Supreme industries initiating coverage

26

COMPANY RESEARCH REPORT INITIATING COVERAGE SUPREME INDUSTRIES LIMITED RECOMMENDATION: BUY CMP: Rs. 144 1st TARGET: Rs. 230 2nd TARGET: Rs. 244 HOLDING PERIOD: 1 – 2 Years RISK PROFILE: AGGRESSIVE 2010

description

Equity Research report by Hedge Equities Limited.

Transcript of Supreme industries initiating coverage

COMPANY RESEARCH REPORT October 28, 2010

COMPANY RESEARCH REPORT INITIATING COVERAGE

SUPREME INDUSTRIES LIMITED

RECOMMENDATION: BUY

CMP: Rs. 144

1st TARGET: Rs. 230

2nd TARGET: Rs. 244

HOLDING PERIOD: 1 – 2 Years

RISK PROFILE: AGGRESSIVE

2010

BUSINESS SUMMARY

Supreme Industries Limited (SIL) is one of the largest plastic processing companies in India, processing over two lakh metric tonnes of plastic per annum. The company’s core operations involve processing polymers and resins into plastic products which are quote diversified and spread over four broad product categories namely: - Piping products, Industrial products, Consumer products and Packaging products.

INVESTMENT RATIONALE/RISKS

SIL is involved in an industry that is extremely under-penetrated, fragmented and dominated by the unorganized sector and thereby offering tremendous scope for a large and organized player the potential to stake a claim and scale up their operations. The company has put in place a well thought out and rigorous strategy that is due to play out all the way until 2015.

SIL has a fantastic distribution network, diversified and vast product offerings, a superior brand image and is very well positioned across India (SIL possesses 19 manufacturing units that are spread out across the four key zones across India).

The next two years (most notably the current year) will see SIL generate revenue through its non-core construction business which is likely to be a crucial EPS booster.

Both the historical financials and the forecasted financials of SIL over the next two years paint a very healthy picture of the firm, be it earnings growth rates, ever-increasing margins, best-in-class ROE and ROCE, cash flow position, debt levels, strength of the balance sheet and dividend payouts.

Risks include the possible volatility in PVC resin prices (crucial component in the manufacture of piping products) and rising crude oil prices (the prices of polymers such as polyethylene, polypropylene are closely tied to crude oil prices. The other major risk is the valuation (exemplified by the trailing PE ratio) which is just a tad lower than the industry average. Institutional participation in the stock too is relatively lower and significant outperformance may depend on renewed institutional appetite.

(In crores) JUN-09 JUN-10 JUN-11E JUN-12E

SALES 1654.94 2007.02 2616.74 2928.77

PAT 94.34 142.08 259.50 335.46

EPS 7.42 11.18 20.42 26.40

PE 19.38 12.87 7.04 5.45

Source: Multiple Sources

0.0050.00100.00150.00200.00

0.005000.00

10000.0015000.0020000.0025000.00

29

-Dec

-09

29

-Ja

n-1

0

28

-Feb

-10

31

-Ma

r-1

0

30

-Ap

r-1

0

31

-Ma

y-1

0

30

-Ju

n-1

0

31

-Ju

l-1

0

31

-Au

g-1

0

30

-Sep

-10

31

-Oct

-10

30

-No

v-1

0

Sensex vs SIL

SENSEX SIL

50%

0%4%

46%

SIL's SHAREHOLDING PATTERN AS AT SEP 2010

PROMOTER DII FII OTHERS

Sector: Plastic EPS (TTM): Rs.13.01 PE (TTM): 11.17 Industry PE: 12.29 Mkt. Cap: 1829.19 52 Wk high: Rs. 169.90 52 Wk low: Rs. 71.00 P/BV: 4.84 Beta: 0.45 Yield (%): 2.50 Face Value: 2.00 Debt/Equity: 0.78 Institutional: 4.56 %

NSE Code: SUPREMEIND

BSE Code: 509930

ISIN Code: INE195A01028

Reuters Code: SUPI.BO

Bloomberg Code: SI IN

Website:

www.supreme.co.in

COMPANY RESEARCH REPORT December 30, 2010

Contents

BRIEF PROFILE .............................................................................................................................................................................. 2

COMPANY ADDRESS................................................................................................................................................................. 2

TOP MANAGEMENT ................................................................................................................................................................. 2

BUSINESS ...................................................................................................................................................................................... 3

SECTOR ......................................................................................................................................................................................... 7

OUTLOOK AND SCOPE .................................................................................................................................................................. 9

FINANCIALS AND VALUATIONS .................................................................................................................................................. 13

HISTORICAL FINANCIALS ........................................................................................................................................................ 13

FINANCIAL OUTLOOK ............................................................................................................................................................. 14

RISKS ........................................................................................................................................................................................... 16

INVESTMENT RATIONALE ........................................................................................................................................................... 17

FINANCIAL HIGHLIGHTS -CONSOLIDATED.................................................................................................................................. 20

FINANCIAL RATIOS -CONSOLIDATED .......................................................................................................................................... 21

FINANCIALS GRAPH AND PEER GROUP COMPARISON .............................................................................................................. 22

ANALYST NOTES AND COMPANY NEWS .................................................................................................................................... 23

COMPANY RESEARCH REPORT December 30, 2010

2

BRIEF PROFILE

Supreme Industries Limited (SIL) is one of the most

prominent plastic manufacturing companies in India,

having been set up in 1942, and having over 44 years

of experience under the current management. The

company is today one of the largest plastic processing

companies in India, processing over 2 lakh metric

tonnes of plastic per annum. The company’s core

operations involve processing polymers and resins

into plastic products, which are quite diversified and

spread over four broad product categories namely:-

Industrial Products, Consumer Products, Piping

Products and Packaging Products. SIL is credited with

pioneering various products in the industry which

include Cross- Laminated Films, HMHD Films,

Multilayer Films, SWR Piping Systems, PP Mats and

more. SIL has two subsidiaries. The company has a

29.88% stake in Supreme Petrochem Limited (SPL)

which is involved in the manufacture of polystyrene,

expanded polystyrene, extruded polystyrene boards

and compounds of polystyrene and polyolefins. SPL is

the largest exporter of polystyrene (PS) from India

exporting to over 80 countries across the globe. SIL

also enjoys a 100% stake in Supreme Industries

Overseas (FZE) which is located in the United Arab

Emirates (UAE). Another element of strength

associated with SIL is the fact that it is extremely well

spread out across the country. This subsidiary has

enabled SIL to have a product presence in 21

countries. The company has 19 manufacturing

locations across all the key zones of India (North,

South, West, East and Central India).

COMPANY ADDRESS

Supreme Industries Limited,

E-2, Ansa Industrial Estate,

Saki Vihar Road,

Saki Naka,

Andheri (E),

Mumbai- 400072

TOP MANAGEMENT

1. Chairman – B L Taparia

2. Managing Director – M P Taparia

3. Director – B V Bhargava

4. Director – H S Parikh

5. Director – N N Khandwala

6. Director – S R Taparia

7. Director – Y P Trivedi

8. Executive Director – S J Taparia

9. Executive Director – V K Taparia

COMPANY RESEARCH REPORT December 30, 2010

3

BUSINESS

Supreme Industries

Limited (SIL) is involved

in the business of

processing polymers and

resins into finished

plastic products which

are broadly spread across

four product categories

namely Industrial

Products, Piping

Products, Consumer

Products and Packaging

Products. Of the four

product segments, piping

products are the largest

contributor to the top-

line having contributed

around 43.5% in both

2009 and 2010. It is

followed by the Packaging Product segment, the

Industrial Product segment and the Consumer

Product segment that have contributed on average

24%, 20% and 12% to the top line in the last two

years. SIL also has a marginal exposure to the

construction sector, a story which is expected to play

out until December 2011.

Piping Products

SIL is considered to be the leader in the plastic piping

segment with its products being using in 19 different

applications. The company enjoys an 18% market

share in the organized domestic plastic piping

segment in India and in the broader piping segment

market in India valued at Rs.1000 crore, the

company was able to secure a 7.3% market share in

2009-10. In fact the popularity of SIL’s piping

products are not just limited to India alone and have

garnered a good response

in territories such as the

UK, Australia and New

Zealand. Some of the key

applications where the

company’s piping

products are used include

the field of irrigation,

water transportation,

industrial usage,

infrastructure

requirements, borewell

applications, the building

industry, sewerage

industry and rain water

harvesting. The key piping

product of Supreme

includes UPVC Pipes,

Injection Moulded

Fittings, Polypropylene

Copolymer Pipes and Fittings, HDPE Pipe Systems,

CPVC Pipe Systems, LLDPE Tube and Inspection

Chambers. SIL has introduced various pioneering

productas in this segment which include SWR

Drainage System, Acqu Gold High Pressure Plumbing

System, Indo- Green PP-R-hot and cold water

system, Eco-Drain structured wall hi-tech pipes and

Nu-drain underground drainage system. The

company recently introduced the sprinkler system in

several states (which is essentially devised using

polyethylene pipes) and this is one item that is

expected to be a key driver in the coming years as

the volume of polyethylene pipes had grown by

close to 100% volume on a y-o-y basis. Another

product that stands out in the piping product

segment of SIL is the company’s lead free “Aqua

Business Vertical Product Portfolio

Targeted Customer Segment

Plasic Piping System

uPVC Pipes, Injection Moulded fittings, Handmade fittings, Polypropylene Random, Co-polymer Pipes & Fittings, HDPE Pipe Systems, CPVC Pipes Systems, LLDPE Tube and Inspection Chambers

Portable Water Supply, Irrigation, Drainage & Sanitation Housing

Consumer Products Furniture and Mats

Retail Stores and Exports

Industrial Products

Industrial Component, Material Handling Products (Crates, Pallets and Dustbins)

Auto Sector, Electronic Appliances, Water Purification, Soft Drink Companies, Agriculture & Fisheries

Packaging Products

Specialty Films, Protective Packaging products, Cross Laminated Films

Electronics, Food Industry, Sports Goods, Insulation, Construction, Agriculture, Floriculture, Horticulture, Grain Storage Tarpaulin

COMPANY RESEARCH REPORT December 30, 2010

4

gold” plumbing system that carries cold water. This

product has been successful in replacing the GI pipes

(Galvanized Iron) in the housing industry as the cost

of production is 50% less and enjoys far superior

durability. The company is also a very prominent

manufacture of PVC pipes that are fast becoming the

preferred mode of piping over the traditional forms.

The advantages that PVC pipes has over the other

pipes include a greater life span without any loss of

strength, being lightweight and hence reduction in

transportation costs, as well as ease of installation.

Source: Company

Consumer Products

SIL’s consumer products include furniture and mats.

The company is considered to be the second largest

player in the plastic moulded furntiture with a

manufacturing capacity of 21700MT. Of the Rs.1100

crore valued market, SIL was able to garner a market

share of 13% in 2009-2010. The company’s vast

range of plastic furniture can be divided into eight

sub categories, namely Upholsters, Premium

monoblock chairs, monoblock chairs, Armless chairs,

Centre tables & trolley, Dining tables, Baby chairs

and Stools. Another distinct feature of SIL’s furniture

manufacturing expertise lies in the fact that it is

made using 100% virgin polymers, using computer

designed moulds at their various ISO certified plants.

SIL also enjoys the distinction of pioneering

lacquered and upholstered moulded plastic furniture

in India and also being the first to utilize high end

injection moulding technology in their

manufacturing process. The company’s strategy in

the future includes focusing on the lacquered

segment and premium furniture products. Recently

the company introduced a designer chair called

“DIVA” that has been very well accepted by the

market due to its inbuilt metal legs that provides

stability, gas moulded plastic seats that provides

strength and transparent back that provides

aesthetic beauty.

In order to sell its furniture items SIL has set up 209

exlusive franchise show rooms all across India and

will be ramping up their showroom strength to 300

units in the current year.

SIL’s mats segment hasn’t been doing particularly

well as a considerable proportion of the final

products are exported to countries abroad and that

segment was badly hit during the recession era. The

mats segment of SIL is still in a process of

convalescence. However the management is

confident of turning things around in this segment

and believes that the future bodes well for this

segment as most of the economies are beginning to

come out of the woods.

Industrial Products

Under this broad product segment SIL manufactures

industrial components and material handling

products. The estimated market size of the material

handling segment is Rs.560 crores and SIL enjoys an

18% market share. The company’s material

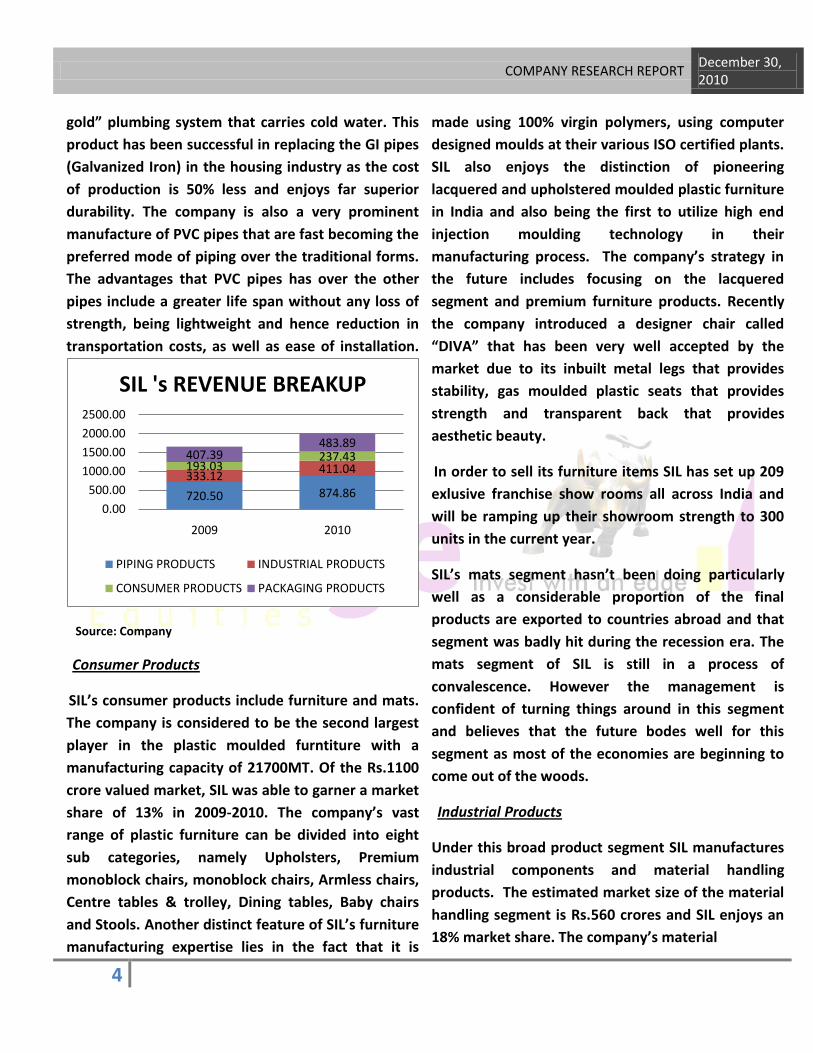

720.50 874.86

333.12411.04193.03237.43407.39483.89

0.00

500.00

1000.00

1500.00

2000.00

2500.00

2009 2010

SIL 's REVENUE BREAKUP

PIPING PRODUCTS INDUSTRIAL PRODUCTS

CONSUMER PRODUCTS PACKAGING PRODUCTS

COMPANY RESEARCH REPORT December 30, 2010

5

handling and storage product range is extremely

comprehensive, from small Bins to Super Jumbo

Crates, Injection

Moulded and Roto

Moulded Pallets,

Injection moulded and

Roto moulded Garbage

bins. The company’s

material handling

equipment are used in a

whole host of industries

ranging from the

electronic industry,

engineering industry,

automotive industry,

textile industry, fisheries,

fruits and vegetable

handling, soft drinks

handling, dairy products

handling and more. Of all

these industries, SIL’s

material handling

equipment are perhaps

most popular in the soft

drinks industry where

the company is

considered to be the

largest supplier of crate

equipment and related

matter in the country.

Recently SIL has been manufacturing value additive,

tailor made crates that are fast replacing the

conventional and standard crates. Another industry

in which SIL’s industrial products enjoy a degree of

popularity is the auto industry. The company

supplies various body parts for illustrious auto

makers such as Tata Motors and Maruti Suzuki. SIL

has been striving to become a tier 1 supplier in the

auto industry by associating itself with suppliers

right from the

conceptualization stage.

Body parts are also

provided for various

electrical appliance

manufacturers in the

country and Whirlpool is

one of SIL key clients.

Earlier in the year SIL was

able to secure a rather

prestigious project from

Tata Chemicals for the

manufacture of water

purifiers called Tata

Swach and the reasoning

for Tata selecting SIL was

due to the latter’s

admirable geographical

spread across India.

Packaging Products

SIL’s packaging

products are categorized

as Specialty Films,

Protective Packaging

Products and Cross

Laminated Films. The

products manufactured in

this division are most often

utilized for packaging purposes, construction

purposes and insulation purposes. As is the case in

the most of its other product segments, SIL has

introduced various path-breaking technologies in the

country such as Instant Polyurethane Foams,

Reticulated foam for air filtration, Sound absorbing

SIL’S MANUFACTURING UNITS

Sr. No. Unit Location Piping

Products Industrial products

Consumer Products

Packaging Products

1 Jalgaon

(Maharashtra) YES

2 Noida (Uttar

Pradesh) YES

3 Pune

(Maharashtra) YES

4 Halol

(Gujarat) YES

5 Malanpur (Madhya Pradesh)

YES

6 Raigad

(Maharashtra) YES

7 Hosur

(Karnataka) YES

8 Pondicherry

(Union Territory)

YES YES

9 Silvassa (Union

Territory) YES

10 Khushkhera (Rajasthan)

YES

11 Derabassi (Punjab)

YES YES

12 Durgapur

(West Bengal) YES YES

13 Kanpur (Uttar

Pradesh) YES

14 Guwahati (Assam)

YES

15 Jalgaon I

(Maharashtra) YES YES YES YES

16 Urse

(Maharashtra) YES

17 Jalgaon II

(Maharashtra) YES

18 Malanpur (Madhya Pradesh)

YES

19 Sriperumbdur (Tamil Nadu)

YES

Source: Company

COMPANY RESEARCH REPORT December 30, 2010

6

open cell foam, High temperature and File Resistant

Melamine Foam. SIL also has the distinction of being

the only Indian company to have the technology to

manufacture XF films under the brand name of

Silpaulin. Silpaulin is used in agricultural

applications, civil engineering applications,

packaging application, export marketing and general

application purposes.

In the previous fiscal the company’s collaborators

had developed the Cross Line Bonded Films which is

essentially a next generation XF film with superior

properties. SIL has been granted Indian patents uptil

2023 and also enjoys the exclusive right to produce

the same, in India & SAARC

Countries, as well as the right to

export the product to all the

countries in the world, except

Portugal, Spain and

Switzerland. In the last fiscal

there was another interesting

development for the packaging

product segment as the

company’s Khopoli

manufacturing unit was able to

procure the BRC (British Retail Consortium)

Certificate, thereby making in the First Multilayer

Packaging company in India to receive this

certification. An admirable facet of this product is

that since it is a flat product it is not freight

intensive. This first mover advantage will enable the

company to tap the European Marketand the

company has already been in touch with various

companies that have been scouting for materials

that have the BRC certification.

Construction Business

SIL has established a 11 storied state-of-the-art

commercial complex in Andheri, Mumbai called

Supreme Chambers. The complex was designed by

Sanjay Puri who is considered to be one of India’s

leading architects. SIL is now looking to sell 2,75,000

square feet of the project and in fact has already

been successful in selling about 40,000 square feet

and raising Rs.60.20 crore through that sale. The

management is now looking to sell the entire

complex except one floor and is looking to achieve

sale closure by December 2011, with a sales target of

Rs.375 crore. There has been no clarity on whether

this construction activity of

Supreme is just a one-off, or

something that the company will

continue to look at in the future

as well.

Research & Development

For a company that is involved in

the business of churning out

pioneering products on a

consistent basis, one would

expect SIL to have a strong R&D culture and the

company doesn’t disappoint on that front. The

company’s R&D centre is located in Mumbai and

undertakes CAD (Computer Aided Design), CAM

(Computer Aided Manufacture) and CAE (Computer

Aided Engineering) related projects, particularly for

engineering and fabricating intricate moulds and

dies. Before the product is sent out for commercial

manufacture, an evaluation of the product is done

by simulating the prospective performance of the

product. Product development teams at all Supreme

Divisions work in synergy with the Centre, to

effectively turn specific customer requirements into

SUPREME CHAMBERS- A LUCRATIVE AVENUE

FOR SIL

2,75,000 sq.feet to be sold for

Rs.375 crore.

Project cost- Rs. 155 crore.

40,000 sq.feet already been sold

for Rs.60.20 crore.

Sale to fructify by December

2011.

COMPANY RESEARCH REPORT December 30, 2010

7

precisely tailored products. In addition to the in-

house R&D Centre, SIL has also collaborated with

global partners in places such as Switzerland,

Belgium, Japan and Korea to develop a whole host of

products, most notably in its packaging products

segment.

SIL’S R&D COLLABORATIONS

COMPANY PRODUCT LINE

Rasmussen Polymer

Development,

Switzerland

Cross Laminated Films

Sapac Packaging

Solution, Belgium

Instant Packaging Solution

Foam Partner,

Switzerland

Reticulated PU Foam

Sanwa Kako, Japan 2 Stage Foam

PE Tech, Korea Cross Linked Foam

Source: Company

SECTOR

The origins of the Indian plastic industry extend all

the way back to 1957 which was the year which saw

the modest and promising beginning of the

production of Polystyrene, which is essentially a

polymer (Polymers are further processed and refined

to produce plastic). In the initial phases, the plastic

was manufactured using natural and synthetic

materials of different forms, attributes and

appearances. However with time, organic

compounds (materials containing carbon, hydrogen

and other elements) were preferred as ingredients

over natural and synthetic materials. Economic

liberalization from 1991 stimulated the Indian plastic

industry even further, as joint ventures, foreign

investments and easier access to technology from

developed countries began to unfold.

India plastic manufacturers today are proving to be

quite popular on

the global front.

While the

qualities of

finished goods

are quite

superior, what

actually swings it

in the Indian

plastic

manufacturers’

favour is the cost

of production.

Production costs

in India are

estimated to be

20-25% lower

than in the US.

Some of the

characteristics

that are utilized

to describe the

Indian plastic

industry today is

that it is highly

fragmented,

under penetrated

and possesses a

highly dominant

unorganized

sector. Per capita

consumption of

plastic and

polymers in India

leaves much to

be desired in comparison with the world levels. Even

INDIAN PLASTIC

SECTOR HIGHLIGHTS The Indian plastic industry

is characterized by

fragmentation, under-

penetration and the

domination of the

unorganized sector.

Indian plastic

manufacturers are noted

for their low cost expertise.

Plastic consumption in

India in terms of volume

grew by 16% last year.

However India’s plastic

consumption is just 1/5th of

the world average.

Polymer production is

expected to rise in the

current year thereby

allaying fears of raw

material shortage for

domestic players.

Going forward, government

initiatives such as the

Jawaharlal Nehru National

Urban Renewal Mission

and the Housing and Urban

Poverty Alleviation

programe are expected to

boost the fortunes of plastic

piping manufacturers in

India.

COMPANY RESEARCH REPORT December 30, 2010

8

though plastic consumption in India, in volume terms

grew by 16% (yoy) in the last fiscal, to reach 8 million

tonnes, the quantum of consumption in relative

terms is extremely low. To put things into

perspective, India’s consumption of plastic is just

1/5th of the world average. The per capita polymer

consumption stood at a lowly 5.66 kgs. In the US that

figure stood at 71.46 Kgs., while China and Brazil

posted figures of 30.74kgs and 22.71 kgs. However

there is tremendous scope for growth, as the current

consumption level of 8 million tonnes is expected to

double to 16 million tonnes by 2018 and reach 20

million tonnes by 2020.

The cost of raw materials too are not expected to be

a huge impediment in the near term as the

domestic supplies of polymer are expected to

increase and hence serve as a boon for the polymer

processors such as SIL. The expanded capacity of

the PP (Polypropylene) plant of Reliance Industries

Limited at Jamnagar began production earlier in the

year. Another major manufacture of polymers-

Haldia Chemicals too increased the capacities of its

PP (Polypropylene) and PE (Polyethylene) units in

West Bengal. If there is a risk however it is the rising

crude oil prices as it is a key ingredient in the

manufacture of polymers.

While the under-penetration of plastics in India is

quite evident there also exists a number of key

growth drivers that are likely to help bridge the

level of under-penetration in the country and

provide a fillip to the plastic manufacturers in India.

And these growth factors extend across all four of

SIL’s broad product segments. SIL ‘s piping product

segment is likely to see significant traction due to

the government’s thrust on irrigation facilities and

urban sanitation. Under the Jawaharlal Nehru

National

Urban

Renewal

Mission

(JNNURM),

the Central

Government

has given a

special focus

to improve

the

infrastructur

e of 91 cities

from 63

citiers and

towns as

announced

earlier in the country. Under this scheme the

government has budgeted Rs. 11619 crore in FY11

to improve drinking water supply and solid waste

management. In addition to that the government

has budgeted another Rs.1000 crore for Housing

and Urban Poverty Alleviation in FY11.This will

increase the market for plastic piping systems as

real estate developers go about their business. PVC

plastic pipes are fast turning out to the preferred

piping system across the world with China being

one of the biggest propagators of this product. PVC

pipes

Increasing urbanization, improving lifestyles in

semi-urban and rural segments and a pickup in

consumer sentiment in the export markets are

likely to aid the consumer product segments in the

near term. The industrial products division will be

looking to strong growth drivers in the auto

industry and the soft drink industry which are the

biggest users of SIL’s industrial products and

LESS-PUBLICIZED MERITS OF PLASTIC

Plastic has a strong utilitarian value in road construction activities saving 5-10% of bitumen costs per kilometer.

Contrary to the general perception, plastic can actually be recycled into non-critical items of daily use.

Usage of plastic over metals in automobiles reduces CO2 emissions by 50 mmt per year for the automobile sector globally.

COMPANY RESEARCH REPORT December 30, 2010

9

material handling equipment. The packaging

segment as well is bound to prosper due to

increased urbanization and a greater thrust on

packaged foods by the government. The increasing

sale of white goods is expected to be another

stimulant.

There is also great scope in the export market as

currently India only has a miniscule share of 1.5% of

the export volume of plastic. According to CRISIL

world trade in plastics is expected to be 140 MMT

by 2012 and there lies a

very lucrative opportunity

for Indian based plastic

manufacturers. The rating

agency goes on to stress

that however, India would

need to realign its trade

basket to focus more on

high value plastic products

rather the polymers as is

the case currently. India’s

trade basket is skewed

towards polymers with

polymers accounting for

68% and processed plastic

accounting for 32%.

According to CRISIL, in the future, plastic growth

will best be seen in Packaging usages(processed

foods, agricultural produce), plasticulture usages

(irrigation, mulch films, green houses) and

infrastructure usages (pipes, power and telecom

cables and geo-synthetics).

A well-publicized drawback of plastic products or

perhaps a big misconception is that it is not

environmentally friendly and this could perhaps be

one of the reasons why plastic consumption in India

is still below world levels. In fact contrary to

general perception plastic can be recycled into non-

critical items of daily use and waste plastic can also

be used to generate fuel. According to CRISIL,

plastic waste has tremendous utilitarian value in

road construction as it can be blended with Bitumen

to improve binding properties and increase savings

of 5-10% per kilometer in the cost of bitumen. Also

what most people aren’t aware of is the fact that

plastic has energy saving properties. Its energy

savings properties are best

exemplified in the auto and the

electrical appliances industries.

According to the Automotive

Research Association of India,

the replacement of metals by

plastics improves the mileage of

vehicles and reduces CO2

emissions by 50 mmt per year

for the automobile sector

globally.

OUTLOOK AND

SCOPE

SIL has done remarkably well up

until now, with its compelling

growth story. In a hypothetical sense most

companies that may have followed SIL’s growth

chart may be tempted to consolidate for a while

before embarking on further growth initiatives but

when one is involved in an extremely under

penetrated and fragmented market such as the

Indian plastics market that would represent an

opportunity lost. Keeping this is mind SIL has put in

place some very interesting targets that it hopes to

achieve by 2014-2015. It is already widely

acknowledged to be the leader in the Indian plastics

5 YEAR STRATEGY OF SIL

Reach the Rs.4500 landmark on the

topline.

Increase share of value added

products (Products with OPM>17%).

Diversify product portfolio.

Expand capacity to 595000MT by

2014-15.

Increase the number of manufacturing

units from 19 to 31.

Capital expenditure of Rs.1000 crore

over the next 5 years.

COMPANY RESEARCH REPORT December 30, 2010

10

segment and has such a vast spread in terms of

distribution network and strategically positioned

manufacturing units, but the management now

wants to take the company to the next level.

If the “Management Discussion and Analysis”

segment in an annual report is anything to go by,

then one can certainly expect a very eventful future

for SIL. Some of the targets that the management

has set until 2014-2015

include increasing the

number of manufacturing

units from the existing 19

units to 31 units, enhancing

the manufacturing capacity to

595000MT augmented by

Rs.1000 crores of capital

expenditure, diversifying

their product portfolio even

further by focusing on

technological innovation and

increasing the component of

value added products and

specialty products across all

its four product segments

(The value added products

are essentially high margin

products or OPM>17%, that contribute additional

value without adding to the cost. The company

wants to increase the contribution of value added

products of SIL to 30% by 2014 and 20% in the

current year. Last year the contribution of value

added products to total sales was 17.78%). As part

of the company’s initiative to develop and

introduce innovative products for new applications,

the company sees great scope in the micro

irrigation and composite segment and the

infrastructure and gas distribution segment where it

will be looking to develop electrofusion and

compression moulded fittings. The company also

wants to widen and deepen its distribution network

and increase the number of its channel partners.

The management feels that there are still several

towns where dealer net works have to be created

and over the next two years the target will be to

cover the unrepresented towns with growth

potential.

However while all those plans

are going to transpire in the

long-term, things are looking

fairly encouraging in the near-

term as well and the next two

years particularly the current

year, one could see a huge

surge in the company’s top line

and bottom line as it goes

about disposing blocks of its 12

storied commercial complex-

The Supreme Chambers. SIL is

looking to sell 275000 square

feet of the state-of-the art

property that is estimated to

fetch them revenues to the

tune of Rs.375 crores. The

management has stated their

desire to see the fructification of the entire sale of

the commercial complex bar one floor by December

2011. There are obviously certain question marks

over SIL’s corporate focus as it is not clear if the

construction business is something that the

company will be looking to continue with, in the

future, but it is certainly going to be earnings

accretive in the current year and that is something

shareholders or prospective shareholders of SIL

should welcome.

SIL’S LIST OF NEW MANUFACTURING UNITS TO BE SET UP BY 2015

Division No. of New Locations

Proposed Locations

Industrial Moulded Products

3 Ahmedabad,

Jamshedpur & Pondicherry

Plastic Piping System

1 West Bengal

Cross Laminated Film

1 Halol

Protective Packaging Products

4 Hosur,Gujarat, West Bangal &

Rajasthan

Furniture 3 Andhra,East Zone

& North Zone

Source: Company

COMPANY RESEARCH REPORT December 30, 2010

11

Interestingly enough SIL is also

looking to strengthen its strong

brand equity position and has

set up a training centre to train

people about the right method

of the installation of its wide

range of piping products. It has

also set up a Display Centre

showing various systems made

by the company. Both the

training and display centres

have started operations since

September 2010. The

management is quite

optimistic about this initiative

and is encouraging its channel

partners to bring their

dealers/sub-dealers and end

customers to visit the training

and display centre.

The company’s core activities of

converting polymers and resins

into finished plastic products

across four broad categories,

too looks fairly encouraging.

The management took the

decision of shutting down its

Nandesari unit which was not

contributing to the business

growth due to pollution issues

and other factors. Since then

the company has reconditioned

and shifted all the major

equipment to other plans and

those equipments are now

running to their original design

capacity. The company was also

able to secure crucial cash flow

from the sale of the land and

building as well.

In the last fiscal the company’s

material handling equipment

division (crates) was adversely

affected by the disappointing

monsoon conditions as retail

chains tend to use the

company’s material handling

equipment for the

transportation of crops such as

Tomatoes and Grapes during

post harvest transportation (SIL

is the preferred supplier of

crates in this segment). In the

current year due to the

spectacular monsoon, this

segment is likely to post better

results. SIL has also developed

several new moulds to cater to

its ever increasing applications

and the supplies of these

products have just started.

With regard to its consumer

product segment, the company

is continuing to ramp up the

production of its value added

products and recently launched

its Designer Chair “DIVA” which

is already proving to be quite

popular. The company currently

has 209 exclusive showrooms

that showcase SIL’s superior

range of furniture and intends to

increase the number of

TWO YEAR OUTLOOK OF SIL

Sale of SIL’s Supreme Chambers to

fructify by December 2011.

Strengthening of brand equity,

particularly through the new

training and display centres that

were set up in September 2010.

Retail marketing initiatives will be

stepped up on a pan India basis.

Demand for SIL’s food handling

crates (particularly Tomatoes and

Grapes) to increase in the current

fiscal.

The number of consumer product

showrooms to be increased from

209 to 300 in the current year.

Besides the West Zone consume

product market to flourish due to

logistical advantages provided by

the Gadgeaon plant that

commenced manufacture of

furniture in September 2010.

The furniture manufacturing

capacities of SIL’s Durgapur,

Pondicherry and Guwahati plants to

be enhanced.

Production generating capacity of

the Kanpur plant to be increased

from 8000 tonnes p.a. to 15000

tonnes p.a.

Demand for SIL’s piping products to

get stimulated from the

replacement market.

COMPANY RESEARCH REPORT December 30, 2010

12

showrooms to 300 by the end of the year. To

augment the increase in showrooms the company

will also be increasing the furniture manufacturing

capacity of its Durgapur, Pondicherry and Guwahati

plants. Besides, in September 2010, the company

started the manufacture of furniture from its

Gadegaon plant in order to cater to the West Zone

market. Previously it was catering to this market

from its Pondicherry unit and this was nurturing

logistical disadvantages for the company. Andhra

Pradesh is another territory where the company is

looking to set up a furniture manufacturing plant in

order to nullify the logistics cost disadvantage and it

has also initiated actions to acquire land in the state

as well as look for channel partners in this region.

The mats’ sales of the company as well are expected

to pick up as most of the economies across the

world, are slowly coming out of the woods and

exports account for a bulk of the mats’ sales of SIL.

As far as its piping products division is concerned the

company is looking to enhance the production

generating capacity of its Kanpur plant from 8000

tonnes p.a to 15000 tonnes p.a. To facilitate the

expansion, the company had acquired a further 7

acres of adjoining land. At its Piping manufacture

plant at Gadegaon the company had not only

completed the expansion of its UPVC and CPVC

production lines but had also increased the level of

automation in the production capacity. In the last

fiscal due to severe drought conditions a lot of state

governments had enforced a ban on the digging of

new borewells and this had affected the business of

this division. Due to the fantastic monsoon in the

current year, the situation is expected to be

reversed. This has thrown up a number of benefits

for the firm such as increase in output, reduction in

man power requirements, improvement in the

environment of the mixing division and consistency

in quality. PVC resin is one of the crucial components

used for making SIL’s pipes and the prices of that

material are something that could affect margins of

this division. The company will also be launching

sprinkler systems in several states for the first time

and that should contribute decently to SIL’s

financials. The management also sees significant

scope in the replacement market as more and more

buildings are undergoing renovation. To meet the

additional requirement of this market the

management has stated that they will be focusing on

retail marketing on a PAN India basis.

There have also been recent reports suggesting that

SIL is in the process of manufacturing plastic gas

cylinders which, if true, could prove to be a path

breaking product. It would also give the company a

first mover advantage. However the management

has stated that one of their thrust areas in the future

will be electro fusion and compression moulded

fittings for infrastructure and gas distribution.

While the management is going to be investing

around Rs.180-270 crores of capex in the current

year, most of it is going to be devoted to the

Industrial products division, Consumer products

division and Piping products division. The

management will not be devoting much to the

performance packaging films segment and the cross

laminated film segment as committed capacities in

these two segments still have to go into production

due to low capacity utilization and a shortage of

labour.

COMPANY RESEARCH REPORT December 30, 2010

13

FINANCIALS AND VALUATIONS

HISTORICAL FINANCIALS

The historical financials of the company provide a

relevant picture of the degree of prosperity that SIL has

enjoyed up until now. Before dissecting the financials, it

must be noted that SIL’s annual results are published

every June (SIL follows a July-June time period for

accounting).

From June 2007 - June 2010, SIL‘s revenue has grown

from Rs. 1116.22 crore to Rs. 2007 crores, growing at a

CAGR of 19.7%. Taking into consideration a two year

average, the plastic piping product segment has been

the biggest contributor to SIL’s annual revenue

contributing around 44 % to the topline, the next big

contributor is the packaging product segment

contributing around 24 % to the top line. The industrial

products segment and the consumer products segment

contribute around 20% and 12% respectively to the

overall top line.

The operating profit for the same time period has grown

from Rs. 121 crores to Rs. 289 crores, growing at a rather

impressive CAGR of 33%. Operating margins (OPM) have

climbed up the ladder quite impressively. OPM which

stood at 10.4% moved up year on year to end at 14.79%

at the end of June 2010.

SIL’s debt levels have always hovered around a

manageable level and consequently interest payments

haven’t been a major impediment in transferring the

buoyancy at the operating level down the bottom line.

The debt equity ratio which stood at 1.03 at the end of

June 2007 rose up marginally for the next two years to

reach 1.13 before petering down to 0.78 at the end of

June 2010. Consequently interest as a % of sales has

been quite negligent. Interest as a % of sales was 2.9% at

the end of June 2007 and even though it rose to 3.3% the

double impact of expanding top line growth and

decrease in interest payment sent that figure to a lowly

1.7% at the end of June 2010.

Depreciation too has been another item that hasn’t

caused a lot of strain on the profits. Depreciation as a %

of Net sales which stood at 3.4% at the end of June 2007

dropped to 2.63% at the end of June 2010. All in all the

profits of the

company have

grown at a

notable CAGR of

44% from Rs. 47

crores at the end

of June 2007 to

Rs.142 crores at

the end of June

2010. PAT

margins as well

have moved up

in the last three

years (there was

a decline in 2008

however on a

yoy basis due to

increase in the

interest

component. The

company had

increased its

secured loan

component

significantly by

Rs.72 crore in

that year) from

4% at the end of

June 2007 to 7%

at the end of

June 2010.

SIL also has a decent set of cash levels. It has been able

to maintain a strong set of cash at both the operating

levels and net levels in every year. At the end of June

2010, SIL has generated cash worth Rs.146 crores from its

operating activities and Rs.19 crores of net cash.

HISTORICAL FINANCIALS

3 year historical sales has grown at a CAGR of 19.7% from Rs.1116.22 crore to Rs.2007 crores.

Piping products are the biggest contributor to the topline contributing around 44%, followed by packaging products, industrial products and consumer products that contributed 24%, 20% and 12% respectively.

Debt equity ratio has ranged from 1.03 to 0.78 in the last three years.

3 year operating profits have grown at a CAGR of 33% from Rs.121 crore to Rs.289 crore.

3 year net profits have grown ata CAGR of 44% from Rs.47 crores to Rs.142 crores.

Operating profit margins in the last three years have increased from 10.4% to 14.7%.

Net profit margins in the last three years have increased from 4% to 7%.

Last year’s ROE and ROCE were 39.8% and 38.7% respectively.

COMPANY RESEARCH REPORT December 30, 2010

14

FINANCIAL OUTLOOK

SIL’s management has put in place a set of targets

which it hopes to achieve by 2014-2015 and has

given a decent guidance on some of the initiatives it

will be taking up until then. The management has set

a target of achieving Rs.4500 crore on the top line by

2014-2015 which would represent a CAGR of around

17%+. This top line growth will be augmented by

increasing the number of manufacturing units from

the current 19 to 31 by the end of 2014-2015 and a

grand capital expenditure plan of Rs.1000 crores (an

average of

around Rs.200

crore per year).

What’s also

quite

impressive is

that the

management is

looking to

generate this

figure through

superior sales

and internal

accruals rather

than debt. SIL

has also set

dual objectives

of seeking

greater top line

growth and

increasing the

component of

value added

products or

specialty

products as a %

of total products. Value added products are products

that have an OPM >17%.

However since we are only forecasting for a two year

time horizon we have only considered information

that is relevant within that stipulated time frame for

arriving at our share price targets. All things

considered the next two years look very encouraging

for SIL both from a top line and bottom line

perspective. In addition to the management’s

initiatives to spur top line growth, there also exists

some strong tailwinds (macro-economic, industry-

oriented and government oriented factors) that are

likely to stimulate SIL’s fortunes.

Despite putting up a decent set of financials in the

last fiscal, the sales of some of SIL’s key products

came under pressure due to the drought like

scenario. However this year’s superior monsoons are

likely to rectify that scenario. Of particular relevance

was SIL’s piping product segment, where the

government had to ban borewell digging due to the

drought situation. Besides PVC pipes are fast

becoming poular around the world, with China

placing special emphasis on PVC pipes over the

traditional pipes. This year will also see SIL introduce

the sprinkler system for the first time in various

states. In addition to the likely buoyancy in the

piping segment, the industrial product division

(material handling equipemt) too is likely to benefit

this year after having faced some difficulties in the

last year. SIL’s crates are used by retail chains for the

transportation of crops such as Tomatoes and

Grapes during the post harvest season and last year

there was some pressure seen due to the poor

monsoon. The thrust of the government in various

issues tied directly or indirectly to the plastic

industry, too, are likely to boost top line growth.

2 YEAR FINANCIAL OUTLOOK

Top line to grow by 30% in the first year and 12% in the second year.

The contribution of value added products (products with OPM>17%) to total sales to increase from 17.78% to 20% in the current year.

Operating profits to grow at a 2 year CAGR of 37%.

OPMs to increase from 14.3% to 16.6% and 18.6% for the next two years.

Rs.180 crore to Rs.270 crore of CAPEX to be spent in the current year.

Interest as a % of net sales to be brought down to less than 1%. It was 1.7% in the previous year.

Depreciation to grow at a 2 year CAGR of 20% as rapid plant expansion comes into play.

Net profits to grow at a 2 year CAGR of 54% and NPMs to reach 10% and 11.4% over the next two years.

COMPANY RESEARCH REPORT December 30, 2010

15

Under the FY11 Union Budget, the government has

allocated Rs.11619 crore for the Jawaharlal Nehru

National Urban Renewal Mission (JNNURM), to

improve the infrastructure of 91 cities and improve

the drinking water supply and solid waste

management. Besides the government has also

allocated a further Rs.1000 crore under the Housing

and Urban Poverty Alleviation in FY11 which will lift

real estate development and demand for piping

products. SIL is also resorting to significant brand

building exercises and strengthening its presence in

untapped towns and the unorganized sector of India.

However perhaps the most attractive features of SIL

over the near term is going to be the revenue they

will secure through their construction business. The

company in collaboration with one of India’s leading

architects (Sanjay Puri) has completed the

construction of Supreme Chambers, a 2, 75,000

square feet commercial complex for which the

company has already sold 40,000 square feet, raising

Rs.60.20 crore ( but only Rs.36 crore accounted for in

the previous quarter which means the remaining

Rs.24 crore will be accounted for in the December

quaryer. The management has stated their desire to

fructify the entire sale by the end of December 2011

and is looking to accrue a total of Rs.375 crore

(inclusive of the Rs.60.20 crore). The cost of the

project is estimated to be Rs.155 crore so taking a

net figure of Rs.220 crore and providing for the sum

already received, one is expecting at least Rs.184

crore to be collected at an average of around Rs.37

per quarter for the next five quarters.

Keeping all these factors in mind and including the

construction income, we are forecasting the sales of

SIL to grow by 30% from the June 2010 figure of

Rs.2007 crore to Rs. 2470 crores and grow by a lower

12% (high base effect, marginal income from

construction business).

As previously mentioned the SIL management has

already stressed their desire to gradually increase

the contributions of value added products or

specialty products across all its product segments

and this is likely to throw up much superior

operating margins. The contribution of value added

products to total sales was 17.78% at the end of June

2010 and SIL intends to increase that figure to 20% in

the current year and 30% by 2014. The management

is also looking to maintain cost competitiveness

through continuously enhancing operational

efficiencies, leveraging on economies of scale and

effective working capital management. Assuming a

degree of stability in commodity prices, the rationale

of high value added products and superior top line

growth operating profits for the next two years are

expected to grow at a CAGR of 37% while operating

margins are expected to rise from 14.3% to the

16.6% in June 2011 and 18.6% in June 2012 (SIL’s

management wants to maintin OPMs of >15% till

2015 at least).

From different sources of data it is determined that

SIL will be spending anything between Rs.180 crores

to Rs.270 crores in the current fiscal and perhaps the

most impressive facet of that figure is that the

management is looking to procure that sum mainly

through sales revenue and internal accruals which

means it is all but certain that the debt component

or interest component isn’t likely to go down. In fact

the management has stated that they will be looking

to bring down the interest as a % of net sales figure

to less than 1 in the current year. Interest as a % of

net sales stood at 1.7% at the end of June 2010. SIL

will also be increasing the number of manufacturing

COMPANY RESEARCH REPORT December 30, 2010

16

units from 19 to 31 in the next 5 years and the

depreciation component is most certain to go up.

Even though it is not likely to increase in terms of

sales (due to the greater sales effect), depreciation in

isolation, is likely to go up in absolute terms. This

non cash expense which grew at a miserly 6.3% from

FY06-FY10 is expected to grow by a far superior 20%

over the next two years.

Bringing all these factors into the equation, we are

forecasting the net profits to grow at a 2 year CAGR

of 53.6% with an June 2011 EPS of 20.4 and a June

2012 EPS of 26.4. At a CMP of Rs.148, the stock is

trading at 7.3 times its June 2011 EPS and 5.7 times

its June 2012 EPS.

RISKS

PVC resin prices are a crucial component in the

manufacture of SIL’s PVC pipes, and in the last fiscal

these prices were fairly stable with less volatility. In

fact last year there was a supply shortage in the

domestic shores, and about 0.6 million tonnes had

to be imported to make up for the demand. No

major large capacity additions of PVC resins are

expected in the world markets and there is a

likelihood that SIL will continue to depend on these

huge imports that could see significant price rises if

demand moves up. Crude Oil is another commodity

that plays a key role in SIL’s manufacturing process

(the prices of PVC resin, polyethylene and

polypropylene are linked to crude oil prices) and if

crude oil prices continue their northward journey

that could as well hurt SIL’s cost of production.

The valuations of the SIL stock when viewed from a

price to earnings multiple are quite close to the

industry average of around 12, and may not wholly

appeal to the consummate value investor, but we

feel that SIL’s spectacular bottomline growth over

the last three years (35%) and the prospect of an

even better bottom line growth metric (53%) over

the next two years more than justifies entry at this

point. Besides, in comparison to the valuation of

India’s benchmark index, a PE multiple of 11.3

doesn’t appear too daunting, particularly while

considering the fact that the company is one of the

biggest players or perhaps the biggest player in an

extremely under penetrated, all pervasive and

growth oriented industry such as the plastic

industry.

Pedantic business theorists, who attach

considerable attention to corporate focus, may not

be particularly buoyed by SIL’s significant, one-off

(unconfirmed) construction venture, despite it

being earnings accretive in the near term.

RISKS

PVC resin prices were fairly stable last year. However

in the current fiscal, no major capacity additions are

forecasted in the world market and this might result

in price rise if demand goes up in the current year.

Rising crude oil prices are another concern as it

shares a very close correlation to plastic oriented

polymers.

The trailing PE multiple of the SIL stock is very close

to the average industry PE and value investors may

question the prospect of outperformance at these

levels.

SIL’s one-off construction business may not wholly

appeal to pedantic or traditional business theorists.

COMPANY RESEARCH REPORT December 30, 2010

17

INVESTMENT RATIONALE

The SIL stock has pretty much all the ingredients

that make for a fundamentally robust stock. SIL is

involved in the business of manufacturing a product

that is ubiquitous and has tremendous utilitarian

value in a whole host of applications. In fact, if one

were to just pause and look around one’s

surroundings, it would be hard to disregard the

prevalence of plastic in one’s life. Being such an

omnipresent product one would expect the plastic

market to be dominated by a whole host of players

with little scope for growth but that is not the case

in the Indian plastic market. Firstly compared to the

global rates, consumption of plastic in India leaves

much to be desired. The country’s consumption of

plastic is just one-fifth of the global consumption

average. Under penetration, fragmentation,

domination by the unorganized sector and very few

publicly listed players all suggest that the Indian

plastic market is crying out for a strong plastic

manufacturer to grab it by the scruff of the neck

and stake a claim. The Indian plastic market is a

fantastic market to build a strong market share and

scale up, and SIL with its impressive branding

initiatives, geographical diversification and spread

in both its manufacturing and distribution network

and superior resources, diversification in the

product portfolio and leadership (SIL’S leadership

theory is far from irrefragable as Sintex Industries, a

listed peer, posted marginally better sales in the

previous year on a standalone basis and has a far

superior market capitalization to SIL. However

“leadership” is not an absolute term in the Indian

plastic industry as it is such a wide industry with

innumerable products and dominated by the

unorganized sector). There exists a wonderful

opportunity for SIL to stake a claim and dominate

the plastic industry and the management has set in

place a whole host of initiatives in order to

capitalize, all the way uptil 2015 atleast.

SIL is hoping to reach the Rs.4500 crore sales figure

landmark by 2015 and that is to be augmented by

increasing the number of manufacturing units from

19 to 31 for the same time period. Product wise as

well, they have a nice diversified mix across four

broad segments, and the company’s R&D unit (and

in some cases), in collaboration with global

technology majors (Schoeller Wavin Systems

International Services Germany, Rasmussen

Polymer Development AG Switzerland is constantly

looking to add more innovative and value added

products across its entire product basket. The

company is also looking to strengthen its dealer

network, its channel partners and try and capture

various untapped towns and regions that have good

growth potential. With regard to its consumer

product segment which it displays through 209

showrooms, SIL has set a target of increasing the

number of showrooms to 300 by the end of this

year.

A number of government policies such as the

JNNURM and the Housing and Urban Poverty

Alleviation programme coupled with strong

industry and other macroeconomic tailwinds

(monsoon, better harvest season, pickup in global

economies that will benefit SIL’s consumer

products, strong prospects in various plastic

dependent economies such as infrastructure,

irrigation oriented, real estate, soft drinks, autos,

electrical appliances) too are quite conducive for

SIL’s fortunes, atleast over the next two years.

COMPANY RESEARCH REPORT December 30, 2010

18

Another impressive facet of

SIL’s strategy is to increase the

component of value added

products in terms of total sales

which will lead to better

margins for the company. In

fact the management of SIL

has set a strong base target of

maintaining a 15% OPM

(Operating Profit Margin) for

the next five years and that

certainly gives out an air of

reassurance. Overall its

historical financials have been

very good and over the next

two years as well, that trend is

expected to continue. Solid

growth rates, ever-increasing

margins, best-in-class ROE and

ROCE, moderate or low levels

of debt and strong cash flows

are some of the strong points

of SIL.

Traditionally SIL has been

extremely generous with

rewarding its shareholders

with divided largesse. The

dividend payout ratios have

hovered between 29-41% for

the last four years. In the

previous year, the dividend

payout ratio stood at 29.32%.

However the big positive

kicker for SIL over the next

two years, particularly in the

current year is the fact that it

is going to be generating a

construction income over the

next two years. While the

debate over corporate focus

may be stimulated, we see this

avenue being a one-off, shot in

the arm for the company’ two

year EPS.

While fundamentally, SIL has

ticked pretty much all the boxes,

the current valuation of the

stock may worry some of the

core value investors as the stock

is currently trading at 11.3 times

its trailing earnings in

comparison to the industry

average of 12 and this would

perhaps suggest limited upside

at current levels. We would

however like to argue that SIL’s

strong earnings growth more

than justifies a PE of 11.3.

Historically earnings have grown

at a four year CAGR of 35% and

thus employing a PEG ratio one

gets a figure of 0.32 which is

extremely encouraging. If one

were to consider future eps

growth rates the PEG drops even

further to 0.21.

Investors may note that our

share price targets are quite

steep from current levels and

our justification for the same, in

addition to the strong

investment rationale thesis, is

INVESTMENT RATIONALE

SIL is functioning in an industry that is

under-penetrated, fragmented and

lacks leadership in the real sense of the

word. SIL has all the ingredients to

become a dominant force in this

industry in years to come.

Macro-economic factors, government

policies and industry opportunities are

all very conducive for SIL to flourish.

SIL has put in place a very lucid and

impressive growth strategy up until

2015.

Key facets of the strategy include

expanding manufacturing units,

showrooms and distribution network,

funding a bulk of the expansion plans

through internal accruals and sales

rather than debt, increasing the

prevalence of value added products in

the product structure, diversifying the

product basket even more, maintaining

a base level for OPMs and achieving

Rs.4500 crore on the top line.

SIL’s construction income is expected

to be a pivotal EPS booster for the next

two years.

Dividend payout ratios of SIL have

varied between 29-41% for the last four

years.

Best-in-class ROE and ROCE (close to

40%).

Current trailing PE valuations may

suggest that it is not an ideal entry

point, particularly for value investors,

but a trailing PEG ratio of 0.32 and a

forward PEG ratio of 0.21 provides

ideal support for an entry into the SIL

stock.

COMPANY RESEARCH REPORT December 30, 2010

19

that our share price targets are based on annual eps

targets. Considering that SIL’s annual results will

only be announced at the end of June of every year

as opposed to the popular and standard trend of

announcing annual results at the end of every

March, expectations have been built in for a longer

period (nine months as opposed to other companies

which have only about six months left to run,

before annual results are announced).

Investors with a one-two year time horizon and

those with an aggressive risk appetite (because of

the high valuation feature) are advised to consider

investing in the SIL stock at current levels with a 1-2

year time horizon with share price targets of Rs.230

and Rs.244.

COMPANY RESEARCH REPORT December 30, 2010

20

FINANCIAL HIGHLIGHTS -CONSOLIDATED

Description Jun-10 Jun-09 Jun-08 Jun-07 Jun-06

Inc / Exp Performance

Gross Sales 2007.02 1654.94 1310.40 1162.22 1130.67

Total Income 2023.20 1662.34 1317.80 1175.05 987.46

Total Expenditure 1718.41 1417.12 1166.61 1040.86 885.02

PBIDT 304.79 245.22 151.20 134.19 102.44

PBIT 251.85 198.91 111.71 104.37 78.03

PBT 216.98 143.08 71.37 70.62 50.34

PAT 142.09 94.34 48.22 47.28 39.97

Cash Profit 195.03 146.88 87.75 87.53 81.31

Sources of Funds

Equity Paid Up 25.41 25.41 27.62 27.62 13.81

Reserves and Surplus 388.67 278.72 242.85 215.92 202.41

Net Worth 412.65 301.36 267.53 240.52 213.13

Total Debt 229.06 324.98 317.60 228.32 237.49

Capital Employed 641.71 626.34 585.12 468.84 450.61

Application of Funds

Gross Block 968.88 903.55 827.87 694.73 670.61

Investments 69.29 49.60 53.59 51.12 49.56

Cash and Bank balance 18.67 10.74 46.02 14.39 7.77

Net Current Assets 65.06 87.22 29.32 13.96 87.72

Total Current Liabilities 473.12 432.66 399.79 291.43 172.54

Total Assets 643.13 629.10 588.07 471.86 453.71

Cash Flow

Cash Flow from Operations 145.66 188.55 105.94 159.21 92.70

Cash Flow from Investing activities -67.52 -140.42 -136.13 -119.80 -77.21

Cash Flow from Finance activities -70.21 -66.12 44.53 -32.79 -15.23

Free Cash flow 166.60 -37.47 -80.88 -142.92 -46.23

Market Cues

Close Price (Unit Curr.) 112.78 50.59 35.00 46.63 31.61

High Price (Unit Curr.) 117.98 51.50 84.00 49.04 48.25

Low Price (Unit Curr.) 46.00 18.51 34.40 26.30 24.31

Market Capitalization 1432.61 642.63 483.38 644.00 436.49

EPS 12.28 7.15 3.89 3.73 3.40

Price / Book Value(x) 0.69 0.43 0.36 0.54 0.20

Equity Dividend % 180.00 120.00 80.00 75.00 100.00

Enterprise Value 1643.00 956.87 754.96 857.92 666.20

Dividend Yield % 3.19 4.74 4.57 3.22 3.16 Source: Ace Equity

COMPANY RESEARCH REPORT December 30, 2010

21

FINANCIAL RATIOS -CONSOLIDATED

Description Jun-10 Jun-09 Jun-08 Jun-07 Jun-06

Operational & Financial Ratios

Adjusted EPS (Rs.) 12.28 7.15 3.89 3.73 3.4

CEPS(Rs) 76.77 57.82 31.77 31.69 58.87

DPS(Rs) 18 12 8 7.5 10

Adj DPS(Rs) 3.6 2.4 1.6 1.5 2

Book Value (Rs) 162.43 118.62 96.85 87.08 154.32

Adjusted Book Value (Rs) 32.49 23.72 19.37 17.42 15.43

Tax Rate(%) 34.52 34.06 32.44 33.05 20.6

Dividend Pay Out Ratio(%) 29.32 33.56 41.1 40.21 29.44

Margin Ratios

PBIDTM (%) 15.19 14.82 11.54 11.55 9.06

EBITM (%) 12.55 12.02 8.52 8.98 6.9

Pre Tax Margin(%) 10.81 8.65 5.45 6.08 4.45

PATM (%) 7.08 5.7 3.68 4.07 3.53

CPM(%) 9.72 8.88 6.7 7.53 7.19

Performance Ratios

ROA (%) 22.34 15.5 9.1 10.22 8.81

ROE (%) 39.8 33.17 18.98 20.84 18.75

ROCE (%) 39.72 32.84 21.2 22.7 17.32

Asset Turnover(x) 3.16 2.72 2.47 2.51 2.49

Inventory Turnover(x) 7.49 8.23 9.82 11.15 11.51

Debtors Turnover(x) 16.3 13.11 9.98 9.8 10.11

Sales/Fixed Asset(x) 2.14 1.91 1.72 1.7 1.69

Working Capital/Sales(x) 30.85 18.97 44.69 83.26 12.89

Efficiency Ratios

Fixed Capital/Sales(x) 0.47 0.52 0.58 0.59 0.59

Receivable days 22.4 27.85 36.59 37.26 36.1

Inventory Days 48.75 44.35 37.17 32.74 31.72

Payable days 23.31 22.65 25.45 30.84 39.05

Financial Stability Ratios

Total Debt/Equity(x) 0.78 1.13 1.07 1.03 1.11

Current Ratio(x) 1.31 1.38 1.13 1.12 1.72

Quick Ratio(x) 0.6 0.73 0.72 0.71 1.07

Interest Cover(x) 7.22 3.56 2.77 3.09 2.82

Total Debt/Mcap(x) 0.8 2.53 3.29 1.77 5.44 Source: Ace Equity

COMPANY RESEARCH REPORT December 30, 2010

22

FINANCIALS GRAPH AND PEER GROUP COMPARISON

Peer Group Comparison (Consolidated) (INR in CRORE)

Company Name Year End

Net Sales PBIDT PAT EPS PBIDTM% PATM% ROCE% ROE%

Hitech Plast 201003 261.92 41.62 15.73 11.34 15.89 6.01 23.09 25.84

Supreme Ind. 201006 2007.02 304.79 142.09 12.28 15.19 7.08 39.72 39.8

Kemrock Industries

201006 716.7 164.03 55.73 33.01 22.22 7.55 8.62 9.85

Time Technoplast

201003 1011.35 196.64 98.26 4.34 18.29 9.14 17.67 19.45

Sintex Industries

201003 3281.64 625.87 31.12 12.14 18.3 9.68 11.16 18.31

Source: Ace Equity

COMPANY RESEARCH REPORT December 30, 2010

23

29/12/2010

Investors can consider buying the stock at current levels (Rs.142- Rs.148) as it has been trading within that range for a while and it seems unlikely to fall below those levels in the near term. Technical Analysts suggest that the delivery support is at Rs.140.

ANALYST NOTES AND COMPANY NEWS

COMPANY RESEARCH REPORT December 30, 2010

24

Researched and prepared by: Amar Chandramohan Sr. Fundamental Analyst Email: [email protected]

Ph: (0484) 3040400, 3040419 Krishnan Thampi K

Head of Research and Strategies

Email: [email protected]

Muhammed Aslam E

Jr. Fundamental Analyst

Email: [email protected]

HEDGE RESEARCH & STRATEGIES GROUP

Head of Research: Krishnan Thampi K

Sr. Fundamental Analyst: Amar Chandramohan

Jr. Fundamental Analyst: Muhammed Aslam E

Sr. Equity Technical Analyst: Anish Chandran C V

Sr. Commodity & Equity Technical Analyst: Kesavamoorthy B

Jr. Technical Analyst: James George

Futures & Options Analyst: Yunus Ismail

Access all our research reports online at www.HedgeEquities.com

DIRECT ALL RESEARCH QUERIES TO: Research & Strategies Group

Hedge Equities Ltd

12 Floor, -Mini Muthoot Tech Towers

Kaloor, Kochi– 682017, Kerala, India

Phone: (0484) 3040400

Email: [email protected]

Disclaimer

The information contained in our report does not constitute an offer to sell securities or the solicitation of an offer to buy, any security. This report is prepared for

private circulation only. The information in our report is not intended as financial advice. Hedge Equities Ltd does not undertake the responsibility for any

investment decision taken by the readers based on this report. Moreover, none of the information in the research report is intended as a prospectus within the

meaning of the applicable laws of any jurisdiction. The information and opinions contained in our research reports have been compiled or arrived at from

sources believed to be reliable in good faith, but no representation or warranty, express or implied, is made by Hedge Equities Ltd, to their accuracy. Moreover,

you should be aware of the fact that investments in securities or other financial instruments involve risks. Past results do not guarantee future performance.