Takeover Law An Introduction Dr. Christian TEMMEL, MBA (Oxford) Partner DLA Piper Weiss-Tessbach,...

50

Takeover Law An Introduction Dr. Christian TEMMEL, MBA (Oxford) Partner DLA Piper Weiss-Tessbach, Vienna

-

Upload

gary-black -

Category

Documents

-

view

216 -

download

0

Transcript of Takeover Law An Introduction Dr. Christian TEMMEL, MBA (Oxford) Partner DLA Piper Weiss-Tessbach,...

Takeover Law

An Introduction

Dr. Christian TEMMEL, MBA (Oxford)

Partner

DLA Piper Weiss-Tessbach, Vienna

Overview

3

Overview

Background

Definitions and concepts

Mandatory Takeover bid

Voluntary Takeover bid

Proceedings and Timing

Selected questions

Background

5

Background

Applicable law

Austrian Takeover Act

Idea of the takeover regime

Facilitation of companies’ access to equity on good terms

Attraction of investors

Protection of shareholders

6

Background

The Austrian Takeover Act

The Austrian Takeover Act (Übernahmegesetz) first came into force in January 1999.

Material changes ever since

In particular: European Takeover Directive in 2006 (Directive 2004/25/EC of the European Parliament and of the Council of 21 April on takeover bids, Official Journal L 142/12 of 30 April 2004).

Covers Austrian takeover regulations from its scope and basic principles to more detailed information on the types of bids

7

Background

The Austrian Takeover Act: Statistics

37 takeover offers in total from 1999 - 2009

On average: 3-4 takeover offers a year

In 2000: 7 takeover offers, in 2002: 6 takeover offers

In 2006: 0 takeover offers, in 2001: 1 takeover offer

Depends partly on economic conditions

8

Background

Selected Companies for which offers have been made:

TEERAG-ASDAG (2000)

Lauda Air (2001)

Adolf Darbo AG (2002)

BauMax AG (2004)

Bank Austria Creditanstalt AG (2005)

Böhler-Uddeholm AG (2007)

To come:

Austrian Airlines AG (2009)

9

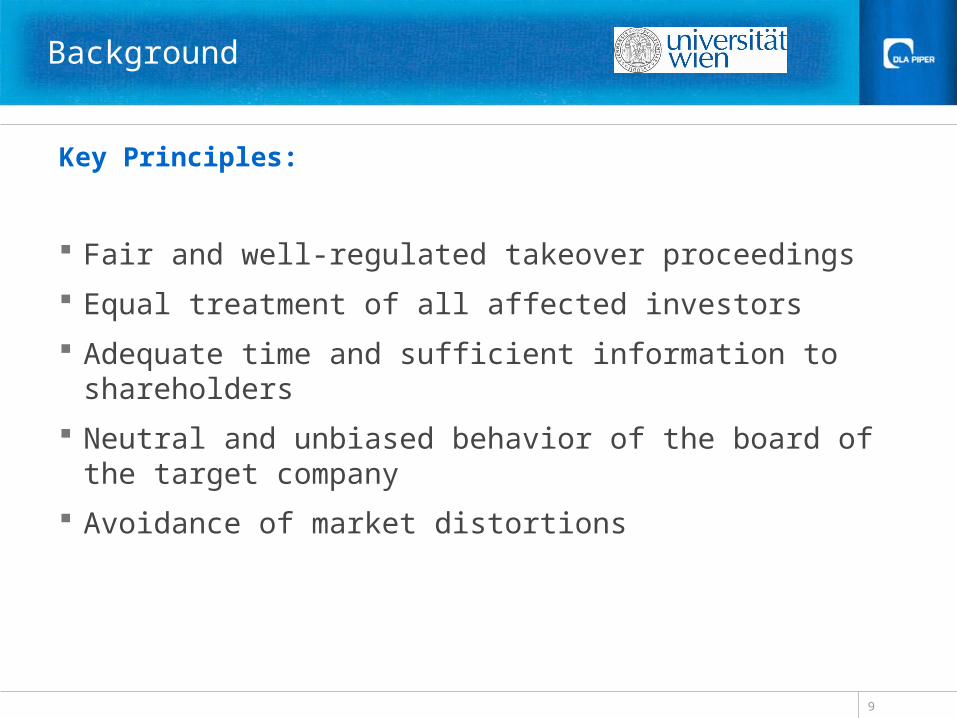

Background

Key Principles:

Fair and well-regulated takeover proceedings

Equal treatment of all affected investors

Adequate time and sufficient information to shareholders

Neutral and unbiased behavior of the board of the target company

Avoidance of market distortions

Definitions and concepts

11

Definitions and concepts

Takeover bid (bid)

A public offer made to the holders of the equities of a stock corporation (Aktiengesellschaft) to acquire all or part of such equities by consideration in cash or in exchange for other equities;

Target company

The target company is a stock corporation whose equities are the object of a bid;

Offeror (bidder)

The offeror (bidder) is any natural person, legal entity or partnership making a bid, intending to make such a bid or obligated to do so;

12

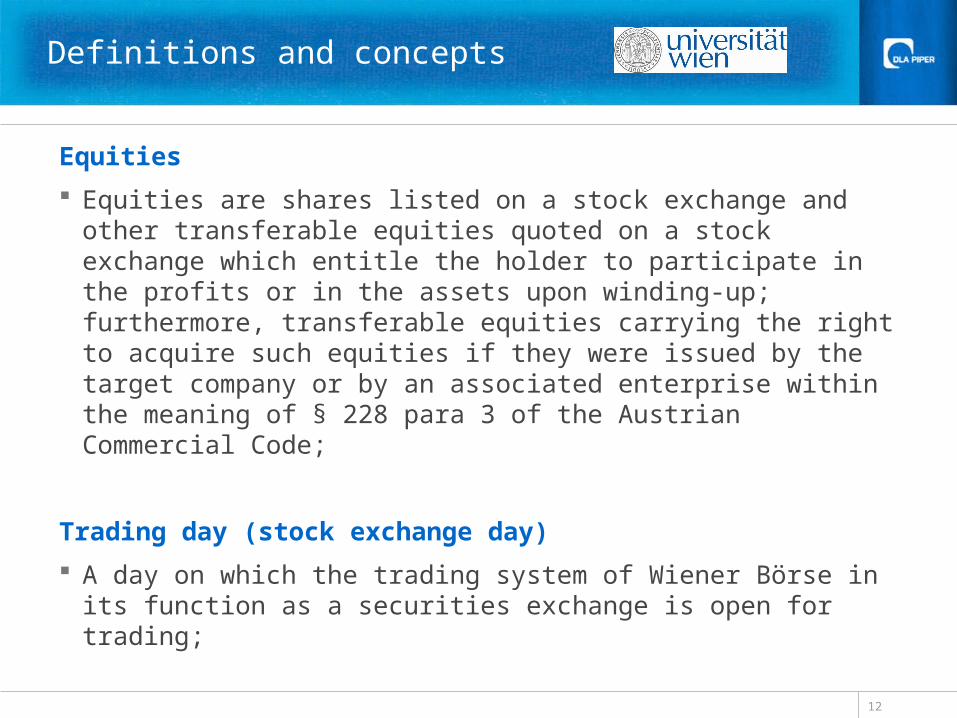

Definitions and concepts

Equities

Equities are shares listed on a stock exchange and other transferable equities quoted on a stock exchange which entitle the holder to participate in the profits or in the assets upon winding-up; furthermore, transferable equities carrying the right to acquire such equities if they were issued by the target company or by an associated enterprise within the meaning of § 228 para 3 of the Austrian Commercial Code;

Trading day (stock exchange day)

A day on which the trading system of Wiener Börse in its function as a securities exchange is open for trading;

13

Definitions and concepts

Parties acting in concert

Natural or legal persons who cooperate with the offeror on the basis of an agreement aimed at acquiring or exercising control over the offeree company, especially by concerting votes, or who cooperate with the offeree company to frustrate the successful outcome of a takeover bid. If a party holds a direct or indirect controlling interest (§ 22 para 2 and 3) in one or more other parties, it is assumed that all of these parties are acting in a concerted manner; the same applies if several parties reach agreement on the exercise of voting rights when electing the members of the Supervisory Board;

Regulated market A market contained in the list of regulated markets pursuant to Art.

16 of Directive 93/22/EEA (i.e. Official Market and Second Regulated Market of the Vienna Stock Exchange in Austria).

14

Definitions and concepts

Controlling interest

A shareholding of 30% is considered a controlling interest in the target company.

Targeting such acquisition triggers the obligation to make a mandatory public bid, to publish the bid and notified to the target company and the Austrian Takeover Commission.

No flexible concept, but rather a strict threshold (in general).

15

Definitions and concepts

Voluntary takeover bids

Not aimed at acquiring a controlling interest in the target company

Mostly realized by acquiring non-voting shares or aiming at a participation of less than 30% of the shares in total (control threshold).

Mandatory takeover bids

Aimed to obtain, either directly or indirectly, a controlling interest in a target company.

Such mandatory public bid must be made for all shares of the target company carrying profit participation rights or rights to participate in the assets upon winding-up of the company.

16

Definitions and concepts

Austrian Takeover Commission (Übernahmekommission)

the competent authority for takeover matters in Austria

consists of specialised, independent members.

independent means, that they are not subject to any instructions by any body of the public administration or dismissal.

it has exclusive competence to adopt decisions in all matters concerning the Austrian Takeover Act, ensuring increased legal certainty in the takeover matters.

decisions of the Austrian Takeover Commission do not govern future cases but serve as a measure and source of interpretation of the Austrian Takeover Act.

Mandatory takeover bid

18

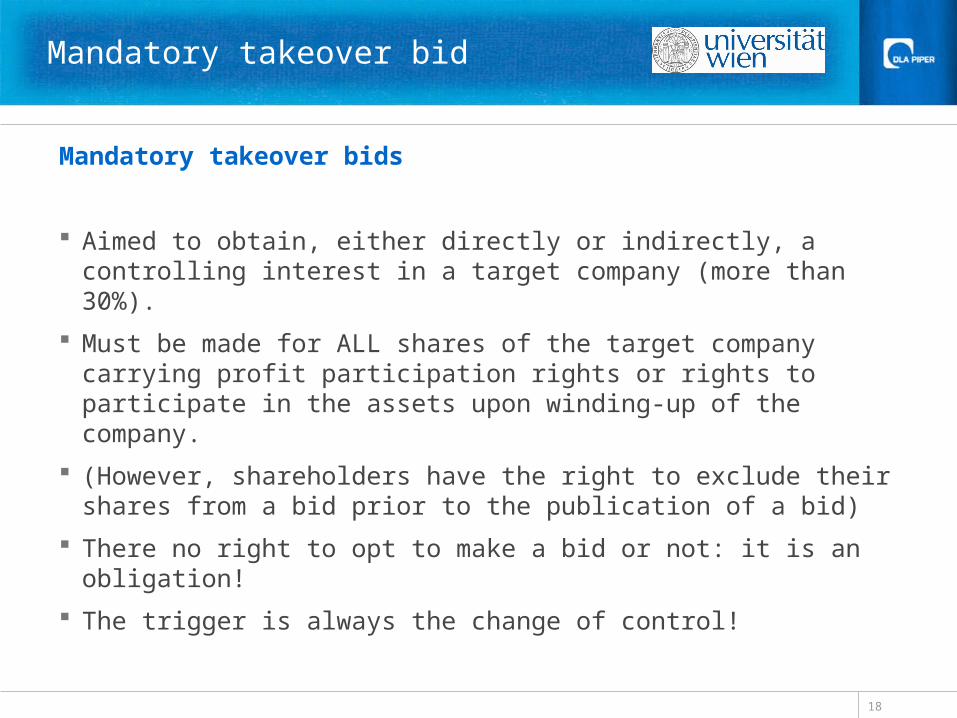

Mandatory takeover bid

Mandatory takeover bids

Aimed to obtain, either directly or indirectly, a controlling interest in a target company (more than 30%).

Must be made for ALL shares of the target company carrying profit participation rights or rights to participate in the assets upon winding-up of the company.

(However, shareholders have the right to exclude their shares from a bid prior to the publication of a bid)

There no right to opt to make a bid or not: it is an obligation!

The trigger is always the change of control!

19

Mandatory takeover bid

Procedure

Bidder has to notify the Austrian Takeover Commission of the takeover bid before the publication of such bid.

If the bidder has publicly announced its intentions to make a takeover bid: obligation to notify the Austrian Takeover Commission within 10 trading days after such announcement.

The bidder has to publish his takeover bid between the 12th and 15th trading day after such notification of the Austrian Takeover Commission. The publications must also be made in a state-wide newspaper or the official Austrian gazette (Amtsblatt zur Wiener Zeitung).

Every person aiming at obtaining a controlling interest has to ensure in advance to have sufficient means available to fulfill the (cash) consideration offered in the takeover bid. The controlling interest passively obtained is exempted from this rule.

20

Mandatory takeover bid

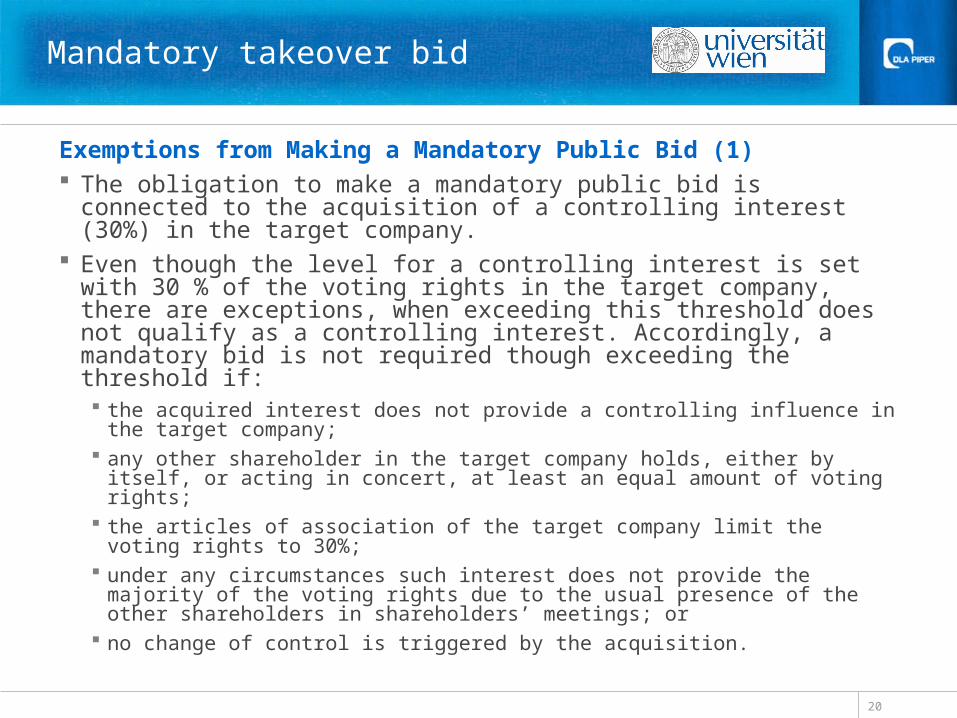

Exemptions from Making a Mandatory Public Bid (1) The obligation to make a mandatory public bid is connected to the

acquisition of a controlling interest (30%) in the target company. Even though the level for a controlling interest is set with 30 % of the

voting rights in the target company, there are exceptions, when exceeding this threshold does not qualify as a controlling interest. Accordingly, a mandatory bid is not required though exceeding the threshold if: the acquired interest does not provide a controlling influence in the target

company; any other shareholder in the target company holds, either by itself, or acting in

concert, at least an equal amount of voting rights; the articles of association of the target company limit the voting rights to 30%; under any circumstances such interest does not provide the majority of the

voting rights due to the usual presence of the other shareholders in shareholders’ meetings; or

no change of control is triggered by the acquisition.

21

Mandatory takeover bid

Exemptions from Making a Mandatory Public Bid (2)

The Austrian Takeover Act provides an example list of cases in which no change of control occurs although the 30% threshold is exceeded. Examples are, if:

the shareholder transfers shares in the target company to any legal entity in which he already holds a direct or indirect controlling interest (downstream restructuring);

the shares are transferred to a legal entity holding a direct or indirect controlling interest in the transferring shareholder (upstream restructuring);

the transferring shareholder transfers the shares to a private foundation (Privatstiftung) with a management exclusively under his controlling influence; or

if the controlling influence does not change as a result of the execution of termination of a voting agreement.

22

Mandatory takeover bid

Exemptions from Making a Mandatory Public Bid (3a)

Further exemptions from the mandatory takeover bid are if:

Upon the acquisition of an indirect controlling interest, the book value of the direct interest in the target company amounts to less than 25% of the book-entry net asset value of the legal entity holding the direct controlling interest.

The shares are acquired exclusively for the purpose of reorganizing or securing receivables of the target company.

The number of voting rights required constituting a controlling interest is exceeded only temporarily and such excess is reversed immediately.

The shares are acquired by way of donation between certain relatives, heredity or a splitting of assets due to a divorce, annulment or invalidation of a marriage.

23

Mandatory takeover bid

Exemptions from Making a Mandatory Public Bid (3b)

Further exemptions from the mandatory takeover bid are if: Shares are transferred to another legal entity in which only certain

relatives of the former shareholder are directly or indirectly holding shares; the same applies for the transfer to a private foundation, provided those relatives can exercise a controlling influence on the management.

The offeror squeezes out the remaining shareholders of the target company according to the Austrian Squeeze-out Act within five months following the obtainment of the controlling interest; in such case the compensation has to equal the highest price paid or appointed for the timeframe until the registration of the squeeze-out to the companies’ register.

Such exemptions are subject to evaluation by the Austrian Takeover Commission which may impose certain obligations on the respective shareholder.

Requirement to notify the takeover Commission within 20 trading days.

24

Mandatory takeover bid

Exemptions from Making a Public Bid: Passive obtainment of control

Shareholder obtains control of the target company, (unconditionally) not by acquiring additional shares, but solely due to another shareholder reducing its shareholding to a non-controlling level.

The shareholder has to proof that it had no reason to expect it would gain a controlling interest and neither caused it (particularly by acquiring shares). The Austrian Takeover Commission will have to be notified in such case without undue delay, at least within 20 trading days.

Voting rights of the respective shareholder passively obtaining control limited to 26%.

The respective shareholder may though apply to the Austrian Takeover Commission to rescind such limitation and impose any other restrictions or conditions the Commission considers to unfold equivalent protection of the other shareholders of the target company.

25

Mandatory takeover bid

Pricing of a mandatory bid (1)

The price of a mandatory bid shall not be less than

the highest consideration in money paid or agreed on for those shares of the target company or any parties acting in concert with it within the preceding 12 months before the announcement of the bid, or

the price shall correspond at least to the average exchange price weighted by the respective trading volumes of the respective equities in the past six months before the day on which the intention to make a bid was announced.

26

Mandatory takeover bid

Pricing of a mandatory bid (2)

Always a cash offer required!

Shares can be offered alternatively, but not exclusively!

27

Mandatory takeover bid

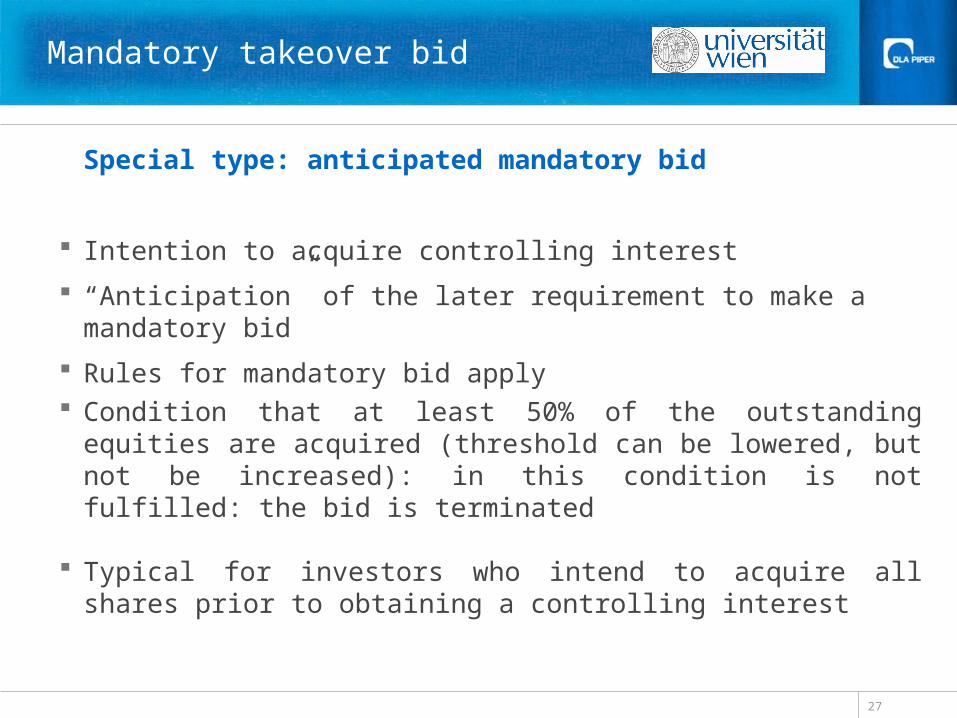

Special type: anticipated mandatory bid

Intention to acquire controlling interest

“Anticipation” of the later requirement to make a mandatory bid

Rules for mandatory bid apply Condition that at least 50% of the outstanding equities are acquired

(threshold can be lowered, but not be increased): in this condition is not fulfilled: the bid is terminated

Typical for investors who intend to acquire all shares prior to obtaining a controlling interest

Voluntary takeover bid

29

Voluntary takeover bid

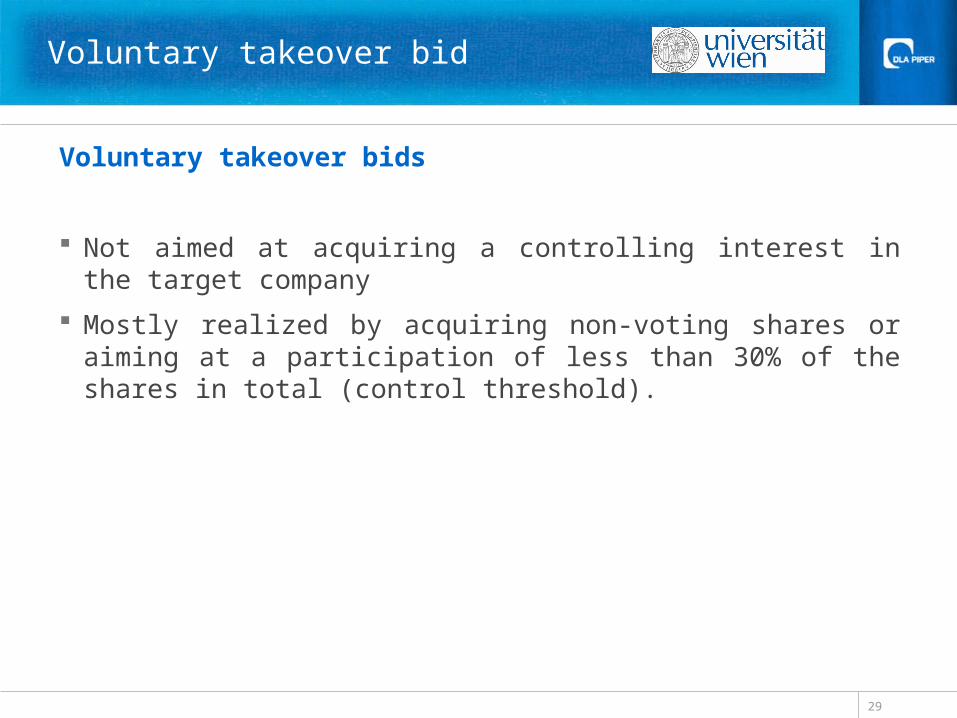

Voluntary takeover bids

Not aimed at acquiring a controlling interest in the target company

Mostly realized by acquiring non-voting shares or aiming at a participation of less than 30% of the shares in total (control threshold).

30

Voluntary takeover bid

Voluntary takeover bids

Rules for mandatory public bids are largely applicable to voluntary bids.

A voluntary public bid can be submitted by any person at any time, provided the bidder has secured sufficient finance to provide the required consideration.

Failing a public bid though results in a blockage for one year (commencing from the publication of the offer results) for:

submitting a voluntary public bid for shares of the same target company; and

acquiring shares in that target company that would trigger the obligation to submit a mandatory public bid.

31

Voluntary takeover bid

Pricing rules

No pricing rules apply.

Acquisition can be targeted at a certain percentage (e.g. 10% or 15%).

Proceedings and timing

33

Proceedings and timing

Minimum timing

Day 1: Announcement of the intention to make a takeover bid.

Day 14: Filing of the offer documentation to the Takeover Commission within ten trading days (which is about two weeks) from the announcement of the intention to make a takeover bid (may be extended to a maximum of 40 days upon request).

Day 26: Publication of the offer documentation (at the earliest on the 12th and at the latest on the 15th trading day after providing the offer documentation to the Takeover Commission. This is the begin of the acceptance period.)

Day 40: End of acceptance period (the acceptance period must last at least two weeks and at most ten weeks).

34

Proceedings and timing

Minimum timing

Day 41 (or 42): immediately after the end of the acceptance period: publication of the result in the takeover bid

Another 3 months acceptance period for those holders of equities who have initially not accepted the offer in the case of

A mandatory takeover bid

A voluntary bid which has led to a shareholding of more than 90% of the bidder after the bid

A voluntary bid which has been subject to a minimum condition and such minimum condition has been fulfilled

35

Proceedings and timing

Offer documentation

the content of the bid;

details on the offeror and if applicable any parties acting in concert;

the quantity of shares in the target company, the public bid is aiming at, including information on targeted minimum and/or maximum thresholds;

terms and conditions under which the shares shall be acquired, in particular the acceptance period and offer price;

conditions and rights of withdrawal;

details on the offeror’s intentions regarding the future business of the target company; and

applicable law and jurisdiction.

36

Proceedings and timing

Offer documentation

Expert needs to be involved on the side of the bidder:

Expert reviews offer documentation and confirms compliance with law and correctness of the offered price

Usually auditors act as experts (banks would also be eligible)

Insurance required! (expensive!)

Once the offer is published:

Management board and supervisory board of the target company provide statement on the offer

Expert of the target company also needs to written provide statement

37

Proceedings and timing

38

Proceedings and timing

Selected questions

40

Selected questions

Creeping-in

Creeping-in is raising a controlling interest that has not reached a majority (50 % or more) of the voting rights of the target company.

If this interest is raised by more than 2% within 12 months the bidder is forced to make a mandatory public bid. This rule shall prevent a creeping into a majority of voting rights while circumventing takeover regulations.

E.g.: investor holds 40%; such investor may only acquire 2% within a year (resulting in 42%).

If a higher stake is acquired within a year: obligation to launch a mandatory bid

41

Selected questions

Shareholders’ agreements (Syndicate agreements)

Formation, change and dissolution of a shareholders’ agreement may trigger a mandatory bid (constituting a change of control)

Basically two types of syndicates:

Subordination syndicate

Unanimity syndicate

Change of control within the syndicate is trigger for mandatory bid

42

Selected questions

“Safe harbour”

Interest between 26% and 30% of voting rights: no obligation to make a mandatory public bid.

But: obligation to notify the Austrian Takeover Commission within 20 trading days and the voting rights of the respective shareholder will be statutorily limited to 26%. Such limitation does not apply if:

another shareholder acting alone or in concert holds at least an equal amount of voting rights;

the voting rights are limited to 26% by the articles of association; or

there is no actual change of control.

Nevertheless, the Austrian Takeover Commission can rescind such limitation of voting rights on application.

43

Selected questions

Parallel purchases

Possible to purchase shares during a takeover offer.

But: if offer price is exceeded, such price has to be paid to all other shareholders

44

Selected questions

Notification requirements

Exceeding or falling below 5%, 10%, 15%, 20%, 25%, 30%, 35%, 40%, 45%, 50%, 75% and 90% triggers obligation to inform the target company, the stock exchange and the Financial Market Authority

Neutrality and objectivity

Management board and supervisory board of the target company must not take any action which hinders the shareholders to freely evaluate and accept the offer.

Any existing “hindering actions” require the consent of the shareholders’ meeting

45

Selected questions

Competing bids

A bid for the same shares in the target company, competing against a voluntary or mandatory public bid may be published at any time.

Shareholders who have accepted the first public offer are granted the right of withdrawal of their acceptance until the last four trading days preceding the expiration of the first public offer’s acceptance period.

This time based limitation serves as a prevention of last minute offers in the ultimate, most decisive phase of the bid.

Should the shareholders however remain inactive, their declaration of acceptance persists unhindered.

46

Selected questions

Blocking period / Failure of a bid

In case a bid fails, the bidder (and any parties acting in concert) are blocked from either making another bid for the target company or acquiring shares in the target company to an extent that would trigger an obligation to make a mandatory public bid for one year commencing the publication of the results of the bid.

The same applies for certain circumstances under which the information of an envisaged bid has become publicly known.

The Austrian Takeover Commission may limit the blocking period.

47

Selected questions

Merger control

Acquisitions of at least 25% of a company’s shares or any other kind of association between companies which enables a company to exercise a controlling influence over the other company is subject to merger control under the Austrian Cartel Act or EU law.

Mandatory bids can usually not be subject to conditions, except for the condition of merger clearance or other regulatory approvals (banking, insurance etc).

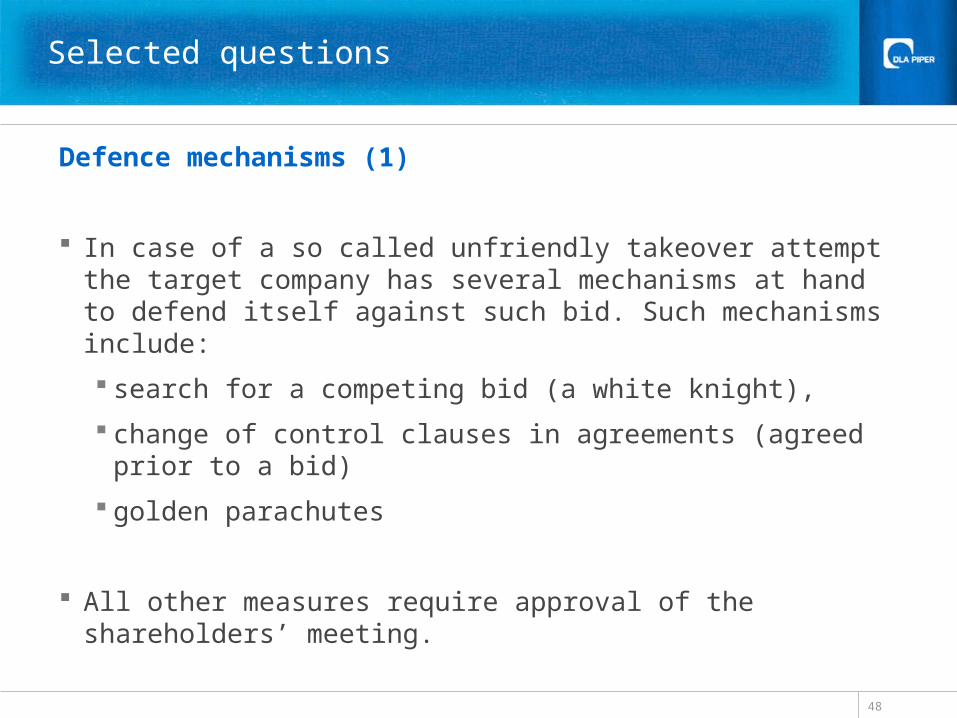

48

Selected questions

Defence mechanisms (1)

In case of a so called unfriendly takeover attempt the target company has several mechanisms at hand to defend itself against such bid. Such mechanisms include:

search for a competing bid (a white knight),

change of control clauses in agreements (agreed prior to a bid)

golden parachutes

All other measures require approval of the shareholders’ meeting.

49

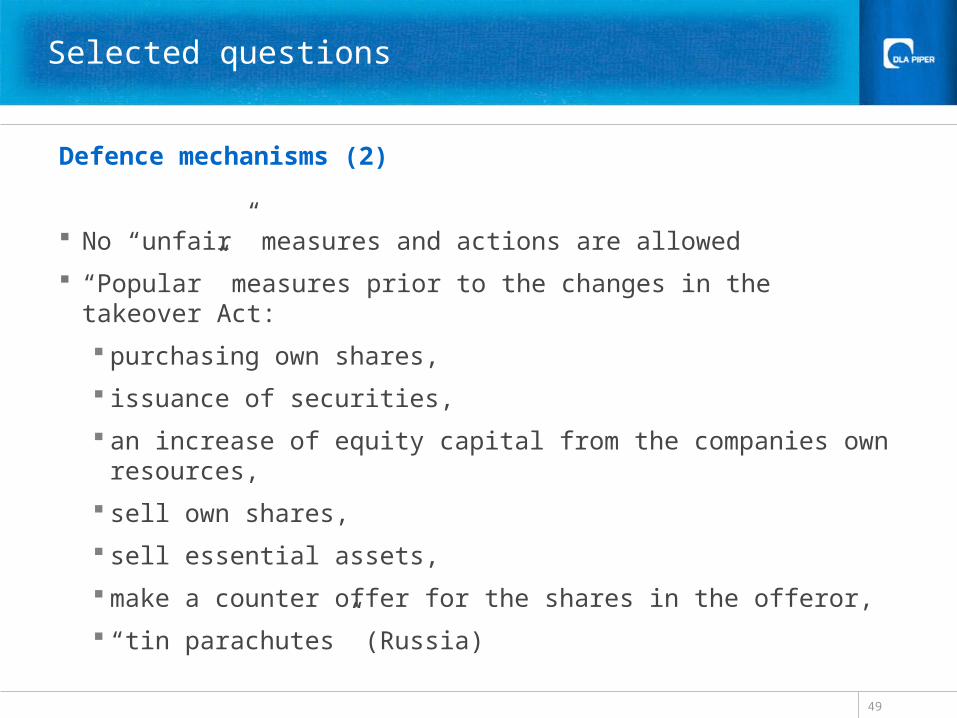

Selected questions

Defence mechanisms (2)

No “unfair” measures and actions are allowed

“Popular” measures prior to the changes in the takeover Act:

purchasing own shares,

issuance of securities,

an increase of equity capital from the companies own resources,

sell own shares,

sell essential assets,

make a counter offer for the shares in the offeror,

“tin parachutes” (Russia)

END

Thank you for your attention!