SUPPORT FOR LIVABLE CITIES CASE STUDY COLOMBO, SRI LANKA LITERATURE REVIEW: TRANSPORT ... · ·...

19

SUPPORT FOR LIVABLE CITIES CASE STUDY COLOMBO, SRI LANKA LITERATURE REVIEW: TRANSPORT SITUATION Amal S. Kumarage November 2011

Transcript of SUPPORT FOR LIVABLE CITIES CASE STUDY COLOMBO, SRI LANKA LITERATURE REVIEW: TRANSPORT ... · ·...

SUPPORT FOR LIVABLE CITIES

CASE STUDY COLOMBO, SRI LANKA

LITERATURE REVIEW: TRANSPORT SITUATION

Amal S. Kumarage

November 2011

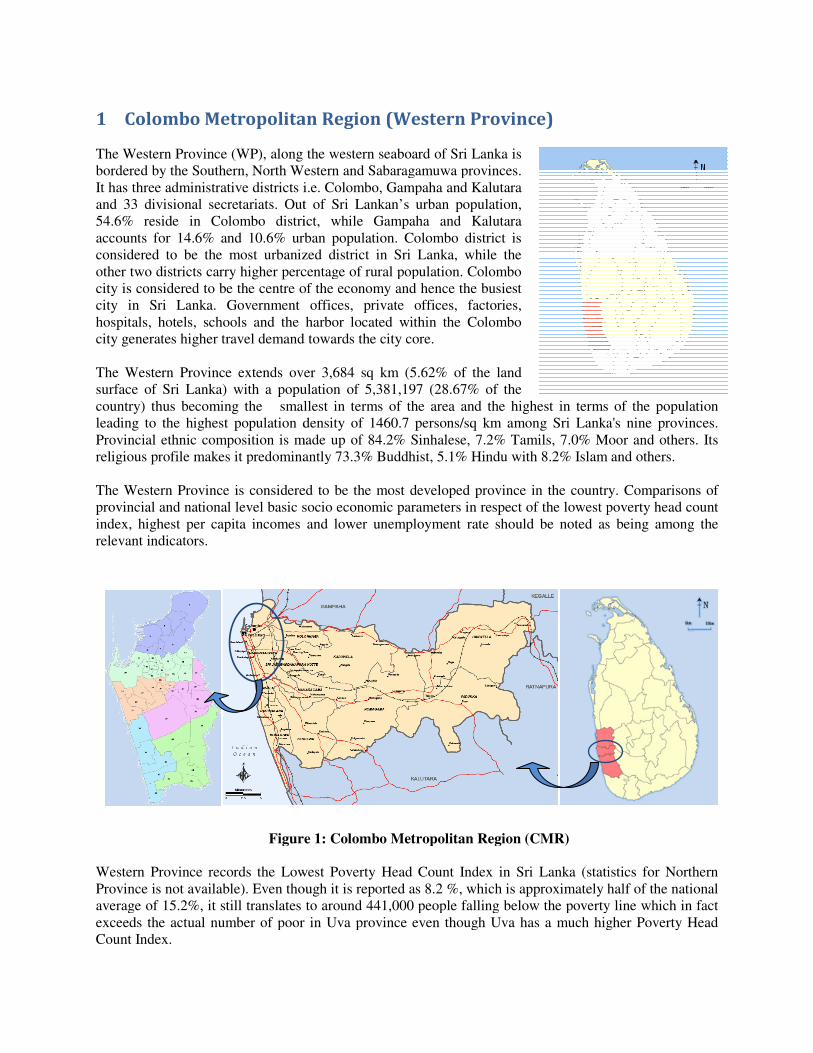

1 Colombo Metropolitan Region (Western Province)

The Western Province (WP), along the western seaboard of Sri Lanka is

bordered by the Southern, North Western and Sabaragamuwa provinces.

It has three administrative districts i.e. Colombo, Gampaha and Kalutara

and 33 divisional secretariats. Out of Sri La

54.6% reside in Colombo district, while Gampaha and Kalutara

accounts for 14.6% and 10.6% urban population. Colombo district is

considered to be the most urbanized district in Sri Lanka, while the

other two districts carry higher percentage of rural population. Colombo

city is considered to be the centre of the economy and hence the busiest

city in Sri Lanka. Government offices, private offices, factories,

hospitals, hotels, schools and the harbor located within the Colombo

city generates higher travel demand towards the city core.

The Western Province extends over 3,684 sq km (5.62% of the land

surface of Sri Lanka) with a population of 5,381,197 (28.67% of the

country) thus becoming the smallest in terms of the area and the hig

leading to the highest population density of 1460.7 persons/sq km among Sri Lanka's nine provinces.

Provincial ethnic composition is made up of 84.2% Sinhalese, 7.2% Tamils, 7.0% Moor and others. Its

religious profile makes it predominantly 73.3% Buddhist, 5.1% Hindu with 8.2% Islam and others.

The Western Province is considered to be the most developed province in the country. Comparisons of

provincial and national level basic socio economic parameters in respect of the lo

index, highest per capita incomes and lower unemployment rate should be noted as being among the

relevant indicators.

Figure 1: Colombo Metropolitan Region (CMR)

Western Province records the Lowest Poverty Head Count Inde

Province is not available). Even though it is reported as 8.2 %, which is approximately half of the national

average of 15.2%, it still translates to around 441,000 people falling below the poverty line which in fact

exceeds the actual number of poor in Uva province even though Uva has a much higher Poverty Head

Count Index.

Colombo Metropolitan Region (Western Province)

The Western Province (WP), along the western seaboard of Sri Lanka is

bordered by the Southern, North Western and Sabaragamuwa provinces.

It has three administrative districts i.e. Colombo, Gampaha and Kalutara

and 33 divisional secretariats. Out of Sri Lankan’s urban population,

54.6% reside in Colombo district, while Gampaha and Kalutara

accounts for 14.6% and 10.6% urban population. Colombo district is

considered to be the most urbanized district in Sri Lanka, while the

ercentage of rural population. Colombo

city is considered to be the centre of the economy and hence the busiest

city in Sri Lanka. Government offices, private offices, factories,

hospitals, hotels, schools and the harbor located within the Colombo

erates higher travel demand towards the city core.

The Western Province extends over 3,684 sq km (5.62% of the land

surface of Sri Lanka) with a population of 5,381,197 (28.67% of the

country) thus becoming the smallest in terms of the area and the highest in terms of the population

leading to the highest population density of 1460.7 persons/sq km among Sri Lanka's nine provinces.

Provincial ethnic composition is made up of 84.2% Sinhalese, 7.2% Tamils, 7.0% Moor and others. Its

it predominantly 73.3% Buddhist, 5.1% Hindu with 8.2% Islam and others.

The Western Province is considered to be the most developed province in the country. Comparisons of

provincial and national level basic socio economic parameters in respect of the lowest poverty head count

index, highest per capita incomes and lower unemployment rate should be noted as being among the

Figure 1: Colombo Metropolitan Region (CMR)

Western Province records the Lowest Poverty Head Count Index in Sri Lanka (statistics for Northern

Province is not available). Even though it is reported as 8.2 %, which is approximately half of the national

average of 15.2%, it still translates to around 441,000 people falling below the poverty line which in fact

exceeds the actual number of poor in Uva province even though Uva has a much higher Poverty Head

hest in terms of the population

leading to the highest population density of 1460.7 persons/sq km among Sri Lanka's nine provinces.

Provincial ethnic composition is made up of 84.2% Sinhalese, 7.2% Tamils, 7.0% Moor and others. Its

it predominantly 73.3% Buddhist, 5.1% Hindu with 8.2% Islam and others.

The Western Province is considered to be the most developed province in the country. Comparisons of

west poverty head count

index, highest per capita incomes and lower unemployment rate should be noted as being among the

x in Sri Lanka (statistics for Northern

Province is not available). Even though it is reported as 8.2 %, which is approximately half of the national

average of 15.2%, it still translates to around 441,000 people falling below the poverty line which in fact

exceeds the actual number of poor in Uva province even though Uva has a much higher Poverty Head

Western provincial share of the national GDP is around 48.4% and has recorded the highest per capita

income of Rs 303,536 (approx USD 2,500) in 2007. But the rate of unemployment and hence the

unemployed population is still higher when compared to other provinces. This indicates that though

Western province has reached a certain level of economic development, it is still to be developed in social

aspects. (Kumarage, 2010),

2 Historical Perspective of Transport in CMR

It was after the arrival of the Dutch in the 18th century that the first network of inland waterways (IWT)

were constructed in the Western Province (WP) connecting the port in Colombo for the export of coconut

and spices. It was these waterways that provided the catalyst for the growth of Colombo as a transport

hub and led to the Western Province becoming the most economically dominant province.

The opening of the Suez Canal and the simultaneous introduction of rail transport in the 1860s led to the

formation of a multi modal transport hub in Colombo. Rubber and teas as export crops were added with

the connection of the hill country to Colombo by railway and later by road transport. Colombo became

the administrative and commercial capital with the road network and the subsequent long distance bus

and trucking routes also being centred on Colombo Fort. Thus the Colombo became a uni-polar transport

hub for the country and had as its central node, the Central Business District in Colombo where the Port

of Colombo, IWT network, road and rail networks as well as truck and bus route networks were located.

The international airport was located south of the city in Ratmalana and later in 1964 moved to

Katunayake a distance of 32 kms to the north of the city

3 Significance of Colombo City

Colombo is the largest city with an area of 37 km2 and commercial capital of Sri Lanka with a city

population of 647,100. Although the city limits are defined by the Colombo Municipal Council (CMC)

boundary, its economic activities spread over Greater Colombo area which extends Kadawatha in the

north, Kaduwela in the west and Moratuwa in the south.

It also becomes the centre of the economy in Sri Lanka as the major government and private offices,

factories, hospitals, hotels, schools and harbour are located within the city inducing a large daily regular

travel demand towards the city. It also attracts a large number of irregular travellers since it links all parts

of the country by keeping country’s major road and rail passenger transport node within the centre of the

city. Therefore, most of the passengers travelling between the western part and the rest of the country

have to at least touch the Colombo city in their journeys.

4 Transport Supply and Regulation

Colombo has an extensive public transport system based on buses. The bus service is operated by both

private and government-owned Sri Lanka Transport Board (SLTB). Train transport within the city is

limited, carrying mere 10% of trips, since most trains are meant for transport to and from the city rather

than within the city and are often over crowded. The central bus stand and Fort railway station function

as the island’s primary hub for bus and rail transport respectively. Other means of transport includes

three wheelers and taxi cabs. Three wheelers are entirely operated by individuals while cab services are

run by private companies and are metered. Table 1 indicates that even though Sri Lanka has a

comparatively high road density the road penetration in urban areas is poor.

Table1: Transport Network Density

Feature CMC Colombo District Western Province Island-wide

Area (sq km)(% island wide) 37.3 (0.1%) 699.0 (1%) 3,684.0 (6%) 65,610.0

Road Length (km) 129.8 3774.6 15,409.0 113,219.0

Railway(km) 27.5 109.5 194.4 1571.7

Road and Rail Density (km/sqkm) 4.2 5.6 4.2 1.7

4.1 Bus Transport

The RPTA of the Western Province is authorized to issue route permits for intra-provincial buses and for

regularizing bus transport within the province. Currently there are around 6,540 private omnibuses

operating with permits issued by the RPTA of the WP. In addition there are around 1,413 state owned

buses belonging to the Sri Lanka Transport Board, which comes under the Ministry of Transport of the

Central Government which are not issued route permits but are also operating within the province.

Besides this there are another 865 buses issued with permits by National Transport Commission for inter-

provincial (long-distance) services starting from within the province.

The National Transport Commission provides financial reimbursements to 213 dedicated school bus trips

within the WP under the ‘Sisu Saeriya’ program. There are also a further 109 dedicated rural bus services

under the ‘Gami Saeriya’ program. Both programs are delivered through certification of delivery and

attainment of standards monitored by a local user committee. These provide important connections

between rural and town centres within a province. These services are expected to be significantly

increased this year.

Other vehicles operating within the province for fee or reward such as school vans, office vans, and three

wheelers or taxis are regulated in the WP, by Act No 3 of 2006 and by Gazette No 1518 of 2007. Three

Wheelers of which there are nearly 141,559 vehicles registered within the province, provides passenger

services within town areas and in rural areas, especially where regular public transport does not operate or

after such services cease to operate in the evenings. These are mostly unregulated except for insurance

and annual licensing as motor vehicles.

4.2 Railways

The railway network also covers much of the WP. Along the four corridors namely Mainline, Coastal

line, Kelani Valley line and Puttalam line, railway provide an important service during the peak period as

it acts as a commuter service from the outer suburbs to central Colombo. Similar to the road network

which has nodal centre in Colombo, all railway lines radiate from Colombo, this covering over 200 km

within the province. The railway carries around 210,000 passengers across the city boundary every day

which translates to around 13% of all passenger movements. Its contribution to freight transport is much

less at around 3%. (Kumarage, 2010)

4.3 Roads

The total road network in WP is comparatively larger when compared to other provinces. The length of

National Roads maintained by the RDA in the Western Province is estimated as 1,510.8 km of which

254.59 km are A Class roads and 1256.2 km of B Class Roads.

4.3.1 National Roads

Of the National Roads, around 73% of the length of roads in the province is less than standard 2 lanes,

while 6% is 4-lane width or wider. The balance 21% of the road length falls within 2 to 4 lanes. The

condition of these roads as measured by the International Road Roughness Index (IRI) shows that less

than 2% of the length of the network is in very good condition with an IRI of 2 or less and 92% of the

length is in poor condition with an IRI of 4 or more.1 (Kumarage, 2010)

The trunk roads of the national network such as A1, A2, A3, A4 close to the boundary of the Colombo

city carries traffic volumes of between 60,000 to 80,000 vehicles per day2. But the volumes of traffic on

these same roads are in the range of 15,000 to 20, 000 at the provincial boundary. On provincial roads the

traffic volumes are generally in the range 3,000 to 10,000 vpd and for local authority roads it was found

to be in most instances between 100 to 1,000 vpd. The typical vehicle composition on national roads

within the province is that around 65-70 % of vehicles are four wheeled or larger. The typical average

speeds on the national roads are between 15 km/hr within the city, to 40 km/hr away from the city while

that of the provincial network are in the range of 15 to 40 km/hr depending on the terrain and condition of

road.

4.3.2 Provincial Roads

Length of the provincial road network in Western Province is 1,975 km, of which 849 km classified under

C class and 1,126 km under D class. There are 227.8 km of recently surfaced Double Bitumen Surface

Treated DBST roads. At present around 30% of the provincial road network is termed to be in poor

condition. Only 15% of the network is in very good condition. However in general the network is

considered to be comparatively in satisfactory motorable condition.

4.3.3 Local Authority Roads

It is estimated that there are 11,923 km administered by the different local governments (MC, UCs and

PS) in Western Province3. But the local authorities especially the Pradeshiya Sabhas, do not maintain

records of the condition of their road network. Hence an assessment of the condition of the roads is not

possible. Visual observation indicates that other than the larger municipal councils such as Colombo all

other municipal councils as well as urban councils are not maintaining their roads on a regular basis. It is

most likely that over 50% of the road length may be considered to be in poor condition. In the case of

Pradeshiya Sabhas this may be even more with between 2/3rd

and 3/4th of the road lengths being

considered to be in poor condition.

1 Source: TransPlan Database, University of Moratuwa

2 TransPlan Traffic Estimation Model, University of Moratuwa, 2008

3 Commissioner of Local Government, Western Province

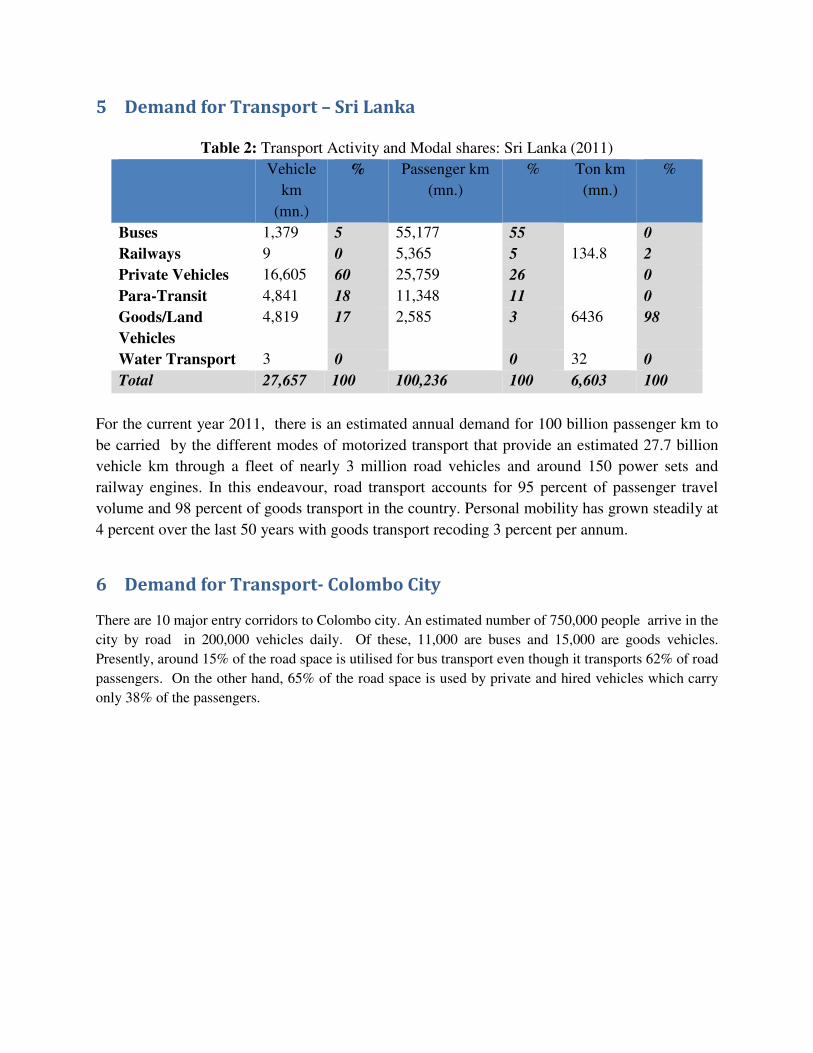

5 Demand for Transport – Sri Lanka

Table 2: Transport Activity and Modal shares: Sri Lanka (2011)

Vehicle

km

(mn.)

% Passenger km

(mn.)

% Ton km

(mn.)

%

Buses 1,379 5 55,177 55 0

Railways 9 0 5,365 5 134.8 2

Private Vehicles 16,605 60 25,759 26 0

Para-Transit 4,841 18 11,348 11 0

Goods/Land

Vehicles

4,819 17 2,585 3 6436 98

Water Transport 3 0 0 32 0

Total 27,657 100 100,236 100 6,603 100

For the current year 2011, there is an estimated annual demand for 100 billion passenger km to

be carried by the different modes of motorized transport that provide an estimated 27.7 billion

vehicle km through a fleet of nearly 3 million road vehicles and around 150 power sets and

railway engines. In this endeavour, road transport accounts for 95 percent of passenger travel

volume and 98 percent of goods transport in the country. Personal mobility has grown steadily at

4 percent over the last 50 years with goods transport recoding 3 percent per annum.

6 Demand for Transport- Colombo City

There are 10 major entry corridors to Colombo city. An estimated number of 750,000 people arrive in the

city by road in 200,000 vehicles daily. Of these, 11,000 are buses and 15,000 are goods vehicles.

Presently, around 15% of the road space is utilised for bus transport even though it transports 62% of road

passengers. On the other hand, 65% of the road space is used by private and hired vehicles which carry

only 38% of the passengers.

Figure 1: Road Passenger

6.1 Traffic Demand Within CMC

Following Table shows the zonal distribution of trips produced to CMC in 1996

process to update these and result swill be available in March 2012.

Table 6: Travel Pattern in CMC

Movement Type

Outside CMC to outside CMC (via CMC)

Outside CMC to inside CMC

Inside CMC to outside CMC

Inside CMC to inside CMC

Total Journeys

6.2 Traffic Flow Variation All city entry corridors experience two major traffic peaks in the morning and afternoon. Obviously,

school trips and work trips and jointly create the morning peak during 7.30 am to 8.30 am towards the

direction of the city while the return school trips a

direction during 1.30 pm to 2.30 pm and 4.30 pm to 5.30 pm respectively. Typical representation of

traffic flow on Colombo-Negombo is shown

Car/Saloon

29%

(12% of Pax)

Utility

28%

(15% of Pax)

Figure 1: Road Passenger- Vehicle& Passenger share at CMC boun

Traffic Demand Within CMC

shows the zonal distribution of trips produced to CMC in 1996. Surveys are currently in

process to update these and result swill be available in March 2012.

: Travel Pattern in CMC Area, 1996 (24-hours, weekday)

Person Journey

Private

Vehicle

Bus Rail

Outside CMC to outside CMC (via CMC) 25 200 4

190 315 81

190 315 81

680 200 3

1085 1030 169

All city entry corridors experience two major traffic peaks in the morning and afternoon. Obviously,

school trips and work trips and jointly create the morning peak during 7.30 am to 8.30 am towards the

direction of the city while the return school trips and work trips create congestion towards city outbound

direction during 1.30 pm to 2.30 pm and 4.30 pm to 5.30 pm respectively. Typical representation of

Negombo is shown in Figure 2.

Motor Cycle

18%

(6% of pax)

3wheeler

19%

(5% of Pax)

Car/Saloon

(12% of Pax)

Mini Bus

2%

Large Bus

4%

(62% Pax

incl.mini bus)

dary

. Surveys are currently in

hours, weekday)

(000s)

Goods

Vehicle

Journeys

2

12.5

12.5

36

63.5

All city entry corridors experience two major traffic peaks in the morning and afternoon. Obviously,

school trips and work trips and jointly create the morning peak during 7.30 am to 8.30 am towards the

nd work trips create congestion towards city outbound

direction during 1.30 pm to 2.30 pm and 4.30 pm to 5.30 pm respectively. Typical representation of

Figure 2: Traffic flow variation along parliam

Figure 2 clearly illustrates that the peak period congestion is purely created by private passenger vehicles

such as motor cycles, three wheelers, cars and vans as their flow is always close to the total vehicle flow

during the day. Therefore, congestion management should focus on reducing passenger vehicle entry to

the city or else providing an adequate road way capacity for them.

6.3 Trip Purpose

One end of the most of trips coming to the city is a home. 41% of home based trips at the CMC boundary

are coming to the city with the purpose of working. The majority of 17% home based other trips are

produced for schooling purposes. Non

equaling to the home based work trips.

: Traffic flow variation along parliament road

the peak period congestion is purely created by private passenger vehicles

such as motor cycles, three wheelers, cars and vans as their flow is always close to the total vehicle flow

ngestion management should focus on reducing passenger vehicle entry to

the city or else providing an adequate road way capacity for them.

One end of the most of trips coming to the city is a home. 41% of home based trips at the CMC boundary

are coming to the city with the purpose of working. The majority of 17% home based other trips are

produced for schooling purposes. Non-home based trips such as business and official trips are in 41%

equaling to the home based work trips.

the peak period congestion is purely created by private passenger vehicles

such as motor cycles, three wheelers, cars and vans as their flow is always close to the total vehicle flow

ngestion management should focus on reducing passenger vehicle entry to

One end of the most of trips coming to the city is a home. 41% of home based trips at the CMC boundary

are coming to the city with the purpose of working. The majority of 17% home based other trips are

home based trips such as business and official trips are in 41%

Figure 3: Travelling Purpose of trip makers at CMC boundary

According to the Figure 3, higher percentage of morning and evening peak period traffic is comprised

with home based work trips. Home based other trips such as school trips are raised in the morning and the

afternoon creating several local peaks. Non-home based trips are gradually increased once the day

progress and start to diminish at about afternoon after reaching its maximum.

Figure 4: Variation of Trip Purpose by Time of Day for Persons entering CMC

Bus/Rail passenger interviews conducted by University of Moratuwa in 2007 reveal following issues

which reflect the behavior of passengers coming to CMC.

• 53% of bus passengers and 37% of rail passengers come to Fort/Pettah to transfer to another bus

going out of CMR. Greater portion of these travelers come to city during the day time.

• Majority of trips between CMC and outside CMC can be considered as HBW & Schooling trips

and 43.2% of bus and 46.9% of rail passengers make transfers at Pettah/ Fort to local services

from intra & inter provincial services.

0

10

20

30

40

50

60

70

80

90

100

7.0

0-7

.30

7.3

0-8

.00

8.0

0-8

.30

8.3

0-9

.00

9.0

0-9

.30

9.3

0-1

0.0

0

10

.00

-10

.30

10

.30

-11

.00

11

.00

-11

.30

11

.30

-12

.00

12

.00

-12

.30

12

.30

-13

.00

13

.00

-13

.30

13

.30

-14

.00

14

.00

-14

.30

14

.30

-15

.00

15

.00

-15

.30

15

.30

-16

.00

16

.00

-16

.30

16

.30

-17

.00

17

.00

-17

.30

17

.30

-18

.00

18

.00

-18

.30

% o

f T

rip

Cat

ego

ry

Time

HBW Trips

HBO Trips

NHB Trips

6.4 Growth of Demand

Kumarage and Weerawardena (2009) have estimated growth of passenger demand in Colombo City as

follows:

Since country’s major administrative, business, commercial and educational activities were centralized to

the Colombo city centre, it has experienced a steady traffic growth for several decades. But in last few

years it is observed that the outskirt areas of Colombo city such as Nugegoda, Maharagama, Panadura and

Kiribathgoda were also rapidly developed and used for administrative and economic functions by

reducing certain amount of passenger trips driven towards the centre of city. This scenario is affirmed by

that though CMC is experienced an annual increase of 5% in the number of persons arriving to the city on

a daily basis from 1965 to 1995, it is started decrease since 1995 due to the development of afore-

mentioned city suburbs.

Interestingly however, during the last decade, even though the number of people coming has reduced, the

number of vehicles coming to the city has continued to increase. This means that more and more people

have shifted from public transport to private vehicles which take more space on the road per person, thus

allowing fewer people to enter the city especially during peak periods.

Figure 5: Comparison of Passenger Modal Share Since 1975 to 20034

Over the last 30 year period the share of trips made by cars and motor cycles have increased from just 5%

to 20% leading to an explosion in the demand for road space from around 25,000 vehicles per day to

175,000 a seven fold increase. This phenomenon is not particular to Colombo as most cities experience

4 Source: Transportation Engineering Division, University of Moratuwa, 2004

similar problems when public transport fails to match the improved quality of transport and complexity of

mobility needs that arise with increasing incomes of the population. This can be observed when one

compares the relative deterioration in the comfort of bus or rail transport when compared with the ever

increasing features in private vehicles. Even though buses have increased in number, the quality of

service, reliability, conditions of bus stops and terminals have continued to deteriorate. The railway

service is also plagued by loss in quality and also struggles to meet its timetable requirement due to lack

of rolling stock.

Table 4: Growth of Traffic Entering to Colombo City5

Year Private Vehicles Buses Goods Vehicles Total

ADT 1985 130,000 31,950 16,850 178,800

AAGR(1985-95) 4.6 -1.7 3.7 3.6

ADT 1995 203,215 27,084 24,158 254,457

AAGR(1995-05) 5.3% -1.3% 2.6% 3.9%

ADT 2005 341,893 23,893 31,311 374,381

6.5 Transport Capacity Projections

The passenger transport capacity within the CMC was calculated by WS Atkins and University of

Moratuwa in 1999 as given as below.

Table 5: Passenger Capacity by Corridor and Mode of Transport Corridor

(Bus/PV

Ratio)

Mode 2005 2010 2020 2030

Capacity Note Capacity Note Capacity Note Capacity Note

Galle Road

(60/40)

Bus 257 (1,2

3,4)

257 257 257

PV 170 170 170 170

Railway 96 (5) 96 - (7) -

LRT/MRT - 60 (6) 160 (8) 240 (9)

Negombo

(65/35)

Bus 251 (10,

11)

251 251 251

PV 205 205 205 205

5 Source: Transportation Engineering Division, University of Moratuwa, 2004

Railway 32 (12) 48 (13) 64 (14) 64 (16)

LRT/MRT - - 120 (15) 240 (17)

Kandy

(70/30)

Bus 180 (18) 327 (19) 327 327

PV 126 218 218 218

Railway 96 (20) 150 (21) 200 (22) 200

LRT/MRT - - - -

Ratnapura

(60/40)

Bus 226 (23) 226 226 226

PV 150 150 150 150

Railway 12 (24) 12 12 12

LRT/MRT - 60 (25) 120 (26) 240 (27)

Cotta Rd/SJP

(45/55)

Bus 154 (28) 154 154 154

PV 188 188 188 188

LRT/MRT - 60 (29) 120 (30) 240 (31)

Horana Rd

(50/50)

Bus 98 (32) 98 98 98

PV 98 98 98 98

Kolonnawa

(60/40)

Bus 45 (33) 45 45 45

PV 31 31 31 31

Narahenpita

(30/70)

Bus 16 (34) 16 16 16

PV 37 37 37 37

Low Level

(50/40)

Bus 46 (35) 46 46 46

PV 33 33 33 33

Total by

Mode Bus 1,273 1,420 1,420 1,420

PV 1,038 1,130 1,130 1,130

Railway 236 306 276 276

LRT/MRT - 180 520 960

TOTAL All 2,547 3,036 3,346 3,786

Source WS Atkins and University of Moratuwa, 1999

6.6 Origin Destinations of Demand

Based on 2004 surveys (Kumarage and Weerawardena, 2009), there are about 41% of home

based work trips in total private vehicle trips produced between CMC and CMR region. Of the

total motorized work trips made in the CMR, 23% are terminating in the CBD. A further 34%

have their trip ends in the non CBD part of CMC. Only 43% of motorized work trip rends are

outside the CMC. This indicates a strong attraction for motorized work trips in the CBD.

Figure

The Table 6 shows the private vehicle trips that are attracted and generated in each DSD, as per surveys

conducted in 1996. There are no surveys since this covering the entire CMR to update this data.

Table 6: Inter-Zonal Trips in Western Province by Private Vehicle,

DSD

Home Based Work

Gen

Total

% by

All Total

Colombo 8,021 14 40,937

Hanwella 572 30

Homagama 2,838 31

Kaduwela 4,135 38 2,689

Maharagama 3,445 30 1,357

Kesbawa 3,494 40

Nugegoda 8,639 22 4,888

Dehiwala 6,241 24 4,264

Moratuwa 3,285 23 1,054

Figure 6: Trip Attractions in Colombo

shows the private vehicle trips that are attracted and generated in each DSD, as per surveys

conducted in 1996. There are no surveys since this covering the entire CMR to update this data.

Zonal Trips in Western Province by Private Vehicle, 1995

Trip Purposes

Home Based Work Home Based Other Non Home Based

Att

Gen Att Gen Att

Total

% by

All

40,937 31 18,267 45,477 32,631 46,055

311 16 859 1,230 471 381

753 19 5,012 2,446 1,439 765

2,689 34 4,304 2,636 2,493 2,626

1,357 13 4,831 5,125 3,203 3,626

871 17 3,663 2,299 1,549 2,066

4,888 18 16,530 9,428 14,204 12,451

4,264 17 10,209 8,153 9,234 12,924

1,054 22 4,411 1,731 6,330 1,997

shows the private vehicle trips that are attracted and generated in each DSD, as per surveys

conducted in 1996. There are no surveys since this covering the entire CMR to update this data.

1995

All Trips

Gen Att

46,055 58,919 132,469

381 1,902 1,922

765 9,289 3,964

2,626 10,932 7,951

3,626 11,479 10,108

2,066 8,706 5,236

12,451 39,373 26,767

12,924 25,684 25,341

1,997 14,026 4,782

Kolonnawa 3,146 21 779 13 5,855 2,995 5,700 2,204 14,701 5,978

Gampaha 1,388 24 1,230 15 3,569 5,506 865 1,641 5,822 8,377

Divulapitiya 238 19 89 15 796 370 189 129 1,223 588

Katana 591 15 1,449 37 1,677 1,693 1,578 730 3,846 3,872

Negombo 248 16 254 20 637 582 622 408 1,507 1,244

Wattala 2,947 22 709 8 6,706 3,319 3,780 5,152 13,433 9,180

Ja-ela 1,429 17 622 13 2,084 2,888 5,126 1,360 8,639 4,870

Kelaniya 7,757 39 2,515 23 3,729 2,561 8,211 6,058 19,697 11,134

Biyagama 938 32 694 46 907 524 1,070 276 2,915 1,494

Dompe/Weke 535 19 139 13 2,094 721 204 251 2,833 1,111

Attanagalla 779 19 213 14 1,823 1,135 1,426 165 4,028 1,513

Minuwangoda 773 28 204 12 1,907 902 128 562 2,808 1,668

Miriagma 200 26 54 21 478 186 83 20 761 260

Mahara 2,809 37 619 16 2,799 2,144 1,975 1,106 7,583 3,869

Beruwala 49 5 108 10 564 600 289 360 902 1,068

Matugama 43 22 20 40 98 26 56 4 197 50

Walallawita 57 12 11 3 426 195 3 176 486 382

Agalawatte 5 12 5 23 37 11 0 6 42 22

Dodangoda 5 10 0 0 28 14 15 9 48 23

Buulatsinghela 114 12 50 18 647 178 193 56 954 284

Horana 636 30 288 13 1,050 1,510 461 343 2,147 2,141

Bandaragama 178 14 56 9 1,008 354 75 198 1,261 608

Kalutara 344 18 307 23 874 732 683 315 1,901 1,354

Panadura 1,842 42 182 10 1,807 1,015 718 584 4,367 1,781

TOTAL 67,721 24 67,721 24 108,686 108,686 105,003 105,003 281,410 281,410

Source: University of Moratuwa,1995

OD Matrices by DSD for CMR area for 2004 (Kumarage and Weerawardena, 2009) have been shown in

Appendix. The matrices show separately the passenger vehicle travel taking place within the region and

travel taking place to destinations from and origins outside the CMR. This is currently not available for

passenger travel by public transport.

6.7 Travel Demand by Vehicle Used

The modal choice of users to travel to Colombo is given in Table 7.

Table 7: Percentage of trips by its purposes at CMC boundary towards city, 2004

Corridor (Location) Total Passengers Per Day (Two-way)

M ot

or

Cy

cle

3w he

ele r Ca

r/s

al

oo n

(Pi

ck up

/Je

epVe

hi

cle s

Bu

ses

Ra il wa y

To

tal

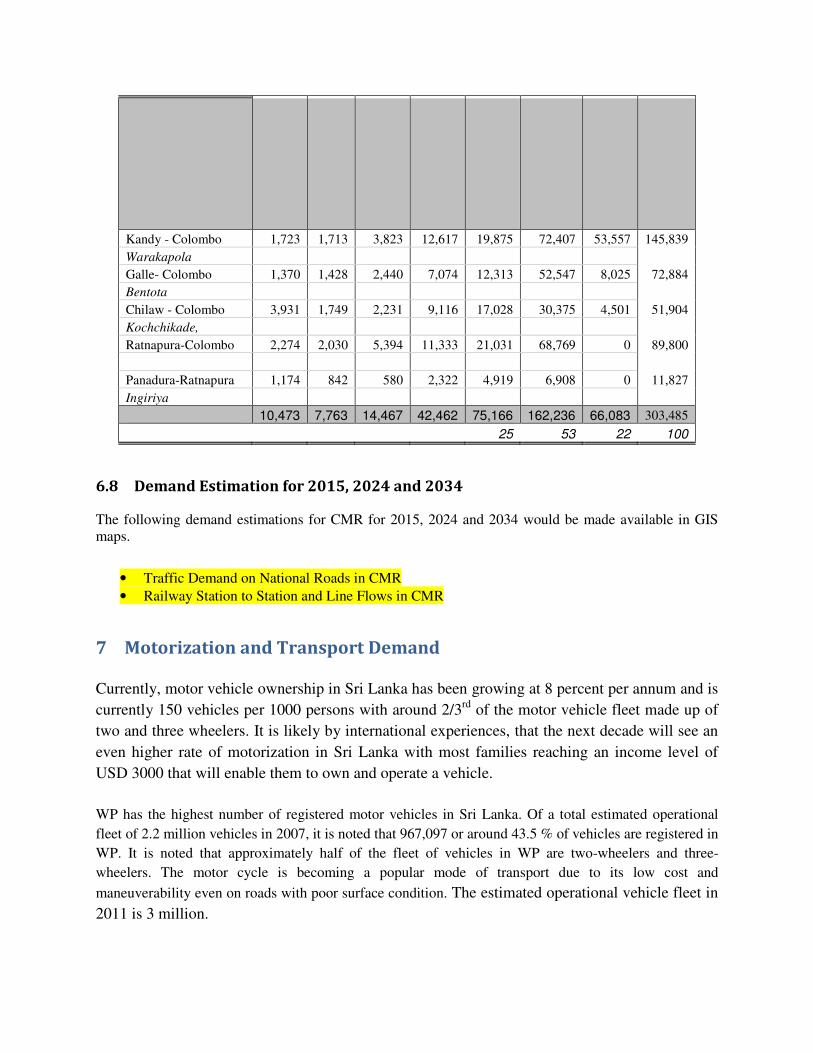

Kandy - Colombo 1,723 1,713 3,823 12,617 19,875 72,407 53,557 145,839

Warakapola

Galle- Colombo 1,370 1,428 2,440 7,074 12,313 52,547 8,025 72,884

Bentota

Chilaw - Colombo 3,931 1,749 2,231 9,116 17,028 30,375 4,501 51,904

Kochchikade,

Ratnapura-Colombo 2,274 2,030 5,394 11,333 21,031 68,769 0 89,800

Panadura-Ratnapura 1,174 842 580 2,322 4,919 6,908 0 11,827

Ingiriya

10,473 7,763 14,467 42,462 75,166 162,236 66,083 303,485

25 53 22 100

6.8 Demand Estimation for 2015, 2024 and 2034

The following demand estimations for CMR for 2015, 2024 and 2034 would be made available in GIS

maps.

• Traffic Demand on National Roads in CMR

• Railway Station to Station and Line Flows in CMR

7 Motorization and Transport Demand

Currently, motor vehicle ownership in Sri Lanka has been growing at 8 percent per annum and is

currently 150 vehicles per 1000 persons with around 2/3rd

of the motor vehicle fleet made up of

two and three wheelers. It is likely by international experiences, that the next decade will see an

even higher rate of motorization in Sri Lanka with most families reaching an income level of

USD 3000 that will enable them to own and operate a vehicle.

WP has the highest number of registered motor vehicles in Sri Lanka. Of a total estimated operational

fleet of 2.2 million vehicles in 2007, it is noted that 967,097 or around 43.5 % of vehicles are registered in

WP. It is noted that approximately half of the fleet of vehicles in WP are two-wheelers and three-

wheelers. The motor cycle is becoming a popular mode of transport due to its low cost and

maneuverability even on roads with poor surface condition. The estimated operational vehicle fleet in

2011 is 3 million.

Table 8: Vehicle Ownership, 2009

Vehicle Category Number of Vehicles

CMC WP All Island

Omnibuses 1,182 6,419 12,243

Private Coaches 3,419 10,925 23,500

Dual Purpose Veh. 29,416 100,840 175,384

Private Cars 69,522 182,078 250,943

Land Vehicles 5,837 14,396 65,974

Goods Vehicles 27,880 81,767 180,739

Motor Cycles 78,597 416,527 1,150,966

Three Wheelers 29,288 154,582 372,626

Others 1,346 1,803 12,733

Total 246,487 969,337 2,245,108

7.1 Trends in Vehicle Growth

Table 9: Trends in Vehicle Growth in Western Province and CMC

Vehicle Category

Number of Vehicles

2002 2004 2005 2006 2007 2008 2009

WP WP WP CMC WP CMC WP CMC WP CMC WP

Omnibuses 7,028 7,774 8,105 2,721 8,421 1,344 7,124 1,152 6,493 1,182 6,419

Private Coaches 9,296 9,229 11,360 2,988 11,678 3,676 12,096 3,393 11,290 3,419 10,925

Dual Purpose Veh. 81,720 91,835 99,469 30,259 102,821 32,010 106,571 29,705 102,613 29,416 100,840

Private Cars 110,799 131,128 146,909 69,287 166,223 74,124 182,421 73,225 183,687 69,522 182,078

Land Vehicles 11,827 12,575 14,700 6,309 15,455 6,582 16,793 5,999 14,969 5,837 14,396

Goods Transport Veh. 55,836 62,381 82,405 27,653 78,609 29,294 83,891 27,175 82,254 27,880 81,767

Motor Cycles 276,277 355,368 430,767

61,118 370,226 73,269 414,770 77,246 421,324 78,597 416,527

Three Wheelers 24,428 132,809 25,895 141,559 26,839 148,183 29,288 154,582

Others 11,714 12,650 1,117 392 1 460 1,872 498 1,974 1,346 1,803

Total 564,497 682,940 794,832 225,155 886,243 246,654 967,097 245,232 972,787 246,487 969,337

7.2 Distribution of Vehicle Ownership

The vehicle ownership by category for each DSD is given in Table 10.

Table 10; Under preparation.

The vehicle ownership summary in provided in Table 11.(To be updated)

Table 11: Vehicle Ownership per Capita (1998)

Area Estimated

Vehicle

Ownership (Per

1000 persons)

Ownership Level by Vehicle Type

(Percentage of Vehicle Fleet)

Motor

Cycles

Three

Wheelers

Cars, &

Vans

Freight Bus

CMC 262 66 (25%) 31 (12%) 113

(43%)

45 (17%) 8 (03%)

Colombo

District

141 45 (32%) 16 (11%) 56

(40%)

20 (14%) 4 (03%)

CMR 97 40 (41%) 9 (09%) 32

(33%)

13 (13%) 3 (03%)

Sri Lanka

(1996)

74 38 (51%) 2 (03%) 21

(29%)

12 (16%) 1 (02%)

8 Trip Rate

Further information on this is being processed currently

Trip rates per person per day for different trip purposes is given below (Liyanage, 2006).

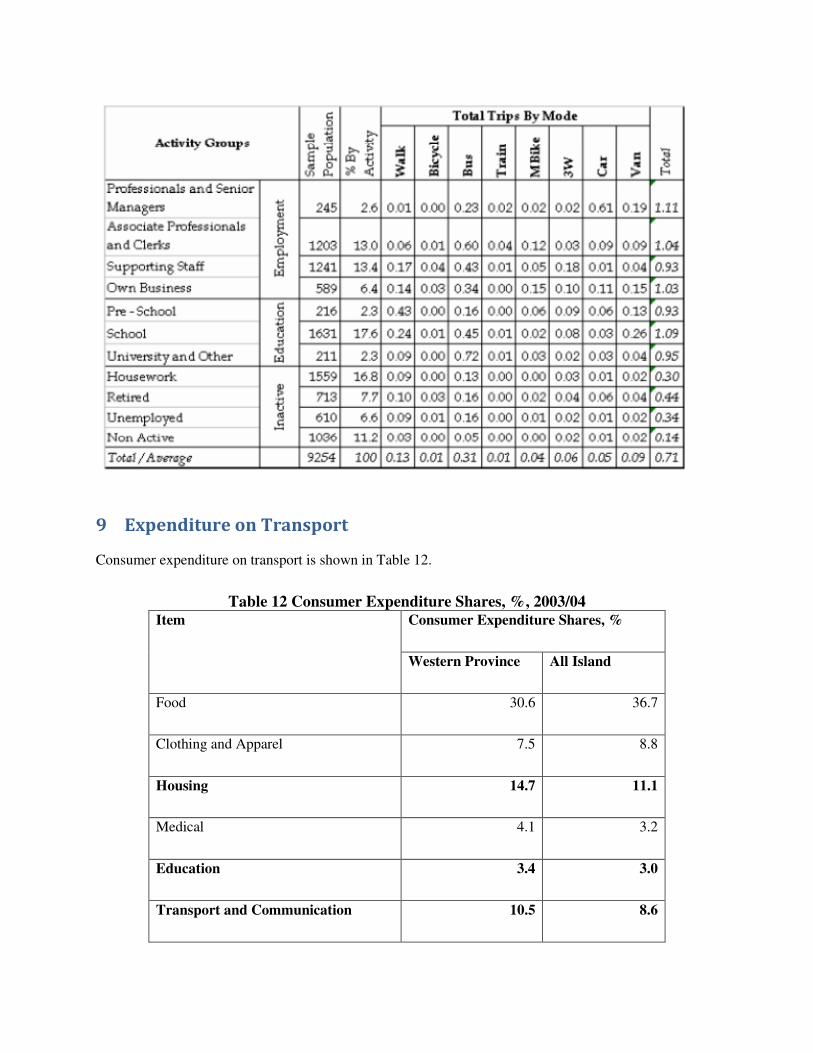

9 Expenditure on Transport

Consumer expenditure on transport is shown in Table 12.

Table 12 Consumer Expenditure Shares, %, 2003/04

Item Consumer Expenditure Shares, %

Western Province All Island

Food 30.6 36.7

Clothing and Apparel 7.5 8.8

Housing 14.7 11.1

Medical 4.1 3.2

Education 3.4 3.0

Transport and Communication 10.5 8.6

Fuel and Light 4.5 4.4

Consumer Durables 8.4 9.7

Interest on Debt 1.9 1.4

Other 14.4 13.0

In accordance to the above issues it is revealed that the people are presently spent higher proportion of

their earnings for the comfort of traveling by means of using their own vehicles or residing close to their

offices/schools. Therefore it is understandable that if comfortable passenger transport service can be

provided, some proportion of them can be attracted for such services even at a higher rate since they

already spent higher amount of their earning on this issue.

References

• Kumarage Amal. S., Review of Sri Lanka’s Transport Sector, World Bank, Colombo, 2010

• WS Atkins and University of Moratuwa, Colombo Urban Transport Study - Stage 2, Working

Paper 25: A Masterplan for the Development of Transport in the Colombo Metropolitan Region,

1999.

• Kumarage Amal S. and Janaka Weerawardena, Greater Colombo Traffic Management, Research

Report 0902, University of Moratuwa, 2009.

• Liyanage Tissa, Electricity Consumption and Trip Generation, PhD Thesis, University of

Moratuwa, 2006.