Table of Contents - o2.co.uk · Table of Contents i Table of Contents INTRODUCTION.....1

2017 | RISK MANAGEMENT ANNUAL REPORT | 1

TABLE OF CONTENTS

1. Executive Summary

2. Introduction

2.1 Regulatory Environment

2.2 The Scope

2.3 Risk Policy Framework in Banco Santander (Mexico)

3. Integral Risk Management

3.1 Basic Principles of Integral Risk Management

3.2 Instruments for proper Integral Risk Management

3.3 Management and control of risks

3.4 Governance Structure for Integral Risk Management

3.5 Risk Information Management

3.6 Risk appetite

4. Credit Risk Management

4.1 General Aspects

4.2 Credit Risk Cycle

4.2.1 Risk Study

4.2.2 Planning and setting boundaries

4.2.3 Decision on operations

4.2.4 Monitoring

4.2.5 Measurement and Control

4.2.6 Recovery Procedure

4.3 Risk Mitigation Techniques

4.4 Methodologies for Calculating Reserves for Credit Risk

4.4.1 Regulatory framework

4.4.2 Portfolios Authorized to Banco Santander (Mexico) for the use

of internal Calculation of Reserves for Credit Risk

Methodologies

4.4.3 Principles of the Rating System Applied in Banco Santander

(Mexico)

4.4.4 Main Characteristics of Internal Methodologies with Foundation

Approach Authorized to Banco Santander (Mexico)

4.4.5 Main Characteristics of Internal Methodologies with Advanced

Approach allowed to Banco Santander (Mexico)

4.4.6 Internal Rating Systems Control

4.5 Counterparty Risk and Financial Instrument Transactions

2017 | RISK MANAGEMENT ANNUAL REPORT | 2

4.6 Securitization Exposures Information

4.7 Distribution of Exposures by Credit Risk

4.7.1 General Aspects

4.7.2 Exposure by Portfolio Type

4.7.3 Exposure by Remaining Term

4.7.4 Exposure by Federative Entity

4.7.5 Estimates of Credit Risk by Federative Entity

4.7.6 Portfolio Companies by Economic Sector Exposure

4.7.7 Estimates for Credit Risk by Economic Sector Portfolio

Companies

5. Market Risk Management Trading Activity

5.1 Activities Subject to Market Risk Trading

5.2 Basic Principles in Risk Management Market Trading

5.3 Key processes in Risk Management Market Trading

5.4 Trading Market Risk Control

A. Trading Market Risk Metrics

B. Trading Market Control Risk Procedures

C. Figures from the Reporting Period

5.5 Derivative Financial Instruments

6. Structural Risk Management

6.1 Activities subject to Structural Risk

6.2 Basic Principles on the Structural Risk Management

6.3 Key Processes in the Structural Risk Management

6.4 Control of structural risks

A. Figures from the Reporting Period

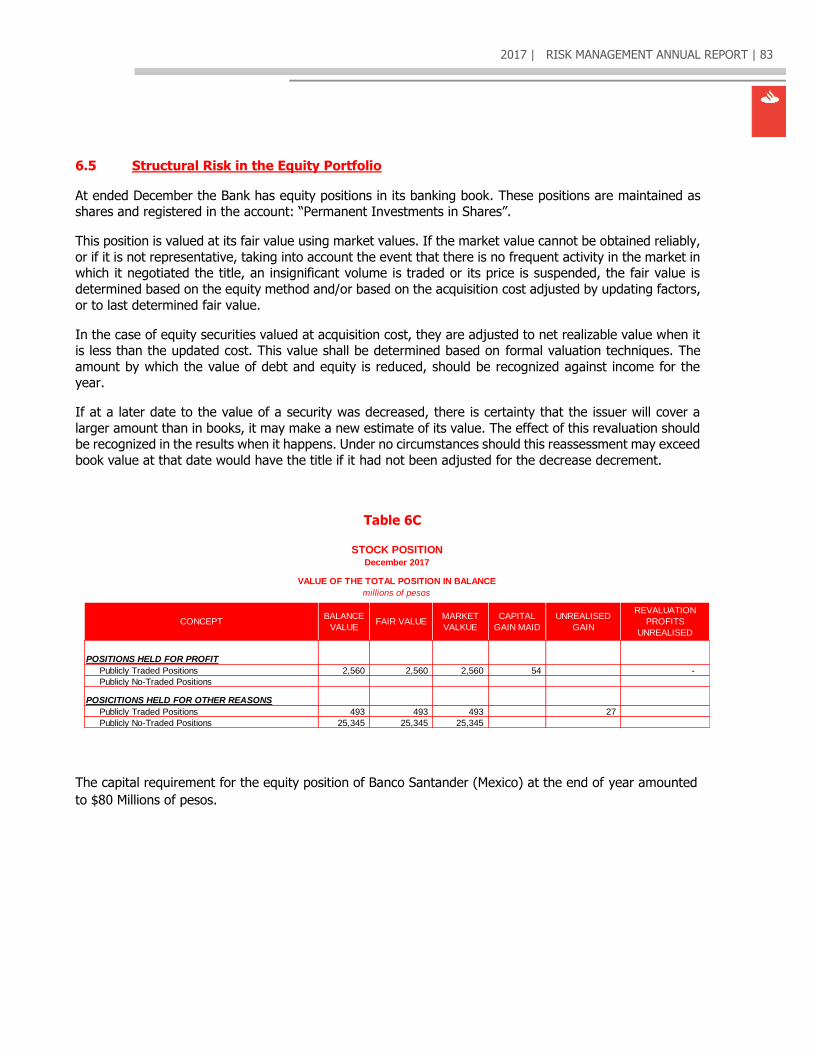

6.5 Structural Risk in the Equity Portfolio

7. Liquidity Risk Management

7.1 Activities subject to Liquidity Risk

7.2 Basic principles on Liquidity Risk Management

7.3 Key Procedures in the Liquidity Risk Management

7.4 Control of Liquidity Risk

A. Figures from the Reporting Period

2017 | RISK MANAGEMENT ANNUAL REPORT | 3

8. Operational Risk Management

8.1 General Aspects

8.2 Operational Risk Control

9. Capital

9.1 General Aspects

9.2 Function of the Capital

9.3 Calculation of the Capital Requirement for Credit Risk

9.4 Calculation of the Capital Requirement for Counterparty Risk

9.5 Calculation of the Capital Requirement for Market Risk

9.6 Calculation of the Capital Requirement for Operational Risk

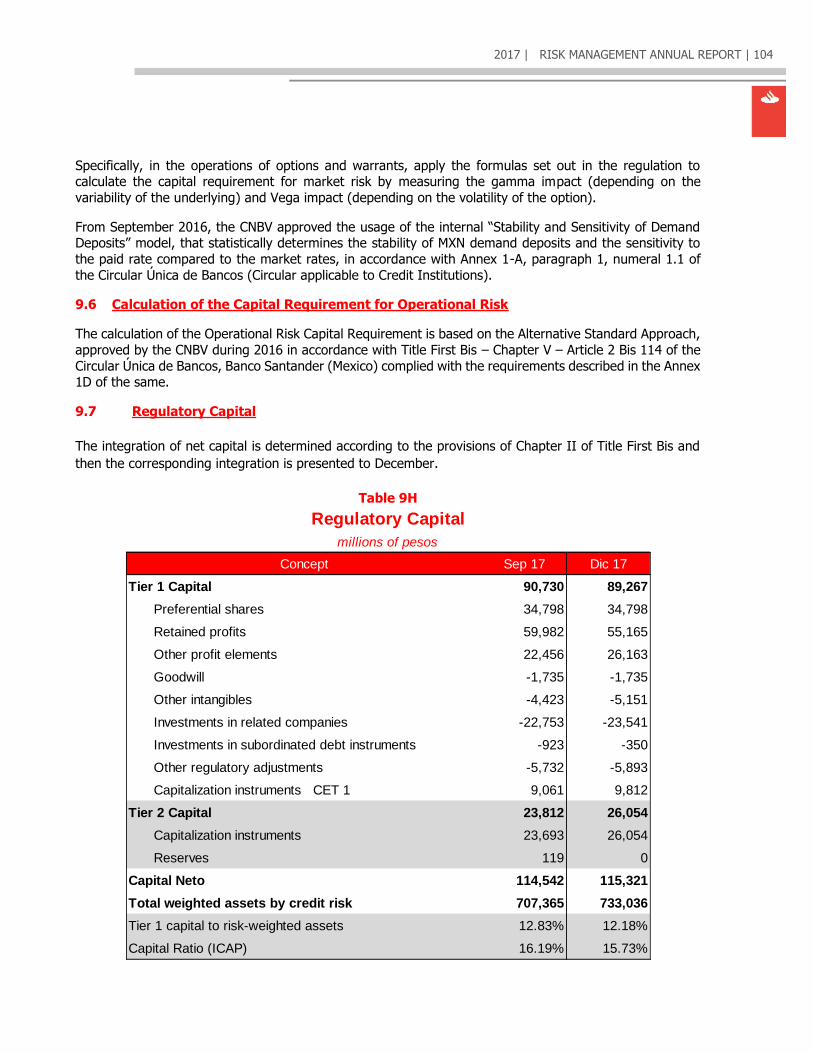

9.7 Regulatory Capital

2017 | RISK MANAGEMENT ANNUAL REPORT | 4

1. Executive Summary

With the publication of this report, Banco Santander (Mexico) complies with the obligation set forth in Article

88 of the CUB where banking institutions are obliged to disclose to the public, through its website, information on the comprehensive risk management that takes place on a daily basis in the institution.

Specifically, banking institutions are required to publish the objectives and policies for managing each of

the different types of risk faced, including their strategies, processes, methodologies and levels of risk assumed. The information to be published is classified as both quantitative and qualitative. Quantitative

information shall be disclosed quarterly and qualitative information may be disclosed annually.

The views expressed in this report and statistical information included (unless otherwise stated) comprises

the following institutions:

a) Banco Santander (México), S.A., Institución de Banca Múltiple, Grupo Financiero Santander México. b) Santander Hipotecario, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada.

Grupo Financiero Santander México. c) Santander Vivienda, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo

Financiero Santander México.

d) Santander Consumo, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo Financiero Santander México.

e) Santander Inclusión Financiera, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo Financiero Santander México1.

Through December 2016, the Extraordinary Stockholders General Assemblies of Santander Hipotecario S.A. de CV. and Santander Vivienda S.A de CV. took place, in which the merge of both entities was agreed,

Santander Hipotecario will be the merged company and Santander Vivienda the merger company.

This report is prepared in accordance with applicable mexican regulations in determining exposures, capital requirements for risks and reserve estimate.

Chapter 1 includes this Executive Summary.

Chapter 2 includes generally the Regulatory Framework for Risk within Banco Santander (Mexico).

Meanwhile Chapter 3 deals with Integral Risk Management, and outlines the basic principles and tools for

proper Risk Management. It stresses that for the management of risk inherent in the Bank's operations, it is essential to understand and determine the behaviour of its financial situation and for the creation of a

long-term value, fully attached to the regulatory requirements established by the CNBV (Spanish acronym

for National Banking and Exchange Commission) and Banco de Mexico.

It also delineates how the management and risk control is structured in three lines of defence to develop

three distinct functions:

a) First line of defence: Risk management from its genesis.

1 At the end of December 2017, 3 credits to 26 clients were given, reporting a total investment of MXN105,000, with

an expected loss of MXN2,798. In the information reported in this document, this figures are included in credit to individuals (consumer).

2017 | RISK MANAGEMENT ANNUAL REPORT | 5

b) Second line of defence: responsible for overseeing risk-taking activities across the bank and report

to senior management on risk related items.

c) Third line of defence: Independent review of the risk activity.

Banco Santander (Mexico) has an agile and efficient governance structure that, among other things,

ensures: (i) the participation in risk decisions and in monitoring and control of the governing bodies and senior management; (ii) coordination between the different lines of defence set the functions of

management and risk control; (iii) the alignment of objectives, the monitoring of compliance and the implementation of corrective measures, and (iv) the existence of an adequate environment management

and risk control.

Risk management and control require a high availability of hard data, capacity to analyse these data, and

solid reporting procedures. Banco Santander (Mexico) management of risk information is governed by principles such as responsibility; technology architecture; risk data reconciliation; availability data;

completeness and comprehensiveness; data quality indicators; quality control data; readiness; flexibility and adaptability; prospective approach and availability of documentation; data analysis and expert

judgment.

The third chapter also defines the risk appetite as the maximum level and type of risk that the organization is willing to take, within its risk capacity to achieve its strategic objectives and the development of its

business plan.

Chapter 4 describes major policies and fundamentals for credit risk management, as well as the detail of the key features of the methodologies to qualify the portfolios and determine the amount of the reserves

for credit risk.

From the point of view of credit risk management, segmentation is based on the distinction between three

types of customers:

Individuals: Includes all private persons, except those with an entrepreneurial activity. It

comprises portfolios of non-revolving mortgage loans for housing, credit card and consumer loan

not revolving portfolio.

SMEs, companies and institutions: involves natural and juridical persons with business activity,

as well as public and private entities of non-profit sector.

Global Corporate Banking (GCB): It consists of corporate, financial and sovereign institutions,

which make up a closed list, which is reviewed annually.

Credit Risk goes through a cycle or life process, whose phases are valid for any operation, notwithstanding the important differences that can be seen in the cycles of the risks of different segments, specifically

between the private persons and the companies. 2

Three stages are differentiated in the cycle of credit risk: pre-sale, sale and after-sales.

This process is constant feedback, joining into the study of the risk and into the pre-sale planning and the

2 The processes belonging to the pre-sale stage are those referring to the study of risk and are conducted as a prelude

to the credit risk approval step. The processes that belong to the sales phase are those that take place during the decision approving stage. Finally, the after-sales processes are those that take place after the approval of credit risk.

2017 | RISK MANAGEMENT ANNUAL REPORT | 6

results and conclusions of the after-sales phase.

The processes that take place in each of the above phases are:

a) Study of risk and credit rating procedure.

b) Planning and setting limits.

c) Decision on operations.

d) Monitoring.

e) Survey and Control.

f) Recovery management.

This chapter also details how credit risk is mitigated in general terms, through the use of securities. A

security is defined as a measure of reinforcement added to an operation of credit in order to mitigate the loss in breach of the payment. The security is a component that mitigates the severity of the operation in

case of default. The purpose of the security is to bring down the final operating loss, among other cases, where a long-term operation increases the risk of damage to the customer or because of possible and

relevant external events that could jeopardize the success of the operation and to the creditor, it is difficult

to manage.

Likewise, Chapter 4 explains clearly the criteria under which admission and security management are

governed:

a) Expressly, subsidiary, accessory and essential character of the sureties.

b) Prudent and expert assessment.

c) Rating upgrade.

d) Securities correct Instrumentation.

e) Cautions on the conservation and availability of security.

f) Capacity of execution and settlement of surety.

g) Security block.

h) Security amendment.

i) Security implementation.

j) Security expiration.

Based on CUB provisions, this chapter explains that in order to calculate the reserves for Credit Risk,

institutions may use:

a) Standard Method.

b) Some of the methods based on internal ratings, basic or advanced, provided prior authorization

from the CNBV.

Since 2012 the CNBV authorized Banco Santander to use internal methodologies with the Foundation

Approach3 to corporate businesses, Global Corporate Banking, financial institutions, banks and SME’s. In

3 Under internal Methodologies with Foundation Approach (FIRB), the institutions obtained the Probability of Default

on its positions subject to credit risk, while for the rest of the components of risk, the institutions must conform to the provisions in accordance to Paragraph C Section Three of CUB.

2017 | RISK MANAGEMENT ANNUAL REPORT | 7

October 2015, it allowed the use of internal methodologies with advanced approach4 for calculating credit

reserves for portfolios of SME’s and property developers.

The rest of the chapter details the main features of the internal methodologies authorized to Banco

Santander (Mexico) and includes quantitative information on major exposures of the institution to credit risk. There is also a section on the counterparty risk, which is the one that the institution assumes with

Government, government agencies, financial institutions, corporations, companies and individuals in its Treasury and correspondent banking activities. The survey and control of the credit risk on financial

instruments, counterparty risk, is conducted by a specialized unit and with organizational structure independent of the business areas and control of this type of risk is performed daily, which allows to know

the line of credit available with any counterparty.

Chapter 5 provides information on the activities subject to trading market risk and discusses its

development during this year. It also describes the different methodologies and metrics used in the institution. The perimeter of identification, measurement, control and monitoring of the market risk function

covers those operations that assume the equity risk. The survey of market risk quantifies the potential change in value of the positions taken as a result of changes in market risk factors. The risk arises from

changes in risk factors: interest rate, exchange rate, equity, credit spread and volatility of each of the above, and liquidity risk of the various products and markets in which it the institution operates.

Trading activities include both the provision of financial services to customers, in which the entity is the counterpart, as the activity of sale and own positioning in financial instruments. This heading provided the

positions, which the entity keeps in their trading books. The basic principles of the Trading Market Risk

Management are based on:

a. Independence of trading activities and balance sheet management.

b. Overview of risk assumed.

c. Definition of limits and allocations.

d. Control and monitoring.

e. Homogeneous and aggregated metrics.

f. Consistent and documented methodology.

Additionally, the Chapter 5 explains the metrics and processes used for the trading market risk control:

Metrics:

Value at Risk (VaR).

Stressed VaR.

Value at Earnings (VaE).

Scenario Analysis.

Trading Market Risk Limits Trading.

Proceedings:

Market data retrieval.

Analysis of the metrics and trading market risk positions.

Control of the excesses of limits and products authorized.

Control of insurance operations.

4 In the case of internal Methodologies with Advanced Approach (AIRB), the institutions estimate the Probability of

Default, Loss Given Default, Exposure at Default and Maturity Term.

2017 | RISK MANAGEMENT ANNUAL REPORT | 8

Control of assessment model.

Control of long and short positions.

Control of liquidity.

Price control.

Financial Settlement.

The rest of the chapter includes quantitative information on this type of risk.

Chapter 6 contains information very similar to the one presented in Chapter 5 but in reference to the structural risks. Structural risks consist of market risks inherent in the institution's balance sheet, excluding

negotiation portfolios. This risk includes both losses from price variation affecting the sale and maturity

portfolios available, as losses arising from the management of assets and liabilities. The main structural risks are the following:

Structural Interest Rate risk.

Structural Change Risk.

Structural Equity Risk.

Inflation risk.

Market Liquidity Risk.

Prepayment or Cancellation Risk.

As part of the financial management of the institution, Chapter 6 examines the sensitivity of the financial

margin and the equity value of the various items of the balance sheet against changes in interest rates. This sensitivity arises from gaps in the dates of maturity and modification of interest rates occurring in the

different categories of assets and liabilities. The rest of the chapter discusses the quantitative information on this type of risk.

Chapter 7 is very similar to the previous two chapters but deals with liquidity risk, which is fixed as the

possibility of defaulting obligations on time or with excessive costs. The types of losses caused by these risk losses include enforced sales of assets or impacts on margin by the mismatch between cash outflows and

inflows forecasts. This is the risk of loss of value of the buffer of liquid assets of the entity and is responsible

for the variation of its operating value (derivatives and securities, etc.) which may involve additional collateral requirements and, therefore, worsening liquidity. Liquidity risk is classified into the following

categories:

a) Financing Risk. b) Mismatch Risk.

c) Contingency Risk.

The metrics that Banco Santander (Mexico) used for monitoring and controlling of liquidity risk are:

Ratio of Structural Finance.

Liquidity horizon for a local systemic crisis.

Liquidity Risk Limits.

Liquidity Gap.

Available Liquidity.

Concentration of Funding Sources.

Stress Test.

Liquidity coverage ratio (LCR)

Net Stable Funding Ratio (NSFR)

2017 | RISK MANAGEMENT ANNUAL REPORT | 9

The rest of the chapter includes quantitative information on this type of risk.

Chapter 8 describes the main policies and principles for the management of the operational risk, covering

losses by failures or deficiencies in internal controls, errors in processing and storage operations or transmission of information, as well as adverse administrative and judicial resolutions, fraud or theft, and

comprises, among others, technological and legal risks.

For the identification and grouping of operational risks the different categories and business lines defined by both local regulators and the supervision of the institution they are used. The methodology is based on

the identification and documentation of risks, controls and related processes also uses quantitative and

qualitative tools such as self-assessment questionnaires, the development of historical databases and operating risk indicators, to name a few, both control and mitigation, and disclosure thereof.

For the calculation of regulatory capital required for operational risk the Basic Indicator Approach as defined

in the CUB, published by the CNBV it is used.

Chapter 9 of this report describes the main policies and principles for capital management of the institution and how to calculate the capital requirement. Special mention is made to the internal methodology

authorized for use by Banco Santander (Mexico) by the CNBV to calculate its capital requirement for credit risk.

Capital management in the institution seeks to ensure the solvency of the company and maximize

profitability, ensuring compliance with internal capital targets and regulatory requirements. It is an essential tool for making strategic decisions in their management using the established objectives in determining the

Appetite Risk, planning and Capital budget, as well as the use of metrics that allow to evaluate the

profitability and the creation of their business value.

Capital management begins with the following key aims:

1. Capital Budget.

2. Planning Capital.

3. Establishment of Risk Appetite.

4. Minimum criteria.

Capital policies that set the general guidelines are specified, which must govern the actions of the areas involved in the processes of management and control of capital.

Autonomy of the Capital.

Centralized Monitoring.

Proper distribution of own resources.

Strengthening Capital.

Capital Preservation.

Prudent management.

Maximizing value creation.

The rest of the chapter includes quantitative information on capital management and some metrics as the

probability of default and the credit risk weights.

2017 | RISK MANAGEMENT ANNUAL REPORT | 10

2. Introduction

2.1 Regulatory Environment

During 2017 a number of amendments to the general provisions applicable to credit institutions (Circular

Applicable to Credit Institutions, CUB) were made; mainly seeking stability and the correct functioning of the Financial System, also aiming to decrease cost of credit, enhance Bank’s security and continue aligning

the Mexican Regulation with international regulative standards (Basel)5.

Also in this year amendments were issued on:

Credit Risk: Revolving Consumption Credit Score Methodology

In order to better reflect the credit risk incurred by credit institutions:

The rating methodology of the non-revolving and mortgage credit portfolios and their

associated regulatory reports are updated by incorporating new dimensions of credit risk,

such as the level of indebtedness of each client, their payment behavior in other financial and non-financial entities, as well as the specific risk profile of each product.

A portfolio rating methodology for microcredits is established.

The loss severity estimation is specified for the calculation of preventive reserves, when the collateral guarantees are recognized, in order to reduce the amount of preventive reserves derived from the credit

portfolio rating, similarly, the term to constitute 100% of the amount of credit risk reserves that correspond to portfolios of non-revolving consumer, mortgage and microcredit is extended, in accordance with the new

applicable methodology, also the time Financial Institutions should disclose such information in their financial statements and through other public communications is specified.

Credit Risk: Agricultural loans credit score methodology

The prices’ coverage that some borrowers have is recognized in the calculation of preventive reserves for

credit risk for agricultural loans, in order to adequately reflect the risk incurred by the institutions.

Counterparty Risk

A weighted credit risk equal to 0% is established for the operations carried out by credit institutions with

Banco de Mexico, which are subject to an additional capital requirement due to credit valuation adjustments for derivative transactions.

Capital Risk

In order to align the applicable treatment to the implicit support scenario with the international standards

issued by the Basel Committee for Banking Supervision, and adequately reflect the risk incurred by credit institutions when they update the assumption of granting implicit support to securitization structures in

which they act as originators or transferors of the underlying assets, and avoid excessive capital

requirements when updating those assumptions, the obligation of maintaining capital for all the underlying

5 Reference: CNBV regulatory newsletter; released at www.cnbv.gob.mx

2017 | RISK MANAGEMENT ANNUAL REPORT | 11

assets of the current securitization schemes is limited only to the securitization structures for which implicit support had been granted.

Clarifications are made in the capital requirement definition which credit institutions must have to support

their credit risk; the treatment to be applied by credit institutions for the calculation of market risk capital

requirements is modified for the investments they make in social equity of brokerage houses and securities’ deposit institutions in order to reflect their risk as any other similar instrument; regarding the use of internal

models, credit risk measurement of portfolios granted to micro, small and medium enterprises is improved.

Market risk

The accounting criteria applicable to credit institutions’ held to maturity securities is adjusted extending the

period by which they may be sold or reclassified before their maturity, without affecting the ability to use

the securities’ category.

Additionally, in order to achieve greater adherence and consistency with the international regulations

established in the International Financial Reporting Standards, the requirements of isolated events that are outside the control of the credit institution are specified.

Operational Risk

The procedures and mechanisms that credit institutions use to identify any possible client identity

supplanting are strengthened.

Feasibility Plans

It is specified that only Banks classified as Domestic Systemically Important Banks, will be required to

update their contingency plans during March of each year, while the rest of the institutions must do it every two years.

2.2 Scope

The information in this report, as well as including statistical data (unless otherwise stated) comprises the

following institutions:

a) Banco Santander (México), S.A., Institución de Banca Múltiple, Grupo Financiero Santander México. b) Santander Hipotecario, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada.

Grupo Financiero Santander México. c) Santander Vivienda, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo

Financiero Santander México.

d) Santander Consumo, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo Financiero Santander México.

e) Santander Inclusión Financiera, S.A. de C.V., Sociedad Financiera de Objeto Múltiple, Entidad Regulada, Grupo Financiero Santander México.

2017 | RISK MANAGEMENT ANNUAL REPORT | 12

It is important to recall that through December 2016, the Extraordinary Stockholders General Assemblies of Santander Hipotecario S.A. de CV. And Santander Vivienda S.A de CV. took place, in which the merge of

both entities was agreed, Santander Hipotecario will be the merged company and Santander Vivienda the merger company.

This report is prepared in accordance with applicable Mexican regulations in determining exposures, capital

requirements for risks and reserve estimate.

Statistical information as well as accounting financial statements come from reports regulatory sent to the CNBV and the Banco de Mexico, for the characteristics of the portfolio of the institution (credit by credit

information). The CNBV, through its website, has recognized the high quality of the information sent by the institution, and recommends its use without restriction.

2.3 Risk Policy Framework in Banco Santander (Mexico)

The internal manuals for Risk Management are technical documents that contain policies, procedures, data

flow diagrams, models and methodologies necessary for the management and analysis of the different types

of risk and requirements processing systems of information.

The risk internal regulation of Banco Santander (Mexico) develops in the following types of documents:

1. Corporate Frameworks: reflected the general principles and define the framework for action to be

adjusted to other more concrete documents.

2. Models: develop frameworks or particular aspects thereof; specify the principles, processes and

responsibilities, governance and instruments of regulated activity.

3. Risk policies: set quantitative limits and qualitative criteria to be observed in the processes of risk

decision.

4. Regulations: meets the inner workings of the committees and other joint decision or deliberation

forums.

5. Procedures: detail the embodiment of a process or set of processes.

6. Guidelines: collect additional elements to the internal rules, necessary for a complete replication of

the process or for a better understanding of them.

The internal regulation of risk within Banco Santander (Mexico) provides documentation that Risk

Management be developed in compliance with the principles described in Table 1A.

2017 | RISK MANAGEMENT ANNUAL REPORT | 13

Table 1A Principles that complies the documentation of Banco Santander (Mexico)

Reflection of risk management All relevant activities of the risk function should be duly regulated. Internal risk regulations should reflect the way in

which risk is managed in the entity, but should also be used to encourage the evolution of activities towards best practices.

Responsibility of the regulations

Those responsible for the risk activities have to ensure that

their activity is regulated in accordance with the risk policy

model and in line with external regulations or standards.

Governance of the regulations Control (validation) and governance procedures have to be established to enable authorities to be assigned to approve each

document type at the pertinent level, including the due weighing up of opinions and consultation of all those involved.

Coordination of the regulations Producing consistent regulations, disseminating best practices,

transferring knowledge and ensuring efficiency in the development of internal regulations requires extensive

coordination in their development process, between both the

Group's different units and the affected functions.

Accessibility and knowledge of

the internal regulations

The internal risk regulations will be accessible to all affected staff

members, and the training activities necessary for awareness of

these should be promoted. Use of reference documents The regulatory development of those aspects for which there are

reference documents has to be based, insofar as possible, on these, in order to add consistency to the Group's regulations and

promote the use of best practices.

The governance of the internal regulations of risks is carried out through the support of several committees:

Board of Directors: responsible for approving and modifying the general risk policy.

Comprehensive Risk Management Committee (CRMC): responsible for validating and ratifying

frameworks, models and policies for comprehensive risk management, based on the objectives,

guidelines and policies established by the Board of Directors.

Risk Policy Committee: approver of the risk policy documents and its prior validation regarding

risks or others that may have implications for the risk area.

3. Integral Risk Management

3.1 Basic Principles of the Integral Risk Management

Risk management is considered by Banco Santander (Mexico) as a competitive element of strategic nature

with the purpose of maximizing the value for the stockholder. This management is defined, from a conceptual and organizational sense, as a comprehensive management of the different risks assumed by

2017 | RISK MANAGEMENT ANNUAL REPORT | 14

Banco Santander (Mexico) for the development of its activities. Managing the risk inherent in the operations of the Bank is essential to understand and determine the behavior of its financial situation and to create

long-term value; entirely, it is attached to the regulatory requirements established by the CNBV and Banco de Mexico.

The Integral Risk Management is defined as the set of actions required for identification, decision,

measurement, evaluation, monitoring and control of all risks.

On a fist level, the Risk Map that the institution has defined includes the following types of risk:

Credit Risk: this risk is caused by the possibility of losses arising from the total or partial

failure of the institution financial obligations by its customers or counterparts.

Counterparty Risk: is the risk that the counterparty to a financial contract will default prior

to the expiration of the contract and will not make all the payments required by the contract.

Counterparty risk applies to the following financial instruments: derivatives, repurchase

transactions, and securities lending.

Market Risk: risk incurred as a result of the possibility of changes in the market that affect

the value of the positions in trading portfolios.

Structural Risk: menace caused by the management of the different items of the balance

sheet, including those relating to the sufficiency of own resources and those arising from the

activities of insurance and pensions.

Liquidity Risk: crisis of failing to meet payment obligations on time or doing so with an

overcost.

Operational Risk: risk of losses by deficiencies in internal controls, errors in processing and

storage operations or transmission of information, as well as adverse administrative and legal Resolutions, fraud or theft; includes, among others, the technological and legal risks:

Legal Risk: potential loss by failure to comply with the applicable legal and

administrative provisions, the issuance of unfavorable administrative and judicial

resolutions, and the application of sanctions, in connection with the transactions which the institution carries out.

Technological Risk: potential losses from damage, interruption, alteration or failures

derived from the use of hardware, software, systems, applications, networks and any other means of transmission in the provision of banking services to customers of the

institution.

Conduct Risk: risk occasioned by inadequate work placements and the relationship between

the bank and his clients, as well as the treatment of products offered to their clients, also the

customization of their products to their clients.

Model Risk: acknowledge of losses originated by decisions made mainly by the outcome of

the models, this comes because mistakes made in the inception, application and use of this

models.

Reputational Risk: damage made by the perception of the bank form the public opinion,

clients, investors, or any other stakeholder.

Risk Management at Banco Santander (Mexico) is governed by different principles, which are aligned with

the strategy and business model of the institution:

a) Incorporation of a Risk Culture.

2017 | RISK MANAGEMENT ANNUAL REPORT | 15

A strong risk culture, extending to all areas and employees and covers all types of risks is promoted. This culture includes a set of attitudes, values, skills and guidelines from the

dangers integrated into all processes, including decision making change management and strategic planning and business.

b) Involvement of senior management.

There is a direct participation of the governing bodies and senior management in the

development and implementation of risk culture, as well as in the management and control

thereof.

c) Independence of the risk function.

The risk function operates independently to other competitions, covering all risks and providing adequate separation between the generating areas of risk and those responsible

for its control and supervision. It has sufficient authority and direct access to the bodies responsible for setting and monitoring of the strategy and policies of management and

Government risks.

d) Definition of Risk Appetite.

A key aspect of risk management is the definition of the risk appetite that determines the

amount and type of risks considered reasonable to assume in the execution of its business strategy. The risk function boosts its definition, as well as its continuous control.

e) Comprehensive Consideration of Risks.

The identification and assessment of all risks that might impact on the income statement or

capital position are basic premises to enable its management and control. The management and risk processes cover all activities and businesses. Risk management considers both the

risks generated directly as those originating from outside the institution, but which may still

affect it.

f) Organizational Model and Governance.

A model assigned to all risks, responsible for management and control while preserving the principle of independence and with clear and consistent reporting mechanisms.

g) Decision in Collegiate Bodies.

Decision-making through collegiate bodies is an effective tool to facilitate a proper analysis

and different perspectives to be considered in risk management. The decision-making

process includes a neat contrast of opinions provided to the potential decision impact and

the complexity of the factors that may determine it. The risk governance model not only

identifies the different bodies that compose it, but also defines the granting of faculties and

powers of each of them.

h) Anticipation and Predictability.

Risk assessment is an eminently proactive vocation, in order to estimate the evolution of

risks in different scenarios and time horizons. Therefore, it focuses on the future projection of all those variables that determine the results. Whenever possible, the intention is that the

risk assessment should include its quantification or measurement. The quantification of the

risk is based on widespread use of models. In cases where this is not feasible, risk assessment aims to identify the elements of greater incidence on the probability of occurrence of a loss

event and its impact, in order to facilitate the implementation of mitigation measures and controls.

i) Risk Limitation.

All financial risks incurred are subject to objective, verifiable and consistent limits with risk

appetite, both in regard to the types of acceptable risk and its quantitative level. The limits

2017 | RISK MANAGEMENT ANNUAL REPORT | 16

are allocated to the various types of risk, as well as the different activities and businesses. For non-financial and cross-cutting risks consistent tolerance level is set with its nature.

3.2 Adequate tools for Risk Management

All risks in its various manifestations should have a responsible for control and management. Also, the

structure of the risk function is proportional to the nature, scale and complexity of its activities.

The institution has the following essential tools for a proper performance of Risk Management:

Table 3A Tools for Risk Management

A regular process for identifying

and assessing all risks

A periodic process simulation of the evolution of relevant risk factors and their impact on the capital

and results

A uniform risk reporting framework with common

standards and metrics

Periodic planning processes of capital

and liquidity

Periodic (technological and operational) contingency and

business continuity plans

Periodic plans of feasibility and,

where appropriate, of

resolution.

2017 | RISK MANAGEMENT ANNUAL REPORT | 17

3.3 Management and Control of Risks

The management and control of risks is structured in three lines of defense that developed three different functions:

a) First Line of Defense: Risk Management from its generation.

The first line of defense consists of lines of business or activities that originate the exposure

to risk in the institution as part of its activity. The generation of risk in the first line of defense is set to appetite and defined limits. To serve its function, they have the means to identify,

measure, manage and report the risks assumed. b) Second Line of Defense: Control and Consolidation of Risks, Monitoring its Management.

The second line of defense is made up of teams specialized in risk control and supervision of the management of them. This line is responsible for the effective control of risks and ensures

that they are managed according to the level of risk appetite defined by senior management;

is responsible for the identification, measurement, management and reporting of the risks involved, without prejudice the needs of the first line for a proper management. Promotes

the development of a common culture of risk, and provides guidance, advice and expert judgment in all matters related to risks, constituting the point of reference for the entity to

these themes, as well as to propose methodologies of measurement and analysis.

c) Third Line of Defense: Independent Review of Risk Activity.

As a third line of Defense, are Internal Audit processes. Periodically evaluates that the policies, methods and procedures are appropriate and checks that they are effectively

implemented in the operational management of the institution.

The management and control of risks includes processes of different natures which, according to their scope

and complexity, may differ in: (i) strategic management processes, which are those that form part of the

definition, implementation and monitoring of the risk strategy; (ii) the decision processes are taking place

to adopt and adequately implement concrete decisions that require management and risk control and (iii)

instrumental processes are necessary to make possible the above. An overview of these processes is

included in Table 3B.

2017 | RISK MANAGEMENT ANNUAL REPORT | 18

Table 3B: Risk Management Processes

Strategic Management Processes

Formulation and monitoring the Bank's risk appetite.

Defining the types and levels of risk consistent with the objectives.

Identification and implementation of strategies and activities to achieve and maintain

the desired risk profile.

Evaluation of the effectiveness of these deviations and the objectives pursued.

Setting targets and metrics to control it and follow it.

Decision Processes

Origination: They occur before effectively take the risk. These processes determine

whether to assume new risks.

Anticipation: they are intended to prevent situations of increased level of risk and

facilitate the adoption of corrective measures.

Mitigation: They cover the decisions to reduce the consequences of the events of loss,

both before and since such events occur. The key elements of mitigation processes

are anticipation and early identification of loss events; the development of specific

mechanisms for the management of these events and the agility in implementing these

mechanisms.

Instrumental Processes

Identification of the risks associated with operational activity or business.

Evaluation and measurement of risks, which aims to obtain an estimate of the

likelihood of different scenarios of loss as well as the potential impact of each.

Monitoring and control processes, ensures the continuous availability of updated

information on the levels of risk assumed in the development of a business. Also cover

policies and procedures compliance.

The information, which includes the generation, dissemination and provision of

relevant people the necessary information to know and assess the situation of the risks

and be able to take decisions and actions needed.

Governance Structure for Risk Management

Banco Santander (Mexico) has a structure of agile and efficient government that, among other things,

ensures: (i) participation in risk decisions and in monitoring and control of the governing bodies and senior management; (ii) coordination between the different lines of defense which set the functions of

management and risk control; (iii) alignment of objectives, monitoring compliance and implementation of corrective actions and (iv) existence of an adequate environment management and risk control.

To achieve these objectives, the scheme of the Committees Governance Model within the Bank is designed

to ensure adequate:

a) Structure: It implies, at least, the stratification according to the levels of relevance, balanced

capacity of delegation and the elevation of incidents protocols.

b) Composition: With members of sufficient level of dialogue and appropriate representation of

the business and support areas.

c) Operability, the frequency, level of minimum assistance and timely procedures.

2017 | RISK MANAGEMENT ANNUAL REPORT | 19

In Banco Santander (Mexico), risk decision-making bodies start from the Board of Directors towards the administrative units responsible for the management and control of each one of them.

Board of Directors

In terms of risks, among other things, the Board of Director is responsible for establishing the model

of management and control of risks and to formulate the appetite for risk of the entity and to conduct

a regular monitoring of the adequacy of the risk profile of the institution to the defined risk appetite.

It establishes the minimum requirements of balance between profitability and risk of business or

activities and makes decisions on operations or specific limits.

Comprehensive Risk Management Committee (CRMC)

The CRMC aims to manage the risks to which the institution is exposed, as well as monitor that the

operations, complies with the objectives, policies and procedures for the Integral Risk Management

(IRM) and the global limits of exposure to risk, that they have been previously approved by the Board

of Directors.

The functions of the Committee are:

Propose to the Board of Directors for approval: Objectives, guidelines and policies for IRM, as well as any modifications made to them.

Global limits of exposure to risk and specific risk exposure limits, considering:

− The Consolidated Risks, broken down by business unit or risk factor, cause or origin, as set out in Articles 79-85 of the CUB and, where appropriate, risk

tolerance levels. − The mechanisms for the implementation of correctives actions.

− The cases or special circumstances that may exceed both the global limits of exposure to risk as a specific risk exposure limits.

Approve:

An exceptional specific limits adjustment and secondary of the risk appetite was made, when the Board had the faculties and approval com the Executive risk Committee, the

risk levels tolerance (once a year), as well as the liquidity risk (article VIII).

Specific risk exposure limits, when the Board has delegated authority to do so, the levels of risk tolerance and liquidity risk indicators (Article 81 fraction VIII of the CUB).

Methods and procedures to identify, measure, monitor, limit, control, report and disclose the different types of risk to which the institution is exposed.

Models, parameters, scenarios, assumptions, including those relating to stress testing

established for liquidity risk (Annex 12-B CUB), to be used to carry out the assessment, measurement and control of risks to propose IRM.

Methodologies for the identification, evaluation, measurement and control of the risks of new operations, products and services that are intended to offer the market.

Corrective actions proposed by IRM as provided in section 69 of the CUB. Manuals for the CUB, according to the objectives, guidelines and policies established

by the Board. These must be technical documents containing, among others, policies,

procedures, data flow diagrams, models and methodologies necessary for the management of the various types of risk (Article 78 of the CUB).

Technical Evaluation of the AIR (Article 77 of the CUB) for presentation to the Board and Committee.

Report of Technical Evaluation (Article 77).

2017 | RISK MANAGEMENT ANNUAL REPORT | 20

Assign (remove), notifying the Board of Directors, the responsible for Comprehensive Risk Management Unit.

Report to the Board at least quarterly:

Risk profile of the institution. Exposure to risk assumed by the Institution.

The adverse effects which could occur in the operation thereof.

The non-compliance of the desired risk profile, limits of exposure to risk and levels of risk tolerance established.

Corrective actions implemented (Article 69 of the CUB).

Ensuring awareness by all personnel involved in taking risks:

Desired risk profile.

Limits of exposure to risk.

Levels of risk tolerance.

Report to the Board at least once a year:

Business Continuity Plan. Effectiveness test of the Business Continuity Plan.

Approve methodologies for estimating quantitative and qualitative impacts of operational contingency referred to in Article 74 fraction XI of the CUB.

Adjust or authorize the excess on specific risk exposure limits:

Exceptionally. Approval of the Board.

According to the objectives, guidelines and policies for Integral Risk Management When the conditions and environment of the institution so require.

Request to the board, the adjustment or the authorization to exceed, by way of

exception, the global risk exposure limits.

Executive Committee of Risks

The Executive Committee of Risks is intended for all the Bank's risks, ensuring the proper identification,

measurement, monitoring, control, reporting and risk mitigation, and the availability of means for adequate

risk management.

The Committee's functions are as follows:

Propose to the relevant committees of Bank risk appetite.

Approve the specific risks levels or secondary risk appetite when the conditions in the institution

environment requires, this will be informed to the board of directors

Propose the methodology of Risk Identification and Assessment (RIA) of the Bank.

Suggest risk management models.

Evaluate the procedures in risk according to the normative corporate models.

Approve the creation and modification of Risk Committees according to the corporate

governance

Follow the Bank Risk in all areas.

- Credit Risk: (i) Propose additional credit provisions required, (ii) approve credit operations

as deemed appropriate and (iii) follow operations/customers whose size could have a significant impact on the Bank's results.

- Market Risk: (i) Operational know as they consider appropriate, (ii) follow-up of limits whose size can have a relevant impact on the Bank's results.

2017 | RISK MANAGEMENT ANNUAL REPORT | 21

- Operational Risk: (i) Monitor the budget/size limits that may have a significant impact on

the Bank's results.

Take the necessary measures to comply with the recommendations of the regulator and the

auditors.

Approve the corresponding provisions models and monitor their proper implementation.

Supervise and approve the monthly calculation of provisions, ensuring the sufficiency of

provisions in accordance with the regulations, as well as follow up on the agreements or application plans that are defined in this regard, including those that refer to modify the final

amount in cases that he considers it convenient.

Committee of Risks Control

The Committee of Control Risks has the power to monitor and control the risks of the Bank, giving a comprehensive, regular and adequate monitoring of all risks identified in the risk map of the general

framework of risk, reporting and, if necessary, appropriate scaling the alerts to higher organisms.

The Committee's functions are as follows:

Review the determination of risk appetite and the defined strategy for its management.

Monitoring methodology Risk Identification and Assessment and monitoring the resulting

assessment.

Ensure the implementation of Organizational Model Lines of Defense, at three levels: Risk Managers, Risk Drivers and Audit, clearly defining roles and responsibilities.

Supervise the fulfillment of the normative model of risks and their specific principles, in

particular to define, evaluate and follow up the policies of risk deemed appropriate.

Validate the existence, updating and dissemination of Governance Risk Model, which defines

the risk decision-making bodies, their powers, members and delegated powers.

Assess scenarios and assumptions to be used in conducting stress tests.

Follow up on recommendations from the audits of regulators and auditors.

Inform to the Executive Committee of Risks about important deviations, identifying sources of

concern.

Committee of Information Management and Data Quality

The Committee of Information Management and Data Quality is the body responsible for ensuring compliance and periodic review of Risk Information Framework and the implementation of the actions

necessary to improve them, taking care to ensure the correct treatment of the information for the proper management and risk control of the unit, ensuring proper quality of data and processes necessary to their

availability, extraction, aggregation and analysis.

The Committee's functions are as follows:

Promote the preparation of documentation that supports the government of the data and its elevation to the corresponding statutory governing bodies for approval and ensure compliance.

Review and approve the relevant modifications in the data governance process.

Approve data quality objectives and follow-up reporting on compliance to government bodies

Approve certification reports, establish mitigation plans and send to the corporate counterpart

committee for ratification.

Propose, approve and supervise all activities related to the identification, evaluation and management of the quality of risk data and with the information and aggregation of risk data.

2017 | RISK MANAGEMENT ANNUAL REPORT | 22

Validate and communicate any limitation that prevents a complete aggregation of risk data in the reports.

Follow the status and quality indicators of the risk data and other properties thereof.

Assess the status of the risk information processes, reporting relevant incidents to the Risk

Executive Committee and executing the necessary measures to ensure that the required standards are maintained.

Ensure the execution of the measures determined by the highest administrative body in relation to the data aggregation processes and the presentation of risk reports, coordinating the

necessary functions and proposing other actions that may be necessary.

Propose and approve improvements and modifications applicable to the risk information model, governance of information and data and validate its application status and compliance with

regulatory principles and requirements, in accordance with the regulatory risk model.

Receive, prioritize and coordinate all requirements related to risk reports.

Approve local taxonomies of risk and data reports and their modifications; as well as adhering

to corporate taxonomies.

Approve the certification procedure and the risk information model, governance of information and data according to the regulatory risk model.

Review projects related to the aggregation processes and the generation of risk reports.

Committee of Operational Risk

The Committee of Operational Risk observe the identification, mitigation, monitoring and reporting of

operational risk, survey the compliance with the Framework of operational risk limits and risk tolerance policies and procedures in this subject. Oversees the identification and control of current, emerging and

operational risks, their impact on the risk profile and the integration of identification and management of operational risk in their decision-making processes.

The Committee's functions are as follows:

Promote and review the availability of the Framework and Model Operational Risk Management,

policies that develop and follow its implementation and development in the Institution.

Monitor the evolution of the operational risk profile through information provided by the

established tools (loss database, self-assessment questionnaires, risk indicators, business

environment, scenarios and metrics defined) as well as through other sources (customer claims, technological incidents, audit reports and supervisors, etc.) and check the evolution of the

established metrics, raising, where necessary, appropriate alarms.

Perform the monitoring of operational risk losses annual budgets.

Review the main events of each period, determining if they fit into the categories of operational

risk. In which case, analyze the causes and identify the controls set.

Advise on issues appetite and tolerance for operational risk.

Propose, approve or validate, as a result of the powers assigned, action plans, mitigation

measures and monitoring plans and identified current controls.

Recommend the beginning of thematic reviews on specific processes or sources of risk.

Understand, assess and monitor the observations and recommendations made by supervisory

authorities and by Internal Audit in relation to operational risk.

2017 | RISK MANAGEMENT ANNUAL REPORT | 23

Track changes and developments of the regulations related to operational risk, assess the

issuance of comments by the Bank in this regard and further plans of action for its

implementation.

Contribute to the development and implementation of the culture of operational risk

management in the organization, through training programs, meetings and other outreach

initiatives.

Monitor the implementation of programs and initiatives of a corporate nature and/or regulatory.

Participate in the revision and issue the opinion of different versions of the plans, like the

previous process to the presentation others committees if is the case, and the formal approval

of the government.

Assist the consultative committee regarding technical questions about the content plans

Define steps to be taken along with a responsible in order to reduce the operational risk

exposure for action drivers and issues identified by Operational Risk environment.

Guarantee that the business continuity plans and procedures are developed and updated for

Grupo Financiero Santander Mexico, as well as to ensure that the trials and drills as will be

effective according to the corporate policy and local regulation, ensuring an effective response

and continuity of the business in case any contingency will be presented.

Committee of Capital

The Capital Committee is responsible for the supervision, authorization and valuation of all aspects related

to the capital and the solvency of the Institution.

The functions of the Committee are the following:

a) Supervise:

The analysis of solvency and capital adequacy.

Compliance with budgets, capital planning and stress test analysis.

Monitoring of capital consumption, RORAC and EVA, of the institution and by businesses.

Monitoring of all aspects related to the implementation of advanced models.

Regarding capital management, the eventual decision to activate the Feasibility Plan in

terms of solvency, as this is established corporately, as it will be responsible for submitting

it to the CAIR.

b) Authorize:

Review and validation of capital planning and stress test exercises prior to their internal

and corporate approval or presentation to the corresponding supervisory authority.

Changes in capital models and methodologies, considered relevant for internal purposes,

accompanied by the report of the independent validation area, previously presented in the

Local and Corporate Models Committee for risks under the perimeter of competence of the

General Risk Department.

For the purposes of this framework, relevant changes are considered, those whose impact

exceeds a threshold of 1% of the Group's capital consumption. Annually, all the changes

made to capital models and methodology will be raised for consideration by CAIR.

Identification of proposals.

Capital objectives for the planning horizon contemplated in the Capital Self-Assessment

Report.

2017 | RISK MANAGEMENT ANNUAL REPORT | 24

Optimization of capital consumption.

Improvement of solvency ratios.

Improvement of capital models and the integration of these in management.

In terms of capital, this Committee coordinates the relationships with the supervisors and the flow

of information (Capital, RORAC and EVA) to the market.

3.4 Management of Risk Information

Risk management and control require high availability of hard data, ability to group and analyze these data as well as solid reporting procedures. The management of risk information in Banco Santander (Mexico) is

governed by the following principles:

a) Responsibility: The Board of Directors is ultimately responsible for ensuring the implementation

of the framework for managing Risk Information.

b) Technological Architecture: It has a technological architecture for each type of risk that ensures

that risk information and baseline data provide answers to the general requirements established

for the Institution and reporting risks.

c) Reconciliation of risk data: The risk information is reconciled with the accounting data to ensure

the accuracy of it, and, where appropriate, with other relevant sources that may exist.

d) Data Availability: data are available ensuring an appropriate level of detail for certain users

identified at all times through appropriate access credentials. The relevant users regarding risks

have full access to risk data to ensure that they can be added, validate and reconcile properly

with risk reports.

e) Completeness and Exhaustiveness: Reports of risk management and aggregation criteria cover

all material risks consistent with the risk map.

f) Indicators of Data Quality: They are defined quality indicators covering aspects such as accuracy,

integrity, completeness, tolerance and availability in both normal and stress situations.

g) Data Quality Controls: There are controls over processes in order to ensure data quality at all

levels.

h) Promptness: The reports should be available in the manner and time established, taking into

account the nature and volatility of the risk involved and the relevance of the report.

i) Flexibility and adaptability: The risk management reports are prepared according to the needs

of the organs and the key areas involved in risk management and monitoring.

j) Forward-looking Approach and availability of documentation: The risk reports contain, where

relevant, the likely path in the Bank's capital situation and risk profile thereof, and provide

information on estimates and forecasts in different scenarios, analyzing and identifying stress

levels and trends of emerging risks.

k) Data analysis and Expert judgement: The reports are both descriptive and prescriptive and

provide quantitative and qualitative data, including explanations, recommendations and

conclusions.

l) The above principles are developed through the implementation of various key processes in the

Information of Risk Management:

− Data availability: The aim is to have a common infrastructure, accurate and reconciled on

different variables to respond to multiple requests for information necessary. To do this,

the information requirements are set; selected data needed to satisfy these requirements

are identified; data source systems are extracted; the source data is transformed into the

required data and data stored in repositories available for the exploitation and use thereof.

2017 | RISK MANAGEMENT ANNUAL REPORT | 25

− Aggregation of Data: The aggregation process is driven by a particular data structure based

on different criteria and rules that allow a precise and homogeneous grouping of data in

order to generate different views of information, responding to needs analysis different

users.

− Analysis and use of information: The data and risk information are available for use in a

homogeneous, flexible and with sufficient granularity environment, also are easily

understandable and accessible in a timely manner for use, analysis and distribution. The

information is available for use in both the reporting and other requirements for the

management processes and risk control.

- Reporting and distribution to third parties: The process of reporting and distribution

guarantees it is available to all relevant parties. That provision, its form and frequency

depends on the relevance and materiality of informed risk and should be done on time and

according to established schedules.

The Committee of Information Management and Data Quality ensure adequate quality of the data and the processes needed for its availability, extraction, aggregation and analysis, and its main functions are:

a. Promote the development of the documentation supporting the government data.

b. Review and approve any significant changes in the process of government data.

c. Approve the data quality objectives (criticality, indicators, tolerances, quality plans).

d. Propose, approve and monitor all activities related to the identification, assessment and

management of data quality and risk information and risk data aggregation.

3.5 Risk Appetite

Risk appetite is the maximum level and type of risk the organization is willing to take, within its risk capacity

to achieve its strategic objectives and the development of its business plan.

The risk capacity is the maximum level and nature of risks that the company can assume without

compromising its viability, determined by the level of sufficient resources (capital, liquidity, asset and liability management systems and capabilities) to develop the activity the entity to the demands of

regulators, governments, shareholders, investors, customers, employees, suppliers and social community.

The Risk Appetite Framework (RAF) is the set of instruments that articulate the risk appetite of the institution. The risk appetite is expressed, in general, aggregate and by type of risk, in Risk Appetite

Statement (RAS). The RAS sets, using quantitative metrics and qualitative indicators, the criteria to be submitted to the Bank's risk exposure in both current conditions and under different future stressed

scenarios.

The criteria set by the RAS are taken into account and respected throughout the developing taken of the

other elements that constitute the RAF, which are developed to the level of detail necessary, policies, limits

and other criteria applicable in different lines of business and types of risk. The risk limits are all the

quantitative and qualitative limitations that distribute and move the restrictions set in the RAS to the different

business lines, specific categories of risk or any other relevant level of disaggregation.

The risk appetite considered desirable risk profile of both the present,medium and long term. When

analyzing the possible evolution of the risk profile, both considered the most likely circumstances as other

unfavorable situations (stress scenarios). It incorporates quantitative metrics and qualitative indicators

2017 | RISK MANAGEMENT ANNUAL REPORT | 26

relating to key performance indicators, which are aggregated, understood by the entire organization and

clearly reflect the reasons for taking or not taking risks in decision-making processes.

Risk appetite is integrated into the management through a dual approach bottom-up and top-down:

Top-Down Vision: The Board of Directors leads the fixing of risk appetite, ensuring its

disintegration and translation of specific limits that are set at portfolio level, business unit or

line.

Bottom-Up Vision: the risk profile that contrasted with risk appetite is determined by the

aggregation of measurements made at the portfolio level, unit or business line. The risk

appetite of the entity arising from the consideration of the business objectives and their

interaction with the potential risks to take and existing capabilities.

The maximum management body, The Board of Directors, is responsible for determining and approving

risk appetite; It promotes its articulation in the form of policies and limits to ensure its implementation, communication and monitoring. The Board of Directors and the Risk Management Authority, it is up to

formulate the risk appetite of the entity, identifying its development elements and assign responsibilities for it, and perform periodic monitoring of the adequacy of the risk profile of the entity risk appetite defined.

The Executive Risk Committee is responsible for ensuring the consistency of the actions of the Bank's risk

appetite determined by the Board of Directors, and approves actions on the level of risk in light of the analysis and monitoring of risk appetite.

2017 | RISK MANAGEMENT ANNUAL REPORT | 27

4. Credit Risk Management

4.1 Overview

The credit risk arises from the possibility of losses derived from the total or partial failure to meet financial obligations to the institution by its clients or counterparties. The credit risk is caused by the possible failure

to pay by the accredited both in lending operations that have involved a payment and those that do not

involve any but whose performance is guaranteed by the Bank.

Segmentation from the point of view of credit risk management is based on the distinction between three

types of customers:

Individuals segment includes all natural person except for those with business people.

Includes holdings of residential mortgage, credit card and non-revolving consumer portfolio.

SME’S, Companies and Institutions including legal entities and individuals with business

activity. In addition to public sector entities and private sector entities nonprofit.

Global Corporate Banking (GCB) is composed of corporate, financial and sovereign

institutions, which make up a closed list reviewed annually. This list is determined by a

thorough analysis of the company.

The governance of the Credit Risk Management is a committee structure that are responsible, among other

things, the following functions:

The decisions on ratings, operations and risk limits, within the powers that have been granted

by the bodies envisaged in the general framework of risk and credit risk and its monitoring.

Validation and supervision of policies of credit portfolios.

Validation and monitoring of annual plans portfolios.

Monitoring the performance of exposures.

These committees, in appropriate cases, will have representatives of the business functions and may

delegate the functions they consider relevant in other organs, with the relevant regulations of these

committees to establish the process of granting powers and duties of each of them, including qualitative

and quantitative limits that define its scope and decision.

The credit risk is undoubtedly the most important risk in banking

Possible Causes: Insolvency of accredited.

Related-party transactions. Excessive concentration. Inadequate guarantees.

Other causes.

Table 4A Causes of Credit Risk

2017 | RISK MANAGEMENT ANNUAL REPORT | 28

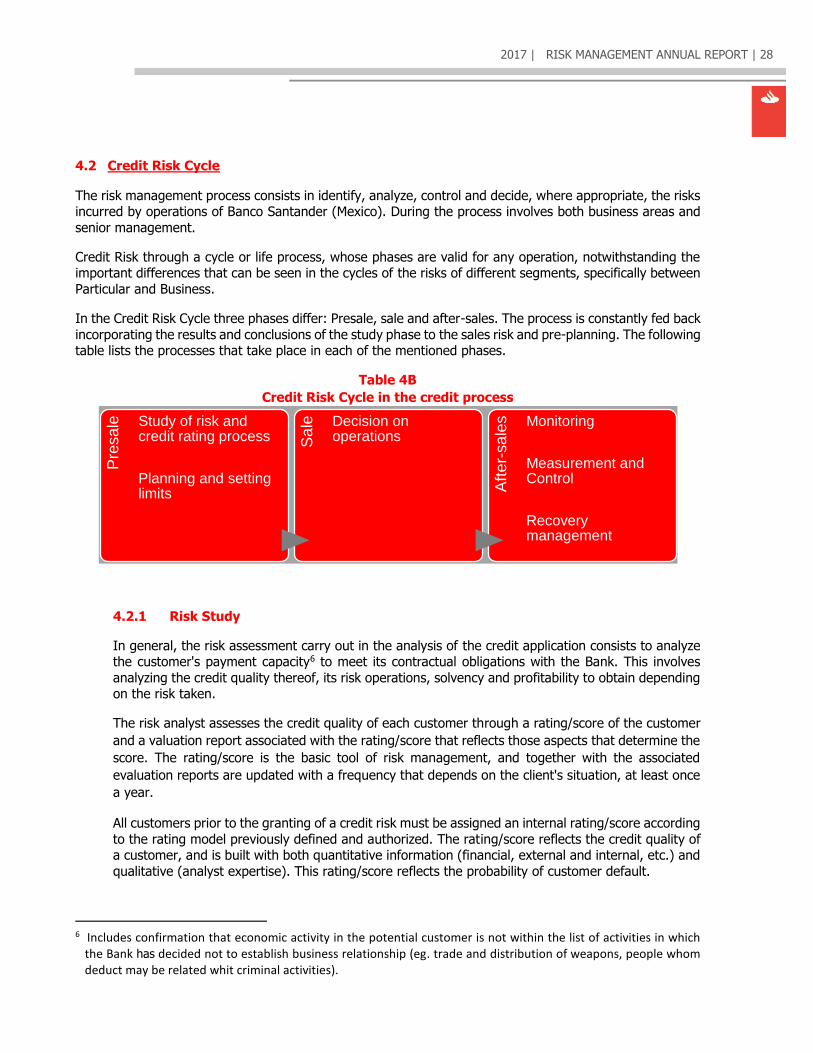

4.2 Credit Risk Cycle

The risk management process consists in identify, analyze, control and decide, where appropriate, the risks incurred by operations of Banco Santander (Mexico). During the process involves both business areas and

senior management.

Credit Risk through a cycle or life process, whose phases are valid for any operation, notwithstanding the important differences that can be seen in the cycles of the risks of different segments, specifically between

Particular and Business.

In the Credit Risk Cycle three phases differ: Presale, sale and after-sales. The process is constantly fed back

incorporating the results and conclusions of the study phase to the sales risk and pre-planning. The following table lists the processes that take place in each of the mentioned phases.

Table 4B

Credit Risk Cycle in the credit process

4.2.1 Risk Study

In general, the risk assessment carry out in the analysis of the credit application consists to analyze the customer's payment capacity6 to meet its contractual obligations with the Bank. This involves

analyzing the credit quality thereof, its risk operations, solvency and profitability to obtain depending on the risk taken.

The risk analyst assesses the credit quality of each customer through a rating/score of the customer

and a valuation report associated with the rating/score that reflects those aspects that determine the

score. The rating/score is the basic tool of risk management, and together with the associated

evaluation reports are updated with a frequency that depends on the client's situation, at least once

a year.

All customers prior to the granting of a credit risk must be assigned an internal rating/score according

to the rating model previously defined and authorized. The rating/score reflects the credit quality of a customer, and is built with both quantitative information (financial, external and internal, etc.) and

qualitative (analyst expertise). This rating/score reflects the probability of customer default.

6 Includes confirmation that economic activity in the potential customer is not within the list of activities in which

the Bank has decided not to establish business relationship (eg. trade and distribution of weapons, people whom deduct may be related whit criminal activities).

Pre

sa

le Study of risk and credit rating process

Planning and setting limits

Sa

le Decision on operations

Aft

er-

sa

les Monitoring

Measurement and Control

Recovery management

2017 | RISK MANAGEMENT ANNUAL REPORT | 29

To manage properly the credit risk must be reached a near vision to the client, both in quantitative

and qualitative aspects, in order to meet their needs and anticipate risks that might affect the good

end of the contracted operations. Customer allocation to a risk analyst has the primary goal that the

analysts have an intimate knowledge of him.

The ratings accorded to customers are regularly reviewed, at least once a year, incorporating new

financial information and experience in the development of the banking relationship. The frequency of review is increased in the case of clients who reach certain levels in the automatic warning systems

and in those classified as special monitoring. Similarly, the tools of rating are reviewed to be able to

adjust the accuracy of the rating given 7.

Against the use of ratings in the wholesale world and the rest of the companies and institutions, in

particular the individuals segment dominated the scoring techniques, which almost always,

automatically assigned a valuation of transactions that occur and have designed to identify the credit

quality of customers, in addition to estimating the probability of default. This process is aided by

origination tool for high-volume applications and seeks to discriminate in the best way possible to the

good from the bad payers.

4.2.2 Planning and setting limits

The commercial strategic planning is implemented through the Strategic Business Plan. This plan is

the union of the business plan with the credit policy and the means required for their achievement on which the business budget is based and must be approved prior to the budget. The three elements

are closely connected and feed each other:

Business plan: set goals in exercise and specific action plan to be implemented to achieve the budget.

Credit Policy: moved the risk appetite to each business line in the form of portfolio

policies, policies for the granting, management and credit recovery and decision rules.

Media Plan (infrastructure): lists the models, systems and resources required for the implementation of planned actions.

The commercial and strategic planning should include safeguard, first of all, the principles established

in the General Corporate Framework of Risks. It is also ruled by principles that are structured in the following categories:

a) Principles of integration and consistency with other management tools. b) Principles concerning the scope of planning.

c) Organizational and governance principles.

Within the annual planning, the levels of risk the bank assumes limited in an efficient and comprehensive and budgets of each of the Bank's business are set out in terms of objectives and

limits on portfolio level, within defined limits risk appetite and risk policies established, defining the

scope of the entity's risk management, and media (models, resources, processes and systems) needed for the annual achievement of these objectives are set.

7 Banco Santander (Mexico) has an internal area of Risk Methodology, responsible for the development, review and

calibration tools.

2017 | RISK MANAGEMENT ANNUAL REPORT | 30

The credit policies moved the risk appetite to each business line, setting the scope of the annual plan. The definition of the general, policies and portfolio approval policies, management and recovery

of credit policies are the responsibility of the risk function, and its approval competence of the governing bodies established for the purpose of risk.

The annual process of setting limits is a dynamic process that determines the willingness to take