Tapping the capital markets the Islamic way: the Sukuk phenomenon Alberto G. Brugnoni.

48

-

Upload

elijah-powell -

Category

Documents

-

view

221 -

download

0

Transcript of Tapping the capital markets the Islamic way: the Sukuk phenomenon Alberto G. Brugnoni.

Tapping the capital markets the Islamic way:the Sukuk phenomenon

Alberto G. Brugnoni

An historical perspective: the IFSI as the continuation of a millennium-long wave

A general consideration on today’s IFSI

A distinguishing feature of IFSI: funding of trade in, or production of, real assets

Introduction

IFSI market size $ 500bn to ... $ 1000bn

REGIONAL AND GLOBAL GROWTH TOTALS

$m 2007 2006 % change

GCC 178,129 127,826 39.35%

Non-GCC MENA 176,822 136,157 29.87%

MENA Total 354,951 263,984 34.46%

Sub-Saharan Africa 4,707 3,039 54.90%

Asia 119,346 98,709 20.91%

Australia/Europe/America 21,475 20,300 5.79%

Global Total 500,481 386,033

Source: Maris Strategies & the Banker

Rankby

RoA

Institution CountryReturn

on assets

Rankby

RoAInstitution Country

Return on

assets

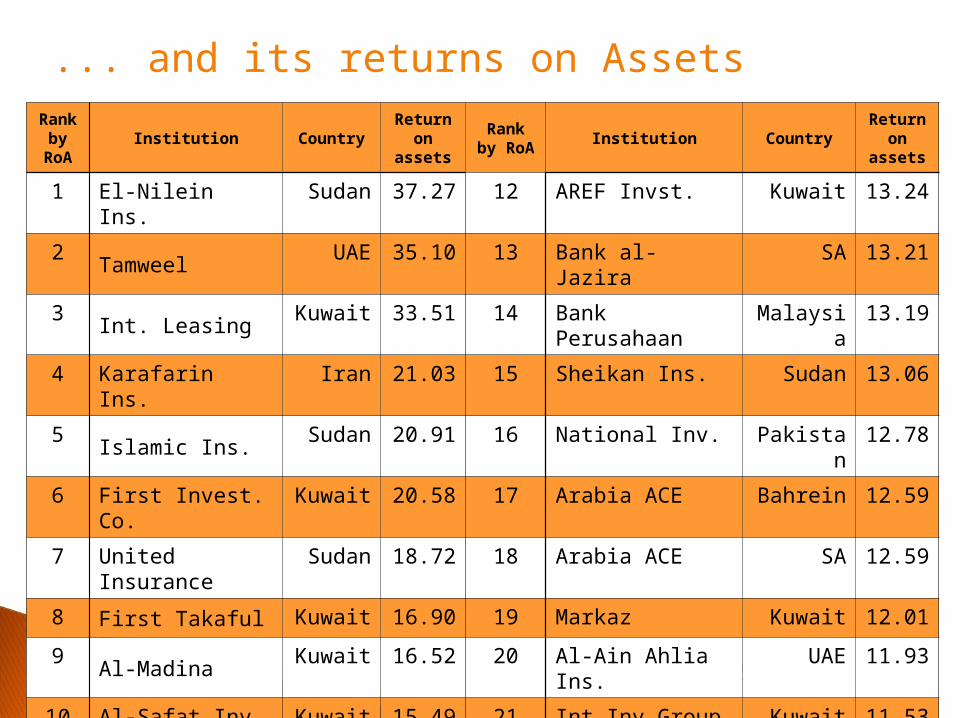

1 El-Nilein Ins. Sudan 37.27 12 AREF Invst. Kuwait 13.24

2 Tamweel UAE 35.10 13 Bank al-Jazira SA 13.21

3Int. Leasing

Kuwait 33.51 14 Bank Perusahaan

Malaysia 13.19

4 Karafarin Ins. Iran 21.03 15 Sheikan Ins. Sudan 13.06

5 Islamic Ins. Sudan 20.91 16 National Inv. Pakistan 12.78

6 First Invest. Co. Kuwait 20.58 17 Arabia ACE Bahrein 12.59

7 United Insurance

Sudan 18.72 18 Arabia ACE SA 12.59

8 First Takaful Kuwait 16.90 19 Markaz Kuwait 12.01

9 Al-Madina Kuwait 16.52 20 Al-Ain Ahlia Ins. UAE 11.93

10 Al-Safat Inv. Co. Kuwait 15.49 21 Int.Inv.Group Kuwait 11.53

11Unicorn

Bahrein

13.62 22 Ithmaar Bank Bahrain 10.82

Source: The Banker

... and its returns on Assets

Rank Country SCAin $m

SCA/ Assets

Rank Country SCAin $m

SCA/Assets

1 Iran 154,616 100% 12 Qatar 9,459 25%

2 Saudi Arabia

69,379 31% 13 Sudan 4,467 100%

3 Malaysia 65,083 25% 14 Bangladesh 4,331 58%

4 Kuwait 37,684 37% 15 Egypt 3,852 6%

5 UAE 35,354 29% 16 Jordan 2,635 100%

6 Brunei 31,535 100% 17 Indonesia 2,223 3%

7 Bahrain 26,251 31% 18 Switzerland 813 0.07%

8 Pakistan 15,918 25% 19 Algeria 564 100%

9 Lebanon 14,315 75% 20 Yemen 339 100%

10 UK 10,420 0.10%

21 Tunisia 279 100%

11 Turkey 10,065 100% 22 Palestine 219 100%Source: The Banker

Percentages of SCA to total assets

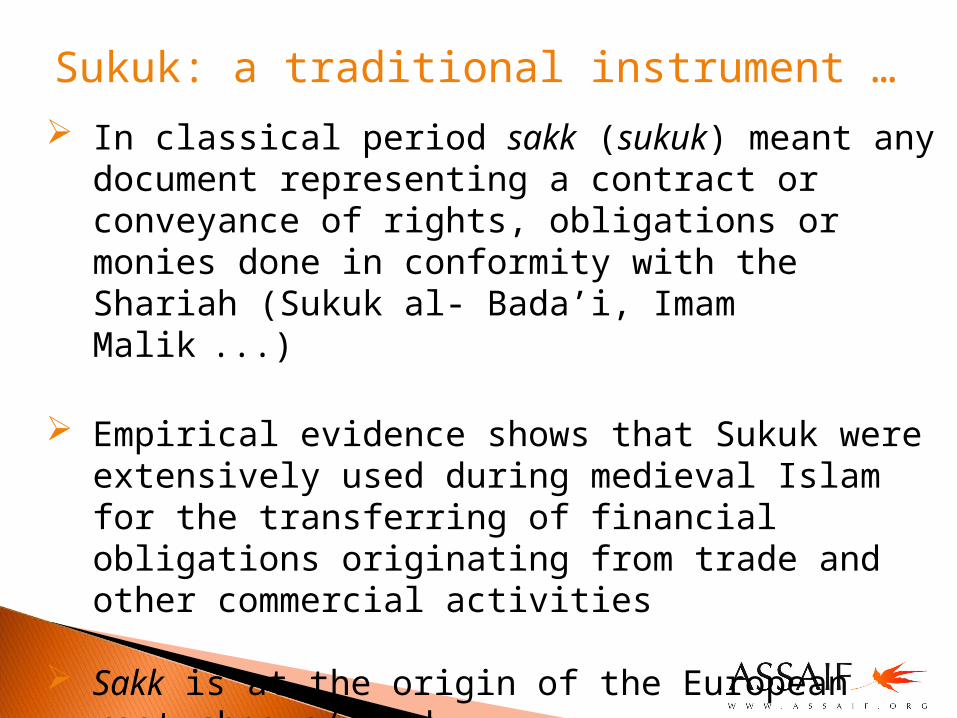

Sukuk: a traditional instrument … In classical period sakk (sukuk) meant any

document representing a contract or conveyance of rights, obligations or monies done in conformity with the Shariah (Sukuk al- Bada’i, Imam Malik ...)

Empirical evidence shows that Sukuk were extensively used during medieval Islam for the transferring of financial obligations originating from trade and other commercial activities

Sakk is at the origin of the European root cheque/check

... fit for a contemporary use ... Malaysia re-introduced Islamic bonds in the

1990’ and they were termed as Bai bi-thaman Ajil Bonds

In the Middle East, Bahrain re-introduced the Sukuk al-Ijara instrument to the Islamic market in September 2001 and Malaysia pioneered the global Sukuk al-Ijara issue in June 2002

The Middle Eastern Islamic bond market evolved gradually with the support of top-tier issuers like the Islamic Development Bank, the States of Qatar and Dubai, the Republic of Pakistan ...

... with a contemporary added value

The essence of this product, in the modern Islamic perspective, lies in the concept of asset monetization - the so called securitization - that is achieved through the process of issuance of sukuk (taskeek)

His great potential is in transforming an asset’s future cash flow into present cash flow

The legitimacy of Sukuk

Qur’an - Sura 2:282

The Islamic Jurisprudence Council decision n° 5/1988 to uphold the issuance of sukuk:- representation of assets in a note or bond- salability of the written note or bond

AAOIFI’s “Shariah standards on investment Sukuk”, Bahrain May 2003

Sukuk: a definition Sukuk are asset-backed trust certificates

evidencing ownership of an asset or its usufruct

These certificates are, in turn, based on Islamic traditional financial structures that have been in use for the last 1500 years

Sukuk are not a completely new asset class. They are securities that employ existing financial engineering techniques (securitization structures) that create ‘asset-backed’ bond that are also Shari’ah-compliant

Sukuk share similarities (?) with bonds … Marketability: sukuk are monetized real

assets that are liquid and (easily?) tradable

Rateability: sukuk are easily analyzed and rated by international and regional agencies

Enhanceability: different sukuk structures may allow for credit enhancements or wraps that broaden their appeal to risk-averse investors

Versatility: structuring across legal and tax domains of products that meet diverse financing need

... and differences as well Sukuk represent actual and legal ownership

stakes in assets and services and are not monetary documents relating to receivables

The Sukuk holder share the return and bear the losses and he is not a creditor

Sukuk are valid only if issued after receipt of the value of the sukuk and the employment of the funds

Sukuk are issued and traded according to shari’a nominated contracts

The prospectus document should provide complete transparency. Inherent right to information

A primary condition: tangibility Existence and identification of suitable assets

Returns and cash flows must be linked to assets purchased or those generated from an asset once constructed (project finance)

Borrowers to raise compliant financing will need to utilize assets in the structure. Borrowers that provide the assets are commonly referred to as originators

This requirement has consequential effects for derivatives

More on tangibility

Equity. It is an asset: equity financing is Shari’ah compliant and fits well with the risk/return concepts

Receivables. Their trading for anything other than par is not permissible. However, some Shariah boards have accepted that, as long as such receivables are a small (?) portion of the overall income flows, their presence is acceptable in Sukuk

Malaysia does not place receivables in the category of money and hence allows Sukuk to be 100% backed by receivables. This is a major difference with GCC countries

Asset-backed Sukuk Sukuk can be consider to be asset-backed or

asset-secured, and therefore sharia compliant, only if the key securitization elements are in place

These elements should ensure that the Sukuk holders have beneficial title and realizable security over the assets with no encumbrances (no claw back clauses ...). The SPV role

The credit risk ratings of these Sukuk depends solely on the underlying assets. The standard methodologies on securitized assets apply

Unsecured Sukuk: are they Sharia compliant?

Such analysis becomes irrelevant if the legal structure does not support Sukuk holders’ rights to the underlying assets and to their cash flows

In fact, an analysis of the commercial terms and legal structures shows that for some Sukuk performance is not governed by the assets and that the credit risk is really that of the originator

The ratings of these Sukuk depends on the riskiness of the originator

Sukuk asset classes

Sukuk may be issued on existing as well as specific assets that may become available at a future date. This ‘non-exhaustive’ list includes:

Sukuk al-ijarah: securitization of existing tangible leased assets

Sukuk ijarah mowsufa bi-thima: mobilization of the acquisition cost of tangible to-be-leased assets

Sukuk manfaa ijarah: securitization of the usufruct of existing leased assets

Sukuk asset classes Sukuk manfaa ijarah mowsufa bi-thima:

securitization of the usufruct of assets to be acquired and leased

Sukuk milkiyat al-khadamat: pre-sale of the cost of services and their expected benefits

Sukuk al-salam: pre-sale of future delivery of goods or commodities

Sukuk al-istisna’a: mobilization of the cost of construction and manufacturing of specific assets

Sukuk asset classes Sukuk al-murabaha: mobilization of the

acquisition cost of goods to be sold under a murabaha

Sukuk al-musharaka: sale of capital participations into a partnership

Sukuk al-mudharaba: mobilization of funds from capital providers

Sukuk al-wakala: mobilization of capital to acquire certain goods that are entrusted to an agent

Sukuk asset classes

Sukuk al-muzra’a: mobilization of funds for the cultivation of land

Sukuk al-musaqa: mobilization of funds for the irrigation and maintenance

Sukuk-al-muqarasa: mobilization of funds for the maintenance of land and crops

Sukuk al-Ijara

Ijara (lease) is a contract according to which a party purchases and leases out equipment required by the client for a rental fee

Sukuk al-Ijara are securities representing the ownership of defined and known assets that are tied up to a lease contract

Sukuk al-Ijara structure

SPVIssuer/Lessor

Obligator as sellerObligator leases

back assetsas lessee

Sukuk holders

1.Title to asset

4.Periodic rentals and capital

amount payments

2.Sukuk proceeds

2.Sukuk proceeds 3.Lease agreement

4.Periodic rentals and capital amountdistributions

Sukuk al-Ijara structure

1. The Originator/Obligator seeking financing make a true sale of its asset to the Sukuk SPV for a value equal to the financing provided

2. The SPV issues Sukuks and ...

2. ... with the proceeds pays the Originator/Obligator

3. The Originator leases the asset back and ...

4. ... makes lease & repurchase payments to the SPV

4. The SPV distributes these periodic rentals among the Sukuk holders

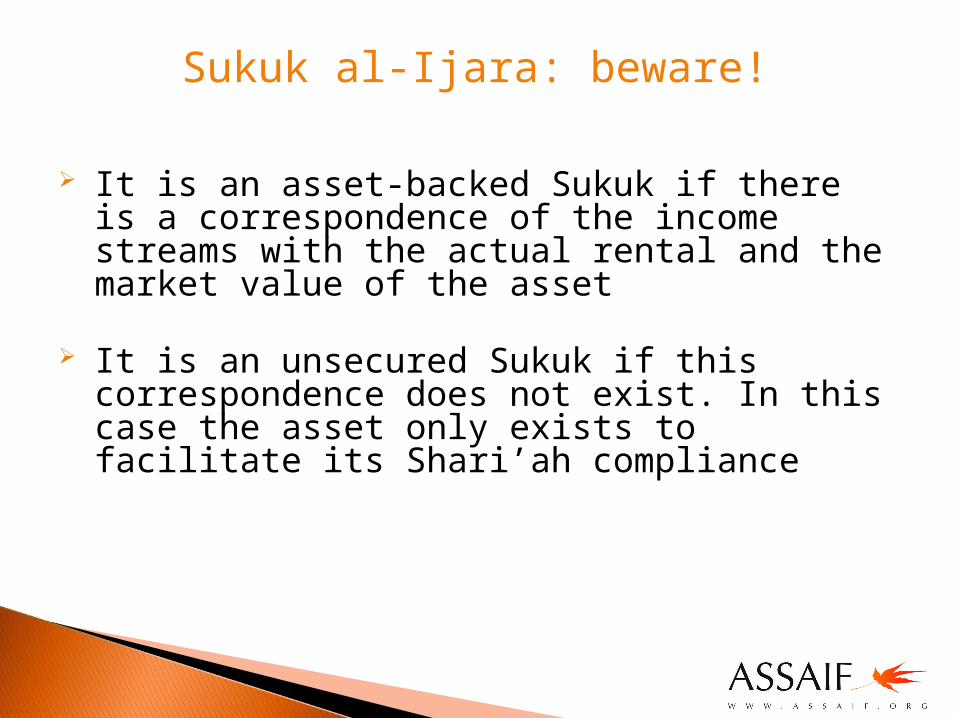

Sukuk al-Ijara: beware!

It is an asset-backed Sukuk if there is a correspondence of the income streams with the actual rental and the market value of the asset

It is an unsecured Sukuk if this correspondence does not exist. In this case the asset only exists to facilitate its Shari’ah compliance

Sukuk al-Ijara characteristics

Risks related to lessee and market

Returns not always predetermined

Full negotiability

Highly flexible

Sukuk holders bear responsibility to the property

Sukuk al-Musharaka

Under a Musharaka contract the parties agree by mutual consent to share profits and losses in a joint business

All providers of capital are entitled to participate in management but are not necessarily obliged to do so

The profit is distributed among the partners in pre-agreed ratios and the loss is borne by every partner in proportion to their respective capital contributions

Sukuk al-Musharaka structure

SPV

Musharaka

Originator/Corporate

1.Physicalasset contribution

2a. Sukuk proceeds

3b.Periodic profits +incentive fees

3a.Periodic profits

2b. Sukuk proceeds

4. Periodic distribution of profit

Investors

0&5. Musharaka Arrangement +Undertaking to buy Musharaka shares of the SPV on a periodic basis

Sukuk al-Musharaka structure1. The Originator/Corporate contributes some

specific assets and management skills

2. a&b The Sukuk issuer (usually a SPV) contributes the investor’s Sukuk proceeds

3. a&b The Originator/Corporate runs the JV, operates the assets and invests the funds. It distribute the profits

4. Sukuk holders are entitled to the Issuer’s rights in the JV whatever they are

5. The Corporate irrevocably undertakes to buy at a pre-agreed price the Musharaka shares of the SPV

Sukuk al-Musharaka: beware!

The precise description of the profit distribution and business plan is key part of the offering documentation

Should the cash flows generated by the assets under the business plan of the JV not be sufficient to fund these payments, the Issuer may have the option to call the purchase undertaking

Sukuk al-Musharaka characteristics

Documents of equal value issued with the aim to establish/develop a project on the basis of a partnership contract

The certificate holders become the owners of the project as per their respective shares

Full negotiability

Sukuk al-Mudharaba

In a Mudharaba agreement one of the two parties provides the capital (rabb al-mal) and the other (mudharib) the work

The profit is to be shared between them according to a pre-agreed ratio

Losses are borne by the capital providers (rabb al-mal) only

Sukuk al-Mudharaba structure

Project owner

Project

Primary subscriber

4. Project handed overupon completion

3. Capital proceeds and profits distribution

1. Agreement SPV as mudharib

Secondary market

2. Sukuk issues and Sukuk proceeds

3. Capital proceeds and profits collection

Sukuk al-Mudharaba structure

1. Mudharib enters into an agreement with project owner for construction/commissioning of the project

2. SPV issues Sukuk to raise funds

3. SPV collects regular profit payments and final capital proceeds from project activity for onward distribution to investors

4. Upon completion, mudharib hands over the finished project to the owner

Sukuk al-Mudharaba characteristics

The issuer of the Sukuk is the mudharib whereas the subscribers are the rabb al-mal

They have the right to receive their capital at the time the Sukuk are surrendered and an annual proportion of the realized profits as agreed but bear the losses

A Sukuk holder is entitled to all rights, which have been determined by Sharia upon his ownership of the Mudharaba bond

Sukuk al-Murabaha

Murabaha is basically the sale of goods at a price comprising the purchase price plus a margin of profit

The margin of profit must be negotiated and agreed upon by both parties to the transaction

Sukuk al-Murabaha structure

‘Borrower’

Issuer SPV

Commoditybuyer

2. Sukuk issuesand Sukuk proceeds

6.Sale price + profits

1.Masteragreement

3. Commodity

Investors

Commoditysupplier

3. Spot payment

4. MurabahaCommodity

4. Deferred payment

5. Commodity

5. Spot payment

Sukuk al-Murabaha structure

1.A master agreement is signed between the SPV and the ‘borrower’

2.SPV issues Sukuk to investors and receive proceeds

3.SPV buys commodity on spot basis from the supplier

4.SPV sells the commodity to the ‘borrower’ at the spot price plus a profit margin payable on installments

5.The borrower sells the commodity to the commodity buyer on spot basis

6.The investors receive the final sale price and profits

Sukuk al-Murabaha characteristics

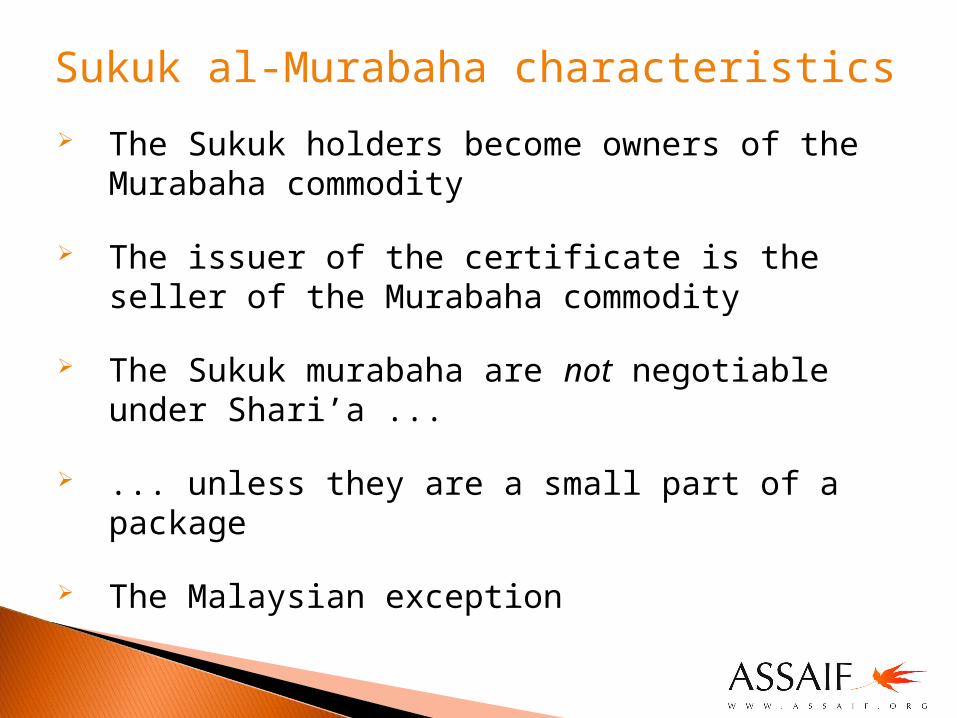

The Sukuk holders become owners of the Murabaha commodity

The issuer of the certificate is the seller of the Murabaha commodity

The Sukuk murabaha are not negotiable under Shari’a ...

... unless they are a small part of a package

The Malaysian exception

Sukuk al-Istisna’

Istisna’ is a contractual agreement for manufacturing goods and commodities

It allows cash payment in advance and future delivery or a future payment and future delivery

Sukuk al-Istisna’ structure

SPVContractor/builder End buyer

Sukuk holders(investors)

2.Payments4.MonthlyPayments

1.Sukuk proceeds

3. Title to assets

4. Title to assets

5. Distribution ofreturns

Sukuk al-Istisna’ structure

1.SPV issues Sukuk to investors and receive proceeds

2.Sukuk proceeds are used to pay the contractor/ builder to build and deliver the future project

3.Title to assets is transferred to the SPV

4.Property/project is leased or sold to the end buyer. The end buyer pays monthly installments to the SPV

5.The returns are distributed among the Sukuk holders

Sukuk al-Istisna’ characteristics

Issued with the aim of mobilizing the funds required for producing products owned by the certificate holders

The issuer of these certificates is the manufacturer (supplier/seller)

The subscribers are the buyers of the intended product

The certificate holders own the product and are entitled to the sale price of the certificates

Legal environment Most GCC have a Civil Code and commercial

disputes tend to fall before a commercial court

As in any new jurisdiction, there may be a lack of precedent and uncertainty regarding matters of law. The legal framework in many countries remains untested. No precedent with regards to bankruptcy practices

Country’s domestic risks: political risks, legal uncertainties and the efficiency of the local financial markets

Many of existing transactions are governed by UK or New York laws due to their creditor friendly nature

Legal environment and Sha’riah

While Shari’ah is acknowledged as one source of law, it is not the law enforced in the courts. Shari’ah takes usually precedence only for personal matters

The only operational Shari’ah court exists in Saudi Arabia. It is unlikely that such court would be familiar with complex financial structures which first require all documents to be translated into Arabic

The problem of Shari’ah a non-compliance: the secondary market issue

Rating Sukuk

Two Aspects Of Rating Sukuk: Sharia compliance and Transaction Security

The determination of the bond’s legal enforceability

Sharia boards disagreement not to affect the obligation’s enforceability but perhaps its liquidity

What lies ahead ?