Summary/Brief Notes of Company Law by KCC Ludhiana

16

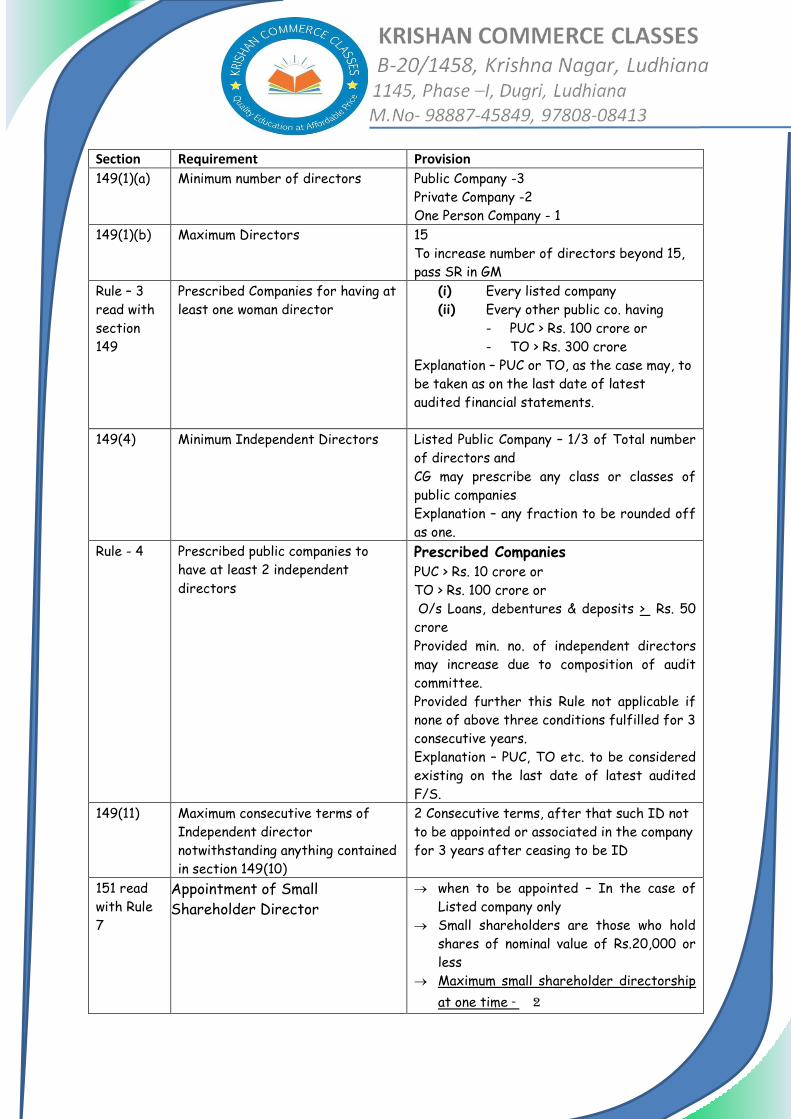

Section Requirement Provision 149(1)(a) Minimum number of directors Public Company -3 Private Company -2 One Person Company - 1 149(1)(b) Maximum Directors 15 To increase number of directors beyond 15, pass SR in GM Rule – 3 read with section 149 Prescribed Companies for having at least one woman director (i) Every listed company (ii) Every other public co. having - PUC > Rs. 100 crore or - TO > Rs. 300 crore Explanation – PUC or TO, as the case may, to be taken as on the last date of latest audited financial statements. 149(4) Minimum Independent Directors Listed Public Company – 1/3 of Total number of directors and CG may prescribe any class or classes of public companies Explanation – any fraction to be rounded off as one. Rule - 4 Prescribed public companies to have at least 2 independent directors Prescribed Companies PUC > Rs. 10 crore or TO > Rs. 100 crore or O/s Loans, debentures & deposits > Rs. 50 crore Provided min. no. of independent directors may increase due to composition of audit committee. Provided further this Rule not applicable if none of above three conditions fulfilled for 3 consecutive years. Explanation – PUC, TO etc. to be considered existing on the last date of latest audited F/S. 149(11) Maximum consecutive terms of Independent director notwithstanding anything contained in section 149(10) 2 Consecutive terms, after that such ID not to be appointed or associated in the company for 3 years after ceasing to be ID 151 read with Rule 7 Appointment of Small Shareholder Director when to be appointed – In the case of Listed company only Small shareholders are those who hold shares of nominal value of Rs.20,000 or less Maximum small shareholder directorship at one time - 2

-

Upload

kcc-tutorials -

Category

Education

-

view

22 -

download

0

Transcript of Summary/Brief Notes of Company Law by KCC Ludhiana

Section Requirement Provision

149(1)(a) Minimum number of directors Public Company -3

Private Company -2

One Person Company - 1

149(1)(b) Maximum Directors 15

To increase number of directors beyond 15,

pass SR in GM

Rule – 3

read with

section

149

Prescribed Companies for having at

least one woman director

(i) Every listed company

(ii) Every other public co. having

- PUC > Rs. 100 crore or

- TO > Rs. 300 crore

Explanation – PUC or TO, as the case may, to

be taken as on the last date of latest

audited financial statements.

149(4) Minimum Independent Directors Listed Public Company – 1/3 of Total number

of directors and

CG may prescribe any class or classes of

public companies

Explanation – any fraction to be rounded off

as one.

Rule - 4 Prescribed public companies to

have at least 2 independent

directors

Prescribed Companies PUC > Rs. 10 crore or

TO > Rs. 100 crore or

O/s Loans, debentures & deposits > Rs. 50

crore

Provided min. no. of independent directors

may increase due to composition of audit

committee.

Provided further this Rule not applicable if

none of above three conditions fulfilled for 3

consecutive years.

Explanation – PUC, TO etc. to be considered

existing on the last date of latest audited

F/S.

149(11) Maximum consecutive terms of

Independent director

notwithstanding anything contained

in section 149(10)

2 Consecutive terms, after that such ID not

to be appointed or associated in the company

for 3 years after ceasing to be ID

151 read

with Rule

7

Appointment of Small

Shareholder Director

when to be appointed – In the case of

Listed company only

Small shareholders are those who hold

shares of nominal value of Rs.20,000 or

less

Maximum small shareholder directorship

at one time - 2

Tenure:- 3 years

163 Option to adopt principle of

Proportional representation for

appointment of directors

If AOA so provides, at least 2/3rd of

total directors shall be so appointed

Voting may be by single transferable

vote or system of cumulative voting or

otherwise and

such appointment may be made once in 3

years

Tenure of directors so appointed - 3

years

Casual vacancy of such directors – as per

section 161(4) i.e by BOD

165 Maximum limit of Directorships - 20 directorships including alternate

directorship

- Maximum number of directorships in

public companies = 10

- Private Ltd co. which is a Holding or

Subsidiary of a public company to be

considered as public company.

177 Audit Committee Applicability – Listed Company and such

other class or classes of companies, as may

be prescribed, shall constitute Audit

Committee.

Prescribe Public Companies (Rule – 6)

PUC > Rs. 10 crore or

TO > Rs. 100 crore or

Total o/s Loans, debentures &

deposits > Rs. 50 crore

Explanation – PUC, TO etc. to be considered

existing on the last date of latest audited

F/S.

Composition – Minimum 3 Directors and out

of them majority to be of independent

directors:

Provided that majority of members of Audit

Committee including its Chairperson shall be

persons with ability to read and understand,

the financial statement.

Section

178

Nomination and Remuneration

Committee

Applicability – Every listed company and

prescribed companies

Prescribe Public Companies (Rule – 6)

PUC > Rs. 10 crore or

TO > Rs. 100 crore or

Total o/s Loans, debentures &

deposits > Rs. 50 crore

Explanation – PUC, TO etc. to be considered

existing on the last date of latest audited

F/S.

Composition - >3 non-executive directors

out of which at least ½ shall be independent

directors:

Provided that the chairperson of the

company (whether executive or non-

executive) may be appointed as a member of

the Nomination and Remuneration Committee

but shall not chair such Committee.

Section

178

Stakeholders Relationship

Committee The Board of Directors of a company which

consists of more than 1,000 shareholders,

debenture-holders, deposit-holders and any

other security holders at any time during a

financial year shall constitute a Stakeholders

Relationship Committee consisting of a

chairperson who shall be a non-executive

director and such other members as may be

decided by the Board.

Section

181

Company to contribute to bona fide

charitable & other funds By passing BR in BM – up to 5% of

average net profits for the 3

immediately preceding f/y, in any

financial year.

By passing OR in GM – beyond 5 %

Section

182

Prohibitions and restrictions

regarding political contributions Who cannot make:- (i) Government

Companies, (ii) Companies which has been

in existence for less than 3 years

To Whom:- (i) to political party, (ii) to

any other person for political purposes

Maximum amount in a f/y to Contribute:-

7.5% of average of last 3 F/Ys Profits

Requirement - Pass BR in BM

Section

183 Contribution to National Defence

Fund etc.

Pass BR

No Limit on Contribution

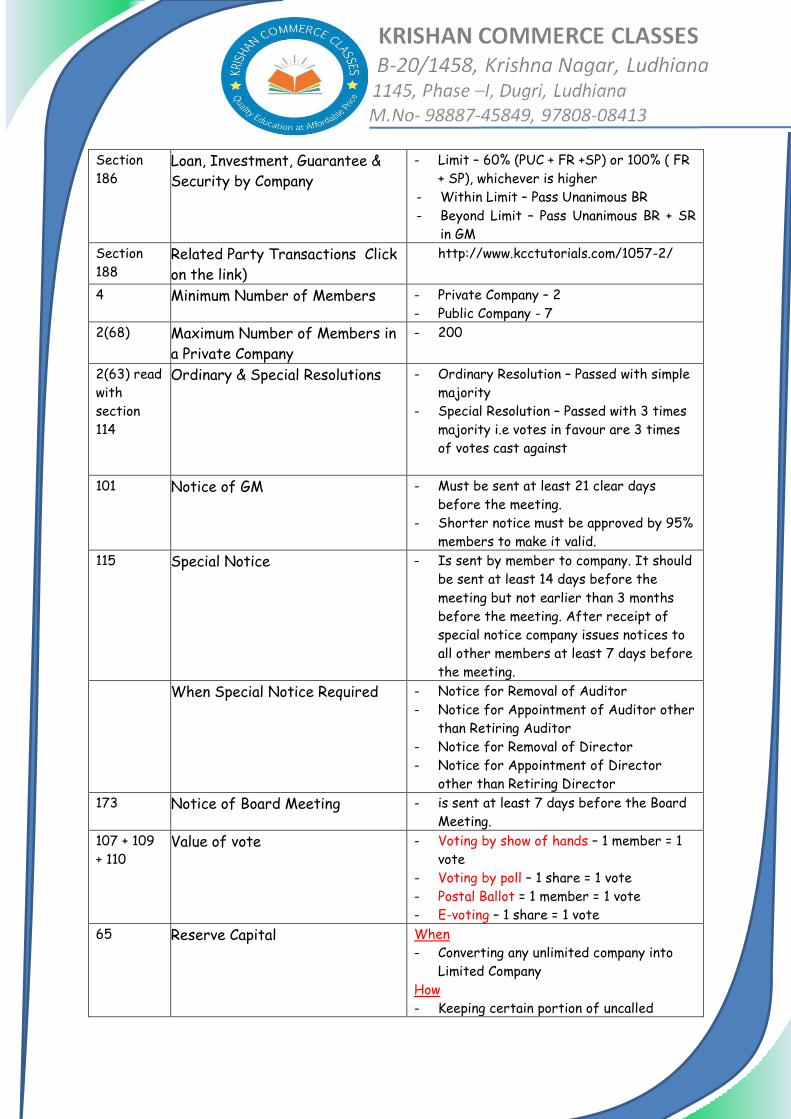

Section

186 Loan, Investment, Guarantee &

Security by Company

- Limit – 60% (PUC + FR +SP) or 100% ( FR

+ SP), whichever is higher

- Within Limit – Pass Unanimous BR

- Beyond Limit – Pass Unanimous BR + SR

in GM

Section

188 Related Party Transactions Click

on the link)

http://www.kcctutorials.com/1057-2/

4 Minimum Number of Members - Private Company – 2

- Public Company - 7

2(68) Maximum Number of Members in

a Private Company

- 200

2(63) read

with

section

114

Ordinary & Special Resolutions - Ordinary Resolution – Passed with simple

majority

- Special Resolution – Passed with 3 times

majority i.e votes in favour are 3 times

of votes cast against

101 Notice of GM - Must be sent at least 21 clear days

before the meeting.

- Shorter notice must be approved by 95%

members to make it valid.

115 Special Notice - Is sent by member to company. It should

be sent at least 14 days before the

meeting but not earlier than 3 months

before the meeting. After receipt of

special notice company issues notices to

all other members at least 7 days before

the meeting.

When Special Notice Required - Notice for Removal of Auditor

- Notice for Appointment of Auditor other

than Retiring Auditor

- Notice for Removal of Director

- Notice for Appointment of Director

other than Retiring Director

173 Notice of Board Meeting - is sent at least 7 days before the Board

Meeting.

107 + 109

+ 110 Value of vote - Voting by show of hands – 1 member = 1

vote

- Voting by poll – 1 share = 1 vote

- Postal Ballot = 1 member = 1 vote

- E-voting – 1 share = 1 vote

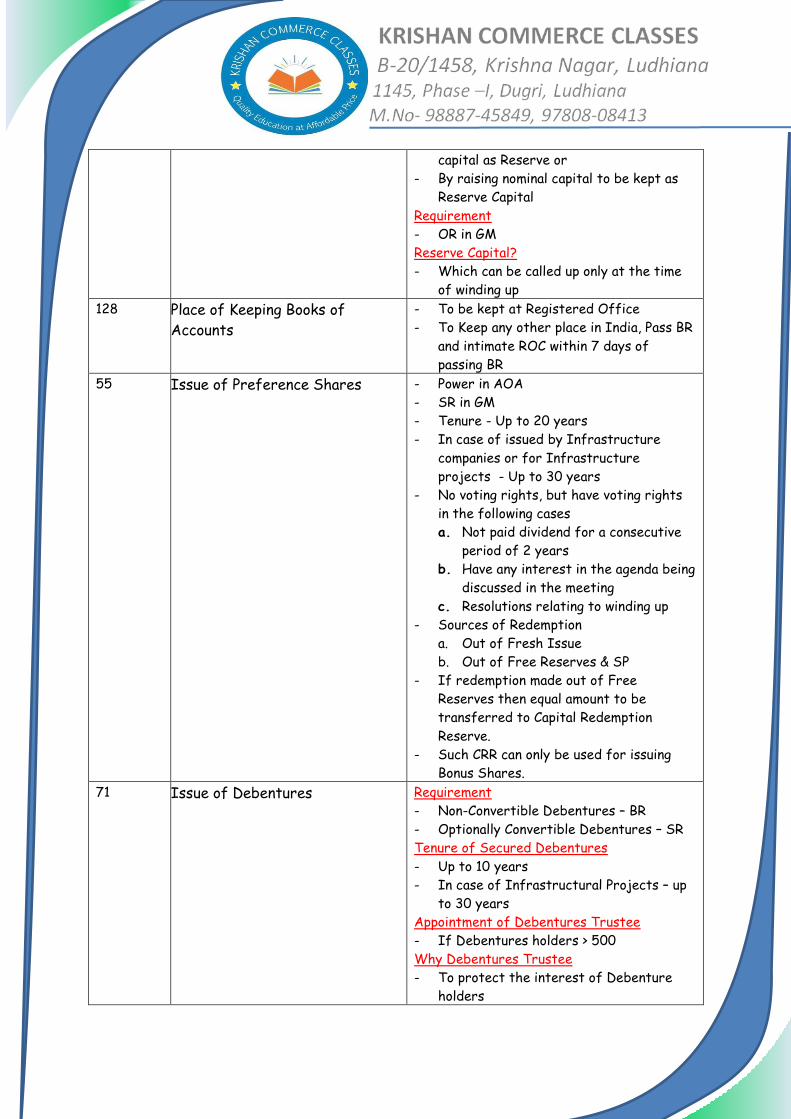

65 Reserve Capital When

- Converting any unlimited company into

Limited Company

How

- Keeping certain portion of uncalled

capital as Reserve or

- By raising nominal capital to be kept as

Reserve Capital

Requirement

- OR in GM

Reserve Capital?

- Which can be called up only at the time

of winding up

128 Place of Keeping Books of

Accounts

- To be kept at Registered Office

- To Keep any other place in India, Pass BR

and intimate ROC within 7 days of

passing BR

55 Issue of Preference Shares - Power in AOA

- SR in GM

- Tenure - Up to 20 years

- In case of issued by Infrastructure

companies or for Infrastructure

projects - Up to 30 years

- No voting rights, but have voting rights

in the following cases

a. Not paid dividend for a consecutive

period of 2 years

b. Have any interest in the agenda being

discussed in the meeting

c. Resolutions relating to winding up

- Sources of Redemption

a. Out of Fresh Issue

b. Out of Free Reserves & SP

- If redemption made out of Free

Reserves then equal amount to be

transferred to Capital Redemption

Reserve.

- Such CRR can only be used for issuing

Bonus Shares.

71 Issue of Debentures Requirement

- Non-Convertible Debentures – BR

- Optionally Convertible Debentures – SR

Tenure of Secured Debentures

- Up to 10 years

- In case of Infrastructural Projects – up

to 30 years

Appointment of Debentures Trustee

- If Debentures holders > 500

Why Debentures Trustee

- To protect the interest of Debenture

holders

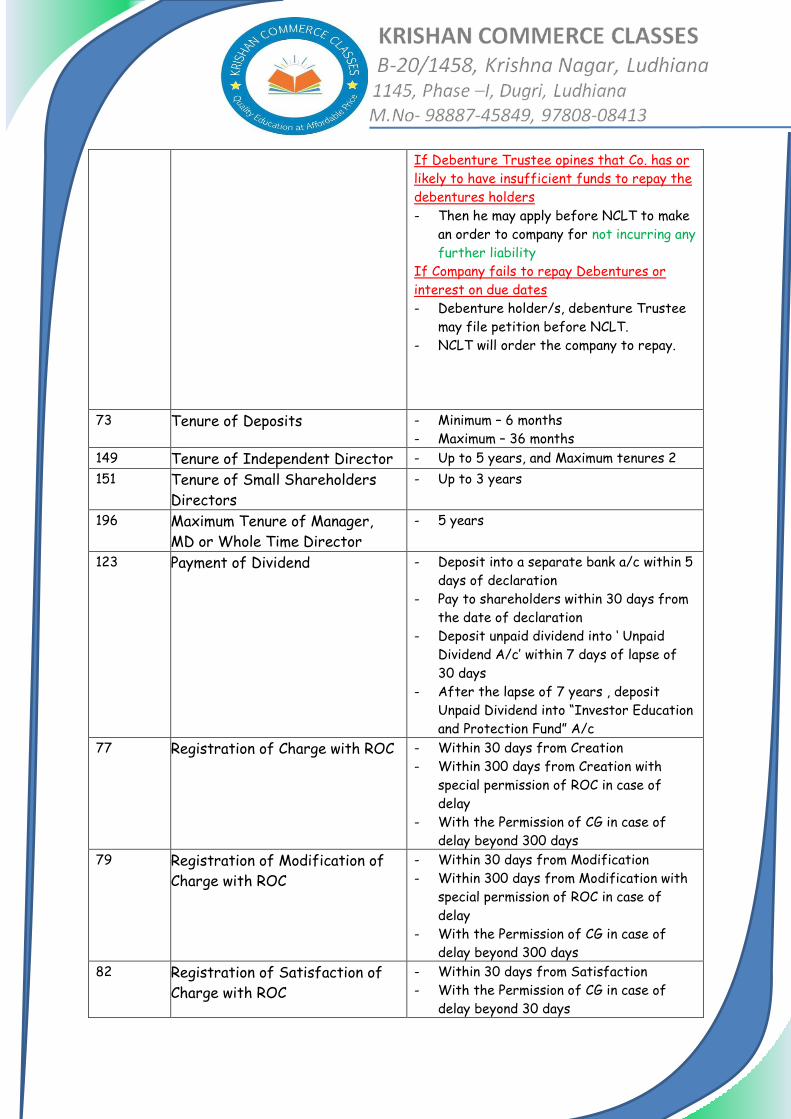

If Debenture Trustee opines that Co. has or

likely to have insufficient funds to repay the

debentures holders

- Then he may apply before NCLT to make

an order to company for not incurring any

further liability

If Company fails to repay Debentures or

interest on due dates

- Debenture holder/s, debenture Trustee

may file petition before NCLT.

- NCLT will order the company to repay.

73 Tenure of Deposits - Minimum – 6 months

- Maximum – 36 months

149 Tenure of Independent Director - Up to 5 years, and Maximum tenures 2

151 Tenure of Small Shareholders

Directors

- Up to 3 years

196 Maximum Tenure of Manager,

MD or Whole Time Director

- 5 years

123 Payment of Dividend - Deposit into a separate bank a/c within 5

days of declaration

- Pay to shareholders within 30 days from

the date of declaration

- Deposit unpaid dividend into ‘ Unpaid

Dividend A/c’ within 7 days of lapse of

30 days

- After the lapse of 7 years , deposit

Unpaid Dividend into “Investor Education

and Protection Fund” A/c

77 Registration of Charge with ROC - Within 30 days from Creation

- Within 300 days from Creation with

special permission of ROC in case of

delay

- With the Permission of CG in case of

delay beyond 300 days

79 Registration of Modification of

Charge with ROC

- Within 30 days from Modification

- Within 300 days from Modification with

special permission of ROC in case of

delay

- With the Permission of CG in case of

delay beyond 300 days

82 Registration of Satisfaction of

Charge with ROC

- Within 30 days from Satisfaction

- With the Permission of CG in case of

delay beyond 30 days

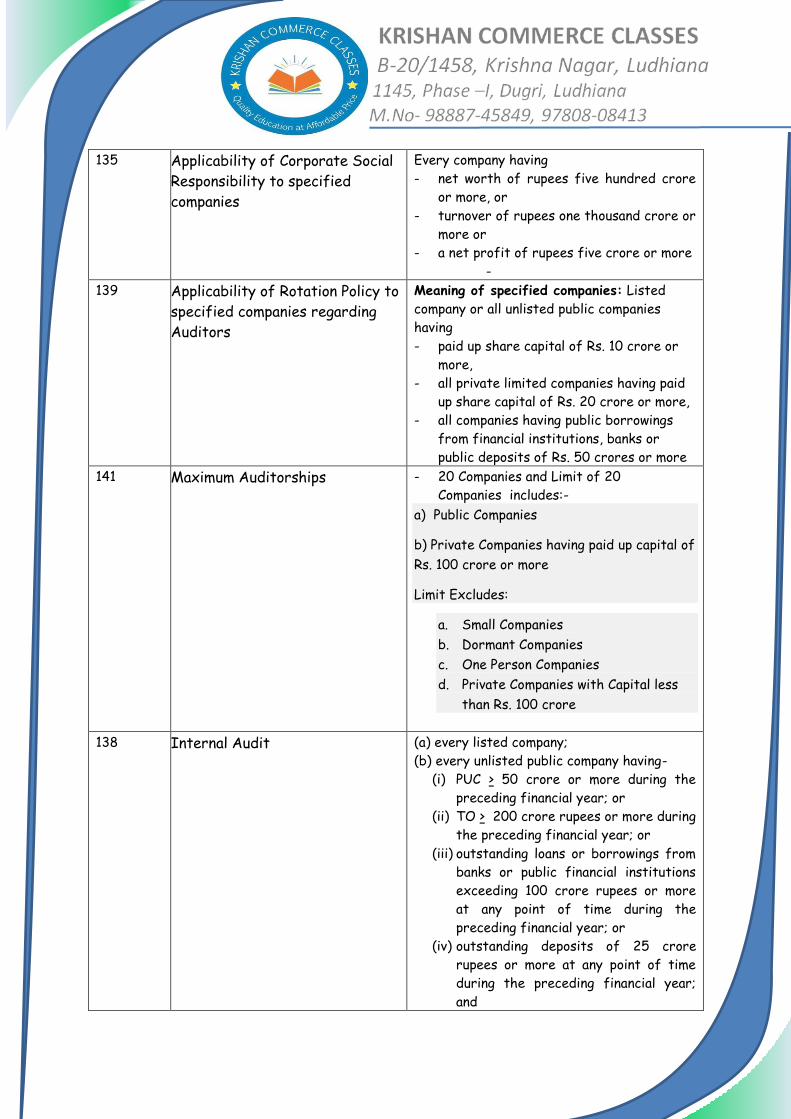

135 Applicability of Corporate Social

Responsibility to specified

companies

Every company having

- net worth of rupees five hundred crore

or more, or

- turnover of rupees one thousand crore or

more or

- a net profit of rupees five crore or more

-

139 Applicability of Rotation Policy to

specified companies regarding

Auditors

Meaning of specified companies: Listed

company or all unlisted public companies

having

- paid up share capital of Rs. 10 crore or

more,

- all private limited companies having paid

up share capital of Rs. 20 crore or more,

- all companies having public borrowings

from financial institutions, banks or

public deposits of Rs. 50 crores or more

141 Maximum Auditorships - 20 Companies and Limit of 20

Companies includes:-

a) Public Companies

b) Private Companies having paid up capital of

Rs. 100 crore or more

Limit Excludes:

a. Small Companies

b. Dormant Companies

c. One Person Companies

d. Private Companies with Capital less

than Rs. 100 crore

138 Internal Audit (a) every listed company;

(b) every unlisted public company having-

(i) PUC > 50 crore or more during the

preceding financial year; or

(ii) TO > 200 crore rupees or more during

the preceding financial year; or

(iii) outstanding loans or borrowings from

banks or public financial institutions

exceeding 100 crore rupees or more

at any point of time during the

preceding financial year; or

(iv) outstanding deposits of 25 crore

rupees or more at any point of time

during the preceding financial year;

and

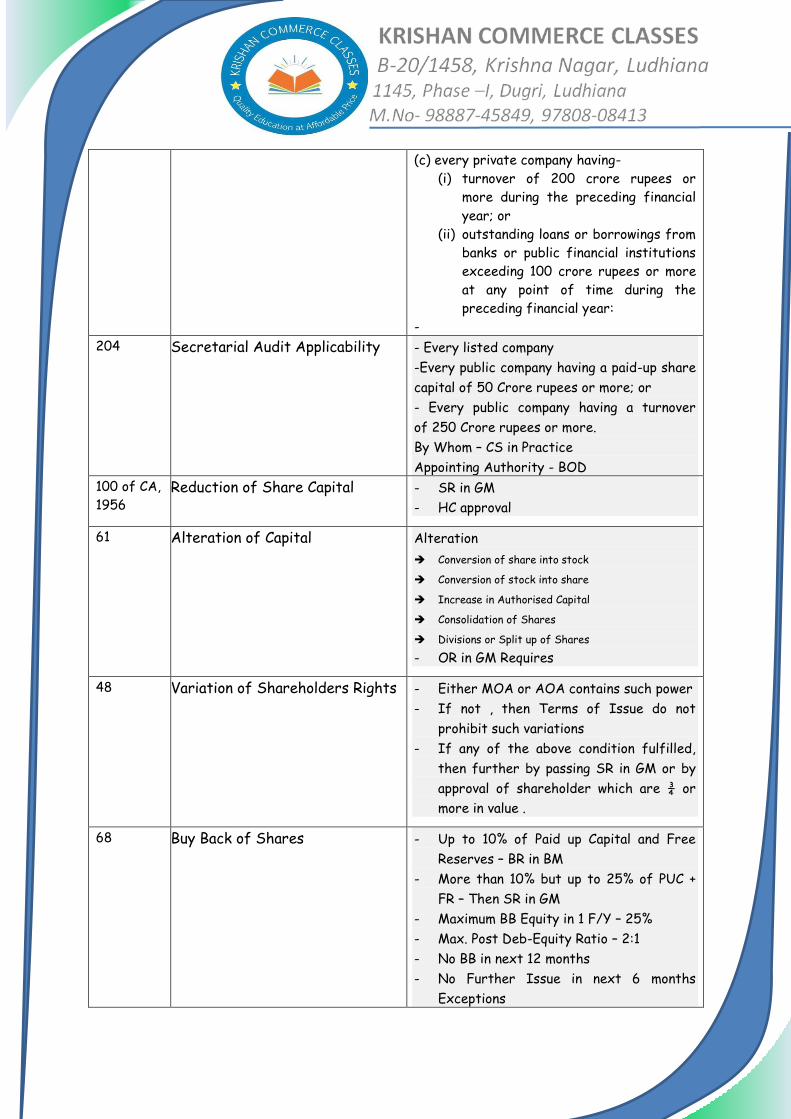

(c) every private company having-

(i) turnover of 200 crore rupees or

more during the preceding financial

year; or

(ii) outstanding loans or borrowings from

banks or public financial institutions

exceeding 100 crore rupees or more

at any point of time during the

preceding financial year:

-

204 Secretarial Audit Applicability - Every listed company

-Every public company having a paid-up share

capital of 50 Crore rupees or more; or

- Every public company having a turnover

of 250 Crore rupees or more.

By Whom – CS in Practice

Appointing Authority - BOD

100 of CA,

1956 Reduction of Share Capital - SR in GM

- HC approval

61 Alteration of Capital Alteration

Conversion of share into stock

Conversion of stock into share

Increase in Authorised Capital

Consolidation of Shares

Divisions or Split up of Shares

- OR in GM Requires

48 Variation of Shareholders Rights - Either MOA or AOA contains such power

- If not , then Terms of Issue do not

prohibit such variations

- If any of the above condition fulfilled,

then further by passing SR in GM or by

approval of shareholder which are ¾ or

more in value .

68 Buy Back of Shares - Up to 10% of Paid up Capital and Free

Reserves – BR in BM

- More than 10% but up to 25% of PUC +

FR – Then SR in GM

- Maximum BB Equity in 1 F/Y – 25%

- Max. Post Deb-Equity Ratio – 2:1

- No BB in next 12 months

- No Further Issue in next 6 months

Exceptions

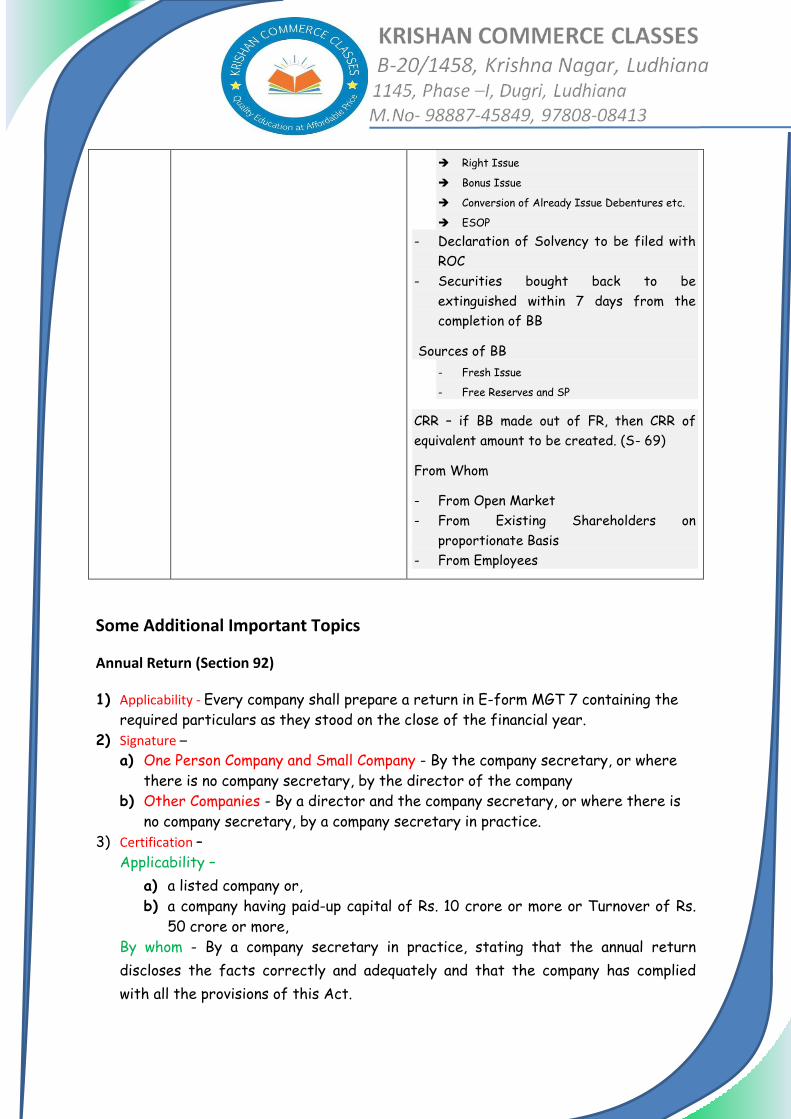

Right Issue

Bonus Issue

Conversion of Already Issue Debentures etc.

ESOP

- Declaration of Solvency to be filed with

ROC

- Securities bought back to be

extinguished within 7 days from the

completion of BB

Sources of BB

- Fresh Issue

- Free Reserves and SP

CRR – if BB made out of FR, then CRR of

equivalent amount to be created. (S- 69)

From Whom

- From Open Market

- From Existing Shareholders on

proportionate Basis

- From Employees

Some Additional Important Topics

Annual Return (Section 92)

1) Applicability - Every company shall prepare a return in E-form MGT 7 containing the

required particulars as they stood on the close of the financial year.

2) Signature –

a) One Person Company and Small Company - By the company secretary, or where

there is no company secretary, by the director of the company

b) Other Companies - By a director and the company secretary, or where there is

no company secretary, by a company secretary in practice.

3) Certification –

Applicability –

a) a listed company or,

b) a company having paid-up capital of Rs. 10 crore or more or Turnover of Rs.

50 crore or more,

By whom - By a company secretary in practice, stating that the annual return

discloses the facts correctly and adequately and that the company has complied

with all the provisions of this Act.

4) Filing of Annual Return –

a) The copy of Annual Return to be filed with the Registrar,.

b) AR to be filed within 60 days from the date

on which the AGM is held or

where no AGM is held in any year within 60 days from the date on which the

annual general meeting should have been held together with the statement

specifying the reasons for not holding the AGM, with such fees or additional

fees as may be prescribed, within the time as specified, under section 403.

5) An extract of the annual return in E-form MGT-9 shall be attached to the

Director’s Report. 6) Contents of Annual Return

The Annual Return shall contain the following particulars:

a. its registered office, principal business activities, particulars of its holding,

subsidiary and associate companies;

b. its shares, debentures and other securities and shareholding pattern;

c. its indebtedness;

d. its members and debenture-holders along with changes therein since the

close of the previous financial year;

e. its promoters, directors, key managerial personnel along with changes

therein since the close of the previous financial year;

f. meetings of members or a class thereof, Board and its various committees

along with attendance details;

g. remuneration of directors and key managerial personnel;

h. penalty or punishment imposed on the company, its directors or officers and

details of compounding of offences and appeals made against such penalty or

punishment;

i. matters relating to certification of compliances, disclosures as may be

prescribed;

j. details, as may be prescribed, in respect of shares held by or on behalf of

the Foreign Institutional Investors indicating their names, addresses,

countries of incorporation, registration and percentage of shareholding held

by them; and

k. such other matters as may be prescribed,

7) Penalty on Company - If a company fails to file its annual return before the expiry

of the period specified under section 403 with additional fee, the company shall

be punishable with fine which shall not be less than Rs. 50, 000 but which may

extend to Rs. 5,00,000 and every officer of the company who is in default shall

be punishable with imprisonment for a term which may extend to 6 months or

with fine which shall not be less than Rs. 50,000 but which may extend to five

lakh rupees, or with both.

8) Penalty on CS - If a company secretary in practice certifies the annual return

otherwise than in conformity with the requirements of this section or the rules

made thereunder, he shall be punishable with fine which shall not be less than

Rs. 50,000 but which may extend to Rs. 5,00,000.

Copies of the Registers and Annual Return [Rule 16 of the Companies (Management

and Administration) Rules, 2014]

Copies of the registers maintained under section 88 or entries therein and annual

return filed under section 92 may be furnished to any member, debenture-holder,

other security holder or beneficial owner of the company or any other person on

payment of such fee as may be prescribed in the Articles of Association of the

company but not exceeding rupees ten for each page.

Preservation of Register & Records of Members and Annual Return [Rule 15 of the

Companies (Management and Administration) Rules, 2014]

The provisions with regard to preservation of records are contained in Rule 15

a) Register of members along with the index

Tenure - Permanently

Custody – CS of the company or any other person authorized by the Board for

such purpose; and

b) Register of debenture holders or any other security holders along with the index

Tenure - 8 years from the date of redemption of debentures or securities, as

the case may be

Custody – CS of the company or any other person authorized by the Board for

such purpose; and

c) Copies of all Annual Returns prepared under section 92 and copies of all

certificates and documents required to be annexed thereto

Tenure - shall be preserved for a period of 8 years from the date of filing with

the Registrar.

d) Foreign register of members

Tenure - Permanently unless it is discontinued and all the entries are

transferred to any other foreign register or to the principal register.

Custody - The foreign register shall be kept in the custody of the person

authorized by the Board for authentication of the entries made therein.

e) Foreign register of debenture holders or any other security holders

Tenure - shall be preserved for a period of 8 years from the date of redemption

of such debentures/ securities.

Custody - The foreign register shall be kept in the custody of the person

authorized by the Board for authentication of the entries made therein.

Surrender of shares

The Companies Act contains no provision for surrender of shares. Surrender of shares

is valid only when Articles of Association provide for the same and:

(i) Where forfeiture of such shares is justified; or

(ii) When shares are surrendered in exchange for new shares of same nominal value.

“Surrender of shares” means the surrender to the company on the part of the

registered holder of shares already issued. Where shares are surrendered to the

company, whether by way of settlement of a dispute or for any other reason, it will

have the same effect as a transfer in favour of the company and amount to a reduction

of capital. But if, under any arrangement, such shares, instead of being surrendered to

the company, are transferred to a nominee of the company then there will be no

reduction of capital [Collector of Moradabad v. Equity Insurance Co. Ltd., (1948) 18

Com Cases 309: AIR 1948 Oudh 197]. Surrender may be accepted by the company

under the same circumstances where forfeiture is justified. It has the effect of

releasing the shareholder whose surrender is accepted from further liability on shares.

Forfeiture of shares

a) Power in AOA - There must be power in the Articles of Association, otherwise it

will be void. If Articles authorise, the forfeiture shall include forfeiture of all

dividends declared in respect of the forfeited shares and such dividend is not

actually paid before the forfeiture of the shares.

a) Board Resolution - Board Resolution is required for forfeiture.

b) There is no requirement of NCLT approval.

c) As per Regulations - Forfeiture must be made strictly in accordance with the

regulations regarding notice, procedure and manner stated therein.

d) Bona fide - The power of forfeiture must be exercised bona fide and in the interest

of the company. It should not be collusive or fraudulent.

e) Proper Notice - Before the shares of a member are forfeited, a proper notice to

that effect must have been served. Regulation 29 of Table F provides that a notice

shall name a further day (not less than 14 days from the date of service of the

notice) on or before which the payment is to be made. The notice must also mention

that in the event of non payment, the shares will be liable to be forfeited.

Both forfeiture and surrender lead to termination of membership. But in the former

case, it is at the initiative of company and in the latter case at the initiative of member

or shareholder.

Signature in Various Cases

Annual Return

One Person Company and Small Company - By the company secretary, or where there is

no company secretary, by the director of the company

Other Companies - By a director and the company secretary, or where there is no

company secretary, by a company secretary in practice.

Meeting u/s 100

The notice shall be signed by all the requistionists or by a requistionists duly

authorized in writing by all other requistionists on their behalf or by sending an

electronic request attaching therewith a scanned copy of such duly signed requisition.

Signing of Financial Statements

Financial statement should be signed on behalf of the board by atleast

chairperson of company, duly authorised board, or

two directors of whom one should be the managing director, and

chief executive officer, if he is director, chief financial officer and company

secretary, if any in the company

One person company's financial statements shall be signed by only one director.

Signing of Board Report

Board Report and any annexure thereto must be signed by its Chairperson of the

company if he is authorised by the Board and where he is not so authorised, shall be

signed by at least two directors, one of whom shall be a managing director, or by the

director where there is one director.[ section 134(3)

Signing of Minutes Book

Each page of every Minute book shall be initialled or signed and the last page of the

record of proceedings of each meeting or each report in such books shall be dated and

signed.

a) Board or Committee of Board Meeting Minutes - By the chairman of the said meeting

or the Chairman of the next succeeding meeting;

b) General Meeting Minutes - By the Chairman of the same meeting within the

aforesaid period of 30 days or in the event of the death or inability of that

Chairman within that period, by a director duly authorized by the Board for the

purpose;

c) In case of every resolution passed by postal ballot - By the Chairman of the Board

within the aforesaid period of 30 days or in the event of there being no

chairman of the Board or the death or inability of that chairman within that

period, by a director duly authorized by the Board for the purpose.

Common Seal

Companies (Amendment) Act, 2015, has diluted the mandatory adoption of common seal.

The Company may or may not adopt a common seal. The company may contract under its

common seal, if any and in case, the company does not have a common seal then

according to the requirements of that particular section the contract shall be

validated.

Effects on the provisions of Company Law

As per section 12(3)(a) , Every company shall have its name engraved in legible

characters on its seal, if any.

Execution of bills of exchange etc. – Section 22

(1) A bill of exchange, hundi or promissory note shall be deemed to have been made,

accepted, drawn or endorsed on behalf of a company if made, accepted, drawn, or

endorsed in the name of, or on behalf of or on account of, the company by any person

acting under its authority, express or implied.

(2) A company may, by writing under its common seal, if any, authorise any person,

either generally or in respect of any specified matters, as its attorney to execute

other deeds on its behalf in any place either in or outside India.

“Provided that in case a company does not have a common seal, the authorisation under

this sub-section shall be made by two directors or by a director and the Company

Secretary, wherever the company has appointed a Company Secretary.”;

(3) A deed signed by such an attorney on behalf of the company and under his

seal shall bind the company.

Section – 46

(1) A Certificate, “issued under the common seal, if any, of the company or signed by

two directors or by a director and the Company Secretary, wherever the company

has appointed a Company Secretary, specifying the shares held by any person, shall

be prima facie evidence of the title of the person to such shares.

(2) A duplicate certificate of shares may be issued, if such certificate —

a) is proved to have been lost or destroyed; or

b) has been defaced, mutilated or torn and is surrendered to the company.

(3) Notwithstanding anything contained in the articles of a company, the manner of

issue of a certificate of shares or the duplicate thereof, the form of such

certificate, the particulars to be entered in the register of members and other

matters shall be such as may be prescribed.

(4) Where a share is held in depository form, the record of the depository is the prima

facie evidence of the interest of the beneficial owner.

(5) If a company with intent to defraud issues a duplicate certificate of shares, the

company shall be punishable with fine which shall not be less than five times the

face value of the shares involved in the issue of the duplicate certificate but which

may extend to ten times the face value of such shares or rupees ten crores

whichever is higher and every officer of the company who is in default shall be

liable for action under section 447.

Limits under Section 188

Rule 15(3) of the Companies (Meetings of Board and Its powers) Rules, 2014 provides

the limits as follows:

(a) sale, purchase or supply of any goods or materials;

sale, purchase or supply of any goods or materials, directly or through

appointment of agent, exceeding 10% of the turnover of the company or Rs. 100

crore, whichever is lower, as mentioned in clause (a) and clause (e) respectively

of sub-section (1) of section 188;

(b) selling or otherwise disposing of, or buying, property of any kind;

selling or otherwise disposing of or buying property of any kind, directly or

through appointment of agent, exceeding 10%. of net worth of the company or

Rs. 100 crore, whichever is lower, as mentioned in clause (b) and clause (e)

respectively of sub-section (1) of section 188;

(c) leasing of property of any kind;

leasing of property of any kind exceeding 10%. of the net worth of the company

or 10% of turnover of the company or Rs. 100 crore, whichever is lower, as

mentioned in clause (c) of sub- section (1) of section 188;

(d) availing or rendering of any services;

availing or rendering of any services, directly or through appointment of agent,

exceeding 10% of the turnover of the company or Rs. 50 crore, whichever is

lower, as mentioned in clause (d) and clause (e) respectively of sub-section (1) of

section 188:

Note: the limits specified above (a to d) shall apply for transaction or

transactions to be entered into either individually or taken together with the

previous transactions during a financial year.

(e) appointment of Related party to any office or place of profit in the company, its

subsidiary company or associate company

Approval of the members of the company shall be required for appointment to

any office or place of profit in the company, its subsidiary company or associate

company at a monthly remuneration exceeding Rs. 2,50,000 by a resolution.

As per explanation (a) to section 188(1), the expression “office or place of

profit” means any office or place-

(i) where such office or place is held by a director, if the director holding it

receives from the company anything by way of remuneration over and above

the remuneration to which he is entitled as director, by way of salary, fee,

commission, perquisites, any rent-free accommodation, or otherwise;

(ii) where such office or place is held by an individual other than a director or by

any firm, private company or other body corporate, if the individual, firm, private

company or body corporate holding it receives from the company anything by way

of remuneration, salary, fee, commission, perquisites, any rent-free

accommodation, or otherwise; (f) underwriting the subscription of any securities

or derivatives of the company:

Remuneration paid for underwriting the subscription of any securities or

derivatives thereof of the company exceeding one per cent of the net worth of

the company. As per Second proviso to section 188 (1) of the Companies Act, 2013, no member of

the company shall vote on such resolution, to approve any contract or arrangement

which may be entered into by the company, if such member is a related party. In case of Private Company, exemption has been given to the private company from

applicability of second proviso to section 188(1), who is also a related party, to vote on

such resolution at the general meeting. (vide MCA notification dated 05.06.2015)