Best Practices in Identifying and Monitoring the Systemic Risks of Hedge Funds

Systemic Risks in Repo Markets

Somnath ChatterjeeCCBS, Bank of England

8, November 2013

Outline

• Repo markets introduction• Pro-cyclicality• Role of Collateral• UK banks’ aggregate repo activity• Margin flows under a 100 bps rates shock• Comparing securities lending and repo lending

CEMLA, November 2013

Introduction (1) – what is repo used for

• Financing long positions

• Covering short positions

• Risk taking by banks’ “matched book” desks

CEMLA, November 2013

Introduction (2) – who uses repo?

• Repo is used by hedge funds, securities dealers and the investment banking arms of commercial banks to fund their long positions and cover shorts

• Funding comes from non-bank cash providers or commercial banks

• An inter-dealer market exists to intermediate repo and take incremental risk

CEMLA, November 2013

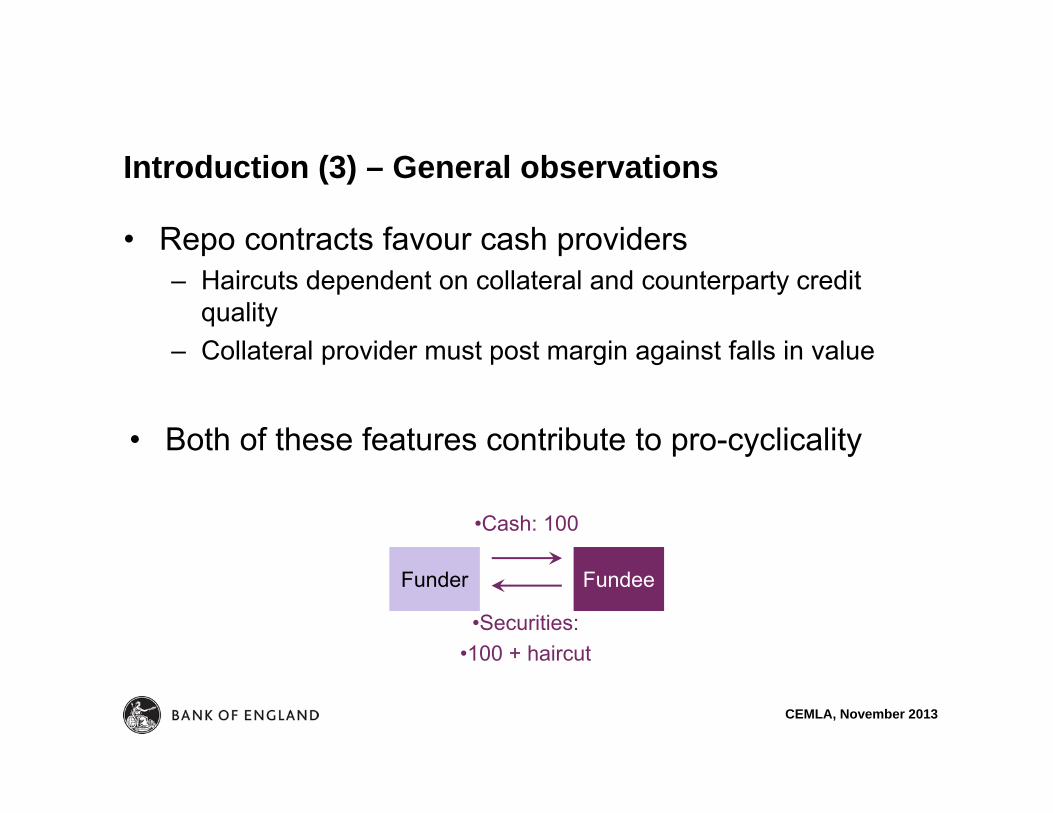

Introduction (3) – General observations

• Repo contracts favour cash providers– Haircuts dependent on collateral and counterparty credit

quality– Collateral provider must post margin against falls in value

• Both of these features contribute to pro-cyclicality

CEMLA, November 2013

Funder Fundee

•Securities:•100 + haircut

•Cash: 100

Pro-cyclicality (1)

• Haircut levels are based on the volatility/liquidity of the underlying instrument and the credit quality of the borrower

• As markets rise and volatility falls, haircuts fall: leverage can increase. A positive feedback mechanism.

• As markets fall and volatility rises, haircuts rise: leverage falls. An adverse feedback mechanism

CEMLA, November 2013

Pro-cyclicality (2)

• Are haircuts the true leverage constraint?

• Even without haircuts, repo is an inherently pro-cyclical funding tool– As collateral values rise more leverage is available– As collateral values fall cash borrowers must post more collateral or

other margin

• In the latter case repo acts as a mechanical contingent claim on the cash borrowers balance sheet.

CEMLA, November 2013

Pro-cyclicality (3): implications

• The requirement to post additional margin against declining alters the credit quality of the cash borrower (MF Global)

• Strategies or institutions that depend on repo may be inherently weaker than those who use unsecured funding

• Is this reflected in current regulation? If not should there be a change.

CEMLA, November 2013

What do we need to know?

• What leverage and maturity transformation is being generated through repo

• Against what instruments

• Haircuts– Pro-cyclical?– Do they constrain leverage?

• How do cash and collateral providers manage their leverage and maturity transformation?

CEMLA, November 2013

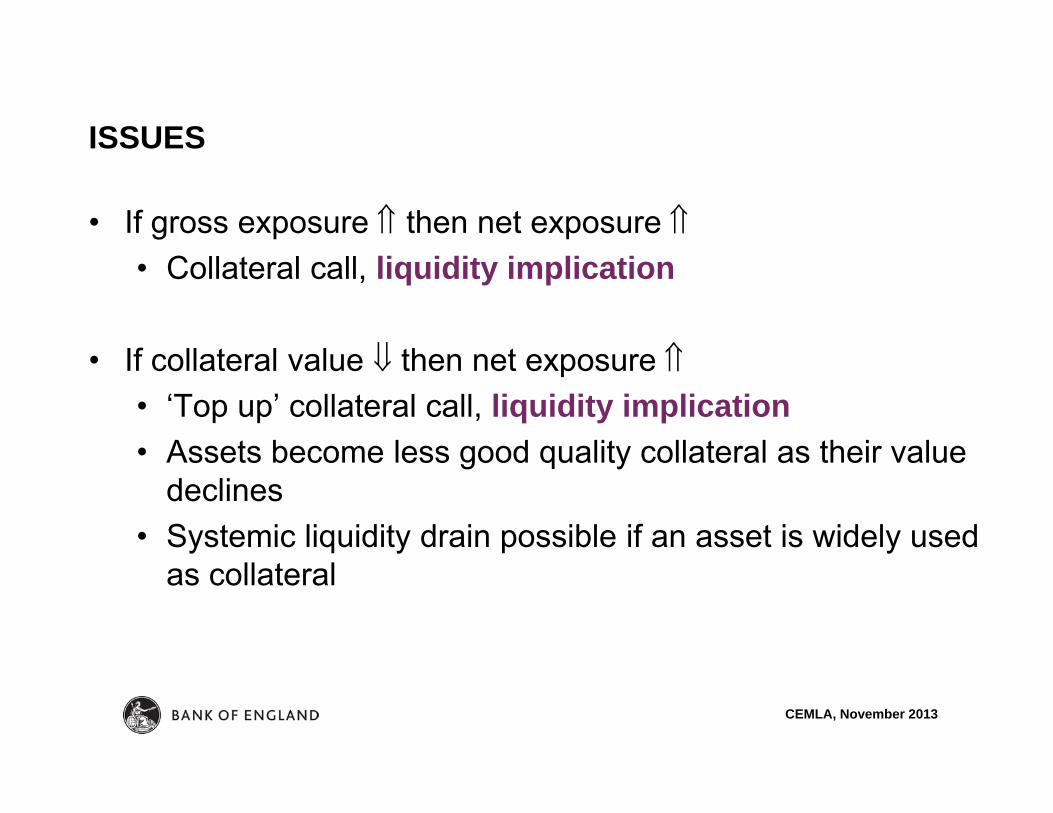

• If gross exposure then net exposure • Collateral call, liquidity implication

• If collateral value then net exposure • ‘Top up’ collateral call, liquidity implication• Assets become less good quality collateral as their value

declines• Systemic liquidity drain possible if an asset is widely used

as collateral

ISSUES

CEMLA, November 2013

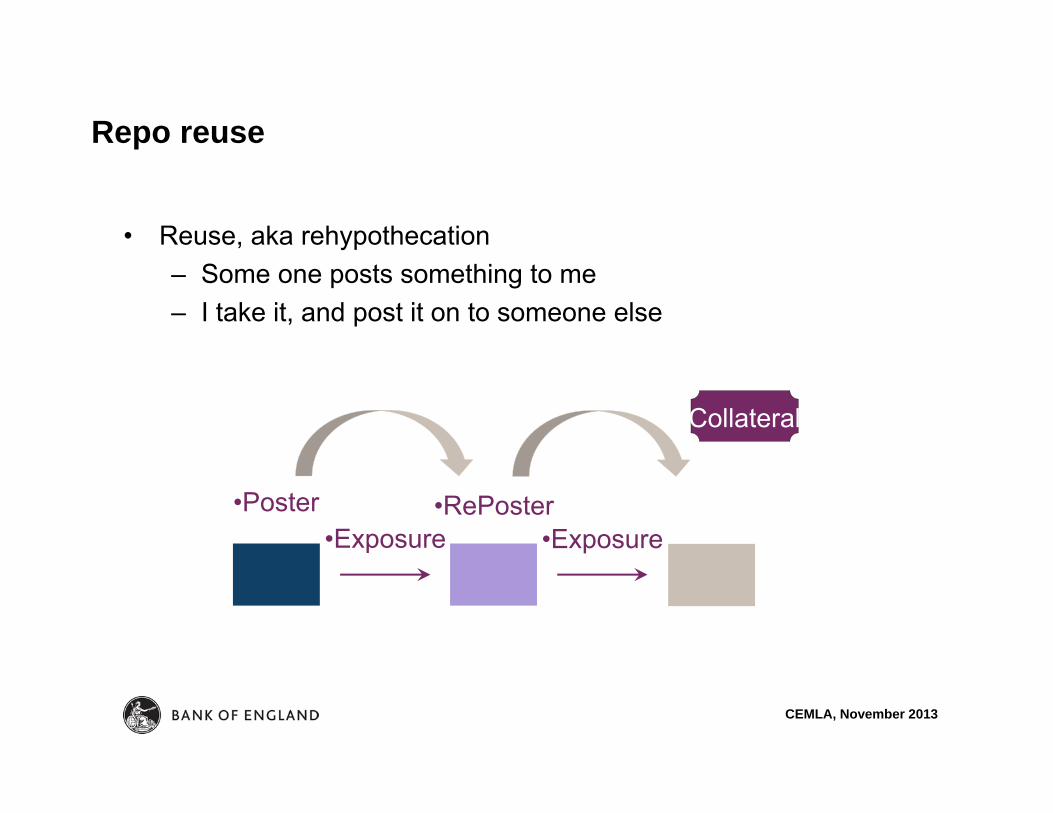

• Reuse, aka rehypothecation– Some one posts something to me– I take it, and post it on to someone else

Repo reuse

•Poster •RePoster•Exposure •Exposure

Collateral

CEMLA, November 2013

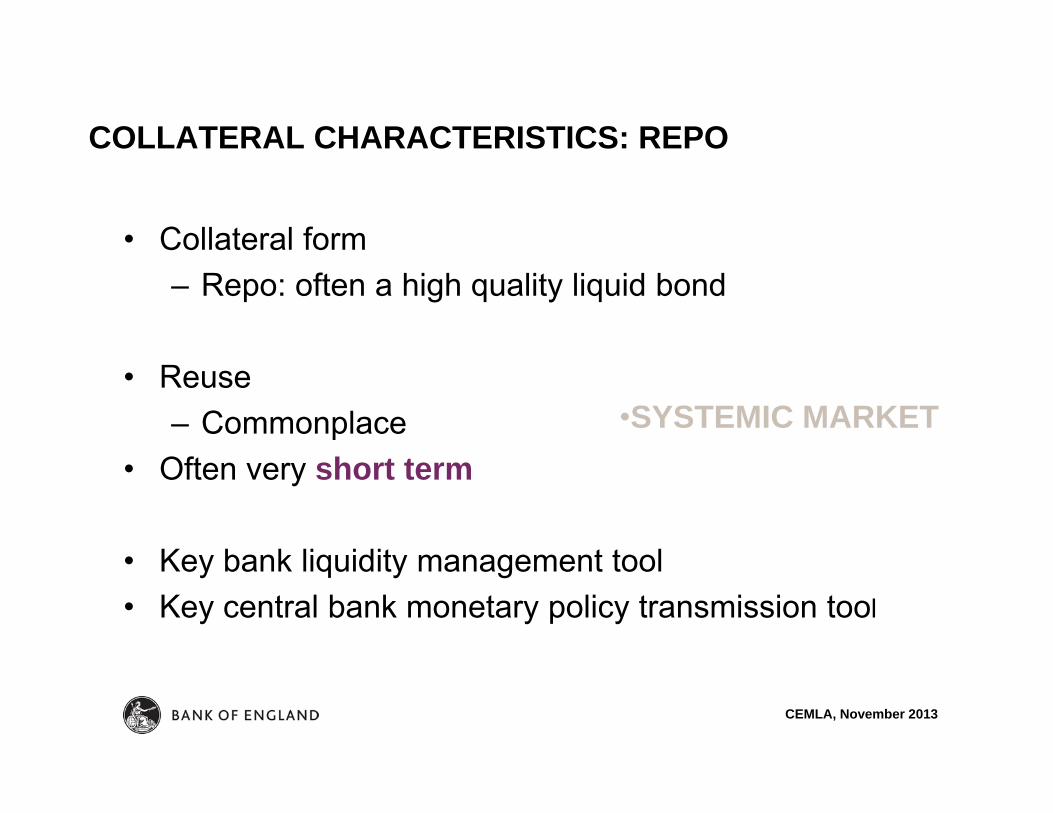

• Collateral form– Repo: often a high quality liquid bond

• Reuse– Commonplace

• Often very short term

• Key bank liquidity management tool• Key central bank monetary policy transmission tool

COLLATERAL CHARACTERISTICS: REPO

•SYSTEMIC MARKET

CEMLA, November 2013

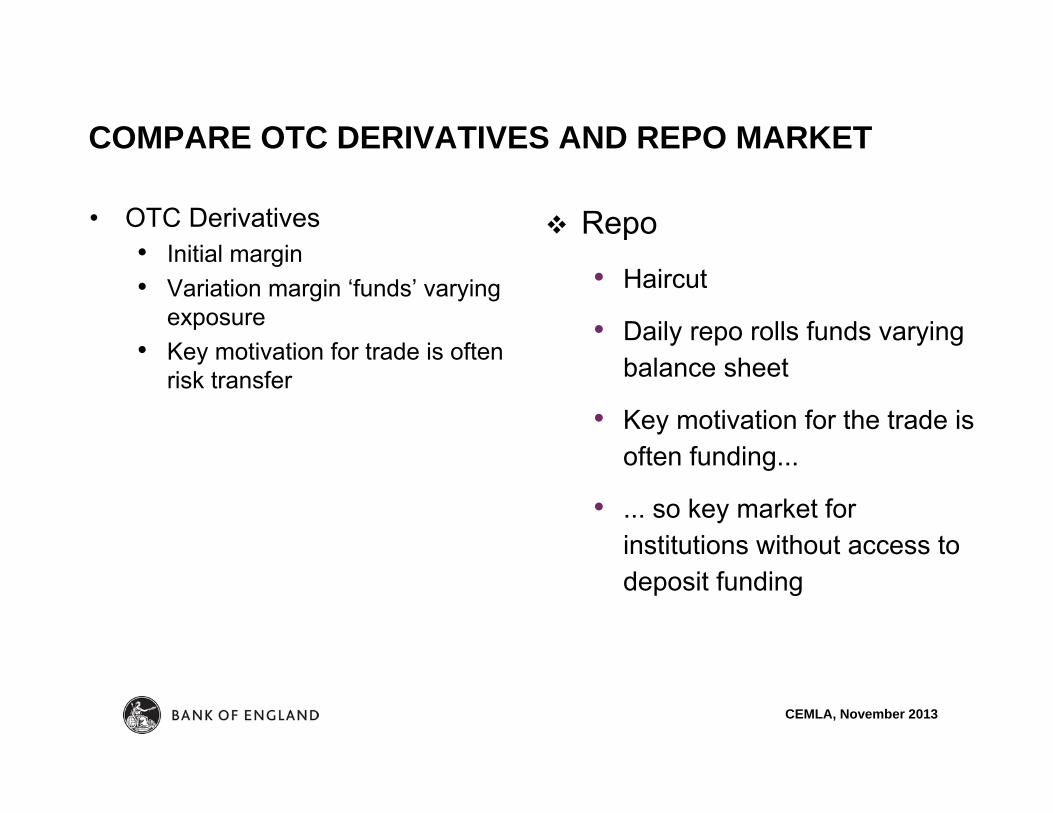

COMPARE OTC DERIVATIVES AND REPO MARKET

• OTC Derivatives• Initial margin• Variation margin ‘funds’ varying

exposure• Key motivation for trade is often

risk transfer

Repo

• Haircut

• Daily repo rolls funds varying balance sheet

• Key motivation for the trade is often funding...

• ... so key market for institutions without access to deposit funding

CEMLA, November 2013

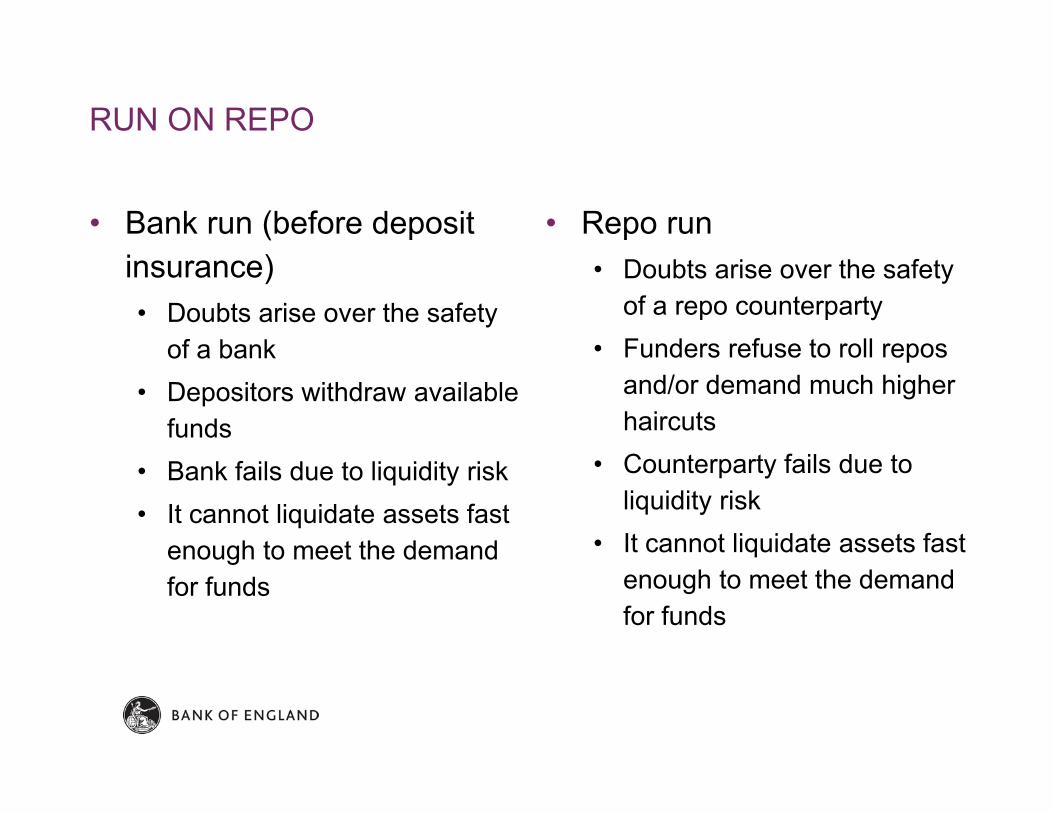

• Bank run (before deposit insurance)• Doubts arise over the safety

of a bank• Depositors withdraw available

funds• Bank fails due to liquidity risk• It cannot liquidate assets fast

enough to meet the demand for funds

• Repo run• Doubts arise over the safety

of a repo counterparty• Funders refuse to roll repos

and/or demand much higher haircuts

• Counterparty fails due to liquidity risk

• It cannot liquidate assets fast enough to meet the demand for funds

RUN ON REPO

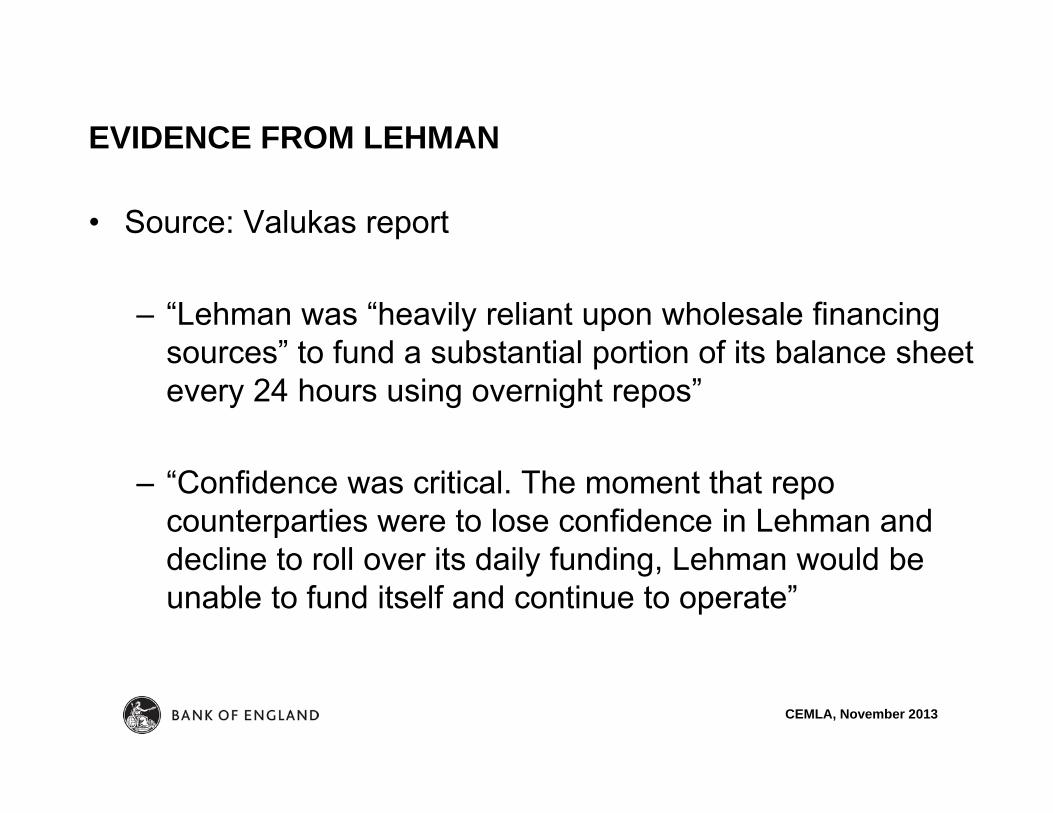

• Source: Valukas report

– “Lehman was “heavily reliant upon wholesale financing sources” to fund a substantial portion of its balance sheet every 24 hours using overnight repos”

– “Confidence was critical. The moment that repo counterparties were to lose confidence in Lehman and decline to roll over its daily funding, Lehman would be unable to fund itself and continue to operate”

EVIDENCE FROM LEHMAN

CEMLA, November 2013

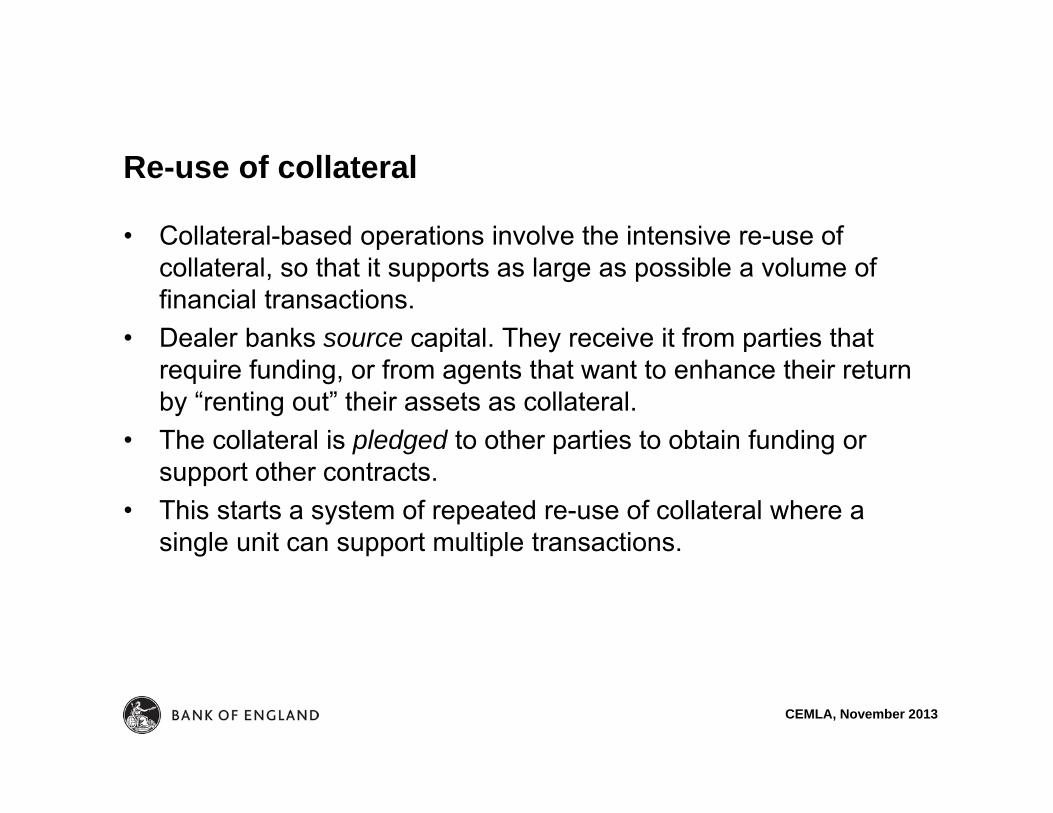

Re-use of collateral

• Collateral-based operations involve the intensive re-use of collateral, so that it supports as large as possible a volume of financial transactions.

• Dealer banks source capital. They receive it from parties that require funding, or from agents that want to enhance their return by “renting out” their assets as collateral.

• The collateral is pledged to other parties to obtain funding or support other contracts.

• This starts a system of repeated re-use of collateral where a single unit can support multiple transactions.

CEMLA, November 2013

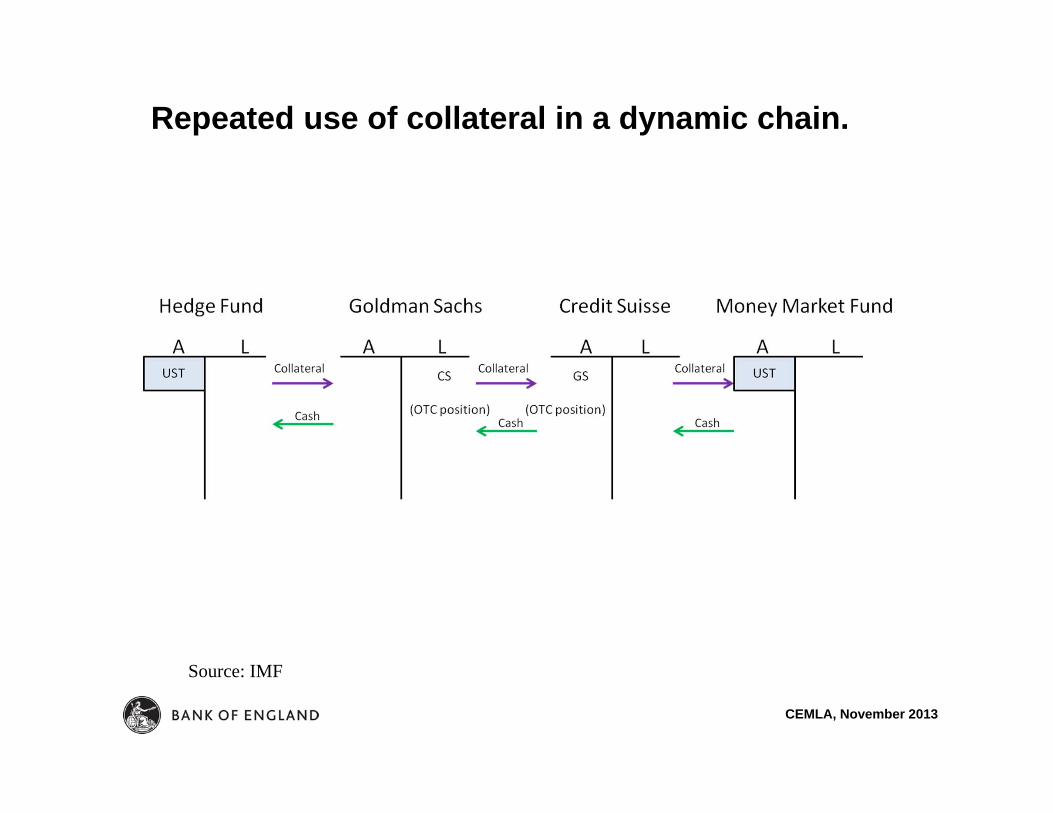

Repeated use of collateral in a dynamic chain.

Source: IMF

CEMLA, November 2013

Mapping the UK Financial System• Linking sectors financial balance sheets to draw a map of the UK

financial system

• Secured financing market (repo in particular) is a key inter-linkage as it:- represents a significant source of funding for banks and non-banks- supports liquidity in secondary asset markets

• Data availability is very patchy

• Built a UK-resident bank repo book balance sheet by combining imperfectly over-lapping data from a large number of sources

CEMLA, November 2013

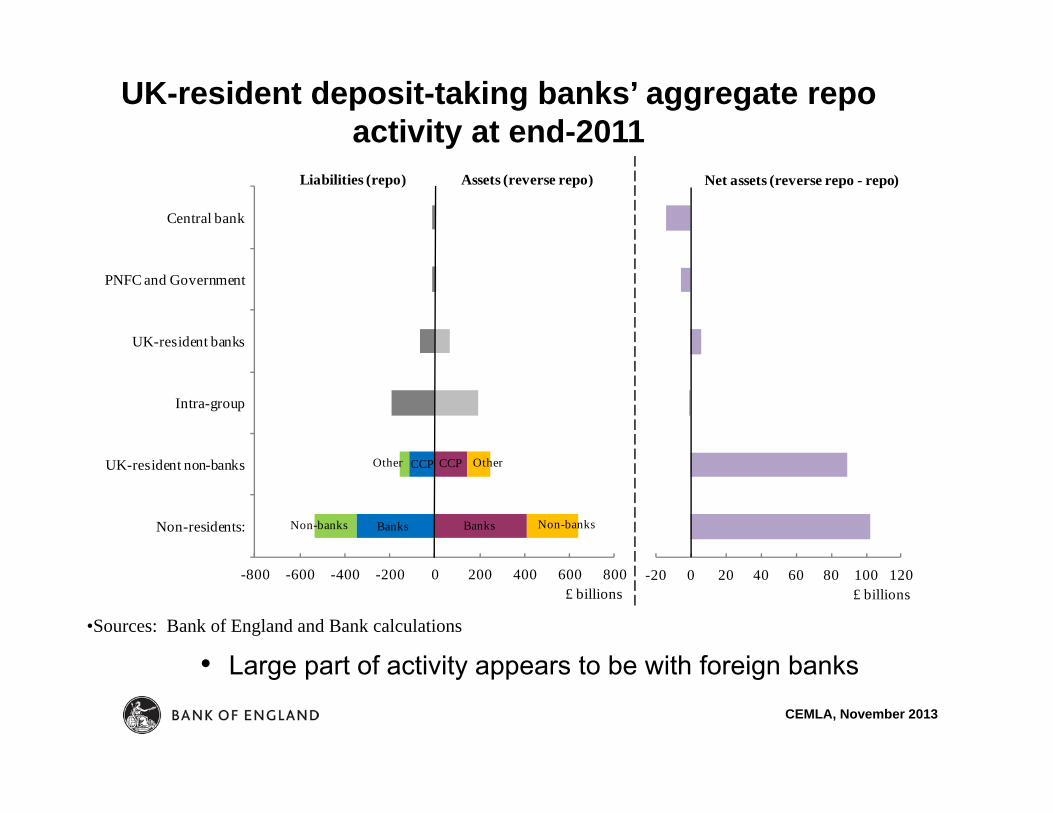

-800 -600 -400 -200 0 200 400 600 800

Non-residents:

UK-resident non-banks

Intra-group

UK-resident banks

PNFC and Government

Central bank

£ billions

Assets (reverse repo)Liabilities (repo)

Banks Non-banksNon-banks Banks

CCP OtherCCPOther

-20 0 20 40 60 80 100 120£ billions

Net assets (reverse repo - repo)

UK-resident deposit-taking banks’ aggregate repo activity at end-2011

• Large part of activity appears to be with foreign banks•Sources: Bank of England and Bank calculations

CEMLA, November 2013

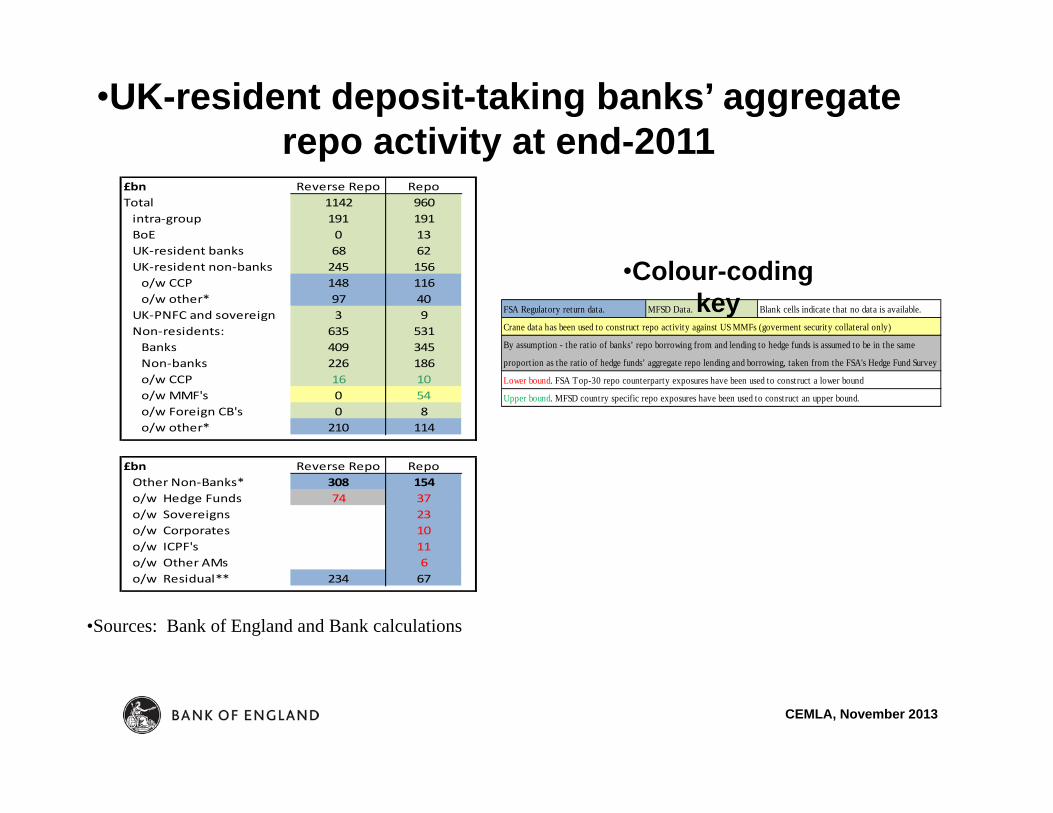

•UK-resident deposit-taking banks’ aggregate repo activity at end-2011

•Sources: Bank of England and Bank calculations

£bn Reverse Repo RepoTotal 1142 960intra‐group 191 191BoE 0 13UK‐resident banks 68 62UK‐resident non‐banks 245 156o/w CCP 148 116o/w other* 97 40

UK‐PNFC and sovereign 3 9Non‐residents: 635 531Banks 409 345Non‐banks 226 186o/w CCP 16 10o/w MMF's 0 54o/w Foreign CB's 0 8o/w other* 210 114

£bn Reverse Repo RepoOther Non‐Banks* 308 154o/w Hedge Funds 74 37o/w Sovereigns 23o/w Corporates 10o/w ICPF's 11o/w Other AMs 6o/w Residual** 234 67

FSA Regulatory return data. MFSD Data. Blank cells indicate that no data is available.

Crane data has been used to construct repo activity against US MMFs (goverment security collateral only)

By assumption - the ratio of banks’ repo borrowing from and lending to hedge funds is assumed to be in the same

Lower bound. FSA Top-30 repo counterparty exposures have been used to construct a lower bound

Upper bound. MFSD country specific repo exposures have been used to construct an upper bound.

proportion as the ratio of hedge funds’ aggregate repo lending and borrowing, taken from the FSA's Hedge Fund Survey

•Colour-coding key

CEMLA, November 2013

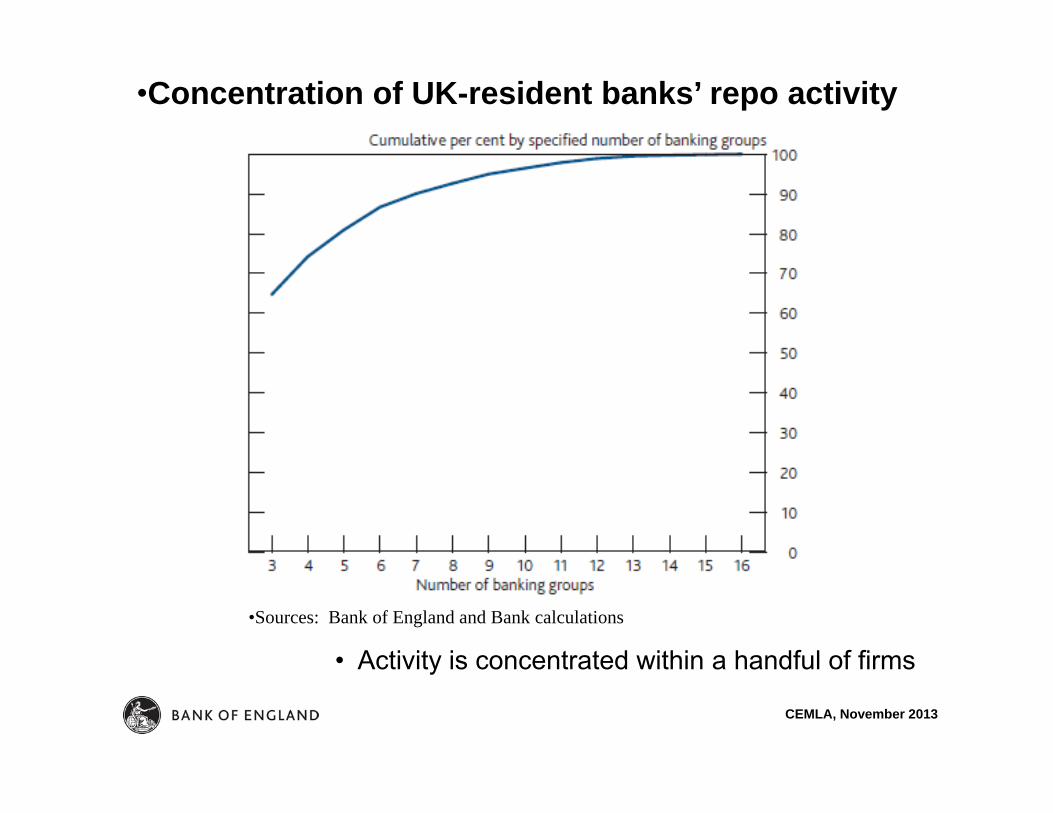

•Concentration of UK-resident banks’ repo activity

• Activity is concentrated within a handful of firms

•Sources: Bank of England and Bank calculations

CEMLA, November 2013

New European Systemic Risk Board data

• ESRB data collection exercise on the re-use of non-cash collateral through securities financing transactions

• Major European banks asked to provide data on the value of collateral received / posted, broken down by counterparty sector and collateral type, as at end-Feb 2013

• Differences versus mapping-exercise data sources:• - Values reflect collateral values (including hair-cuts)• - Data includes Barclays large US matched repo book• - Excludes some large UK-resident subsidiaries (e.g. JPM) and all

UK-resident branches of foreign banks (e.g. DB)

• Despite these differences the stories are broadly similar....

CEMLA, November 2013

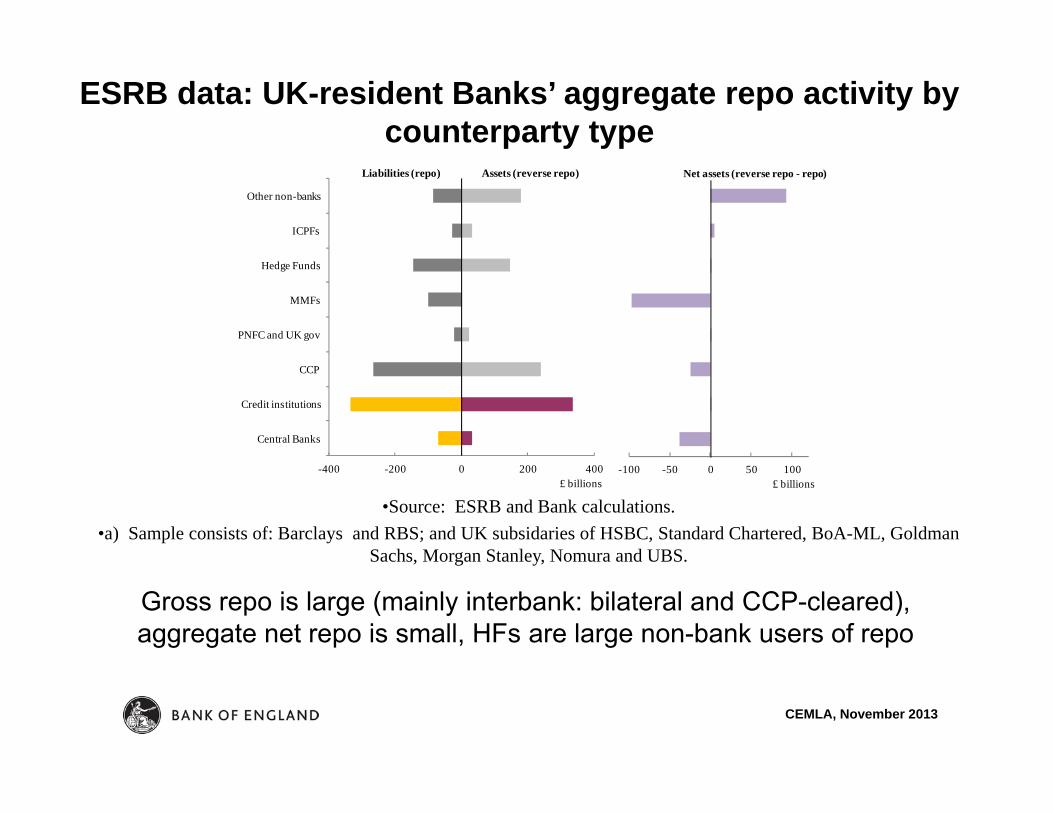

ESRB data: UK-resident Banks’ aggregate repo activity by counterparty type

Gross repo is large (mainly interbank: bilateral and CCP-cleared), aggregate net repo is small, HFs are large non-bank users of repo

-400 -200 0 200 400

Central Banks

Credit institutions

CCP

PNFC and UK gov

MMFs

Hedge Funds

ICPFs

Other non-banks

£ billions

Assets (reverse repo)Liabilities (repo)

-100 -50 0 50 100£ billions

Net assets (reverse repo - repo)

•Source: ESRB and Bank calculations.•a) Sample consists of: Barclays and RBS; and UK subsidaries of HSBC, Standard Chartered, BoA-ML, Goldman

Sachs, Morgan Stanley, Nomura and UBS.

CEMLA, November 2013

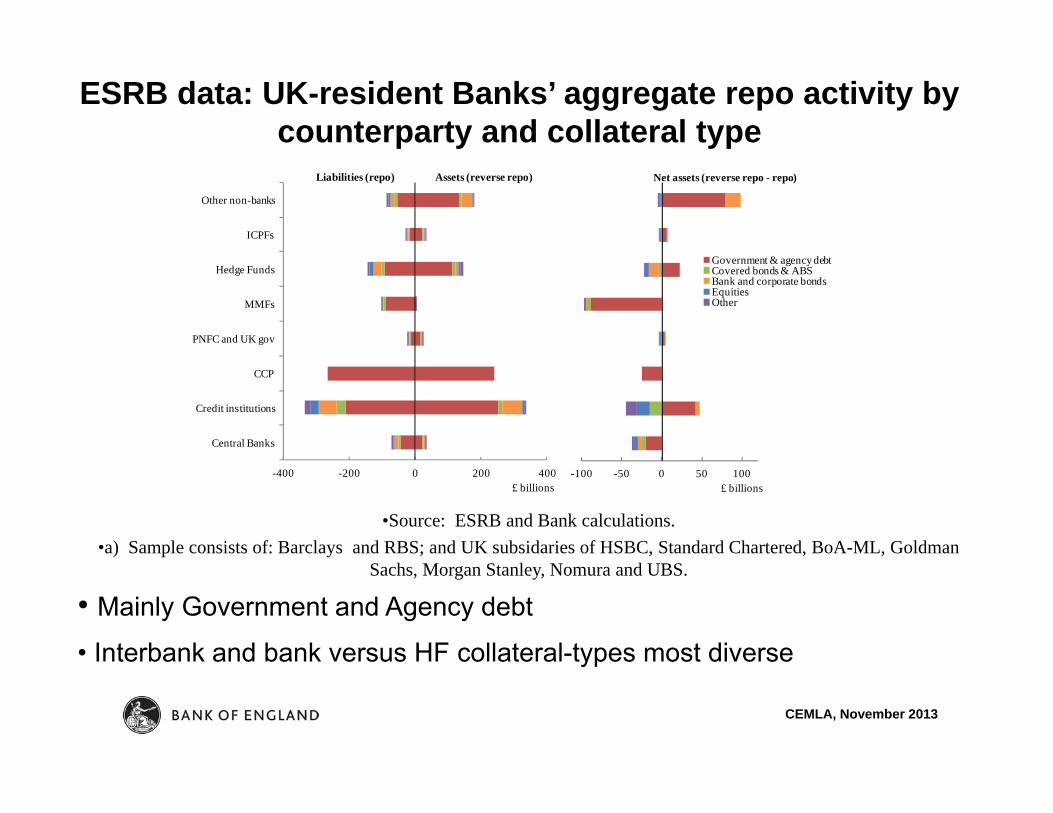

• Mainly Government and Agency debt

• Interbank and bank versus HF collateral-types most diverse

•Source: ESRB and Bank calculations.•a) Sample consists of: Barclays and RBS; and UK subsidaries of HSBC, Standard Chartered, BoA-ML, Goldman

Sachs, Morgan Stanley, Nomura and UBS.

-400 -200 0 200 400

Central Banks

Credit institutions

CCP

PNFC and UK gov

MMFs

Hedge Funds

ICPFs

Other non-banks

£ billions

Assets (reverse repo)Liabilities (repo)

-100 -50 0 50 100

Government & agency debtCovered bonds & ABSBank and corporate bondsEquitiesOther

£ billions

Net assets (reverse repo - repo)

ESRB data: UK-resident Banks’ aggregate repo activity by counterparty and collateral type

CEMLA, November 2013

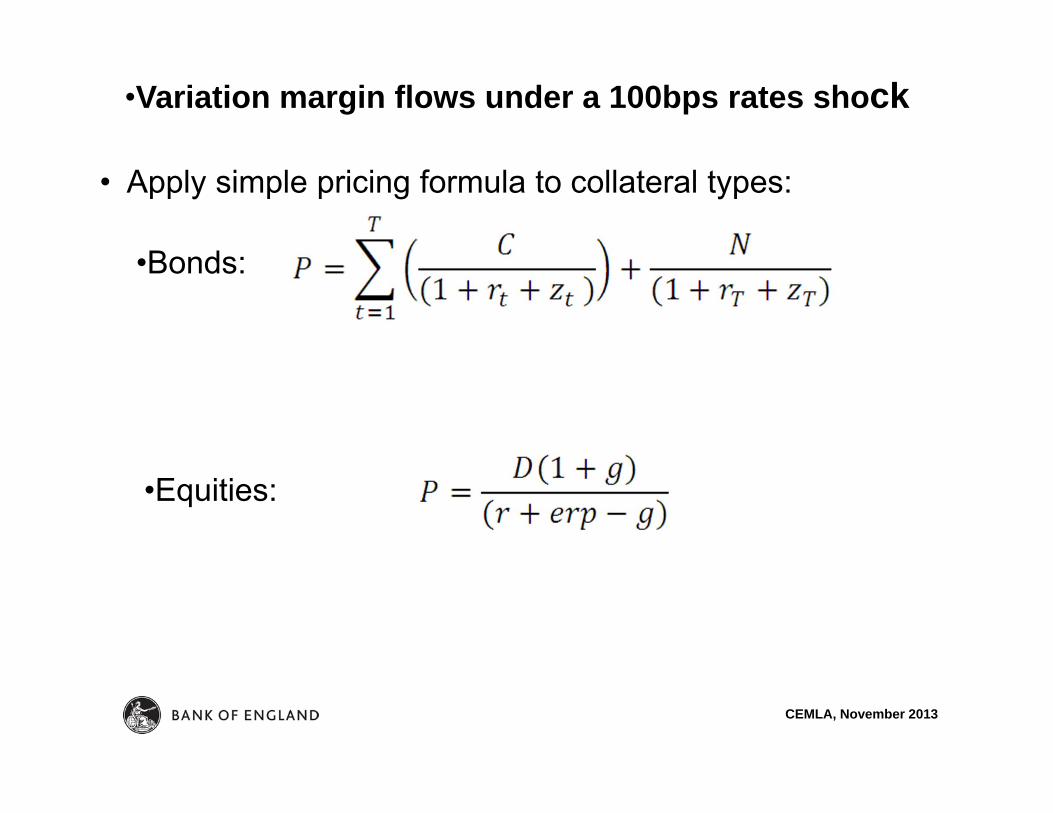

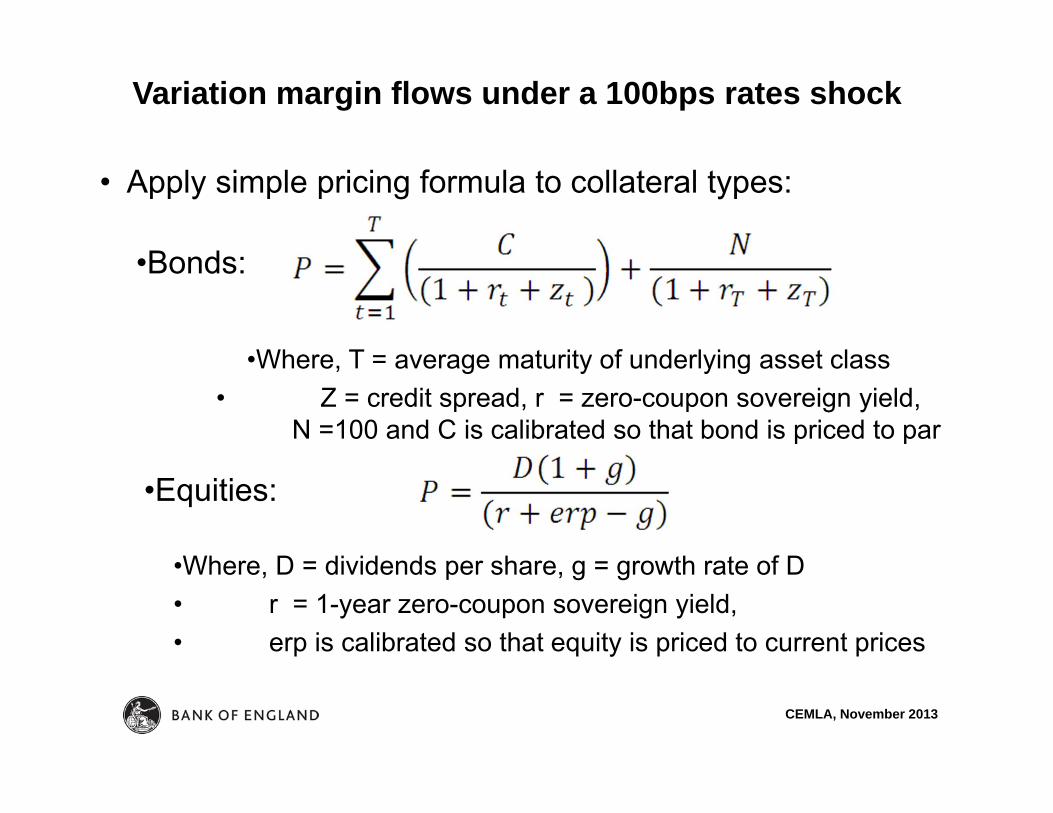

•Variation margin flows under a 100bps rates shock

• Apply simple pricing formula to collateral types:

•Bonds:

•Equities:

CEMLA, November 2013

Variation margin flows under a 100bps rates shock

• Apply simple pricing formula to collateral types:

•Bonds:

•Equities:

•Where, T = average maturity of underlying asset class• Z = credit spread, r = zero-coupon sovereign yield,

N =100 and C is calibrated so that bond is priced to par

•Where, D = dividends per share, g = growth rate of D• r = 1-year zero-coupon sovereign yield,• erp is calibrated so that equity is priced to current prices

CEMLA, November 2013

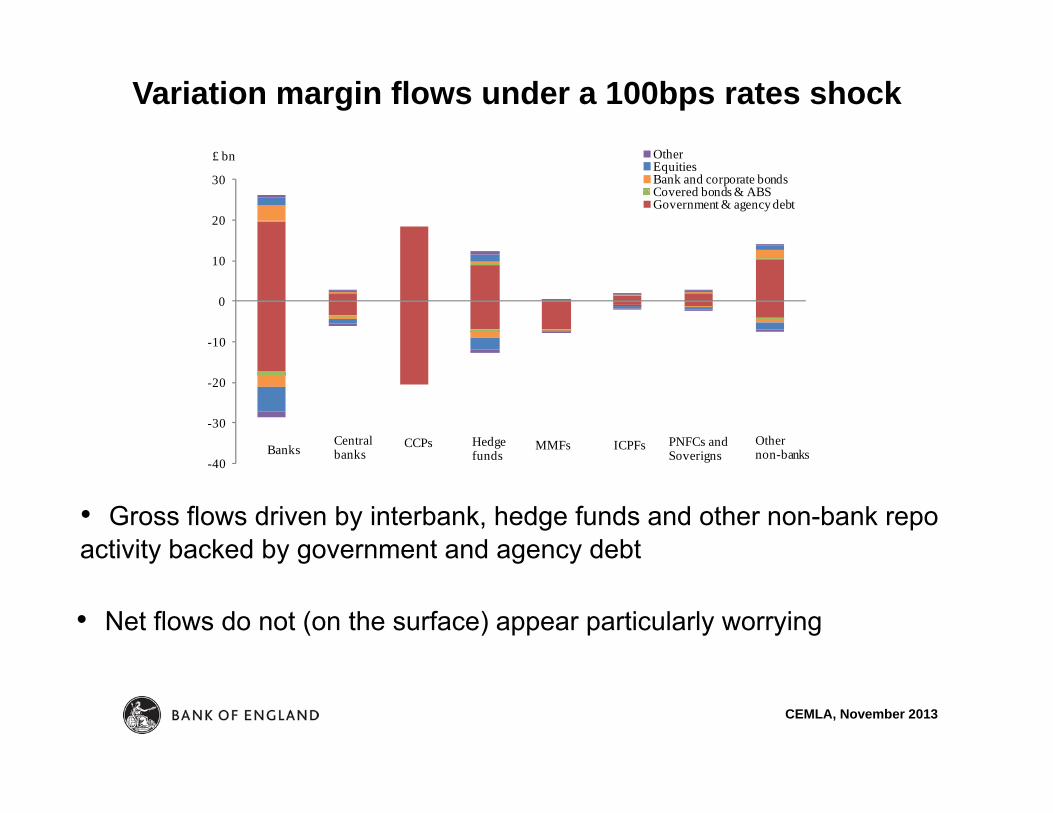

Variation margin flows under a 100bps rates shock

• Gross flows driven by interbank, hedge funds and other non-bank repo activity backed by government and agency debt

-40

-30

-20

-10

0

10

20

30

OtherEquitiesBank and corporate bondsCovered bonds & ABSGovernment & agency debt

BanksCentralbanks

CCPs Hedgefunds

MMFs ICPFs PNFCs and Soverigns

Othernon-banks

£ bn

• Net flows do not (on the surface) appear particularly worrying

CEMLA, November 2013

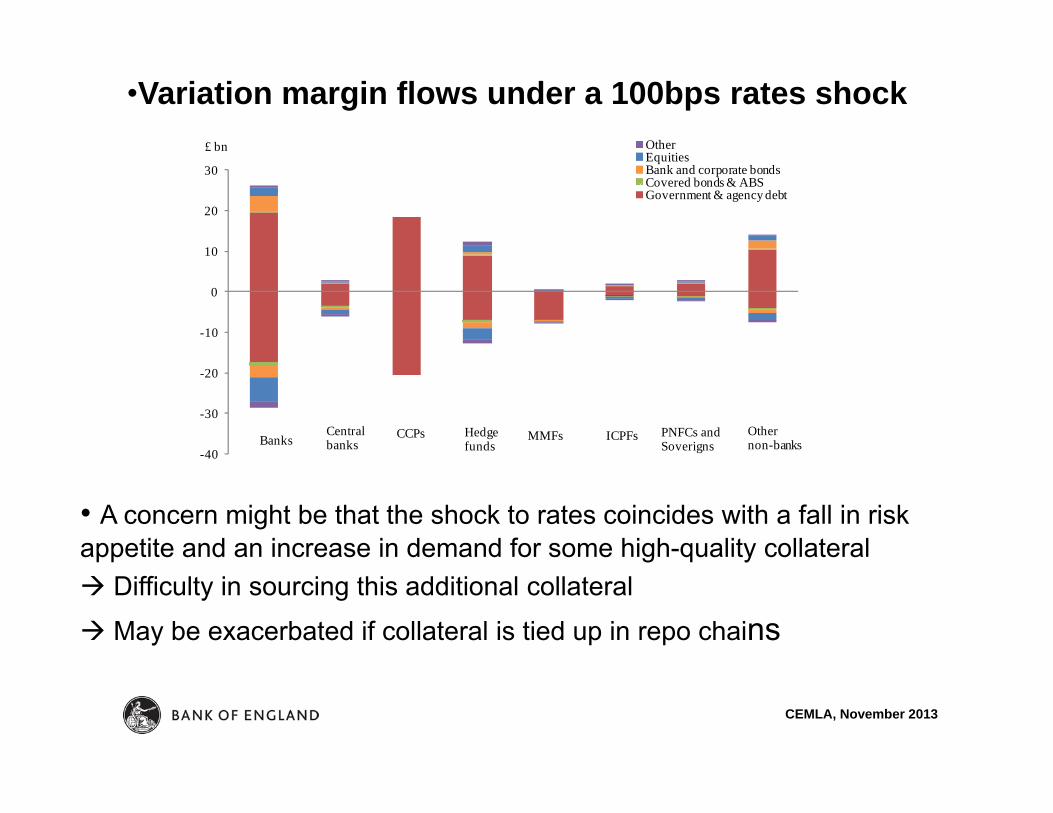

•Variation margin flows under a 100bps rates shock

• A concern might be that the shock to rates coincides with a fall in risk appetite and an increase in demand for some high-quality collateral Difficulty in sourcing this additional collateral

May be exacerbated if collateral is tied up in repo chains

-40

-30

-20

-10

0

10

20

30

OtherEquitiesBank and corporate bondsCovered bonds & ABSGovernment & agency debt

BanksCentralbanks

CCPs Hedgefunds

MMFs ICPFs PNFCs and Soverigns

Othernon-banks

£ bn

CEMLA, November 2013

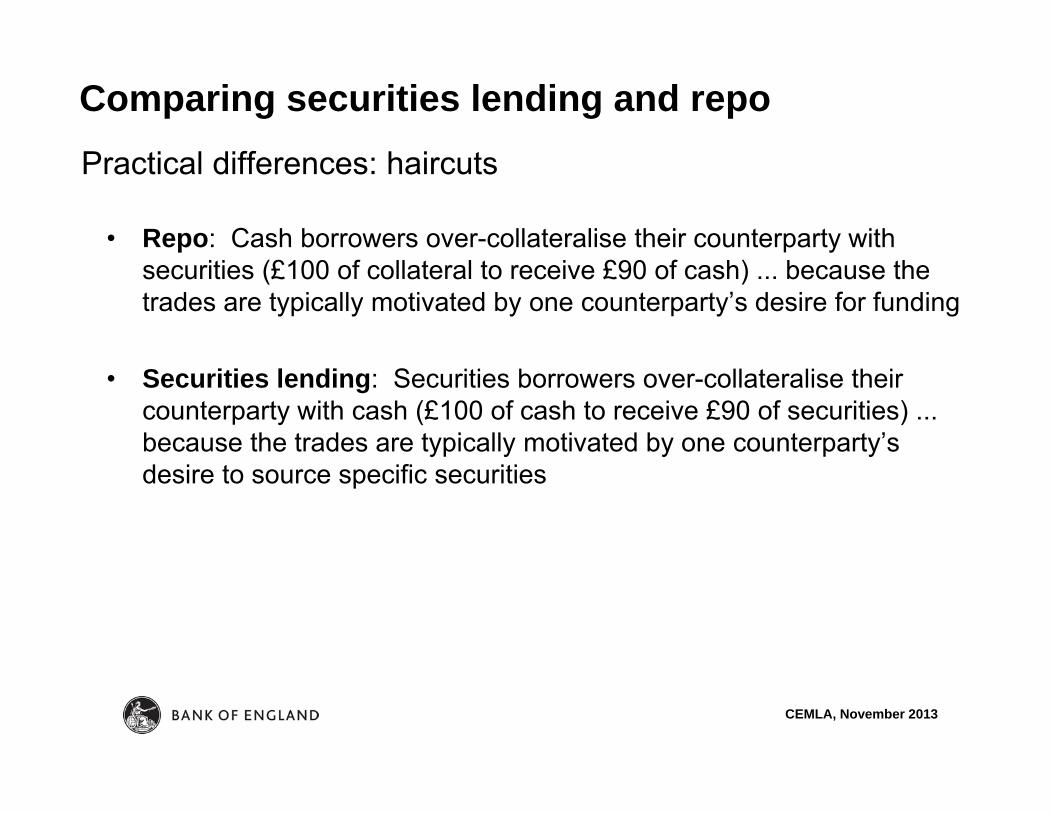

• Repo: Cash borrowers over-collateralise their counterparty with securities (£100 of collateral to receive £90 of cash) ... because the trades are typically motivated by one counterparty’s desire for funding

• Securities lending: Securities borrowers over-collateralise their counterparty with cash (£100 of cash to receive £90 of securities) ... because the trades are typically motivated by one counterparty’s desire to source specific securities

Comparing securities lending and repoPractical differences: haircuts

CEMLA, November 2013

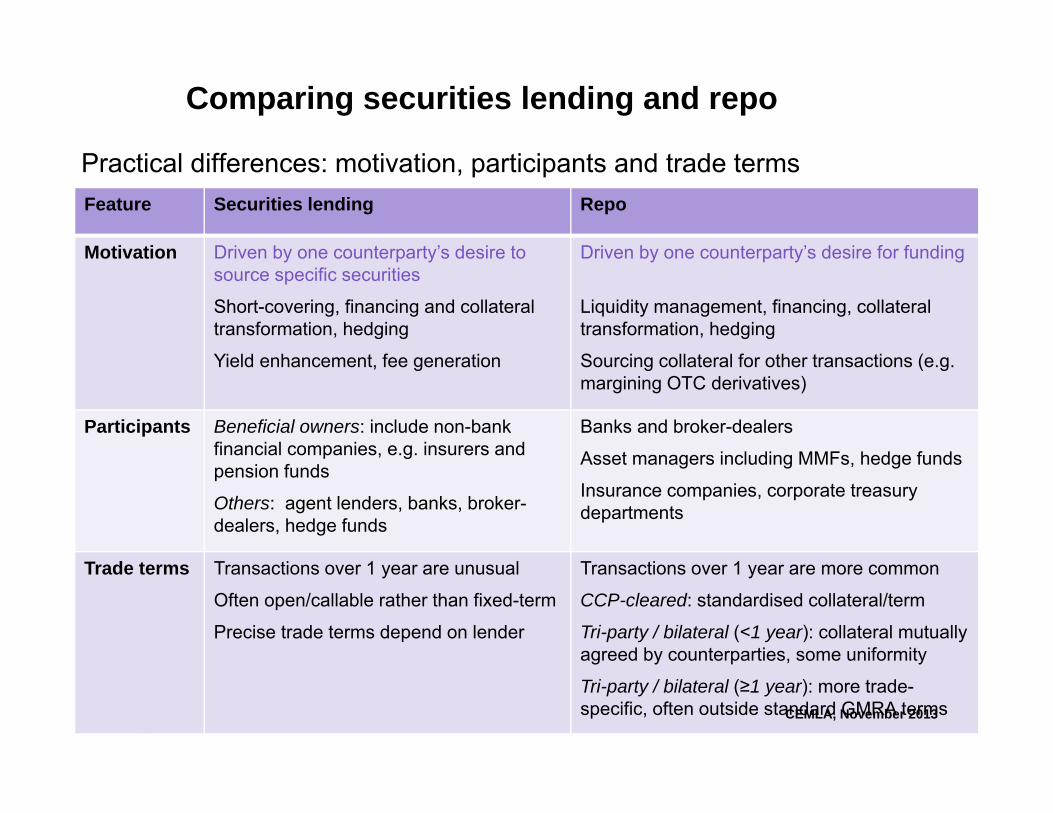

Practical differences: motivation, participants and trade terms

Comparing securities lending and repo

Feature Securities lending Repo

Motivation Driven by one counterparty’s desire to source specific securities

Short-covering, financing and collateral transformation, hedging

Yield enhancement, fee generation

Driven by one counterparty’s desire for funding

Liquidity management, financing, collateral transformation, hedging

Sourcing collateral for other transactions (e.g. margining OTC derivatives)

Participants Beneficial owners: include non-bank financial companies, e.g. insurers and pension funds

Others: agent lenders, banks, broker-dealers, hedge funds

Banks and broker-dealers

Asset managers including MMFs, hedge funds

Insurance companies, corporate treasurydepartments

Trade terms Transactions over 1 year are unusual

Often open/callable rather than fixed-term

Precise trade terms depend on lender

Transactions over 1 year are more common

CCP-cleared: standardised collateral/term

Tri-party / bilateral (<1 year): collateral mutually agreed by counterparties, some uniformity

Tri-party / bilateral (≥1 year): more trade-specific, often outside standard GMRA termsCEMLA, November 2013