T HE ABC’ S OF B USINESS V ALUATION Jim Turner, C.P.A. CVA Turner Business Appraisers & Advisors.

51

THE ABC’S OF BUSINESS VALUATION Jim Turner, C.P.A. CVA Turner Business Appraisers & Advisors

-

Upload

janis-watkins -

Category

Documents

-

view

218 -

download

4

Transcript of T HE ABC’ S OF B USINESS V ALUATION Jim Turner, C.P.A. CVA Turner Business Appraisers & Advisors.

THE ABC’S OF BUSINESS VALUATIONJim Turner, C.P.A. CVA

Turner Business Appraisers & Advisors

SEMINAR OBJECTIVES

You will learn how to utilize the 3 established approaches to value a business and we will estimate the value employing a good rule of thumb

By the end of our session you will understand the basic steps required to calculate the value of a business….Valuation is both an Art and a Science

We will discuss the nuances of valuing businesses; including marketability discounts, normalizing adjustments and the concept of control

BUSINESS VALUATION & THE BABY BOOMERS

75 Million baby boomers

7 Million own privately held businesses

It is forecasted that between 1.36 and 2 million firms will be for sale in the next five to ten years

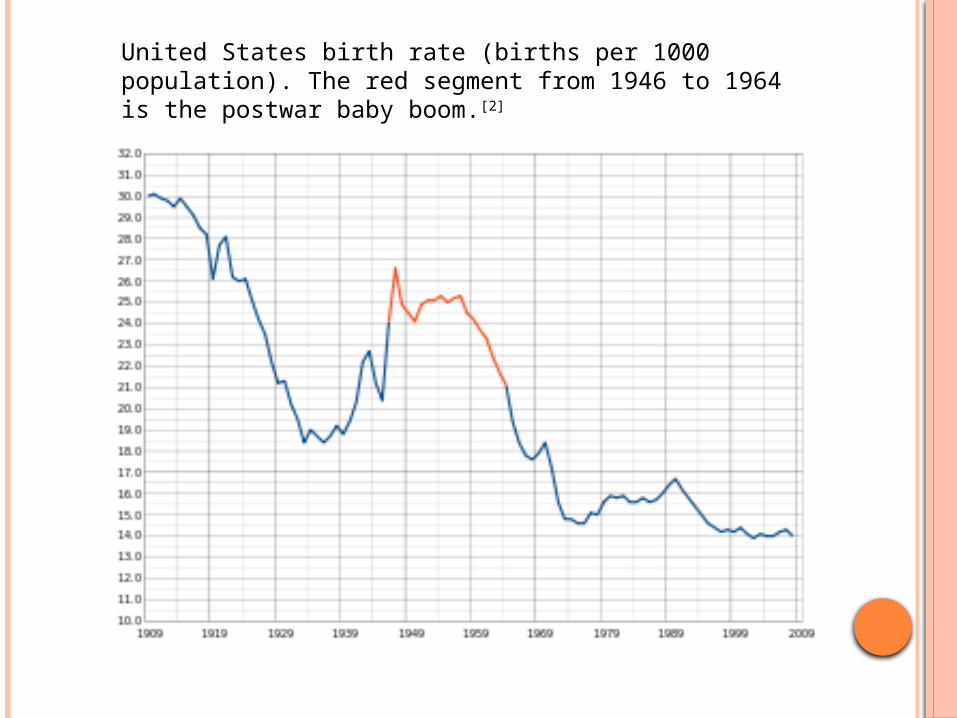

United States birth rate (births per 1000 population). The red segment from 1946 to 1964 is the postwar baby boom.[2]

WHY VALUE A BUSINESS?

Buy/Sell decisions

Gift or Estate Tax (IRS)

Shareholder actions

Equitable distribution

Key man or Key Woman Life insurance

WHO ARE THE EXPERTS

ABV = Accredited in Business Valuation

CVA = Certified Valuation Analyst is a CPA, MBA, Ph.d or Degreed Financial Professional

ASA = An Accredited Senior Appraiser

APPROACHES TO VALUING A BUSINESS

The established approaches to value IRS Revenue Ruling 59-60

Income Approach Market Approach Asset Approach

Sanity Check/Quick estimate Rules of thumb

SAMPLE BUSINESS VALUATION

Purpose of the valuation – The owner is contemplating selling the business; so he wants to know the fair market value of the business in exchange

Common deal terms of a small business transaction Asset Sale

Includes: Equipment, inventory and goodwill Does not include: Cash or accounts receivable

THE AMERICAN DREAM

OUR ENTREPRENEURS

Living the Dream!

SAMPLE BUSINESS VALUATION

SAMPLE BUSINESS VALUATION

SAMPLE BUSINESS VALUATIONINCOME APPROACH

SAMPLE BUSINESS VALUATIONIBBOTSON BUILD-UP METHOD

Source: 2013 Ibbotson® Stocks, Bonds, Bills and Inflation Valuation Yearbook, Morningstar, Inc., Chicago, Illinois.

SAMPLE BUSINESS VALUATIONINCOME APPROACH

SAMPLE BUSINESS VALUATIONMARKETABILITY DISCOUNT (INCOME APPROACH)

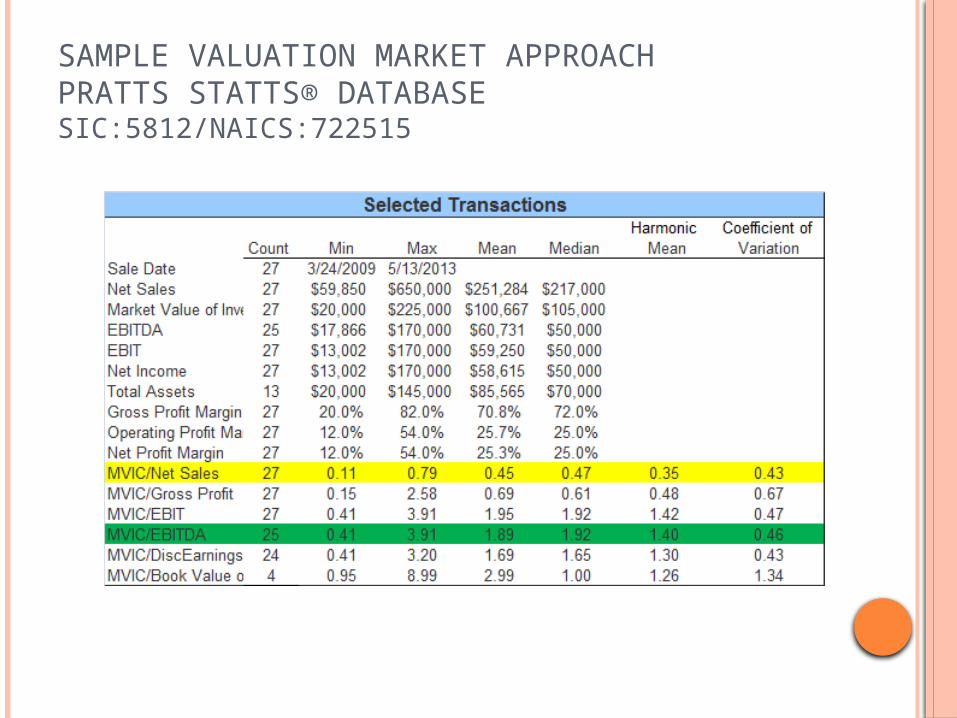

SAMPLE VALUATION MARKET APPROACHPRATTS STATTS® DATABASE SIC:5812/NAICS:722515

SAMPLE VALUATION MARKET APPROACH

SAMPLE VALUATION ADJUSTED NET ASSET VALUE APPROACH

The appraised fair market value of the equipment was $60

SAMPLE BUSINESS VALUATION

Summarized results table

Based upon the results of the 3 approaches to value; our opinion of value for the subject company is $1,500

SANITY TEST

SANITY TEST CONTINUATION

USING RULES OF THUMB

RULES OF THUMB

The single best source for rules of thumb for small business is the, “Business Reference Guide,” published by Business Brokerage Press

Pricing multiples: multiples of EBITDA or SDE Sellers discretionary earnings is earnings before

interest, taxes, depreciation and amortization plus one owners salary or “EBITDAOC “

– Multiple of sales

RULES OF THUMB

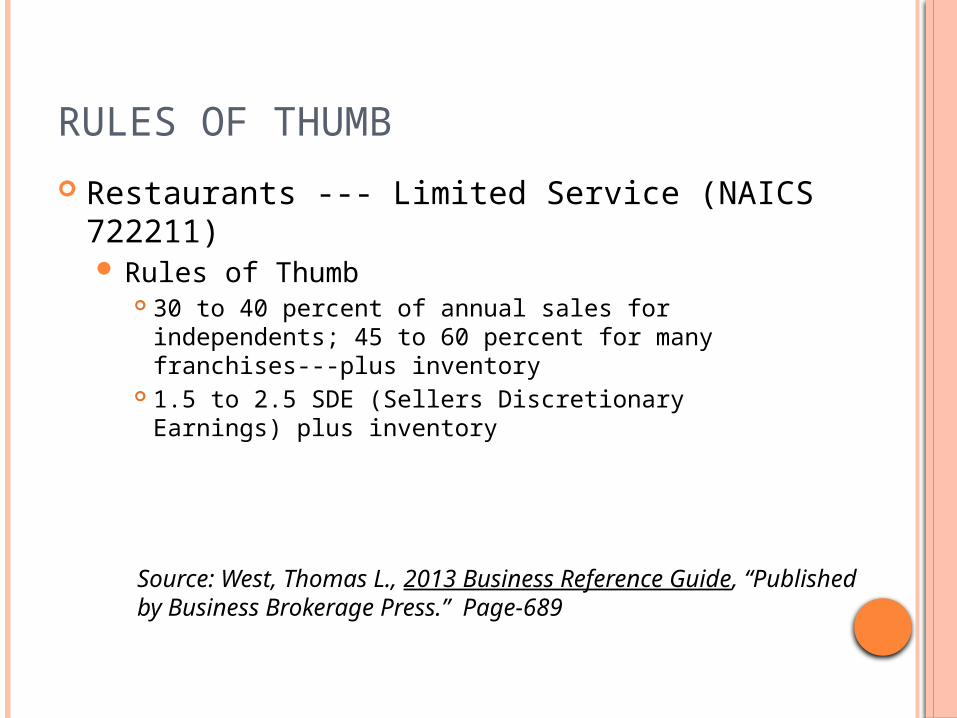

Restaurants --- Limited Service (NAICS 722211) Rules of Thumb

30 to 40 percent of annual sales for independents; 45 to 60 percent for many franchises---plus inventory

1.5 to 2.5 SDE (Sellers Discretionary Earnings) plus inventory

Source: West, Thomas L., 2013 Business Reference Guide, “Published by Business Brokerage Press.” Page-689

RULES OF THUMB

*Rule of Thumb #1 is in harmony with the results of the income approach and our opinion of value - $1,500.

PART II – THE FUTURE AFFECTS VALUE TODAY

INDUSTRY INDICATORS

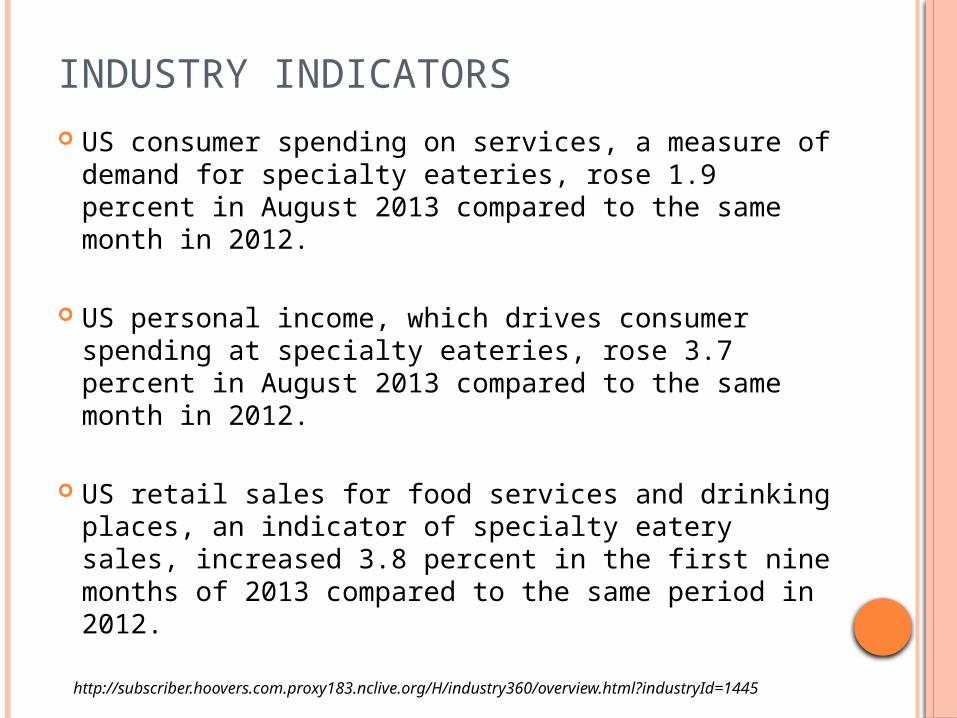

US consumer spending on services, a measure of demand for specialty eateries, rose 1.9 percent in August 2013 compared to the same month in 2012.

US personal income, which drives consumer spending at specialty eateries, rose 3.7 percent in August 2013 compared to the same month in 2012.

US retail sales for food services and drinking places, an indicator of specialty eatery sales, increased 3.8 percent in the first nine months of 2013 compared to the same period in 2012.

http://subscriber.hoovers.com.proxy183.nclive.org/H/industry360/overview.html?industryId=1445

INDUSTRY GROWTH FORECAST

Source:http://subscriber.hoovers.com.proxy183.nclive.org/H/industry360/overview.html?industryId=1445

First Research forecasts are based on INFORUM forecasts that are licensed from the Interindustry Economic Research Fund, Inc. (IERF) in College Park, MD. INFORUM's "interindustry-macro" approach to modeling the economy captures the links between industries and the aggregate economy.

FEDERAL RESERVE BEIGE BOOK

Fifth District--Richmond Beige Book -- October 16, 2013

District economic conditions improved modestly, on balance, since our last report.

Source: http://www.federalreserve.gov/monetarypolicy/beigebook/beigebook201310.htm?richmond

NORTH CAROLINA ECONOMIC OUTLOOK SUMMER 2013

Executive Summary: A Return to Growth, and the Old Issues

Economic improvement is expected to continue in North Carolina in the second half of 2013 and in 2014.

Nationally, 2 million payroll jobs will be added in 2013, and 2.5 million payroll jobs will be added in 2014, thereby lowering the jobless rate to 6.8% at the end of 2013 and 6.2% at the close of 2014.

Source: http://ag-econ.ncsu.edu/sites/ag-econ.ncsu.edu/files/faculty/walden/nceconomicoutlooksummer2013.pdf

CHARLOTTE MSA ECONOMY

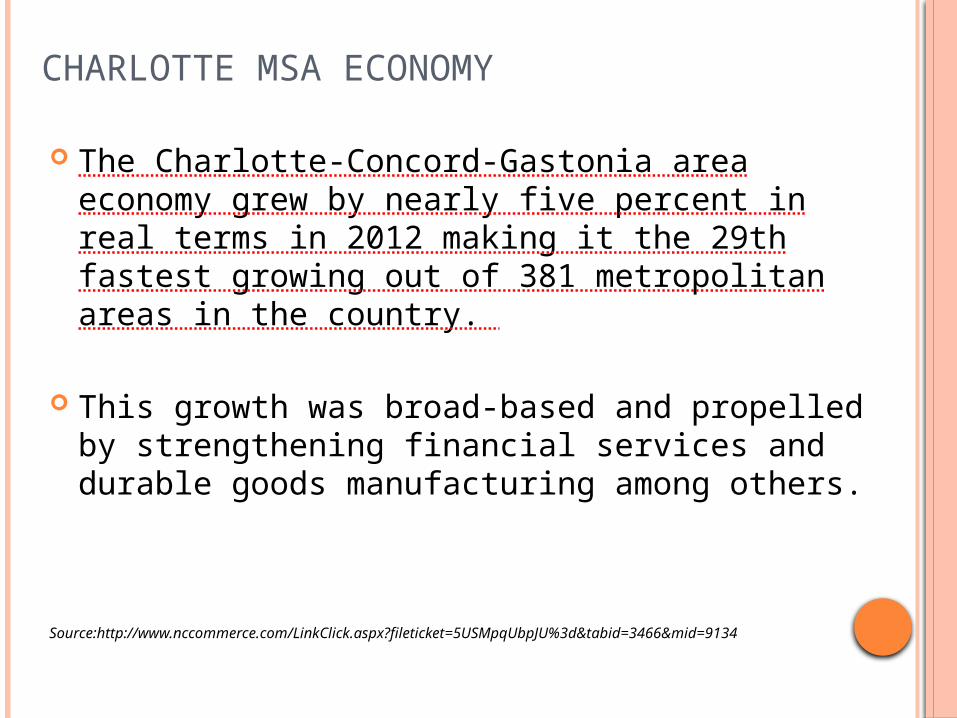

The Charlotte-Concord-Gastonia area economy grew by nearly five percent in real terms in 2012 making it the 29th fastest growing out of 381 metropolitan areas in the country.

This growth was broad-based and propelled by strengthening financial services and durable goods manufacturing among others.

Source:http://www.nccommerce.com/LinkClick.aspx?fileticket=5USMpqUbpJU%3d&tabid=3466&mid=9134

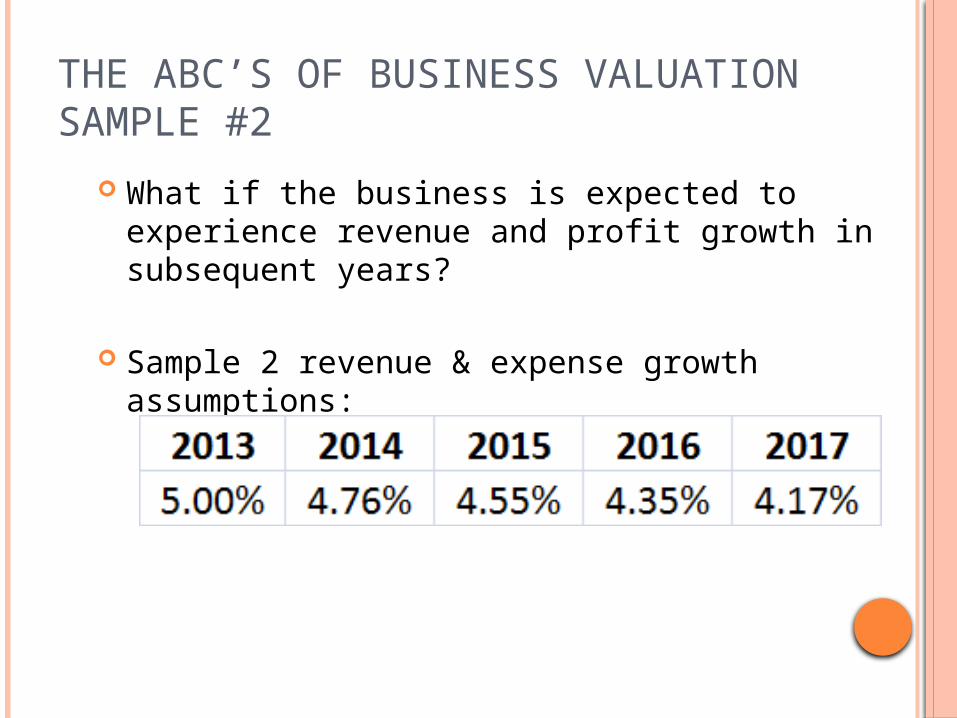

THE ABC’S OF BUSINESS VALUATION SAMPLE #2

What if the business is expected to experience revenue and profit growth in subsequent years?

Sample 2 revenue & expense growth assumptions:

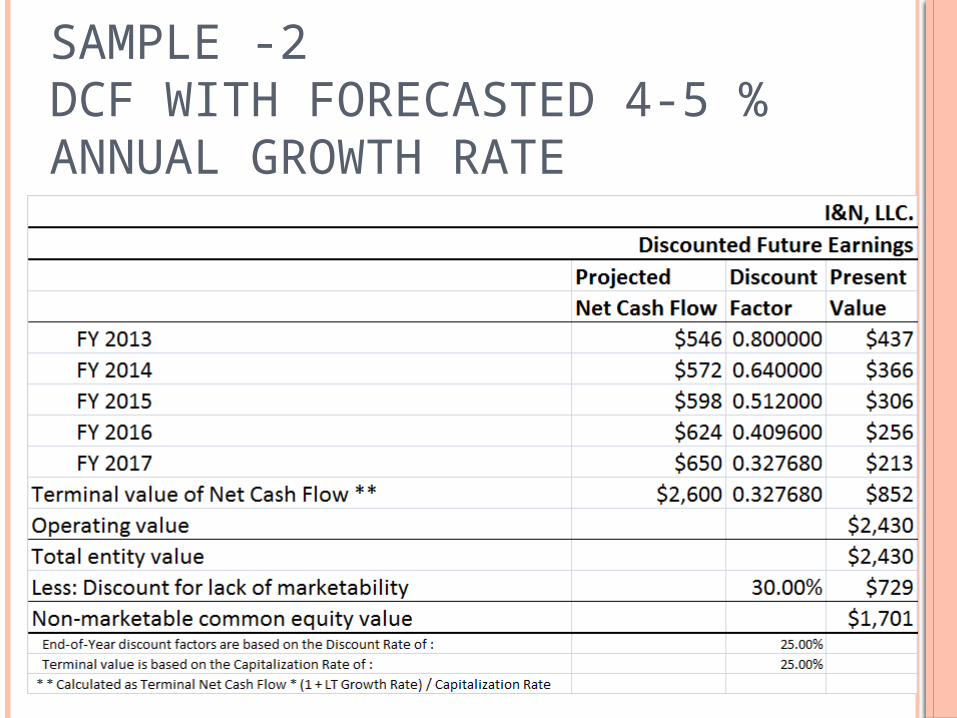

SAMPLE-2 WITH 4-5% ANNUAL GROWTH

SAMPLE -2 DCF WITH FORECASTED 4-5 % ANNUAL GROWTH RATE

PART III – “APPLES TO APPLES ”COMMON SIZE ANALYSIS

COMMON SIZE BALANCE SHEET

*Source: https://www.profitcents.com/USEN/runreport/generatereport.aspx?GUID=40b10acb-4149-4d43-9b7c-cbd4b6e1e2f2

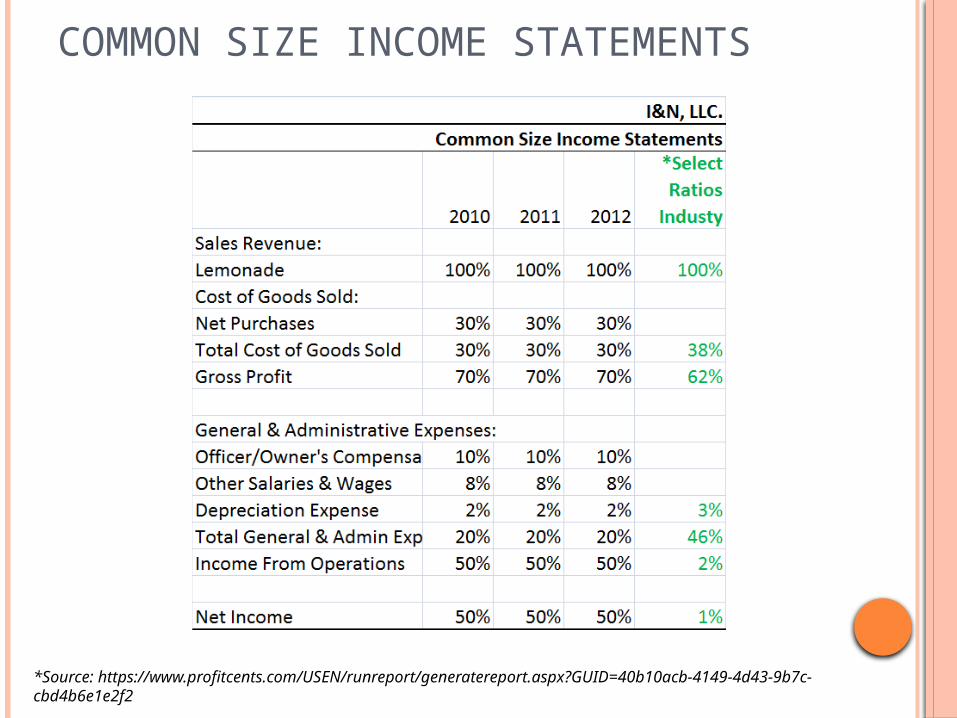

COMMON SIZE INCOME STATEMENTS

*Source: https://www.profitcents.com/USEN/runreport/generatereport.aspx?GUID=40b10acb-4149-4d43-9b7c-cbd4b6e1e2f2

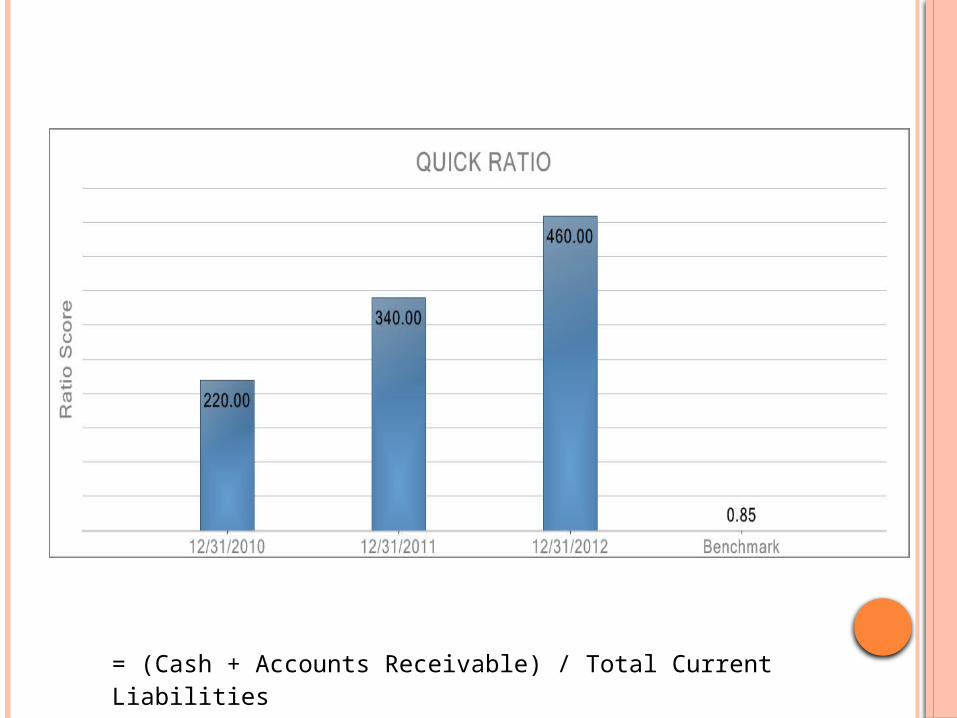

LIQUIDITYA measure of the company's ability to meet obligations as they come due.

Checking the pulse of a business: Key Financial Ratios

= (Cash + Accounts Receivable) / Total Current Liabilities

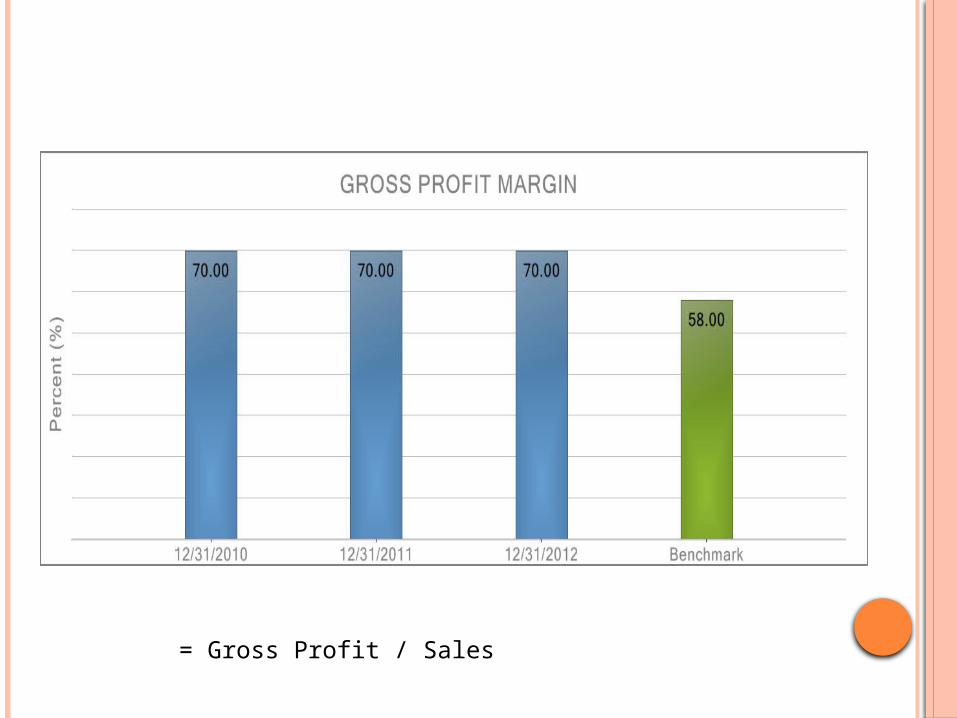

PROFITS & PROFIT MARGINA measure of whether the trends in profit are favorable for the company.

= Gross Profit / Sales

ASSETSA measure of how effectively the company is utilizing its gross fixed assets.

= Net Income / Total Equity

OVERVIEW OF I&N, LLC. RATIOS COMPARED TO INDUSTRY PEERS

Rating Metric

LIQUIDITY

PROFITS & PROFIT MARGIN

SALES

BORROWING

ASSETS

Source: https://www.profitcents.com/USEN/runreport/generatereport.aspx?GUID=40b10acb-4149-4d43-9b7c-cbd4b6e1e2f2

PART IV – “NORMALIZING” IS AN EFFORT TO ADJUST TAX OR GAAP BASIS FINANCIALS INTO ECONOMIC REALITY

It is widely accepted that most financial statements often paint a picture that is different from economic reality*

Highly aggressive expensing policies to reduce income taxesExcessive or insufficient compensation to owner(s)Lavish perquisites (perks) paid to the owner(s)Leases (Capital vs. Operating)

Source: “Business Valuations: Fundamentals, Techniques and Theory,” 1995-2009 National Association of Certified Valuation Analysts 2009.v3, page-3-3

SAMPLE #3 NORMALIZING ADJUSTMENT TO OWNERS COMPENSATION

NORMALIZED NET CASH FLOW

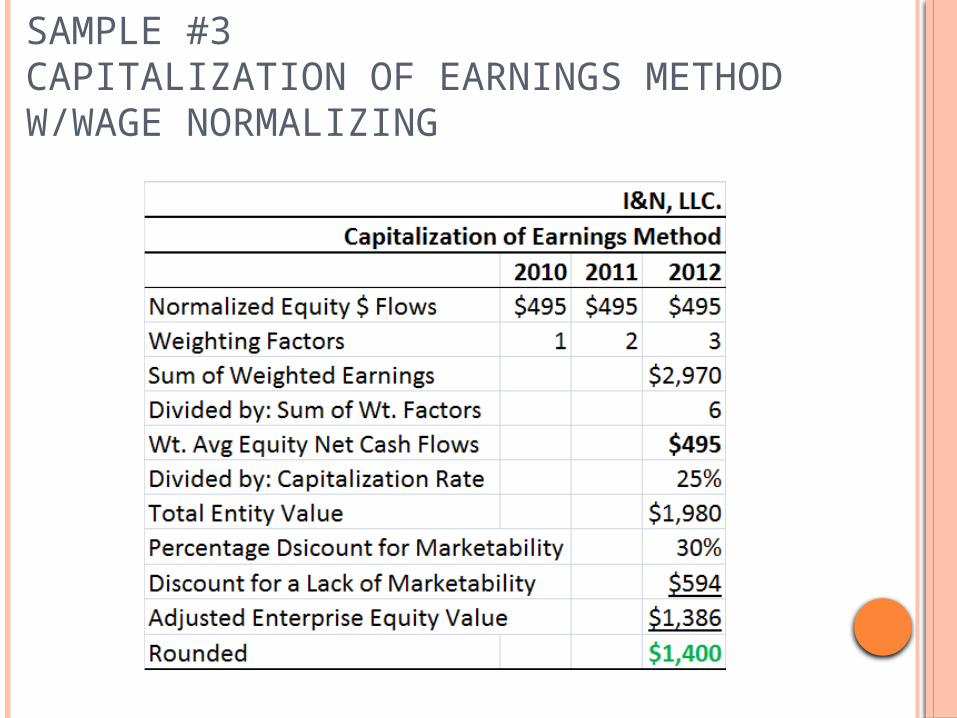

SAMPLE #3 CAPITALIZATION OF EARNINGS METHOD W/WAGE NORMALIZING

CONCLUSION

Fifty-one percent is usually one-hundred percent better than forty-nine percent.

Peanuts, popcorn, cotton-candy, cigarettes….discount for a lack of marketability

Render unto Caesar that which is Caesars (normalizing adjustments)

OUR ENTREPRENEURS AFTER THE SALE