Sustainability Development Roadmap for Listed · PDF fileSustainability Development Roadmap...

49

1 Sustainability Development Roadmap for Listed Companies Social Sustainability Corporate Sustainability Confidence for Shareholders As of May 2014

Transcript of Sustainability Development Roadmap for Listed · PDF fileSustainability Development Roadmap...

1

Sustainability Development Roadmap for Listed Companies

Social Sustainability

Corporate Sustainability

Confidence for Shareholders

As of May 2014

2

Background of SD

Roadmap

Current Status

Trends and

Issues

Roadmap Action Plan

Contents

3

Background of theSustainability Development Roadmap

• In 2004, the National Corporate Governance Committee approved a plan outlining policies and measures that had yielded a considerable CG improvement. Review of the plan is now required to ensure its consistency with the current global conditions.

• Increasing attention has been given to Corporate Social Responsibility (CSR). There is a growing number of foreign investors and companies that are concerned to take company‟s CSR policies and activities intoconsideration when making their investment decision and suppliers selection.

• More awareness of global warming, natural resources depletion, severe and frequent natural disasters, social inequality, and corruption is evident in Thailand.The impact can occur at all levels: global, national as well as corporate; it is therefore necessary that all must participate in alleviating the problems.

• In December 2013, the SEC Board has approved „the Sustainability DevelopmentRoadmap‟ outlining processes that aim not only to improve corporate sustainabilitybut also enhance environmental and social sustainability as a whole. The roadmap is part of the SEC Strategic Plan 2013-2015.

Source: UN PRI

4

Economic

Environ-mentSocial

From Corporate Governance to ESGfor Sustainability Development

Return- strategy

- innovation- risk management

CG

Building confidence for shareholders.

AimDeveloping SD for all stakeholders, which subsequently leads to social sustainability.

Sustainability Development

Emphasis on credibility to shareholders

Include all stakeholders

N.B. In practice, the terms „CSR‟, „ESG‟ and „SD‟ are often used interchangeably.

Rationale

5

International Standards & Initiatives on ESG

- The ten Principles covering 1) Human Rights2) Labour 3) Environment 4) Anti-Corruption- Participants are voluntaryto be signatory. - Signatory commits to issuing annual COP (Communication on Progress) on progress made in implementing the 10 principles –otherwise, delisted - 10,000 participants from 145 countries. -Known as “the World’s largest voluntary corporateresponsibility initiative”

- Guidelines onSustainability Reporting that provide information on strategies, operations, governance, management, and positive and negative ESG bottom line. - latest guidelines GRI-G4- 5,753 organisationsworldwide esp. large listed companies have adopted the GRI for their sustainability reporting.

- Voluntary recommendations for responsible business conduct for multinational enterprises. Notregulation nor protectionist measures. - Cover 6 topic areas: 1) Disclosure 2) Employment 3) Environment 4) Anti-corruption 5) Consumer Interests 6) Science and Technology- 30 OECD member states and 9 non-member states support the use of the guidelines.

- A voluntary guidance standard for all organisations containing7 core subjects: 1) organisationalgovernance 2) human rights 3) labour practices 4) environment 5) fair operating practices 6) consumer issues 7) community involvementand development- Thai Industrial StandardsInstitute encourages business entities to adopt ISO 26000. - Likely to become certified standard.

- A framework for sustainability reporting that integrates companysustainable development and strategies. - The framework highlightsthe disclosure of company’svarious capitals, namely 1) financial capital 2) manufactured capital 3) intellectual capital 4) human capital 5) social and relationship capital and 6) natural capital-Officially launched in December 2013, with100 organisationsparticipatedthe pilot programme.

6

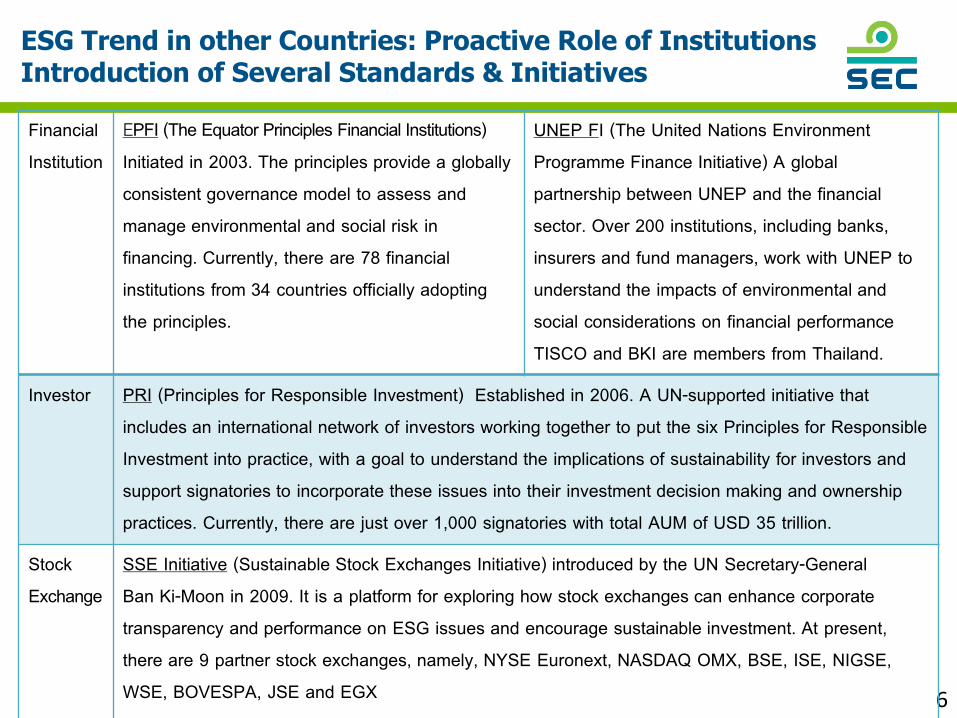

ESG Trend in other Countries: Proactive Role of InstitutionsIntroduction of Several Standards & Initiatives

FinancialInstitution

EPFI (The Equator Principles Financial Institutions)Initiated in 2003. The principles provide a globally consistent governance model to assess and manage environmental and social risk in financing. Currently, there are 78 financial institutions from 34 countries officially adopting the principles.

UNEP FI (The United Nations Environment Programme Finance Initiative) A global partnership between UNEP and the financial sector. Over 200 institutions, including banks, insurers and fund managers, work with UNEP to understand the impacts of environmental and social considerations on financial performance TISCO and BKI are members from Thailand.

Investor PRI (Principles for Responsible Investment) Established in 2006. A UN-supported initiative that includes an international network of investors working together to put the six Principles for Responsible Investment into practice, with a goal to understand the implications of sustainability for investors and support signatories to incorporate these issues into their investment decision making and ownership practices. Currently, there are just over 1,000 signatories with total AUM of USD 35 trillion.

Stock Exchange

SSE Initiative (Sustainable Stock Exchanges Initiative) introduced by the UN Secretary-General Ban Ki-Moon in 2009. It is a platform for exploring how stock exchanges can enhance corporate transparency and performance on ESG issues and encourage sustainable investment. At present, there are 9 partner stock exchanges, namely, NYSE Euronext, NASDAQ OMX, BSE, ISE, NIGSE, WSE, BOVESPA, JSE and EGX

7

CG and CSR Principles

Corporate Governance

1. The Rights of Shareholders and Key Ownership Functions

2. The Equitable Treatment of Shareholders

3. The Role of Stakeholders in Corporate Governance

4. Disclosure and Transparency

5. The Responsibilities of the Board

(OECD Principles of Corporate Governance, 2004)

Corporate Social Responsibility

1. Good Corporate Governance

2. Fair business conduct

3. Anti-corruption

4. Human rights

5. Equitable treatment of labours

6. Accountability to customers

7. Support environmental responsibilities

8. Community and social development

9. Innovation and its promotion

10. Sustainability Reporting

(CSRI, Stock Exchange of Thailand Guidelines for Social Responsibility)

8

Corporate Social Responsibility (CSR)

1. CSR after Process

Project / Social Activity/ Philanthropy

2. CSR in Process*(main objective)

Embedded in core business process

3.CSR as Process Social Enterprise

Business Enterprise

Social Enterprise

9

Corporate Sustainability Development

IdentifyStakeholders‟ need

Formulate Strategies

Operations

Reporting

Trends & issues including social and environmental changes

Key factors, such as product development, production process, etc. should be included.

Select the development level: compliance, do it better, ordifferentiate oneself. KPIs are identified for every strategy.

CSR in-process: Fairness and Impacts

International Accepted Standards, for instance, GRI and Integrated Report are used as a guide. Strategies and ESG should be related and KPIs identified.

10

Summary of the SD Roadmap

CG in substance

Board and executives drive the company to

achieve its performance with good governance

and sustainability in real practice.

CSR in process

Responsible to social and environmental

concerns that embedded in day-to-day business

operation. Change agent that influences others to

respect CSR.

Anti-corruption in practice

Firm commitment not to initiate or facilitate any corruption practices.

Become a role model for others in the Thai business sector.

Social Sustainability

Corporate Sustainability

Confidence for Shareholders

11

Current Status

12

Shareholding StructureMost of listed companies have controlling shareholders.

• Top 50 companies = 76.5% of total market

capitalisation (as of 2013)

• Majority of listed companies = SMEs

• Avg. free float = 47% (139 companies have > 50%)

• Prevalence of concentrated ownership:

66% of listed companies are family-owned, while

14% are SOEs.

Benefit Managers are major shareholders, which

helps align the interests of management and

shareholders, long-term commitment and more

adaptive to competition.

Challenges Often received poor CG score from

international assessments. Tunnelling and lack of

sustainability and succession planning remain

concerned issues.

Alternative framework/model of CG should

be suggested.

Family businesses in Asia, 2011

India 67%

Philippines 66%

Thailand 66%

Singapore 63%

Malaysia 62%

Indonesia 61%

Hong Kong, China 62%

South Korea 58%

Chinese Taipei 35%

China 13%

Source: Credit Suisse, 2011 “Asian Family Businesses Report”

13

International CG Assessment Reports have ranked Thailand top in ASEAN and third in Asia. Key challenges remain, for example, the board responsibilities category.

CG Watch market scores : 2007 to 2012

2007 2010 2012

1. Hong Kong (67) 1. Hong Kong (67) 1. Singapore (69)

2. Singapore (65) 2. Singapore (65) 2. Hong Kong (66)

3. India (56) 3. Japan (57) 3. Thailand (58)

4. Taiwan (54) 4. Thailand (55) 4. Japan (55)

5. Japan (52) 5. Taiwan (55) 5. Malaysia (55)

6. Korea (49) 6. Malaysia (52) 6. Taiwan (53)

7. Malaysia (49) 7. India (49) 7. India (51)

8. Thailand (47) 8. China (49) 8. Korea (49)

9. China (45) 9. Korea (45) 9. China (45)

10. Philippines (41) 10. Indonesia (40) 10. Philippines (41)

11. Indonesia (37) 11. Philippines (37) 11. Indonesia (37)

Source: 1. ACGA, September 2012

2. The World Bank – “Report on the Observance of Standards and Codes (ROSC) : Corporate Governance Country Assessment – Thailand, January 2013

3. Thai IOD 2013

The World Bank’s CG ROSC Thailand receives higher scores than regional averages in every category.

ASEAN CG Scorecard : average score of top100

Thai listed companies is higher than those of the regional counterparts.

14

Enforcement and CG culture need to be improved. Corruption tarnishes overall CG in Thailand.

CG Watch Report 2012

Comments1. Non-financial reporting is more of form than substance.2. Enforcement remains inefficient. Number of cases settled in court is comparatively lower

than cases filed by the SEC.3. Limited progress on the amendment of laws. 4. SEC‟s and SET‟s website should be more accessible, and all data available in English.5. Uncertainty remains with regard to the impact of the private sector‟s anti-corruption practices.

15

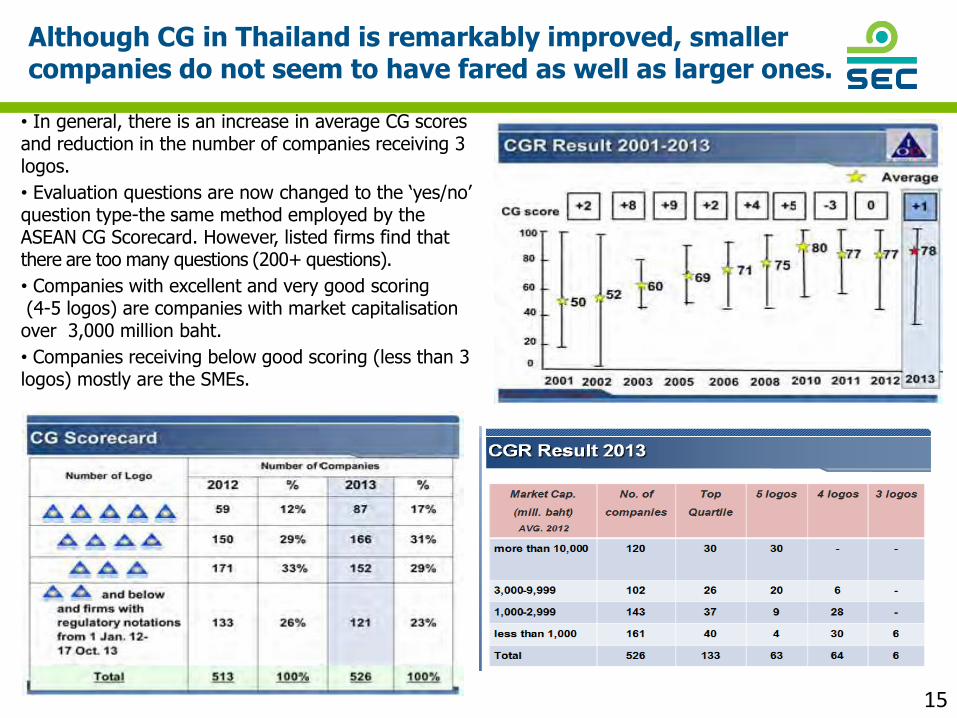

Although CG in Thailand is remarkably improved, smaller companies do not seem to have fared as well as larger ones.

• In general, there is an increase in average CG scores and reduction in the number of companies receiving 3 logos.

• Evaluation questions are now changed to the „yes/no‟ question type-the same method employed by the ASEAN CG Scorecard. However, listed firms find that there are too many questions (200+ questions).

• Companies with excellent and very good scoring(4-5 logos) are companies with market capitalisationover 3,000 million baht.

• Companies receiving below good scoring (less than 3 logos) mostly are the SMEs.

16Source : Thai IOD 2013

The CGR latest result shows that SMEs generally received lower score than their larger peers.

CGR Result 2013

17

CGR 2013 – The Role of Stakeholders and Board Responsibilities categories received comparatively low average scores.

CGR 2013

100

80

60

40

20

0Overall A. Rights of

ShareholdersD. Disclosure

and Transparency

E. Board Responsibilities

B. Equitable Treatment

of Shareholders

C. Role of Stakeholders

ASEAN CG Scorecard (2012)CG Score by Category

89

68

88

64

8678

31

97

21

47

97100

30 28

97

67

43

84 86

50

97

6851

95

70

48

87

56

26

78

100 100 100 100

15 0

Average

18

Treatment of Shareholders: AGM Evaluation produced good but levelling off result. Information disclosure before AGM remained weak.

2013

• 17 listed companies received score of 100%.• 14% of listed companies received score

of less than 70%.• Assessment questions only reviewed

standard agenda items. No specific questions were asked regarding the quality of information disclosure of important agenda items.

19

ESG/CSR/SD

Dow Jones Sustainability World Index Dow Jones Sustainability Emerging Markets Index

Brazil

China

Taiwan

South Africa

Colombia

India

Thailand

Mexico

Malaysia

Chile

Philippines

Turkey

• 3 Thai listed companies are SCG, PTT and PTTGC. They account for 0.16% of the total weight.

• Only one company, TOP, is included in this index, it accounts for 2.78% of the total weight.

N.B. as of Mar. 2014 (Source: http://www.sustainability-index.com)

There are 333 listed companies on the DJSI World; 3 of which are Thai listed companies. Meanwhile, there are 81 companies on the DJSI Emerging Markets including one Thai listed company. In 2014,there are 31 Thai listed companies that have passed the initial assessment criteria, and are eligible for the Sustainability Assessment.

USA

UK

Switzerland

Germany

France

Australia

Spain

Canada

South Korea

Japan

others

Thailand

20

ESG/CSR/SD

Majority of listed companies still consider CSR as a philanthropic or charitable activity, which is in fact known as „CSR after process‟. The importance of ESG, its related risks, and strategies for sustainability are yet to be completely realised.

Q: How relevant is sustainability to your business?

source: PWC, Pulse check on sustainability, Feb 2013

Extremely relevant

Very relevant

somewhat relevant

not relevant

21

Survey Result of ESG Disclosure

22

ESG/CSR/SD

• Following the SEC‟s CSR guidelines (2006), the Corporate Social ResponsibilityInstitute (CSRI) has further enhanced CSR of listed companies by:

– issuing guidelines for social responsibilities, guidelines for sustainability reporting (based on the GRI) and guidelines for various industry groups.

– organising seminars and CSR Awards event (76 listed companies participated the event in 2013).

– supporting listed companies in preparing their sustainability reports and listing on the DJSI.

– developing the SET SI.

• The CSRI 3-year plan (2014-2016) aims to raise the standard of CG and CSR practices to the internationally accepted level. In addition to supporting listed companies and developing the SET SI, as mentioned above, CSRI promotes the concept of Socially Responsible Investment (SRI) to investors.

• In 2013, SEC has published a notification on the compulsory disclosure of CSR policies and activities (effective from 2014). Prior to the notification, only 33 companies, mostly the large ones, have already published their CSR reports.

23

Anti-Corruption

• The Corruption Perceptions Index (CPI) 2013 of the Transparency International (TI) – Thailand

received a score of 35 out of 100 and ranked 102nd out of 176 countries.

• Private Sector – leading force in reducing corruption. The Anti-Corruption Thailand (ACT) and

the Private Sector Collective Action Coalition Against Corruption (CAC) (the latter was initiated

by the Thai IOD).

309 signed the Declaration of IntentOnly 14 are CAC’s certified members

119 business enterprises

140 out of 562 listed companies

35 out of65

Securities/ Inv. Mngt

15 out of 20 commercial

banks

• Many listed firms are still reluctant to

stop bribery, with concern that this might

hinder their business progress and

competitiveness.

The Anti-Corruption Thailand

campaigns, watchdog group, signing integrity pact with the public

sector for large procurement contracts.

• The SEC has issued guidelines on the

disclosure of anti-corruption policy and

procedures, and encouraged the

institutional investors to ask questions

about these policy and procedures at the

AGMs.

24

Trends & Issues

25

OECD’s Corporate Governance Developments

• The OECD Principles of Corporate Governance - an internationally accepted

standard, first released in 1999 and last revised in 2004. A further review starts in

2014 with the objective of conclusion within one year. The review is expected to

include the role of board in governing company subsidiaries (the issue is already

addressed and included in the requirement of the annual registration statement

(Form 56-1) disclosure).

• Asian CG Roundtable – a regional forum for promoting CG practices. The

Roundtable analyses policy options particularly for companies in the region with

concentrated ownership structure (many of them are family-owned, state-owned,

or with subsidiaries) Priorities are:

1. Effective enforcement: related-party transaction, ownership & control

disclosure, and fiduciary duties. The Roundtable is working on the following best

practices

• Legal frameworks – though converge, different interpretation remains

• Structure and responsibilities of the regulator and law enforcement agencies

• Roles of regulatory authorities: supervising, monitoring, and penalising

• Enforcement action / practices disclosure

• Court and justice system

• Cross-border enforcement

26

OECD’s Corporate Governance Developments

2. Board Independence

„Board Member Nomination and Election report, 2012‟

Recommendations– Transparent, fair, formal and empowered board nomination & election process (SEC

and SET have not imposed the requirement of nomination committee establishment)

– Facilitating participation of all shareholders and widening the pool of qualified candidates

– Enhancing transparency and board evaluation

3. Related party transactions: RPT

„Guide on Fighting Abusive Related Party Transactions in Asia, 2011‟ - Thailand has generally completed key areas as recommended in the report.

Regulations on RPT is currently under review.

4. Studies on CG DevelopmentSome studies have found that given insufficient knowledge and understanding of

corporate landscape, and the complexity of the equity market with various types of shareholders, the public sector was uncertain with regard to its authoritative and legal enforcement roles. Other studies have suggested that each investor‟s investment policy and business model affect their economic incentives level, which in turn determine their interest in the company‟s CG policies and practices. By imposing regulation on the investors to encourage more of their concern on the topic may prove to be costly and ineffective. It was recommended that the dynamics and culture of each company should be sustained and communication with stakeholders fostered.

27

Corporate Governance in other Countries

• Securities Commission Malaysia has published a Corporate Governance Blueprint 2011 that includes

• Shareholder Right

• Role of Institutional Investors

• The Board‟s Role in Governance

• Disclosure and Transparency

• Role of Gatekeepers and Influencers

• Public and Private Enforcement

• Dodd-Frank Wall Street Reform and Consumer Protection Act (2010) Say on Pay - a firm's shareholders have the right to vote on the remuneration of executives, in addition to information disclosure and the establishment of remuneration committee.

• Companies realise the value of integrating Governance, Risk and Compliance (GRC) as an approach to enhance business value through improving operational decision making and strategic planning, in addition to the emphasis on checks and balances.

28

CG Progress in Thailand: IOD’s CG priorities

Source: Dr. Bandid Nijathaworn‟s speech at the National Director Conference 2013

29

Progress on ESG

30

Development of ESG

International level

• It is believed that if social and environmental impacts were easily measurable, ESG could be successfully developed. However, some issues, such as quality of life, are hard to measure and take some time to evident the outcome.

• The International Federation of Accountants (IFAC) is in the process of developing an information disclosure standard. Some issues remain to be discussed.

• Given the pervasive social issues, many businesses have already adopted the „Creating Shared Value‟ or the „Strategic CSR‟ approach.

• In 2011, Thailand ratified the United Nations Convention against Corruption (UNCAC), which commits the country to ratifying, implementing and monitoring of the UNCAC framework (more than 170 countries have ratified the UNCAC).

• In order to promote corporate social responsibility, one of the objectives of the ASEAN Socio-Cultural Community (ASCC) Blueprint is to encourage the business sector to include CSR initiatives in the corporate agenda.

• The CSR Club, the Thai Listed Companies Association, the ASEAN Foundation and business groups from four countries have jointly established the ASEAN CSR Network to serve as a venue for supporting and exchanging experiences and knowledge on CSR to the member countries in the region.

31

Development of ESG

National Level

• The Cabinet Resolution on 12 Oct. 2010 and the National Committee for Promotion of Social Welfare have assigned the Ministry of Social Development and Human Security to develop a „CSR Strategic Plan‟ to be submitted to the cabinet in 2014.

• Ministry of Industry has initiated the „Green Industry Project‟ with the purpose to promote environmental sustainability in the industry sector. The participation to the Project is divided into 5 levels as follows:

Level 1 "Green Commitment" - a commitment to reduce the environmental impact, and communicate the commitment within the organisation.

Level 2 "Green Activity" - an activity to reduce impact on the environment.

Level 3 "Green System" - the systematic approach to environmental management that involves the monitoring, assessment, and review process to ensure continuous development. This also includes receiving well-recognised awards and environmental certifications.

Level 4 "Green Culture" – the organisational culture that encourages all members of the organisation to take into consideration and responsibility to the environment, and to follow best „green‟ practice as part of their day-to-day work life.

Level 5 "Green Network" – the commitment to the environment throughout the supply chain. Companies encourage their partners are to participate the „Green Industry Project‟. Source: www.greenindustry.co.th

32

Sustainability DevelopmentRoadmap

33

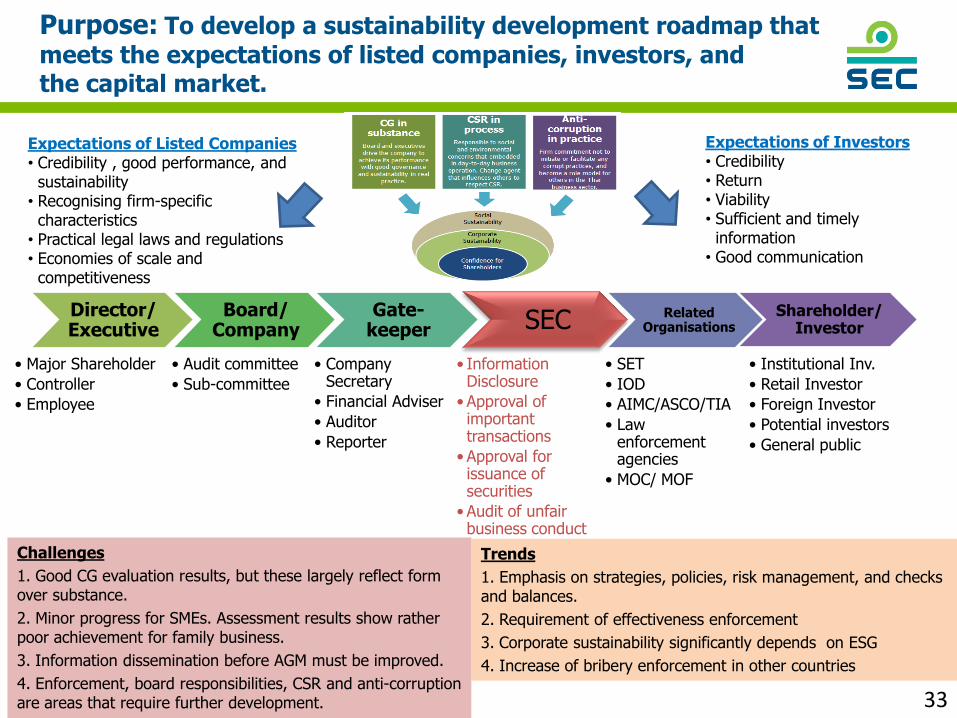

Purpose: To develop a sustainability development roadmap that

meets the expectations of listed companies, investors, and the capital market.

Trends

1. Emphasis on strategies, policies, risk management, and checks and balances.

2. Requirement of effectiveness enforcement

3. Corporate sustainability significantly depends on ESG

4. Increase of bribery enforcement in other countries

Challenges

1. Good CG evaluation results, but these largely reflect form over substance.

2. Minor progress for SMEs. Assessment results show rather poor achievement for family business.

3. Information dissemination before AGM must be improved.

4. Enforcement, board responsibilities, CSR and anti-corruption are areas that require further development.

Director/Executive

• Major Shareholder

• Controller

• Employee

Board/Company

• Audit committee

• Sub-committee

Gate-keeper

• Company Secretary

• Financial Adviser

• Auditor

• Reporter

SEC

• Information Disclosure

• Approval of important transactions

• Approval for issuance of securities

• Audit of unfair business conduct

Related Organisations

• SET

• IOD

• AIMC/ASCO/TIA

• Law enforcement agencies

• MOC/ MOF

Shareholder/Investor

• Institutional Inv.

• Retail Investor

• Foreign Investor

• Potential investors

• General public

Expectations of Listed Companies• Credibility , good performance, and

sustainability• Recognising firm-specific

characteristics• Practical legal laws and regulations• Economies of scale and

competitiveness

Expectations of Investors• Credibility• Return• Viability• Sufficient and timely

information• Good communication

34

Sustainability DevelopmentRoadmap

1. Enhancing CG accountability of the board

4. Strengthening the roles of investors

5. Strengthening the roles of gatekeepers

6. Continuously improving information disclosure

7. Increasing enforcement's efficiency and effectiveness

8. Building SEC as a sustainable organisation

3. Fostering commitment on anti-corruption practices

2. Promoting corporate social and environmental

responsibility

Present Next 5 years

Self DisciplinesMarketDisciplines

Regulatory Disciplines

35

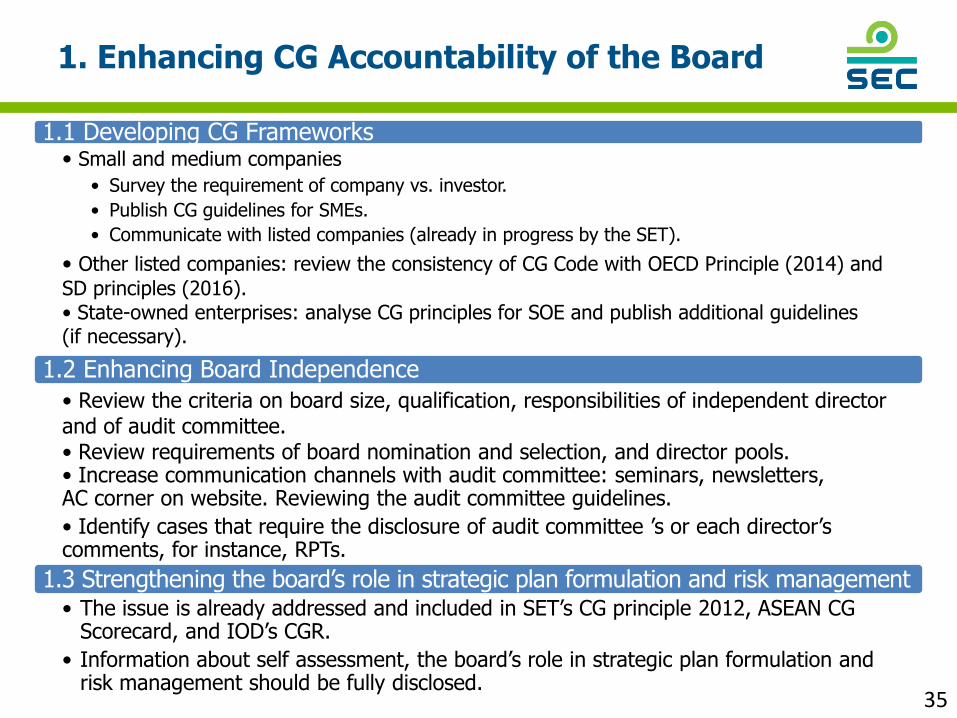

1.1 Developing CG Frameworks • Small and medium companies

• Survey the requirement of company vs. investor.

• Publish CG guidelines for SMEs.

• Communicate with listed companies (already in progress by the SET).

• Other listed companies: review the consistency of CG Code with OECD Principle (2014) and

SD principles (2016).• State-owned enterprises: analyse CG principles for SOE and publish additional guidelines (if necessary).

1.2 Enhancing Board Independence

• Review the criteria on board size, qualification, responsibilities of independent director and of audit committee.• Review requirements of board nomination and selection, and director pools.• Increase communication channels with audit committee: seminars, newsletters, AC corner on website. Reviewing the audit committee guidelines.

• Identify cases that require the disclosure of audit committee ‟s or each director‟s comments, for instance, RPTs.

1.3 Strengthening the board‟s role in strategic plan formulation and risk management• The issue is already addressed and included in SET‟s CG principle 2012, ASEAN CG

Scorecard, and IOD‟s CGR.

• Information about self assessment, the board‟s role in strategic plan formulation and risk management should be fully disclosed.

1. Enhancing CG Accountability of the Board

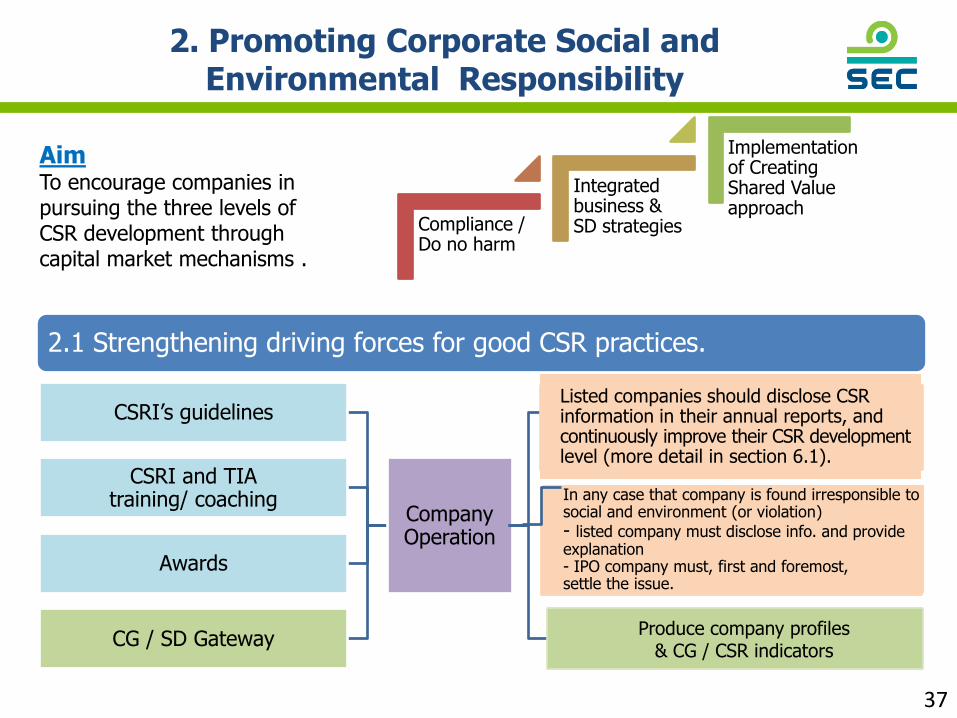

36

Board Practices

Guidelines : SET‟s CG Principles 2012

IOD‟s director & company secretary training

Guidelines, handbooks,and checklist

CG / SD Gateway

1. Enhancing CG Accountability of the Board

1.4 Strengthening driving forces to foster good CG.

• Develop CG Gateway as a knowledge portal.

• Develop company profiles and compiling CG indicators.

• Promote the use of ASEAN CG Scorecard evaluation.

• Revise the CGR criteria to ensure its consistency with the reviewed CG Framework

Guide to CG best practices (in addition to legal requirement)

„Comply or Explain‟ disclosure

IOD publishes CGR results.

Disclose the results of ASEAN Scorecard Assessment

Produce company profiles & CG / CSR indicators

37

Company Operation

CSRI‟s guidelines

CSRI and TIAtraining/ coaching

Awards

CG / SD Gateway

Compliance /Do no harm

Integrated business & SD strategies

Implementation of Creating Shared Value approach

AimTo encourage companies in pursuing the three levels of CSR development through capital market mechanisms .

Produce company profiles & CG / CSR indicators

Listed companies should disclose CSR information in their annual reports, and continuously improve their CSR developmentlevel (more detail in section 6.1).

In any case that company is found irresponsible to social and environment (or violation)

- listed company must disclose info. and provide explanation- IPO company must, first and foremost, settle the issue.

2.1 Strengthening driving forces for good CSR practices.

2. Promoting Corporate Social and Environmental Responsibility

38

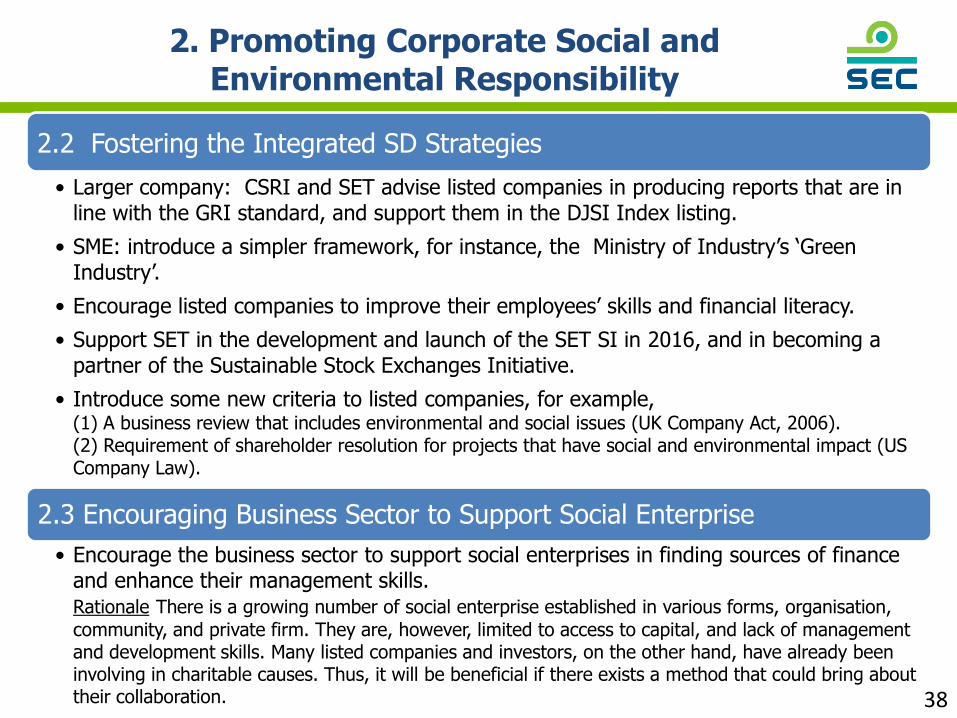

2. Promoting Corporate Social and Environmental Responsibility

2.2 Fostering the Integrated SD Strategies

• Larger company: CSRI and SET advise listed companies in producing reports that are in line with the GRI standard, and support them in the DJSI Index listing.

• SME: introduce a simpler framework, for instance, the Ministry of Industry‟s „Green Industry‟.

• Encourage listed companies to improve their employees‟ skills and financial literacy.

• Support SET in the development and launch of the SET SI in 2016, and in becoming a partner of the Sustainable Stock Exchanges Initiative.

• Introduce some new criteria to listed companies, for example, (1) A business review that includes environmental and social issues (UK Company Act, 2006).(2) Requirement of shareholder resolution for projects that have social and environmental impact (US Company Law).

2.3 Encouraging Business Sector to Support Social Enterprise

• Encourage the business sector to support social enterprises in finding sources of finance and enhance their management skills. Rationale There is a growing number of social enterprise established in various forms, organisation,

community, and private firm. They are, however, limited to access to capital, and lack of management and development skills. Many listed companies and investors, on the other hand, have already been involving in charitable causes. Thus, it will be beneficial if there exists a method that could bring about their collaboration.

39

3. Fostering Commitment on Anti-Corruption Practices

Aim

Firm commitment not to initiate or facilitate any corruption practices. Become a role model for others in the Thai business sector.

3.1 Strengthening driving forces to good anti-corruption practices.

Company Operation

IOD‟s CAC

IOD and TIATraining

Anti-corruption questions included in CGR Assessment

CG / SD Gateway Produce company profile &anti-corruption progress indicators

Letter of Commendation. Encouraging listed, securities, and asset management

companies to become CAC certified members.

Monitor their implementation

Listed companies should disclose anti-corruption information in their annual

reports.

Target

60% of listed companies

40

3.2 Encouraging investors to consider investing in listed companies with anti-corruption policies and procedures.

• Liaise with the institutional investors, for instance, the Association of Thai Securities Companies and Association of Investment Management Companies, to monitor and enquire about the company‟s anti-corruption action at the Annual General Meetings (starting in 2014) and to publish some guidelines on the exercise of voting rights.

• Work with the Thai Investors Association in defining a set of appropriate questions for the Protection of Shareholder Rights volunteers to ask at the company‟s Annual General Meetings.

• Co-operate with the Investment Analysts Association and Association of Thai Securities Companies in placing emphasis on the company‟s anti-corruption policy in their analyst reports.

3.3 Developing standards for the Financial Advisor on the due diligence practices that address the IPO company‟s anti-corruption-related issue/news.

• The Financial Advisor should advise the company on clarification or information disclosure about any anti-corruption-related issue/news that could significantly impact the company.

3. Fostering Commitment on Anti-Corruption Practices

41

4.1 Promoting investment in a company with CG & CSR policies and practices

• Encourage the institutional investors to actively consider CG and CSR to support their investment decisions. They should also be encouraged to use their voting rights and ask questions at the AGMs.

• Advise the institutional investors on the development of an investment code, based on the UK Stewardship Code (2012) and UN Principles for Responsible Investors (UNPRI).

• Encourage the analysts to include CG / CSR indicators in their analyst reports.

• Encourage the retail investors to invest in mutual funds and listed companies with excellent CG/CSR policies and practices, for instance, those on the SET SI.

4.2 Enhancing the roles of the Thai Investors Association (TIA)

• Review the AGM Checklist manual to include the quality of information disclosure and the SD

operational process.

• Encourage the TIA to actively comment on any of the company‟s important items and issues.

• Provide relevant training courses to the Protection of Shareholder Rights volunteers.

4.3 Examining legal mechanisms that protect the investors‟ rights

• Review mechanisms that accommodate the investors with their compensation demand, for example,

the Securities Investors Association Singapore‟s methods of monitoring listed companies.

• Follow up the enactment of the Class Action law (currently, under the Senate‟s consideration)

• Follow up the amendment (such as E-voting /E-proxy clauses) of the Public Limited Companies Act.

4. Strengthening the Roles of Investors

42

5. Strengthening the Roles of Gatekeepers

Company/Board

Investor/Regulator

InformationApproved Items

5.1 Company Secretary

• Increase the qualification of company secretary with the requirement of company secretary certification.

• Support the promotion of the Thai Company Secretary Club to become an association.

• Support the Thai Listed Companies Association/ universities‟ curriculum development.

5.2 Investor Relations

•No qualification is presently required of the investor relations agents.

•Organise training programmes and forums for exchanging experiences among the IR members.

•Disclosure of the qualification of the investor relations agencies.

5.3 Financial Advisor

• Organise trainings on CG, CSR and Anti-corruption topics to the Financial Advisor.

• Develop standards on due diligence practices that include CG, CSR, and anti-corruption issues.

5.4 Auditor

•Promote independence of the Auditor.

• Issue guidelines on the non-audit services.

Gatekeepers

InformationApproved Items

43

6. Continuously Improving Information Disclosure

• Set „step-up‟ targets to consistently raise the level of SD disclosure.

• Develop SD progress indicators to be included in the company profiles.

• Encourage listed companies to prepare annual report by integrating normal business operations and SD strategies.

• Consider the issuance of guidelines to account for social and environmental impact.

6.2 Improving the disclosure of non-financial items

• Monitor and advise listed companies on the disclosure of non-financial items (CG/CSR/Corruption/MD&A) as required in the revised annual registration statement (Form 56-1).

• Further improve the followings:

• ownership structure

• guidelines for risk factors to be more in line with the SD concept.

• relevant ratios for each business sector/ industry (co-operating with the Investment Analysts Association)

• Improve information disclosure in the notice to call shareholder‟s meeting to ensure sufficient information for shareholders to make voting decisions, and strengthen the board‟s fiduciary duty in providing opinions to shareholders.

Disclosure of present CSR policies & activities.

Disclosure of ESG/SD related risks.

SD is included business strategies.

Integrated business & SD strategies.2014

2015

2016

2017-2018

6.1 Requirement of information disclosure to encourage listed companies to continuously improve their CSR practices.

44

6.3 Supporting the full adoption of IFRS

• Current Status of the IFRS Adoption: 32 standards are already published in Royal Government Gazette; 18 draft standards are interpreted, and a few are under review by the Federation of Accounting Professions.

• Challenges of the full adoption:

• According to section 34 of the Accounting Professionals Act B.E.2547, the accounting standard must be made in Thai language, however, the translation of IFRS has proved to be a lengthy and resource-intensive process.

• Some requirements of IFRS are impracticable.

• A few countries have also encountered the translation issue. They have therefore declared that the full adoption must be conformed to the promulgation procedures in that country.

• Possible Solutions

• Request the Federation of Accounting Professions to consider the full adoption to be conformed to the promulgation process.

• Prepare the full adoption guidance for listed companies.

• Provide communication channels, such as C1 IOSCO for sharing experiences and obstacles to the full adoption.

6. Continuously Improving Information Disclosure

45

7. Increasing Enforcement's Efficiency and Effectiveness

• Improve RPT and acquisition/divestiture rules with emphasis on the board‟s roles and opinions as preventive measures for wrongdoing.

• Develop an alert system to monitor more promptly any possible wrongdoing.

• Improve the SEC‟s market surveillance system.

Monitor& Prevent

Wrongdoing

• Improve evidence management system.

• Co-operate with other financial regulators and other law enforcement agencies.

Inspection of Offences

• Utilise measures under the Anti-Money Laundering Act to increase effectiveness and expedite enforcement process.

• Consider leveraging untrustworthy characteristics of directors as minimum sanction on top of the normal criminal proceedings.

• Closely co-operate with related agencies.

LegalProceedings

• Consider utilising the Stock Exchange‟s authority stated in the sections 172 -175 of the Securities and Exchange Act.

• Expedite the amendment process, and add sections on civil sanction, elements of offence, and evidence.

AppropriatePunishment

• Improve disclosure of enforcement information in press release and on the SEC‟s website. Ensure its accessibility and straightforward and concise contents (the OECD will publish some guidelines in 2014).

• Consider disclosing enforcement on „director, company, and management criminal and administrative sanctions‟ in a package to foster compliance and culture in companies.

Communicateto the Public

46

Background/ Rationale

• Given the SEC has required listed companies to adhere to CG, CSR in-process and anti-corruption policies and practices, the SEC must also adhere to the same requirementsin order to strengthen its role as a sustainable organisation. However, to ensure appropriateness of good governance for the SEC, the Public Sector‟s Good Governance principles should also be considered.

• As an important enabler of the capital market, the SEC should continuously develop itself into a sustainable organisation in order to achieve its core mission in supporting the sustainability development of the capital market.

• In 2012, the SEC initiated a policy to publish an SD report. The SEC itselfattempted to publish its own SD report by adopting the GRI guidelines. During the report preparation process, it was found that:

– the SEC‟s operational processes are actually considered as „CSR-as process‟ activities. However, many of these activities have not been systematically rationalised for coherent operational processes and understanding throughout the organisation.

– experts in the field have given feedbacks that the report should contain one key element of SD, which is the analysis of the impacts of the ESG factors on stakeholders, and how to incorporate these factors into the strategic plan formulation process in order to meet the stakeholders‟ requirements.

– some of the SEC‟s operational processes and activities are in themselves socially responsible processes. However, appropriate KPIs for performance measurement and improvement are not identified for many of these activities.

8. Building SEC as a Sustainable Organisation

47

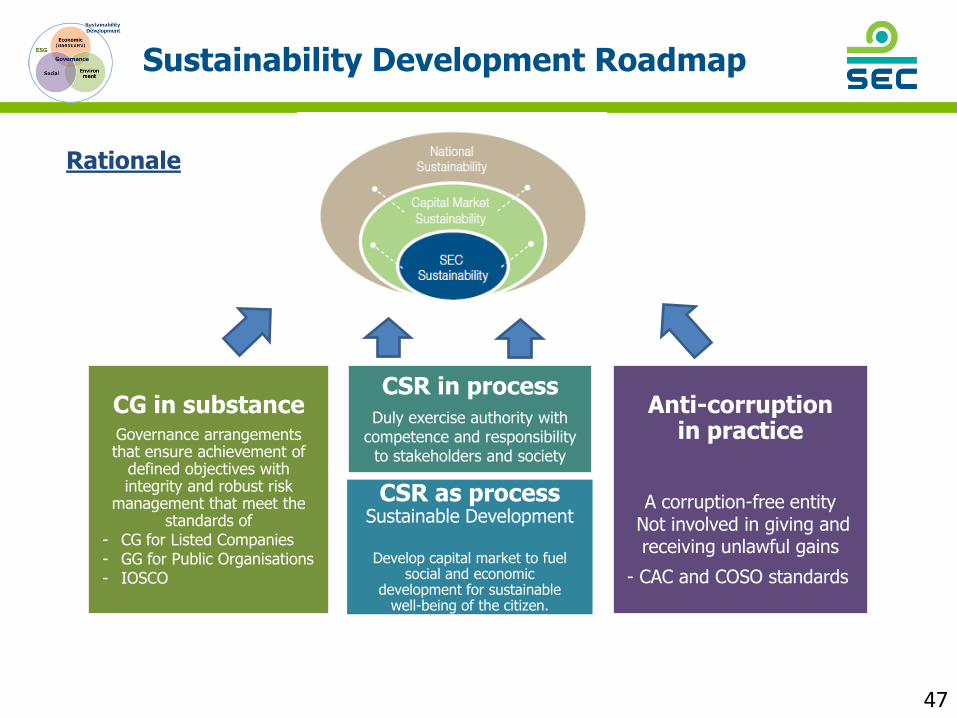

Sustainability Development Roadmap

CG in substanceGovernance arrangements that ensure achievement of

defined objectives with integrity and robust risk

management that meet the standards of

- CG for Listed Companies- GG for Public Organisations- IOSCO

CSR in processDuly exercise authority with

competence and responsibility to stakeholders and society

Anti-corruption in practice

A corruption-free entity Not involved in giving and receiving unlawful gains

- CAC and COSO standards

CSR as processSustainable Development

Develop capital market to fuel social and economic

development for sustainable well-being of the citizen.

Rationale

48

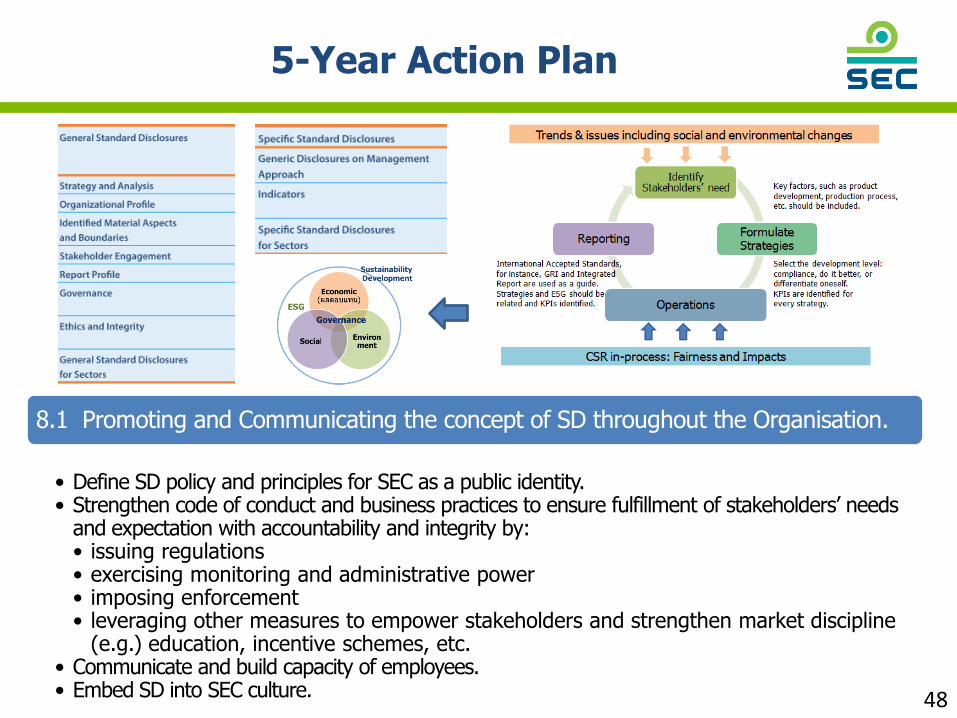

5-Year Action Plan

8.1 Promoting and Communicating the concept of SD throughout the Organisation.

• Define SD policy and principles for SEC as a public identity.• Strengthen code of conduct and business practices to ensure fulfillment of stakeholders‟ needs

and expectation with accountability and integrity by:• issuing regulations• exercising monitoring and administrative power• imposing enforcement• leveraging other measures to empower stakeholders and strengthen market discipline

(e.g.) education, incentive schemes, etc. • Communicate and build capacity of employees.• Embed SD into SEC culture.

49

5-Year Action Plan

8.2 Reviewing SEC‟s governance framework

• Update CG codes for SEC to ensure consistency with international standards for CG, SD framework, good governance for public sector and other Thai governance standards.

• Revise codes of conduct for commissioners and officers to heighten the standards on

• managing conflicts of interests

• receiving and offering gifts (already completed)

8.3 Ensuring a corruption-free entity

• Conduct corruption risk assessment by using the CAC‟s anti-corruption procedures to improve the SEC‟s procedures to ensure good practices beyond corporate standard.

• Review procurement rules and practices to ensure efficiency and compliance with government standard.

• Report annual progress and outcome, based on GRI‟s anti-corruption indicators.

Anti-Corruption KPIs (refer to the GRI)• Percentage and total number of business units analysed for risk related to corruption.

• Key corruption risks. • Percentage of directors, executives, employees and suppliers acknowledged and trained in organisation‟s

anti-corruption policies and procedures.• Actions taken in response to incidents of corruption, such as terminate a contract with a corrupt supplier.