Sunil Hi Tech Engineers Ltd BUY -...

23

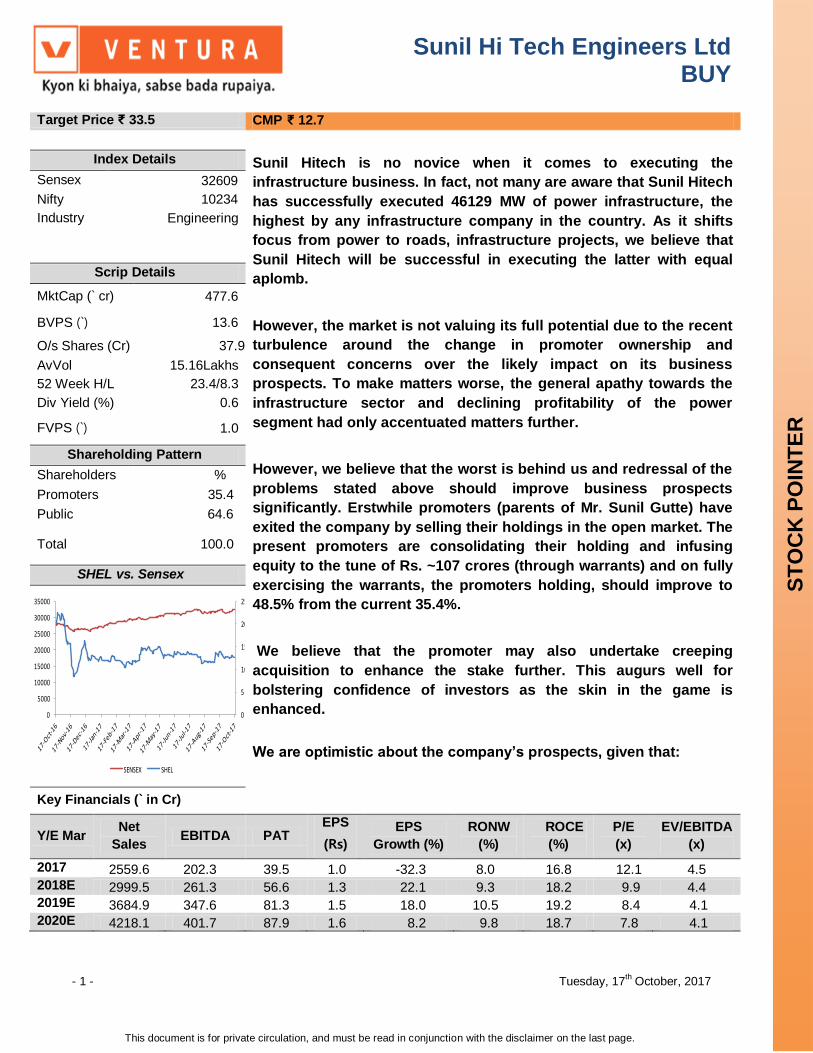

Sunil Hi Tech Engineers Ltd BUY - 1 - Tuesday, 17 th October, 2017 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. STOCK POINTER Target Price ₹ 33.5 CMP ₹ 12.7 Index Details Sunil Hitech is no novice when it comes to executing the infrastructure business. In fact, not many are aware that Sunil Hitech has successfully executed 46129 MW of power infrastructure, the highest by any infrastructure company in the country. As it shifts focus from power to roads, infrastructure projects, we believe that Sunil Hitech will be successful in executing the latter with equal aplomb. However, the market is not valuing its full potential due to the recent turbulence around the change in promoter ownership and consequent concerns over the likely impact on its business prospects. To make matters worse, the general apathy towards the infrastructure sector and declining profitability of the power segment had only accentuated matters further. However, we believe that the worst is behind us and redressal of the problems stated above should improve business prospects significantly. Erstwhile promoters (parents of Mr. Sunil Gutte) have exited the company by selling their holdings in the open market. The present promoters are consolidating their holding and infusing equity to the tune of Rs. ~107 crores (through warrants) and on fully exercising the warrants, the promoters holding, should improve to 48.5% from the current 35.4%. We believe that the promoter may also undertake creeping acquisition to enhance the stake further. This augurs well for bolstering confidence of investors as the skin in the game is enhanced. We are optimistic about the company’s prospects, given that: Sensex 32609 Nifty 10234 Industry Engineering Scrip Details MktCap (` cr) 477.6 BVPS (`) 13.6 O/s Shares (Cr) 37.9 AvVol 15.16Lakhs 52 Week H/L 23.4/8.3 Div Yield (%) 0.6 FVPS (`) 1.0 Shareholding Pattern Shareholders % Promoters 35.4 Public 64.6 Total 100.0 SHEL vs. Sensex 0 5 10 15 20 25 0 5000 10000 15000 20000 25000 30000 35000 SENSEX SHEL Key Financials (` in Cr) Y/E Mar Net Sales EBITDA PAT EPS (Rs) EPS Growth (%) RONW (%) ROCE (%) P/E (x) EV/EBITDA (x) 2017 2559.6 202.3 39.5 1.0 -32.3 8.0 16.8 12.1 4.5 2018E 2999.5 261.3 56.6 1.3 22.1 9.3 18.2 9.9 4.4 2019E 3684.9 347.6 81.3 1.5 18.0 10.5 19.2 8.4 4.1 2020E 4218.1 401.7 87.9 1.6 8.2 9.8 18.7 7.8 4.1

Transcript of Sunil Hi Tech Engineers Ltd BUY -...

Sunil Hi Tech Engineers Ltd BUY

- 1 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

ST

OC

K P

OIN

TE

R

Target Price ₹ 33.5 CMP ₹ 12.7

Index Details Sunil Hitech is no novice when it comes to executing the

infrastructure business. In fact, not many are aware that Sunil Hitech

has successfully executed 46129 MW of power infrastructure, the

highest by any infrastructure company in the country. As it shifts

focus from power to roads, infrastructure projects, we believe that

Sunil Hitech will be successful in executing the latter with equal

aplomb.

However, the market is not valuing its full potential due to the recent

turbulence around the change in promoter ownership and

consequent concerns over the likely impact on its business

prospects. To make matters worse, the general apathy towards the

infrastructure sector and declining profitability of the power

segment had only accentuated matters further.

However, we believe that the worst is behind us and redressal of the

problems stated above should improve business prospects

significantly. Erstwhile promoters (parents of Mr. Sunil Gutte) have

exited the company by selling their holdings in the open market. The

present promoters are consolidating their holding and infusing

equity to the tune of Rs. ~107 crores (through warrants) and on fully

exercising the warrants, the promoters holding, should improve to

48.5% from the current 35.4%.

We believe that the promoter may also undertake creeping

acquisition to enhance the stake further. This augurs well for

bolstering confidence of investors as the skin in the game is

enhanced.

We are optimistic about the company’s prospects, given that:

Sensex 32609

Nifty 10234

Industry Engineering

Scrip Details

MktCap (` cr) 477.6

BVPS (`) 13.6

O/s Shares (Cr) 37.9

AvVol 15.16Lakhs

52 Week H/L 23.4/8.3

Div Yield (%) 0.6

FVPS (`) 1.0

Shareholding Pattern

Shareholders %

Promoters 35.4

Public 64.6

Total 100.0

SHEL vs. Sensex

0

5

10

15

20

25

0

5000

10000

15000

20000

25000

30000

35000

SENSEX SHEL

Key Financials (` in Cr)

Y/E Mar Net

Sales EBITDA PAT

EPS

(Rs)

EPS

Growth (%)

RONW

(%)

ROCE

(%)

P/E

(x)

EV/EBITDA

(x)

2017 2559.6 202.3 39.5 1.0 -32.3 8.0 16.8 12.1 4.5 2018E 2999.5 261.3 56.6 1.3 22.1 9.3 18.2 9.9 4.4 2019E 3684.9 347.6 81.3 1.5 18.0 10.5 19.2 8.4 4.1 2020E 4218.1 401.7 87.9 1.6 8.2 9.8 18.7 7.8 4.1

- 2 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Order book of 5018 crores as on 30th June, 2017 (2x FY17 revenues)

continues to remain robust and this should lead to sustaining the strong

revenue growth of 18.1% CAGR to Rs. 4218.1 by FY20.

Margins are set to expand as the revenue share of the high margin road

business improves. We expect margins to improve by ~160 bps to 9.5% by

FY20.

Recently, the company won a Hybrid Annuity Model (HAM) project for Rs

982 crores. We believe that the high ROCE HAM projects would encourage

the management to up its bidding for further such projects as the way

forward.

Earnings are expected to grow at a CAGR of 30.6% to Rs 87.9 crores by

FY20 with a healthy improvement in return ratios of ROE and ROCE by 180

bps and 200bps to 9.8% and 18.7% respectively.

With ratios returning to industry levels, the valuation is also expected to

improve sharply.

Currently the stock trades at 4.1x FY19 EV/EBITDA which is at a significant

discount of ~83% to the median industry level of 9.2x FY19EV/EBIDTA. We

recommend a BUY at the CMP of Rs 12.7 for a price target of Rs 33.5,(7.5x

FY19EV/EBIDTA) representing an upside of 165.7% over a period of 24

months.

- 3 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Company Background

Sunil Hitech Engineers Limited (SHEL), a major Engineering, Procurement &

Construction (EPC) Company, started its journey as M/s. Sunil Engineering

Works (SEW) in 1984 (a proprietary company led by Mr. Ratnakar M. Gutte). In

1998, the company got incorporated as Sunil HiTech Engineers Pvt. Ltd. The

company was converted into Sunil Hitech Engineers Ltd (“SHEL” or “The

Company”) on, 18th August 2005 and got listed in 2006. The company

undertakes EPC projects across the business segments of power, roads,

building construction and has an impressive list of marquee clients. Recently,

the company has also won an award for a HAM project.

Business Verticals of Sunil Hitech Ltd

Source :Sunil Hitech Ltd, Ventura Research, (FY17 consolidated segment wise classification not yet available), RS- Revenue share

Impressive portfolio of marquee clients

Source :Sunil Hitech Ltd, Ventura Research (FY17 consolidated segment wise classification not yet available)

- 4 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Investment Highlights

Strong revenue growth on the cards

Historically revenues grew at a scorching pace but margins were

sacrificed

Over the period FY07 to FY13, the revenues of SHEL grew at a handsome

CAGR of 42.7% to Rs 1252.8 crore in FY13 from Rs 148.3 crore clocked in

FY07. This growth journey was primarily driven by order wins from the power

sector and the business margins peaked at 14.6% (in FY11). However, with new

projects coming to a standstill amidst intense competition, margins took a hit

falling by 300bps over the period FY11-13. Realizing the shifting dynamics of

the power segment, the company took a conscious decision to diversify towards

road EPC as they are high ticket orders as compared to power EPC business

and thus with increasing contribution from road EPC, margins are expected to

get a boost.

The period FY14-17 saw margins stagnate below 10% (except FY16 where

margins just touched 10%) and hit a trough of 7.9% in FY17 due to a one time

write off to the tune of Rs 19.5 crore on account of bad debts. Despite poor

margins the revenues have grown at a healthy CAGR of 17.6% from Rs 1574.6

crore in FY14 to Rs 2559.6 crore in FY17.

Although the management has guided for >10% margins in coming years as

activity in road segment gathers pace, we would like to err on the side of caution

and require to see the proof in the pudding. We have therefore built margins of

8.7%/9.4%/9.5% in FY18/19/20.

Historical strong growth at the cost of margins

0

2

4

6

8

10

12

14

16

18

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Sales EBIDTA EBIDTA margins (%)

Rs in cr

(%)Margins were compressed from FY14-17

Margins to return to >10% levels.Margins > 10%

CAGR 42.7%

Source: Sunil Hitech Ltd, Ventura Research

Margins fell in FY17 due to one time write off on account of bad debt to the tune of Rs

19.5 crores.

- 5 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

During FY15-17, the revenues from the roads witnessed a sharp ramp up as the

order book bulged.

Strong order backlog to maintain high growth in revenues

With a current order book of Rs 5018 crore, we expect net revenues to grow at a

CAGR of 18.1% from Rs 2559.6 crore in FY17 to Rs 4218.1 crore in FY20 on

the back of:

a) The NHAI plans to build 50,000 km of roads worth USD 2.5 billion by

2022 as part of a long term goal of doubling the length of the national

highway network to 2,00,000 km.

b) The management has guided for an order intake of 3500-4000 crore

in FY18, which will help the company maintain an order book size of

2x-2.2x company’s sales.

c) The company has received LoA for four/six laning of the Bodhre to

Dhule stretch of new NH-211 from NHAI in Maharashtra under the

Hybrid Annuity Model (HAM) of Rs 982 crore.

Sunil Hitech has historically seen strong order book and is expected to maintain the growth

Particulars (Rs in crores) FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Opening order book 1702.0 1723.4 2295.0 3243.0 3580.0 3249.6 5189.2 5863.8 6743.4

Add: Order Inflow** 979.2 1824.5 2522.6 2173.5 1690.9 4499.2 3674.1 4564.5 5229.6

Less: Execution* 957.8 1252.8 1574.6 1836.5 2021.3 2559.6 2999.5 3684.9 4218.1

Closing order book 1723.4 2295.0 3243.0 3580.0 3249.6 5189.2 5863.8 6743.4 7754.9

a)Civil and sructural 1420.5 1338.5 1086.6 901.5 630.3 269.3

b)Roads 494.4 863.5 3183.5 3664.8 3767.8 3289.8

c)Others 1665.1 1047.6 919.1 1297.5 2345.3 4195.8

Revenues 957.8 1252.8 1574.6 1836.5 2021.3 2559.6 2999.5 3684.9 4218.1

Book to bill (x) 1.8 1.8 2.1 1.9 1.6 2.0 2.0 1.8 1.8

Source: Sunil Hitech Ltd, Ventura Research (Order book bifurcation not available for FY12-14)

As revenues from roads picks up….EBIDTA will improve

Particulars (Rs in cr) FY15 FY16 FY17

Roads revenue 0.0 101.2 327.9

Roads order book 494.4 863.5 3183.5

Overall EBIDTA margins in % 9.4 10.2 7.9

Source: S Source: Sunil Hitech Ltd, Ventura Research

- 6 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Further the management has guided for an order intake of 3500-4000 crore in

FY18, which will help the company to maintain order book size of ~2x

company’s sales.

We believe that Sunil Hitech should achieve its guidance as the company is

slowly carving a niche in the road segment which is visible from the fact that

recently the company’s qualification for Road EPC projects from NHAI and

MORTH was upgraded to 2/4/6 lanes from erstwhile 2/4 lane projects. Similarly,

the company is now qualified to bid for EPC projects worth upto Rs 700 crore

(500 crore earlier) and BOT and Annuity projects of upto Rs 1200 crore (900

crore earlier). Besides EPC for roads, the company has also forayed into EPC

for various high growth sectors like solar, railways, water and sewage

management.

Going forward HAM will be the preferred vehicle for Road EPC thrust

Recently, SHEL has won its first HAM project to construct and widen the

existing 2-lane Bodhre to Dhule road section of NH-211 to four/six lane

configuration in the State of Maharashtra for a consideration of Rs 982 crores.

Besides this, there is also a provision of 6% inflation over the awarded price for

the project. The project is to be completed by April, 2021. SHEL will execute the

project through its subsidiary in which it will have a 70% stake. As per the

management, the total cost of the project is around Rs 800 crores and the

company will receive a grant from NHAI to the tune of Rs 425 crore, which will

bring down the project cost to Rs 375 crores. Of this Rs 375 crore, the equity

component will be for Rs 75 crores while the remaining component will be raised

via debt. This project will open doors for SHEL to win many such projects in the

HAM segment in the future.

HAM project capital structure

Particulars Rs in cr Rs in cr Rs in cr

Awarded Price 982.0

Cost of Project

i) Grant by NHAI 425

ii) Funding to be done

Debt @ 80% 300.0

Equity @ 20% 75.0 375.0 800.0

Source: Sunil Hitech Ltd, Ventura Research

- 7 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

We have valued the HAM project of Rs 982 crore separately by discounting the

future cash profits @ 9.2% (which is the weighted average cost of capital) and

have arrived at the present value of future cash profits. Accordingly, we have

arrived at the share value of Rs 5.6 by March, 20.

Onward strategy: More of Roads, less of Power

SHEL has selected to focus on road building (via EPC or HAM) and civil

construction projects while moderating exposure to Balance of Plant power

projects which enjoys low margins as compared to roads. This will progressively

increase the minimum hurdle rate as far as profitability is concerned, enable

cost-effective project execution, timely receivables and a lower debt

dependence. This has begun to strengthen the Company’s overall margins and

business sustainability in the last three years. Further the segment has also

proved to be highly margin accretive and management expects the margins to

be around ~12-14% in this segment in the future.

The road segment is also expected to be a big contributor to the order book of

the company going forward (current order book of Rs 3183.5 crore). This is also

visible by the fact that the order book for roads has increased at a staggering

rate of 153.8% over FY15-17.

Value of HAM project per share

Valuation of HAM project

FV at end of Mar,20 320.5 crores

FV at end of Mar,19 293.6 crores

FV at end of Mar,18 269.0 crores

PV as on 30th Sept,2017 @ 9.2% 257.2 crores

No of shares as on date 37.8 nos

Value per share as on date 6.8 Rs/share

No of shares as on Mar 18 51.0 nos

Value per share as on Mar 18 5.3 Rs/share

No of shares as on Mar 19 57.2 nos

Value per share as on Mar 19 5.1 Rs/share

No of shares as on Mar 20 57.2 nos

Value per share as on Mar 20 5.6 Rs/share

Source: Sunil Hitech Ltd, Ventura Research

- 8 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

We expect overall revenues from the road segment to grow at a CAGR of 54.4%

over FY17-20 to Rs 1478 crore in FY20 as the company starts booking

revenues from the HAM project.

Further, the company expects to receive early completion bonus for the

Bankura-Purulia project in the range of Rs 9.5-10 crores, which proves the

company’s execution capability in the road segment.

Road order book grew at CAGR of 153.8%

494.4

863.5

3183.5

0

500

1000

1500

2000

2500

3000

3500

FY15 FY16 FY17

Road order book

Rs in cr

Source: Sunil Hitech Ltd, Ventura Research

Road revenues expected to see significant jump

0

2

4

6

8

10

12

14

0

200

400

600

800

1000

1200

1400

1600

FY17* FY18E FY19E FY20E

Rs in crores (%)

Source: Sunil Hitech Ltd, Ventura Research *Consolidated figure is estimated from standalone figure breakup

- 9 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

EPC for Power (Structural & Civil)

The Company entered this business vertical space in 1998 and was associated

with the completion of 46129 MW worth of power plants in India, the largest by

any company.

The Company specialises in EPC / turnkey projects up to 800MW, erection of

boilers, TG and auxiliaries, BTG renovation and modernisation, T&D projects,

overhauling, operation and maintenance of power plants upto 600 MW.

Further, the Company possesses in-house engineering and fabrication

competence in boiler components through subsidiary SEAM Industries Limited

(94% holding).

The company also plans to foray into EPC for solar power projects and as a

pilot, the company commissioned a self owned 5 MW EPC renewable energy

project in Solapur (through a 100%-subsidiary) for establishing qualification for

the EPC solar sector. The plant generated revenues of Rs 5.9 crore in FY17.

We expect revenues from Civil & Structural business to remain more or less

stable as the company focuses more and more on road EPC. As per our

Ongoing road projects and their status of completion

Name of the Project and authority Scope Amt in cr Date of LOA Completion Year

Bankura- Purulia Road Section of NH60 A- MORTH 84 Km 322.0 3/31/2017 Mar-18

Sitamrahi- Jaynagar- narahia section of NH-104

MORTH 28.5Km 154.7 10/15/2015 May-18

Sitamrahi- Jaynagar- narahia section of NH-104

MORTH 77.1 Km 319.7 10/15/2015 Dec-18

Madhugiri- Mulbagal Road Section MORTh 56.5 Km 122.0 2/27/2015 Jul-17

Hunli- Anini Stretch - NHIDCL 92.5 Km 434.0 9/12/2016 Oct-19

Bodhre - Dulhe Section of NH -211- NHDP-IV 67.2 Km 982.0 3/2/2017 Apr-21

Parli-Pimpa Dahiguda Road- MORTH 18.4 Km 134.5 3/30/2017 Jun-19

Mehkar to Ajispur -MORTH 35.8 Km 160.2 3/31/2017 Jul-17

Ajanta- Buldhana- Khamgaon- Shegaon- Deori

Road- MORTH 49.1 km 257.4 3/31/2017 Aug-19

Nanded- Bhokar- Himayatnagar- Kinwat-Sarkhani-

Mahur-Arni Road- MORTH 57 km 308.2 3/30/2017 Jun-19

Kutchery Chowk-Ranchi-Piska Mre-Biju Para

section- NHAI 34 km 235.9 3/31/2017

Appointed date yet

to be finalised

Total 3430.5

S Source: Sunil Hitech Ltd, Ventura Research

- 10 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

estimates, we expect a dip in revenues in FY18 from this segment mainly due to

a decline in the order book. However, post that, we expect the company to again

pick up activity in this segment and to return to ~811 crore levels by FY20.

Major Projects undertaken for Power

Project Description CV Inr crs

Koradi- MAHAGENCO

Civil, structural & Arch works of

3x660W Main plant package 215.0

DB Power- Raigad, CG

Civil, structural & Arch works of

2x660W Main plant & BOP

package 170.0

NTPC Kudgi

Construction of Ash Dyke for

3x800MW 183.0

NTPC Meja

CW and make up water system

package of 2x660MW 174.9

MAHAGENCO Parli

Balance of Plant (BOP) Package on

EPC Basis 487.0

BHEL North Karanpura

Main Plant Civil works package of

Unit-1 &3, 3x660 200.0

ACPL/Abir Singhi Rtarai

Erection testing & Commissioning

of boilers for 2x600 MW 130.0

Source: Sunil Hitech Ltd, Ventura Research

Civil & structural revenues to see flat growth

6

7

8

9

10

0

100

200

300

400

500

600

700

800

900

FY17* FY18E FY19E FY20E

Rs in crores (%)

Source: Sunil Hitech Ltd, Ventura Research *Consolidated figure is estimated from standalone figure breakup

- 11 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Solid waste management- A high growth opportunity

Sunil Hitech views this segment as a high-growth business and possesses the

requisite technical expertise to execute large and complex projects in the urban

solid waste management space. Further, the company is undertaking Solid

Waste Management projects worth Rs 220 crore at Patna (Bihar) and Kolhapur

(Maharashtra).

EPC Buildings- Steady Performace

The Company entered the buildings space for Public Works Department (PWD)

and other Govt. departments, providing construction services for hospitals,

national institutions, government housing projects, industrial, commercial

buildings, hostels and industrial sheds etc. SHEL is qualified for up to Rs 500

crores for a single project for government buildings. However, SHEL has said

that it would focus more on institutional buildings like IITs, IIMs, AIIMS and

administration building, etc. The company’s order book in this segment stands at

Rs 630.1 crore as on 31st March, 2017. The Company enjoys a margin of 7.5-

9% in this segment.

We expect overall revenues from the Buildings segment to grow at a CAGR of

6.7% over FY17-20 to Rs 687.1 crore in FY20.

Buildings EPC to see moderate growth

6

7

8

9

10

0

100

200

300

400

500

600

700

800

FY17* FY18E FY19E FY20E

Rs in crores (%)

Source: Sunil Hitech Ltd, Ventura Research

* Consolidated figure is estimated from standalone figure breakup

- 12 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

O & M – a high margin business

Over the years, the Company has extended its business to operations,

overhauling and maintenance (renovation and modernization) for power and

steel plants. The Company’s service portfolio covers the entire spectrum of

operations and maintenance - boilers, turbine generators and auxiliaries; repair,

modification and rehabilitation for utility boilers up to 800 MW; pressure plants,

milling system, rotating parts and ducting; high pressure/low pressure piping

works; renovation, modernisation and retrofitting of ESP; coal and ash handling

plants. We expect overall revenues from the segment to grow at a CAGR of

15.5% over FY17-20 to Rs 950 crore in FY20.

Major Projects for EPC Buildings

Projects Description

CV INR

(Crs.)

Kanpur- KDA Construction of EWS Houses 89.4

Singreni- SCCL

Construction of Staff quarters, GM

Bungalow at Singareni TPP 92.3

Bihar -BSHB

Construction of 1054 flats at Dalpatpur

(G+11) 415.5

Firozabad-UPRNNL

Construction of medical college

buildings 130.0

Bathinda & Govindval Construction of Central Sudhar Griha 350.0

Source: Sunil Hitech Ltd, Ventura Research

OM/BoP to see good growth

6

7

8

9

10

0

100

200

300

400

500

600

700

800

900

1000

FY17* FY18E FY19E FY20E

Rs in crores(%)

Source: Sunil Hitech Ltd, Ventura Research

* Consolidated figure is estimated from standalone figure breakup

- 13 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Manufacturing

SHEL undertakes manufacturing of Super heater and re-heater coils,

Economizer and LTSH coils, Water wall panels, High pressure parts bend,

Technological structures for power and process industry, Tanks and vessels

Piping, Boiler pressure parts tubes up to 660 MW, Collection and emitting

electrodes of ESP. Most of the manufacturing work is done by its subsidiary

Seam Industries Limited.

We expect overall revenues from the segment to grow at a CAGR of 30% over

FY17-20 to Rs 292 crore in FY20.

Fresh Infusion of equity by promoters- lends credence to the growth story

and will help shore up debt to equity

In order to meet the working capital requirements and future capex of the

company, the promoter of the company has been allotted 7.4 crore warrants at

conversion price of Rs 14.43 for 1 equity share of FV of Rs 1. Further, the

promoter of the company has already got 34.75 lakh warrants issued which is

convertible at Rs 55.4 (The price after bonus and split works out to be Rs 2.77

per share). Thus, the promoter of the company has committed ~Rs 107 crore

over the next 18 months which will help the company to maintain debt at

sustainable levels. Further, we believe that the promoter group will try to infuse

more funds into the business to shore up their holding in the company in the

long run. Prior to Mr Sunil Gutte taking over as CEO/MD, the erstwhile promoter

Mr Ratnakar Gutte (Father of Mr Sunil Gutte) had exited his shareholding by

selling his stake in the open market. Subsequently, he resigned from the

company and from his post.

Boilers & Auxiliaries to see good growth

6

7

8

9

10

0

50

100

150

200

250

300

350

FY17* FY18E FY19E FY20E

Rs in crores (%)

Source: Sunil Hitech Ltd, Ventura Research

* Consolidated figure is estimated from standalone figure breakup

- 14 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Proposed listing of its 2 subsidiaries- VAG Buildtech Limited and Seam

Industries Ltd on the SME platform to help unlock value

VAG Buidtech Limited is the infrastructure development arm of SHEL and

focuses on urban infrastructure, solid waste management and road

development. In 2017, the company achieved topline of 185.9 crore and PAT of

Rs 4.0 crore,

Seam Industries Limited manufactures boiler pressure parts and components,

industrial boilers, ROB and RUB railway girder slabs, steel pipes, and pipe

fittings etc and complements Sunil Hitech’s EPC Projects. It had achieved a

topline of Rs 149.0 Crores and a PAT of Rs 2.6 crores for the year ended 31st

March 2017.

As per the BSE filling dated 18.08.2017, the company has proposed to list its 2

subsidiaries VAG Buildtech Limited (subsidiary of SHEL with 74% stake as on

today) and SEAM Industries Ltd (subsidiary of SHEL with 94% stake as on

today) for fresh issue of equity shares. We believe that potential listing will help

the company to raise money for its future projects in both the subsidiaries and

will also help in unlocking of value for SHEL.

Financials of VAG Buildtech Pvt Ltd

Particulars

Year Ending FY15 FY16 FY17

Contract Receipts 150.5 174.8 185.9

Other Income 1.2 0.2 0.2

PBDIT 9.8 11.0 4.2

Interest Expenses 2.7 3.4 3.9

Depreciation 0.1 0.2 0.3

PAT 4.7 5.0 4.0

Cash Accruals 4.8 5.1 4.3

Term Debt- Secured 3.1 3.3 6.5

Term Debt – Unsecured - 3.1 -

Short Term Borrowings 0.0 17.1 24.3

Tangible Net Worth 10.0 16.1 20.1

Rs in crores

Source: Sunil Hitech Ltd, Ventura Research

Financials of SEAM Industries Ltd

Particulars

Year Ending FY15 FY16 FY17

Contract Receipts 165.8 156.9 149.0

Other Income 0.8 0.6 0.4

PBDIT 20.9 15.7 12.2

Interest Expenses 9.3 8.2 8.8

Depreciation 4.9 3.6 3.4

PAT 4.2 2.4 2.6

Cash Accruals 9.1 6.0 6.0

Term Debt- Secured 9.6 4.5 2.3

Term Debt- Unsecured 3.0 8.4 9.7

Short Term Borrowings 38.3 43.0 38.0

Tangible Net Worth 38.6 41.0 43.7

Rs in crores

Source: Sunil Hitech Ltd, Ventura Research

- 15 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Key Risks

SHEL has contingent liabilities of Rs 796 crore as on 31st March,2017

Infra companies normally have a huge amount of contingent liabilities in their

books by way of performance guarantees. Although this is inherent risk for every

infra company, going forward, we expect an increase in such contingent

liabilities as the company aims to bid for more and more road projects.

Other Risks

1. Delay in project execution can shift revenue trajectory

2. Major policy changes

Contingent liability comparison of peer companies

Particulars (Rs. in Crs.) FY15 FY16 FY17

Sunil Hitech

Cont liabilities 28.4 638.6 796.0

Networth 411.2 466.7 519.7

Revenues 1,836.5 2,021.3 2,559.6

As a % of networth 6.9 136.8 153.2

Dilip buildcon

Cont liabilities 2,409.6 2,246.2 2,900.0

Networth 805.1 932.1 1,719.0

Revenues 2,762.0 4,300.5 5,319.2

As a % of networth 299.3 241.0 168.7

PNC infra

Cont liabilities 1,137.7 1,274.7 1,631.7

Networth 871.1 1,357.9 1,461.0

Revenues 1,860.9 2,836.8 2,252.3

As a % of networth 130.6 93.9 111.7

Ashoka buildcon

Cont liabilities 1,215.5 2,970.7 3,541.8

Networth 1,356.9 1,714.6 1,671.7

Revenues 2,290.1 2,223.7 2,904.9

As a % of networth 89.6 173.3 211.9

Sou Source: Sunil Hitech, Ventura Research

- 16 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Performance

In Q1FY18, SHEL Ltd reported a robust 23.5% growth in its standalone topline

to Rs 548.4 crore from Rs 444.0 crore reported in Q1FY17. The EBIDTA

margins declined by around 60 bps, from 9.6% to 9.0%, due to an increase in

contract and site expenses. The total PAT stood at Rs 13.7 crore as against Rs

11.2 crore in Q1FY17, registering growth of 23.2% YoY.

During FY17, SHEL’s consolidated topline stood at Rs 2559.6 crore, registering

a growth of 26.6% YoY. The EBIDTA margin decreased by ~228 bps YoY to

7.9%, mainly due to the writing of bad debts to the tune of Rs 19.5 crore in the

power segment. The PAT stood at Rs 39.5 crore, declining by 26.1% YoY

mainly due to lower margins and an increase in interest costs.

Financial Performance (Rs in crores)

Description Q1FY18* Q1FY17* FY17 FY16

Profit & Loss Statement

Net Sales 548.4 444.0 2559.6 2021.3

Growth(%) 23.5% 26.6%

Total Expenditure 499.2 401.4 2357.3 1815.4

% of sales 91.0% 90.4% 92.1% 89.8%

EBDITA 49.1 42.6 202.3 205.9

EBDITA Margin % 9.0% 9.6% 7.9% 10.2%

Other Income 5.6 4.1 13.3 14.2

PBDIT 54.7 46.7 215.7 220.1

Depreciation 8.6 7.7 38.2 36.8

Interest 25.4 22.0 110.9 98.4

Exceptional items 0.0 0.0 0.0 0.0

PBT 20.8 17.0 66.6 85.0

Margin % 3.8% 3.8% 2.6% 4.2%

Tax Provisions 7.0 5.8 25.9 29.1

Minority Interest NA NA -1.2 -2.4

Reported PAT 13.7 11.2 39.5 53.4

Margin % 2.5% 2.5% 1.5% 2.6%

Sou Source: Sunil Hitech Ltd, Ventura Research *Standalone figures

- 17 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financial Outlook

The revenue trajectory is expected to continue to grow, going forward, as the

management expects to maintain its order book at ~2x trailing sales to fuel its

growth. We expect overall revenues to grow at a CAGR of 18.1% over FY17-20

to Rs 4218.1 crore from Rs 2559.6 crore reported in FY17. We expect the

EBIDTA of the company to move from Rs 202.3 crore in FY17 to Rs 401.7 crore

in FY20. The margins are expected to move gradually to 9.5% in FY20 from

7.9% in FY17 as the company plans to increase its revenue share of Road EPC

in the overall sales mix (Road EPC has better margins of ~12% relative to other

segment).

We expect the profitability to more than double by FY20 to Rs 87.9 crore from

Rs 39.5 crore in FY17. However, the conversion of warrants will remain an

overhang on the EPS in the short term and hence we expect the EPS to grow to

Rs 1.6 in FY20 from Rs 1 posted in FY17.

Revenues, EBIDTA and PAT margins

0

2

4

6

8

10

12

14

0

500

1000

1500

2000

2500

3000

3500

4000

4500

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Net sales EBIDTA (%) PAT (%)

Rs in cr (%)

Source: Sunil Hitech Ltd, Ventura Research

- 18 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

We expect the company to post better return ratios and increase its interest and

debt paying capacity due to the expansion of EBIDTA. However, we expect the

working capital cycle to stay moderate as SHEL tries to add more and more

orders in roads and institutional building, which will keep debtor days at an

elongated level of ~ 3 months.

Improving financials to boost ROE and ROCE

0

5

10

15

20

25

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

ROE (%) ROCE (%)

(%)

So Source: Sunil Hitech Ltd, Ventura Research

Operating cycle to remain moderate

0

20

40

60

80

100

120

140

160

180

FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Inventory days Receivable days Payable days Total

No of days

So Source: Sunil Hitech Ltd, Ventura Research

- 19 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Valuation

We initiate coverage on Sunil Hitech as a BUY with a SOTP price objective of

Rs 33.5, representing a potential upside of 165.7% over a period of 24 months

from the CMP of Rs 12.7.

Valuation table

Particulars Basis

Multiple

(x)

EV ( Rs in

crores)

Value of Civil & Strucutral business FY20E EBIDTA- 60.8 crore 6.1 370.9

Value of EPC for Buildings FY20E EBIDTA- 61.8 crores 6.2 383.2

Valuation of EPC for Roads FY20E EBIDTA- 124.8 crores 7.0 873.6

Value of Boilers & Auxiliaries FY20E EBIDTA- 20.4 crores 6.1 124.4

Value of BoP, O&M FY20E EBIDTA- 96.0 crores 8.0 768.0

Total EV excluding HAM project 2520.1

Less- FY20 Debt 1138.2

Add- FY20 Cash 212.2

Market Capitalisation 1594.0

No of shares outstanding 57.2

Value per share 27.9

Value per share of HAM project 5.6

Total value per share 33.5

Source: Sunil Hitech Ltd, Ventura Research

- 20 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

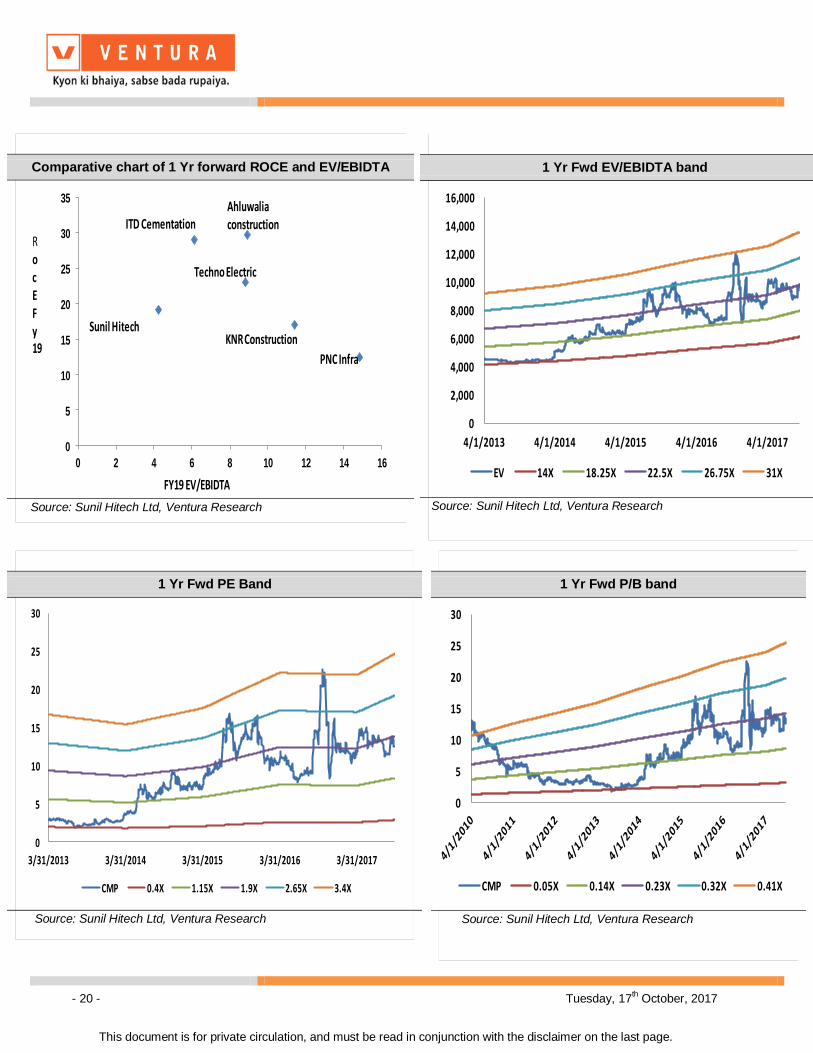

1 Yr Fwd PE Band

0

5

10

15

20

25

30

3/31/2013 3/31/2014 3/31/2015 3/31/2016 3/31/2017

CMP 0.4X 1.15X 1.9X 2.65X 3.4X

Source: Sunil Hitech Ltd, Ventura Research

1 Yr Fwd P/B band

0

5

10

15

20

25

30

CMP 0.05X 0.14X 0.23X 0.32X 0.41X

Source: Sunil Hitech Ltd, Ventura Research

Comparative chart of 1 Yr forward ROCE and EV/EBIDTA

0

5

10

15

20

25

30

35

0 2 4 6 8 10 12 14 16

Ahluwaliaconstruction

Techno Electric

KNR Construction

PNC Infra

Sunil Hitech

ITD CementationRocEFy19

FY19 EV/EBIDTA

Source: Sunil Hitech Ltd, Ventura Research

1 Yr Fwd EV/EBIDTA band

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

4/1/2013 4/1/2014 4/1/2015 4/1/2016 4/1/2017

EV 14X 18.25X 22.5X 26.75X 31X

Source: CMI Source: Sunil Hitech Ltd, Ventura Research

- 21 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Peer Comparison (Rs in crores)

Y/E March Sales EBITDA PAT

EBITDA

Margin (%)

PAT Margin

(%) ROE(%) ROCE(%) P/E P/BV

EV/

EBITDA

Sunil Hitech

2016 2021.3 205.9 53.4 10.2 2.6 12.2 19.5 6.9 0.8 3.7

2017 2559.6 202.3 39.5 7.9 1.5 8.0 16.8 12.1 0.9 4.5

2018E 2999.5 261.3 56.6 8.7 1.9 9.3 18.2 9.9 0.8 4.4

2019E 3684.9 347.6 81.3 9.4 2.2 10.5 19.2 8.4 0.8 4.1

PNC Infratech

2016 2346.1 407.3 177.2 17.4 7.6 17.8 15.6 65.0 2.0 19.8

2017 2109.9 624.1 118.3 29.6 5.6 13.3 9.8 25.4 2.1 23.9

2018E 2513.8 482.5 158.1 19.2 6.3 9.6 9.4 87.6 2.0 19.8

2019E 3607.0 622.4 201.9 17.3 5.6 12.0 12.5 29.7 1.8 14.8

KNR Construction

2016 993.7 174.2 126.4 17.5 12.7 15.1 11.4 12.8 2.1 23.0

2017 1641.6 264.0 125.8 16.1 7.7 15.2 31.0 23.6 3.3 15.6

2018E 1938.7 337.7 172.0 17.4 8.9 14.5 17.2 22.9 2.0 13.0

2019E 2321.5 392.6 188.5 16.9 8.1 14.4 17.1 19.9 1.7 11.4

J kumar Infra

2016 1366.2 248.4 103.2 18.2 7.6 10.0 16.8 18.4 1.6 8.6

2017 1572.8 249.4 105.6 15.9 6.7 7.9 13.6 18.5 1.4 8.5

2018E 1851.7 312.0 127.4 16.8 6.9 11.5 15.6 12.0 1.1 6.5

2019E 2325.6 395.6 164.7 17.0 7.1 12.1 16.2 9.3 1.0 5.2

ITD Cementation

2016 3088.6 209.9 48.1 6.8 1.6 9.1 27.5 48.1 4.2 11.0

2017E 2433.1 267.5 88.7 11.0 3.6 14.6 20.4 29.4 4.0 8.7

2018E 2927.5 314.6 129.1 10.7 4.4 18.8 22.8 18.8 3.3 7.2

2019E 3508.9 381.6 167.3 10.9 4.8 19.7 29.1 15.1 2.8 6.1

Ahluwalia Construction

2016 1246.9 160.8 84.4 12.9 6.8 22.2 27.7 24.1 4.8 12.9

2017 1426.5 173.0 86.0 12.1 6.0 18.5 25.9 24.4 4.1 11.7

2018E 1601.6 197.6 108.8 12.3 6.8 18.3 27.9 19.8 3.4 10.4

2019E 1791.1 228.2 132.8 12.7 7.4 18.4 29.8 15.9 2.8 8.9

Techno Electric

2016 1091.0 221.3 116.2 20.3 10.7 12.0 12.9 25.9 3.4 15.0

2017 1339.1 312.5 192.4 23.3 14.4 18.1 18.0 23.7 4.1 14.0

2018E 1536.5 352.9 231.9 23.0 15.1 19.2 23.3 15.5 2.9 10.1

2019E 1812.2 395.7 270.5 21.8 14.9 19.4 23.1 13.2 2.4 8.8

Source: Sunil Hitech Ltd, Ventura Research

- 22 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Financials & Projections

Y/E March, Fig in ` Cr FY17 FY18E FY19E FY20E Y/E March, Fig in ` Cr FY17 FY18E FY19E FY20E

Profit & Loss Statement Per Share Data (Rs)

Net Sales 2559.6 2999.5 3684.9 4218.1 Adj. EPS 1.0 1.3 1.5 1.6

% Chg. 27% 17% 23% 14% Cash EPS 2.1 2.2 2.4 2.6

Total Expenditure 2357.3 2738.2 3337.3 3816.3 Book Value 13.7 15.8 15.7 17.4

% Chg. 30% 16% 22% 14% DPS 0.1 0.1 0.1 0.1

EBDITA 202.3 261.3 347.6 401.7 Capital, Liquidity, Returns Ratio

EBDITA Margin % 7.9% 8.7% 9.4% 9.5% Debt / Equity (x) 1.2 1.1 1.2 1.2

Other Income 13.3 15.0 17.0 20.0 Current Ratio (x) 1.4 1.4 1.4 1.4

PBDIT 215.7 276.3 364.6 421.7 ROE (%) 8.0 9.3 10.5 9.8

Depreciation 38.2 40.7 47.5 55.1 ROCE (%) 16.8 18.2 19.2 18.7

Interest 110.9 136.3 174.4 212.3 Dividend Yield (%) 0.0 0.0 0.0 0.0

Exceptional items 0.0 0.0 0.0 0.0 Valuation Ratio (x)

PBT 66.5 99.2 142.7 154.3 P/E 12.1 9.9 8.4 7.8

Tax Provisions 25.9 39.7 57.1 61.7 P/BV 0.9 0.8 0.8 0.7

Reported PAT 40.6 59.5 85.6 92.6 EV/Sales 0.4 0.4 0.4 0.4

Minority Interest -1.2 -3.0 -4.3 -4.6 EV/EBIDTA 4.5 4.4 4.1 4.1

PAT 39.5 56.6 81.3 87.9 Efficiency Ratio (x)

PAT Margin (%) 2% 2% 2% 2% Inventory (days) 50 45 46 50

RM / Sales (%) 50% 52% 53% 53% Debtors (days) 90 95 97 100

Tax Rate (%) 39% 40% 40% 40% Creditors (days) 82 80 78 75

Balance Sheet Cash Flow Statement

Share Capital 37.8 51.0 57.2 57.2 Profit Before Tax 73.0 99.2 142.7 154.3

Reserves & Surplus 477.0 629.2 793.8 881.7 Depreciation 38.2 40.7 47.5 55.1

Money against share warrants 4.8 22.4 0.0 0.0 Working Capital Changes (134.7) (223.9) (278.4) (244.8)

Minority Interest 18.7 21.7 25.9 30.6 Others 87.7 81.7 100.3 130.6

Borrowings 144.77 188.97 247.83 294.61 Operating Cash Flow 64.2 (2.4) 12.1 95.2

Other liabilities 122.3 133.8 159.8 179.6 Capital Expenditure (28.8) (50.0) (90.0) (100.0)

Total Liabilities 805.5 1047.0 1284.5 1443.6 Other Investment Activities (9.3) (0.2) (11.7) (11.8)

Gross Block 526.1 576.1 666.1 766.1 Cash Flow from Investing (38.1) (50.2) (101.7) (111.8)

Less: Acc. Depreciation 251.9 292.6 340.1 395.2 Changes in Share Capital 6.6 126.3 67.1 -

Net Block 274.3 283.6 326.0 370.9 Changes in Borrowings 96.0 154.3 226.0 153.4

Non current Investments 30.8 46.0 74.7 106.5 Dividend and Interest (110.0) (136.3) (174.4) (212.3)

Long term Loans & Advances 51.9 63.6 90.0 109.7 Cash Flow from Financing (7.4) 144.2 118.7 (58.9)

Other Non Current assets 10.3 12.0 14.0 15.0 Net Change in Cash 18.7 91.7 29.1 (75.5)

Net Current assets 438.1 641.7 779.7 841.6 Opening Cash Balance 148.2 166.9 258.6 287.7

Total Assets 805.5 1047.0 1284.5 1443.6 Closing Cash Balance 166.9 258.6 287.7 212.2

- 23 - Tuesday, 17th October, 2017

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Disclosures and Disclaimer

Ventura Securities Limited (VSL) is a SEBI registered intermediary offering broking, depository and portfolio management services to clients. VSL is member of BSE, NSE and MCX-SX. VSL is a depository participant of NSDL. VSL states that no disciplinary action whatsoever has been taken by SEBI against it in last five years except administrative warning issued in connection with technical and venial lapses observed while inspection of books of accounts and records.

Ventura Commodities Limited, Ventura Guaranty Limited, Ventura Insurance Brokers Limited and Ventura Allied Services Private Limited are associates of VSL. Research Analyst (RA) involved in the preparation of this research report and VSL disclose that neither RA nor VSL nor its associates (i) have any financial interest in the company which is the subject matter of this research report (ii) holds ownership of one percent or more in the securities of subject company (iii)

have any material conflict of interest at the time of publication of this research report (iv) have received any compensation from the subject company in the past twelve months (v) have managed or co-managed public offering of securities for the subject company in past twelve months (vi) have received any compensation for investment banking merchant banking or brokerage services from the subject company in the past twelve months (vii) have received any

compensation for product or services from the subject company in the past twelve months (viii) have received any compensation or other benefits from the subject company or third party in connection with the research report. RA involved in the preparation of this research report discloses that he / she has not served as an officer, director or employee of the subject company. RA involved in the preparation of this research report and VSL discloses that they have not

been engaged in the market making activity for the subject company. Our sales people, dealers, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein. We may have earlier issued or may issue in future reports on the companies covered herein with recommendations/ information inconsistent or different those made in this report. In reviewing

this document, you should be aware that any or all of the foregoing, among other things, may give rise to or potential conflicts of interest. We may rely on information barriers, such as "Chinese Walls" to control the flow of information contained in one or more areas within us, or other areas, units, groups or affiliates of VSL. This report is for information purposes only and this document/material should not be construed as an offer to sell or the solicitation of an offer

to buy, purchase or subscribe to any securities, and neither this document nor anything contained herein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. This document does not solicit any action based on the material contained herein. It is for the general information of the clients / prospective clients of VSL. VSL will not treat recipients as clients by virtue of their receiving this report. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of clients / prospec tive clients. Similarly, this document

does not have regard to the specific investment objectives, financial situation/circumstances and the particular needs of any specific person who may receive this document. The securities discussed in this report may not be suitable for all investors. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. Persons who may receive this document should consider and independently evaluate whether

it is suitable for his/ her/their particular circumstances and, if necessary, seek professional/financial advice. And such person shall be responsible for conducting his/her/their own investigation and analysis of the information contained or referred to in this document and of evaluating the merits and risks involved in the securities forming the subject matter of this document. The projections and forecasts described in this report were based upon a number of estimates and

assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and it can be expected that one or more of the estimates on which the projections and forecasts were based will not materialize or will vary significantly from actual results, and such variances will likely increase over time. All projections and forecasts described in this report have been prepared solely by the authors of this report

independently of the Company. These projections and forecasts were not prepared with a view toward compliance with published guidelines or generally accepted accounting principles. No independent accountants have expressed an opinion or any other form of assurance on these projections or forecasts. You should not regard the inclusion of the projections and forecasts described herein as a representation or warranty by VSL, its associates, the authors of this

report or any other person that these projections or forecasts or their underlying assumptions will be achieved. For these reasons, you should only consider the projections and forecasts described in this report after carefully evaluating all of the information in this report, including the assumptions underlying such projections and forecasts. The price and value of the investments referred to in this document/material and the income from them may go down as well as up,

and investors may realize losses on any investments. Past performance is not a guide for future performance. Future returns are not guaranteed and a loss of original capital may occur. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. We do not provide tax advice to our clients, and all investors are strongly advised to consult regarding any potential

investment. VSL, the RA involved in the preparation of this research report and its associates accept no liabilities for any loss or damage of any kind arising out of the use of this report. This report/document has been prepared by VSL, based upon information available to the public and sources, believed to be reliable. No representation or warranty, express or implied is made that it is accurate or complete. VSL has reviewed the report and, in so far as it includes current or

historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed. The opinions expressed in this document/material are subject to change without notice and have no obligation to tell you when opinions or information in this report change. This report or recommendations or information contained herein do/does not constitute or purport to constitute investment advice in publicly accessible media and should not

be reproduced, transmitted or published by the recipient. The report is for the use and consumption of the recipient only. This publicat ion may not be distributed to the public used by the public media without the express written consent of VSL. This report or any portion hereof may not be printed, sold or distributed without the written consent of VSL. This document does not constitute an offer or invitation to subscribe for or purchase or deal in any securities and neither this

document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document is strictly confidential and is being furnished to you solely for your information, may not be distributed to the press or other media and may not be reproduced or redistributed to any other person. The opinions and projections expressed herein are entirely those of the author and are given as part of the normal research activity of VSL and are given as of

this date and are subject to change without notice. Any opinion estimate or projection herein constitutes a view as of the date of this report and there can be no assurance that future results or events will be consistent with any such opinions, estimate or projection. This document has not been prepared by or in conjunction with or on behalf of or at the instigation of, or by arrangement with the company or any of its directors or any other person. Information in this

document must not be relied upon as having been authorized or approved by the company or its directors or any other person. Any opinions and projections contained herein are entirely those of the authors. None of the company or its directors or any other person accepts any liab ility whatsoever for any loss arising from any use of this document or its contents or otherwise arising in connection therewith. The information contained herein is not intended for publication or

distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Deri vatives Segments” as prescribed by Securities and Exchange Board of India before investing in Securities Market.

Ventura Securities Limited Corporate Office: 8

th Floor, ‘B’ Wing, I Think Techno Campus, Pokhran Road no. 02, Off Eastern Express Highway , Thane (West) 400 607.