Sustainability and the Dynamics of Green Building Nils Kok UC Berkeley Maastricht University John M....

19

Sustainability and the Dynamics of Green Building Nils Kok UC Berkeley Maastricht University John M. Quigley UC Berkeley Piet Eichholtz Maastricht University European C to C Network, July 2010

-

Upload

ariel-mcallister -

Category

Documents

-

view

221 -

download

1

Transcript of Sustainability and the Dynamics of Green Building Nils Kok UC Berkeley Maastricht University John M....

Sustainability and the Dynamics of Green Building

Nils KokUC Berkeley

Maastricht University

John M. QuigleyUC Berkeley

Piet EichholtzMaastricht University

European C to C Network, July 2010

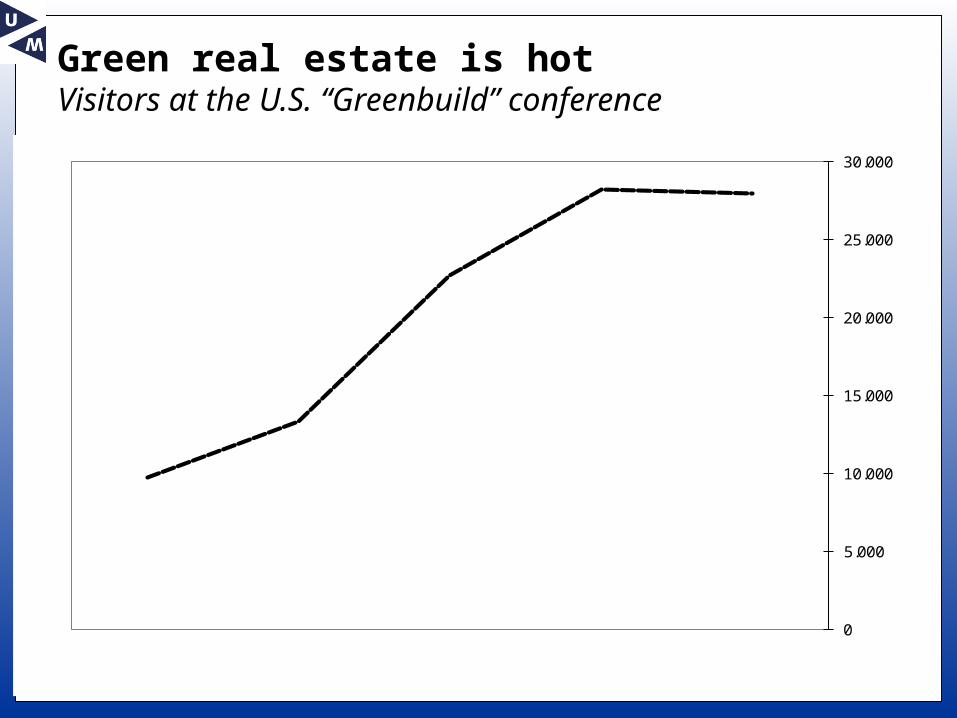

Green real estate is hotVisitors at the U.S. “Greenbuild” conference

0

5.000

10.000

15.000

20.000

25.000

30.000

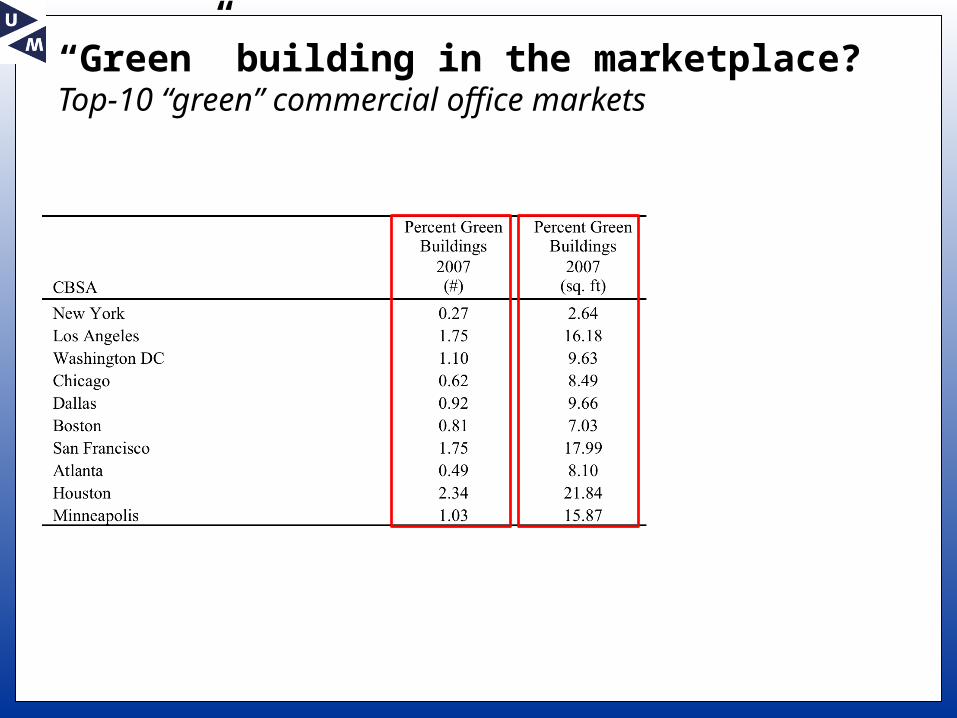

“Green” building in the marketplace?Top-10 “green” commercial office markets

Economic significance of “green” buildingImplications upon the market for commercial space

Trends in “green” building may have economic implications

A higher initial outlay… Not clear how much higher (0 – 20%) ‘Smarter’ building managers/software

… may be compensated by “green” value drivers Cost savings

Energy savings (up to 35%) Emission reduction

Increased rents Reputation effects Improved indoor air quality

Increased economic lives, reduced depreciation

Case studies on the economic implications Focus often on new buildings Results are hard to generalize

Do we still see economic effects of green label?Investment dynamics and the source of green increments

Sample of 28,000 office buildings (2009 cross section), 3,000 of which are certified by EPA or USGBC

1. New evidence on the economic premium for green office buildings Rigorous control for quality differences (PSM) Label vintage

2. Identify the sources of rent and value increments Explicit link to

USGBC measures of “sustainability” EPAs measures of energy efficiency

Example: 101 California St, San FranciscoEnergy Star certified, LEED Gold

Example: 101 California St, San FranciscoEnergy Star certified, LEED Gold

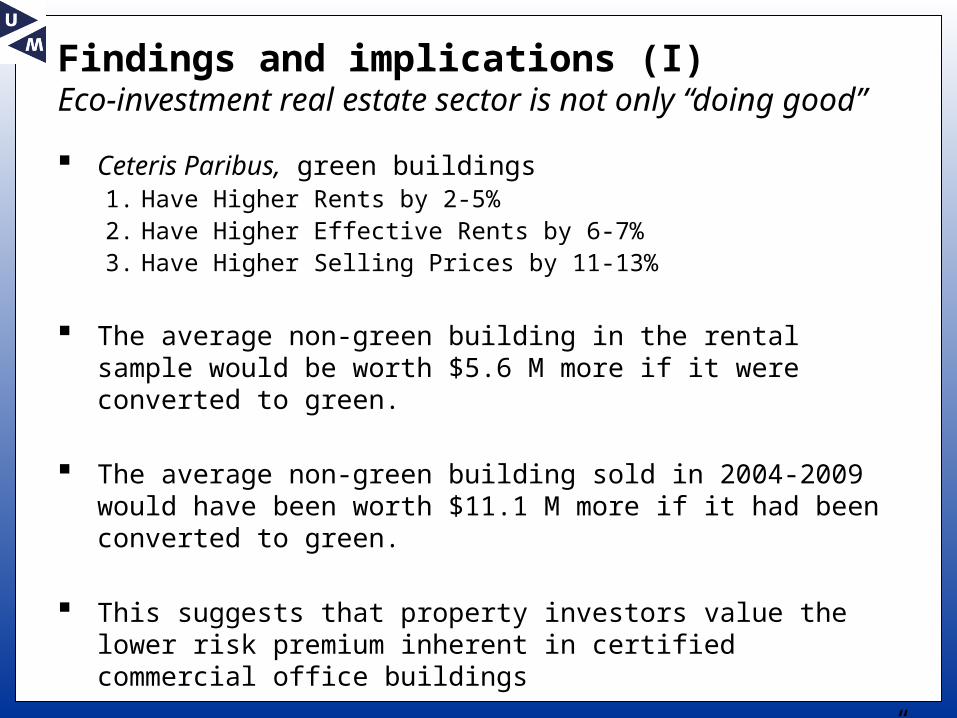

Findings and implications (I)Eco-investment real estate sector is not only “doing good”

Ceteris Paribus, green buildings1. Have Higher Rents by 2-5%2. Have Higher Effective Rents by 6-7%3. Have Higher Selling Prices by 11-13%

The average non-green building in the rental sample would be worth $5.6 M more if it were converted to green.

The average non-green building sold in 2004-2009 would have been worth $11.1 M more if it had been converted to green.

This suggests that property investors value the lower risk premium inherent in certified commercial office buildings

The missing piece…what are the costs of “greening” properties?

Generalization of the modelUnique premium for each “green” building

The increment to rent or market value for the green building in cluster n, relative to the prices of other buildings in that cluster (i.e., controlled for location, climate, and quality):

What is the relation between the variation in the “green” premium and the LEED-score or energy consumption?

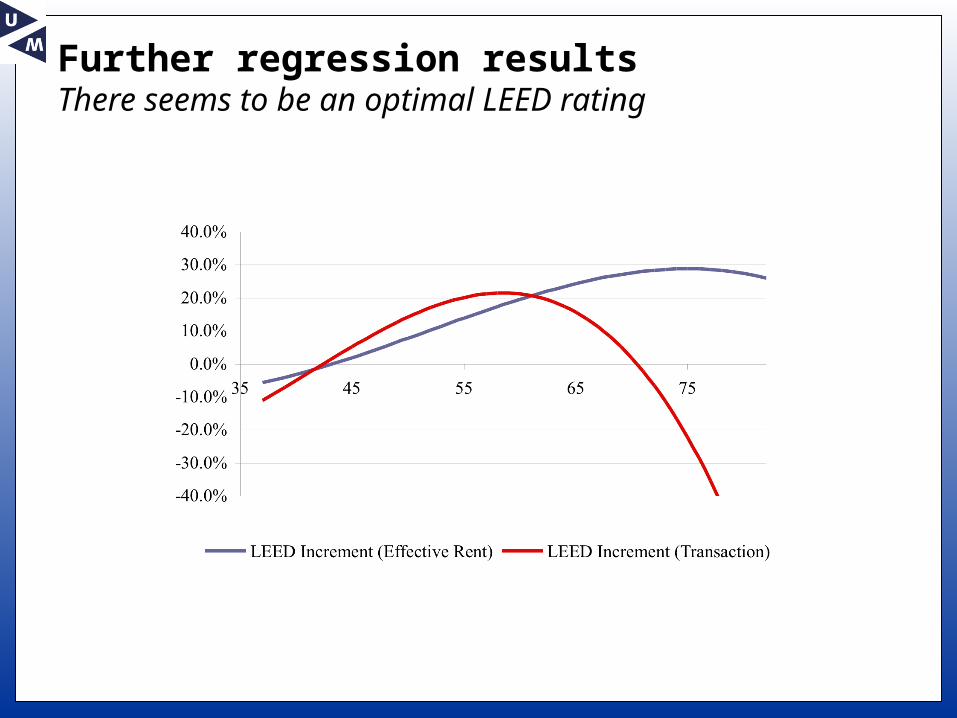

Further regression results There seems to be an optimal LEED rating

Information on Energy Star-rated buildingsEmissions are substantial, and energy savings create value

Average emission of a building in our sample: 4,326 tons of CO2 750 cars, 9,000 barrels of oil, … Energy Star-rated buildings emit at least a quarter less carbon

as compared to conventional office buildings A $1 saving in energy costs is associated with an increase in

effective rent of 95 cents A $1 saving in energy costs is associated with a 4.9 percent

premium in market capitalization, which is equivalent to $13/sq.ft. This implies a cap rate of about 8 percent

Conclusions and implications (II)LEED and Energy Star labels seem to be complimentary

The green increment is systematically related to the underlying characteristics of energy efficiency or “sustainability”

Market seems to be relatively efficient in pricing these aspects

LEED and Energy Star measure somewhat different aspects of “sustainability” and complement each other

Low correlation between LEED-score and EUI-score

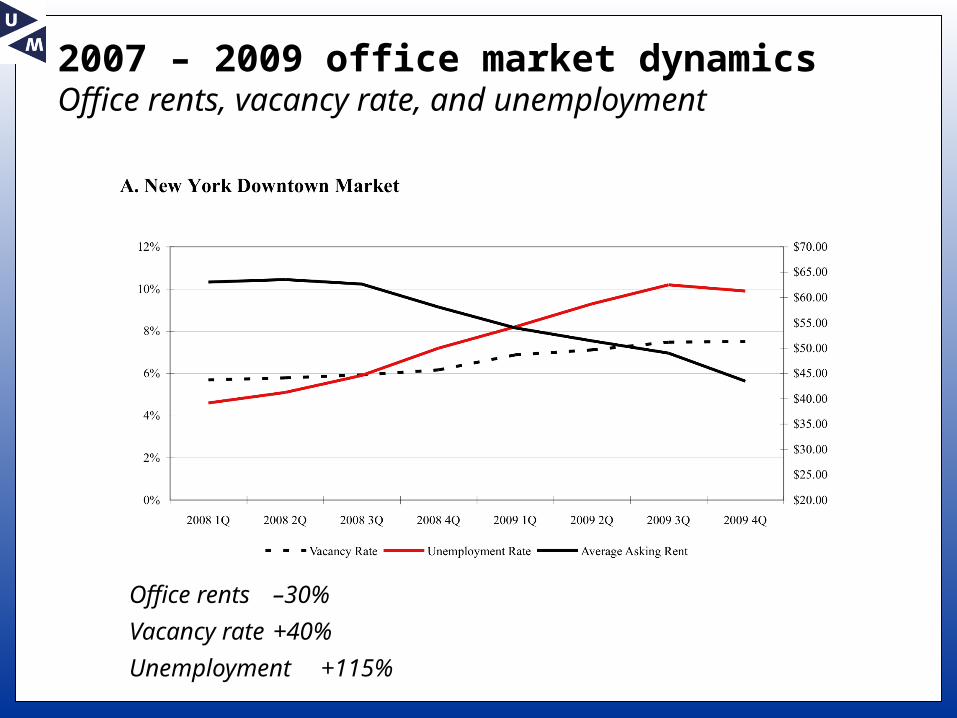

2007 – 2009 office market dynamicsOffice rents, vacancy rate, and unemployment

Office rents –30%

Vacancy rate +40%

Unemployment +115%

2007 – 2009 office market dynamicsOffice rents, vacancy rate, and unemployment

Unemployment x 2

Office rents –30%

Vacancy rate +30%

Short-run price dynamics of green buildingsSubstantial increase in rated space in a contracting economy

8,182 observations as of September 2007 694 rated buildings and 7,488 nearby control buildings Rents, occupancy rates, effective rents

Same sample matched to financial information in October 2009 Drop buildings that were converted to “green” during the sample period

We estimate developments in rents, occupancy rate, effective rents

Conclusions and implications (III)“Green” is getting mainstream

Increased awareness of global warming and the role of the real estate sector have increased attention upon “green” building

Energy efficient and sustainable office space is now a large share of the commercial property sector -- getting mainstream

This may have economic implications for investors, tenants, and policymakers

Buildings certified by Energy Star or LEED command higher rents and prices in the marketplace

The “green premium” has slightly decreased during the period of volatility in property market…

…but the returns to green buildings are not significantly lower relative to identical conventional buildings

So what do property investors do?Property investors talk the talk, but hardly walk the walk

0

20

40

60

80

100

Impl

emen

tatio

n &

Mea

sure

men

t

0 20 40 60 80 100

Management & Policy

GreenWalk Green Stars

Green Laggards GreenTalk

Questions/remarks?

www.corporate-engagement.com