Taking advantage of debt financing and other investment ... · PDF fileTaking advantage of...

36

What opportunities are there for you today? Taking advantage of debt financing and other investment options Amsterdam, 28 January 2014 Bert van der Toorn Managing Director, Head of Oil and Gas, Europe and CIS

Transcript of Taking advantage of debt financing and other investment ... · PDF fileTaking advantage of...

What opportunities are there for you today?

Taking advantage of debt financing and other investment options

Amsterdam, 28 January 2014 Bert van der Toorn Managing Director, Head of Oil and Gas, Europe and CIS

1

Agenda

1. Market trends

2. Financing options (in view of market trends)

3. Structuring your financing package

4. Some case studies

5. Going forwards

6. Questions?

7. Disclaimer

2

Finance Market Finance Package

Key elements

Project O&G Market

3

1. Market trends

4

Project finance volumes (2013 vs 2012)

Source: Dealogic Project Finance Review, Full Year 2013 Final Results, January 2014

5

Debt structures globally

Source: Dealogic Project Finance Review, Full Year 2013 Final Results, January 2014

6

Debt structures in the oil and gas sector

0

10000

20000

30000

40000

50000

60000

70000

2009 2010 2011 2012 2013

Bond (US$m)Loan (US$m)

Source: Based on PFI Financial Leagues Tables

Volume of loans and bonds in the oil and gas sector

7

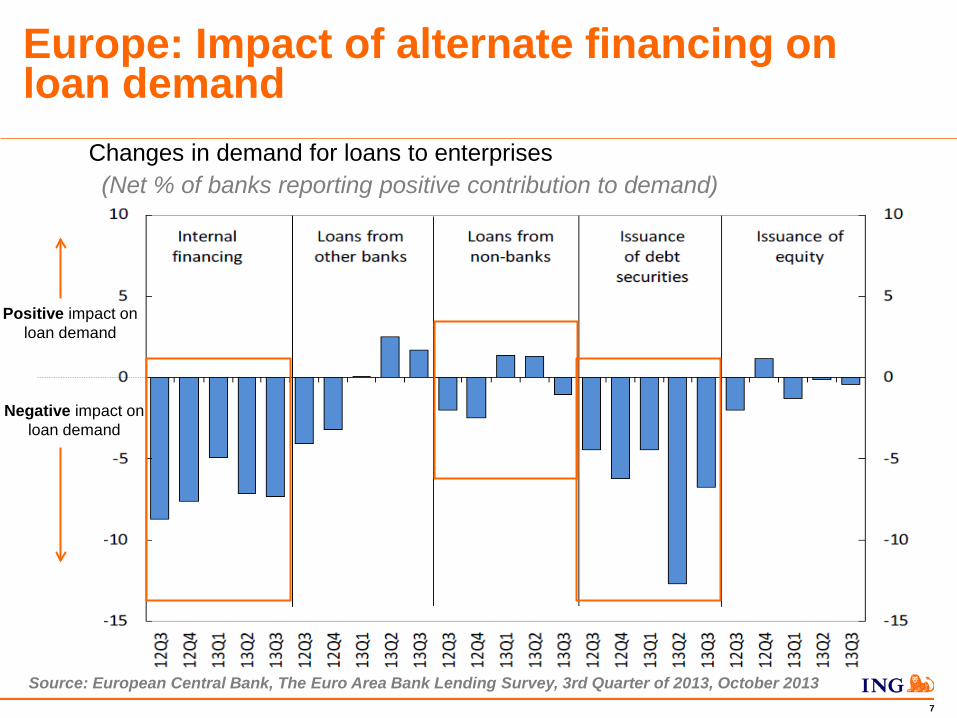

Europe: Impact of alternate financing on loan demand

Source: European Central Bank, The Euro Area Bank Lending Survey, 3rd Quarter of 2013, October 2013

Positive impact on loan demand

Negative impact on loan demand

Changes in demand for loans to enterprises (Net % of banks reporting positive contribution to demand)

8

Summary

• Volumes slowly increasing globally

• Generally: Loan vs bond vs equity mix is changing

• Specifically: increase in bonds (decrease in loans) in oil and gas sector

• Credit standards loosening very slowly

• Demand for bank loans has declined due to alternative finance but less than before

9

2. Financing options (in view of market trends)?

10

Institutional investors

Need to find alternative investments

Direct Structured solutions

11

Direct: Investing in loans • Institutional side regulation (Solvency II for insurers, IAS 19 pension funds)

• (Higher rated) loans attractive under Solvency II

• Loans as an attractive asset class :

A. Depth of market B. Floating-rate yield

C. High recovery rates

In the case of Infrastructure loans:

D. Higher yields

E. Long maturities

Unattractive features:

A. Revolving / Undrawn Facilities

12

Structured solutions: Debt vs Bonds

Some recent activity: Sabine Pass; Sakhalin 2 LNG; OGE; Nord Stream; Castor; South Stream?

Debt Bonds Shorter maturity, refinancing risk Long maturity

Floating rate finance Fixed rate funds

Prepayment flexibility Focus on long-term yield

Relationship lenders Bondholders passive – hard to organise

More flexibility: client driven mentality Difficult to modify terms

Heavily negotiated covenant package with closer monitoring

Lighter covenants: less discretion

Default: typically work out Default: trade out not work out

Less market risk: committed funding and drawdown, when required

One closing: no drawdowns

Ratings not normally required or obtained Ratings are vital

No public disclosure required Public, listing, no confidentiality agreement

13

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

US

EuropeBank loans (excl. Mortgages) Outstanding corporate bonds

United States Europe

• c.80% debt from the public market • 80% of corporate financing from bank

loans

• Increase in direct investments in the form of loans and private placements

• Banks originate credit and hold until maturity.

• Limited share of syndicated loans

• US banks :‘Originate-to-Distribute’ model • Regulatory pressure on banks to shorten their balance sheets

Structured solutions: US vs Europe

14

• Pursue infrastructure targets

• New investment platform :

1. A Note and B Loan Banks seeking longer term

2. A Notes Investors seeking high credit instruments

3. B Loan Banks seeking shorter term

• Regulatory climate

• Availability of finance

PEBBLE financing structure

Background Purpose Benefit

• Procuring Authority

• Sponsors

• A Note Investors

• B Loan Lenders

• Stimulate capital market participation

First PEBBLE-backed financing closed in September 2013:

€300 million (US$405.6m) Zaanstad Prison building in the Netherlands.

Structured solutions: Innovative ways to flavour the market

15

EIB Project Bond Credit Enhancement (PBCE) Initiative

In the form of either: (1) PBCE facility; or (2) contingent letter of credit

• Provide subordinated instruments* to eligible projects

• Enhance credit rating of Senior Bonds

• Appetite of institutional investors

• Sources of finance and minimise funding costs

• Capital market investment

• Regulatory climate

• Low credit ratings

• Drop in credit enhancing mechanisms

Background Purpose Benefit

First project bond under the PBCE initiative closed in July 2013: €1.4 billion (US$1.85bn) project bond issue for

the Castor underground gas storage project in Spain

Structured solutions: Innovative ways to flavour the market

16

Structured solutions: Innovative ways to flavour the market

ECA BOND Wrapped bond

(ECA or monoline insurer)

ECA-backed bond

17

Other interested investors and their perspectives Characteristics Pension funds/ sovereign wealth Infrastructure funds Private equity funds

Investment horizon

• Long-term investors, typically 10-30 years

• Medium-term investors, with holding periods

ranging from 7-13 years

• Short to medium holding period of 3-7 years

Investment level • Diverse, both on holding and asset level

• Diverse, both on holding and asset level

• Typically aim to invest on holding level

Corporate governance

requirements • Limited to medium • High • Medium

Minority vs. Majority

• Typically a minority stake with a passive role

• Majority, aim to obtain control

• Diverse, both minority as well as majority, dependent

on fund

Return requirements

• No cash yield requirement

• IRR of 8-13% • IRR of 20-30%

• Yearly cash yield requirement

• IRR of 13-20%

Attractions

• Long-term investment horizon

• Experienced minority investors

• Control not key

• Attracted by storage market

• Long(er) investment horizon (7-13 years on average)

• Experienced minority investors

• Control not key

• Large number of Oil & Gas oriented PE sponsors with

sufficient capital Supportive of buy & build strategy

18

Summary

• Institutional investor interest

• Bonds have their advantages but…

• ….structured solutions are needed

• Equity investor interests

In the context of market trends :

19

3. Structuring your financing package

1. Company

2. Purpose

3. The business

4. Other lender considerations

20

• Seeking further leverage? • Expansion? • Acquisition finance?

Who are you and what are you looking for?

The company and purpose

• Refinery facility conversion?

1. Existing storage company?

2. Greenfield storage company?

21

tell me about your business…

The business

1. Structure • Ownership / shareholding and assets • Contractual relationships and rights

2. Environment • Location and environmental concerns

• Supply and demand / competition (and

monopolies)

3. Operations & financials • Rating

• EBITDA / opex & capex

22

Impact

Construction & Completion

2

Post-Completion/ Operations & Maintenance

3

Cash Flow Volatility/ Force Majeure

4

Due Diligence

1

Lender considerations Factor

• Legal, Technical, Market, Environmental and Insurance Due Diligence

• Sponsor support

• Lump-Sum EPC Contract

• Technology; Operations and Maintenance

• Accounts / Cash Flow / DSRA / Security / Distributions / Ratio-testing

• No market or margin risk on capacity

• Limited merchant risk

• Structure

23

“Who are you and what would you like?”

“Tell me about your business”

The financing package

The right package - Size - Tenor - Structure - Covenants - Security

Bank debt

Other debt

Bonds

PEBBLE structure

EIB PBCE structure

Infrastructure funds

Private equity funds

Pension funds / sovereign wealth

Other creative structure?

You

Market

24

*Based on publicly available information

4. Some case studies*

25

Sea Tank 510 Liquid Bulk Storage Terminal Structured Finance

ING's role • ING acted as

Mandated Lead Arranger, Technical Bank and Account Bank for the financing

• ING acted as Hedge Coordinator

Financing details Debt:Equity: +/-80:20 Size and structure: US$240 million Tenor: 9 year Financial Covenants: Customary Security: Customary

Natural Resources

Belgium 2011

Undisclosed EUR 165 mn Project Financing

Bookrunner , MLA, Technical Bank and Hedging Coordinator Natural Resources

Belgium 2011 Belgium 2011

SEA-Tank 510 EUR 165mm

Project Financing

Bookrunner, MLA, Technical Bank and Hedging Coordinator

26

Vopak Terminal Eemshaven BV Structured Finance

ING's role • ING acted as

Documentation Bank during the structuring process

• ING acted as Mandated Lead Arranger, Facility Agent, Security Agent and Account Bank for the financing

• ING acted as Hedge Coordinator

Financing details Debt:Equity: 87:13 Size and structure: $121million (in aggr): term loans and smaller facilities Tenor: 17 years for term loans and shorter for small facilities Security: Customary

27

Vopak Horizon Fujairah Limited Structured Finance ING's role

• ING acted as Mandated Lead Arranger

• ING acted as Swap Provider and Hedge Coordinator

Financing details Size and structure: US$130 million Tenor: 8 years Security: Customary

28

Structured Finance

Financing details Size and structure: US$350 high yield bond / US$396 facility Tenor: bond: 10 years / facility: 7 years Financial Covenants: Customary Security: Customary

LBC Tank Terminals ING’s role • ING acted as

Mandated Lead Arranger and Bookrunner in the Syndicated Credit Facilty

• ING acted as bookrunner in the HY Bond

29

Structured Finance

ING's role • ING acted as

Mandated Lead Arranger

• ING acted as Swap Provider

Financing details Size and structure: €420m Tenor: 7 years

Macqpisto oil product storage

30

Structured Finance

ING's role ING acted as Mandated Lead Arranger

Financing details Size and structure:€ 196mln Tenor: 5 years

Oystercatcher

Natural Resources

Luxembourg 03/13

3i – OystercatcherEUR 195mTerm Loan and Revolving Credit Facility

Mandated Lead Arranger

31

5. Going forwards

32

What could we see?

• Changing credit standards

• Institutional investors

• Bonds

• Structured solutions

33

6. Questions?

?

???

34

7. Disclaimer

35

Disclaimer

General This presentation is intended for general information purposes. It does provide basic information concerning individual Commercial Banking products or related services. However none of the information should be interpreted as an offer to sell securities or as investment advice of any kind. Queries concerning these topics should be addressed to the individual business units and/or companies of ING Groep N.V. ("ING Group"). No warranty or representation, express or implied, is given as to the accuracy or completeness of that information. In no event will ING Group, nor any of its directors, employees or advisors accept any liability with regard to the information contained in the individual ING companies', business unit or product group's presentation.

ING Group comprises a broad spectrum of companies (the "ING companies"), many of them operating under their own brand names. Almost every ING company, business unit or product group, has its own website on the internet where it offers information about its products and services. Reference is made to those websites for further details and hyperlinks have been provided from this website to those ING companies, business units and product groups, if available.

It is prohibited to modify, copy, distribute, transmit, display, publish, sell, license, create derivative works or use any content for any other purposes than that of this presentation, i.e. providing information about ING Group and its lines of business.

No Liability While ING Group and ING companies use reasonable efforts to include accurate and up-to-date information in this presentation, errors or omissions sometimes occur. ING Group and ING companies expressly disclaim any liability, whether in contract, tort, strict liability or otherwise, for any direct, indirect, incidental, consequential, punitive or special damages arising out of or in any way connected with your access to or use of this presentation, and/or any other ING companies' presentations whether or not ING Group and/or ING companies were aware of the possibility of such damages.

All information in this presentation, including but not limited to graphics, text and links to other communication means, is provided "as is" and is subject to change without prior notice. Such information is provided, to the fullest extent permissible pursuant to applicable law, without warranty of any kind express or implied, including but not limited to implied warranties of merchantability, fitness for a particular purpose, non-infringement from disabling devices. ING Group does not warrant the adequacy, accuracy or completeness of any information in this presentation and expressly disclaim any liability for errors or omissions therein. Users are responsible for evaluating the accuracy, completeness or usefulness of any information or other content available in this presentation.