Systems of taxation in Ukraine

20

SYSTEMS OF TAXATION Have executed: Natalia Yakovenko Helen Anokhina Svitlana Shapoval Vlad Kozlov

-

Upload

kyiv-national-economic-university -

Category

Documents

-

view

283 -

download

0

Transcript of Systems of taxation in Ukraine

SYSTEMS OF TAXATION

Have executed:

Natalia YakovenkoHelen AnokhinaSvitlana ShapovalVlad Kozlov

System of taxation – is a set of taxes paid to the budget and state funds in the laws of Ukraine the

order and the rights, duties and responsibilities of

taxpayers.

Ukraine's tax system provides the

following forms of taxation:

- general system of taxation;

- simplified system of taxation.

Legal entities and individual entrepreneurs on a

common system of taxation have the right to

engage in any activity not prohibited by law,

have an unlimited amount of income and the

number of employed workers.

General system of taxation

Distribution of taxation for legal entities and individuals

To an object of taxation:

Individuals

Net income =

Taxable income -

expenses

(documented).

Legal entities

Profit sourced from

Ukraine and abroad, as

determined by reducing

the amount of income

for the reporting period

cost of sold goods

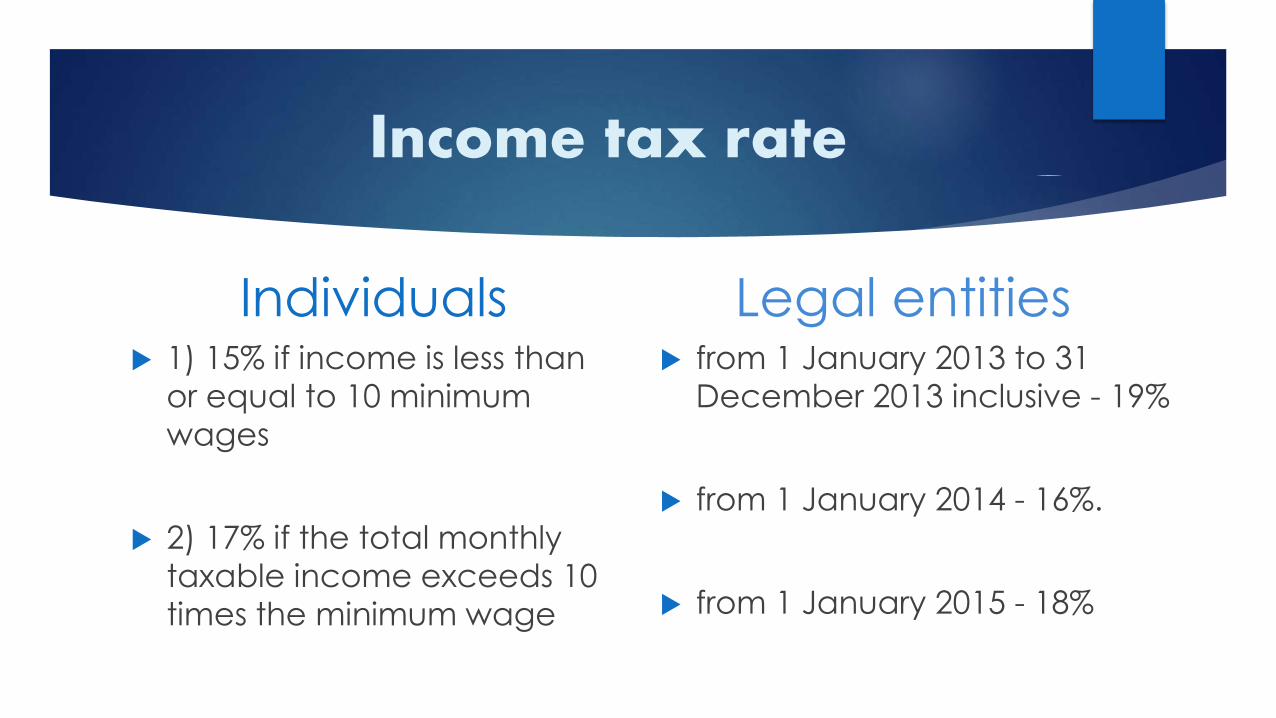

Income tax rate

Individuals 1) 15% if income is less than

or equal to 10 minimum

wages

2) 17% if the total monthly

taxable income exceeds 10

times the minimum wage

Legal entities from 1 January 2013 to 31

December 2013 inclusive - 19%

from 1 January 2014 - 16%.

from 1 January 2015 - 18%

Value-added tax

Individuals When reaching a volume of

taxable transactions 300

thousand. USD. 12 months

entrepreneur is obliged to

register for VAT.

The rate of VAT 12/31/2013 -

20% from 01.01.2014 - 17%.

01/01/2015 - 17%

Legal entities The amount of taxable

transactions in the last 12

months exceeds 300

thousand USD. Compulsory

registration.

VAT rate to 12/31/2013 - 20%

from 01.01.2014 - 17%.

01/01/2015 - 17%

Single social contribution

Individuals

Single Contribution paid

by the entrepreneur in

the amount of 34.7% of

the profit base.

Legal entities

Enterprise paid Single

Contribution at the rate

of 36.76% - 49.7% of

payroll in charges wages

Payment carried out to

the Pension Fund to the

Special Account.

Other tax payments and fees:

Individuals

The entrepreneur may

be the payer of other

taxes and fees,

depending on the type

of ongoing activities.

Legal entities

The company can also

be the payer of taxes

and fees.

National

Legal entities

1) excise tax;

2) environmental tax;

3) rental fee;

4) dues

Local

Legal entities

1) property tax;

2) the fee for parking vehicles;

3) tourist tax.

Simplified system of taxation

Entities applying the simplified system

of taxation, accounting and reporting,

are divided into the following groups of

payers of single tax (Art. 291.4 CLE)

Taxpayers

groups

Criteria for

taxpayers of

single tax

Features of

activities

Basic tax rate Additional tax rate

Individual

entrepreneurs

1 - working without

employees;

- annual income

cannot exceed

300 000 UAH.

- engaged exclusively retail

trade of goods from market

places/ or conduct business

activities to provide domestic

services;

- till 10% of min wage per

calendar month;

- Max. exposure

to 12.01.2015 -

121.80 UAH

Article 293.4 of the Tax

Code Ukraine

from15% :

1) the amount exceeding

the limit of income that

gives the right to use

the simplified system;

2) income derived from

the implementation of

activities not specified

in the certificate payer

of single tax attributed

to 1 or 2 groups;

3) income received in the

application of the

method of settlement

other than cash;

4) income derived from

the implementation of

activities that do not

give the right to apply

the simplified tax

system.

2

- number of

employees - less

than 10 persons;

- annual income

can’t exceed

1500 000 UAH.

- doing business with the

provision of services

(including domestic) and

taxpayers of single tax/or

population, production/or

sale of goods, activity in the

restaurant industry;

- till 20% of the minimum wage

per calendar

month;

Max. exposure to

12/01/2015 -

243.60 UAH

Legal entities

+

Individual

entrepreneurs

3

- number of

employees -

unlimited;

- the amount of

income can’t

exceed 20 million

UAH

- carry out any activities

other than those prohibited

for payers of single tax.

- 2% of income for VAT payers;

- 4% of income

for defaulters of

VAT;

4 group payers of single tax includes farmers, whose share of

agricultural commodity production in the previous tax (reporting)

year equals or exceeds 75%

Single tax levied on land, property rights and the use to which executed and recorded in accordance

with the law/

Single tax rate for 4 group:

- for arable land, hayfields, pastures - 0.45%

(mountain areas and forest areas - up to 0.27%);

- perennial crops - 0.27% and mountain areas

and areas of Polesie - 0.09%;

- for land Water Fund - 1.35%

Calculating the sum of the single tax for 4 group is set current normative monetary valuation of land

taking into account the coefficients of indexation.

Problem

A. decided to register a limited liability

company, the main activities which will

provide various kinds of consulting

services.

Determine, payer of which taxes and

fees may be indicated after registration.

According to the general

system of taxation :

- if customers of services consist

of entities-VAT taxpayers, you

need to register as a VAT payer

company (17%);

- the company also pays income

tax of 18% of the income;

- SC payment to the pension fund

for compulsory social. insurance

of compensation of employees

(36.76% - 49.7%)

- NEED TO REGISTER A SINGLE TAX PAYER 3RD GROUP (ART. 291.4 CLE)

- SINGLE TAX AT THE RATE OF 2%, BUT STILL NEED TO REGISTER AS A VAT PAYER OR SINGLE TAX AT THE RATE OF 4%, EXCLUDING VAT (ART. 293.3 CLE)

According to the simplified system of taxation :

Solution

Conclusion

Analysis of the systems of taxation Ukraine

allows to conclude important inherent

drawbacks. The main drawback is the fiscal

direction of the tax system, the lack of detection

of the regulatory function of the main taxes. You

also need to pay attention to the return of VAT

from small and large businesses. This mechanism

is complicated, resulting in an infinite number of

instances that need to go. This in turn causes the

growth effect "shadow economy".