Swallowfield plc is a market leader in theswallowfield.com/wp-content/uploads/2017/10/RA2017_… ·...

88

-

Upload

truongcong -

Category

Documents

-

view

217 -

download

3

Transcript of Swallowfield plc is a market leader in theswallowfield.com/wp-content/uploads/2017/10/RA2017_… ·...

FORWARD-LOOKING STATEMENTS Certain statements in this Swallowfield plc Annual Report and Accounts 2017 constitute “forward-looking statements”. Forward-looking statements may sometimes, but not always, be identified by words such as “will”, “may”, “should”, “continue”, “believes”, “expects”, “intends” or similar expressions. These forward-looking statements are subject to risks, uncertainties and other factors which, as a result, could cause Swallowfield plc’s actual future financial condition, performance and results to differ materially from the plans, goals and expectations set out in the forward-looking statements. Such statements are made only as at the date of this Report and, except to the extent legally required, Swallowfield plc undertakes no obligation to revise or update such forward-looking statements.

Swallowfield plc is a market leader in the development, formulation, and supply of

personal care and beauty products.

ANNUAL REPORT & ACCOUNTS 2017

HIGHLIGHTS

STRATEGIC REPORT

GOVERNANCE

FINANCIAL STATEMENTS

04 HIGHLIGHTS

08 CHAIRMAN’S FOREWORD

12 CHIEF EXECUTIVE’S REPORT

24 PRINCIPLE RISKS AND UNCERTAINTIES

26 FINANCIAL REVIEW

32 PEOPLE AND SUSTAINABILITY

36 CORPORATE GOVERNANCE

38 BOARD OF DIRECTORS

40 DIRECTORS’ REPORT

42 INDEPENDENT AUDITOR’S REPORT

48 GROUP STATEMENT OF COMPREHENSIVE INCOME

49 GROUP AND COMPANY STATEMENTS OF FINANCIAL POSITION

51 GROUP AND COMPANY STATEMENTS OF CHANGES IN EQUITY

53 GROUP AND COMPANY CASH FLOW STATEMENTS

54 NOTES TO THE ACCOUNTS

85 FIVE YEAR SUMMARY

86 CORPORATE DIRECTORY

CONTENTS

HIGHLIGHTS ANNUAL REPORT & ACCOUNTS 2017– 4 –

5

5

6

25

4

4

20

3

3

15

2

2

10

1

1

5

0

0

0

-1

-1

-5

FINANCIAL HIGHLIGHTS

# FY2014 Revenue adjusted from 53 weeks to a 52 week basis* Adjusted operating profit and adjusted earnings per share are calculated before exceptional items and amortisation of acquisition-related intangibles** Underlying operating profit is calculated by adding back the charge for share-based payments to adjusted operating profit. This measure was adopted as the charge for share-based payments is a material £1.76m (2016: £0.22m), and is intended to provide a more representative reflection of the trading performance of the Group.

ADJUSTEDOPERATINGPROFIT*(£ MILLION)

UNDERLYINGOPERATINGPROFIT**(£ MILLION)

REVENUE#

(£ MILLION)

ADJUSTEDBASICEARNINGSPER SHARE*(PENCE)

74.3 2016: 54.5

3.9 2016: 1.8

5.6 2016: 2.0

17.7 2016: 12.6

+36%

+115%

+180%

+40%

60

50

40

30

20

10

0 FY2017FY2016

54.5

FY2015

49.4

FY2014#

49.1

FY2013

48.6

70

80

74.3

FY2017FY2016

2.0

FY2015

1.0

FY2014

0.8

FY2013

-0.4

5.6

FY2017

FY2017

FY2016

FY2016

1.8

12.6

FY2015

FY2015

1.0

6.6

FY2014

FY2014

0.8

3.9

FY2013

FY2013

-0.4

-4.7

3.9

17.7

ANNUAL REPORT & ACCOUNTS 2017 HIGHLIGHTS– 5 –

STATUTORYBASICEARNINGSPER SHARE(PENCE)

STATUTORYOPERATINGPROFIT(£ MILLION)

15.2 2016: 17.7

3.3 2016: 2.4

-14%

+38%

FY2017FY2016FY2015FY2014#FY2013

5

20

4

15

3

10

2

5

1

0

0

-5

-1

-10

FY2017FY2016FY2015FY2014FY2013

FY2017

FY2017

FY2016

FY2016

FY2015

FY2015

FY2014

FY2014

FY2013

FY2013

2.41.00.4-0.9

3.3

17.76.61.4-8.0

15.2

TOTALDIVIDENDSPER SHARE(PENCE)

NET DEBT(£ MILLION)

5.2 2016: 3.1

3.6 2016: 4.3

+68%

-16%

6

6

5

5

4

4

3

3

2

2

1

1

0

0

3.1

4.3

2.0

5.45.1

2.2

5.7

5.2

3.6

HIGHLIGHTS ANNUAL REPORT & ACCOUNTS 2017– 6 –

FINANCIALHIGHLIGHTS

• Strong revenue growth of +36% (+8% excluding The Brand Architekts acquisition) to £74.3m (2016: £54.5m). Sterling weakness benefitted the top-line with revenue growth on a constant currency basis of +31% and +2% respectively.

• Owned brands now represent 24% of revenues.

• Underlying operating profit increased by 180% year on year to £5.6m (2016: £2.0m).

• Adjusted EPS increased by 40% year on year to 17.7 pence (2016: 12.6 pence).

• Net Debt of £3.6m (2016: £4.3m), inclusive of £2.0m additional term-loan funding to support The Brand Architekts acquisition.

• Proposed final dividend of 3.5p per share (2016: 2.3p), in addition to the interim dividend of 1.7p already paid, to give a full year dividend of 5.2p (2016: 3.1p), an increase of 68%.

ANNUAL REPORT & ACCOUNTS 2017 HIGHLIGHTS– 7 –

OPERATIONALHIGHLIGHTS

• The Brand Architekts acquisition now successfully integrated, delivering strong year on year growth driven by several successful new product launches across all key customers.

• Original Swallowfield brands also showing strong growth and extending retail distribution.

• Manufacturing business performing robustly underpinned by successful launches for global brand owners and new contract wins.

• Further improvements in % contribution margin achieved by growth of owned brands, drive category focus and cost base optimisation, despite material and components price increases.

• Strong financial performance allowing investment in brand support and organisational capability whilst still delivering significantly improved profitability.

• E-commerce now live across seven brands, supported by increasing digital marketing activity.

ANNUAL REPORT & ACCOUNTS 2017– 8 –CHAIRMAN’S FOREWORD

£m unless otherwise stated 2017 2016

Reported Results

Revenue £74.3m £54.5m

Adjusted revenue (constant currency) 1 £70.9m £54.5m

Underlying operating profit 3 £5.6m £2.0m

Adjusted operating profit 2 £3.9m £1.8m

Adjusted earnings per share 2 17.7p 12.6p

Statutory Results

Revenue £74.3m £54.5m

Operating profit £3.3m £2.4m

Basic earnings per share 15.2p 17.7p

Total Dividend per share 5.2p 3.1p

Net debt £3.6m £4.3m

BRENDAN HYNES, CHAIRMAN | 18th September 2017

I am delighted to be able to report another year of considerable progress for Swallowfield and one in which we have seen real benefits from consistent focus on the elements of our ‘Building a Better Swallowfield’ strategy which we first

put in place in 2014. Sales, profitability, earnings per share and shareholder value have again increased significantly, through a combination of both organic growth and successful acquisition activity.

RESULTS2017

1 Revenue translated at 2016 exchange rates

2 Adjusted operating profit and adjusted earnings per share are calculated before exceptional items and amortisation of acquisition-related intangibles.

3 Underlying operating profit is calculated by adding back the charge for share-based payments to adjusted operating profit. This measure was adopted as the charge for share-based payments is a material £1.76m (2016: £0.22m), and is intended to provide a more representative reflection of the trading performance of the Group.

CHAIRMAN’SFOREWORD

ANNUAL REPORT & ACCOUNTS 2017 – 9 – CHAIRMAN’S FOREWORD

Our business comprises two complementary streams and it is pleasing that both have performed well over the course of the year. Our manufacturing business focusses on the development, formulation, and supply of personal care and beauty products for customers which include many of the world’s leading brands. Through continued investment and execution of our Drive Category Focus, our offering to those customers has become increasingly differentiated, which has the dual benefit of a positive impact on margin contribution and also improving our competitive advantage, thereby making the Group more resilient.

Over the last three years we have developed, both organically and through acquisition, a growing portfolio of brands that are owned and managed by the Group and which we control from formulation through to distribution. The acquisition of The Brand Architekts in June 2016 has significantly accelerated this owned brand segment of our business and brought critical mass to our portfolio. This now represents 24% of Group revenues in the period.

DIVIDEND Further evidence of our confidence in the business can be seen in the Board’s intention to propose a final dividend of 3.5 pence. Together with the interim dividend already paid of 1.7 pence this represents a total dividend for the year of 5.2 pence, an improvement of 68% over the prior year (2016: 3.1p).

It remains the directors’ intention to align future dividend payments to the underlying earnings and cash flow of the business, taking in to account the gearing and the operational requirements of the business. BOARD SUCCESSIONAfter eight successful years as Group Finance Director, Mark Warren has decided to retire from his full-time executive career and therefore will be stepping down from the Board. Mark has played a significant role in helping the business grow and develop over that period and the Board and his colleagues in the business are grateful for his contribution and wish him continued success in the future.

Advanced notice of Mark’s intentions has allowed the Board to engage in a thorough and structured search for his successor and we are pleased to announce that Matthew Gazzard will be succeeding Mark. Matthew has extensive experience in senior financial leadership roles. He served as Group Finance Director for four years at Thatchers Cider during a period of substantial growth for that business where he delivered the financial support required to underpin both the development of the Thatchers brand itself and the company’s manufacturing facilities. Prior to that he spent nine years as both Group Finance Director and ultimately CEO of British Ceramic Tiles where he successfully navigated the business through challenging times and to a merger with Ceramic Prints Ltd.

Matthew will join Swallowfield on 2 October 2017 and work alongside Mark until the end of the calendar year to ensure a smooth and thorough handover. Matthew will formally replace Mark on the Board with effect from 1 January 2018.

OUTLOOK We have delivered another significant improvement in business performance in the year helped by the acquisition of The Brand Architekts and major new product launches in our manufacturing business.

We expect the strong momentum in our branded business to continue, supported by a steady stream of new products, innovation and continued strong support for our brands across our retail customers.

In our manufacturing business, the outlook is solid with a steady flow of new product development (NPD) and new contract wins that will positively impact the year ahead. As indicated previously, this needs to be balanced against the normalisation of volumes on particularly large product launches that bolstered H2 FY16 and H1 FY17 performance.

In line with the industry, both business segments have been challenged by increasing material and packaging costs resulting from the fall in sterling and global inflationary pressures. Our teams have put in place a wide range of programmes to mitigate the impact of these increases and we believe that these measures and our strong overall trading momentum will compensate.

Having successfully integrated The Brand Architekts, we continue to be alert to further acquisition opportunities should they offer the potential to build incremental shareholder value.

Over the course of the year we have strengthened both sides of our business with an improved ability to deliver the innovation, quality and service demanded by our customers. This combined with the progress made on our owned brands, gives us confidence that we are well positioned for the future.

Brendan HynesChairman18 September 2017

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 10 –

STRATEGICREPORT

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 11 –

“It has been a year of excellent progress for the Group with the successful execution of our stated strategy”

CHRIS HOW, CHIEF EXECUTIVE OFFICER

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 12 –

It has been a year of tremendous progress for the Group. Our teams have worked extremely hard to maintain the positive momentum in our manufacturing business and to successfully integrate and accelerate the growth of the acquired The Brand Architekts business. Within The Brand Architekts’ portfolio it is pleasing to report that all major brands and major customers are showing year on year growth and that the pace and quality of new product launches have continued seamlessly. This is a great credit to the team at Teddington who have proved themselves to be as talented, professional and committed as we had hoped at the time of acquisition.

In the manufacturing business, our ability to support our customer base with the innovation, quality and service they require has enabled us to continue to grow sales and contribution margins against strong prior year comparators and the headwinds of significant raw material and packaging inflation. Our reputation and relationship has been enhanced across several key customers, both longstanding and new, as we have successfully supported a number of critical product launches for them which contributes to current business performance and augurs well for future projects.

CHIEF EXECUTIVE’SREPORT

OUR BUSINESS AND STRATEGY

WHAT WE DO

MANUFACTURING

Swallowfield plc is a market leader in the development, formulation, and supply of personal care and beauty products, including its own portfolio of brands.

Our business strategy is to leverage our Group expertise, resources and assets across two complimentary and connected value streams, owned brands and manufacturing. Within each value stream we have three strategic pillars which we believe are the critical focus areas to ensure we continue to grow these businesses in the medium and long term.

Our manufacturing business focusses on the development, formulation, and supply of personal care and beauty products for customers which include many of the world’s leading brands. Through continued investment and execution of our Drive Category Focus, our offering to those customers

has become increasingly differentiated, which has the dual benefit of a positive impact on margin contribution and also improving our competitive advantage, thereby making the Group more resilient.

SWALLOWFIELD EXPERTISE AND RESOURCES

MANUFACTURINGVALUE STREAM

• innovation, quality, service, to global brand owners

• drive category focus

• cost base optimisation

OWNED BRANDSVALUE STREAM

• new product development - at pace, consumer and customer relevant

• leverage swallowfield resources

• international growth

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 13 –

Prestige Brands

27%

OUR MANUFACTURING CUSTOMERS AND MARKETSFigure 1 outlines the range of customer types we supply in our manufacturing business. We are proud to work with some of the world’s leading brands and retailers.

Our manufacturing business invoiced 57% of sales to customers in the United Kingdom, 39% to those in Europe and 4% in Rest of World. With a number of customers onward exporting globally. Swallowfield produced products will be found in many markets around the world.

OUR PRODUCTSFigure 2 outlines the current sales value mix of product types for our Manufacturing business.

Beauty/FashionRetailers

32%

Beauty/FashionRetailers

36%

Prestige Brands

29%

Mass Brands

32%Mass Brands

29%

7% GroceryRetailers 8% Grocery

Retailers

Hot Pour Hot Pour

Premium Liquids, Tubes

Roll-ons

Premium Liquids, Tubes

Roll-ons

Figure 1BY CUSTOMER TYPE FY2017

Figure 1BY CUSTOMER TYPE FY2016

Figure 2BY PRODUCT TYPE FY2017

Figure 2BY PRODUCT TYPE FY2016

Personal CareAerosols

54%

Personal CareAerosols

56%

Fragrance& Gifting

15%

Fragrance& Gifting

17%

6% 6%

7% 7%

Colour Cosmetics& Pencils

18%

Colour Cosmetics& Pencils

14%

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 14 –

InnovationOur talented chemists have an industry-wide reputation for developing great new product formulations, especially in our Drive product categories. Packaging SolutionsOur team works across our customer base to design innovative and effective packaging solutions. Regulatory ExpertiseOur team are able to advise customers on regulatory requirements across a broad range of product types and across a variety of geographies thereby enhancing the potential of these products in export markets.

Quality Customer BaseThe vast majority of our products are developed and produced for strong brands or more premium beauty and fashion retailers.

Expertise In Our “Drive” CategoriesWe have an industry reputation for quality, expertise and cost competitiveness in our drive categories (e.g. Aerosols, Hot Pour Products). These product categories also have significant barriers to entry in terms of skill and assets required.

Geographic FlexibilityOur ability to fill and pack products in the UK, Central Europe and Asia enable us to tailor our offer to meet a variety of customer needs around, cost, quality, complexity and lead-times. Formulatory ExpertiseThe majority of our sales are from formulations that we have either developed ourselves or jointly with our customers. This enables our relationships and specific contracts to be on a more secure, long term partnership basis.

OUR COMPETITIVE STRENGTH

FORMULATORYEXPERTISE

RegulatoryExpertise

PackagingSolutions

Innovation

GeographicalFlexibility

QualityCustomer

Base

Expertise inour ‘Drive’Categories

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 15 –

Over the last three years we have developed, both organically and through acquisition, a growing portfolio of brands that are owned and managed by the Group and which we control from formulation through to distribution. The acquisition of The Brand Architekts in June 2016 has significantly accelerated this owned brand pillar and brought critical mass to our portfolio, now representing 24% of Group revenues in the period.

The convergence of a number of macro trends has created a significant and demonstrable opportunity for smaller more agile companies to create and profitably grow well-crafted and well positioned brands in the Personal Care and Beauty sector. National retailers are keen to support brands that can differentiate their offering and thereby drive shopper loyalty. Digital channels and social media allow brands to deliver

well targeted, fast and flexible consumer communication campaigns at a fraction of the cost of traditional media. Smaller companies are able to identify trends and develop new products without the time consuming and complex decision-making processes that can often be a feature of larger global companies.

Bringing together the product development, production and supply chain expertise of Swallowfield with the proven, creative and dynamic brand management team of The Brand Architekts creates a strong and broad capability within the group to profitably realise market opportunities through development of our owned brand portfolio.

OWNED BRANDS

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 16 –

OUR OWNED BRANDS CUSTOMERS AND MARKETSFigure 3 outlines the range of customer types we supply in our owned brands business.

Figure 3BRAND SALES BY CHANNEL FY17

UK Grocery Retail

57%International

24%

UK Non-Food Retail

19%

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 17 –

OUR LOCATIONS

UKWELLINGTON, SOMERSETFACTORY AND GROUP HQOur head office and a manufacturing and development location, predominately focused on aerosol and hot pour deodorant sticks.

BIDEFORD, NORTH DEVONFACTORYManufacturing and development location focused on cosmetic wood pencils and small hot pour lip balms and plastic pencils.

TEDDINGTON, MIDDLESEXTHE BRAND ARCHITEKTS The base of The Brand Architekts, a proven and experienced team.

FRANCEPARISSALES OFFICESales support office, located close to our customers.

CHINASHANGHAIFACTORY A local representative office and location of our 19% investment in Shanghai Colour Cosmetic Technology Company (SCCTC). SCCTC are focused on gift packs and cosmetics.

CZECH REPUBLICTABORFACTORYA filling location focused on cosmetics, fragrance, tubes and roll-ons.

USANEW YORKSALES OFFICESales support office, located close to our customers.

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 18 –

‘CREATING FOR TOMORROW,DELIVERING FOR TODAY’

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 19 –

“Fast paced new product development that quickly identifies and responds to market trends is a core element of our success”

JANE FLETCHER, GROUP SALES AND MARKETING DIRECTOR

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 20 –

Our business strategy is developed on two complimentary platforms:

• the first ‘Creating for Tomorrow’ identifies within each of the manufacturing and owned brands value streams the three strategic pillars which we believe are the critical focus areas to ensure we continue to grow these businesses in the medium and long term.

• the second ‘Delivering for Today’ identifies some key operational focus areas that we need to drive in order to deliver our more immediate (i.e. current fiscal) performance.

EXECUTING OURSTRATEGY

The three strategic pillars that we are focussing on within our owned brands value stream are:

NEW PRODUCT DEVELOPMENT (NPD)Fast paced NPD that quickly identifies and responds to market trends is a core element of The Brand Architekts business model. We are pleased that this responsiveness continues as part of the Swallowfield Group and that retailer appetite remains high. 78 new lines were launched in the course of the financial year across 11 different brands. Of particular note are a range of new beauty accessories launched under a new brand ‘Beautopia’, a new line of Epsom Salts under the Dr.Salts brand, and a new Retinol Serum in our SuperFacialist range. We are busy on further new ranges to be launched in Autumn 2017.

Progress has also continued on our original Swallowfield brands. The Real Shaving Company has grown strongly in the year thanks in part to the good performance of a new gift range but also the effect of digital marketing activity linked to the sponsorship of Somerset T20 cricket. The Bagsy Savannah Miller collection was launched in the year and has helped us to find new distribution opportunities for the brand. MR, our premium male hair loss brand has seen rate of sale increase even further with the introduction of new packaging for the shampoo, conditioner and styling paste lines and continued innovative and impactful digital marketing activity.

We have also seen very good growth in our range of value brands, such as Tru Shave, aimed at the growing UK value retail sector. We have successfully added new products to our offering and in doing so have extended the number of retail customers to virtually all the major national UK chains in this channel.

On 4 September 2017, we concluded a transaction to acquire a 70% shareholding in Sterling Shave Club Ltd. Over the last two years Sterling has established a presence in the fast-growing on-line subscription shave club sector.

The business is currently at a relatively small scale and our investment is appropriately modest. The entire consideration is to be invested into the business to support a significantly enhanced marketing plan directed at accelerating membership recruitment and expanding the range of products available beyond the current range of blades and shaving products, which currently include our own The Real Shaving Company range.

It offers us the opportunity to further develop our knowledge and capabilities in e-commerce which we believe will be critical to the further development of our owned brands business in the years ahead.

As the business will very much be in an ‘invest to grow’ phase, we expect a broadly neutral impact on group profitability in the current financial year moving to a positive contribution in subsequent years.

OWNED BRANDS

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 21 –

LEVERAGE SWALLOWFIELD RESOURCESAt the time of acquisition of The Brand Architekts, we identified a number of opportunities to either drive revenue growth or create savings by leveraging the existing resources and capabilities of the parent business. We are pleased to have made excellent progress in this regard through the course of the year.

Several Swallowfield developed and produced products are now on shelf including Dirty Works Body Sprays and Happy Naturals footcare products. Many more projects are in progress covering not only new products but also the transfer of some existing products from other suppliers.

Swallowfield had, prior to the acquisition, developed a very competent digital marketing and e-commerce capability and we have been able to utilise these resources to launch digital marketing programmes and e-commerce functionality across Dirty Works, SuperFacialist, Quick Fix Facials, and Kind Natured.

PR and Marketing agencies were consolidated across the portfolio in the course of the year which has led to better quality output at lower cost.

On the Supply side, we are leveraging our materials and packaging sourcing network (including our China purchasing office), our knowledge of best practice production processes, and our expertise in product design and formulation to drive cost improvements across the inherited The Brand Architekts supply base. As part of this programme we have secured significant savings in freight and duty on shipments of gifts and accessories from China by combining our expertise and our buying power.

INTERNATIONAL EXPANSIONGrowth in international revenues has been strong, led in particular by export sales to North America. Across the full portfolio of our brands, international sales now account for 24% of segment sales and we are investing to grow this further still. We have put in place dedicated resource to grow this area and are pleased in the course of the year to have opened new distribution channels for a number of our brands in France, Netherlands, Austria and Chile. Additionally, we are extending the international reach of our Christmas gifting ranges with orders already having been received for USA, Turkey, Ireland and South Africa.

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 22 –

We have continued to make measurable progress across our three strategic pillars in this segment of our business.

INNOVATIONOur manufacturing business relies on our ability to bring innovative new products to our customer base which consists of some of the leading global brand owners and retailers in the Personal Care and Beauty sector. In the financial year, we introduced over 200 Swallowfield developed new products, a level of innovation activity that compares favourably to prior year. We were particularly active in haircare and colour cosmetic products with a number of our innovations being taken to market by leading brands. Volumes on our innovative plastic aerosol products continued to grow in the period and during the year we have progressed projects which we expect will lead to the technology being introduced by other customers in the new financial year.

DRIVE CATEGORY FOCUSIn the reporting period, we have seen particularly strong growth in Personal Care Aerosols, Cosmetic Pencils, and Premium Liquids. In each case, recently won contracts to support new product launches have been a major contributor, underlining our position as a reliable partner for major global brand owners. The success of our partnership with a major European cosmetics company has supported a project to increase wood pencil capacity and improve cost efficiency at our Bideford site to meet growing demand. Further improvements in capacity and capability have been completed at our Wellington site with particular focus on Personal Care aerosols and Hot Pour products which enabled us to both extend existing contracts and win new ones.

COST BASE OPTIMISATIONEnergy saving improvements continue at the Wellington site and line efficiency programmes continue to contribute to margin improvement across all sites. The investment in pencil automation in Bideford decreases cost per unit and increases capacity. The flexibility of our site footprint has enabled us to accommodate the needs of a major customer who needed to transfer sourcing from a dollar denominated supply chain out of China to a euro-denominated supply chain.

The first wave of products were produced for The Brand Architekts brands in this financial year. This will now be accelerated with significant volumes brought in-house over the next 18 months.

MANUFACTURING

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 23 –

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 24 –

The Group operates in an environment that is constantly changing and as a result the risks it is facing will change over time. The Group’s management processes assess risks and then develop strategies for dealing with these risks on an ongoing basis. A formal review of these risks is carried out by the Group twice a year. The review process involves the classification of risks, assessment to determine the relative likelihood of them impacting the business and the potential severity of the impact, and determination of whether changes to management processes are needed to manage them effectively. COMPETITIVE ENVIRONMENT AND CUSTOMER REQUIREMENTS The market remains competitive, and the Group therefore has exposure to loss of contracts and/or slow-down in demand for products.

The focus on the six strategic pillars of ‘creating for tomorrow’ outlined earlier in this report are a key part of the risk management process associated with this specific risk. Within the manufacturing business, the drive category focus, product innovation, and cost base optimisation pillars, all help to strengthen customer relations and position the Group as a strong partner, supporting customers’ key needs of innovation, quality, cost efficiency and service. The development of our owned brands adds a further level of diversification to managing this risk, and now represents 24% of Group sales.

PRODUCT QUALITY Product quality is a key strength of the Group and failure to maintain a high standard of quality and safety would have a severe impact on service levels, customer relationships, and have financial repercussions.

We have formalised development protocols to ensure the products we design are safe, fit for purpose and comply with all legal requirements, working with our suppliers to prepare detailed product, component and material specifications and ensure correct materials are chosen and specified, and that the products are clearly labelled for any markets in which they are sold.

The Group’s quality assurance procedures are reviewed continuously with improvements made as appropriate. The Group is subject to frequent internal and external safety, environmental, and quality audits covering both accreditations held and our customers required operating standards.

RISKS ANDUNCERTAINTIES

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 25 –

LABOUR COSTS, PRICES AND SUPPLY The Group, along with other businesses, will face the risk of inflationary pressures through commodities cost increases, further driven by currency weakness post Brexit, the National Living Wage, and other ongoing legislative changes.

The Group in the normal course of its business, transacts in and holds various currencies, and follows a policy of managing currency exposure through natural hedging wherever possible.

The Group maintains a high level of expertise in its purchasing and supply chain team. The team seeks to cultivate strong relationships with major suppliers to ensure continuity of supply at competitive prices.

The regular renovation and innovation across our products can help to manage margin pressures in an effective manner, as far as the competitive environment allows.

Ongoing capital investment and improvements in operational efficiency help reduce the impacts of inflation.

ECONOMIC ENVIRONMENT The market place remains challenging and there is an uncertain macro-economic outlook following the vote to leave the EU. Our focus on executing our clear strategy, outlined earlier in this report, has improved our ability to deliver the innovation, quality and service requirements of our manufacturing business customers, which, alongside the progress made on our owned brands, both developed internally and through acquisition, leaves us well placed to navigate any potential macro uncertainty.

CYBER SECURITYThe Group, along with other businesses, is exposed to the risk of increasingly sophisticated cyber-attacks aimed at causing business disruption, capture of data for financial gain, general embarrassment and reputational damage, or that the Groups’ data privacy protective measures are considered by regulators to be inadequate. PENSION FUND DEFICIT The revaluation of the one defined benefit pension scheme on a technical provision basis at each reporting date can cause large fluctuations in valuations based on factors outside the Groups control. There is an agreed deficit recovery plan fixed until July 2025 or until a new schedule is agreed based on the next triennial valuation which will be at 5 April 2017. This deficit recovery plan provides certainty over cash flows between triennial reviews. The Group maintains a close relationship and regular communication with the Trustees.

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 26 –

FINANCIALREVIEW

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 27 –

“The overall re-shaping of the business towards stronger growth and margins has enabled us to deliver a close to three-fold increase in underlying operating profit.”

MARK WARREN, GROUP FINANCE DIRECTOR

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 28 –

£m unless otherwise stated 2017 2016

Reported Results

Revenue £74.3m £54.5m

Adjusted revenue (constant currency) 1 £70.9m £54.5m

Contribution Margin % 32.2% 31.9%

Underlying operating Profit 3 £5.6m £2.0m

Adjusted operating profit 2 £3.9m £1.8m

Adjusted earnings per share 2 17.7p 12.6p

Statutory Results

Revenue £74.3m £54.5m

Operating profit £3.3m £2.4m

Basic earnings per share 15.2p 17.7p

Total Dividend per share 5.2p 3.1p

Net debt £3.6m £4.3m

KEY PERFORMANCE INDICATORS To implement our growth strategy effectively, we have set ambitious targets and milestones. We monitor these goals closely to focus our effort and ensure we deliver both in the short term and long term.

A summary of the financial measures used are:

FINANCIALREVIEW

RESULTS2017

1 Revenue translated at 2016 exchange rates

2 Adjusted operating profit and adjusted earnings per share are calculated before exceptional items and amortisation of acquisition-related intangibles.

3 Underlying operating profit is calculated by adding back the charge for share-based payments to adjusted operating profit. This measure was adopted as the charge for share-based payments is a material £1.76m (2016: £0.22m), and is intended to provide a more representative reflection of the trading performance of the Group.

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 29 –

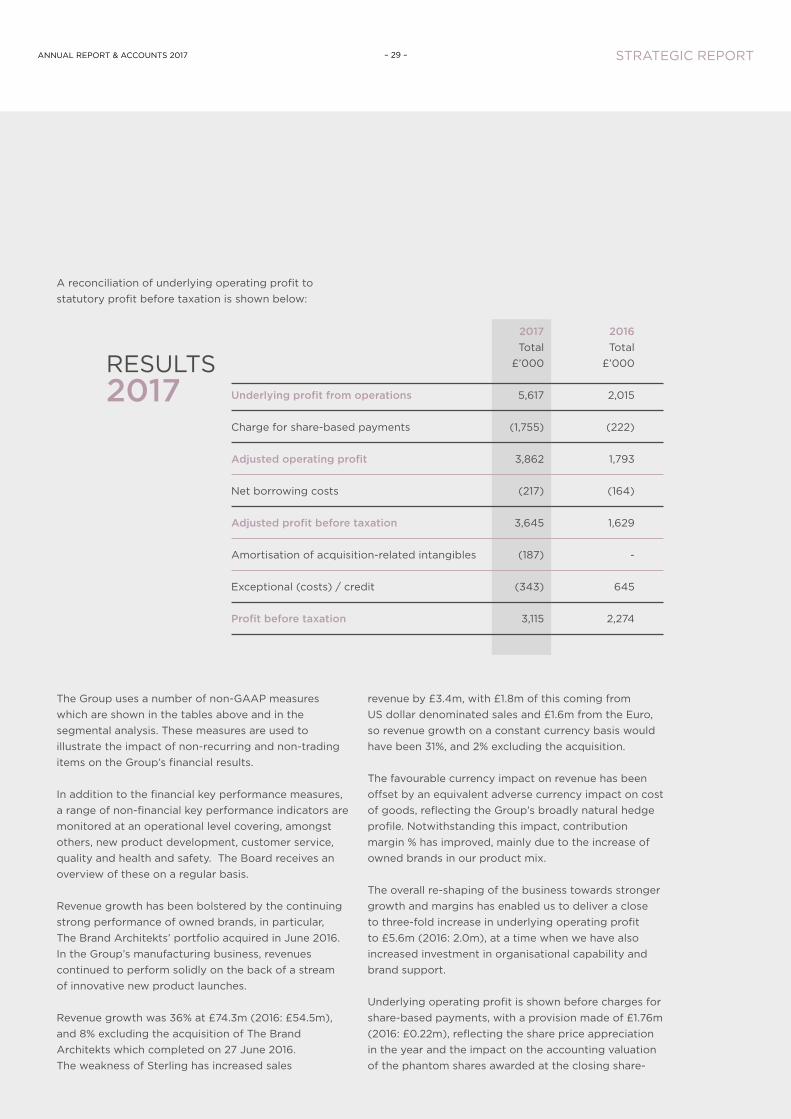

2017 2016 Total Total £’000 £’000

Underlying profit from operations 5,617 2,015

Charge for share-based payments (1,755) (222)

Adjusted operating profit 3,862 1,793

Net borrowing costs (217) (164)

Adjusted profit before taxation 3,645 1,629

Amortisation of acquisition-related intangibles (187) -

Exceptional (costs) / credit (343) 645

Profit before taxation 3,115 2,274

RESULTS2017

A reconciliation of underlying operating profit to statutory profit before taxation is shown below:

The Group uses a number of non-GAAP measures which are shown in the tables above and in the segmental analysis. These measures are used to illustrate the impact of non-recurring and non-trading items on the Group’s financial results.

In addition to the financial key performance measures, a range of non-financial key performance indicators are monitored at an operational level covering, amongst others, new product development, customer service, quality and health and safety. The Board receives an overview of these on a regular basis.

Revenue growth has been bolstered by the continuing strong performance of owned brands, in particular, The Brand Architekts’ portfolio acquired in June 2016. In the Group’s manufacturing business, revenues continued to perform solidly on the back of a stream of innovative new product launches.

Revenue growth was 36% at £74.3m (2016: £54.5m), and 8% excluding the acquisition of The Brand Architekts which completed on 27 June 2016. The weakness of Sterling has increased sales

revenue by £3.4m, with £1.8m of this coming from US dollar denominated sales and £1.6m from the Euro, so revenue growth on a constant currency basis would have been 31%, and 2% excluding the acquisition.

The favourable currency impact on revenue has been offset by an equivalent adverse currency impact on cost of goods, reflecting the Group’s broadly natural hedge profile. Notwithstanding this impact, contribution margin % has improved, mainly due to the increase of owned brands in our product mix.

The overall re-shaping of the business towards stronger growth and margins has enabled us to deliver a close to three-fold increase in underlying operating profit to £5.6m (2016: 2.0m), at a time when we have also increased investment in organisational capability and brand support.

Underlying operating profit is shown before charges for share-based payments, with a provision made of £1.76m (2016: £0.22m), reflecting the share price appreciation in the year and the impact on the accounting valuation of the phantom shares awarded at the closing share-

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 30 –

price of 395p (2016: 180p). The majority of the charge on share-based incentives relates to awards made in 2014 and become exercisable towards the end of 2017. These share options were put in place in order to incentivise the Group’s wider management team (including the executive directors of Swallowfield) and to ensure that their interests are aligned with shareholders. At the time, this incentive plan was introduced the average share price was 95p and since that time shareholders have been rewarded with a capital improvement of over 250% in addition to progressive dividend income.

The net effect is that the Group made an adjusted operating profit of £3.9m (2016: £1.8m). Adjusted profit before tax increased to £3.6m (2016: £1.6m).

The exceptional item of £0.34m in the current period relates to “one off” costs incurred in the acquisition of The Brand Architekts Ltd. In 2016 there was an exceptional credit of £0.65m relating to the closure to future accrual of the defined benefit pension scheme.

The overall effective rate of Group taxation for the period was 17.4% (2016: 12.0%) of pre-tax profits. The prior year benefitted from brought-forward UK tax losses which were fully utilised in the last financial year. The current year tax charge reflects standard UK and the Czech Republic rates of taxation.

This results in adjusted earnings per share of 17.7p (2016: 12.7p).

The Group’s strategic investment of a 19% shareholding in Shanghai Colour Cosmetics Technology Company Limited (SCCTC) was further re-valued upwards by £0.68m during the period, to fair value based on SCCTC’s June 2017 net assets. The initial cost of this investment was £0.14m and this is now valued at £1.24m. This improved valuation reflects a very strong trading performance, supplying customers in Europe and the USA. In addition, a dividend of £0.1m was received in the year (2016: £0.06m).

NET DEBT AND CASH FLOWNet debt decreased to £3.6m (2016: £4.3m). This includes an additional £2m five-year term loan facility taken out to support the acquisition of The Brand Architekts Ltd. The Group maintains a broadly natural hedge position on the Euro and US Dollar, and manages timing differences through a multi-currency invoice finance facility. At the reporting date, the Group was maintaining a hedged position by holding Euro and US Dollar cash balances, whilst drawing on its GBP facility, resulting in an increased cash position in the statement of financial position of £4.1m (2016: £0.8m) whilst retaining an overall net debt position of £3.6m (2016: £4.3m), note 24 provides an analysis of net debt.

The movement in the components of working capital reflect the impact of the four major product launches in our manufacturing business across the prior June year-end, plus the inclusion of The Brand Architekts working capital components in the closing position.

The increase in tax paid reflects the payment of The Brand Architekts prior-year corporation tax, and the re-introduction of quarterly instalments across the enlarged Group.

Financing costs of £0.31m (2016: £0.22m) comprised interest expense of £0.16m (2016: £0.13m) plus a pension scheme notional finance charge of £0.15m (2016: charge £0.08m).

Capital expenditure was £1.4m which was broadly in line with depreciation. We have made a number of investments to improve line efficiencies and support incremental new customer contracts and have an active capital investment programme planned for the new year.

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 31 –

DEFINED BENEFIT PENSION SCHEMEThe defined benefit pension scheme underwent its last triennial valuation as of 5 April 2014. The deficit on a statutory funding basis was £1.3m and the Group entered into a revised deficit recovery plan and schedule of contributions in July 2015. The deficit reduction payment will be £108k per annum (previously £111.5k per annum) for ten years. The scheme was subsequently closed to future accrual with effect from 31 December 2015. The latest triennial valuation at April 2017 is in process, and it is expected will be finalised during year-ending June 2018.

For accounting purposes at 24 June 2017, the Group recognised under IAS19 ‘employee benefits’, a deficit of £6.1m (25 June 2016: £4.5m). The Accounting Standards require the discount rate to be based on yields on high quality (usually AA-rated) corporate bonds of appropriate currency, taking into account the term of the relevant pension scheme’s liabilities. Corporate bond indices are used as a proxy to determine the discount rate. At the reporting date, the yields on bonds of all types were lower than they were at 25 June 2016. This has resulted in lower discount rates being adopted for accounting purposes compared to last year, which has been coupled with an increase in expectations of long term inflation, with the combination materially increasing the fair value of the scheme liabilities, with the strong investment return performance only partially mitigating. This has translated into an increased liability under the IAS19 methodology.

DIVIDENDSThe Board is pleased to announce that it will be proposing a final dividend of 3.5 pence. Together with the interim dividend already paid of 1.7 pence this represents a total dividend for the year of 5.2 pence, an improvement of 68% over the prior year (2016: 3.1p). If approved, the final dividend will be paid on 8 December 2017 to shareholders on the register on 17 November 2017. The shares will be marked as ex-dividend on 16 November 2017.

GOING CONCERNAs part of its normal business practice, the Group prepares annual and longer-term plans and, in reviewing this information the Directors have a reasonable expectation that the Company and Group have adequate resources to continue in operational existence for the foreseeable future. Accordingly, we continue to adopt the going concern basis in preparing the annual report and accounts.

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 32 –

EMPLOYMENT PRACTICES The success of our business is dependent upon the quality, commitment and behaviour of our employees. Therefore, the Group provides clear policies and direction to our employees and strives for the highest standards of behaviour.

The ‘Building a Better Swallowfield’ agenda outlines the key elements of how we want to build a Swallowfield that is an interesting and rewarding place to work, that consistently exceeds the expectations and needs of our customers, and delivers sustained profitable growth for our shareholders. This has provided a framework that clarifies our values, our short, mid and long-term priorities and the key measures in place to measure our progress.

The foundation of this agenda is our values. These are the behaviours that we believe are critical to be successful in everything we do, and are as follows:

‘Making it happen’ - means being action oriented and being accountable for what we have agreed and committed to do with colleagues, customers and suppliers. If something needs doing, let’s get it done.

‘Making it better’ - means a mindset of continuous improvement in everything we do and a challenge to not only identify things that are not working so well, but to also to do something about it.

‘Making it together’ – reminds us that whatever we are trying to make happen or to make better, we are highly unlikely to be able to do it on our own. We will always need the involvement and support of colleagues, customers and suppliers to ensure solutions work best for all concerned.

Also, within the ‘Building a Better Swallowfield’ agenda we have set out both a clear set of near term and longer-term business priorities and focus areas. The nearer term initiatives are set out under the heading of ‘Delivering for Today’ and the longer-term initiatives are set out under the heading of ‘Creating for Tomorrow’. The ‘Delivering for Today’ initiatives have been varied on an annual basis.

All of these elements come together under our ‘Building a Better Swallowfield’ pyramid, which is used across the business as a visual mnemonic to capture how we want to develop the business.

PEOPLE ANDSUSTAINABILITY

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 33 –

EMPLOYEE COMMUNICATION The policy of informing and consulting with employees is given prominence and has continued by means of regular briefing groups and consultative committees. Employees are encouraged to present their views and suggestions in respect of the Group’s performance. During the year a number of employee workshops and briefings have taken place to engage employees in the delivery of ‘Building a Better Swallowfield’. This has been supported through the all employee reward and recognition scheme and an on-line facility to capture employee suggestions and questions. EQUALITY AND DIVERSITY The Group continues to carefully consider applications for employment by an individual from any background, including disabled persons. The Group’s training, development and promotion policies aim to ensure all employment decisions are based on fairness and merit.

CORPORATE SOCIAL RESPONSIBILITY The Group recognises the importance of social responsibility in its business and remains strongly committed to reducing the environmental impact of its production and design processes, and advancing its systems and policies to comply with and, wherever possible, anticipate changing legislative and customer demands. This important area is covered as part of regular team briefs to all members of staff, and the Group uses a variety of key performance indicators as part of its regular reporting cycle.

The Group is subject to regular external audits associated with both accreditations held and customer requirements, and during the year hosted over 35 separate audits. These include ISO 9001; ISO 14001; ISO 22716 Cosmetics GMP; ISO 13485 Medical Devices; FDA; CLAS; BRC; FSC; plus, a number of Ethical, Environmental, Health & Safety Executive (COMAH), and Customer audits.

ETHICAL TRADING The Group is a member of SEDEX (Supplier Ethical Data Exchange) and regularly participate in SMETA audits at its production sites to ensure compliance with all applicable Ethical and responsible business practices in global supply chains covering Labour Standards, Business Ethics, Health & Safety and the Environment.

The Group discloses on and is assessed on the EcoVadis CSR platform giving assurance of meeting the highest standards of sustainable procurement, business practices environment and labour practices. EcoVadis gathers information from around 24,000 subscribers, based in 95 different countries and 145 different industry sectors. Over 100 multinational companies use EcoVadis to monitor the CSR performance of their suppliers. The Group was awarded a Gold award following initial assessment in 2015 and this Gold rating was maintained in 2016, placing the Group in the top 13% of all suppliers assessed across all categories.

Within its supply chain, the Group is also certified to FSC (ensuring the ethical supply chain of wood) and members of RSPO (for ethical & sustainable purchase of palm oil), with each organisation giving assurance that correct business practices are being applied. A statement made pursuant to the Modern Slavery Act 2015 setting out the steps the Group has taken to ensure that slavery and human trafficking is not taking place in our supply chains or in any part of our business has been incorporated within our Ethical Policy, and can be found on our website.

STRATEGIC REPORT ANNUAL REPORT & ACCOUNTS 2017– 34 –

HEALTH AND SAFETYThe philosophy of Continuous Improvement remains core to the Group’s approach to Health and Safety Management. There are regular Health and Safety reviews led by senior management involving the Health and Safety Manager and workforce representatives. All areas of the business are audited twice each year to assess any Health and Safety strengths and remedy any identified weaknesses. Action plans for all issues are developed and monitored by the Health and Safety Manager and local management, and are reviewed by senior management. Risk Assessments are prepared for all foreseen issues and are regularly reviewed. The Group’s Health and Safety System is designed to run parallel to BS 18001.

The Group has invested in the IOSH ‘Working safely’ training package which is being rolled out across all UK employees over a two-year period, with over 120 employees receiving the training to date. The ‘Working safely’ package is a completely different approach to safety and health training. It’s a high-impact programme designed to be enjoyable and stimulating, and is aimed at getting people involved at all levels across the organisation. ‘Working safely’ covers:– defining hazard and risk

– identifying common hazards– improving safety performance– protecting our environment

Successful delegates are awarded an IOSH Working safely certificate, a nationally recognised and respected certificate.

Successful delegates are now utilising their training to run proactive hazard spotting workshops in their own areas of work, with employees coming together to spot potential hazards before they could develop into incidents. These potential hazards are then analysed and if necessary corrective actions are raised.

All Accidents, Incidents and Near Misses are fully investigated to identify root cause and preventive actions are developed and put in place and we continue to increase our focus on near-miss reporting. All the above are afforded a score rating which is assessed each year and monitored through the Group’s ‘Building a Better Swallowfield’ Score Card.

The Group Health and Safety Manager is a chartered member of the Institution of Occupational Safety and Health (IOSH).

ANNUAL REPORT & ACCOUNTS 2017 STRATEGIC REPORT– 35 –

ENVIRONMENTThe Group remains strongly committed to continuously reduce the environmental impact of its operations and products.

The Group’s Environmental Management System was certified by BSI to ISO14001 in December 2005. Since that date, all six-monthly surveillance audits have been passed with no major non-conformances. No major non-conformances were reported in the last financial year & the Group transitioned to the new ISO14001:2015 standard in June 2017.

The Group has made significant steps forward in reducing its consumption of energy and its impact on the environment since 2005/6 and uses site based metrics to monitor energy consumption, water usage and CO2 emissions.

The Group has registered under the UK CRC Energy Efficiency Scheme, and a result of energy saving initiatives such as replacing compressors & installing more LED lighting has seen Group electricity consumption reduce by over 17.9% since 2012 and at 4,102 MWh currently falls well below the full compliance thresholds outlined under CRC of 6,000 MWh. The Group also publicly declares its carbon emissions via the CDP scheme, achieving awareness status & has changed over to the use of Zero Carbon Renewable Electricity in the UK from December 2016. The Group was also given a 64% sustainability rating score from Carbon Clear, compared to an industry average of 49%.

The Energy Savings Opportunity Scheme (ESOS) is a mandatory energy assessment and energy saving identification scheme for large undertakings (and their corporate groups). The Group achieved the mandatory requirement under the ESOS scheme to comply by December 2015. The report continues to assist the Group in identifying any further savings opportunities.

Levels of dry waste recycling or reuse for aluminium, metal, cardboard, wood, paper, plastic etc. were maximised and we continue to focus on improving the percentage of waste recycled.

Challenging objectives have been established for the forthcoming year with the aim of continuing to reduce the overall environmental impact of our business, including that of our operations and products.

The Group continues to seek to be ‘environmentally responsible’ in all its activities and to minimise the impact of our activities on the environment.

Copies of our Health and Safety, Environmental, and Ethical policies plus current certifications and accreditations are available on the Swallowfield website (www.swallowfield.com).

By order of the Board

Chris How Mark WarrenChief Executive Officer Group Finance Director18 September 2017

GOVERNANCE ANNUAL REPORT & ACCOUNTS 2017– 36 –

The Group is committed to business integrity, high ethical values and professionalism in all its activities. As an essential part of this commitment the Group supports the highest standards in corporate governance. The Board is accountable to the Company’s shareholders for good governance and this statement describes how the principles of good governance set out in the UK Corporate Governance Code, published by the Financial Reporting Council are applied within the company. We do not comply with the UK Corporate Governance Code. However, we have reported on our Corporate Governance arrangements by drawing upon best practice available, including those aspects of the UK Corporate Governance Code we consider to be relevant to the Company.

RELATIONS WITH SHAREHOLDERSCommunications with shareholders are given high priority. The Chairman’s foreword and Strategic report on pages 8 to 35 include a detailed review of the business and future developments. There is regular dialogue with institutional and other major shareholders including presentations after the Company’s announcement of final and interim results. The Board also uses the Annual General Meeting to communicate with private and institutional investors and welcomes their participation. All Directors will be available to answer questions at the Annual General Meeting on 9 November 2017 and the resolutions to be proposed can be found on the separate circular sent to shareholders with a copy of this Report and Accounts. The Chairman and Non-Executive Directors meet and communicate with shareholders as requested. They also use the Company’s broker and informal discussions after the Annual General Meeting, to maintain open routes of communication with shareholders. All presentations to shareholders are shown in the investors section of the Group’s website.

THE WORKINGS OF THE BOARD AND ITS COMMITTEESThe BoardThe Board currently comprises an Independent Non-Executive Chairman, the Chief Executive Officer, two other Executive Directors and three other Non-Executive Directors. The biographies appearing on page 38-39 demonstrate a range of experience and sufficient calibre to bring independent judgement on issues of strategy, performance, resources and standards of conduct that are vital to the success of the Group. The Board is responsible to shareholders for the proper management of the Group. A statement of the Directors’ responsibilities in respect of the accounts is set out on page 41 and a statement of going concern on page 31.

The Board has overall responsibility for the Group and there is a formal schedule of matters specifically reserved for decision by the Board. Each Executive Director has been given responsibility for specific aspects of the Group’s affairs and independent advice is available to all Directors. Appropriate training is given when Directors are appointed to the Board.

The Board meets a minimum of six times per year to review trading performance, set and monitor strategy, approve matters reserved for decision by the Board and to ensure that adequate funding exists. All Directors are supplied with information in a manner to enable the Board to discharge its duties.

Indemnity InsuranceThe Group carries liability and indemnity insurance for Directors, Officers and Senior Managers.

CORPORATEGOVERNANCE

ANNUAL REPORT & ACCOUNTS 2017 GOVERNANCE– 37 –

Nomination CommitteeThe current members of the Nomination Committee are Brendan Hynes (Committee Chairman), Roger McDowell and Franklin Berrebi. The Committee is responsible for proposing candidates for appointment to the Board, having regard to the balance and structure of the Board. In appropriate cases recruitment consultants are used to assist the process. The terms of reference of the Nomination Committee are published on the Group’s website. All Directors are subject to re–election at least every three years. Audit CommitteeThe current members of the Audit Committee are Edward Beale (Committee Chairman), Brendan Hynes, Roger McDowell and Franklin Berrebi. It meets at least twice a year to review the Group’s accounting policies and reporting procedures, external audit reports and other relevant matters. The external auditors, Group Finance Director and Chief Executive Officer are also invited to attend but are not entitled to vote. The terms of reference of the Audit Committee are published on the Group’s website. The Group receives non-audit services such as taxation and other consultancy advice from the Group’s auditors. The Audit Committee assesses the independence of the external auditors by means of an internal review of relationships with the auditors together with a review of an annual independence report issued by the auditors. The Group does not have an internal audit function.

Remuneration CommitteeThe current members of the Remuneration Committee are Roger McDowell (Committee Chairman), Brendan Hynes, Franklin Berrebi and Edward Beale. The Chief Executive Officer and Group Finance Director attend the Remuneration Committee meetings by invitation but are not entitled to vote. The Committee reviews the terms and conditions of service of Executive Directors, and ensures that salaries, bonuses and share option awards satisfy any relevant performance criteria. Terms of reference of the Remuneration Committee are published on the Group’s website.

INTERNAL CONTROLThe Board is responsible for the Group’s system of internal control and for reviewing its effectiveness. Such a system can only provide reasonable and not absolute assurance against material misstatement or loss. The key procedures established are as follows:

• Responsibility levels, the ethos of the Group, the delegation of authority and other control procedures, together with appropriate accounting policies, are communicated throughout the Group;

• The Group appoints experienced and professional staff of the necessary calibre, both through promotion and recruitment, to fulfil their responsibilities;

• The Group maintains an annual budget process. The Board sets budgets once per year and monitors actual performance against those budgets at every Board meeting. The Board also reviews forecasts and expectations in the light of up-to-date circumstances and takes action as appropriate;

• The Audit Committee considers significant control matters. Management letter points raised by the external auditors are discussed by the Audit Committee and are dealt with as appropriate;

• The Group maintains an expenditure approval process that ensures that the Board approves major expenditure and investments; and

• The Board undertakes a review of internal controls annually.

The Group has established a Group Risk Management Register and the Board has procedures in place for regular reviews.

GOVERNANCE ANNUAL REPORT & ACCOUNTS 2017– 38 –

BRENDAN M HYNESMBA, FCMA

Non-Executive Chairman

CHRIS HOWChief Executive Officer

JANE FLETCHERBSc (Hons)

Group Sales and

Marketing Director

MARK WARRENBSc (Hons) FCCA

Group Finance Director

Brendan joined the Company as Non-Executive Chairman on 1st July 2013. He is also currently the Senior

Independent Non-Executive Director and Chairman of the Audit Committee of Churchill China plc, Non-

Executive Director of private, online education business “Webexaminer”; and a member of the Criticaleye

Advisory Board. He was CEO of Nichols plc from 2007 to 2013 having previously been Group Finance

Director. He has plc main board experience across a range of other sectors including TMT, retail, consumer

goods, buildings and automotive. Previous roles have included Executive Director at Knowledge Management

Software plc and Group Finance Director at William Baird plc a branded clothing business and Director of the

Consumer, Retail and Distribution (CRD) practice of PricewaterhouseCoopers advising Times 100 companies.

Brendan chairs the Nomination Committee and is a member of the Audit and Remuneration Committees.

Chris joined the Company as Chief Executive on 15th July 2013. He has extensive international experience

across the personal care and household sector, having held senior General Management and Sales &

Marketing positions with PZ Cussons and Colgate Palmolive. Chris has previously been Managing Director

PZ Cussons Australia; Regional Director PZ Cussons Europe, Asia, South Pacific; Managing Director PZ

Cussons UK; General Manager, Colgate Palmolive Benelux; as well as holding European and UK Sales Director

positions within Colgate Palmolive. Chris is a member of the Cosmetics, Toiletries and Perfumery Association

(CTPA) executive.

Jane joined the Company in 1996 and was promoted to the position of Group Sales and Marketing Director

in October 2004. Prior to this she gained valuable experience in product buying at Marks and Spencer. Jane

has over 20 years’ experience within the industry, working and developing products with both brands and

retailers.

Mark joined the Company in January 2010 as Group Finance Director. Mark has extensive financial,

commercial and operational management experience from across a range of customer oriented businesses

operating in global markets. Mark previously held senior roles in GEC plc, Whitbread plc, Interbrew SA,

Alpharma Inc. and Actavis.

BOARD OFDIRECTORS

ANNUAL REPORT & ACCOUNTS 2017 GOVERNANCE– 39 –

FRANKLIN BERREBIIndependent

Non-Executive Director

ROGER MCDOWELLIndependent

Non-Executive Director

EDWARD BEALENon-Executive Director

Franklin joined the Company in July 2010 and brings a wealth of international experience in the consumer

goods market having spent 33 years with L’Oréal, latterly as the Managing Director of L’Oréal Consumer

Goods Europe. Since retiring from L’Oréal in 2004 Franklin has worked with AXA Private Equity (now

Ardian) and Activa Capital, and sits on the Board of a number of companies. Franklin is a member of the

Audit, Remuneration and Nomination Committees.

Roger was reappointed to the Board in March 2012 having previously served as a Non-Executive Director

from July 2011 to January 2012. Roger is an experienced director of over 30 years’ standing: he led the

Oliver Ashworth Group through dramatic growth, main market listing and sale to St. Gobain, following which

he was appointed to a number of non-executive roles, including chairmanships in both public and private

equity backed businesses. He is currently Chairman of Avingtrans plc, and is Senior Non-Executive Director

of Servelec Group plc and Tribal Group plc. He is also a Non-Executive Director of D4T4 Solutions plc and

Proteome Sciences plc. Roger chairs the Remuneration Committee and is a member of the Audit and

Nomination Committees.

Edward joined the Company as a Non-Executive Director on 1 July 2014. Mr Beale is a Chartered Accountant

and is the Finance Director of Marshall Monteagle plc. He is a member, previously chairman, of the Corporate

Governance Committee of the Quoted Companies Alliance. He was a member of the Accounting Standards

Board of the Financial Reporting Council for six years to 31st August 2013. He is a non-executive director

of London Finance & Investment Group P.L.C., Western Selection P.L.C., Heartstone Inns Limited, and some

of their subsidiary and associated companies. Edward chairs the Audit Committee and is a member of the

Remuneration Committee.

GOVERNANCE ANNUAL REPORT & ACCOUNTS 2017– 40 –

Significant Shareholdings Shareholding Percentage of issued shares

SFM UK 2,163,000 12.8

WESTERN SELECTION 1,500,000 8.9

R & A PERSEY 1,375,936 8.2

HARGREAVE HALE LIMITED 1,167,134 6.9

OLD MUTUAL PLC 920,540 5.5

CHARLES STANLEY & CO LTD 851,250 5.0

RIVER AND MERCANTILE 750,000 4.4

FIL LIMITED 674,209 4.0

BUSINESS GROWTH FUND PLC 581,000 3.4

DIRECTORSThe Company’s current Directors are listed on page 38-39, together with their biographical details.

The Directors who served at any time during the year and since the year end were as follows:

B M Hynes M W Warren R S McDowellC G How F P Berrebi E J BealeJ M Fletcher

STRATEGIC REPORTThe Strategic Report set out on pages 10-35 provides a fair review of the Group’s business for the year ended June 2017. It also explains the objectives and strategy of the Group, its competition and the markets in which it operates, the principal risks and uncertainties it faces, employee information, the Group’s financial position, key performance indicators and likely future developments of the business.

DIRECTORS’REPORT

SHAREHOLDINGS

Save for these interests, the Directors have not been notified that any person is directly or indirectly interested in 3% or more of the issued ordinary share capital of the Company.

SUBSTANTIAL SHAREHOLDINGSAs at 18 September 2017, the following shareholders had notified the Company that they held an interest in 3% or more of its issued ordinary share capital:

ANNUAL REPORT & ACCOUNTS 2017 GOVERNANCE– 41 –

GENERAL MEETINGThis year’s Annual General Meeting will be held at the Registered Office, on Thursday 9 November 2017, at 12 noon. A separate circular has been sent to shareholders and includes the following:

• Notice of meeting;• Form of proxy;• Details and information on the resolutions to be proposed.

Grant Thornton UK LLP (‘Grant Thornton’) have expressed their willingness to continue in office as auditors and a resolution proposing their reappointment will be presented at the forthcoming Annual General Meeting.

STATEMENT OF DIRECTORS’ RESPONSIBILITIES The Directors are responsible for preparing the Annual Report and the financial statements in accordance with applicable law and regulations.

Company law requires the Directors to prepare financial statements for each financial year. Under that law the Directors have elected to prepare financial statements in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union. The financial statements are required by law to give a true and fair view of the state of affairs of the Company and the Group and of the profit or loss of the Group for that period. In preparing these financial statements, the Directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and estimates that are reasonable and prudent;

• state whether applicable IFRS’s have been followed, subject to any material departures disclosed and explained in the financial statements; and

• prepare financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

The Directors are responsible for keeping adequate accounting records which disclose with reasonable accuracy, at any time, the financial position of the Group and enable them to ensure that the financial statements comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Group and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The Directors are responsible for the maintenance and integrity of the corporate and financial information on the Group’s website. Legislation in the United Kingdom governing the preparation and dissemination of the financial statements and other information included in annual reports may differ from legislation in other jurisdictions.

DISCLOSURE OF INFORMATION TO AUDITORSAt the date of making this report each of the Company’s Directors, as set out on page 38-39, confirm the following:

• so far as each Director is aware, there is no relevant information needed by the Company’s auditors in connection with preparing their report of which the Company’s auditor is unaware; and

• each Director has taken all the steps that they ought to have taken as a director in order to make themselves aware of any relevant information needed by the Company’s auditors in connection with preparing their report and to establish that the Company’s auditor is aware of that information.

By Order of the Board

Mark Warren Group Finance Director and Company Secretary 18 September 2017

Company Number: 01975376

GOVERNANCE ANNUAL REPORT & ACCOUNTS 2017– 42 –

OUR OPINION ON THE FINANCIAL STATEMENTS IS UNMODIFIED We have audited the financial statements of Swallowfield plc (the ‘company’) and its subsidiaries (the ‘group’) for the 52 week period ended 24 June 2017 which comprise the group statement of comprehensive income, the group and company statements of financial position, the group and company statements of changes in equity, the group and company cash flow statements and notes to the financial statements, including a summary of significant accounting policies. The financial reporting framework that has been applied in the preparation of the group financial statements is applicable law and International Financial Reporting Standards (IFRSs) as adopted by the European Union and, as regards the company financial statements, as applied in accordance with the provisions of the Companies Act 2006.

In our opinion:• the financial statements give a true and fair view of the state of the group’s and of the company’s affairs as at 24 June 2017

and of the group’s profit for the period then ended;• the group financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union;• the company financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union

and as applied in accordance with the provisions of the Companies Act 2006; and• the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

BASIS FOR OPINION We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the financial statements section of our report. We are independent of the group and the company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the FRC’s Ethical Standard as applied to listed entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

WHO WE ARE REPORTING TOThis report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

CONCLUSIONS RELATING TO GOING CONCERNWe have nothing to report in respect of the following matters in relation to which the ISAs (UK) require us to report to you where:• the directors’ use of the going concern basis of accounting in the preparation of the financial statements is not appropriate; or• the directors have not disclosed in the financial statements any identified material uncertainties that may cast significant

doubt about the group’s or the company’s ability to continue to adopt the going concern basis of accounting for a period of at least twelve months from the date when the financial statements are authorised for issue.

INDEPENDENTAUDITOR’S REPORT

TO THE MEMBERS OF SWALLOWFIELD PLC

OPINION

ANNUAL REPORT & ACCOUNTS 2017 GOVERNANCE– 43 –

OVERVIEW OF OUR AUDIT APPROACH• Overall materiality: £372,000, which represents 0.5% of total group revenues for the period ended 24 June 2017• Key audit matters were identified as the acquisition of The Brand Architekts Limited (applicable to the Group), the accounting

treatment applied in relation to share based payments (applicable to the Company), and disclosures in relation to the defined benefit pension scheme (applicable to the Company)

• We performed full scope UK statutory audit procedures on the company and significant components Swallowfield Consumer Products Limited, MR. Haircare Limited, and The Brand Architekts Limited

• Full scope audit procedures were performed by the component auditor Grant Thornton Prague on the significant component Swallowfield s.r.o.

• Analytical procedures at group level were performed by us for non-significant components Swallowfield s.a.r.l., Swallowfield Inc., and Bagsy Beauty Limited

KEY AUDIT MATTERSKey audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) that we identified. These matters included those that had the greatest effect on: the overall audit strategy, the allocation of resources in the audit; and directing the efforts of the engagement team. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

KEY AUDIT MATTER - GROUP

Acquisition of The Brand Architekts LimitedOn 27 June 2016 the Group acquired the entire issued share capital of The Brand Architekts Limited. The total consideration payable was £12.08m, of which £1.85m was contingent upon The Brand Architekts Limited performance during the first 12 months post acquisition. The contingent consideration was accrued at the period end and was paid on 24 July 2017. The acquisition was financed via the issue of 5,558,985 new £0.05 Ordinary shares to raise £8.6m and a new £2.00m loan facility.

Following the acquisition of The Brand Architekts Limited a purchase price allocation exercise was performed by management to determine how the assets associated with the acquisition should be recognised within the consolidated financial statements.

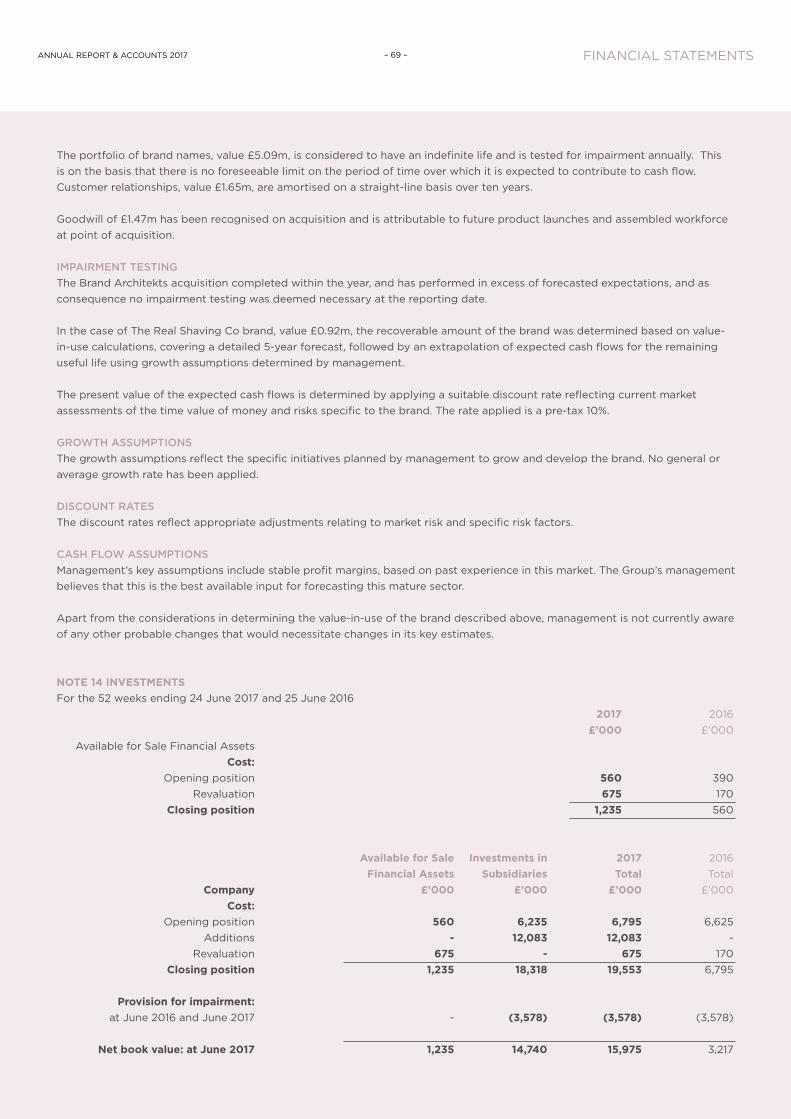

Following this exercise, intangible assets with a total value of £8.21m were recognised. This total value is classified as brands (£5.09m), customer relationships (£1.65m), and goodwill (£1.47m).