Tallink Group - Tallink Silja

13

Tallink Group - Tallink Silja Fraktutvecklingen mellan Norden och Baltikum Håkan Fagerström, Mari ehamn 16. Maj Sjöfartens Dag – Maritime Day

Transcript of Tallink Group - Tallink Silja

Tallink Group - Tallink SiljaFraktutvecklingen mellan Norden och Baltikum

Håkan Fagerström, Mari ehamn 16. Maj

Sjöfartens Dag – Maritime Day

Tallink

§ Tallink is the leading European prov ider of leisure and business trav el and sea transportation services in the Baltic Sea

§ Fleet of 19 vessels§ Operating five hotels§ Revenue EUR 944 million§ EUR 1.7 billion asset base§ 6 799 employees§ Over 9 million passengers annually§ Over 270 thousand cargo units annually§ Listed on Nasdaq OMX Baltic – TAL1T

Over 50 years of operating and cruising experience

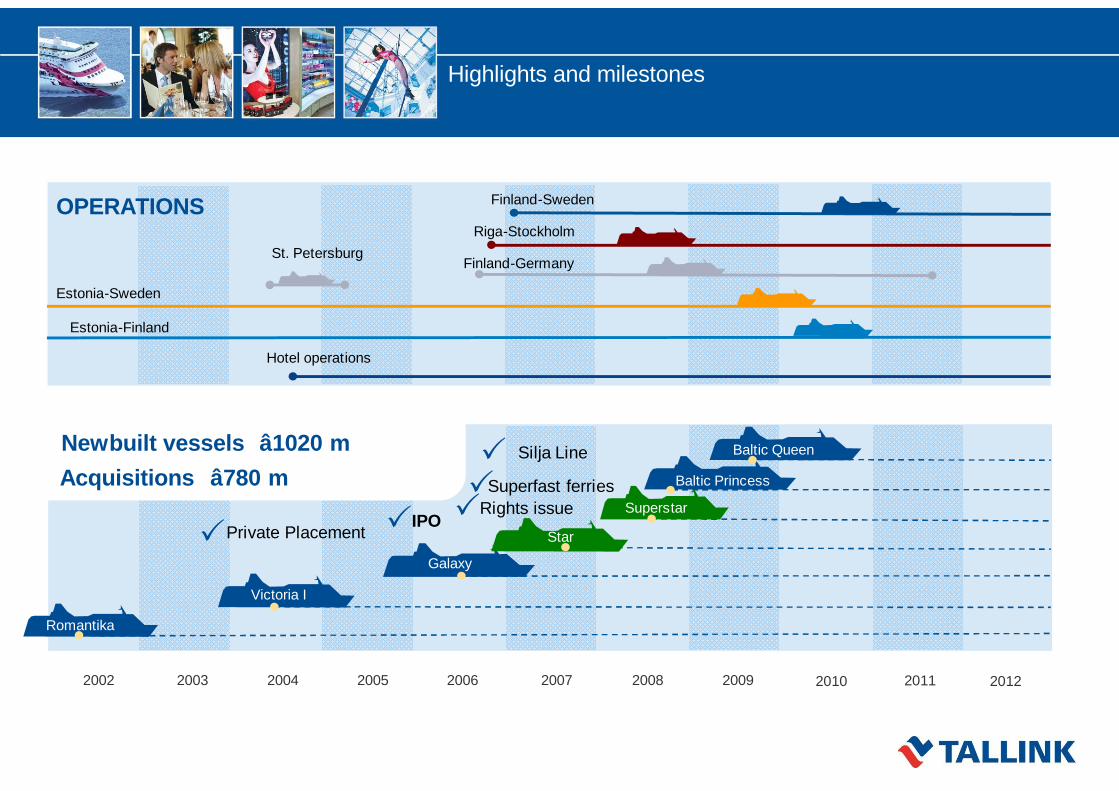

Highlights and milestones

2002 2003 2004 2005 2006 2007 2008

Newbuilt vessels € 1020 m

Estonia-Finland

Acquisitions € 780 m

2009

Estonia-Sweden

Silja Line

Riga-StockholmSt. Petersburg

Hotel operations

Superfast ferries

Finland-Germany

Finland-Sweden

PP

IPO

P

PPrivate Placement

2010 2011

Romantika

Victoria I

Galaxy

Star

Superstar

Baltic Princess

Baltic Queen

OPERATIONS

2012

Rights issueP

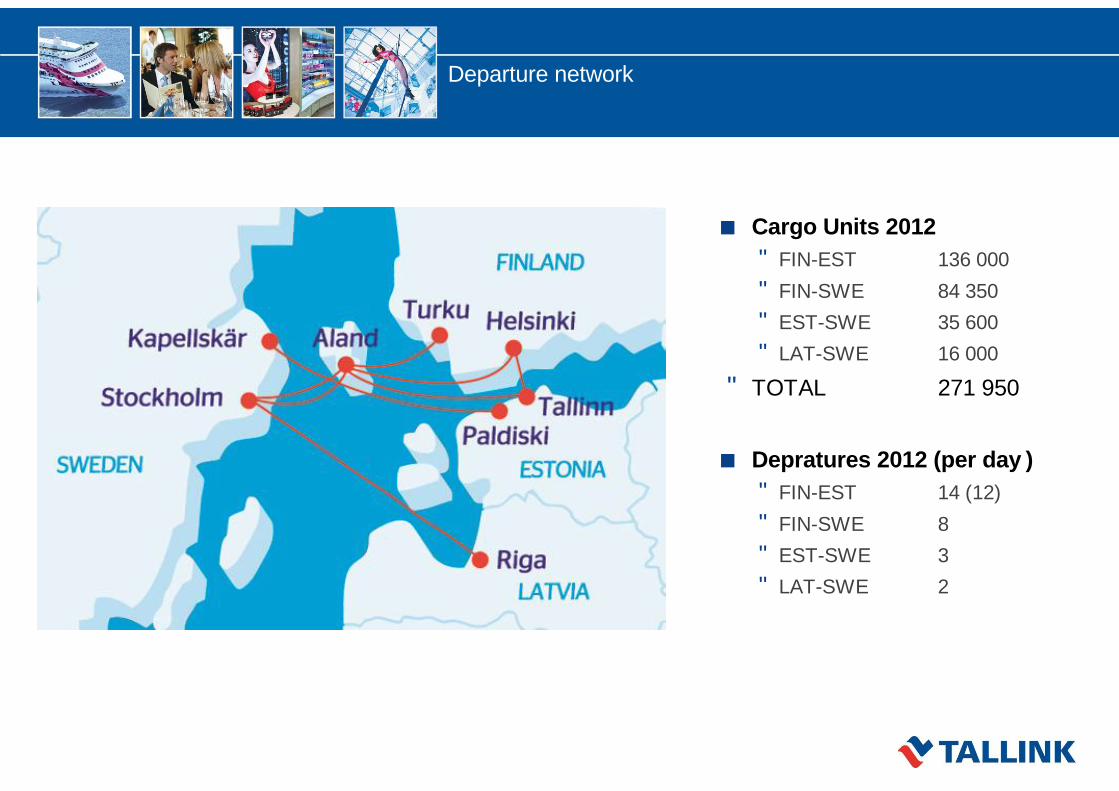

¢ Cargo Units 2012• FIN-EST 136 000• FIN-SWE 84 350• EST-SWE 35 600• LAT-SWE 16 000

• TOTAL 271 950

¢ Depratures 2012 (per day )• FIN-EST 14 (12)• FIN-SWE 8• EST-SWE 3 • LAT-SWE 2

Departure network

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

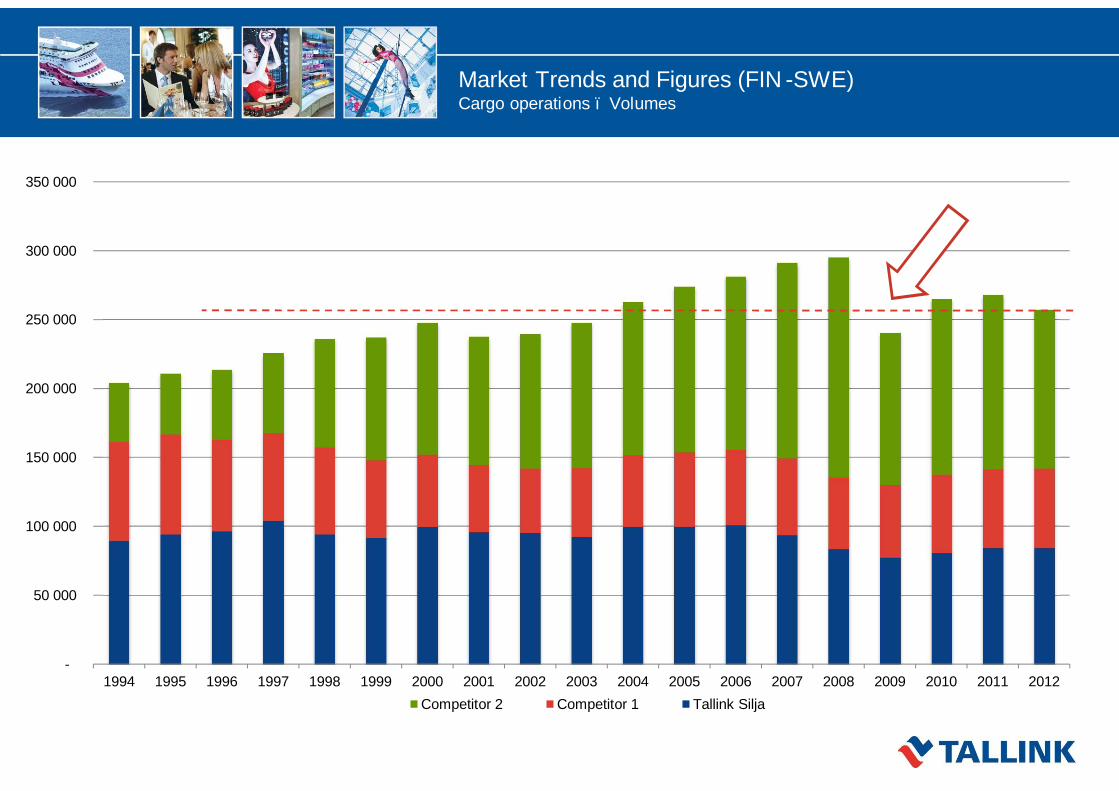

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Competitor 2 Competitor 1 Tallink Silja

Market Trends and Figures (FIN -SWE)Cargo operations – Volumes

0

50 000

100 000

150 000

200 000

250 000

300 000

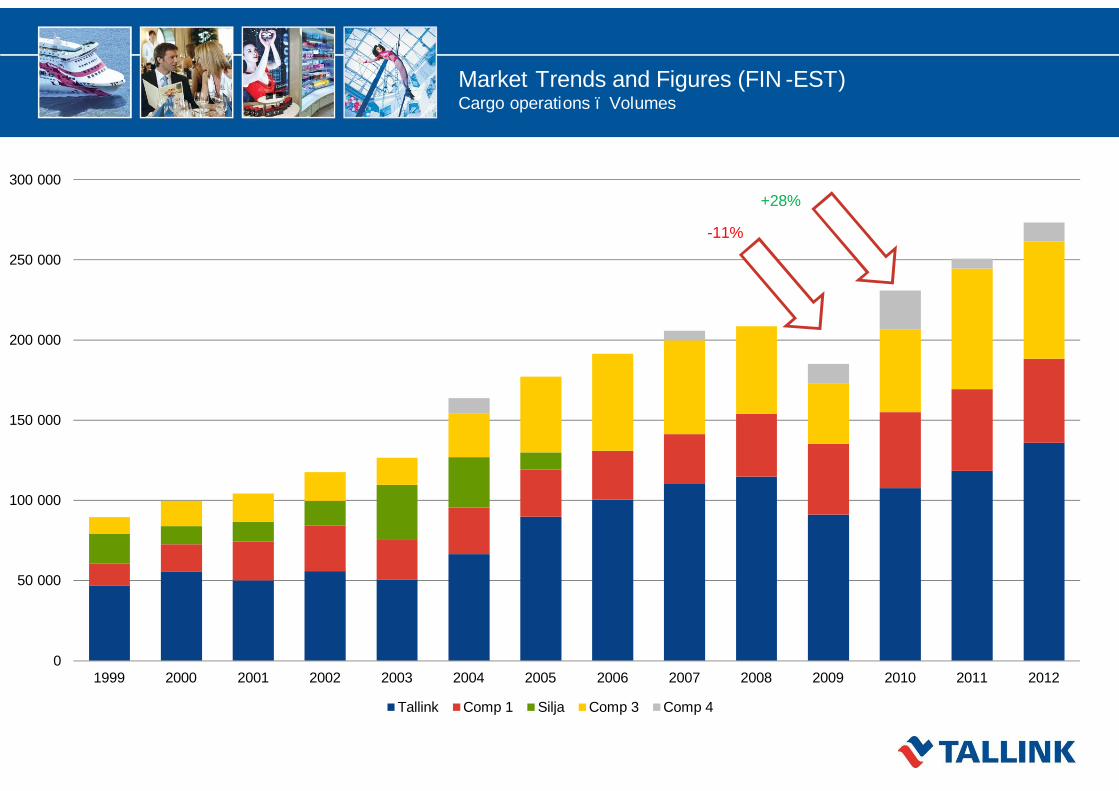

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Tallink Comp 1 Silja Comp 3 Comp 4

-11%

+28%

Market Trends and Figures (FIN -EST)Cargo operations – Volumes

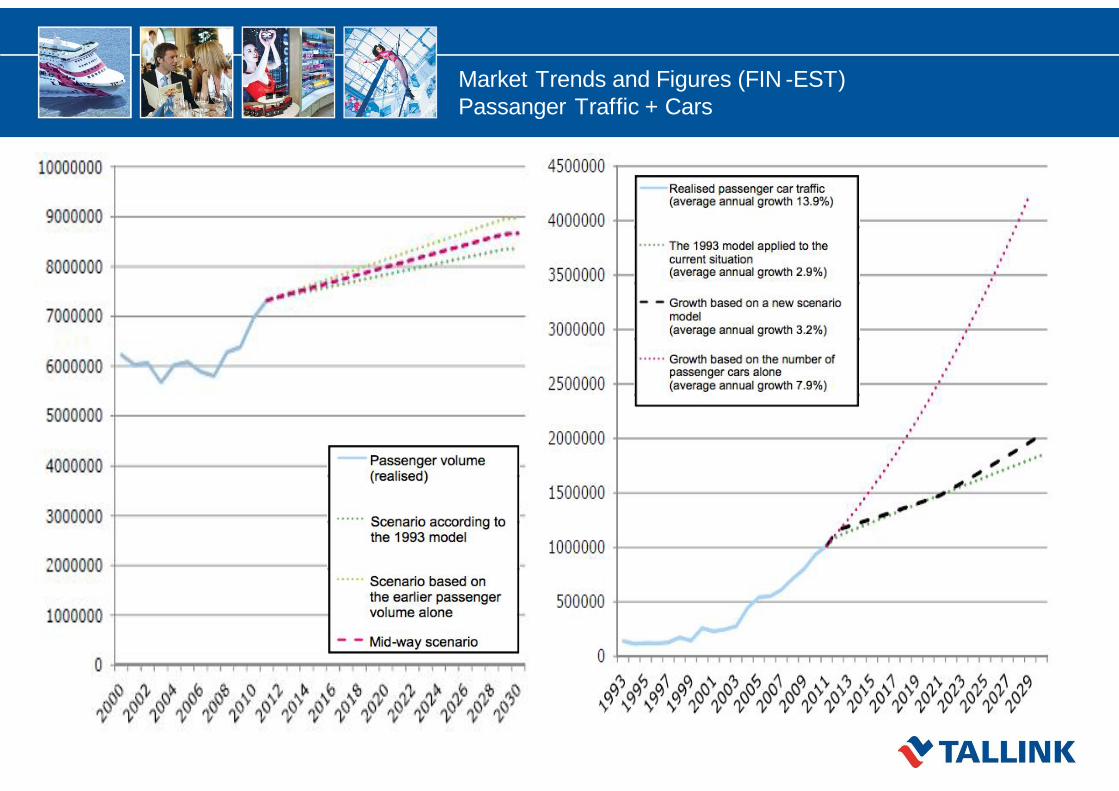

Market Trends and Figures (FIN -EST)Passanger Traffic + Cars

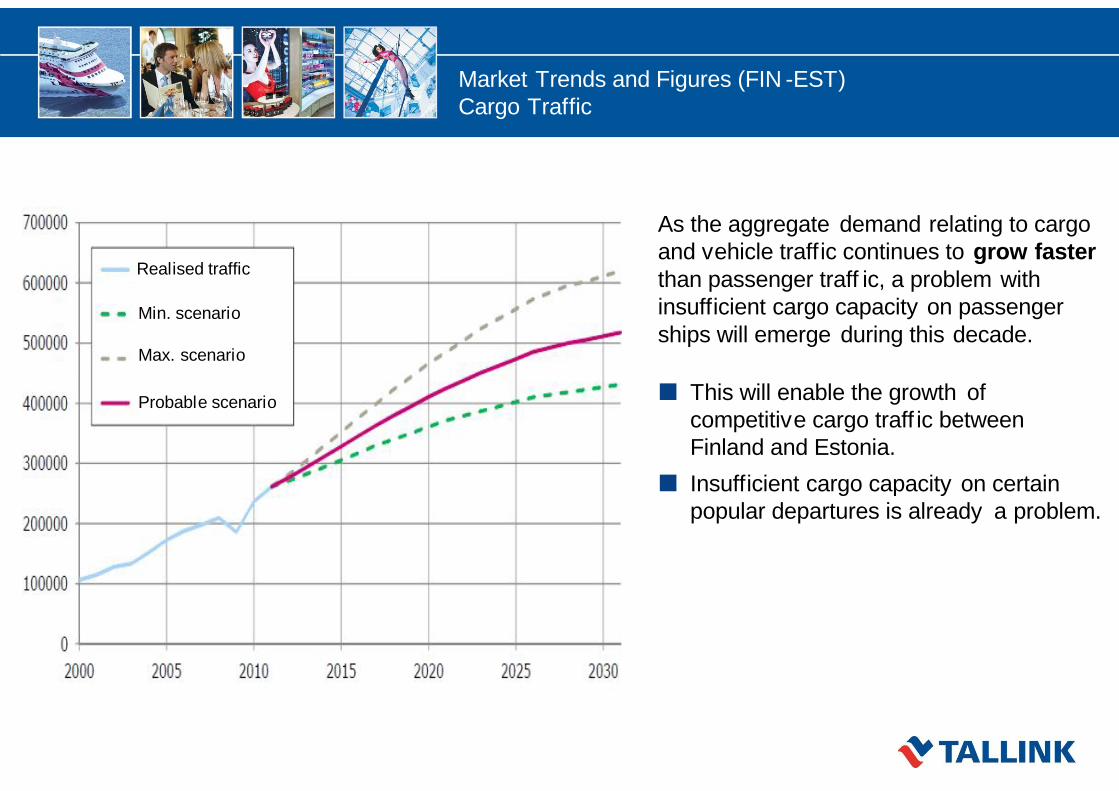

As the aggregate demand relating to cargo and vehicle traff ic continues to grow faster than passenger traff ic, a problem with insufficient cargo capacity on passenger ships will emerge during this decade.

¢ This will enable the growth of competitive cargo traff ic between Finland and Estonia.

¢ Insufficient cargo capacity on certain popular departures is already a problem.

Market Trends and Figures (FIN -EST)Cargo Traffic

Probable scenario

Max. scenario

Min. scenario

Realised traffic

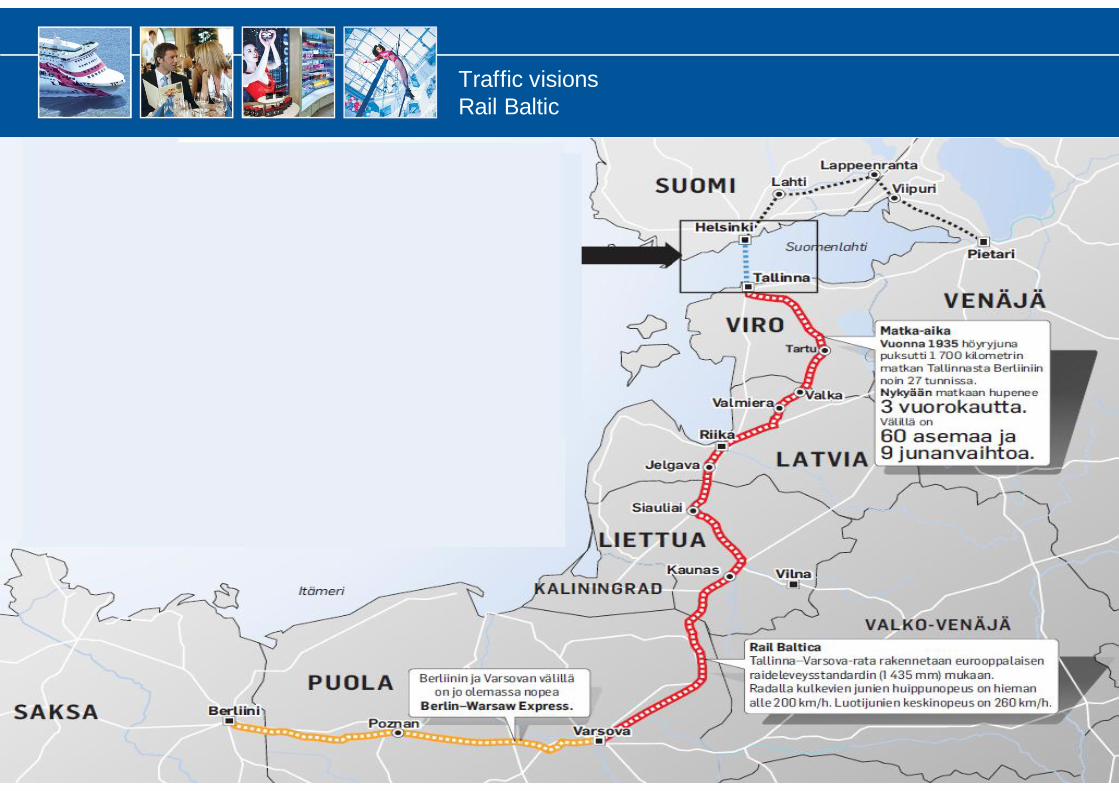

Traffic visionsRail Baltic

Market Trends and Figures (FIN -EST)Cargo operations

¢ Central European market is influencing FIN-EST traffic.

¢ HEL-TAL may be a substitute to FIN-GER in the future -> MarPol 2015

¢ Development of RAIL BALTICA will have a major impact on HEL-TAL route

¢ Development of scheduled HUCKEPACK rail-line Southern Sweden – Stockholm will gain new possibilities for UK traffic.

Market Trends and FiguresOur concept – Combine Passanger + CargoEstimate of consquences when separating Passanger and Cargo

Combining Passenger + Cargo -> an environmentally friendly option§ Strengths§ Possibility to provide extensive amount of departures -> financial result not 100% dependent of cargo.§ Reliable network and timetables§ Environmentally beneficial -> sharing the emission between passengers and cargo makes the transport mode

very environmental friendly compared to pure cargo operations.

§ Weaknesses§ Capacity fluctuation because of seasonal changes on passengers market.§ Limited possibilities to transport Dangerous Goods

§ Conclusion§ Separating cargo from passenger liners ex. on HEL-TAL would cause following:§ Additional CAPEX abt. 250m€ (3 RO-PAX)§ Additional OPEX abt. 80m€/annually§ Annual carbon dioxide emissions would increase by approx. 100,000 t

annually (cf. HRT's annual emissions of 103,000 t).§ At the time being, this would cause increased freight rates on both passenger as well as on cargo side!

Cargo Traffic visions

¢ Possible market threats..• MarPol Annex VI

• Major impact on the traf fic within the Baltic• Via Baltica's influence on the market will grow dramatically

• Possible additional emission charges for Road Traffic• Lack of trucks and driv ers (insufficient fleet)• Need to separate Cargo and Passengers

• aggregate demand for CARGO capacity grows faster than passenger traf fic.• get “cargo only” ferry-line feasible on this market area -> imminent need to raise freight

rates• Restrictions for growth (Political Decisions)

¢ Possible market opportunities …• Rail Baltica ’s impact on Helsinki – Tallinn• Growing traffic -> better deck utilization

Thank You for Your attention!Our fleet is ISO 14 001 certified“With us you can protect the environmentand still arrive faster”

To get latest news about us and our operations, Follow Us on Facebook“Tallink Silja” & “Tallink Silja Cargo”