T2S News - securities.bnpparibas.comsecurities.bnpparibas.com/.../report_t2s-news_2014-06-01.pdf ·...

12

T2S News Issue 06 – Summer 2014

Transcript of T2S News - securities.bnpparibas.comsecurities.bnpparibas.com/.../report_t2s-news_2014-06-01.pdf ·...

T2S NewsIssue 06 – Summer 2014

Editorial 03

Latest news from the ECB 04

Clients adaptations to T2S 06

A superior platform to support our 08whole T2S settlement business

Cash solutions in T2S 10

Contents

3

Welcome to the latest issue of our TARGET2-Securities newsletter!

With only 12 months to go until the first wave migration, T2S preparations are in full gear.

We kick off with an update on the European Central Bank programme plan with highlights of the most important initiatives and harmonisation projects (pages 4-5).

The focus is now on client preparations to manage the changes that T2S will bring. We provide you with some highlights from our webinar and materials you may have received or obtained on our website (pages 6-7).

In the second part of the newsletter we provide you with some insight on the road to T2S through the implementation of our global platform. This also includes some market specifics and how we adapted to ensure clients get the maximum benefit from any new development.

To conclude this issue, we address cash solutions which have become a key topic of discussion as clients define their final operating model.

We hope you will find this issue informative and useful.

BNP Paribas Securities Services

Editorial

4

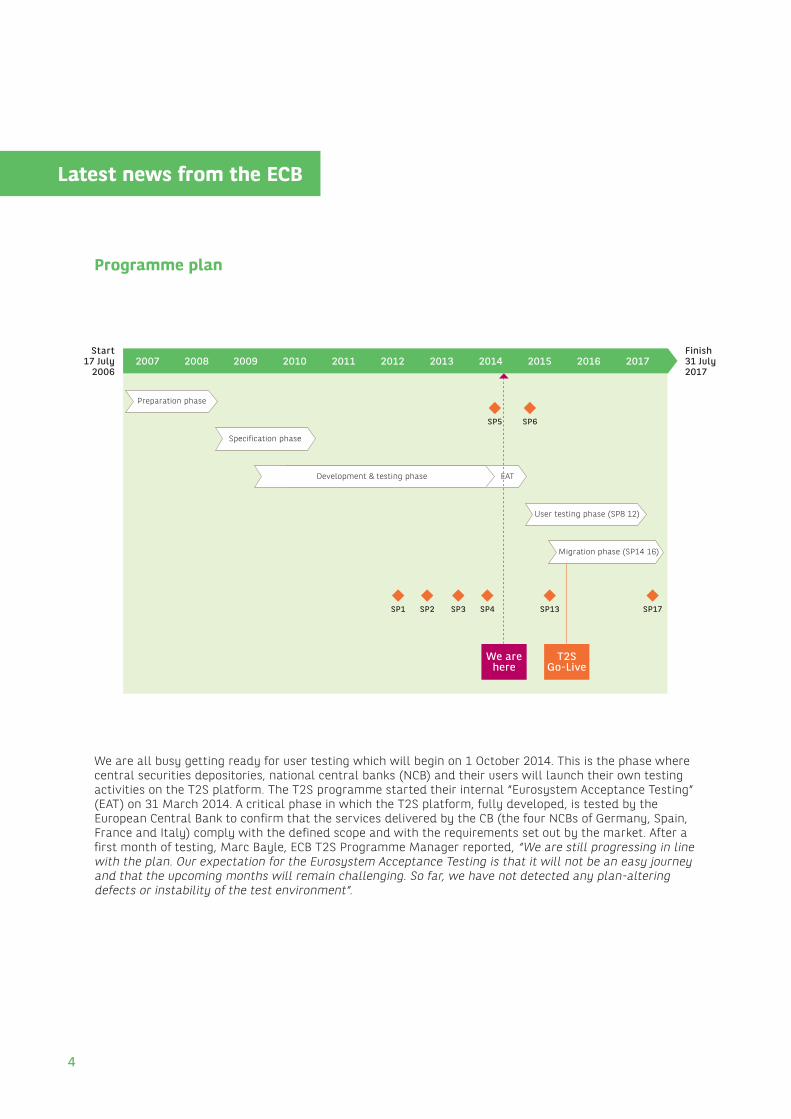

Latest news from the ECB

Programme plan

We are all busy getting ready for user testing which will begin on 1 October 2014. This is the phase where central securities depositories, national central banks (NCB) and their users will launch their own testing activities on the T2S platform. The T2S programme started their internal “Eurosystem Acceptance Testing” (EAT) on 31 March 2014. A critical phase in which the T2S platform, fully developed, is tested by the European Central Bank to confirm that the services delivered by the CB (the four NCBs of Germany, Spain, France and Italy) comply with the defined scope and with the requirements set out by the market. After a first month of testing, Marc Bayle, ECB T2S Programme Manager reported, “We are still progressing in line with the plan. Our expectation for the Eurosystem Acceptance Testing is that it will not be an easy journey and that the upcoming months will remain challenging. So far, we have not detected any plan-altering defects or instability of the test environment”.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Start

17 July 2006

Finish31 July 2017

Preparation phase

Specification phase

Development & testing phase EAT

User testing phase (SP8 12)

Migration phase (SP14 16)

SP1 SP2 SP3 SP4

SP5 SP6

SP13 SP17

We are here

T2SGo-Live

5

Directly Connected Participants (DCPs) in T2S

On 3 March 2014, we declared our intention to become DCP as of wave 1 for Monte Titoli and BOGS on the securities side and to the Banque de France on the cash side.

The DCP forum, initially created to share information and opinions about the requirements to be a DCP, will become an official T2S Group called the ‘DCP Group’. We are part of this group that will now be included within the T2S governance structure.

Autocollateralisation in T2S

The initial inability for the ECB to allow multi-market custodians the ability to use one single pool of collateral to cover settlement across all CSDs is being solved. The technical barrier initially imposed by T2S will be removed before the launch. The legal framework is still being discussed among NCBs with a strong recommendation for a maximum flexibility regarding the collateral.

T2S and harmonisation initiatives

The post trade harmonisation is still a main driver for T2S with many initiatives.

First and foremost, the fourth harmonisation progress report was published in March 2014 showing T2S market readiness to test and operate in line with the T2S harmonisation standards. It reveals that corporate actions remain the most difficult standard to implement.

The Cross-Border Market Practices Sub-group (XMAP) will deliver an interim report about the potential impacts of CSD restriction rules on the cross-border settlement efficiency by June 2014.

The CSD Regulation was adopted by the European Parliament on 15 April 2014. This regulation includes key elements for the T2S harmonisation agenda on securities settlement and central securities depositories. The ECB anticipated this adoption by creating task forces for two main topics of the CSD Regulation including the harmonisation of the settlement cycle to T+2 and the settlement discipline. We are active participants in both task forces.

The T+2 task force is in charge of the coordination among T2S markets to adopt T+2. The task force recently completed a paper “Best practices for T2S markets’ Migration to T+2” which was sent to ESMA (European Securities and Markets Authority) 1.

The settlement discipline task force will provide recommendations to ESMA for the definition of the technical standards on settlement discipline. Harmonisation for all the principles related to the settlement discipline and buy-ins is necessary to ensure a level playing field between CSDs.

1. http://www.ecb.europa.eu/paym/t2s/progress/pdf/taskforcet2/2014-05-02_HSG_proposals.pdf

Clients adaptations to T2S

T2S live date is approaching fast and interest is now focused on what has to be done to be ready for the first T2S migration on wave 1. We gathered the 10 most important themes of getting ready in our “T2S quick guide” sent to clients in January 2014. The guide’s aim was to help understand the implications and the necessary adaptations to be made ahead of T2S. Our ambition was to offer our clients an easy document to quickly assess what is going to change and how T2S is going to affect their business and their relationship with us. Shortly after our quick guide, we published a new Swift 15022 booklet dedicated to T2S incorporating the news emerging from T2S that will provide new opportunities for messaging.

The adaptation to T2S is undoubtedly the hot topic leading up to the one year mark before T2S. This is why we organised our first T2S web seminar titled “Getting ready for T2S” on 1 April 2014. We are now organising bilateral meetings with clients to enter into any additional aspect or concern that clients might have.

Our quick guide identified 10 main items to be considered and for each of them we have summarised the relevant implications, what is changing and how BNP Paribas Securities Services is going to shield clients as much as possible from the changes.

The 10 items considered are

1. New day schedule

2. Account set-up

3. Impact on standing settlement instructions (SSI)

4. Connectivity with us

5. Matching in T2S and the new information required

6. Enhanced T2S functionalities

7. Management of corporate actions

8. Testing

9. Cash and liquidity management

10. Impact to contractual documentation

For most of the items covered there will be limited or no impact as our priority has been to shield clients against any adaptation cost. We will offer service continuity and the possibility to exploit the advantages coming from T2S. Some adaptations will still be required to match the needs of the new platform.

What we suggest to clients is to focus on the new matching fields: mandatory, optional and additional matching fields, and also on the new enhanced T2S functionalities.

The adaptation to T2S is undoubtedly the hot topic leading up to the one year mark before T2S

Our priority has been to shield clients against any adaptation cost

Dario Locatelli, head of product management for local settlement and custody services

6

We will offer the possibility to exploit them in a more sophisticated way than T2S offers

With regards to mandatory matching fields, the “new” information to be managed in the static data, SSI, and to be reported in the instruction is the CSD of the settlement counterpart that becomes a key element for T2S to unambiguously identify the relevant accounts. It will have to be provided as a BIC11 code.

As far as the other mandatory matching fields are concerned it is important to remember that the trade date becomes mandatory for all transactions types, and above all, that it will be used in the calculation of the eligibility of the transactions to corporate actions.

Optional matching fields are important to prevent cross-matching but may also be a cause of unmatching as well, if exact information is not properly shared and a clear market practice has not been established. This type of matching field, and in particular the “second layer matching”, what is called party 2 in T2S, is already successfully used in a few markets, in Italy in particular. We will ensure that it is used in the other countries when we can reasonably believe that the market is ready to cope with it.

Additional matching fields (OPT OUT or CUM/EX) are a bit more dangerous as they do not match with blanks, this means that if quoted by one counterparty the other has to do the same otherwise it will be a cause of unmatching. In our role of custodian we cannot disregard or “hold” this information as this is a relevant feature of the transaction, if quoted in client instructions we are supposed to forward it in our T2S message. This is why we strongly recommend to clients that these fields are used in exceptional cases only, when required by the transaction type of course, and that they are agreed with the counterparty at trading time.

To conclude on matching criteria, they might imply some adaptations by clients as well as to ensure that counterparties agree on their usage and provide their custodian all the relevant information.

As far as the “enhanced” T2S functionalities are concerned the good news is that for some of them, in particular prioritisation and partialisation we will offer the possibility to exploit them in a more sophisticated way than T2S offers. We will avoid the need to provide specific information at instruction level by simply applying defaults at clients’ safekeeping account level.

Finally, for the more complex ones like “hold and release” or “linkage and pooling” more relevant adaptations are required. They can be considered as new options offered by T2S that clients can implement if and when they deem appropriate.

We hope you enjoyed this tour of what you will need to change and invite you to visit our dedicated T2S internet page (click here) 2 to get a copy of our settlement quick guide and the new swift booklet.

7

2. http://securities.bnpparibas.com/jahia/cms/T2S-1

A superior platform to support our whole T2S settlement business

Christian Houillon, T2S program manager

This quickly led to a conclusion: to fulfil all these objectives we needed to become a T2S directly connected participant (DCP) and setup a single settlement operating platform for the T2S area. From a technology perspective, that meant we would need a technical platform that could handle the T2S new connectivity, messages and processes while still managing remaining market specificities from CSD’s and CCP’s dedicated platforms and interfaces. It also meant that system performance was going to be a key element in order to cope with the settlement activity of our clients in a single processing cycle. The system would need to be extremely

flexible to implement new settlement services that would complement the T2S standard services and accompany our clients in the setup of new

scenarios. Most would probably imagine that meant starting from scratch with a new system! Fortunately, it was not the case…

Introducing AceTP, a proven platform In 2000, we moved forward with the plan aligned with our strategy to support our clients locally everywhere it mattered for them, worldwide. This gave birth to our Global Reengineering Programme which included the

creation of a single settlement platform that would both replace the existing array of local systems and could be quickly adapted for deployment in new markets. One of the most important elements to our plan was to maintain the benefits of a mutualised platform. The bar was set high, both in terms of technical and functional design, as it was to setup the most efficient project and maintenance process. After years of tremendous collective effort, our

teams launched the platform we call AceTP, now connected to more than 15 CSDs in Europe, Asia and Latin America. For all our T2S adaptations, we can therefore rely on an already well-proven platform and a solid foundation of project management expertise. Let’s look a bit closer at its core capabilities.

AceTP is a system developed by BNP Paribas technology teams using state-of-the-art design principles (object modelling) and technologies (JAVA/J2EE running on redundant Unix servers). Developing this complex piece of software was a choice we made to guarantee full control over the cost and long term strategy of the system. We wanted to be self sufficient in the planning of the system evolution with our own guarantees on the quality of services. A dedicated central IT team was set up alongside the business analyst team in charge of the global technical

When starting our T2S project back in January 2010, we already knew that adapting to T2S would be a huge effort. Not only was T2S introducing a new set of standards for settlement, it was also enabling new direct settlement and custody models and new services for our clients. Obviously, we wanted our clients to benefit directly from the harmonisation driven by T2S across continental Europe.

Extremely flexible to implement new settlement services that would complement the T2S standard services and accompany our clients in the setup of new scenarios

For all our T2S adaptations, we can therefore rely on an already well-proven platform and a solid foundation of project management expertise

8

maintenance and core functional evolutions of the platform. The team is supported by professionals in each of our branches with local market expertise to define the specific local requirements and test their implementation.

One of the key characteristics of AceTP is the ability to address multiple specific needs from a single software code delivered in the common live environment every quarter. An efficient software maintenance organisational process, the ability to easily grant access to new features for testing while not harming the day-to-day operations and highly automated non-regression testing tools have all been the recipe to allow a fast and secure development cycle. And this is a

cycle that we have tested several times through our progressive worldwide deployment.

As an answer to the original

requirement to onboard in one system the capabilities required to deal with many markets specificities, AceTP is designed to deal with the many proprietary message formats used by CSDs. One example is Poland that uses messaging that is quite close to T2S ISO 20022. Also as a consequence of the mutualisation strategy, the new services developed for a given market can be easily reused in another. Finally, our own internal operations benefit from its modern and very responsive user interface, allowing them for example to query the database according to dozens of criteria, model the screens according to their activity and the most frequent needs of clients as well as schedule and generate ad-hoc reports by themselves.

Our (busy) roadmap to T2SSo indeed AceTP was an obvious choice to support our T2S solutions, but it would not come without a major effort to begin by implementing the system in some of our key European markets: Euronext (Euroclear ESES, NBB-SSS, Interbolsa), Spanish (Iberclear) and Greece. Before adapting AceTP to T2S, migrating to AceTP was a mandatory first move to avoid a simultaneous migration to the system and to T2S.

We started with Euronext in 2010. This was the largest project and investment given the number of markets, specificities, clients, volumes and other systems that connect with the settlement platform. After almost three

years of hard work, all our clients have been successfully migrated to AceTP by the end of 2013, on time and on budget!

The migration of the Spanish local activity to AceTP will be performed in a different context. A major market reform is ongoing, paving the way to T2S by redefining the current registration process. The market will provide T2S-like services as well as introduce a new CCP and all these by the second quarter of 2015. AceTP is thus being adapted to replace the legacy platform, integrating the existing local specificities that will remain after the reform and the ones that will emerge.

Greece should be migrated to AceTP for 2015 as well. However the choice of Helex, the equities CSD, to stay out of T2S unlike BOGS, the govies CSD, creates a particular situation. We have decided to give the choice to stay on the current platform for both Helex and BOGS, or to benefit from our new T2S services and cash pooling in Paris by migrating to AceTP, but for BOGS only.

Finally, NBB-SSS, the National Bank of Belgium CSD, chose to fully replace its settlement and custody platform by a new package that will bring ahead of T2S, ISO 20022 and some of the T2S features. We are leveraging this opportunity to anticipate the developments of the new messages and future T2S settlement services. We are currently testing the new system and messaging with NBB-SSS – while the Eurosystem will not provide any testing environments for CSD participants before March 2015.

With all these migration projects added to other dedicated T2S adaptations, the AceTP teams and all our local experts and operational teams will certainly remain busy for the next few years! We anticipated this work and have

built extra bandwidth throughout our locations by maximising the Lisbon International operations centre. Given our expertise in planning for migrations of this

magnitude, we are very confident to guarantee a smooth transition to T2S for our clients and deliver new and harmonised added-value settlement services for T2S.

AceTP is designed to deal with the many proprietary message formats used by CSDs

We anticipated this work and have built

extra bandwidth throughout our

locations by maximising the

Lisbon International operations centre

9

Cash solutions in T2S

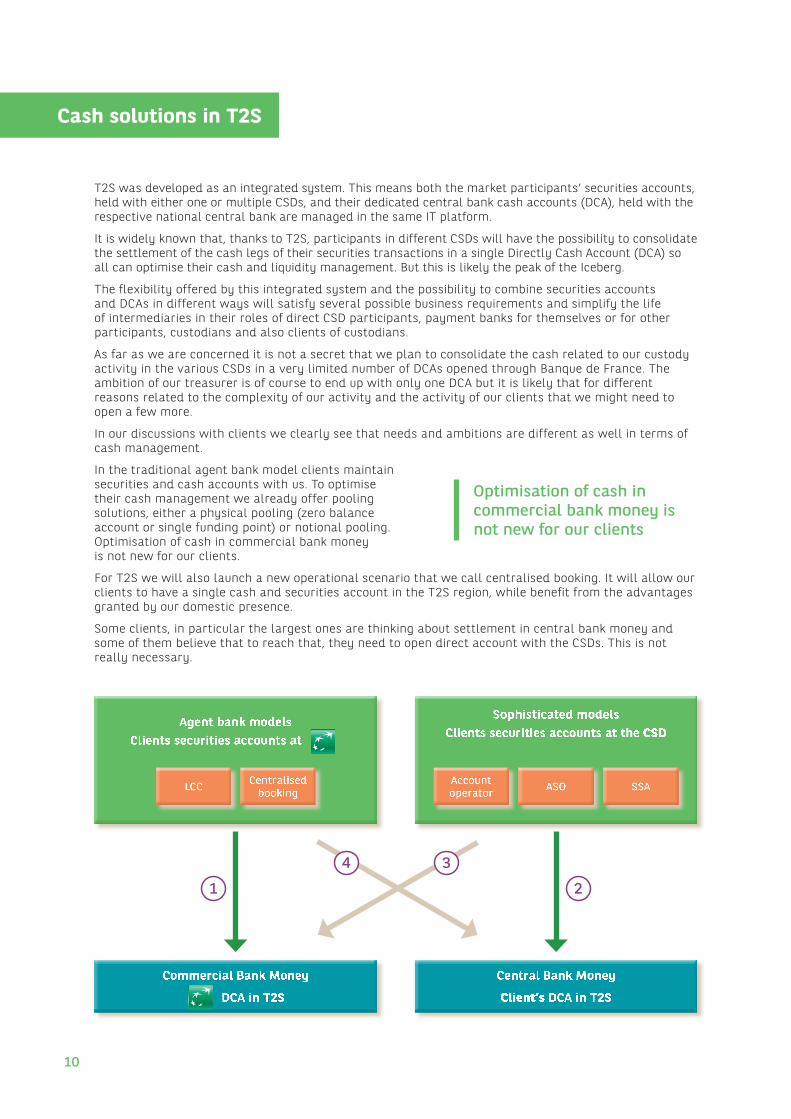

T2S was developed as an integrated system. This means both the market participants’ securities accounts, held with either one or multiple CSDs, and their dedicated central bank cash accounts (DCA), held with the respective national central bank are managed in the same IT platform.

It is widely known that, thanks to T2S, participants in different CSDs will have the possibility to consolidate the settlement of the cash legs of their securities transactions in a single Directly Cash Account (DCA) so all can optimise their cash and liquidity management. But this is likely the peak of the Iceberg.

The flexibility offered by this integrated system and the possibility to combine securities accounts and DCAs in different ways will satisfy several possible business requirements and simplify the life of intermediaries in their roles of direct CSD participants, payment banks for themselves or for other participants, custodians and also clients of custodians.

As far as we are concerned it is not a secret that we plan to consolidate the cash related to our custody activity in the various CSDs in a very limited number of DCAs opened through Banque de France. The ambition of our treasurer is of course to end up with only one DCA but it is likely that for different reasons related to the complexity of our activity and the activity of our clients that we might need to open a few more.

In our discussions with clients we clearly see that needs and ambitions are different as well in terms of cash management.

In the traditional agent bank model clients maintain securities and cash accounts with us. To optimise their cash management we already offer pooling solutions, either a physical pooling (zero balance account or single funding point) or notional pooling. Optimisation of cash in commercial bank money is not new for our clients.

For T2S we will also launch a new operational scenario that we call centralised booking. It will allow our clients to have a single cash and securities account in the T2S region, while benefit from the advantages granted by our domestic presence.

Some clients, in particular the largest ones are thinking about settlement in central bank money and some of them believe that to reach that, they need to open direct account with the CSDs. This is not really necessary.

Optimisation of cash in commercial bank money is not new for our clients

10

Commercial Bank Money

DCA in T2S

Central Bank Money

Client’s DCA in T2S

Agent bank models

Clients securities accounts at

LCCCentralised

booking

Sophisticated models

Clients securities accounts at the CSD

Accountoperator

ASO SSA

34

1 2

In the picture above you can immediately perceive that on top of combinations already available in the current securities settlement systems that new ones can be added. T2S is extremely flexible and for our clients it will be possible to link accounts opened with us with a DCA in their name and linked to their T2S account. We realised that this scenario might be appealing in particular for clients that already manage their own domestic activity. As they already have their own DCA, they might want to link to the activity they settle with us in other T2S markets to their own DCA. Thanks to a recent change request related to the management of the autocollateralisation process in T2S, this operational scenario should also allow our clients easy access to the autocollateralisation, if necessary. This is an aspect we are currently investigating with a few central banks. Another interesting matter to be developed with regulators is how they assess this scenario in terms of responsibilities.

Since our last newsletter, T2S has moved from white board conversations on what could work to a more practical discussion of what will work. We are working closely with all our clients to listen and understand their specific requirements. Their

requirements are helping us develop the combination of direct account solutions with our added value services offered through managed connections. We have

proven through our discussions that different models fit the needs equally well amongst our client base. The merits of commercial bank money settlement and the full service model remain while we continue engaging on adapted solutions that meet specific requirements.

T2S has moved from white board conversations on what could work to a more practical discussion of what will work

The information contained within this document (‘information’) is believed to be reliable but BNP Paribas Securities Services does not warrant its completeness or accuracy. Opinions and estimates contained herein constitute BNP Paribas Securities Services’ judgment and are subject to change without notice. BNP Paribas Securities Services and its subsidiaries shall not be liable for any errors, omissions or opinions contained within this document. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For the avoidance of doubt, any information contained within this document will not form an agreement between parties. Additional information is available on request.

BNP Paribas Securities Services is incorporated in France as a Partnership Limited by Shares and is authorised and supervised by the ACPR (Autorité de Contrôle Prudentiel et de Résolution) and the AMF (Autorité des Marchés Financiers).

BNP Paribas Securities Services, London branch is authorised by the ACPR, the AMF and the Prudential Regulation Authority and is subject to limited regulation by the Financial Conduct Authority and Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority and regulation by the Financial Conduct Authority are available from us on request. BNP Paribas Securities Services, London branch is a member of the London Stock Exchange. BNP Paribas Trust Corporation UK Limited (a wholly owned subsidiary of BNP Paribas Securities Services), incorporated in the UK is authorised and regulated by the Financial Conduct Authority.

In the U.S., BNP Paribas Securities Services is a business line of BNP Paribas which is incorporated in France with limited liability. Services provided under this business line, including the services described in this document, if offered in the U.S., are offered through BNP Paribas, New York Branch (which is duly authorized and licensed by the State of New York Department of Financial Services); if a securities product, through BNP Paribas Securities Corp. or BNP Paribas Prime Brokerage, Inc., each of which is a broker-dealer registered with the Securities and Exchange Commission and a member of SIPC and the Financial Industry Regulatory Authority; or if a futures product through BNP Paribas Securities Corp., a Futures Commission Merchant registered with the Commodities Futures Trading Commission and a member of the National Futures Association.

Printed on recycled paper by Edit’overso – Designed by the graphics department, corporate communications, BNP Paribas Securities Services – June 2014

Follow us on Twitter @BNPP2S

For more information, please visit securities.bnpparibas.com