1 February 19, 2008 ROTH Capital Growth Conference Roth Capital Growth Conference.

Summary Overview

February 2020

Patron Capital Overview• Established European property investor over 20 years

➢ Operations across Europe with advisory offices in the UK, Luxembourg and Spain with major operating partners in

most markets including in Germany, France and Portugal

➢ Experienced 73-person team including 30 investment professionals, supported by 11 advisers, with regional and

product focused expertise

o Average of 19 years experience across the investment team

➢ Hybrid owner operator model supporting local partners across Europe

$109,700,000

PATRON CAPITAL L.P., I

Pan-European valueoriented property and asset based corporate investments

October 2002

€303,000,000

PATRON CAPITAL L.P., II

October 2004

Pan-European value-oriented property and asset-based

corporate investments

€895,000,000

PATRON CAPITAL L.P., III

March 2007

Pan-European value-oriented property and asset-based

corporate investments

(with GP commitment of up to €45,000,000)

€1,100,000,000

PATRON CAPITAL L.P., IV

July 2012

Pan-European opportunisticdistressed property and assetbased corporate investments

(including €100,000,000 dedicated discretionary co-investment pool and apx. €220,000,000 of co-investment

capital within investments)

C. £62,000,000

(C. €96,000,000)

PATRON CAPITAL

CAPTIVE FUND

DEDICATED FUND RAISE

FOR THE ACQUISITION OF

OCWEN UK (RENAMED

IGROUP) A LEADING

PLAYER IN THE SUB-PRIME

MORTGAGE MARKET

October 1999

€948,632,391

PATRON CAPITAL, V L.P.

July 2016

TARGETING OPPORTUNISTIC

DISTRESSED AND UNDERVALUED

PROPERTY AND PROPERTY

RELATED INVESTMENTS ACROSS

EUROPE

(including €143,000,000 of co-investment capital )

2

Deep Value Investment Strategy

3

• Identify granular and/or complexopportunities and properties withincorporates

• Value-add through asset management,improved strategy and introduction of clearfocus, sell into domestic market once assetstabilised

• Drive net equity multiple of 1.6x+ over 3-5years

➢ Target unlevered p.a. return of 11%-13%;approximate net profits of 35%-45% ontotal cost

➢ Use leverage 50%-65% LTC debt to movelevered returns to 16%+ and 1.6x+ equitymultiple

• Ensure fund/capital pools properlydiversified; limited development risk

• Limit leverage as tail risk protection6m 1y 2y 3y 4y 5y

Classic Investment Path

2.2x/20-25%+50%

1.5x/17-20%+20%

>1.0x/5-10%+10%

0%

1.8x/17-20%+35%

Multiple/IRRNet Margin

Patron Zone(less leverage)

Opportunistic Zone

ValueIndicator

Time

4

Target %

Property assets below intrinsic value deemed non-core

by parent/owner

Companies with strong cash flow and value supported

by underlying real estate assets, properties that have

operational-tied variable cash flow

20-30%

Challenged situations solved by repositioning assets or

platforms for broader market appeal

Financial securities (e.g., loans, equity release) backed

by real estate, typically residential

Institutional Non-Core and

Distressed Property

Corporate Acquisitions and

Operational Real Estate

Complex Positions

Real Estate Credit

Focus on Investments below Intrinsic Value

CALA Banner

40-50%

20-40%

10-30%

10-20%

Deep Value Investment Strategy

5

Origination - Geographic Focus• Western Europe remains the prime focus with increasingly more granular smaller opportunities dominating our activities

(1) Where at least one day a week required of investment team

Note: The % in the above charts represent proportion by capital

(1)

Other1%

Germany / Switzerland

15%

Western Europe36%

UK / Ireland44%

Central Europe3%

Eastern Europe1%

Total Evaluated Opportunities : 1999-2019

3,047 Opportunities - $123.2bn

Other0%

Germany / Switzerland

33%

Western Europe33%

UK / Ireland34%

Total Evaluated Opportunities : AGM 2018 - AGM 2019

254 Opportunities - $7.2bnOther

0%

Germany / Switzerland

33%

Western Europe33%

UK / Ireland34%

Total Evaluated Opportunities : AGM 2018 - AGM 2019

254 Opportunities - $7.2bn

(1)

Patron Platform – Integrated and Interactive (41)

6

Christoph Ignaczak

Julian Rosenberg

Pedro Barcelo

Arnau Osorio

Yolanda Leal

Alejandro Pasquin

Vicente Conesa *

Mark Collins

Daniel Weisz

Matteo Busà

Jonatas Szkurnik

Rafael Fitoussi

• Dedicated 73-person team including 41 investment professionals averaging 19 years of experience and Senior Team averaging 24 years of experience

COUNTRY FOCUS

Keith M. BreslauerShane Law

Vanessa Sloan

Matthew Utting

Sir David Capewell *

Kevin Cooke

Richard Sykes

Emilio Cereijo

ADVISERS

GENERALISTS

Senior Team Member

ACROSS EUROPE, ACROSS PRODUCTS

Wiktor Lesinski

Tim Swift

Nicolò Benzi

Juan Du

Roy Binkowicz

Julius Kühn

Clothilde Guittard

Corporate

Hotels & Leisure

Pubs

Home Building

Development

Commercial Credit &

DistressedResidential & Consumer Distressed

Healthcare

Education

Strategy & Business

Development

Social Impact (WISH Fund) Project Management

KEY

* Senior Adviser

Robert BoothJason MeadsBertrand Schwab

Guillaume LefortMichael Capaccio

Leonardo Kutova

Ashish Kashyap

Nate Kornfeld *

Stephen Green

Irina Stamate-Rocha

Fei Xie

Tim Street *

Danny Kay *

PRODUCT FOCUS

Rod MacKinnon

Patron Support Team, Risk and Compliance (32)

7

Investment TeamKeith M. BreslauerManaging Director

Shane LawChief Operating Officer

Senior Team

Jackie Burn *Human Resource

Kendall LangfordGeneral Counsel/Compliance

Mark ParnellFinance Director Geraldine Schmit

Managing Director

Daniel Cohn Senior Legal Counsel

Farhod MoghadamSenior Legal Counsel

Caroline McGrath Investment & Closing

Denise GoodwinInvestment & Tax

Mark HarrisGroup Financial Accountant

Seemone CheungFinancial Accountant

Andreas BlumSenior Accountant

Administration

Charlene CarrLegal PA

Lisa DaveSenior Team PA

Victoria CollinsFinance PA

Meritxell GonfausAdmin, Spain

Stephanie BohlerAdmin, Lux

Legal Finance & Tax Luxembourg

Stuart AnsherFinancial Accountant

Suchilla DillonAccountant

Steve Van Den BroekCOO

Halim MekbelAccountantRichard Carter

Assistant Fund AccountantMoses Kim

Transaction Assistant

Michael HaydonSenior Accountant

Senior AdvisersJonathan PaganelliSenior Corporate

Officer

Alexis TabarySenior Corporate

Officer

Amelia CarterPA to Keith M. Breslauer

Hayley St AngeTeam PA

Andrew HaigFinancial Accountant/

Fund Modeller

Kalie CoveleyTeam Support

William Davies-HumphreysLegal Associate

Sylvie NuceraAccountant

* Senior Adviser

Floella JohnsonSenior Team PA

Investment Performance – Overall

8

• Since 1999, Patron has invested in 80 investments totalling €2.9 billion of equity and over €12 billion of

gross asset value predominantly across Western Europe

➢ The primary strategy, comprising 87% of invested equity, is towards opportunities in Western

Europe. Notwithstanding the effect of the GFC, these investments have seen very positive returns

➢ Patron’s overall performance since the GFC has been significantly higher

Past Eighteen Years

Number of

Investments

Invested &

Identified

Equity

Realised

Proceeds

Unrealised

Proceeds

Total Realised

& Unrealised

Proceeds Gross IRR

Gross Equity

Multiple

Western Europe

(primary strategy)

71 €2,430m €2,776m €1,108m €3,884m 17% 1.60x

Post GFC 44 €1,570m €1,826m €1,039m €2,865m 22% 1.83x

Note: Performance figures as at September, 2019

WORKING HARD TO HELP CHANGE THE WORLD

To date, Patron Charitable Initiatives have helped…

Recent Awards - Selection

10

Property Fund Manager

of the Year

Best Places to Work in Property

Responsible Investor of the Year 2016

HealthcareProperty Developer of

the YearFinancial ServicesDeal of the Year

Property Fund of the Year

Corporate Social Responsibility Award

2019Deal of the Year 2018

11

Specific Investment Review

Selected Opportunities

(ordered by Fund and by investment size within each Fund)

Opportunity

• Grainger, a listed residential property company, changed its focus to developing PRS units

and decided to sell its non-core Retirement Solutions (RS) business. The business

comprises a portfolio of over 3,800 ‘Home Reversion’ equity release assets.

• On 31st December 2015, Patron exchanged contracts with Grainger to acquire the RS

Business.

• Completion took place in May 2016 post regulatory approval – renamed Retirement

Bridge Group.

• June 2017 – acquired Sovereign Reversions (c. 700 assets)

Home Reversion

• Home reversion is an equity release product where the homeowner sells part or all of the

equity in his home in exchange for a discounted appraisal value of the equity and a right to

live in the property until it is vacated upon the occupant’s death or move into long term

care.

• The industry underwent a significant improvement in market perception after home

reversions were regulated by the FCA since 2007.

Portfolio (as at May 2015 cut-off date)

• 3,839 properties located across the whole of the UK, with concentration in the south of

England.

• Very seasoned portfolio (over 10 years on average) with average age of tenant of 82 years.

Business Plan

• As part of the acquisition, Patron acquired the platform, including staff, systems,

regulatory licences, brand and any other intellectual property.

• Strategy assumes no new origination or acquisition and sale of the business in 4 years.

12

UK Consumer – Retirement Bridge (Fund V)

13

UK Consumer Leisure Program (Fund V)

• The acquisition of Punch Taverns Plc in August 2017, following

Competition and Mergers Authority approval. The acquisition was

funded in part by the simultaneous back to back sale of a

substantial portfolio of Punch’s assets to Heineken.

• A total of 3,254 pubs were acquired, of which 1,879 were sold to

Heineken. Patron retained ownership of 1,375 pubs and the head

office operations, of which 1,323 are held in a securitisation

structure and 52 pubs and the head office operations held at

TopCo.

• Add-on acquisition of Laine in 2018 with 55 pubs and other single

assets, small portfolios

• The business plan is predicated on

➢ strategic capex across the core estate to improve the underlying

quality of the portfolio

➢ continued roll-out of a hybrid tenanted / managed operating

model

➢ sale of the non-core pubs

EastPoint, Ireland – sold (Fund V)• Acquisition of 4 multi-let office buildings with gross internal area of c.153,000 sq.

ft. on EastPoint Business Park in Dublin, Ireland.

• EastPoint is c.40 acres in size, with approx. 1.5 million square feet of primarily office

space (grade B) across 35 buildings. EastPoint has been developed in phases since

the site was originally acquired and developed by Earlsfort Developments in the

1990s. The park is located adjacent to Dublin Docklands (where a lot of central

Dublin office development is taking place, including the new Central Bank HQ), and

in close proximity to the traditional core CBD area. The park has attracted a

concentration of TMT tenants.

• The assets were acquired in joint-venture with O’Callaghan Properties (“OCP”) and

Earlsfort Developments (“Earlsfort”). OCP are Fund IV’s existing JV partner on

Project Drive, including acting as asset manager on Northside Shopping Centre,

where there is a strong working relationship. Earlsfort originally developed

EastPoint and are the existing part-owner and asset manager for several units on the

Park, demonstrating their good knowledge of the Assets / local market. Both OCP

and Earlsfort are investing alongside Patron.

• Strategy is to lease up vacant space and regear/release existing let space, where

appropriate.

• Further 80,000 sqft acquired early 2017 - 3 assets - J, K and U on map

• Sold in September 2018 to Madison International Realty

14

• Acquisition of 43 retail units (32 supermarkets, 5 Cash&Carry

and 6 high street units) across Spain, comprising 41,567sqm of

GLA. Main tenant is El Árbol/DIA (#2 chain in Spain), with 31

leases, and other individual tenants (including ING, Sanitas,

Cortefiel).

• Purchased from Blackstone who acquired the portfolio within a

larger €23bn transaction from GE in 2015.

• Strategy comprises lease up of vacant space and sale over a 3-4

year investment period, with some capex across portfolio as

appropriate.

• Business plan undertaken by Patron team working with key local

brokers with extensive experience in each region, as well as

Aguirre Newman, CBRE and Vicente Conesa (Patron’s long

term advisor and local partner in the Fund III Poblenou

investment).

15

Project Green, Spain (Fund V)

GSPP – Cologne, Germany – sold (Fund V)

• Acquisition of a 14,372 sqm office building on theborder of Cologne’s city centre, with significant andunique redevelopment potential in an economicallystrong and affluent city with a good micro location andexcellent connections to public transport.

• Seller was Patrizia who shifted strategy from a directinvestor to primarily a Spezialfonds manager. As aresult the asset became non-core for them.

• JV partner is Development Partner AG, an experiencedoffice and retail developer and investor with a strongtrack record.

• Strategy to reposition the asset as a good building and acheaper alternative within the premium segment whichis undersupplied in the local market, supported by anextensive capex program and lease up of the asset.

• Sold in July 2019 to AEW

16

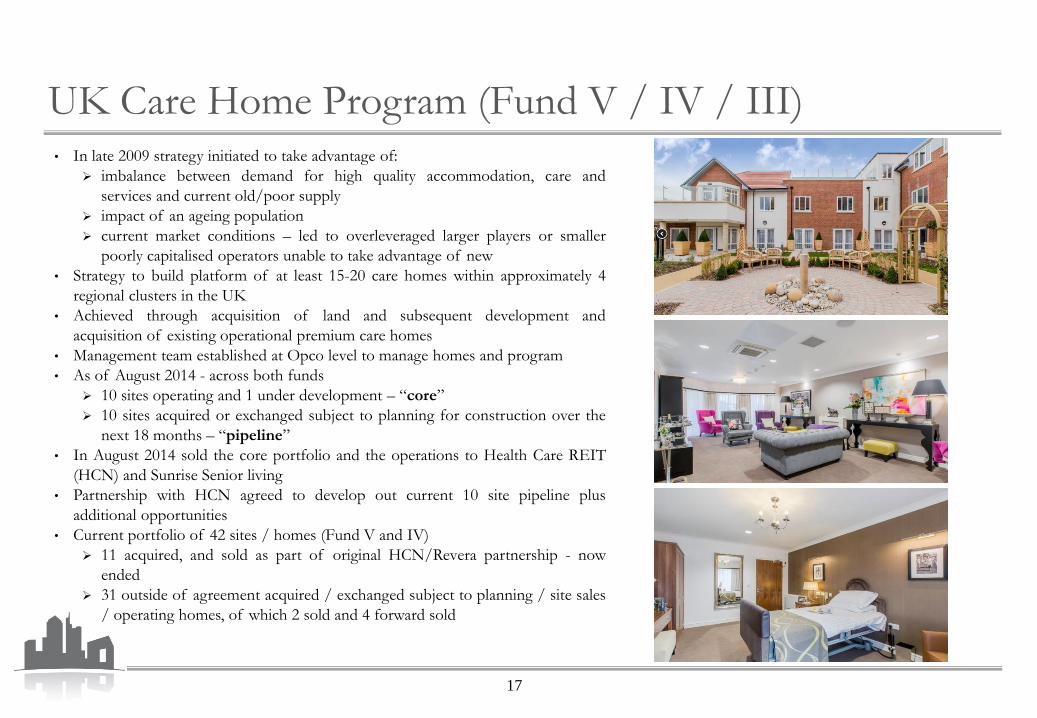

• In late 2009 strategy initiated to take advantage of:

➢ imbalance between demand for high quality accommodation, care and

services and current old/poor supply

➢ impact of an ageing population

➢ current market conditions – led to overleveraged larger players or smaller

poorly capitalised operators unable to take advantage of new

• Strategy to build platform of at least 15-20 care homes within approximately 4

regional clusters in the UK

• Achieved through acquisition of land and subsequent development and

acquisition of existing operational premium care homes

• Management team established at Opco level to manage homes and program

• As of August 2014 - across both funds

➢ 10 sites operating and 1 under development – “core”

➢ 10 sites acquired or exchanged subject to planning for construction over the

next 18 months – “pipeline”

• In August 2014 sold the core portfolio and the operations to Health Care REIT

(HCN) and Sunrise Senior living

• Partnership with HCN agreed to develop out current 10 site pipeline plus

additional opportunities

• Current portfolio of 42 sites / homes (Fund V and IV)

➢ 11 acquired, and sold as part of original HCN/Revera partnership - now

ended

➢ 31 outside of agreement acquired / exchanged subject to planning / site sales

/ operating homes, of which 2 sold and 4 forward sold

17

UK Care Home Program (Fund V / IV / III)

CALA Homes - sold (Fund IV)• Acquisition in March 2013 of CALA Homes, a leading UK premium volume house builder

from Lloyds Banking Group (“LBG”) as part of bank’s non-core asset disposal strategy and

subsequent add-on acquisition in March 2014 of Banner Homes

• CALA is a national house builder with a 15,846 plot land bank equivalent to c.6.8 years of

production. CALA achieves the highest average selling price (“ASP”) among the UK

volume house builders, £509k vs. average of £233k

• CALA focuses on 3+ bedroom, single family homes in affluent districts of the UK, with

customers who are generally equity rich, with average LTVs of 65%

• For strategic as well as capital diversification reasons, Patron brought Legal & General

(“L&G”) and Electra Partners into the investment with Patron at 37%, L&G holding

47.5%, Electra 10.5%, management 5% - from a governance perspective Patron retains

operational control, with both Patron and L&G having board seats and Electra having a

passive role subject to material matters above a 10% of EV threshold

• Management team includes 21 professionals led by Alan Brown, CEO and Graham Reid,

CFO, who successfully turned around the CALA after the downturn and the LBG debt for

equity swap

• Business plan is predicated on the build out of the land bank acquired during the downturn

at attractive terms and the build out of “legacy” sites acquired pre-recession improving

gross margin from 16% at the time of acquisition to 21%. Profits generated from

developments are sufficient to replenish the land bank and position the business for exit

• In March 2014 CALA acquired Banner Homes, a leading premium house builder operating

in the South East and Midlands with a land bank of 2,360 plots and turnover of c.£140

million

➢ Banner greatly increased CALA’s exposure to more affluent areas in the South East of

England and the increased scale will improve the combined business margins through

operational leverage

• March 2018 – sale of Patron interest to Legal & General

Banner

CALA

18

• 89% equity share in the property assets and business of Motor Fuel Group (“MFG”), the 2nd largest

independent owner & operator of convenience retail / petrol filling stations (“Forecourts”) in the UK

➢ Total of 373 operational Forecourt assets – pro forma 333 (89%) freeholds and 40 (11%) leaseholds, with

unexpired lease terms typically in excess of 25 years

• Joint venture with Alasdair Locke, high-net-worth veteran of the oil, property and insurance industries, and

new management team

➢ Highly specialist and experienced partner with over 450 previous successful forecourt acquisitions,

turnarounds and asset managements to their credit

➢ Management team includes several experienced executives ex Murco UK (the UK subsidiary of Murphy

Oil)

• Initial MFG Platform investment completed Dec 2011 – corporate acquisition of the business and portfolio of

47 Forecourts, MFG then being the 5th largest independent forecourt owner /operator in the UK.

➢ Intrinsically high quality assets, significantly underperforming against industry average and historic

performance

➢ Business plan focussed on enhancing operations and profitability of retail assets via conversion to

efficient ‘Commission Operator’ management structure, systemic shop rebranding, dedicated capex

programme and improved supply agreements

• Enhanced returns from bolt-on acquisitions of additional PFS assets/portfolios - key ones include:

➢ “Scorpion Portfolio” acquisition, July 2013 - freeholds of 53 sites, let on long leases to Murco

Petroleum Limited (“Murco”)

➢ Murco Business acquisition, Sept 2014 - entire UK retail business of Murco, primarily consisting of a

portfolio of 223 high-quality Forecourt assets (including the Scorpion leaseholds), acquired by MFG

effectively off-market

➢ “Project Strawberry” - contracts exchanged 10th April 2015 for the acquisition of a portfolio of 90

Forecourts from Shell. Final completion October 2015, funded by senior debt refinance plus cash on

MFG’s balance sheet - no new equity required

• July 2015 – sale of platform to Clayton, Dubilier & Rice

Asset Location Map – MFG & Target Portfolio

MFG (288) Shell (90)

MFG (288) Shell (90)

19

Motor Fuel Group - sold (Fund IV)

Business Plan

• Target product segment - Prime credit with 65-70% average LTV

• Mid 2017 - launched near prime product up to 75% LTV

• Funding through senior debt from banks at significant advance rate and through capital markets and sales

• Securitisation of loan book completed July 2017

• Explore optionality in the platform - (a) additional secured loan products and (b) secondary loan portfolio acquisitions –acquired and further being explored

Opportunity

• Deleveraging by UK high street banks has resulted in a significant

undersupply of secured credit, creating an opportunity to create a high

yield secured lending platform, focusing on products like second charge

(2nd mortgage) loans, short-term (bridge) loans and shared equity

mortgages and achieve 8%+ unlevered yield

• In July 2013, Patron backed the senior management team of Nemo

Principal Finance, the only mainstream UK second charge mortgage

lender to survive the credit crisis, to setup a new platform and originate

second charge loans, leveraging their significant credit experience and deep

broker relationships

Second Charge Mortgage Product

• Loan to homeowner secured through a second charge on the property,

typically for debt consolidation and home improvement; consolidation

results in lower monthly outgoings

Shared Equity Product

• Shared equity mortgages are loans from housebuilders to new home

buyers which are secured through a second charge and have an equity

share in the underlying property

• Acquisition of loan portfolios, using established Optimum platform for

asset management

• December 2018 – sale of platform to Pepper Group

20

UK Mortgage Investments – sold (Fund IV)

• Investment program targeting acquisition of undervalued commercial properties in strong regional

commercial centres in the United Kingdom

• Program is primarily carried out in JV with Alliance Property Asset Management Limited - a UK asset

manager with significant experience in UK commercial markets and extensive existing asset

management/asset work relationships with UK banks and institutions

• Program Strategy:

➢ Targeting commercial or mixed use assets sub £20m lot size with value-add potential or undervalued

opportunities;

➢ UK focus, with particular emphasis on 2nd and 3rd tier centres still to be impacted by positive

inflows from institutional market

• First Investment - April 2014 - Thorpe Park, Leeds; (3% of program) - SOLD

➢ 21,000 sqft fully let office building located on out of town Leeds business park. Single tenanted

office space with ground floor retail element• Second Acquisition - December 2014 - Crossways, Dartford; (9% of program) - SOLD

➢ 42,600 sq ft office in two Grade A detached office buildings located on Crossways Business Park in

Dartford, South East of London, with 25,500 sqft /60% vacancy in one building• Third Acquisition - March 2015 - Arlington Business Park, Reading; (54% of program)

➢ 330,000 sqft in ten office buildings (with industrial asset sub-sold in April 2015) located on Arlington

Business Park in the Thames Valley / out of town Reading market - a key established office market

(West of London), with c. 105,000 sqft vacancy / 30% of space – subsequent 29,500 sqft 100%

leased add-on asset in November 2015• Fourth Acquisition - April 2015 - The Mint, Leeds; (27% of program) - SOLD

➢ 118,000 sqft modern office building located in Central Leeds, 94% let on acquisition to two tenants,

Asda and Dart PLC• Fifth Acquisition - Sep 2015 – Quattro (Basingstoke, Cardiff, Luton); (7% of program) - SOLD

➢ 68,000 sqft in three office buildings with 35% vacant space across to assets

21

UK Small Property Program (Fund IV)

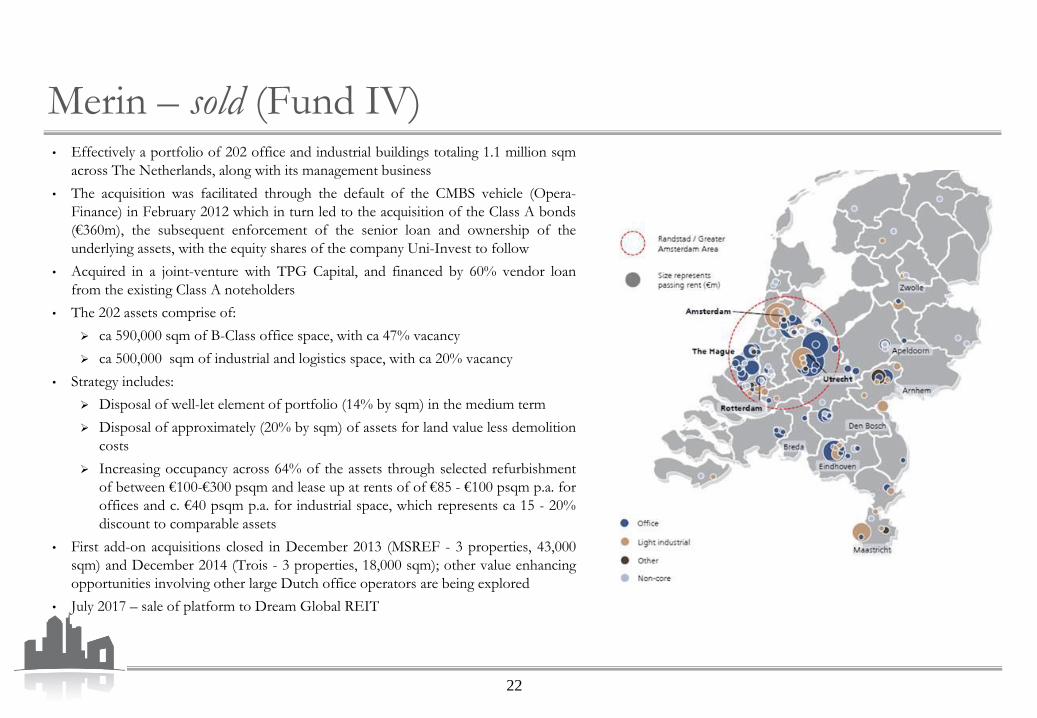

Merin – sold (Fund IV)• Effectively a portfolio of 202 office and industrial buildings totaling 1.1 million sqm

across The Netherlands, along with its management business

• The acquisition was facilitated through the default of the CMBS vehicle (Opera-

Finance) in February 2012 which in turn led to the acquisition of the Class A bonds

(€360m), the subsequent enforcement of the senior loan and ownership of the

underlying assets, with the equity shares of the company Uni-Invest to follow

• Acquired in a joint-venture with TPG Capital, and financed by 60% vendor loan

from the existing Class A noteholders

• The 202 assets comprise of:

➢ ca 590,000 sqm of B-Class office space, with ca 47% vacancy

➢ ca 500,000 sqm of industrial and logistics space, with ca 20% vacancy

• Strategy includes:

➢ Disposal of well-let element of portfolio (14% by sqm) in the medium term

➢ Disposal of approximately (20% by sqm) of assets for land value less demolition

costs

➢ Increasing occupancy across 64% of the assets through selected refurbishment

of between €100-€300 psqm and lease up at rents of of €85 - €100 psqm p.a. for

offices and c. €40 psqm p.a. for industrial space, which represents ca 15 - 20%

discount to comparable assets

• First add-on acquisitions closed in December 2013 (MSREF - 3 properties, 43,000

sqm) and December 2014 (Trois - 3 properties, 18,000 sqm); other value enhancing

opportunities involving other large Dutch office operators are being explored

• July 2017 – sale of platform to Dream Global REIT

22

• Similar to prior funds’ programs, the focus is on building a balanced portfolio ofsmaller buildings and sub-portfolios of smaller assets that are typically a mixture ofpartially vacant, vacant or fully let, but requiring active asset management, includingrefurbishment and redevelopment, re-letting of vacancy and exiting

• First Investment: Mollstrasse; 23% of program SOLD

➢ Acquired in September 2011, a 15,900 sqm primarily vacant office and retailbuilding in the attractive central “Mitte” district of Berlin from a distresseddeveloper

• Second Investment: Ridlerstrasse; 17% of program SOLD

➢ Acquired in April 2014, a 11,200 sqm office building in Munich's West Enddistrict with 40% vacancy and capex requirements

• Third Investment: Campus West; 30% of program SOLD

➢ Acquired in October 2014, a 36,700 sqm office complex also in Munich butfurther west in an established B-office hub, with a diversified tenant base and20% vacancy

• Fourth Investment: Franklinstrasse; 30% of program SOLD

➢ Acquired in May 2015, a 51,000 sqm office complex in Berlin Charlottenburgadjoining Ernst-Reuter-Platz with the Technical University of Berlin in closeproximity. Business plan envisages redevelopment and lease up of 37,000 sqmof office space (95% of total lettable space)

23

German Small Property Program – sold (Fund IV)

Freehold

Leasehold

• Acquisition of 24 office, industrial and retail properties for a total

consideration of £184m located principally in London and South East

England.

• Assets acquired from a distressed CMBS vehicle which reached maturity in

October 2012 and was in LTV breach since 2007, owned by Henderson

Casper LP, a fund managed by Henderson Global Investors.

• Acquired in a 50:50 Joint Venture with Mountgrange Real Estate

Opportunity Fund with new senior debt financing from Santander.

• Simultaneously completed 9 asset sub-sales of assets to institutional

investors.

• Total 15 assets post sub sales at acquisition

➢ Offices (60%), Retail Warehousing (8%), Distribution Warehouse

(25%), High Street Retail (2%), Multi-let Industrial Property (5%).

• Transaction Strategy:

➢ Maintain and improve strong cash flow yields and lease up of the

lettable vacant space amounting to c.a. 100,000 sq. ft. of total area,

including select capex investments, to drive gross income yield

improvement – in progress and significantly completed

➢ Disposal program for stable and stabilized assets over a 4 year period

• All assets now sold

24

Mercury - sold (Fund IV)

• Acquisition of the Clarion Hotel in Dublin, Ireland. The Hotel had been in administration

for nearly 3 years and was underinvested with a poorly motivated management team and a

poorly performing brand. The Hotel was financed by a loan owned by the National Asset

Management Agency (“NAMA”), the Irish-state-owned ‘bad bank’, who was the ultimate

seller.

• Hotel is a modern (opened in 2001) purpose-built 165-room (consisting of 15 suites /

family rooms and 150 standard rooms) 4-star hotel fronting the River Liffey in the

International Financial Services Centre (“IFSC”) in Dublin. The Hotel benefits from 10

conference rooms (catering for between 10 and 150 delegates), a leisure club (including an

18m heated swimming pool; the leisure club has c.1000 members), two dining options and

a bar.

• The Hotel is held on a long lease (184 years remaining) from the Dublin Docks Authority.

The Hotel was previously managed by Choice Hotels Ireland and traded under the Clarion

brand. The Hotel benefits from a strong location in the IFSC (a successful financial

services hub).

• The operating partner in the transaction is Fitzpatrick Lifestyle Hotels (“Fitzpatrick”), an

experienced local owner and manager of mid-market hotels. Hotel is being run on an

independent basis, managed by Fitzpatrick, and rebranded as part of the Fitzpatrick

collection as The Spencer (as announced and launched in March 2014).

• A key part of the business plan was the investment within the first six months of

ownership to refresh the guest rooms, update the health club and the public areas,

including full relaunch of the food & beverage outlets – completed and full launch took

place in July 2014

• Sold November 2016

25

The Spencer - sold (Fund IV)

Badby Park – sold (Fund IV)

26

• In 2012 Patron acquired the Badby Park Care Facility which is set within a

57-acre estate located in Daventry (Midlands, UK). Badby Park comprises

a 68 bed facility dedicated to acquired brain injury, complex care and

neurological disorders providing specialist nursing and rehabilitation

services.

• A further development in Stoke-on-Trent was acquired (75 bed specialist

facility, 24 apartments and 60 bed care home) in March 2015. The 75 bed

specialist unit opened in October 2015 and is currently in “fill” mode

• Worcester (Worcestershire) exchanged in April 2016 subject to planning

• Middlesbrough (40 beds) and Darlington (54 beds) acquired Q4 2016

• 2 further sites, Southampton and Basingstoke, exchanged in November

2016 subject to planning

Strategy Includes:

• Increasing revenue and managing staff agency costs at Badby Park at

mature occupancy

• Exploring the development potential from the excess land on the site and

bolt-on acquisitions - planning consent for 17 bed extension was granted

in 2015

• Fill Stoke, Middlesbrough and Darlington facilities and achieve planning

on exchanged sites

• Operating facilities (Badby, Stoke, Middlesbrough and Darlington) sold

April 2017 – pipeline sites transferred to UK Care Home Program

• Acquisition of budget youth hostel accommodation portfolio and themanagement operations from family owned business based inLondon, with properties in London and Berlin:

➢ The Generator Hostels Ltd: operating company and allintellectual property including brand name “Generator Hostels”

➢ London Freehold: 872 Beds (60,000 ft²), which has nowcompleted a full refurbishment to bring rooms and public areasin-line with newer properties.

➢ Berlin Leasehold: 892 Beds (80,000 ft²)

• Further hostels acquired since initial acquisition and now operating:Copenhagen, Dublin, Hamburg, Barcelona, Berlin Mitte, Venice andParis

• Newest assets Amsterdam and Stockholm opened in H1 2016

➢ Rome in Q3 2016

• Sites recently acquired: Madrid and Miami – both under developmentto open in 2017

• Active pipeline of hostels within Europe and North America –includes freehold, leasehold and management contracts

• Sale exchanged March 2017, completed May 2017

27

Location Tenure Opening Beds RoomsAvg Beds

Per Room

London FH 1994 872 212 4.1

Berlin East LH 2002 892 235 3.8

Copenhagen FH 2011 662 175 3.8

Dublin FH 2011 539 106 5.1

Venice FH 2011 684 161 4.2

Hamburg FH 2012 235 29 8.1

Barcelona FH 2013 727 154 4.7

Berlin Mitte FH 2013 568 146 3.9

Paris FH 2015 917 199 4.6

Amsterdam FH 2016 566 168 3.4

Stockholm LH Jul 2016 826 233 3.5

Rome FH Q3 2016 244 75 3.3

Madrid FH H2 2017 532 128 4.2

Miami FH H2 2017 358 101 3.5

Total 8,622 2,122 4.1

Generator Hostel Program – sold (Fund III)

28

• Capital Park platform was acquired in 2005 with the acquisition of Neptune portfolio (42 assets including redevelopment of selected assets as retail / residential)

• Portfolio expanded to encompass 100 assets with a variety of strategies including

➢ Retail – program to acquire small assets on high streets in Polish

cites to refurbish, relet and exit

➢ Opportunistic – property assets, including land, for refurbishment

and development for residential and office use (including Wilanow

– 37,000 sqm)

➢ Eurocentrum (69,000 sqm)

➢ Norblin (centre Warsaw, > 64,000 sqm)

• After disposals, Portfolio now comprises over 62 assets, representing 249,000 sqm (inc. development potential)

• Platform restructured in 2011 to create independent Polish corporate entity, called Capital Park SA

• Company comprises over 60 staff, encompassing all aspects of investment management, and property development including origination, financing, project management, and tenanting.

• IPO on Warsaw Stock Exchange in December 2013 raising over €30 million in primary capital for growth and business plan execution

• Focus on improving share prices through business plan execution

• In May 2019, sold 90% of position to Madison International Realty; residual portion held with a deferred put option

Capital Park - sold (Fund III / Fund II)

• Acquisition of portfolio of mid market regional UK hotels (2,861 rooms) from theadministrators to Jarvis Hotels Limited by a newly established entity, Jupiter HotelsLimited

• Acquired:

➢ 21 properties on a freehold basis and 5 leaseholds and the operating company

➢ Post re-structuring; now branded Mercure (Accor franchised hotels)

• Acquired in joint venture (50:50) with West Register, Royal Bank of Scotland’s vehicle foracquiring real estate assets from defaulted RBS loans.

➢ First joint venture deal undertaken by West Register

• Jarvis had been in financial distress for 3 years. The acquisition of the business via a pre-packaged administration sale addressed a number of these issues immediately, i.e.:

➢ Over leveraged balance sheet: debt reduced by half (via write-off and cash equity) andprovided on attractive terms - post re-structuring LTC: 64%

➢ Loss-making leasehold properties: 15 leases not transferred to Jupiter (handed backto landlords) and 3 transferred with lower rents

➢ Poorly performing brand (Ramada): new franchise agreed by Jupiter with Accor,under the Mercure brand

• Strategy includes:

➢ Using the Mercure brand to produce an uplift in hotel performance

➢ Significant head office cost savings achievable in the short term by restructuring thehead office given reduced size of portfolio under management and a much smallersales and marketing function due to far higher sales support from Accor

➢ Capex program of £9m over next 2 years to address property related issues inaddition to ongoing FF&E expenditure to support performance growth

• Sold October 2015

Jupiter Hotels - sold (Fund III)

Leasehold Asset*

Freehold Asset

*Bristol asset now freehold

29

• Acquisition of a complex of 5 connected commercial real estate

assets in central Manchester, UK, held on a long leasehold basis

• Complex includes:

➢ The world renowned 21,000 person capacity MEN

entertainment arena, the second largest indoor arena in the

world based on 2009 ticket sales

➢ 149,000 ft2 of office area in two buildings

➢ Retail elements

➢ c.a. 1,250 space car park structure

• Very strong local partner Development Securities PLC (publically

listed property company) with considerable experience and first

rate reputation

• Strategy Includes:

➢ Renegotiation of the main Arena lease with the current tenant

creating a more stable and safe income stream – completed

➢ Agreement of a new Naming Rights deal to replace the

current deal at a higher level – completed

• Sold in October 2013 to UK property fund

Car ParkMartin House (Office)City Square (Retail)MEN ArenaArena Point (Office)

30

Manchester Arena Complex - sold (Fund III)

Poblenou - sold (Fund III)

• Acquisition of 3 residential blocks of apartments in

Barcelona from local developer Habitat (recently

emerged out of insolvency proceedings), comprising:

➢ 208 flats of 1, 2 and 3 bedrooms (14,700 sqm)

➢ 6 retail units (600 sqm)

➢ 230 parking spaces and 14 storage rooms

• Strategy is to sell individual units to tenants, new

occupiers and investors at a significant discount to

market prices (20%-35%%)

• Asset liquidity provided by (i) very good product

quality; (ii) strong location within Barcelona; (iii) micro

market with favourable supply/demand dynamics; and

(iv) attractive sale prices

• Asset management team has proven track record

(same base team as Patron’s Fund II BCN-2 deal)

31

32

• Acquisition in mid 2005 of a portfolio of eight buildings /

assets in France

• Office portfolio – three in and around Paris, one in Lille

• Leisure portfolio – two large Center Parcs, and two smaller

hotels in Courchevel

• Taken public as Vectrane, a French SIIC

• Investment activity included:

• Acquisition of additional office building in Lille and leisure

complex on the Alps

• 2 smaller assets (French Alp Hotels) sold to tenant (Pierre &

Vacances)

• Commencement of major renovation of Tour Anjou

• Sold entire shareholding (78%) to Eurosic in March 2007

Jesta / Vectrane - sold (Fund II)

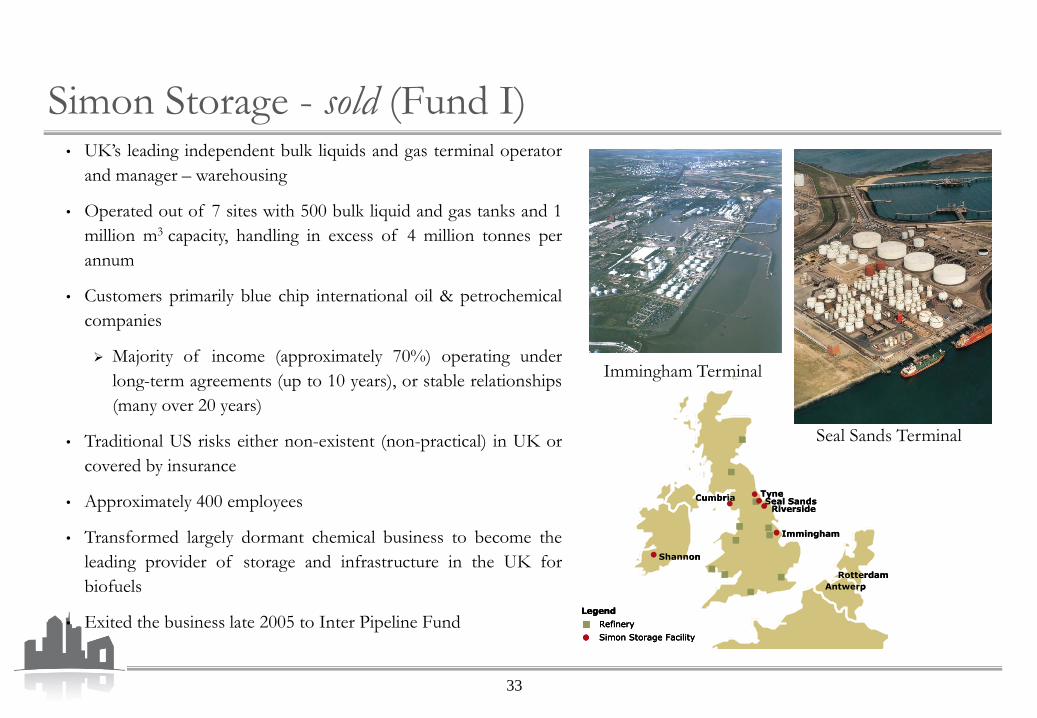

• UK’s leading independent bulk liquids and gas terminal operator

and manager – warehousing

• Operated out of 7 sites with 500 bulk liquid and gas tanks and 1

million m3 capacity, handling in excess of 4 million tonnes per

annum

• Customers primarily blue chip international oil & petrochemical

companies

➢ Majority of income (approximately 70%) operating under

long-term agreements (up to 10 years), or stable relationships

(many over 20 years)

• Traditional US risks either non-existent (non-practical) in UK or

covered by insurance

• Approximately 400 employees

• Transformed largely dormant chemical business to become the

leading provider of storage and infrastructure in the UK for

biofuels

• Exited the business late 2005 to Inter Pipeline Fund

33

Simon Storage - sold (Fund I)

TyneCumbria

Shannon

Seal SandsRiverside

Immingham

Antwerp

Rotterdam

Legend

Refinery

Simon Storage Facility

TyneCumbria

Shannon

Seal SandsRiverside

Immingham

Antwerp

Rotterdam

Legend

Refinery

Simon Storage Facility

Legend

Refinery

Simon Storage Facility

Immingham Terminal

Seal Sands Terminal

34

Hotel ArtsHotel Arts

Office BuildingOffice Building

Land PlotLand Plot

Retail & casino

area

Retail & casino

area

ApartmentsApartments

Hotel ArtsHotel Arts

Office BuildingOffice Building

Land PlotLand Plot

Retail & casino

area

Retail & casino

area

ApartmentsApartments

• Parent company (Sogo) went bankrupt forcing liquidation

• Assets trapped in complex corporate structure with management

contract on hotel

• Considered to be one of the best Ritz Carlton’s in the world

• Via corporate investment, acquisition of mixed use portfolio of

approx. 1.2 million square feet) consisting of:

➢ 44-story, 482-room, 5-Star Hotel Arts

➢ 12,375 sq.m Office Building

➢ 13,084 sq.m Retail Building

➢ 3,611 sq.m Land Parcel

• Deal won “International Hotel Deal of the Year” in 2001

• Harvard Business School case study notes its success despite

adversity

• Over 400 employees

• Majority sold in 2004, while retaining minority stake

• Final Exit in August 2006 to a Host Hotels & Resorts led investor

consortium

Arts Hotel Complex - sold (Fund I)

igroup – sold (Fund I)

• One of the leading players in the subprime UK mortgage

market

• One of the largest MBOs in the UK for 1999

• Growth from £450m to £1.6 billion in assets; growth

from £30m to £105m+ a month in originations at sale

• Company grew from 300+ to 800+ employees

• Equity partners include Royal Bank of Scotland (£76m)

and management

• Sold to GE Capital in 2001 and continues to be leading

performer

• Exit won “British Venture Capital Association Deal of the

Year in 2001”

35

36

Patron Capital Partners

One Vine Street

London W1J 0AH

Tel: +44-20-7629-9417

www.patroncapital.com

Contact Details