer.

For

per

sona

l use

onl

y

16

4. Profile of Confederate

4.1. Disclaimer

The following information about Confederate has been prepared by Emerald using publicly available

information, including information in the Bidder’s Statement, and has not been independently verified.

Accordingly, Emerald does not, subject to the Corporations Act, make any representation or warranty, express

or implied, as to the accuracy or completeness of this information.

The information on Confederate in this Target’s Statement should not be considered comprehensive.

4.2. Introduction to Confederate

As set out in section 3.1 of the Bidder’s Statement, Confederate is a privately held company incorporated on

27 September 2013 as a special purpose vehicle for making the Offer. Confederate’s registered office is

located in Perth, Australia.

The current shareholders of Confederate are:

(a) P & L – 1 Confederate Share; and

(b) Desertfox – 1 Confederate Share.

Confederate is not currently a registered holder of Emerald Shares. However, P & L and Desertfox are each

currently registered holders of 94,300,000 Emerald Shares (being respective interests of 9.99% in the Emerald

Shares on issue at the date of this Target’s Statement). As a result, Confederate and its associates held a total

of 188,600,000 Emerald Shares (being a 19.99% interest in the Emerald Shares on issue at the date of the

Bidder’s Statement).

At the date of this Target’s Statement (based on the most recent substantial shareholder notice lodged with

ASX), Confederate has acquired a relevant interest in 44,765,101 Emerald Shares as a result of contracts arising

upon acceptances of the Offer. As a result, Confederate and its associates have a relevant interest in a total of

233,365,101 Emerald Shares (being a 24.73% interest in the Emerald Shares on issue at the date of this

Target’s Statement).

4.3. Overview of Confederate and its Principal Activities

(a) History and operations

Due to Confederate being recently incorporated, it does not have any significant track record or investments

or returns to investors. Confederate does not have any subsidiaries, interests in any other companies or assets

or carry on any activities other than as described in section 3 of the Bidder’s Statement.

Confederate:

i. has not lodged any financial statements with ASIC; and

For

per

sona

l use

onl

y

17

ii. is not listed on any recognised stock exchange and therefore is not subject to the periodic and continuous

disclosure requirements of the Listing Rules.

(b) Financial information on Confederate

While Confederate does not have any significant track record of investments or returns to investors, it has

entered into the Loan Agreement with its current shareholders and their associated entities for the purpose of

funding the Offer. Further details of the Loan Agreement are set out in section 6.2 of the Bidder’s Statement

and section 2.9 of this Target’s Statement.

4.4. Directors

The directors of Confederate at the date of this Target’s Statement are:

(a) Mr Tim Kestell; and

(b) Mr Peter Pynes.

Profiles of Messrs Kestell and Pynes are set out in section 3.2(b) of the Bidder’s Statement and section 3.2 of

this Target’s Statement.

4.5. Sources of Consideration for the Offer

The sources of the consideration for the acquisition of the Emerald Shares under the Offer are set out in

section 6 of the Bidder’s Statement and section 2.9 of this Target’s Statement.

4.6. Confederate’s intentions in relation to Emerald

Confederate’s intentions in relation to Emerald are set out in section 7 of the Bidder’s Statement.

4.7. Publicly available information about Confederate

Confederate is required to lodged various documents with ASIC. Copies of documents lodged with ASIC by

Confederate may be obtained from, or inspected at, an ASIC office.

4.8. Confederate Shareholder Information

(a) P & L

P&L is a privately held company which was incorporated as an investment vehicle for the benefit of its shareholders. The current directors and shareholders of P&L are Peter Pynes and his wife Lara Pynes who each hold 1 fully paid ordinary share in the capital of P&L. P&L does not carry on or run an active business. It holds equity and property assets on behalf of its members. In addition, P&L acts as trustee for the P & L Capital Trust, a family trust which has been formed to hold assets on behalf of its beneficiaries who are all of the members of Peter Pynes’ immediate family. Other than its interests in Confederate (set out in section 3.1 of the Bidder’s Statement and section 4.2 of this Target’s Statement) and Emerald (set out in section 5.4 of the Bidder’s Statement and section 4.2 of this Target’s Statement), P&L holds 100,000 fully paid ordinary shares in the capital of Indago Resources Pty Ltd (Indago) and 10,001 fully paid ordinary shares in the capital of Capital Custodians Australia Pty Ltd.

For

per

sona

l use

onl

y

18

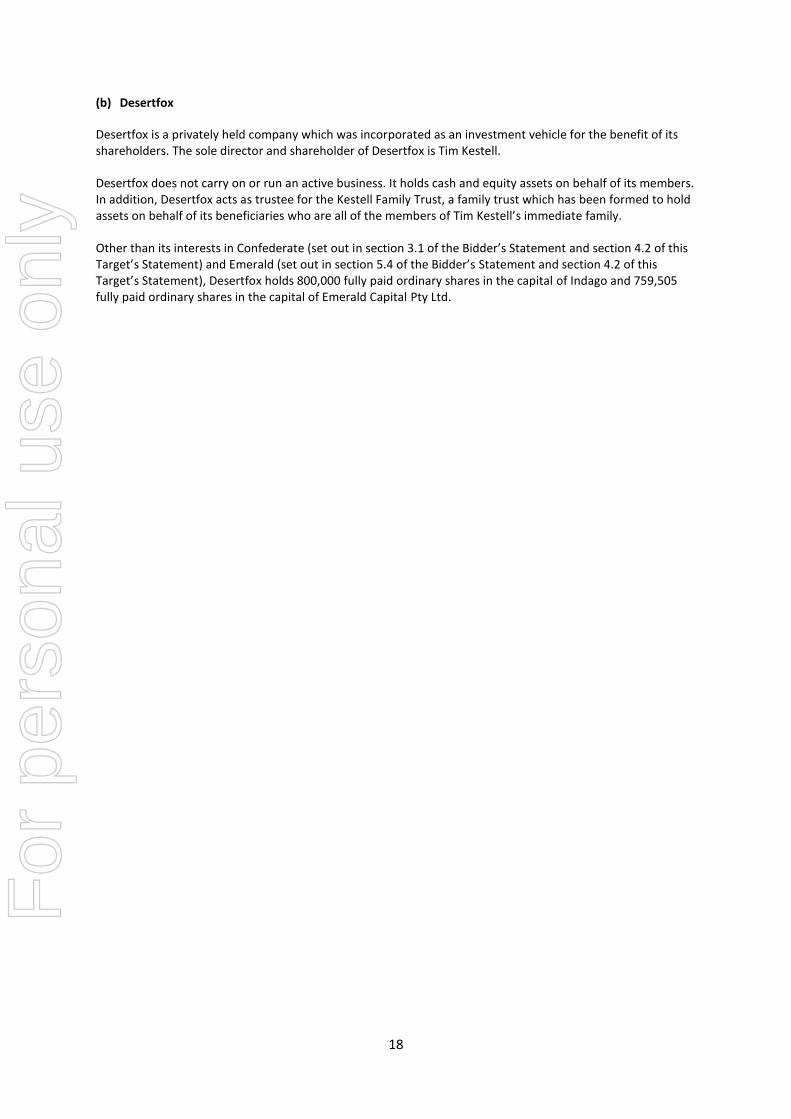

(b) Desertfox

Desertfox is a privately held company which was incorporated as an investment vehicle for the benefit of its shareholders. The sole director and shareholder of Desertfox is Tim Kestell. Desertfox does not carry on or run an active business. It holds cash and equity assets on behalf of its members. In addition, Desertfox acts as trustee for the Kestell Family Trust, a family trust which has been formed to hold assets on behalf of its beneficiaries who are all of the members of Tim Kestell’s immediate family. Other than its interests in Confederate (set out in section 3.1 of the Bidder’s Statement and section 4.2 of this Target’s Statement) and Emerald (set out in section 5.4 of the Bidder’s Statement and section 4.2 of this Target’s Statement), Desertfox holds 800,000 fully paid ordinary shares in the capital of Indago and 759,505 fully paid ordinary shares in the capital of Emerald Capital Pty Ltd.

For

per

sona

l use

onl

y

19

5. Your choices as an Emerald Shareholder

The Independent Emerald Directors’ recommendations in relation to the Offer are set out in section 1.2 of

this Target’s Statement.

As an Emerald Shareholder, you can respond to the Offer in three ways.

5.1. Accept the Offer

To accept the Offer, follow the instructions in section 4 of the Annexure to the Bidder’s Statement and on the

acceptance form accompanying the Bidder’s Statement.

Before deciding how to respond to the Offer you should:

(a) read the Bidder’s Statement (including the Supplementary Bidder’s Statement), the Target’s Statement,

and the Notice Freeing Offer From Defeating Conditions in full;

(b) consider the information given in relation to the Offer in the Bidder’s Statement (including the

Supplementary Bidder’s Statement), the Target’s Statement, and the Notice Freeing Offer From Defeating

Conditions; and

(c) consult your broker, financial or other professional adviser if you are in any doubt as to what action to

take or how to accept the Offer.

If you have any queries about the Offer you may also call Emerald’s company secretary, Mr Graeme Smith, on

(+61 8) 9389 2111 on weekdays between 9.00am and 5.00pm (WST).

The Offer may only be accepted for 30% of you Emerald Shares.

How you accept the Offer depends on whether your Emerald Shares are in an Issuer Sponsored Holding or

CHESS holding.

(a) If you hold your Emerald Shares in an Issuer Sponsored Holding (such holdings will be evidenced by an ‘I’

appearing next to your holder number on the acceptance form enclosed with the Bidder’s Statement), to

accept the Offer you must complete and sign the acceptance form enclosed with the Bidder’s Statement

and return it in accordance with the instructions contained in the acceptance form before the Offer closes.

(b) If you hold your Emerald Shares in a CHESS holding (such holdings will be evidenced by an ‘X’ appearing

next to your holder on the acceptance form enclosed with the Bidder’s Statement), you may accept the

Offer be either:

i. completing and signing the acceptance form enclosed with the Bidder’s Statement and returning it in

accordance with the instructions contained in the acceptance form; or

ii. calling your broker and instructing your broker to accept the Offer on your behalf,

before the Offer closes.

For

per

sona

l use

onl

y

20

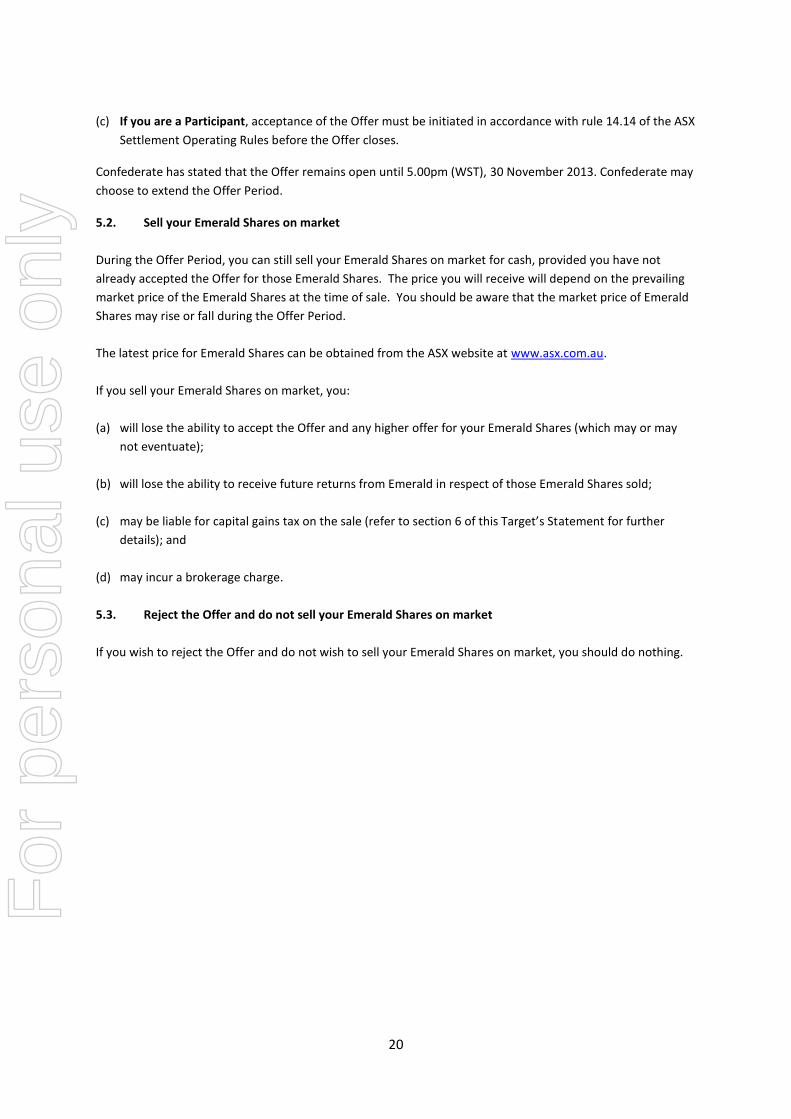

(c) If you are a Participant, acceptance of the Offer must be initiated in accordance with rule 14.14 of the ASX

Settlement Operating Rules before the Offer closes.

Confederate has stated that the Offer remains open until 5.00pm (WST), 30 November 2013. Confederate may

choose to extend the Offer Period.

5.2. Sell your Emerald Shares on market

During the Offer Period, you can still sell your Emerald Shares on market for cash, provided you have not

already accepted the Offer for those Emerald Shares. The price you will receive will depend on the prevailing

market price of the Emerald Shares at the time of sale. You should be aware that the market price of Emerald

Shares may rise or fall during the Offer Period.

The latest price for Emerald Shares can be obtained from the ASX website at www.asx.com.au.

If you sell your Emerald Shares on market, you:

(a) will lose the ability to accept the Offer and any higher offer for your Emerald Shares (which may or may

not eventuate);

(b) will lose the ability to receive future returns from Emerald in respect of those Emerald Shares sold;

(c) may be liable for capital gains tax on the sale (refer to section 6 of this Target’s Statement for further

details); and

(d) may incur a brokerage charge.

5.3. Reject the Offer and do not sell your Emerald Shares on market

If you wish to reject the Offer and do not wish to sell your Emerald Shares on market, you should do nothing.

For

per

sona

l use

onl

y

21

6. Tax considerations

6.1. Introduction

The following is a general description of the Australian income and capital gains tax consequences to Emerald

Shareholders on the acceptance of the Offer. The comments set out below are relevant only to those Emerald

Shareholders who hold their Shares as capital assets for the purpose of investment.

Emerald Shareholders who are not resident in Australia for tax purposes should take into account the tax

consequences under the laws of their country of residence, as well as under Australian law, of acceptance of

the Offer. The following summary is intended only for Australian resident Emerald Shareholders.

The following description is based upon the Australian law and administrative practice in effect at the date of

this Target’s Statement, but it is general in nature and is not intended to be an authoritative or complete

statement of the laws applicable to the particular circumstances of every Emerald Shareholder.

Emerald Shareholders should seek independent professional advice in relation to their own particular

circumstances.

6.2. Australian resident shareholders

Acceptance of the Offer will involve the disposal by Emerald Shareholders of their Emerald Shares by way of transfer to Confederate. This change in the ownership of the Emerald Shares will constitute a capital gains tax event for Australian capital gains tax purposes. Emerald Shareholders who are Australian residents may make a capital gain or capital loss on the transfer of Emerald Shares acquired on or after 20 September 1985, depending on whether their capital proceeds from the disposal of the Emerald Shares are more than the cost base (or in some cases indexed cost base) of those Emerald Shares, or whether the capital proceeds are less than their reduced cost base of those Emerald Shares. The capital proceeds of the capital gains tax event will be the consideration price received by the Emerald Shareholder in respect of the disposal of the Emerald Shares. The cost base of the Emerald Shares generally includes their cost of acquisition and any incidental costs of acquisition and disposal that are not deductible to the shareholder. If the Emerald Shares were acquired at or before 11.45am on 21 September 1999 and held for at least 12

months before their disposal, an Emerald Shareholder may adjust the cost base of the Emerald Shares to

include indexation by reference to changes in the consumer price index from the calendar quarter in which the

Emerald Shares were acquired until the quarter ended 30 September 1999. These indexation adjustments are

taken into account only for the purposes of calculating a capital gain; they are ignored when calculating the

amount of any capital loss.

Individuals, complying superannuation entities or trustees that have held Emerald Shares for at least 12

months but do not index the cost base of the Emerald Shares should be entitled to discount the amount of the

capital gain (after application of capital losses) from the disposal of Emerald Shares by 50% in the case of

individuals and trusts or by 33% for complying superannuation entities.

For

per

sona

l use

onl

y

22

Capital gains and capital losses of a taxpayer in a year of income are aggregated to determine whether there is

a net capital gain. Any net capital gain is included in assessable income and is subject to income tax. Capital

losses may not be deducted against other income for income tax purposes, but may be carried forward to

offset against future capital gains.

6.3. Non resident shareholders

Emerald Shareholders who are not resident in Australia for income tax purposes are generally not subject to

Australian capital gains tax on the disposal of Emerald Shares if they and their associates have not held 10% or

more of the issued Emerald Shares throughout a twelve month period in the two years preceding the disposal

of their Emerald Shares. This is on the assumption that Emerald will be deemed to have over 50% of its

underlying value represented by Australian real property (land and rights relating to land) – which would

generally be the case for Australian mining companies.

6.4. Goods and services tax

Holders of Emerald Shares should not be liable to GST in respect of a disposal of those Emerald Shares.

6.5. Stamp duty

Holders of Emerald Shares should not be liable to stamp duty in respect of a disposal of those Emerald

Shares.

For

per

sona

l use

onl

y

23

7. Directors’ interests

7.1. Directors’ interests in Emerald Shares

As at the date of this Target’s Statement, the Directors of Emerald have direct and indirect relevant interests in

the following securities in Emerald:

Director Emerald Shares Emerald Options

Jeremy Shervington 8,311,915 NIL

Ross Williams NIL NIL

Tim Kestell*

94,300,000 NIL

Peter Pynes* 94,300,000 NIL

* Messrs Kestell and Pynes’ relevant interests in Emerald Shares are held via entities controlled by them, namely, Desertfox and P & L

respectively, and pursuant to Emerald Shares the subject of contracts arising upon acceptances of the Offer.

* Both Desertfox and P & L are associates of Confederate, and Confederate and its associates have a relevant interest in 233,365,101

Emerald Shares.

7.2. Directors’ intentions in relation to their Emerald Shareholdings and the Offer

As at the date of this Target’s Statement, the Directors’ intentions in relation to the Offer for the Emerald

Shares held or controlled by them are as follows:

Jeremy Shervington:

Mr Shervington does not intend to accept the Offer in relation to the Emerald Shares he controls.

Ross Williams:

Mr Williams does not hold or control any Emerald Shares and therefore Offer is not made to him.

Tim Kestell:

Mr Kestell’s interest in Emerald Shares (other than those Emerald Shares which have been accepted into the

Offer at the date of this Target’s Statement) is held via Desertfox which is an associate of Confederate, and as

such, will not be accepted into the Offer.

Peter Pynes:

Mr Pynes’ interest in Emerald Shares (other than those Emerald Shares which have been accepted into the

Offer at the date of this Target’s Statement) is held via P & L which is an associate of Confederate, and as such,

will not be accepted into the Offer.

7.3. Directors’ recent dealings in Emerald Shares

Except as disclosed below, no Director has acquired or disposed of a relevant interest in any Emerald Shares in

the four month period immediately preceding the date of this Target’s Statement:

Tim Kestell (Desertfox):

Date Emerald Shares Total Consideration Consideration per Emerald Share

%

18/9/2013 66,372,627 $696,912.58 1.05 cents 7.03%

1/10/2013 7,140,689 $99,255.58 1.39 cents 0.76%

2/10/2013 6,444,949 $90,229.29 1.40 cents 0.68%

For

per

sona

l use

onl

y

24

3/10/2013 13,541,735 $189,584.29 1.40 cents 1.44%

8/10/2013 800,000 $10,400.00 1.30 cents 0.08%

TOTAL 94,300,000 $1,086,381.74 - 9.99%

Peter Pynes (P & L):

Date Emerald Shares Total Consideration Consideration per Emerald Share

%

18/9/2013 66,372,627 $696,912.58 1.05 cents 7.03%

1/10/2013 7,140,690 $99,255.58 1.39 cents 0.76%

2/10/2013 6,444,949 $90,229.29 1.40 cents 0.68%

3/10/2013 13,541,734 $189,584.28 1.40 cents 1.44%

8/10/2013 800,000 $10,400.00 1.30 cents 0.08%

TOTAL 94,300,000 $1,086,381.74 - 9.99%

Confederate:

According to Confederate’s most recent disclosure to ASX in relation to its interest in Emerald, valid

acceptances under the Offer have been received in respect of 44,765,101 Emerald Shares, comprising 4.83 %

of the total number of Emerald Shares on issue.

7.4. Directors’ interests in Confederate securities

At the date of this Target’s Statement, both Tim Kestell and Peter Pynes have a relevant interest in 1

Confederate share (being 50% of the issued shares of Confederate) via their respective controlled entities,