Super Groups: Legal Issues Associated with the Formation of Large Multi-site Medical Groups a...

32

Super Groups: Legal Issues Associated with the Formation of Large Multi-site Medical Groups a presentation for the Middlesex County Medical Society at Due Mari Restaurant, New Brunswick, N.J. by: Michael F. Schaff, Esq. WILENTZ, GOLDMAN & SPITZER, P.A. 90 Woodbridge Center Drive Woodbridge, NJ 07095 732-855-6047

-

Upload

sheila-owens -

Category

Documents

-

view

213 -

download

0

Transcript of Super Groups: Legal Issues Associated with the Formation of Large Multi-site Medical Groups a...

Super Groups: Legal Issues Associated with the Formation of Large Multi-site Medical Groups

a presentationfor the

Middlesex County Medical Societyat Due Mari Restaurant, New Brunswick, N.J.

by:

Michael F. Schaff, Esq.

WILENTZ, GOLDMAN & SPITZER, P.A.90 Woodbridge Center Drive

Woodbridge, NJ 07095

732-855-6047

[email protected] 17, 2012

I. Overview

• Changes in the Health Care Environment

• Physician Associations– Are Super Groups the

Answer?

• Traps for the Unwary: Assessing prospective Groups

• Questions & Answers

II. Changes in the Health Care Environment

• Managed Care– market penetration– provider panels– reduced fees– consolidation

• Greater Efficiency forced by Market– reduced fees– reduced staff– reduced overhead – greater patient volume

II. Changes in the Health Care Environment

• Regulatory change & uncertainty– Accountable Care

Organizations

– Medicare/Medicaid will change

– Reimbursement Changes

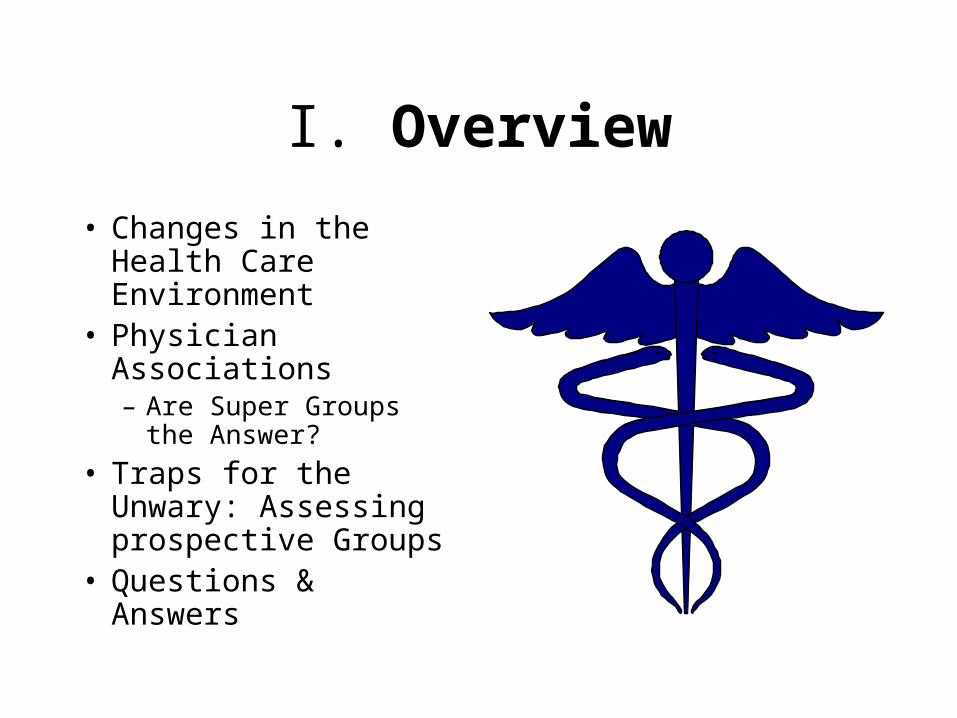

III. Physician Associations OPTIONS

• Employment in private practice; no ownership

• Employment by hospital or other entity

• Solo practice

• Group Practice– small; 2-5 Drs.

– medium; 6-15 Drs.

– large; 16- 25 Drs.

– Super Groups; 26+ Drs.

III. Physician AssociationsYour CURRENT SITUATION

• What do you want?– personal needs

– financial needs

– career needs

• Current Likes & Dislikes• Characteristics

– age

– culture

– personality

III. Physician AssociationsWHAT ALTERNATIVES EXIST?

• All’s Fine• Sell Practice & Retire• Sell Practice & Work• Contract Away Administration

– Management Service Organization (MSO)

– Physician Practice management Company (PPMC)

– Join Hospital

• Merge or Combine Practice– Into existing Super Group?– Start a new Super Group?

III. Physician AssociationsMAJOR CONSIDERATIONS

• Compensation– How much will you make?

• Group Practice– Rights & Obligations

– Control?

• Centralized Management– Benefits

– Costs

IV. Traps for the Unwary:Assessing Prospective Groups

Why Form or Join a Group Practice?

• Significant Benefits• Improved Negotiating• Increased Revenue

Sources – Ancillary Revenue

• Economies of Scale• Shared duties & info.• Coverage• Practice risks• Retirement

IV. Traps for the Unwary:Assessing Prospective Groups

Why Form or Join a Group Practice?• Significant Disadvantages• Reduced Control

– medical

– financial

• Possible change in compensation structure

• Increased Costs- Higher Overhead

• Culture “shock”

IV. Traps for the Unwary:Assessing Prospective Groups

“Culture Shock”• Different styles• Demographics

– age– specialties– culture/ethnicity

• Decision Making• Support staff • Office Policies• Integration of Information

Systems– Practice management systems– Electronic Health Records

(EHR)

IV. Traps for the Unwary:Assessing Prospective Groups

Business Issues• Administrator & Management• Staff Satisfaction• Advisors

– legal

– accounting

– consultants

• Quality of Payer Contracts

IV. Traps for the Unwary:Assessing Prospective Groups

Honeymoon Period

• May ease transition• Disassociation

planning• Cost/profit center

accounting

IV. Traps for the Unwary: Challenges in Combining Groups

Legal Hurdles• Anti-trust laws

– limits mergers that reduce competition– limited exemption for health care professional coalitions– Concerns about the use of “pseudo-merger” to engage in illegal

price fixing – Must do an analysis of increased market power vs. benefits of

integration– There is a PULL between integration requirement vs. desire for

independence• control (decision making)• sharing of profits and losses• clinical, operational and marketing integration

IV. Traps for the Unwary: Challenges in Combining Groups

Legal Hurdles• Self-referral law “group practice”

requirements– centralized billing & management– single taxpayer ID– general sharing of overhead

• Pension plan rules require coordination of plans

• Taxability of transaction– be careful; structure may have significant tax ramifications

IV. Traps for the Unwary:Assessing Prospective Groups

Level of Integration

• Partially Integrated Medical Group “PIMG”– cost/profit centers

• Fully Integrated Medical Group “FIMG”

IV. Traps for the Unwary: Combination Models

• Top to Bottom Merger is a complete merger.

• Division Model is a way to allow existing groups to retain control over various existing elements of their practice, such as staff and billing.

• Leasing Assets vs. Merger or Contributions– tax issues

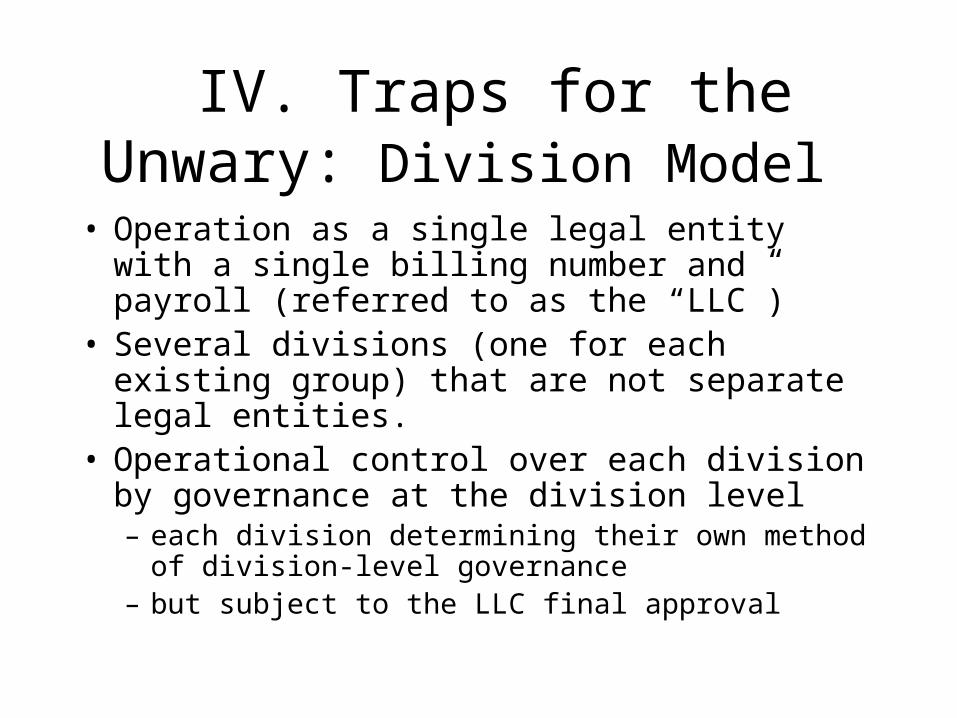

IV. Traps for the Unwary: Division Model

• Operation as a single legal entity with a single billing number and payroll (referred to as the “LLC”)

• Several divisions (one for each existing group) that are not separate legal entities.

• Operational control over each division by governance at the division level– each division determining their own method of

division-level governance– but subject to the LLC final approval

IV. Traps for the Unwary: Division Model (con’t)

• Billing and collection is done in the name of the LLC

• Buy/sell terms and obligations at – Division-level (for Division Assets) and – Centralized Level (Common Asset Level)

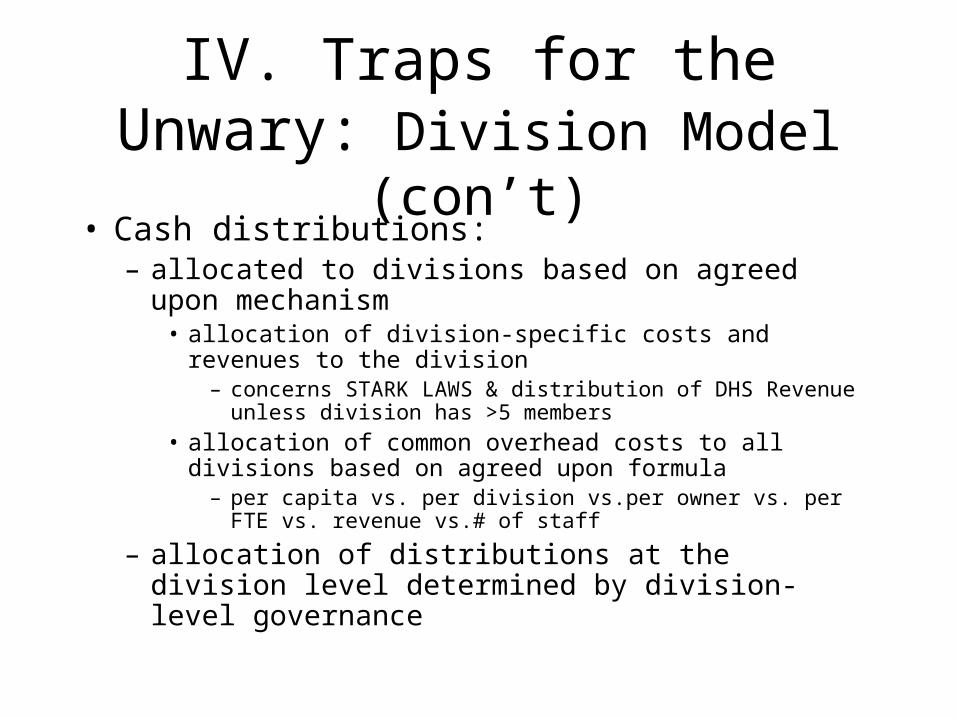

IV. Traps for the Unwary: Division Model (con’t)

• Cash distributions: – allocated to divisions based on agreed upon mechanism

• allocation of division-specific costs and revenues to the division

– concerns STARK LAWS & distribution of DHS Revenue unless division has >5 members

• allocation of common overhead costs to all divisions based on agreed upon formula

– per capita vs. per division vs.per owner vs. per FTE vs. revenue vs.# of staff

– allocation of distributions at the division level determined by division-level governance

IV. Traps for the Unwary: Division Model (con’t)

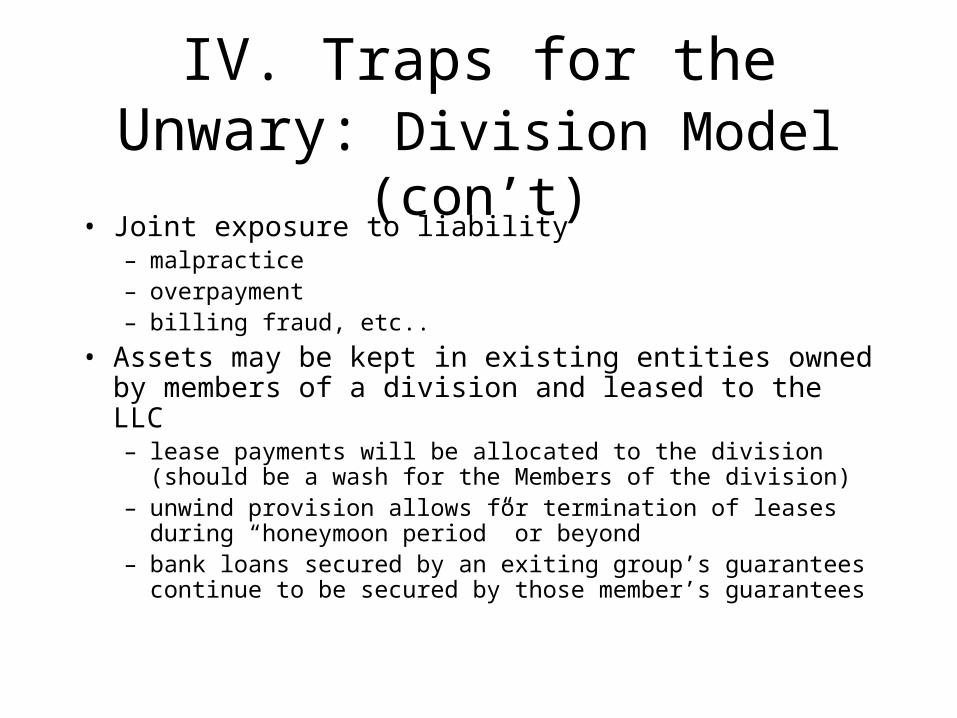

• Joint exposure to liability – malpractice– overpayment– billing fraud, etc..

• Assets may be kept in existing entities owned by members of a division and leased to the LLC– lease payments will be allocated to the division (should be a wash

for the Members of the division)– unwind provision allows for termination of leases during

“honeymoon period” or beyond– bank loans secured by an exiting group’s guarantees continue to be

secured by those member’s guarantees

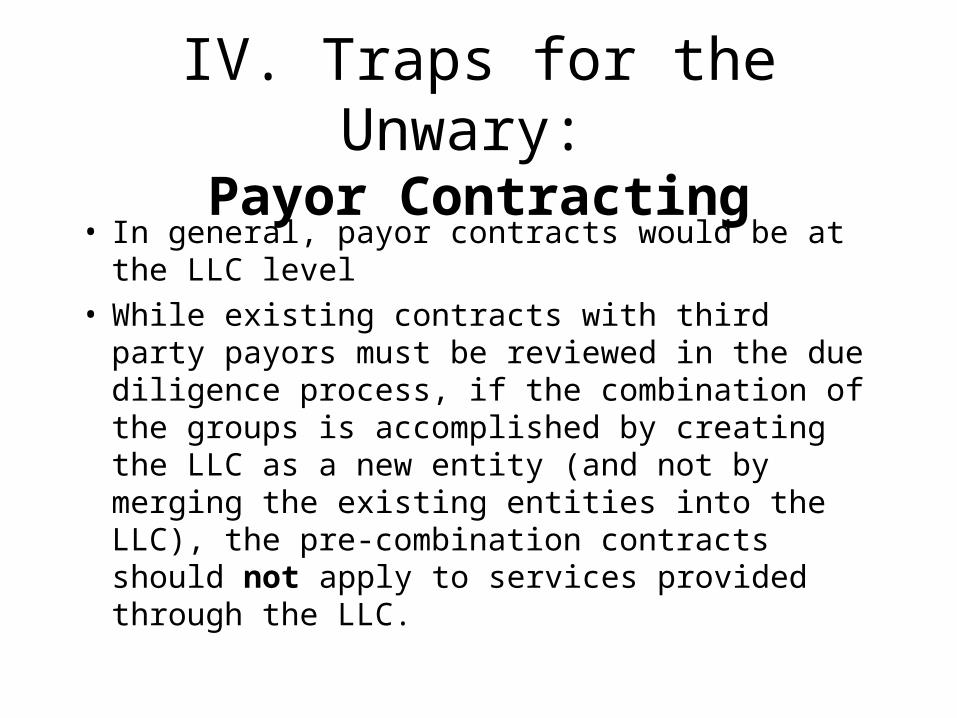

IV. Traps for the Unwary: Payor Contracting

• In general, payor contracts would be at the LLC level

• While existing contracts with third party payors must be reviewed in the due diligence process, if the combination of the groups is accomplished by creating the LLC as a new entity (and not by merging the existing entities into the LLC), the pre-combination contracts should not apply to services provided through the LLC.

IV. Traps for the Unwary:Assessing Prospective Groups

Determination of Ownership

• Value of existing practices

• Adjustments?• Equal?• Other?• Significance of

Ownership– control, compensation

& equity

IV. Traps for the Unwary:Assessing Prospective Groups

Allocation of Control• Centralized Control

– Executive or Management Committee

• Control at Division Level for daily items

• Protection for minority members

• Corporate ethics

• Business decisions

• Medical decisions

IV. Traps for the Unwary:Assessing Prospective Groups

How is Compensation Determined?• Cost/income allocation

– division level

– full integration

• Activities & status– production

– seniority or ownership

– non-medical activities

• Mechanics– formula

– committee

IV. Traps for the Unwary:Assessing Prospective Groups

How can Employment be Terminated?• Voluntary withdrawal

– retirement

– honeymoon period

• Without Cause• Cause

– loss of license, etc...

• Disability• Different Standards?• Appeal Procedure?

IV. Traps for the Unwary:Assessing Prospective Groups

Post-Termination Payments• How Determined?

– Business Valuation– Formula

• How Allocated?– Ownership Interests– Teermination/Deferred

Compensation (Tax issues)

– Restrictive Covenant

• Funding Issues

IV. Traps for the Unwary:Assessing Prospective Groups

Applicability of Restrictive Covenants

• Area and Duration• Prohibited activities• Liquidated Damages

Vs. Injuction• Trial period affect

IV. Traps for the Unwary:Assessing Prospective Groups

Agreements with Related & Unrelated Parties

• Management• Employment

– Non-medical staff

– Medical staff

• Billing & collecting• Equipment Leasing• Real Estate• Labs & ancillary

services

IV. Traps for the Unwary:Assessing Prospective Groups

Agreements with Related & Unrelated Parties -- Concerns

• Who owns entities?• Are certain members

benefiting disproportionately?

• Are non-members benefiting? Are terms “arms length”?

• Do transactions comply with laws & regulations?

V. QUESTIONS AND

ANSWERS

Super Groups: Legal Issues Associated with the Formation of Large Multi-site Medical Groups

a presentationfor the

Middlesex County Medical Societyat Due Mari Restaurant, New Brunswick, N.J.

by:

Michael F. Schaff, Esq.

WILENTZ, GOLDMAN & SPITZER, P.A.90 Woodbridge Center Drive

Woodbridge, NJ 07095

732-855-6047

[email protected] 17, 2012