Target : INR 232 KEY DATA Tilaknagar Industries...

21

Tilaknagar Industries Ltd. Shareholding % 2Q 3Q 4Q Promoters 74.0 74.0 61.0 MF/Banks/Indian FIs 6.0 7.0 2.0 FII/ NRIs/ OCBs 0.0 0.0 8.0 Indian Public 20.0 19.0 29.0 KEY DATA Market Cap (INR bn) 5.2 Market Cap (USD mn) 115.8 52 WK High / Low 177/24 Avg Daily Volume (BSE) 128008 Face Value (INR) 10 BSE Sensex 17639 Nifty 5274 BSE Code 507205 NSE Code NA Reuters Code TILK.BO Bloomberg Code TLNGR IN Performance Chart CMP : INR 172 Rating : Buy Target : INR 232 Initiating Coverage Investment Summary Tilaknagar Industries Ltd (TI) is one of the leading players in the Indian alcoholic beverage industry and manufactures Indian Made Foreign Liquor (IMFL), with over 24 manufacturing units across India. The company has total 16 brands across a diverse range of price and product segments under its portfolio. The IMFL industry (worth USD 2 billion) is expected to grow at CAGR of 12.7% through FY10-FY15E period. We believe, TI is well-placed to tap opportunity in the rising Indian liquor market and expect company to post excellent performance through FY09-FY12E period. Capacity Expansion…to boost volume: In FY09, TI had total installed capacity of 50 KLPD of molasses based ENA. The company has successfully commissioned a new 50 KLPD molasses- based ENA plant and 100 KLPD grain-based ENA plant in Sept09 and Dec09 respectively. We believe that the company will get full benefit of expanded capacity in FY11E and FY12E. We expect total IMFL sales volume to increase by 53.3%, 105.9% and 22.9% YoY in FY10E, FY11E and FY12E respectively. We expect net sales to grow at CAGR of 59.7% through FY09-FY12E period. Healthy growth in IMFL industry: The IMFL segment constitutes 31% of the total Indian liquor market and is a 195 million cases industry. With nearly half of Indian population being young and at working age with rising disposable income, the IMFL segment is expected to grow at a CAGR of 12.7% through FY10-FY15E period. With restriction in direct advertising and strong brand loyalty among consumers, existing alcoholic beverage manufacturers with well-established brands are in sweet pot to exploit the ensuing growth in IMFL industry. Grain-based distillery…less dependence on single feedstock: Molasses is the key raw material for alcohol production. Although, molasses is available in abundant quantity for TI, its prices are volatile as they are subject to vagaries of cyclicality in sugar industry. With setting up of 100 KLPD grain based distilleries, the company has reduced its over-dependence on molasses as a feedstock. In addition, the Maharashtra govt will give INR 10/litre rebate on the excise-duty to the grain-based distilleries, resulting in subsidy of INR 250 million for TI (to be availed till Dec 2013). Margins to improve: Due to increase in sugarcane acreage, on the back of handsome prices paid by sugar mills in SY10, we expect sugarcane production to increase by 30-40% YoY in SY11. Molasses availability being directly linked to sugarcane production, we conservatively expect molasses price to decline by 2.0% YoY in FY11E and FY12E each. (Molasses accounts for ~50% of total raw material cost). Overall, we expect EBITDA margins to expand by 80 bps, 70 bps and 30 bps YoY to 19.3%, 20.0% and 20.3% YoY in FY10E, FY11E and FY12E respectively. Improvement in Return Ratios: With completion of all the major expansion plans in FY10, we expect return ratios to improve going forward. We expect RoE and RoCE to increase from 14.3% and 8.6% in FY09 to 25.7% and 16.5% in FY12E respectively. We also expect company to turn FCF positive in FY12E and debt-equity ratio to increase from 0.8x in FY09 to 1.4x in FY10E and then again decline to 0.9x in FY12E. Key Concerns: Unfavourable judgement in legal case against Dutch spirit company UTO Increase in key input prices Concentration of revenue in Southern Region Valuations: At the current price, the company is trading at 8.4x and 6.2x FY11E and FY12E earnings and 5.7x and 4.3x FY11E and FY12E EV/EBITDA respectively. We initiate coverage on the company with BUY recommendation and price target of INR 232 (average of target FY12E EV/EBITDA of 5.5x and FY12E P/E of 8.0x). Sunny Agrawal Analyst Tel. : 4000 2667 [email protected] April 16, 2010 For Private Circulation Only FINQUEST research also available on BLOOMBERG FSPL <GO> and REUTERS. Financials F09 F10E* F11E (INR Mn.) Net Sales 2369.7 4108.6 7631.1 EBITDA 437.2 792.9 1527.1 EPS 19.1 10.4 20.6 P/E 9.0 16.5 8.4 * Issued Bonus in ratio of 2:1 and accounted for conversion of all CCPS and Warrants issued till FY10E end

Transcript of Target : INR 232 KEY DATA Tilaknagar Industries...

Tilaknagar Industries Ltd.

Shareholding % 2Q 3Q 4Q

Promoters 74.0 74.0 61.0

MF/Banks/Indian FIs 6.0 7.0 2.0

FII/ NRIs/ OCBs 0.0 0.0 8.0

Indian Public 20.0 19.0 29.0

KEY DATA

Market Cap (INR bn) 5.2

Market Cap (USD mn) 115.8

52 WK High / Low 177/24

Avg Daily Volume (BSE) 128008

Face Value (INR) 10

BSE Sensex 17639

Nifty 5274

BSE Code 507205

NSE Code NA

Reuters Code TILK.BO

Bloomberg Code TLNGR IN

Performance Chart

CMP : INR 172Rating : BuyTarget : INR 232

Initiating Coverage

Investment Summary

Tilaknagar Industries Ltd (TI) is one of the leading players in the Indian alcoholic beverageindustry and manufactures Indian Made Foreign Liquor (IMFL), with over 24 manufacturingunits across India. The company has total 16 brands across a diverse range of price and productsegments under its portfolio. The IMFL industry (worth USD 2 billion) is expected to grow atCAGR of 12.7% through FY10-FY15E period. We believe, TI is well-placed to tap opportunityin the rising Indian liquor market and expect company to post excellent performance throughFY09-FY12E period.

Capacity Expansion…to boost volume: In FY09, TI had total installed capacity of 50 KLPD ofmolasses based ENA. The company has successfully commissioned a new 50 KLPD molasses-based ENA plant and 100 KLPD grain-based ENA plant in Sept09 and Dec09 respectively. Webelieve that the company will get full benefit of expanded capacity in FY11E and FY12E. Weexpect total IMFL sales volume to increase by 53.3%, 105.9% and 22.9% YoY in FY10E, FY11Eand FY12E respectively. We expect net sales to grow at CAGR of 59.7% through FY09-FY12Eperiod.

Healthy growth in IMFL industry: The IMFL segment constitutes 31% of the total Indian liquormarket and is a 195 million cases industry. With nearly half of Indian population being youngand at working age with rising disposable income, the IMFL segment is expected to grow at aCAGR of 12.7% through FY10-FY15E period. With restriction in direct advertising and strongbrand loyalty among consumers, existing alcoholic beverage manufacturers with well-establishedbrands are in sweet pot to exploit the ensuing growth in IMFL industry.

Grain-based distillery…less dependence on single feedstock: Molasses is the key raw materialfor alcohol production. Although, molasses is available in abundant quantity for TI, its pricesare volatile as they are subject to vagaries of cyclicality in sugar industry. With setting up of 100KLPD grain based distilleries, the company has reduced its over-dependence on molasses as afeedstock. In addition, the Maharashtra govt will give INR 10/litre rebate on the excise-duty tothe grain-based distilleries, resulting in subsidy of INR 250 million for TI (to be availed till Dec2013).

Margins to improve: Due to increase in sugarcane acreage, on the back of handsome pricespaid by sugar mills in SY10, we expect sugarcane production to increase by 30-40% YoY inSY11. Molasses availability being directly linked to sugarcane production, we conservativelyexpect molasses price to decline by 2.0% YoY in FY11E and FY12E each. (Molasses accountsfor ~50% of total raw material cost). Overall, we expect EBITDA margins to expand by 80 bps,70 bps and 30 bps YoY to 19.3%, 20.0% and 20.3% YoY in FY10E, FY11E and FY12Erespectively.

Improvement in Return Ratios: With completion of all the major expansion plans in FY10, weexpect return ratios to improve going forward. We expect RoE and RoCE to increase from14.3% and 8.6% in FY09 to 25.7% and 16.5% in FY12E respectively. We also expect companyto turn FCF positive in FY12E and debt-equity ratio to increase from 0.8x in FY09 to 1.4x inFY10E and then again decline to 0.9x in FY12E.

Key Concerns:

Unfavourable judgement in legal case against Dutch spirit company UTO

Increase in key input prices

Concentration of revenue in Southern Region

Valuations: At the current price, the company is trading at 8.4x and 6.2x FY11E and FY12Eearnings and 5.7x and 4.3x FY11E and FY12E EV/EBITDA respectively. We initiate coverageon the company with BUY recommendation and price target of INR 232 (average of targetFY12E EV/EBITDA of 5.5x and FY12E P/E of 8.0x).

Sunny AgrawalAnalystTel. : 4000 [email protected]

April 16, 2010

For Private Circulation OnlyFINQUEST research also available on BLOOMBERG FSPL <GO> and REUTERS.

Financials F09 F10E* F11E(INR Mn.)

Net Sales 2369.7 4108.6 7631.1

EBITDA 437.2 792.9 1527.1

EPS 19.1 10.4 20.6

P/E 9.0 16.5 8.4* Issued Bonus in ratio of 2:1 and accountedfor conversion of all CCPS and Warrantsissued till FY10E end

For Private Circulation OnlyApril 16, 2010 2

Particulars ( INR million ) F09 F10E* F11E F12E

Valuation RatiosP/E 9.0 16.5 8.4 6.2EV/EBITDA 5.0 10.3 5.7 4.3P/BV 1.3 2.6 2.1 1.6Dividend Yield (%) 1.5 1.5 1.5 1.5

Per Share Data (INR)EPS 19.1 10.4 20.6 27.7Cash EPS 21.7 12.9 26.9 35.1BVPS 133.7 65.4 83.1 107.9DPS 2.5 2.5 2.5 2.5

P&L (INR mn)Net Sales 2369.7 4108.6 7631.1 9658.3Operating Expenses 1932.4 3315.7 6104.1 7697.8EBITDA 437.2 792.9 1527.1 1960.5PBIT 434.7 738.9 1354.3 1745.4Interest Expense 105.6 217.6 325.0 357.5PBT 329.0 521.3 1029.3 1387.9Tax 116.5 184.5 364.4 491.3PAT 212.5 336.8 664.9 896.6Extra Ordinary items 0.0 0.0 0.0 0.0Adjusted PAT 212.5 336.8 664.9 896.6

Growth rates (%)Net Sales 62.9 73.4 85.7 26.6EBITDA 41.2 81.3 92.6 28.4EBIT 44.4 70.0 83.3 28.9EPS-Diluted 20.7 -45.5 97.4 34.8

Balance Sheet (INR mn)Net worth 1483.8 2114.1 2684.6 3486.7Total Debt 1251.3 3000.0 3500.0 3000.0Creditors 482.5 833.0 1547.1 1958.1Total Liabilities 2792.5 5171.5 6242.0 6544.1Net Fixed Assets 1652.3 3572.8 4167.8 4528.9Cash & Cash Equivalents 43.1 363.3 384.4 83.8Debtors 606.0 1046.8 1944.4 2460.9Total assets 2792.5 5171.5 6242.0 6544.1

Cash Flow (INR mn)PAT 212.5 336.8 664.9 896.6Depreciation 28.9 79.5 205.1 238.8Operating Cash Flow -194.6 277.9 415.7 893.8Capital Expenses 491.2 2000.0 800.0 600.0Chg in Investments 31.4 0.0 0.0 0.0Investing Cash Flow -522.6 -2000.0 -800.0 -600.0Debt raised/(repaid) 674.5 1748.7 500.0 -500.0Dividend Paid 739.9 2042.2 405.5 -594.5Financing Cash Flow 739.9 2042.2 405.5 -594.5

Profitability/Solvency Ratios (%)EBITDA Margin 18.5 19.3 20.0 20.3ROCE 8.6 7.8 12.6 16.5ROE 14.3 15.9 24.8 25.7Debt to Equity 84.3 141.9 130.4 86.0Interest Coverage Ratio 411.4 339.6 416.7 488.2* Issued Bonus in ratio of 2:1 and accounted for conversion of all CCPS and Warrants issued till FY10E end

Company Description

TI is one of the leading players in the Indian

alcoholic beverage industry and manufactures

Indian Made Foreign Liquor (IMFL), with over

16 brands across a diverse range of price and

product segments. TI's primary manufacturing

facility is located in at Shrirampur, Maharashtra.

Currently, the company has 100 KLPD molasses

based and 100 KLPD grain based distillery. The

company commands 4% of domestic IMFL

market.

www.tilind.com

Sector

Alcoholic Beverage

Key Management Personnel

Mr. Amit Dahanukar

MD & Chairman

Mrs. Shivani A Dahanukar

Executive Director

Mr. Lalit Sethi

CFO

PRICE PERFORMANCE (%)

3 M 6 M 12 M

Absolute 1.8 3.4 62.5

Relative (55.9) (129.7) (378.0)

Valuation Thesis

At CMP, the company is trading at 8.4x and 6.2x

FY11E and FY12E earnings and 5.7x and 4.3x

FY11E and FY12E EV/EBITDA respectively. We

recommend BUY rating with price target of INR

232 (average of target FY12E EV/EBITDA of 5.5x

and FY12E P/E of 8.0x).

Financial Summary

For Private Circulation OnlyApril 16, 2010 3

Investment Rationale

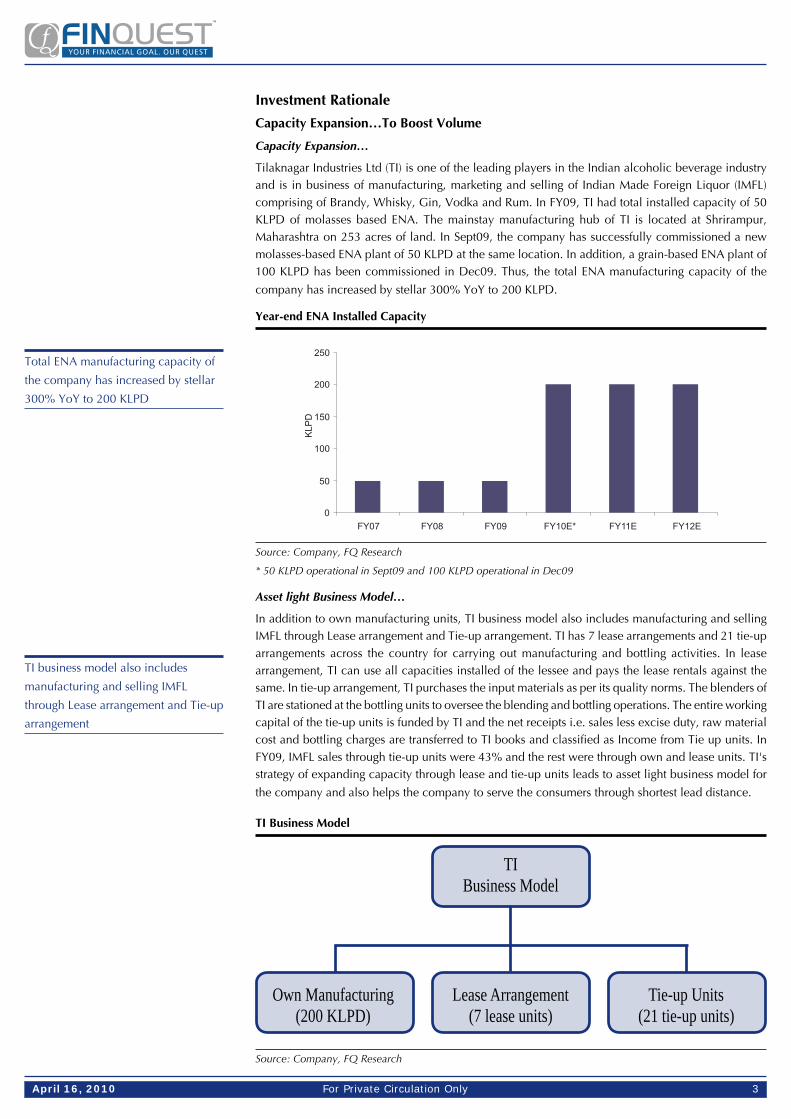

Capacity Expansion…To Boost Volume

Capacity Expansion…

Tilaknagar Industries Ltd (TI) is one of the leading players in the Indian alcoholic beverage industryand is in business of manufacturing, marketing and selling of Indian Made Foreign Liquor (IMFL)comprising of Brandy, Whisky, Gin, Vodka and Rum. In FY09, TI had total installed capacity of 50KLPD of molasses based ENA. The mainstay manufacturing hub of TI is located at Shrirampur,Maharashtra on 253 acres of land. In Sept09, the company has successfully commissioned a newmolasses-based ENA plant of 50 KLPD at the same location. In addition, a grain-based ENA plant of100 KLPD has been commissioned in Dec09. Thus, the total ENA manufacturing capacity of the

company has increased by stellar 300% YoY to 200 KLPD.

Year-end ENA Installed Capacity

Source: Company, FQ Research

* 50 KLPD operational in Sept09 and 100 KLPD operational in Dec09

Asset light Business Model…

In addition to own manufacturing units, TI business model also includes manufacturing and sellingIMFL through Lease arrangement and Tie-up arrangement. TI has 7 lease arrangements and 21 tie-uparrangements across the country for carrying out manufacturing and bottling activities. In leasearrangement, TI can use all capacities installed of the lessee and pays the lease rentals against thesame. In tie-up arrangement, TI purchases the input materials as per its quality norms. The blenders ofTI are stationed at the bottling units to oversee the blending and bottling operations. The entire workingcapital of the tie-up units is funded by TI and the net receipts i.e. sales less excise duty, raw materialcost and bottling charges are transferred to TI books and classified as Income from Tie up units. InFY09, IMFL sales through tie-up units were 43% and the rest were through own and lease units. TI'sstrategy of expanding capacity through lease and tie-up units leads to asset light business model for

the company and also helps the company to serve the consumers through shortest lead distance.

TI Business Model

Source: Company, FQ Research

TIBusiness Model

Own Manufacturing Lease Arrangement Tie-up Units(200 KLPD) (7 lease units) (21 tie-up units)

Total ENA manufacturing capacity of

the company has increased by stellar

300% YoY to 200 KLPD

TI business model also includes

manufacturing and selling IMFL

through Lease arrangement and Tie-up

arrangement

For Private Circulation OnlyApril 16, 2010 4

Well-established brands…Stellar Volume Growth

The company sells its IMFL products under its well-established brand. The Brandy is sold under brand

name of Mansion House, Courrier Napoleon, Master's Doctor and Senate whereas Whisky is sold

under brand name of Senate Royale, Mansion House, Shot, Classic, Royal Choice, Hottt Silk and

Castle Club. In fact, Mansion House won the "Brandy of the Year" award for 2009 at INDSPIRIT 2009.

Including other well-established brands for Rum, Vodka and Gin, the company has over 16 brands

across the diverse range of price and product segments and caters to economy, semi-premium and

premium category of the market.

TI's and Competitors Brand

Products TI's Brand Competitors Brand

Brandy Mansion, Courrier Napoleon, McDowell's, Honey Bee, Old English,

Master's Doctor, Senate Napolean, Bio

Whisky Senate Royale, Mansion House, Shot, Imperial Blue, Red Knight, DSP Black,

Classic, Royal Choice, Hottt Silk, AC Premium, Raffles

Castle Club

Rum Savoy Club, Royal Choice, Madira, Old Monk, Celebration, Hercules, 8 PM,

Castle Club, Senate, Shot Rock Carta Blanka

Gin Savoy Club Dry Gin, Royal Choice, Blue Ribbon, White Lace, Premium Blue,

Duet Gin, Mansion House Royal Choice, SRK Superior

Vodka Classic Vodka, Castle Club Vodka Karmazov Rare, White Mischief, Romanov,

MGM Apple, Magic Moments

Source: Company, FQ Research

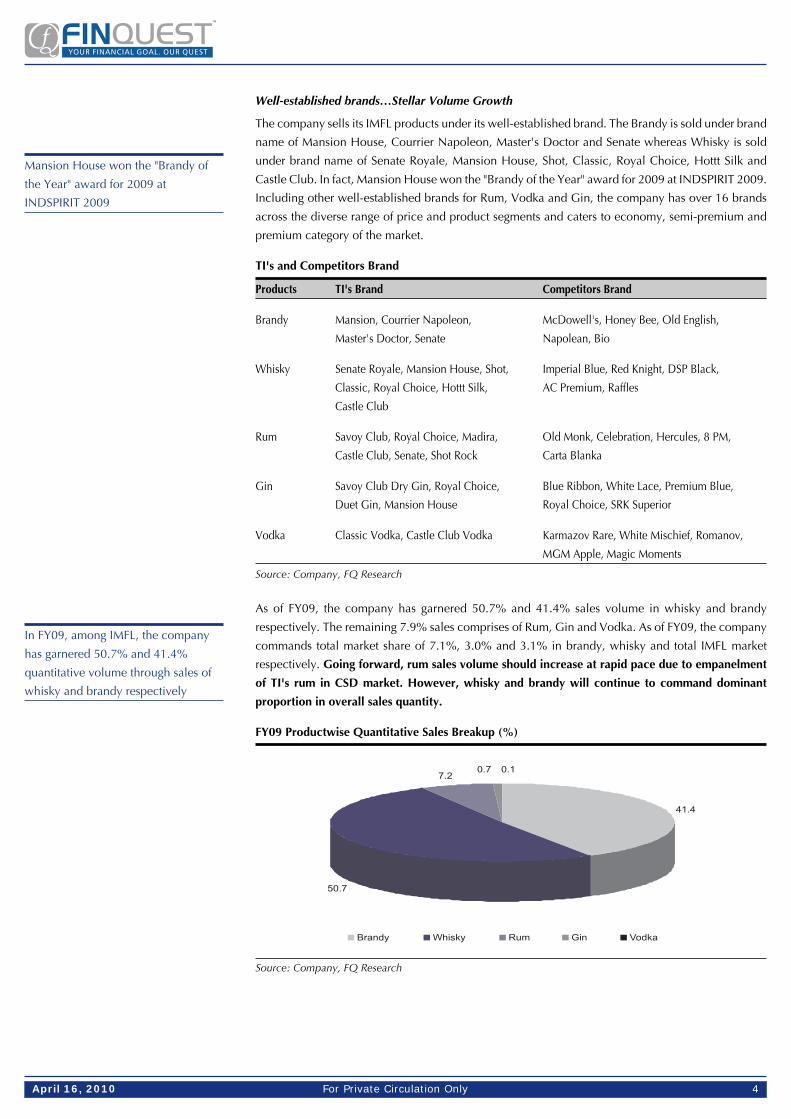

As of FY09, the company has garnered 50.7% and 41.4% sales volume in whisky and brandy

respectively. The remaining 7.9% sales comprises of Rum, Gin and Vodka. As of FY09, the company

commands total market share of 7.1%, 3.0% and 3.1% in brandy, whisky and total IMFL market

respectively. Going forward, rum sales volume should increase at rapid pace due to empanelment

of TI's rum in CSD market. However, whisky and brandy will continue to command dominant

proportion in overall sales quantity.

FY09 Productwise Quantitative Sales Breakup (%)

Source: Company, FQ Research

Mansion House won the "Brandy of

the Year" award for 2009 at

INDSPIRIT 2009

In FY09, among IMFL, the company

has garnered 50.7% and 41.4%

quantitative volume through sales of

whisky and brandy respectively

For Private Circulation OnlyApril 16, 2010 5

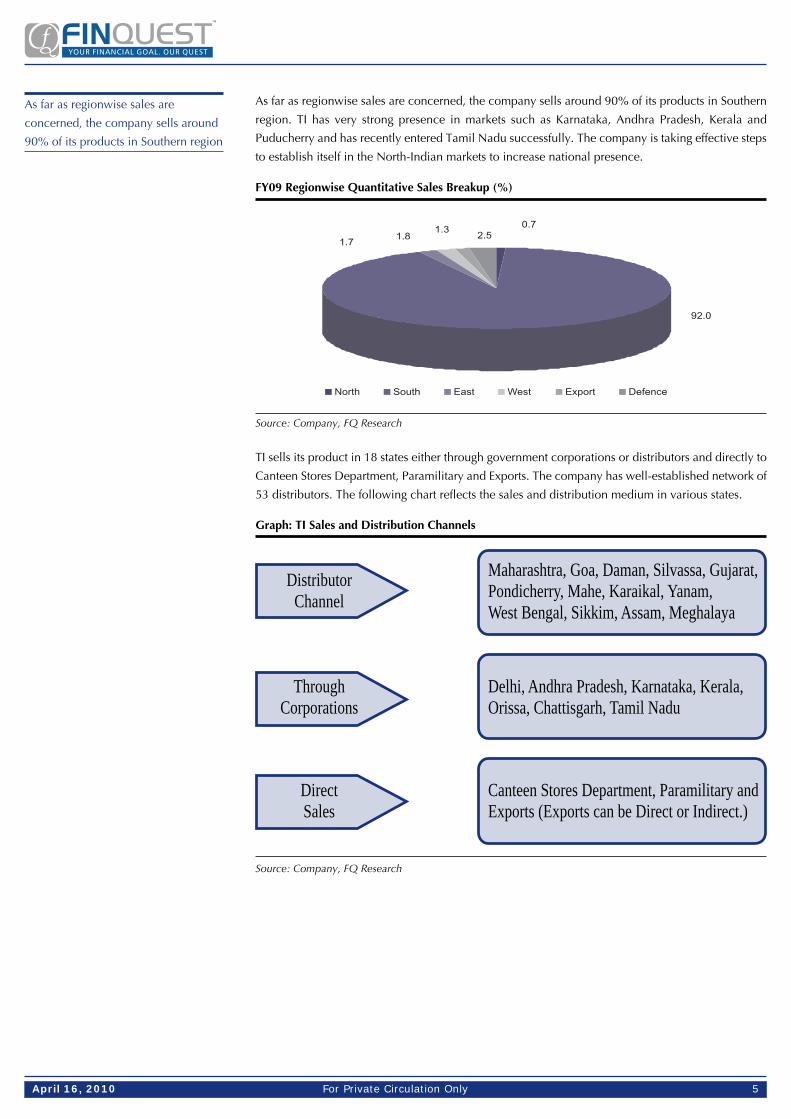

As far as regionwise sales are concerned, the company sells around 90% of its products in Southern

region. TI has very strong presence in markets such as Karnataka, Andhra Pradesh, Kerala and

Puducherry and has recently entered Tamil Nadu successfully. The company is taking effective steps

to establish itself in the North-Indian markets to increase national presence.

FY09 Regionwise Quantitative Sales Breakup (%)

Source: Company, FQ Research

TI sells its product in 18 states either through government corporations or distributors and directly to

Canteen Stores Department, Paramilitary and Exports. The company has well-established network of

53 distributors. The following chart reflects the sales and distribution medium in various states.

Graph: TI Sales and Distribution Channels

Source: Company, FQ Research

ThroughCorporations

Delhi, Andhra Pradesh, Karnataka, Kerala,Orissa, Chattisgarh, Tamil Nadu

DirectSales

Canteen Stores Department, Paramilitary andExports (Exports can be Direct or Indirect.)

DistributorChannel

Maharashtra, Goa, Daman, Silvassa, Gujarat,Pondicherry, Mahe, Karaikal, Yanam,West Bengal, Sikkim, Assam, Meghalaya

As far as regionwise sales are

concerned, the company sells around

90% of its products in Southern region

For Private Circulation OnlyApril 16, 2010 6

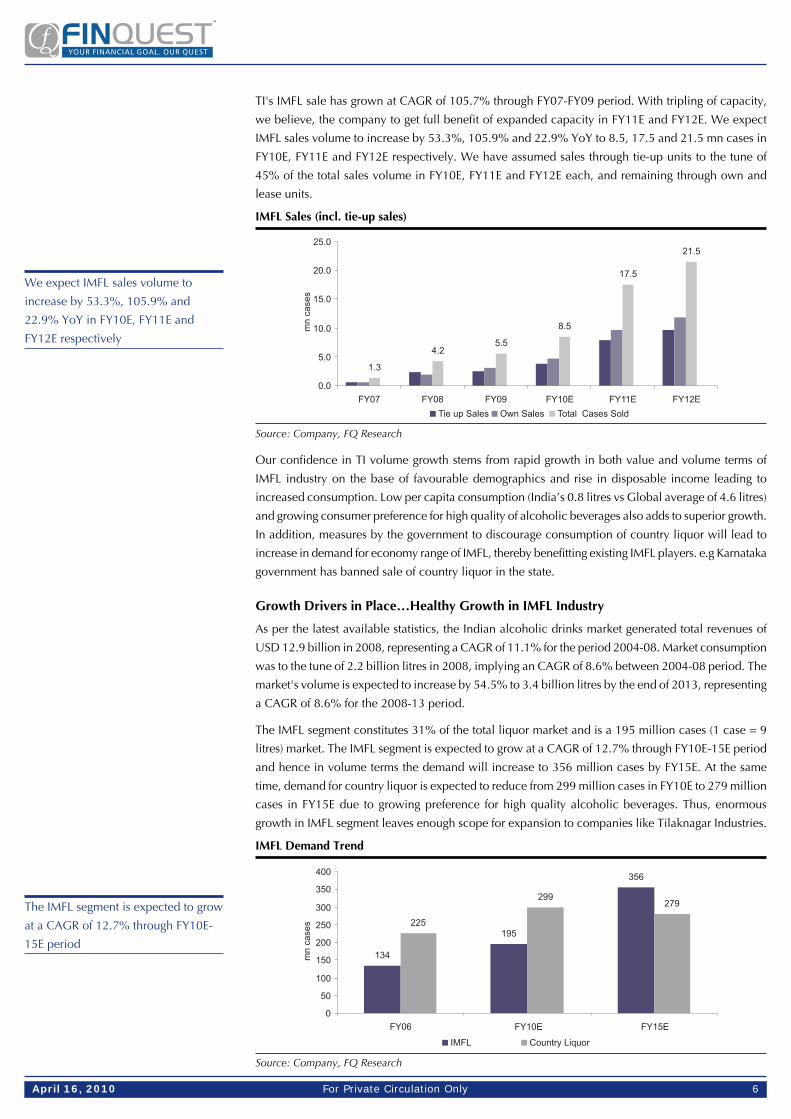

TI's IMFL sale has grown at CAGR of 105.7% through FY07-FY09 period. With tripling of capacity,

we believe, the company to get full benefit of expanded capacity in FY11E and FY12E. We expect

IMFL sales volume to increase by 53.3%, 105.9% and 22.9% YoY to 8.5, 17.5 and 21.5 mn cases in

FY10E, FY11E and FY12E respectively. We have assumed sales through tie-up units to the tune of

45% of the total sales volume in FY10E, FY11E and FY12E each, and remaining through own and

lease units.

IMFL Sales (incl. tie-up sales)

Source: Company, FQ Research

Our confidence in TI volume growth stems from rapid growth in both value and volume terms of

IMFL industry on the base of favourable demographics and rise in disposable income leading to

increased consumption. Low per capita consumption (India’s 0.8 litres vs Global average of 4.6 litres)

and growing consumer preference for high quality of alcoholic beverages also adds to superior growth.

In addition, measures by the government to discourage consumption of country liquor will lead to

increase in demand for economy range of IMFL, thereby benefitting existing IMFL players. e.g Karnataka

government has banned sale of country liquor in the state.

Growth Drivers in Place…Healthy Growth in IMFL Industry

As per the latest available statistics, the Indian alcoholic drinks market generated total revenues of

USD 12.9 billion in 2008, representing a CAGR of 11.1% for the period 2004-08. Market consumption

was to the tune of 2.2 billion litres in 2008, implying an CAGR of 8.6% between 2004-08 period. The

market's volume is expected to increase by 54.5% to 3.4 billion litres by the end of 2013, representing

a CAGR of 8.6% for the 2008-13 period.

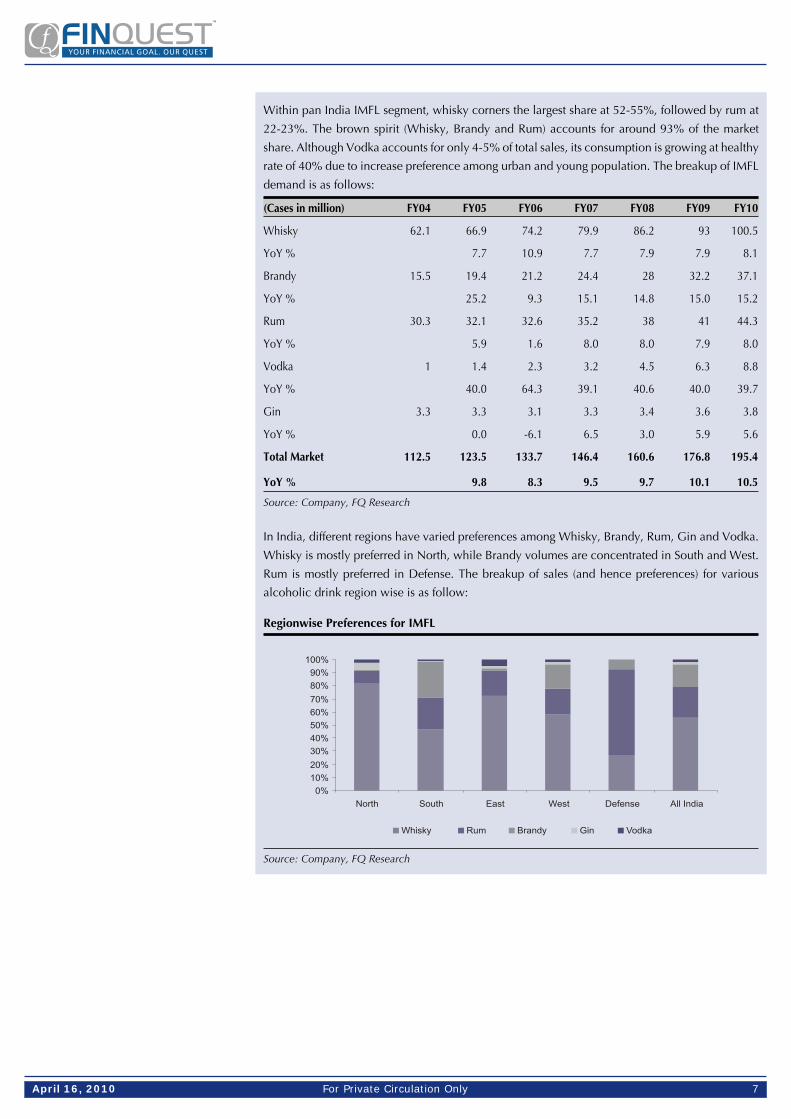

The IMFL segment constitutes 31% of the total liquor market and is a 195 million cases (1 case = 9

litres) market. The IMFL segment is expected to grow at a CAGR of 12.7% through FY10E-15E period

and hence in volume terms the demand will increase to 356 million cases by FY15E. At the same

time, demand for country liquor is expected to reduce from 299 million cases in FY10E to 279 million

cases in FY15E due to growing preference for high quality alcoholic beverages. Thus, enormous

growth in IMFL segment leaves enough scope for expansion to companies like Tilaknagar Industries.

IMFL Demand Trend

Source: Company, FQ Research

We expect IMFL sales volume to

increase by 53.3%, 105.9% and

22.9% YoY in FY10E, FY11E and

FY12E respectively

The IMFL segment is expected to grow

at a CAGR of 12.7% through FY10E-

15E period

For Private Circulation OnlyApril 16, 2010 7

Within pan India IMFL segment, whisky corners the largest share at 52-55%, followed by rum at

22-23%. The brown spirit (Whisky, Brandy and Rum) accounts for around 93% of the market

share. Although Vodka accounts for only 4-5% of total sales, its consumption is growing at healthy

rate of 40% due to increase preference among urban and young population. The breakup of IMFL

demand is as follows:

(Cases in million) FY04 FY05 FY06 FY07 FY08 FY09 FY10

Whisky 62.1 66.9 74.2 79.9 86.2 93 100.5

YoY % 7.7 10.9 7.7 7.9 7.9 8.1

Brandy 15.5 19.4 21.2 24.4 28 32.2 37.1

YoY % 25.2 9.3 15.1 14.8 15.0 15.2

Rum 30.3 32.1 32.6 35.2 38 41 44.3

YoY % 5.9 1.6 8.0 8.0 7.9 8.0

Vodka 1 1.4 2.3 3.2 4.5 6.3 8.8

YoY % 40.0 64.3 39.1 40.6 40.0 39.7

Gin 3.3 3.3 3.1 3.3 3.4 3.6 3.8

YoY % 0.0 -6.1 6.5 3.0 5.9 5.6

Total Market 112.5 123.5 133.7 146.4 160.6 176.8 195.4

YoY % 9.8 8.3 9.5 9.7 10.1 10.5

Source: Company, FQ Research

In India, different regions have varied preferences among Whisky, Brandy, Rum, Gin and Vodka.

Whisky is mostly preferred in North, while Brandy volumes are concentrated in South and West.

Rum is mostly preferred in Defense. The breakup of sales (and hence preferences) for various

alcoholic drink region wise is as follow:

Regionwise Preferences for IMFL

Source: Company, FQ Research

For Private Circulation OnlyApril 16, 2010 8

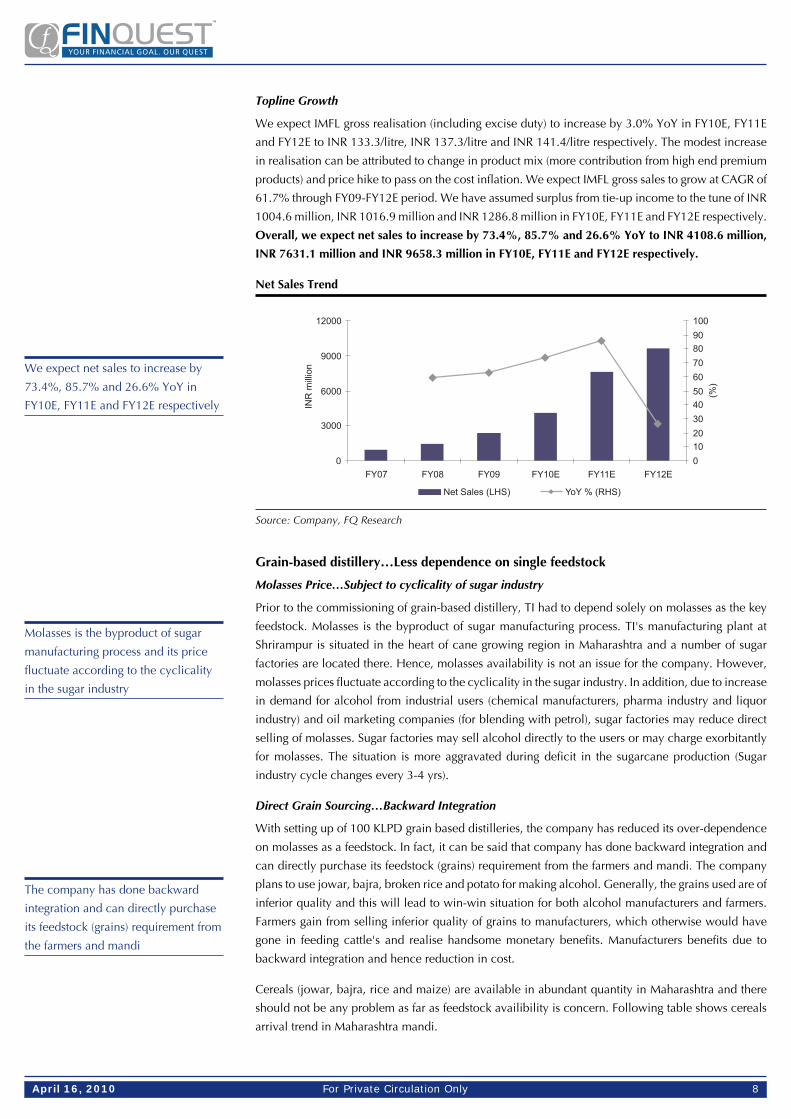

Topline Growth

We expect IMFL gross realisation (including excise duty) to increase by 3.0% YoY in FY10E, FY11E

and FY12E to INR 133.3/litre, INR 137.3/litre and INR 141.4/litre respectively. The modest increase

in realisation can be attributed to change in product mix (more contribution from high end premium

products) and price hike to pass on the cost inflation. We expect IMFL gross sales to grow at CAGR of

61.7% through FY09-FY12E period. We have assumed surplus from tie-up income to the tune of INR

1004.6 million, INR 1016.9 million and INR 1286.8 million in FY10E, FY11E and FY12E respectively.

Overall, we expect net sales to increase by 73.4%, 85.7% and 26.6% YoY to INR 4108.6 million,

INR 7631.1 million and INR 9658.3 million in FY10E, FY11E and FY12E respectively.

Net Sales Trend

Source: Company, FQ Research

Grain-based distillery…Less dependence on single feedstock

Molasses Price…Subject to cyclicality of sugar industry

Prior to the commissioning of grain-based distillery, TI had to depend solely on molasses as the key

feedstock. Molasses is the byproduct of sugar manufacturing process. TI's manufacturing plant at

Shrirampur is situated in the heart of cane growing region in Maharashtra and a number of sugar

factories are located there. Hence, molasses availability is not an issue for the company. However,

molasses prices fluctuate according to the cyclicality in the sugar industry. In addition, due to increase

in demand for alcohol from industrial users (chemical manufacturers, pharma industry and liquor

industry) and oil marketing companies (for blending with petrol), sugar factories may reduce direct

selling of molasses. Sugar factories may sell alcohol directly to the users or may charge exorbitantly

for molasses. The situation is more aggravated during deficit in the sugarcane production (Sugar

industry cycle changes every 3-4 yrs).

Direct Grain Sourcing…Backward Integration

With setting up of 100 KLPD grain based distilleries, the company has reduced its over-dependence

on molasses as a feedstock. In fact, it can be said that company has done backward integration and

can directly purchase its feedstock (grains) requirement from the farmers and mandi. The company

plans to use jowar, bajra, broken rice and potato for making alcohol. Generally, the grains used are of

inferior quality and this will lead to win-win situation for both alcohol manufacturers and farmers.

Farmers gain from selling inferior quality of grains to manufacturers, which otherwise would have

gone in feeding cattle's and realise handsome monetary benefits. Manufacturers benefits due to

backward integration and hence reduction in cost.

Cereals (jowar, bajra, rice and maize) are available in abundant quantity in Maharashtra and there

should not be any problem as far as feedstock availibility is concern. Following table shows cereals

arrival trend in Maharashtra mandi.

We expect net sales to increase by

73.4%, 85.7% and 26.6% YoY in

FY10E, FY11E and FY12E respectively

Molasses is the byproduct of sugar

manufacturing process and its price

fluctuate according to the cyclicality

in the sugar industry

The company has done backward

integration and can directly purchase

its feedstock (grains) requirement from

the farmers and mandi

For Private Circulation OnlyApril 16, 2010 9

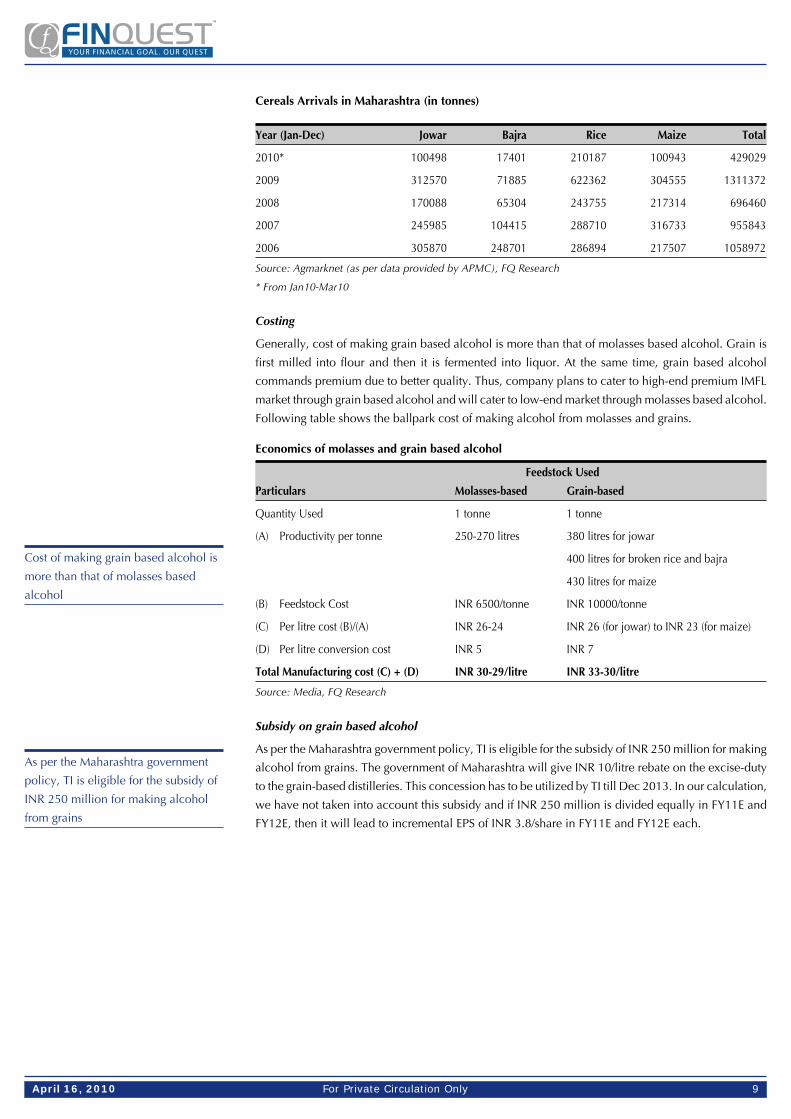

Cereals Arrivals in Maharashtra (in tonnes)

Year (Jan-Dec) Jowar Bajra Rice Maize Total

2010* 100498 17401 210187 100943 429029

2009 312570 71885 622362 304555 1311372

2008 170088 65304 243755 217314 696460

2007 245985 104415 288710 316733 955843

2006 305870 248701 286894 217507 1058972

Source: Agmarknet (as per data provided by APMC), FQ Research

* From Jan10-Mar10

Costing

Generally, cost of making grain based alcohol is more than that of molasses based alcohol. Grain is

first milled into flour and then it is fermented into liquor. At the same time, grain based alcohol

commands premium due to better quality. Thus, company plans to cater to high-end premium IMFL

market through grain based alcohol and will cater to low-end market through molasses based alcohol.

Following table shows the ballpark cost of making alcohol from molasses and grains.

Economics of molasses and grain based alcohol

Feedstock Used

Particulars Molasses-based Grain-based

Quantity Used 1 tonne 1 tonne

(A) Productivity per tonne 250-270 litres 380 litres for jowar

400 litres for broken rice and bajra

430 litres for maize

(B) Feedstock Cost INR 6500/tonne INR 10000/tonne

(C) Per litre cost (B)/(A) INR 26-24 INR 26 (for jowar) to INR 23 (for maize)

(D) Per litre conversion cost INR 5 INR 7

Total Manufacturing cost (C) + (D) INR 30-29/litre INR 33-30/litre

Source: Media, FQ Research

Subsidy on grain based alcohol

As per the Maharashtra government policy, TI is eligible for the subsidy of INR 250 million for making

alcohol from grains. The government of Maharashtra will give INR 10/litre rebate on the excise-duty

to the grain-based distilleries. This concession has to be utilized by TI till Dec 2013. In our calculation,

we have not taken into account this subsidy and if INR 250 million is divided equally in FY11E and

FY12E, then it will lead to incremental EPS of INR 3.8/share in FY11E and FY12E each.

Cost of making grain based alcohol is

more than that of molasses based

alcohol

As per the Maharashtra government

policy, TI is eligible for the subsidy of

INR 250 million for making alcohol

from grains

For Private Circulation OnlyApril 16, 2010 10

Margins to improve…

Sugar Cycle….in reverse gear

During SY09 (Oct08-Sept09), India's sugar production declined to 14.5 million tonnes against the

demand of 22.5 million tonnes. In SY10 (Oct09-Sept10), the sugar production is expected to be

higher at 16-17 million tonnes. However, it will be way below the expected demand of 23.0 million

tonnes. In the wake of cane sourcing competition between sugar mills and gur/khandsari players in

SY10, sugar mills have paid exorbitant cane price of INR 240-280/quintal against fair and remunerative

price of 129/quintal fixed by central government. The exorbitant prices paid by sugar mills in SY10

has incentivize farmers to plant more cane and we expect sugarcane output and hence sugar production

to increase by 30-35% YoY in SY11 (Oct10-Sept11). Molasses availability (being directly linked to

sugarcane output) is also expected to increase proportionately.

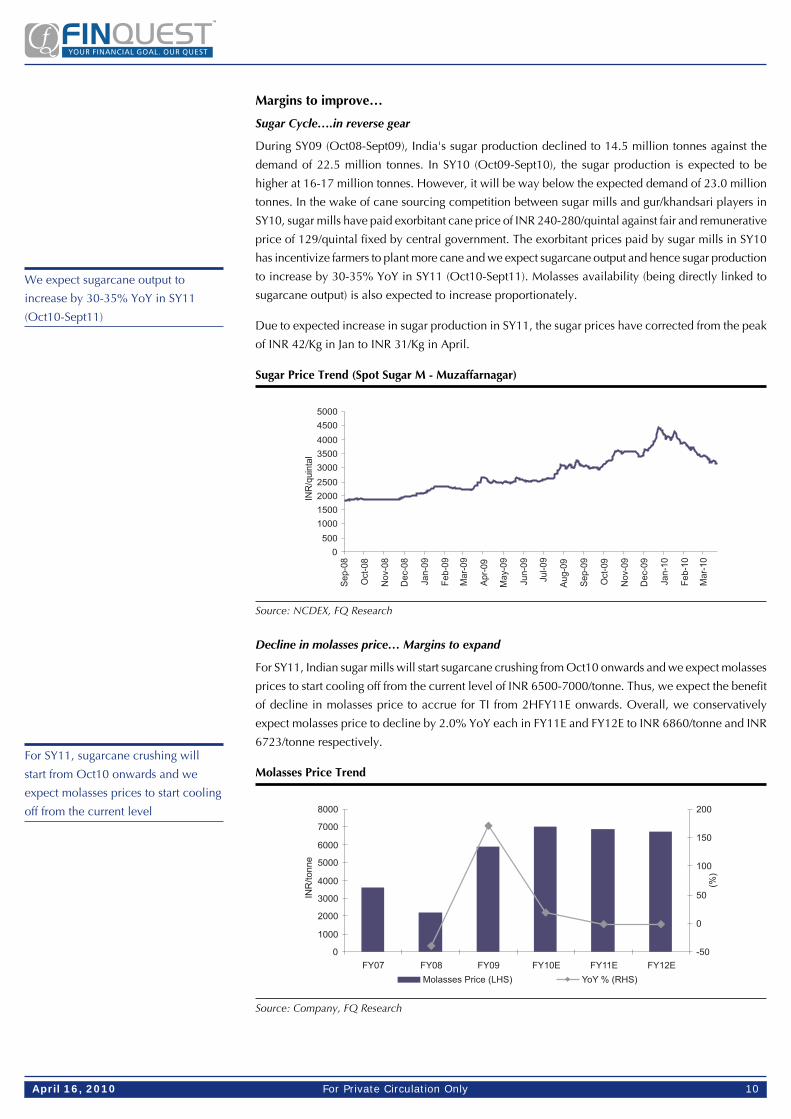

Due to expected increase in sugar production in SY11, the sugar prices have corrected from the peak

of INR 42/Kg in Jan to INR 31/Kg in April.

Sugar Price Trend (Spot Sugar M - Muzaffarnagar)

Source: NCDEX, FQ Research

Decline in molasses price… Margins to expand

For SY11, Indian sugar mills will start sugarcane crushing from Oct10 onwards and we expect molasses

prices to start cooling off from the current level of INR 6500-7000/tonne. Thus, we expect the benefit

of decline in molasses price to accrue for TI from 2HFY11E onwards. Overall, we conservatively

expect molasses price to decline by 2.0% YoY each in FY11E and FY12E to INR 6860/tonne and INR

6723/tonne respectively.

Molasses Price Trend

Source: Company, FQ Research

We expect sugarcane output to

increase by 30-35% YoY in SY11

(Oct10-Sept11)

For SY11, sugarcane crushing will

start from Oct10 onwards and we

expect molasses prices to start cooling

off from the current level

For Private Circulation OnlyApril 16, 2010 11

As far as manufacturing alcohol from grains is concerned, the company doesn't have any operational

history. In our calculation, we have assumed that the company will be using mainly jowar along with

other grains as a feedstock. We have conservatively taken productivity of 380 litres of alcohol for

every tonne of grains processed in FY11E and FY12E each.

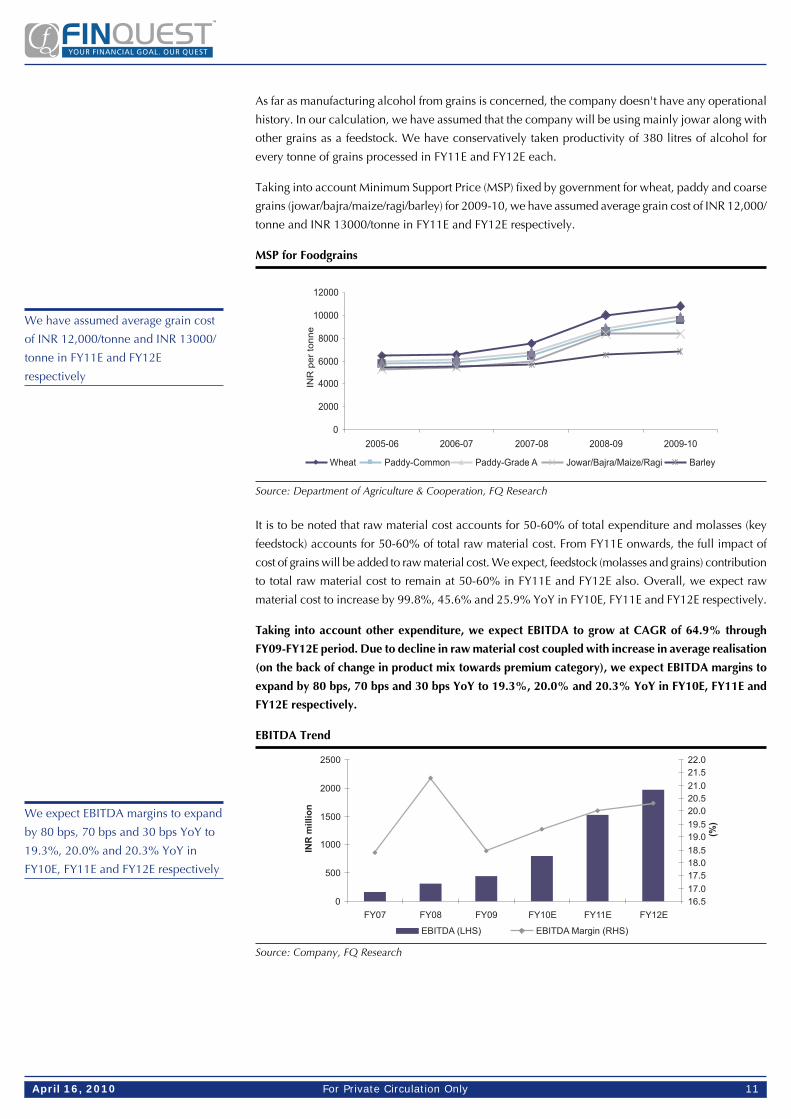

Taking into account Minimum Support Price (MSP) fixed by government for wheat, paddy and coarse

grains (jowar/bajra/maize/ragi/barley) for 2009-10, we have assumed average grain cost of INR 12,000/

tonne and INR 13000/tonne in FY11E and FY12E respectively.

MSP for Foodgrains

Source: Department of Agriculture & Cooperation, FQ Research

It is to be noted that raw material cost accounts for 50-60% of total expenditure and molasses (key

feedstock) accounts for 50-60% of total raw material cost. From FY11E onwards, the full impact of

cost of grains will be added to raw material cost. We expect, feedstock (molasses and grains) contribution

to total raw material cost to remain at 50-60% in FY11E and FY12E also. Overall, we expect raw

material cost to increase by 99.8%, 45.6% and 25.9% YoY in FY10E, FY11E and FY12E respectively.

Taking into account other expenditure, we expect EBITDA to grow at CAGR of 64.9% through

FY09-FY12E period. Due to decline in raw material cost coupled with increase in average realisation

(on the back of change in product mix towards premium category), we expect EBITDA margins to

expand by 80 bps, 70 bps and 30 bps YoY to 19.3%, 20.0% and 20.3% YoY in FY10E, FY11E and

FY12E respectively.

EBITDA Trend

Source: Company, FQ Research

We have assumed average grain cost

of INR 12,000/tonne and INR 13000/

tonne in FY11E and FY12E

respectively

We expect EBITDA margins to expand

by 80 bps, 70 bps and 30 bps YoY to

19.3%, 20.0% and 20.3% YoY in

FY10E, FY11E and FY12E respectively

For Private Circulation OnlyApril 16, 2010 12

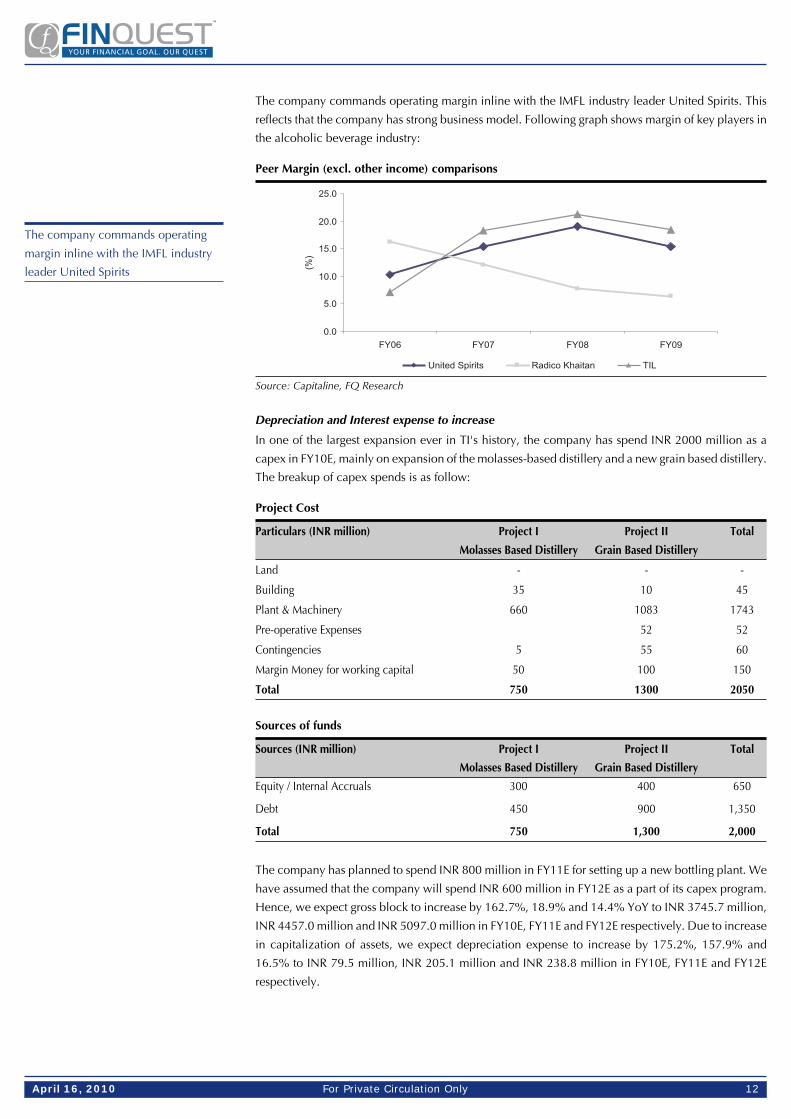

The company commands operating margin inline with the IMFL industry leader United Spirits. This

reflects that the company has strong business model. Following graph shows margin of key players in

the alcoholic beverage industry:

Peer Margin (excl. other income) comparisons

Source: Capitaline, FQ Research

Depreciation and Interest expense to increase

In one of the largest expansion ever in TI's history, the company has spend INR 2000 million as a

capex in FY10E, mainly on expansion of the molasses-based distillery and a new grain based distillery.

The breakup of capex spends is as follow:

Project Cost

Particulars (INR million) Project I Project II Total

Molasses Based Distillery Grain Based Distillery

Land - - -

Building 35 10 45

Plant & Machinery 660 1083 1743

Pre-operative Expenses 52 52

Contingencies 5 55 60

Margin Money for working capital 50 100 150

Total 750 1300 2050

Sources of funds

Sources (INR million) Project I Project II Total

Molasses Based Distillery Grain Based Distillery

Equity / Internal Accruals 300 400 650

Debt 450 900 1,350

Total 750 1,300 2,000

The company has planned to spend INR 800 million in FY11E for setting up a new bottling plant. We

have assumed that the company will spend INR 600 million in FY12E as a part of its capex program.

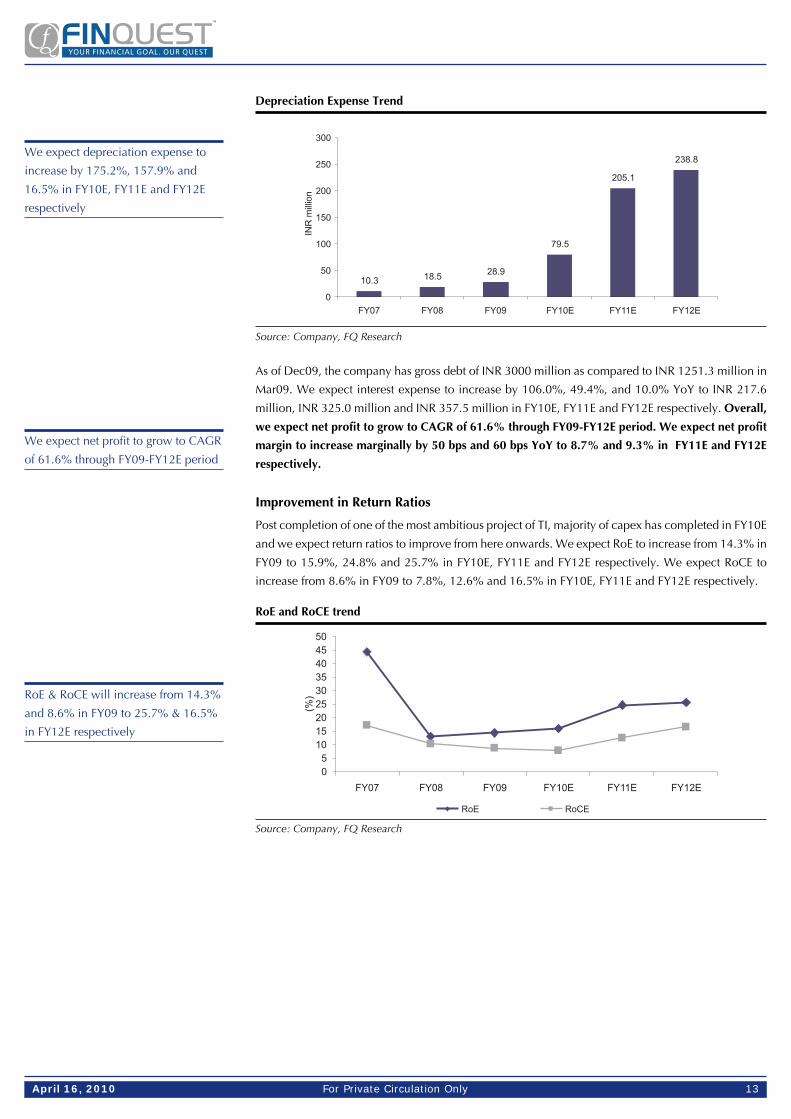

Hence, we expect gross block to increase by 162.7%, 18.9% and 14.4% YoY to INR 3745.7 million,

INR 4457.0 million and INR 5097.0 million in FY10E, FY11E and FY12E respectively. Due to increase

in capitalization of assets, we expect depreciation expense to increase by 175.2%, 157.9% and

16.5% to INR 79.5 million, INR 205.1 million and INR 238.8 million in FY10E, FY11E and FY12E

respectively.

The company commands operating

margin inline with the IMFL industry

leader United Spirits

For Private Circulation OnlyApril 16, 2010 13

Depreciation Expense Trend

Source: Company, FQ Research

As of Dec09, the company has gross debt of INR 3000 million as compared to INR 1251.3 million in

Mar09. We expect interest expense to increase by 106.0%, 49.4%, and 10.0% YoY to INR 217.6

million, INR 325.0 million and INR 357.5 million in FY10E, FY11E and FY12E respectively. Overall,

we expect net profit to grow to CAGR of 61.6% through FY09-FY12E period. We expect net profit

margin to increase marginally by 50 bps and 60 bps YoY to 8.7% and 9.3% in FY11E and FY12E

respectively.

Improvement in Return Ratios

Post completion of one of the most ambitious project of TI, majority of capex has completed in FY10E

and we expect return ratios to improve from here onwards. We expect RoE to increase from 14.3% in

FY09 to 15.9%, 24.8% and 25.7% in FY10E, FY11E and FY12E respectively. We expect RoCE to

increase from 8.6% in FY09 to 7.8%, 12.6% and 16.5% in FY10E, FY11E and FY12E respectively.

RoE and RoCE trend

Source: Company, FQ Research

We expect net profit to grow to CAGR

of 61.6% through FY09-FY12E period

We expect depreciation expense to

increase by 175.2%, 157.9% and

16.5% in FY10E, FY11E and FY12E

respectively

RoE & RoCE will increase from 14.3%

and 8.6% in FY09 to 25.7% & 16.5%

in FY12E respectively

For Private Circulation OnlyApril 16, 2010 14

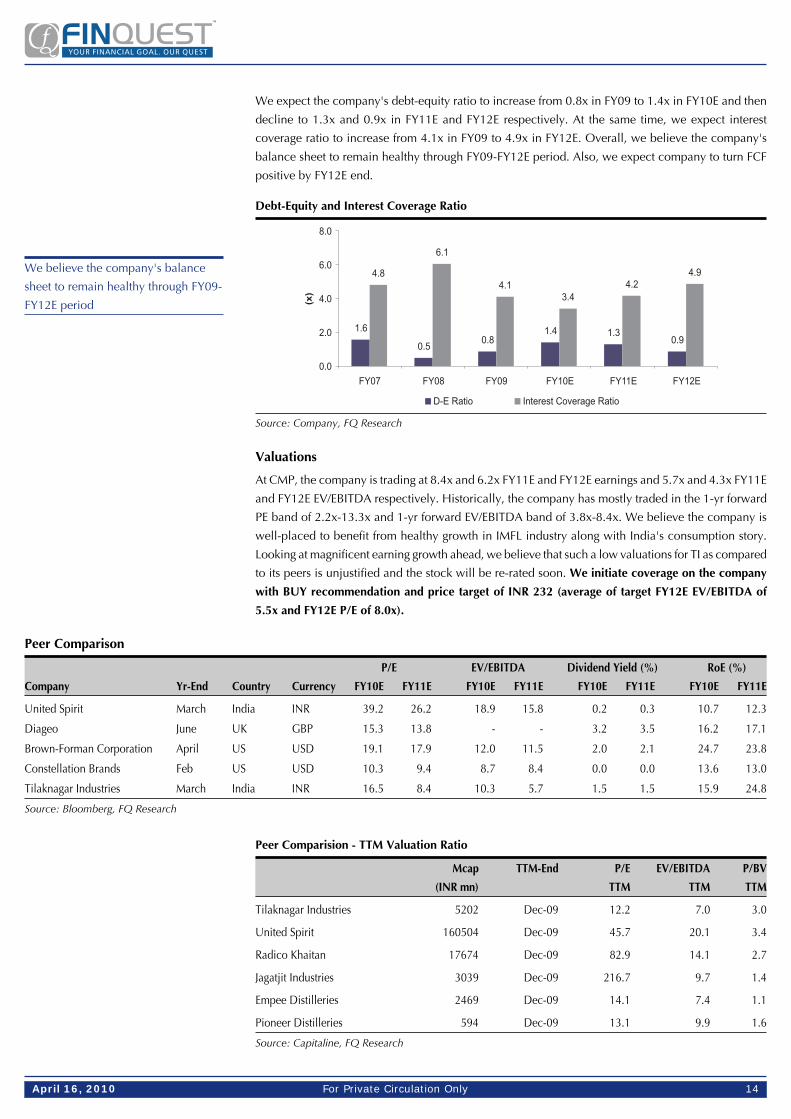

We expect the company's debt-equity ratio to increase from 0.8x in FY09 to 1.4x in FY10E and then

decline to 1.3x and 0.9x in FY11E and FY12E respectively. At the same time, we expect interest

coverage ratio to increase from 4.1x in FY09 to 4.9x in FY12E. Overall, we believe the company's

balance sheet to remain healthy through FY09-FY12E period. Also, we expect company to turn FCF

positive by FY12E end.

Debt-Equity and Interest Coverage Ratio

Source: Company, FQ Research

Valuations

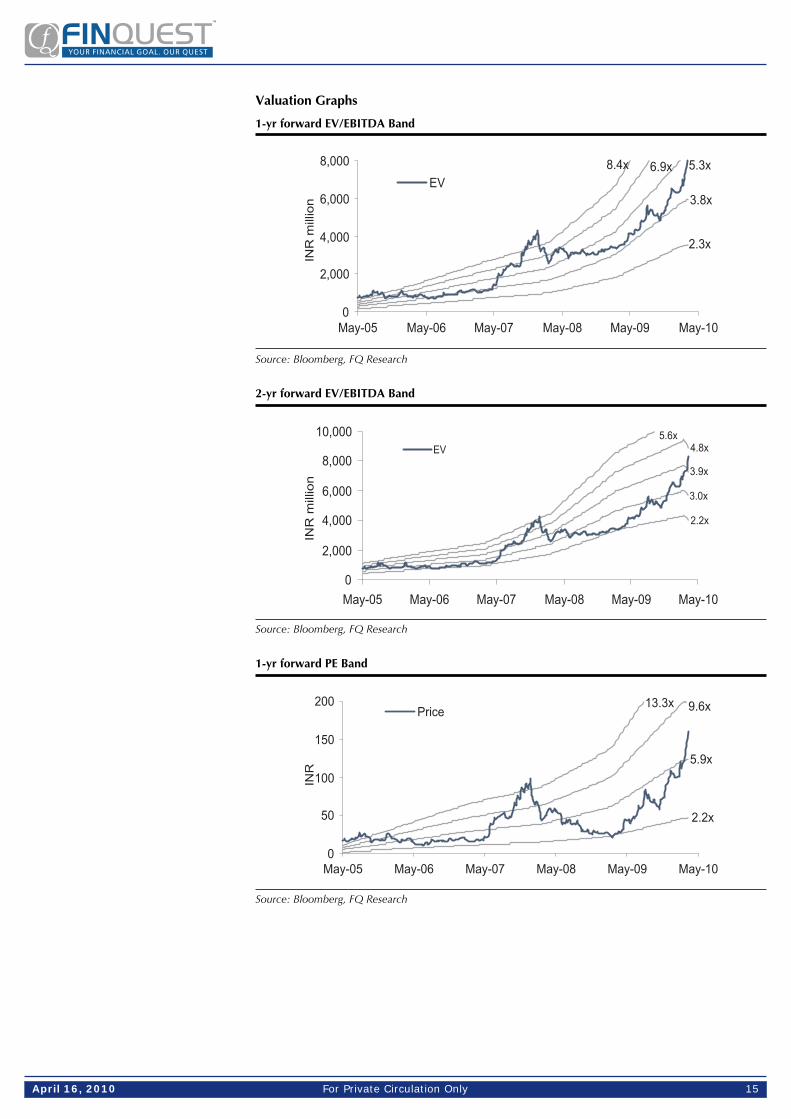

At CMP, the company is trading at 8.4x and 6.2x FY11E and FY12E earnings and 5.7x and 4.3x FY11E

and FY12E EV/EBITDA respectively. Historically, the company has mostly traded in the 1-yr forward

PE band of 2.2x-13.3x and 1-yr forward EV/EBITDA band of 3.8x-8.4x. We believe the company is

well-placed to benefit from healthy growth in IMFL industry along with India's consumption story.

Looking at magnificent earning growth ahead, we believe that such a low valuations for TI as compared

to its peers is unjustified and the stock will be re-rated soon. We initiate coverage on the company

with BUY recommendation and price target of INR 232 (average of target FY12E EV/EBITDA of

5.5x and FY12E P/E of 8.0x).

We believe the company's balance

sheet to remain healthy through FY09-

FY12E period

Peer Comparison

P/E EV/EBITDA Dividend Yield (%) RoE (%)

Company Yr-End Country Currency FY10E FY11E FY10E FY11E FY10E FY11E FY10E FY11E

United Spirit March India INR 39.2 26.2 18.9 15.8 0.2 0.3 10.7 12.3

Diageo June UK GBP 15.3 13.8 - - 3.2 3.5 16.2 17.1

Brown-Forman Corporation April US USD 19.1 17.9 12.0 11.5 2.0 2.1 24.7 23.8

Constellation Brands Feb US USD 10.3 9.4 8.7 8.4 0.0 0.0 13.6 13.0

Tilaknagar Industries March India INR 16.5 8.4 10.3 5.7 1.5 1.5 15.9 24.8

Source: Bloomberg, FQ Research

Peer Comparision - TTM Valuation Ratio

Mcap TTM-End P/E EV/EBITDA P/BV

(INR mn) TTM TTM TTM

Tilaknagar Industries 5202 Dec-09 12.2 7.0 3.0

United Spirit 160504 Dec-09 45.7 20.1 3.4

Radico Khaitan 17674 Dec-09 82.9 14.1 2.7

Jagatjit Industries 3039 Dec-09 216.7 9.7 1.4

Empee Distilleries 2469 Dec-09 14.1 7.4 1.1

Pioneer Distilleries 594 Dec-09 13.1 9.9 1.6

Source: Capitaline, FQ Research

For Private Circulation OnlyApril 16, 2010 15

Valuation Graphs

1-yr forward EV/EBITDA Band

Source: Bloomberg, FQ Research

2-yr forward EV/EBITDA Band

Source: Bloomberg, FQ Research

1-yr forward PE Band

Source: Bloomberg, FQ Research

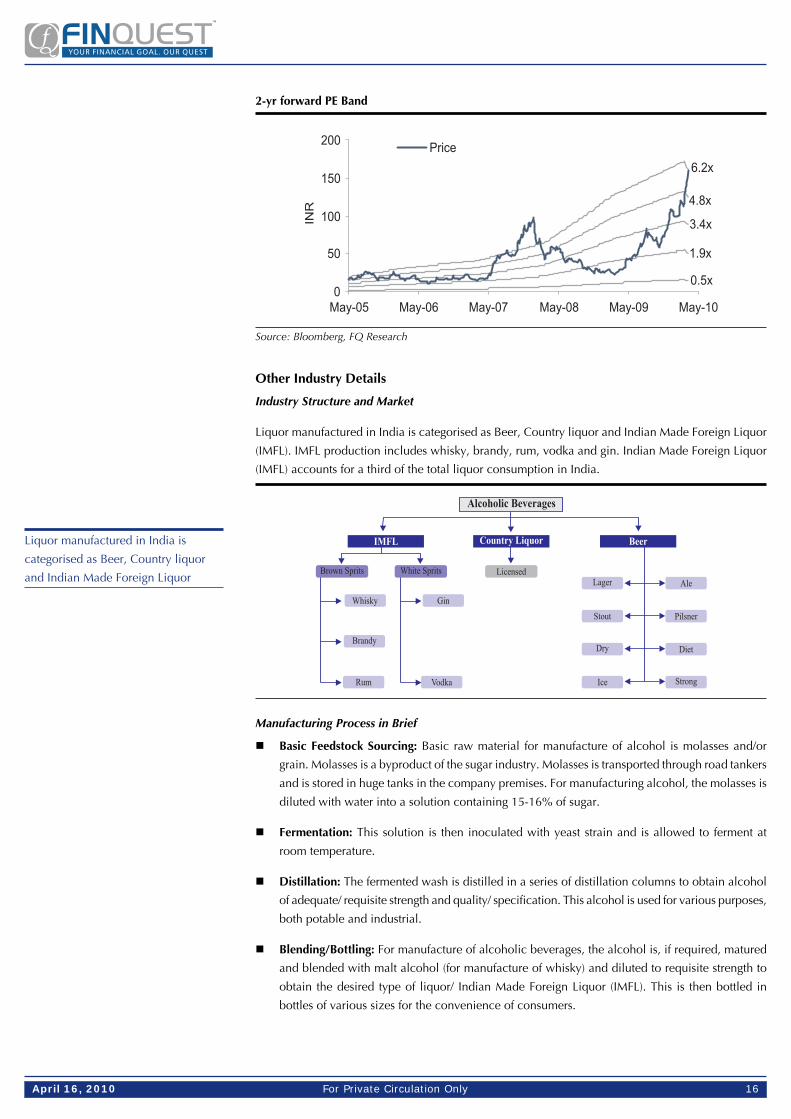

For Private Circulation OnlyApril 16, 2010 16

2-yr forward PE Band

Source: Bloomberg, FQ Research

Other Industry Details

Industry Structure and Market

Liquor manufactured in India is categorised as Beer, Country liquor and Indian Made Foreign Liquor

(IMFL). IMFL production includes whisky, brandy, rum, vodka and gin. Indian Made Foreign Liquor

(IMFL) accounts for a third of the total liquor consumption in India.

Manufacturing Process in Brief

Basic Feedstock Sourcing: Basic raw material for manufacture of alcohol is molasses and/or

grain. Molasses is a byproduct of the sugar industry. Molasses is transported through road tankers

and is stored in huge tanks in the company premises. For manufacturing alcohol, the molasses is

diluted with water into a solution containing 15-16% of sugar.

Fermentation: This solution is then inoculated with yeast strain and is allowed to ferment at

room temperature.

Distillation: The fermented wash is distilled in a series of distillation columns to obtain alcohol

of adequate/ requisite strength and quality/ specification. This alcohol is used for various purposes,

both potable and industrial.

Blending/Bottling: For manufacture of alcoholic beverages, the alcohol is, if required, matured

and blended with malt alcohol (for manufacture of whisky) and diluted to requisite strength to

obtain the desired type of liquor/ Indian Made Foreign Liquor (IMFL). This is then bottled in

bottles of various sizes for the convenience of consumers.

Liquor manufactured in India is

categorised as Beer, Country liquor

and Indian Made Foreign Liquor

For Private Circulation OnlyApril 16, 2010 17

Government Policies and Regulations…Entry Barriers for new entrants

Restriction on direct advertising: Direct advertising of alcoholic beverages is banned in India, curtailing

the attempts of global majors to make a strong entry. Promotions, sponsorships, surrogate advertising

done to build brands. E.g. TI sells packaged drinking water under brand name of Senate Royale

packaged drinking water, UB group sponsorship to majority of the teams in IPL and surrogate advertising

through Kingfisher mineral water etc. At the lower end of the market, brand promotion has been

mainly through retailer discounts.

Licensing: Licenses are required to set up a new manufacturing unit. While one can readily expand

existing units, getting a fresh license is cumbersome.

High taxes: Taxes and duties constitute nearly 45-50% of the final Consumer price. In addition to

excise duties imposed by various states, there are also high taxes on inter-state movement of liquor.

Each state levies taxation and duties on alcohol at its own decided rates. The duty structure of each

State is so different that for a company operating at the national level, it is like dealing with 25

countries.

High import duties: Imported liquor is subject to 100% import duty and 150% CV duty. The total

incidence of taxes on imported liquor increases significantly due to presence of numerous state level

taxes.

Existing strong brands: Strong consumer affinity with brands results in very high degree of repeat

purchase. E.g. Kingfisher, Signature Whisky, Mcdowell, Mansion House etc.

Difficulties in distribution: Each state regulates distribution channels of alcohol in its own way.

Distribution controls take various forms: Auctions, free-market system, government- controlled markets

(corporations) and canteen stores departments.

Under the auction system, the Government fixes a floor price for the shops and the bidders have to

quote prices. The license would go to the highest bidder and the bid price would have to be paid in

equated monthly installments. This system operates in Punjab, Rajasthan, Bihar, Orissa, Uttar Pradesh

and Madhya Pradesh. Since there are limited licences, unfair practices are rampant. Some distributors

bid for as many as ten shops at a time for greater control over the market. For instance, in Rajasthan,

12 groups control the wholesale and retail networks. In Uttar Pradesh, three major lobbies are said to

control 70 per cent of the trade in the State.

In the government-controlled system (corporation), the distribution of liquor is through state agencies

such as the TASMAC in Tamil Nadu, BEVCO in Kerala, the Andhra Pradesh Beverage Corporation in

AP, and the DSIDC in Delhi and so on. Since these agencies are sole wholesalers, they also have the

ultimate say in deciding on the entry of a brand into the State.

In a free-market system, there is no government intervention in the pricing and distribution of liquor.

The manufacturers sell liquor to the wholesaler/distributor who in turn sells it to the retail outlets.

Market forces determine pricing. The government issues wholesale/retail licenses for a fee.

Regionwise Overview

North

Constitutes around 25% of the total Alcohol drinks volume

Standard and economy brands continued to dominate less developed region of Uttaranchal and

Uttar Pradesh

Prospects:

Expected volume growth of 6.6% CAGR in total alcohol from the year 2010 - 2013

Deregulation of distribution and retail policies

Direct advertising of alcoholic

beverages is banned in India,

curtailing the attempts of global

majors to make a strong entry

Taxes and duties constitute nearly 45-

50% of the final Consumer price

Imported liquor is subject to 100%

import duty and 150% CV duty

Each state regulates distribution

channels of alcohol in its own way

For Private Circulation OnlyApril 16, 2010 18

South

Region with the highest consumption ~38% of India's total drinks volume

Leads National consumption of Whiskey, Rum, Brandy and beer

Accounts for 67% of India's brandy consumption

Prospects:

Expected volume growth of 7.4% CAGR in total alcohol from the year 2010 - 2013

Government ban on country liquor in Karnataka opens huge market for economy brands of

IMFL

The youth are prone to experimentation and see white spirits as a trendy trend as opposed to

whisky.

West

Constitute 27% of total sales

Second behind south in spirits, leads in beer and Ready to Drink alcohol

Prospects

Alcoholic drinks to grow in volume terms at CAGR of 6.9% from the year 2010 - 2013

Liberal stance towards alcohol and flourishing of premium brands in Maharashtra

Experimentation will lead to white spirits and other alcohols such as tequila and liqueurs to

grow faster in this region

East and North-East

Low contribution - 10% of total alcohol sales in volume terms

Prospects

Expected volume growth of 6% CAGR in total alcohol from the year 2010 - 2013

State governments depend heavily on excise in this region and hence number of off-trade

outlets is likely to increase

50% under proof alcohol (28% ABV) brands are providing a low cost upgrade from country

liquor to IMFL

West Bengal - Tax changes have made smaller packs of economy spirits cheaper, increasing

demand

Source: Company, Capitaline, FQ Research

Key Players

In IMFL segment, United Spirits is the market leader with ~53% market share and 19 brands with

sales of over 1 million cases in each brand. Other key players are Radico Khaitan, Jagatjit Industries,

Balaji Distilleries, Khoday India, Pioneer Distilleries and Empee Distilleries.

Key Concerns

Unfavourable judgement in legal case against Dutch spirit company UTO

TI and UTO, Dutch-based spirit company is engage in a legal battle over the brand Mansion

House and Savoy Club, details of which is given below:

Dutch spirit company UTO has moved the Bombay High Court to reclaim what its says are its

brand, Mansion House and Savoy Club from TI. UTO claims that it has licensed these brands to

TI in 1983. According to the TI, "Mansion House and Savoy Club are registered by TI in the

trademark registry under the provisions of the trademark law. Mansion House labels are also

registered under the Copyright Act. The said registrations are valid and subsisting and TI, therefore

has an exclusive right to use them". In fact, in 1987, UTO ceded its right to the said trademarks

in favour of TI. Therefore, UTO did not demand the TI to give back the said trademarks, nor did

TI give up its right in the said trademarks. The fact that UTO never staked its claim in the 1990s,

when TI was struggling to promote the said brand and create a market for it, reinforces the feeling

that it is not going to give in easily.

Southern region account for highest

consumption at ~38% of India's total

drinks volume

Western region constitute 27% of total

sales, second behind southern region

For Private Circulation OnlyApril 16, 2010 19

Also, while UTO markets only whisky under the Mansion House brand internationally, TI stopped

importing this concentrate from the former in 1991, and instead, developed its own blend of

whisky (as well as brand) under this brand. On its part, it is this IPR that TI will be depending.

Any unfavourable result for TI can have negative impact for the company as a whole.

Increase in key input prices

Currently, the key input for TI is molasses and going forward, grains will also be the key feedstock.

Any spurt in prices of key feedstock above our expectation, due to any reason, will have direct

impact on bottom line of the company.

Concentration of revenue in Southern Region

As more than 90% of revenue for the company comes from southern region, any decline in sales

in Southern region, due to any unavoidable circumstances, can hit the topline of the company

directly.

About Company

TI is one of the leading players in the Indian alcoholic beverage industry and manufactures Indian

Made Foreign Liquor (IMFL), with over 16 brands across a diverse range of price and product segments.

TI's primary manufacturing facility is located in at Shrirampur, Maharashtra. Currently, the company

has 100 KLPD molasses based and 100 KLPD grain based distillery. The company sells its products in

18 states through well knit sales and distribution network. Southern region is the main market which

contributes around 90% of the total sales. TI's Mansion House has held the unassailable position in

the premium brandy segment for many years. The company commands around 4% of the IMFL

market nationally.

History

Established in 1933 as Maharashtra Sugar Mills Ltd. (MSM), TI was named after the revered freedom

fighter Bal Gangadhar Tilak and was one of Maharashtra's first private sugar factories, which served

the nation for over five decades. Later on, TI moved to an the alcoholic beverage business.

Tilaknagar Distilleries & Industries Ltd. was promoted as a 100% subsidiary of The Maharashtra Sugar

Mills Ltd. The year 1973 saw TI diversify into the businesses of Industrial Alcohol, Indian Made

Foreign Liquor (IMFL) and Sugar Cubes, the company transitioned to the alcoholic the company

transitioned to the alcoholic beverage business in 1987. Both Maharashtra Sugar Mills Ltd. and

Tilaknagar Distilleries & Industries Ltd were merged to form Tilaknagar Industries Ltd. (TI) with effect

from August 6, 1993.

Key Management Personnel

Mr. Amit Dahanukar, MD & Chairman

Mrs. Shivani A Dahanukar, Executive Director

Mr. Lalit Sethi, CFO

For Private Circulation OnlyApril 16, 2010 20

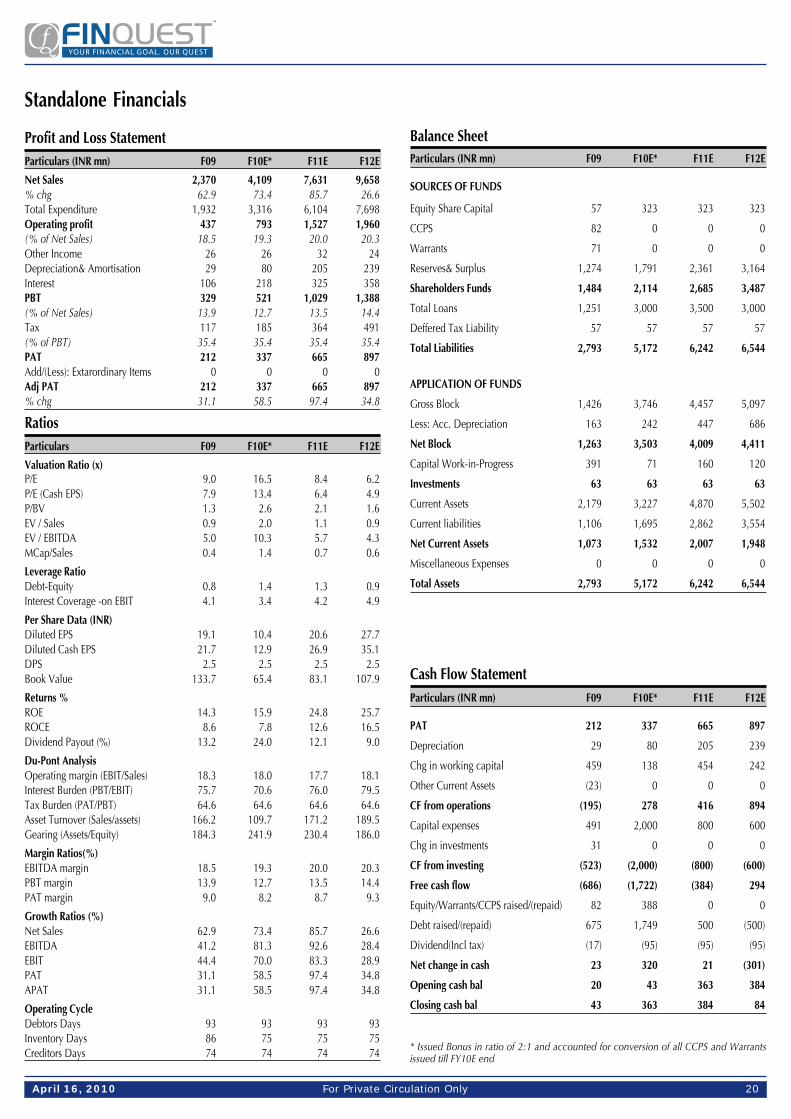

Profit and Loss StatementParticulars (INR mn) F09 F10E* F11E F12E

Net Sales 2,370 4,109 7,631 9,658% chg 62.9 73.4 85.7 26.6Total Expenditure 1,932 3,316 6,104 7,698Operating profit 437 793 1,527 1,960(% of Net Sales) 18.5 19.3 20.0 20.3Other Income 26 26 32 24Depreciation& Amortisation 29 80 205 239Interest 106 218 325 358PBT 329 521 1,029 1,388(% of Net Sales) 13.9 12.7 13.5 14.4Tax 117 185 364 491(% of PBT) 35.4 35.4 35.4 35.4PAT 212 337 665 897Add/(Less): Extarordinary Items 0 0 0 0Adj PAT 212 337 665 897% chg 31.1 58.5 97.4 34.8

RatiosParticulars F09 F10E* F11E F12E

Valuation Ratio (x)P/E 9.0 16.5 8.4 6.2P/E (Cash EPS) 7.9 13.4 6.4 4.9P/BV 1.3 2.6 2.1 1.6EV / Sales 0.9 2.0 1.1 0.9EV / EBITDA 5.0 10.3 5.7 4.3MCap/Sales 0.4 1.4 0.7 0.6

Leverage RatioDebt-Equity 0.8 1.4 1.3 0.9Interest Coverage -on EBIT 4.1 3.4 4.2 4.9

Per Share Data (INR)Diluted EPS 19.1 10.4 20.6 27.7Diluted Cash EPS 21.7 12.9 26.9 35.1DPS 2.5 2.5 2.5 2.5Book Value 133.7 65.4 83.1 107.9

Returns %ROE 14.3 15.9 24.8 25.7ROCE 8.6 7.8 12.6 16.5Dividend Payout (%) 13.2 24.0 12.1 9.0

Du-Pont AnalysisOperating margin (EBIT/Sales) 18.3 18.0 17.7 18.1Interest Burden (PBT/EBIT) 75.7 70.6 76.0 79.5Tax Burden (PAT/PBT) 64.6 64.6 64.6 64.6Asset Turnover (Sales/assets) 166.2 109.7 171.2 189.5Gearing (Assets/Equity) 184.3 241.9 230.4 186.0

Margin Ratios(%)EBITDA margin 18.5 19.3 20.0 20.3PBT margin 13.9 12.7 13.5 14.4PAT margin 9.0 8.2 8.7 9.3

Growth Ratios (%)Net Sales 62.9 73.4 85.7 26.6EBITDA 41.2 81.3 92.6 28.4EBIT 44.4 70.0 83.3 28.9PAT 31.1 58.5 97.4 34.8APAT 31.1 58.5 97.4 34.8

Operating CycleDebtors Days 93 93 93 93Inventory Days 86 75 75 75Creditors Days 74 74 74 74

Balance SheetParticulars (INR mn) F09 F10E* F11E F12E

SOURCES OF FUNDS

Equity Share Capital 57 323 323 323

CCPS 82 0 0 0

Warrants 71 0 0 0

Reserves& Surplus 1,274 1,791 2,361 3,164

Shareholders Funds 1,484 2,114 2,685 3,487

Total Loans 1,251 3,000 3,500 3,000

Deffered Tax Liability 57 57 57 57

Total Liabilities 2,793 5,172 6,242 6,544

APPLICATION OF FUNDS

Gross Block 1,426 3,746 4,457 5,097

Less: Acc. Depreciation 163 242 447 686

Net Block 1,263 3,503 4,009 4,411

Capital Work-in-Progress 391 71 160 120

Investments 63 63 63 63

Current Assets 2,179 3,227 4,870 5,502

Current liabilities 1,106 1,695 2,862 3,554

Net Current Assets 1,073 1,532 2,007 1,948

Miscellaneous Expenses 0 0 0 0

Total Assets 2,793 5,172 6,242 6,544

Cash Flow StatementParticulars (INR mn) F09 F10E* F11E F12E

PAT 212 337 665 897

Depreciation 29 80 205 239

Chg in working capital 459 138 454 242

Other Current Assets (23) 0 0 0

CF from operations (195) 278 416 894

Capital expenses 491 2,000 800 600

Chg in investments 31 0 0 0

CF from investing (523) (2,000) (800) (600)

Free cash flow (686) (1,722) (384) 294

Equity/Warrants/CCPS raised/(repaid) 82 388 0 0

Debt raised/(repaid) 675 1,749 500 (500)

Dividend(Incl tax) (17) (95) (95) (95)

Net change in cash 23 320 21 (301)

Opening cash bal 20 43 363 384

Closing cash bal 43 363 384 84

* Issued Bonus in ratio of 2:1 and accounted for conversion of all CCPS and Warrantsissued till FY10E end

Standalone Financials

For Private Circulation OnlyApril 16, 2010 21

DISCLAIMER: This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any other person. Persons into whose possession thisdocument may come are required to observe these restrictions. Opinion expressed is our current opinion as of the date appearing on this material only. While we endeavor to update on a reasonable basis the informationdiscussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and maybe subject to change without notice. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein. The information in this documenthas been printed on the basis of publicly available information, internal data and other reliable sources believed to be true and are for general guidance only. While every effort is made to ensure the accuracy andcompleteness of information contained, the company takes no guarantee and assumes no liability for any errors or omissions of the information. No one can use the information as the basis for any claim, demand or causeof action. Recipients of this material should rely on their own investigations and take their own professional advice. Each recipient of this document should make such investigations as it deems necessary to arrive at anindependent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of suchan investment. Price and value of the investments referred to in this material may go up or down. Past performance is not a guide for future performance. Certain transactions - futures, options and other derivatives as wellas non-investment grade securities - involve substantial risks and are not suitable for all investors. Reports based on technical analysis centers on studying charts of a stock’s price movement and trading volume, as opposedto focusing on a company’s fundamentals and as such, may not match with a report on a company’s fundamentals. We do not undertake to advise you as to any change of our views expressed in this document. While wewould endeavor to update the information herein on a reasonable basis, FINQUEST, its subsidiaries and associated companies, their directors and employees are under no obligation to update or keep the information current.Also there may be regulatory, compliance, or other reasons that may prevent FINQUEST and affiliates from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictionsand may be subject to change without notice. FINQUEST and affiliates, including the analyst who has issued this report, may, on the date of this report, and from time to time, have long or short positions in, and buy or sellthe securities of the companies mentioned herein or engage in any other transaction involving such securities and earn brokerage or compensation or act as advisor or have other potential conflict of interest with respect tocompany/ies mentioned herein or inconsistent with any recommendation and related information and opinions. FINQUEST and affiliates may seek to provide or have engaged in providing corporate finance, investmentbanking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Outperformer Marketperformer Underperformer

More than 10% to Index Within 0-10% to Index Less than 0-10% to Index

RESEARCH

Chintan MewarVice President - Research4000 [email protected]

Sunny AgrawalAnalyst4000 [email protected]

Dinesh ShuklaAnalyst4000 [email protected]

Rajesh GhodkeProduction4000 [email protected]

ANALYST DISCLAIMER: Each analyst of FINQUEST Securities (P) Ltd. whose name appears on page 1 of the research reports accessible on this website hereby certifies that (i) the recommendations and opinionsexpressed in the research report accurately reflect the research analyst's personal views about any and all of the securities or issuers discussed herein that are within the analyst’s coverage universe and (ii) no part of theresearch analyst's compensation was, is, or will be, directly or indirectly, related to the provision of specific recommendations or views expressed by the research analyst in the research report.

FINQUEST Securities (P) Ltd.602 Boston House, Next to Cinemax, Suren Road, Andheri (East) Mumbai 400 093.Tel.: 91-22-4000 2600 Fax: 91-22-4000 2605 Email: [email protected]

Website: www.finquestonline.com

SALES

Uday KamatSenior Vice President - Institutional Sales4000 [email protected]

Jyoti NangraniTechnical Analyst4000 [email protected]

DEALING

Jackie GandhiInstitutional Dealer4000 [email protected]

Paras ShahInstitutional Dealer4000 [email protected]

Vikas MandhaniaInstitutional Dealer4000 [email protected]