Supply and Demand of High Alumina Raw Materials for ... · The demand for high alumina refractory...

6

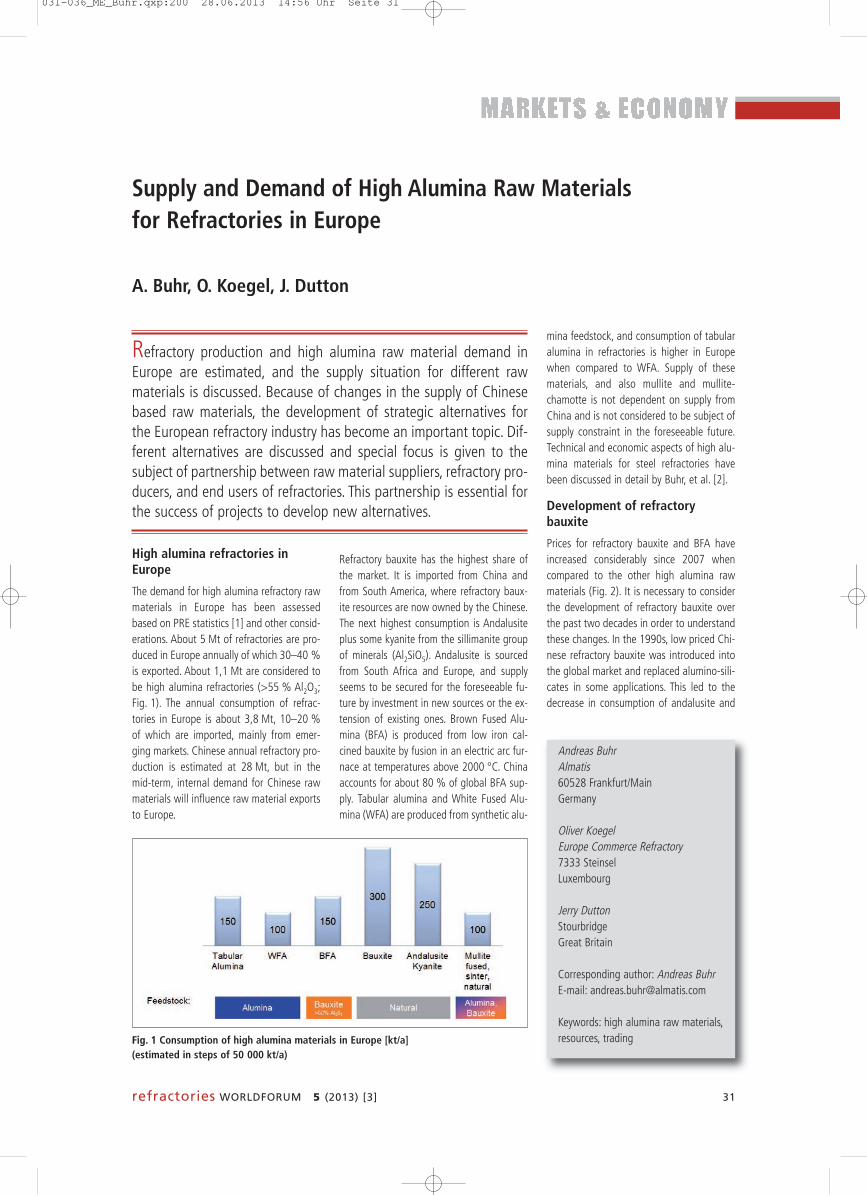

refractories WORLDFORUM 5 (2013) [3] 31 High alumina refractories in Europe The demand for high alumina refractory raw materials in Europe has been assessed based on PRE statistics [1] and other consid- erations. About 5 Mt of refractories are pro- duced in Europe annually of which 30–40 % is exported. About 1,1 Mt are considered to be high alumina refractories (>55 % Al 2 O 3 ; Fig. 1). The annual consumption of refrac- tories in Europe is about 3,8 Mt, 10–20 % of which are imported, mainly from emer- ging markets. Chinese annual refractory pro- duction is estimated at 28 Mt, but in the mid-term, internal demand for Chinese raw materials will influence raw material exports to Europe. Refractory bauxite has the highest share of the market. It is imported from China and from South America, where refractory baux- ite resources are now owned by the Chinese. The next highest consumption is Andalusite plus some kyanite from the sillimanite group of minerals (Al 2 SiO 5 ). Andalusite is sourced from South Africa and Europe, and supply seems to be secured for the foreseeable fu- ture by investment in new sources or the ex- tension of existing ones. Brown Fused Alu- mina (BFA) is produced from low iron cal- cined bauxite by fusion in an electric arc fur- nace at temperatures above 2000 °C. China accounts for about 80 % of global BFA sup- ply. Tabular alumina and White Fused Alu- mina (WFA) are produced from synthetic alu- Supply and Demand of High Alumina Raw Materials for Refractories in Europe A. Buhr, O. Koegel, J. Dutton Andreas Buhr Almatis 60528 Frankfurt/Main Germany Oliver Koegel Europe Commerce Refractory 7333 Steinsel Luxembourg Jerry Dutton Stourbridge Great Britain Corresponding author: Andreas Buhr E-mail: [email protected] Keywords: high alumina raw materials, resources, trading Refractory production and high alumina raw material demand in Europe are estimated, and the supply situation for different raw materials is discussed. Because of changes in the supply of Chinese based raw materials, the development of strategic alternatives for the European refractory industry has become an important topic. Dif- ferent alternatives are discussed and special focus is given to the subject of partnership between raw material suppliers, refractory pro- ducers, and end users of refractories. This partnership is essential for the success of projects to develop new alternatives. mina feedstock, and consumption of tabular alumina in refractories is higher in Europe when compared to WFA. Supply of these materials, and also mullite and mullite- chamotte is not dependent on supply from China and is not considered to be subject of supply constraint in the foreseeable future. Technical and economic aspects of high alu- mina materials for steel refractories have been discussed in detail by Buhr, et al. [2]. Development of refractory bauxite Prices for refractory bauxite and BFA have increased considerably since 2007 when compared to the other high alumina raw materials (Fig. 2). It is necessary to consider the development of refractory bauxite over the past two decades in order to understand these changes. In the 1990s, low priced Chi- nese refractory bauxite was introduced into the global market and replaced alumino-sili- cates in some applications. This led to the decrease in consumption of andalusite and Fig. 1 Consumption of high alumina materials in Europe [kt/a] (estimated in steps of 50 000 kt/a) 031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 31

Transcript of Supply and Demand of High Alumina Raw Materials for ... · The demand for high alumina refractory...

refractories WORLDFORUM 5 (2013) [3] 31

High alumina refractories in Europe

The demand for high alumina refractory rawmaterials in Europe has been assessedbased on PRE statistics [1] and other consid-erations. About 5 Mt of refractories are pro-duced in Europe annually of which 30–40 %is exported. About 1,1 Mt are considered tobe high alumina refractories (>55 % Al2O3;Fig. 1). The annual consumption of refrac -tories in Europe is about 3,8 Mt, 10–20 %of which are imported, mainly from emer -ging markets. Chinese annual refractory pro-duction is estimated at 28 Mt, but in themid-term, internal demand for Chinese rawmaterials will influence raw material exportsto Europe.

Refractory bauxite has the highest share ofthe market. It is imported from China andfrom South America, where refractory baux-ite resources are now owned by the Chinese.The next highest consumption is Andalusiteplus some kyanite from the sillimanite groupof minerals (Al2SiO5). Andalusite is sourcedfrom South Africa and Europe, and supplyseems to be secured for the foreseeable fu-ture by investment in new sources or the ex-tension of existing ones. Brown Fused Alu -mina (BFA) is produced from low iron cal-cined bauxite by fusion in an electric arc fur-nace at temperatures above 2000 °C. Chinaaccounts for about 80 % of global BFA sup-ply. Tabular alumina and White Fused Alu -mina (WFA) are produced from synthetic alu-

Supply and Demand of High Alumina Raw Materials for Refractories in Europe

A. Buhr, O. Koegel, J. Dutton

Andreas BuhrAlmatis60528 Frankfurt/MainGermany

Oliver KoegelEurope Commerce Refractory7333 SteinselLuxembourg

Jerry DuttonStourbridgeGreat Britain

Corresponding author: Andreas BuhrE-mail: [email protected]

Keywords: high alumina raw materials,resources, trading

Refractory production and high alumina raw material demand in Europe are estimated, and the supply situation for different raw materials is discussed. Because of changes in the supply of Chinesebased raw materials, the development of strategic alternatives forthe European refractory industry has become an important topic. Dif-ferent alternatives are discussed and special focus is given to thesubject of partnership between raw material suppliers, refractory pro-ducers, and end users of refractories. This partnership is essential forthe success of projects to develop new alternatives.

mina feedstock, and consumption of tabularalumina in refractories is higher in Europewhen compared to WFA. Supply of thesematerials, and also mullite and mullite-chamotte is not dependent on supply fromChina and is not considered to be subject ofsupply constraint in the foreseeable future.Technical and economic aspects of high alu-mina materials for steel refractories havebeen discussed in detail by Buhr, et al. [2].

Development of refractory bauxite

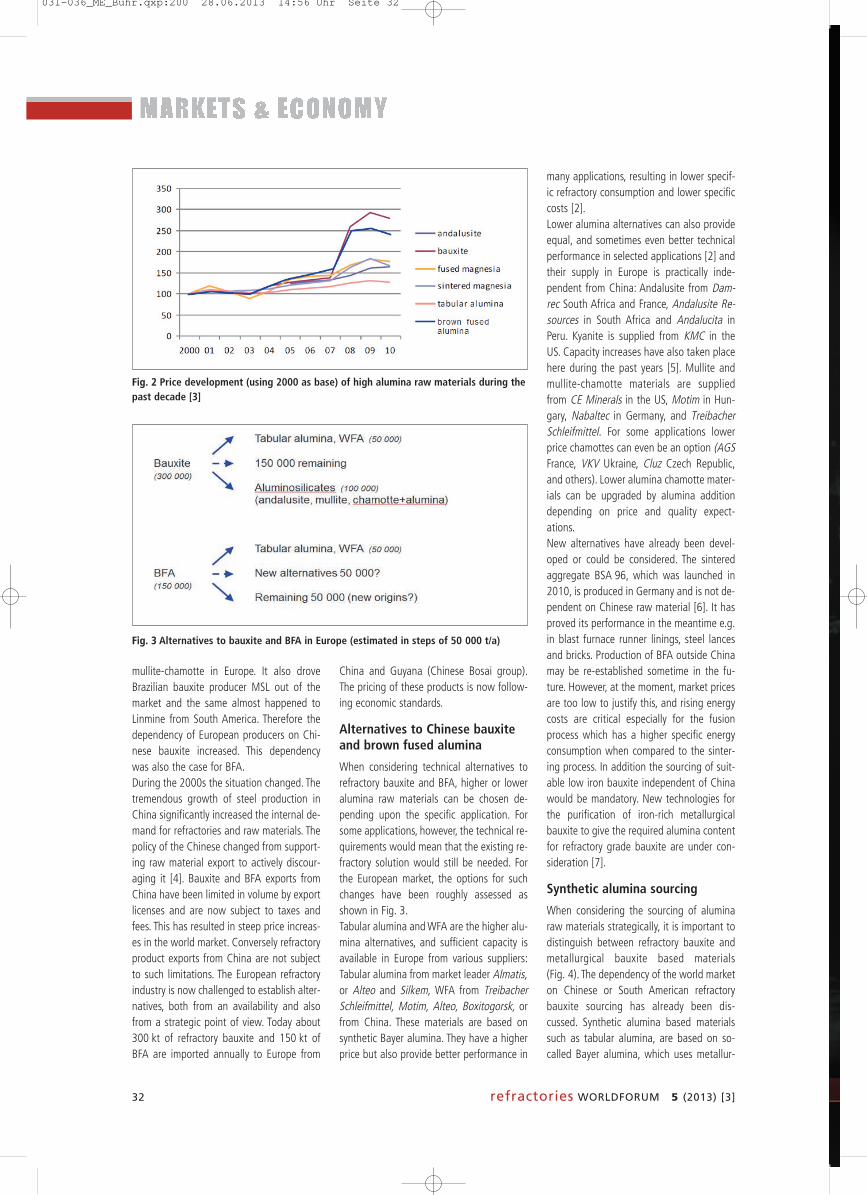

Prices for refractory bauxite and BFA haveincreased considerably since 2007 whencompared to the other high alumina rawmaterials (Fig. 2). It is necessary to considerthe development of refractory bauxite overthe past two decades in order to understandthese changes. In the 1990s, low priced Chi-nese refractory bauxite was introduced intothe global market and replaced alumino-sili-cates in some applications. This led to thedecrease in consumption of andalusite and

Fig. 1 Consumption of high alumina materials in Europe [kt/a] (estimated in steps of 50 000 kt/a)

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 31

32 refractories WORLDFORUM 5 (2013) [3]

mullite-chamotte in Europe. It also droveBrazilian bauxite producer MSL out of themarket and the same almost happened toLinmine from South America. Therefore thedependency of European producers on Chi-nese bauxite increased. This dependencywas also the case for BFA.During the 2000s the situation changed. Thetremendous growth of steel production inChina significantly increased the internal de-mand for refractories and raw materials. Thepolicy of the Chinese changed from support-ing raw material export to actively discour-aging it [4]. Bauxite and BFA exports fromChina have been limited in volume by exportlicenses and are now subject to taxes andfees. This has resulted in steep price increas-es in the world market. Conversely refrac toryproduct exports from China are not subjectto such limitations. The European refractoryindustry is now challenged to establish alter-natives, both from an availability and alsofrom a strategic point of view. Today about300 kt of refractory bauxite and 150 kt ofBFA are imported annually to Europe from

China and Guyana (Chinese Bosai group).The pricing of these products is now follow-ing economic standards.

Alternatives to Chinese bauxiteand brown fused alumina

When considering technical alternatives torefractory bauxite and BFA, higher or loweralumina raw materials can be chosen de-pending upon the specific application. Forsome applications, however, the technical re-quirements would mean that the existing re-fractory solution would still be needed. Forthe European market, the options for suchchanges have been roughly assessed asshown in Fig. 3. Tabular alumina and WFA are the higher alu-mina alternatives, and sufficient capacity isavailable in Europe from various suppliers:Tabular alumina from market leader Almatis,or Alteo and Silkem, WFA from TreibacherSchleifmittel, Motim, Alteo, Boxitogorsk, orfrom China. These materials are based onsynthetic Bayer alumina. They have a higherprice but also provide better performance in

many applications, resulting in lower specif-ic refractory consumption and lower specificcosts [2].Lower alumina alternatives can also provideequal, and sometimes even better technicalperformance in selected applications [2] andtheir supply in Europe is practically inde-pendent from China: Andalusite from Dam-rec South Africa and France, Andalusite Re-sources in South Africa and Andalucita inPeru. Kyanite is supplied from KMC in theUS. Capacity increases have also taken placehere during the past years [5]. Mullite andmullite-chamotte materials are suppliedfrom CE Minerals in the US, Motim in Hun-gary, Nabaltec in Germany, and TreibacherSchleifmittel. For some applications lowerprice chamottes can even be an option (AGSFrance, VKV Ukraine, Cluz Czech Republic,and others). Lower alumina chamotte ma ter -ials can be upgraded by alumina additiondepending on price and quality expect -ations.New alternatives have already been devel-oped or could be considered. The sinteredaggregate BSA 96, which was launched in2010, is produced in Germany and is not de-pendent on Chinese raw material [6]. It hasproved its performance in the meantime e.g.in blast furnace runner linings, steel lancesand bricks. Production of BFA outside Chinamay be re-established sometime in the fu-ture. However, at the moment, market pricesare too low to justify this, and rising energycosts are critical especially for the fusionprocess which has a higher specific energyconsumption when compared to the sinter-ing process. In addition the sourcing of suit-able low iron bauxite independent of Chinawould be mandatory. New technologies forthe purification of iron-rich metallurgicalbauxite to give the required alumina contentfor refractory grade bauxite are under con-sideration [7].

Synthetic alumina sourcing

When considering the sourcing of aluminaraw materials strategically, it is important todistinguish between refractory bauxite andmetallurgical bauxite based materials(Fig. 4). The dependency of the world marketon Chinese or South American refractorybauxite sourcing has already been dis-cussed. Synthetic alumina based materialssuch as tabular alumina, are based on so-called Bayer alumina, which uses metallur -

Fig. 2 Price development (using 2000 as base) of high alumina raw materials during thepast decade [3]

Fig. 3 Alternatives to bauxite and BFA in Europe (estimated in steps of 50 000 t/a)

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 32

| |

Now that’s customerized!

blastcrete.com | 800.235.4867 | International 256.235.2700

MX-10 Wet Shotcrete Mixer / Pump 2200 lb. Pan Mixer AA 020 Piccola Gunite Machine

Call us today or visit getcustomerized.com to see how you can get customerized.

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 33

34 refractories WORLDFORUM 5 (2013) [3]

gical bauxite as feedstock. Metallurgicalbauxite is mined worldwide and volumes aremuch higher than for the special low iron re-fractory bauxite, which is also used in othermarkets such as abrasives (Fig. 4).More than 90 % of Bayer alumina is con-sumed in the production of aluminium. As inthe case of steel, over the past decade, China has become the biggest worldwidealumina and aluminium producer. However,in terms of total bauxite reserves China ac-counts for only 3 % of the global reserves of29 000 Mt [8]. China has become depend-ent on imports of metagrade bauxite. Metal-lurgical bauxite mining and Bayer refine-ment is carried out on all continents andtherefore supply of Bayer alumina for syn-thetic alumina refractory raw material pro-duction is independent from China. Thesematerials provide a strategic alternative.Synthetic alumina raw materials often havespecial requirements with regard to theirBayer alumina feedstock. A distinction ismade between so-called metallurgical andchemical grade alumina. In Europe, aluminaproduction accounts for only 6,4 % of globalmetallurgical alumina but for 29 % of globalchemical alumina production [9]. Thereforethe feedstock supply for synthetic aluminabased refractory raw materials is strategic-ally secured.

Development of new alternatives – partnership is “key”

All projects for the development of new rawmaterial alternatives require a long-termstrategy and considerable investment. This isobvious for new mining projects – from ini-

tial exploration, then the development of themine through to the construction of suitableinfrastructure such as rail, roads, or evennew ports. In addition, environmental as-pects will require the involvement of, andclose cooperation with, the local govern-ments. Often such new mines are in re moteareas where it is not easy to get skilled people as a workforce and intensive trainingand education are necessary. Such large in-dustrial facilities have substantial energy re-quirements and the energy companies willonly commit to supply when long-term vol-ume contracts are in place. Such contractscan become a big challenge when delays oc-cur and supply is required later than thatstated in the initial business case. For ex -ample if the market development of the newproduct starts later than predicted and thecontracted volumes are not yet required.Sound business cases are required for suchbig projects.The development of new aggregate raw ma-terials takes place on a lower economic scalewhen compared to new mining projects.However, such projects can also require con-siderable investment before an economicallysuitable new alternative can be offered tothe market. Cooperation with customersshould start in the very early stages of theproject, to define the market needs and fu-ture requirements, including technical speci-fications of new materials. In order to makea new alternative strategically viable, the ac-cess to suitable feedstock material on a longterm must also be clarified.The development and qualification of newmaterials requires extensive research and

development work for both raw materialsupplier and refractory customers. Industrialup-scaling of the laboratory work shouldalso involve the end users. Therefore thetimeline for introduction, qualification andmarket penetration of new products caneasily be several years. This must be takeninto account when defining the businesscase and considering investment in new pro-cessing units. These are often required fortechnical reasons or to avoid cross contam -ination with other existing production.For example, Almatis Ludwigshafen/DE hasinvested more than USD 6 million in a new30 000 t/a crushing and sizing facility fordifferent high alumina aggregates. This wasmandatory for the cost effective productionof the new sinter aggregate BSA 96. An -other example of cost involved with productdevelopment is the up-scaling of laboratorywork on new sinter aggregates by pilot trialsin existing production units. These are re-quired to validate laboratory results and, justas important, to provide sufficient crushedand sized material for product developmentand application test work at the refrac torycustomers. Such trials can easily cost a 6-digit USD sum, with no advance guaranteethat marketable material will be produced. Ittherefore becomes clear that even smallerscale development projects to produce newraw material alternatives require sound busi-ness cases to limit the economic risk.We must now ask what must be a funda-mental part of such business cases besidesthe usual considerations of product defin -ition and analysis, market and competitiveanalysis, technical and operational assess-ment, risk analysis, and financial assess-ment? It is the close cooperation with re-fractory customers and a clear commitmentof those customers to support the new de-velopment in order to finally achieve re-warding business for all partners involved!It must also be emphasised that such a part-nership approach is not only limited to rawmaterial suppliers and refractory producers.For the costly development of new raw ma-terial alternatives, which are driven bystrategic considerations of long term securedsourcing, it also requires the commitmentand partnership of the end users of re frac -tories. High alumina refractories or highqual ity refractories in general are essentialfor the production of high quality steel andalso for other industries such as cement,

Fig. 4 Metallurgical and refractory bauxite

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 34

When Pro ject Managers needed to re l ine the massive number 7 b last furnace, they chose Putzmeister Shotcrete Technology equipment for the job. Deploying two MR-3300 combination mixer-pumps, they were able to place 500 tons of refractory material in under 38 hours. With a mixer capacity of 3,300 lbs. and a maximum volume output of 17 cubic yards per hour, the MR-3300s made short work of the wet process application, keeping the project on schedule.

No matter what the job site throws at you, be confident thatPutzmeister Shotcrete Technology wil l del iver the r ight solution.

SOLUTIONS DELIVERED @NUMBER 7 BLAST FURNACE

1.800.553.3414 | PutzmeisterShotcrete.com

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 35

36 refractories WORLDFORUM 5 (2013) [3]

nership between raw material suppliers, re-fractory producers, and refractory end usersis essential for such projects in order to pro-vide sound business cases for the invest-ments and to achieve the desired strategicalternatives for the European refractory in-dustry. A competent and experienced localrefractory industry is important for the futuredevelopment of high temperature processesin many industries in Europe. Even in atough economic environment, business ismade between people, and reliable andstrong relationships are becoming evenmore important.

References

[1] PRE statistics, www.pre.eu

[2] Buhr, A.; Spreij, M.; Dutton, J.: Technical and eco-

nomic review of high alumina refractory raw

material for steel refractories. 53th Int. Coll. on

Refractories, Aachen 2010, 10–18

[3] Cerame-Unie, F. Wanecq: The importance of raw

materials for the European refractory industry,

European Parliament Ceramics Forum, 17. No-

vember 2010, www.pre.eu/en/raw-materials

[4] China minerals outlook – the dragon has tur-

ned. Industrial Minerals, March (2009)

[5] Andalusite Resources expansion on course. In-

dustrial Minerals, Oct. (2010)

[6] Amthauer, K.; et al.: New European sinter ag-

gregate with 96 % Al2O3. 54th Int. Coll. on Re-

fractories, Aachen 2011, 95–98

[7] Schönwelski, W.: Possible solutions for the

global shortage of refractory bauxite, refrac -

tories WORLDFORUM 1 (2009) [1] 17–22

[8] US Geological Survey Mineral Commodity Sum-

maries 2011: http://minerals.usgs.gov/minerals/

pubs/commodity/bauxite/

[9] www.world-aluminium.org

glass, petrochemistry, incineration etc. Oftenproduct and process improvements e.g. inthe manufacture of steel, are only possiblewith new, improved refractory materials. Theclose cooperation with com petent and expe-rienced refractory suppliers in the Europeanregion is seen as fundamental for the long-term success of such end user industries.It was mentioned before that, at this time,export of finished refractory products fromChina is not subject to licenses, taxes, andfees. These only apply to export of raw materials. This can provide economic ad -vantages for Chinese refractory producersselling their products in the European mar-ket because they can take advantage of low-er priced raw material sourcing. Import ofChinese refractories may be a short-termstrat-egy for refractory end users to over-come cost increases due to rising raw mate-rial costs for bauxite and BFA. However, dueto rising in ternal Chinese demand and po-tential chan ges of export policy in the future,this is not expected to be a mid or long termsolution. In addition such purchasing strate-gy in Eur ope may risk the existing supply in-frastructure in the European region andthreaten the potential for future technicaldevelopment in refractories and end userprocesses.

Function of traders

Raw material traders play an important rolefor raw material sourcing abroad. Here, thelead time is a key factor in the supply. Pro-ducing refractories on specific demand isdriven by cash flow issues and a buyer´smarket. Raw materials are only ordered forspecific projects. Lead times for raw mater -ials supplied from overseas can be up to four

months, and often traders provide the stock-ing required for short term availability andalso the financing of these stocks. In the re-cent economic crisis, risk management hasbecome an issue and stocks are an import -ant part of it. Financing of stocks requires apredictable price level for the products andreasonable supply contracts with the refrac-tory customers. It is obvious that there is aconflict between a reliable short-term supplyand purchasing at spot market prices. Theraw material trader´s involvement in thebusiness may be reduced because of limitedcommitment by the customers. It is ques-tionable if a trend towards a spot marketwould provide better economic results forthe refractory customers, when orders andbusiness could be lost because of a lack ofraw material supply.

Conclusion

The European refractory industry is import-ing about 40 % of its high alumina raw ma-terial requirements from China in the form ofrefractory bauxite and BFA. Steep price in-creases since 2007 and concerns around themid and long term availability of these ma-terials have triggered the desire for strategicalternatives. Such alternatives exist to someextent in higher or lower alumina contentmaterials, which can be sourced in Europe orother regions independent from China.However, in addition to these products, newalternatives need to be developed. Somenew materials have been launched in the re-cent past or are currently under develop-ment. Projects for new raw material mining,but also for new materials within the exist-ing infrastructure, are capital intensive andrequire a long-term strategic approach. Part-

031-036_ME_Buhr.qxp:200 28.06.2013 14:56 Uhr Seite 36