Summaries - Royal Agricultural Societies...

28

Summaries Summaries of the contributions given at the Workshop 'UK Lowland Animal Production in a Changing World' (5.09.2017), organised by the English Panel of the Fellowship of the Royal Agricultural Societies and held at the Farmers' and Fletchers' Hall in London. 1. Programme, delegates and background statistics provided by Prof Richard Bennett 2. Trends and futures for UK livestock production – Richard Bennett 3. Production and animal welfare – Peter C Jinman 4. Experiences in the pig sector – Meryl Ward 5. Dairy – Robert Craig 6. Poultry – Patrick Hook 7. Producers, consumers and the Government – Amy Jackson For main Report, see: http://royalagriculturalsocietiesawards.org

Transcript of Summaries - Royal Agricultural Societies...

Summaries

Summaries of the contributions given at the Workshop 'UK Lowland Animal

Production in a Changing World' (5.09.2017), organised by the English Panel of the

Fellowship of the Royal Agricultural Societies and held at the Farmers' and Fletchers'

Hall in London.

1. Programme, delegates and background statistics provided by Prof Richard

Bennett

2. Trends and futures for UK livestock production – Richard Bennett

3. Production and animal welfare – Peter C Jinman

4. Experiences in the pig sector – Meryl Ward

5. Dairy – Robert Craig

6. Poultry – Patrick Hook

7. Producers, consumers and the Government – Amy Jackson

For main Report, see: http://royalagriculturalsocietiesawards.org

2

Workshop: UK Lowland Animal Production in a Changing World

Objective This Workshop is intended to bring forward the views of the English section of the Fellowship (FRAgS) on the

ways in which lowland animal production should develop as the UK leaves the Common Agricultural Policy of

the European Union. These views and recommendations will then be welded into a report which we hope will

make a valuable contribution towards the evolution of new national policies.

We are grateful to the Worshipful Company of Farmers for inviting us to use their Hall and are pleased to

welcome members of the Livery as equal contributors to our discussions.

Programme

1030 Registration and coffee

1100 Introduction: Maurice Bichard FRAgS

1105 Background economics and future scenarios: Richard Bennett, ARAgS

1125 Animal Welfare: Peter Jinman, ARAgS

1140 Environmental policies: Teresa Dent, FRAgS

1155 Dairy: Robert Craig, NSch

1210 Pigs: Meryl Ward, FRAgS

1225 Poultry: Patrick Hook, NSch

1240 Producers, consumers, and the Government: Amy Jackson, NSch

1300 Lunch

1345 General discussion: David Leaver, FRAgS

1630 Tea

3

Workshop Delegates

Allen Bill Hart Charlie

Alvis John Hook Patrick

Alvis Johnny Jackson Amy

Arlington Michael Jinman Peter

Bargman Erica Jones Ken

Bennett Richard Leake Alastair

Beynon Neville Leaver David

Bichard Maurice Mead Mary

Blenkiron Andrew Mercer Roger

Bright David Penny Emma

Capper Jude Pexton Tony

Chamberlain Denis Reynolds John

Christensen Poul Roach Mark

Cooper Robert Seals Michael

Courtney Jeremy Stanley John

Crabtree Malcolm Stanley Pat

Craig Robert Stansfield Malcolm

Cross James Stocker Phil

Dent Teresa Tapp Nick

Dodgson Geoff Thorley John

Edwards Lyndon Tweddle Gordon

Fell Fiona Ward Meryl

Fell Hugh Wheatley-Hubbard Thomas

Fell Stephen Wibberley John

French Chris Wickham Teresa

Gardner David Wynn Philip

Godfrey Jim

Green Nick

4

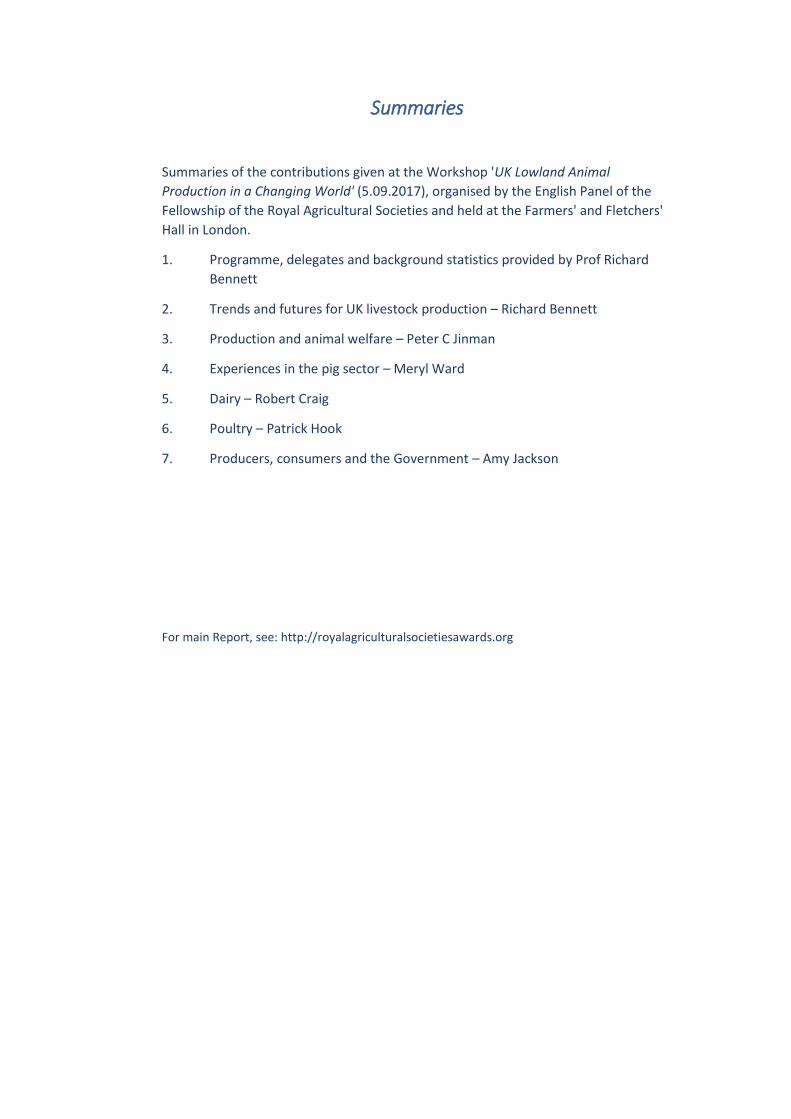

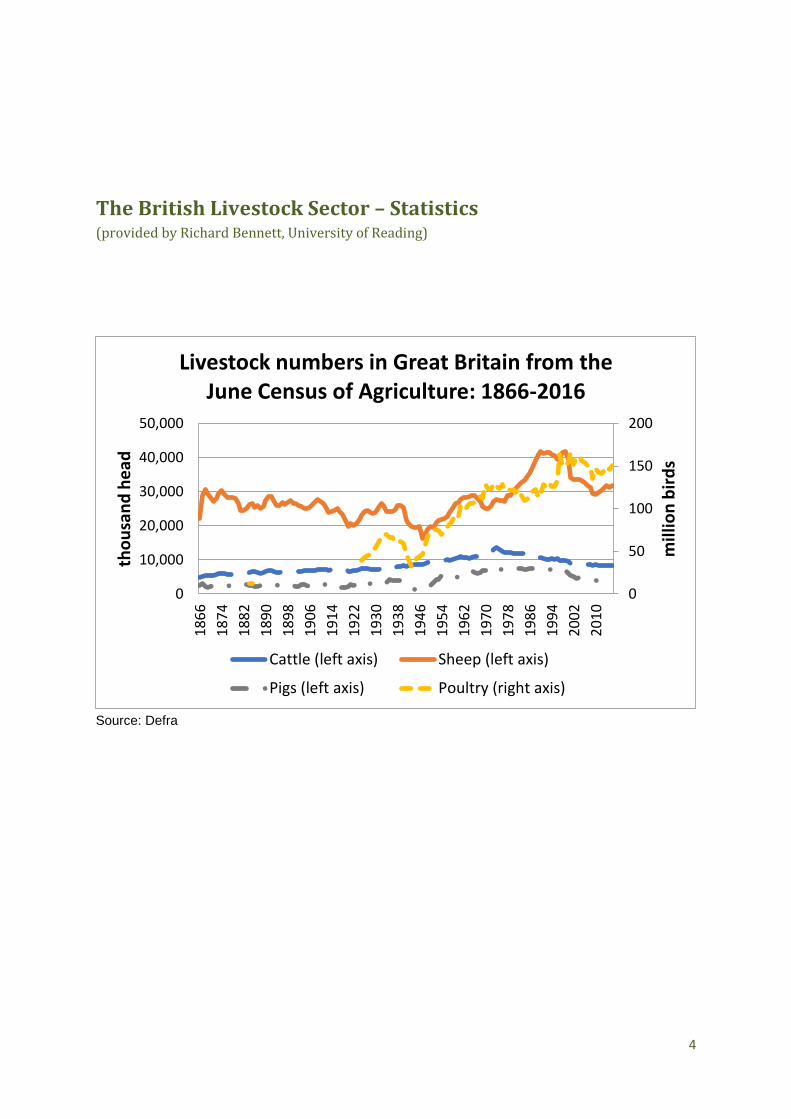

The British Livestock Sector – Statistics (provided by Richard Bennett, University of Reading)

Source: Defra

0

50

100

150

200

0

10,000

20,000

30,000

40,000

50,000

18

66

18

74

18

82

18

90

18

98

19

06

19

14

19

22

19

30

19

38

19

46

19

54

19

62

19

70

19

78

19

86

19

94

20

02

20

10

mill

ion

bir

ds

tho

usa

nd

he

ad

Livestock numbers in Great Britain from the June Census of Agriculture: 1866-2016

Cattle (left axis) Sheep (left axis)

Pigs (left axis) Poultry (right axis)

5

Source: Defra, Agriculture in the United Kingdom

Source: Defra, Agriculture in the United Kingdom

-

50

100

150

200

250

300

350

400

-

10

20

30

40

50

60

70

80

901

98

5

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

ste

ers,

hei

fers

an

d y

ou

ng

bu

lls (

kg)

Pig

s an

d S

hee

p (

kg)

Average dressed carcase weight (kg)

clean pigs (left axis)

clean sheep and lambs (left axis)

steers, heifers and young bulls (right axis)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

UK home-fed production 1985 to 2016 (thousand tonnes)

Beef and veal Pigmeat Mutton and lamb Poultrymeat

6

Source: Defra, Agriculture in the United Kingdom

Source: Defra

0

100

200

300

400

500

600

700

800

900

1,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,0001

98

5

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

Mill

ion

do

zen

Mill

ion

litr

esUK production of milk and eggs 1985 to 2016

(million litres/dozen)

Milk (left axis) Eggs for human consumption (right axis)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Number of UK holdings by type of holding (1987 to 2014)

Pigs and poultry Dairy

Grazing livestock (LFA) Grazing livestock (lowland)

7

Source: Defra, Agriculture in the United Kingdom

Source: Defra

0%

20%

40%

60%

80%

100%

120%

140%

Home-fed production as % of total new supply for use in the UK (1985 to 2016)

Beef Milk Sheep and lamb Pigmeat Poultry Eggs

0

100

200

300

400

500

600

700

800

900

1,000

Dairy cows Cattle and calves Sheep and lambs Female breedingpigs on holdingswith >=5 female

breeding pigs

Fattening pigson holdings with>=10 fattening

pigs

Average number of animals per UK holding

2005

2015

8

Source: Defra, Agriculture in the United Kingdom

Source: Own calculation based on Defra, Agriculture in the United Kingdom

0

20

40

60

80

100

120

140

160

180

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

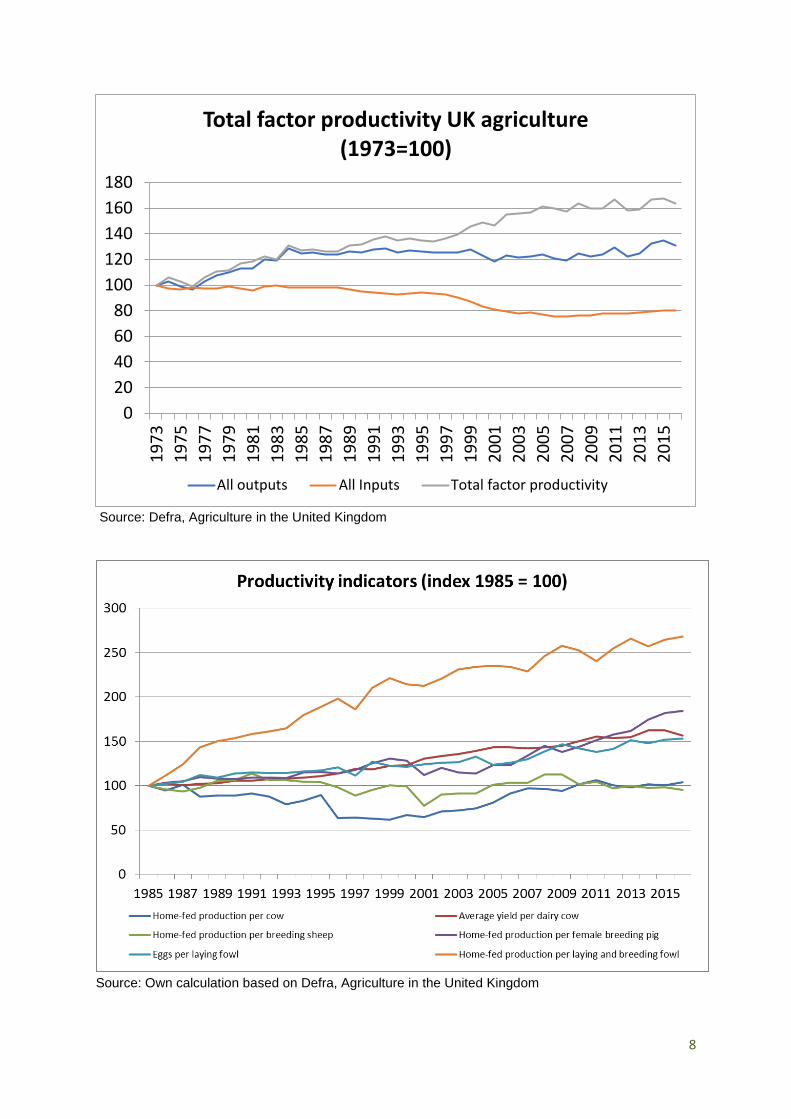

Total factor productivity UK agriculture (1973=100)

All outputs All Inputs Total factor productivity

9

Source: Defra, Agriculture in the United Kingdom

Source: Defra, Agriculture in the United Kingdom

20 000 40 000 60 000 80 000

100 000 120 000 140 000 160 000 180 000

Average farm business income per farm in UK (£ farm)

Dairy Grazing livestock (lowland)

Grazing livestock (LFA) Specialist pigs

Specialist poultry

0

20

40

60

80

100

120

140

160

Price indices for animals and animal products (2010 = 100)

Cattle and calves Pigs Sheep and lambs All Poultry Milk Eggs

10

Source: ONS, Retail Price Index

Source: ONS, Retail Price Index

0

50

100

150

200

250

300

3501

98

7

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

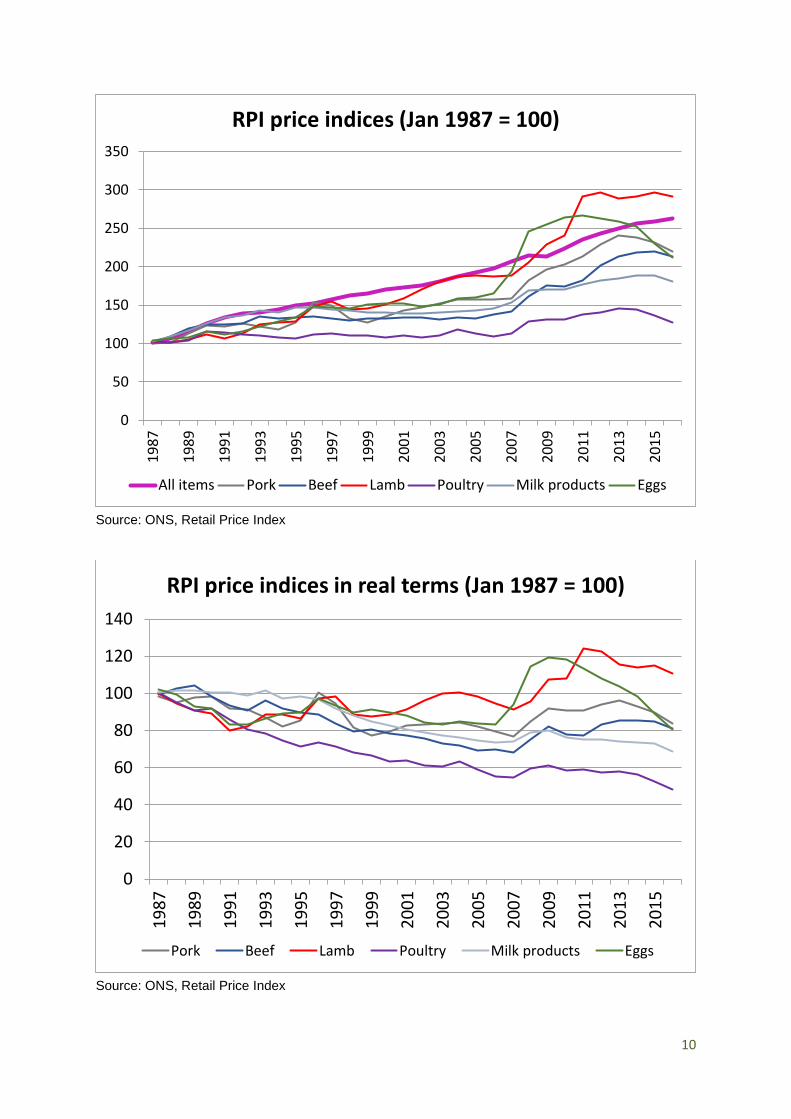

RPI price indices (Jan 1987 = 100)

All items Pork Beef Lamb Poultry Milk products Eggs

0

20

40

60

80

100

120

140

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

RPI price indices in real terms (Jan 1987 = 100)

Pork Beef Lamb Poultry Milk products Eggs

11

Source: Defra, Food Statistics Pocketbook 2016

Source: OECD

9.5

10.0

10.5

11.0

11.5

12.0

Share of spend on food and drink of all UK households (2003-04 - 2015)

0

5

10

15

20

25

30

35

40

45

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

PSE

% o

f gr

oss

far

m r

ece

ipts

Policy transfers to agricultural producers as a share of gross farm receipts for the EU

% Producer Support Estimate

12

Source: Defra, Agriculture in the United Kingdom

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 0001

99

3

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Direct payments to farmers and levies in the UK (£ million)

Total coupled payments less levies Total decoupled and other payments

Total direct payments less levies

13

14

15

16

17

18

Royal Agricultural Societies meeting September 2017

Production and animal welfare

Peter C Jinman

We are constantly told that the message from the market is that the consumer is king. That the farmer

responds to demand and produces as the purchaser requires, the Adam Smith ‘invisible hand of the

market’. Two things that have happened to this simple scenario are that the consumer has become

ever more interested in how, what they put in their mouths is produced and at the same time what it

does to the environment in producing it, both while still seeking or demanding a bargain.

At the time of writing the egg fipronil problem is unfolding with all the echoes of BSE as revelations as

to numbers and the extent of the liquid egg market becomes slowly exposed to the surprise of

government and amazement of the consumer.

So, what has this to do with animal welfare?

The story of modern animal welfare concerns and indeed the science of animal welfare goes back to

the publishing of the book Animal Machines by Ruth Harrison in 1964. It was the spark that set alight

the public interest in industrial scale farming particularly of poultry and pigs and then other livestock.

It gave rise to the Brambell committee and its report in 1965 into the welfare of animals kept under

intensive livestock husbandry systems. [Professor F.W. Rogers Brambell Dec 3rd 1965 HMSO London].

Implicit in the report was the concept of the Five Freedoms which were adapted by the Farm Animal

Welfare Council, itself a product of the deliberations by government after the Brambell report, to

produce in 1979 the now accepted, freedom from hunger, thirst or malnutrition; appropriate comfort

and shelter; prevention or rapid diagnosis and treatment of injury or disease; freedom to display most

normal patterns of behaviour; freedom from fear.

Farm animals were recognised as sentient beings under the EU Treaty of Amsterdam 1999 and

subsequently this was further recognised by the Animal Welfare Act 2006 whereby the duty to provide

for the needs of domesticated animals dependent on man were recognised and protected.

In recent years the Farm Animal Welfare Council [ now Committee] took this further by putting

forward the ethical argument that animals should have a life worth living and that the aim for all

keepers should be to move that basis of husbandry towards one of a good life. At no time should an

animal have a life that is not worth living.

The issue that is again facing the farming and retail industries is that of the welfare of animals and the

large-scale system of agriculture. Can the so called mega farm deliver the same freedoms as the public

perceive can be delivered by the small farmer and as such can the freedom to display normal patterns

of behaviour be accommodated or is this ‘freedom’ to be sacrificed at the altar of production efficiency

and excused on the grounds of the demand for cheap food.

Modern welfare science has moved from the consideration as to what constitutes a good design of a

building or of a production system that can keep an animal warm and dry and safe and well fed to one

of does it meet the behavioural or mental health needs for that species. The use of precision farming

techniques that relate the physiological and behavioural signs of contentment eg sitting or lying or

feeding time, to the structure and functioning of a building has become more important. Live video

linkage via a computer analytical programme of the distribution and behaviour of the birds in a poultry

19

shed can be used to distantly and automatically alter the light levels or heating or ventilation of a

poultry shed thus reducing the need for the owner or keeper of the flock to even be on site. Intra

ruminal boluses can measure the rumen pH of a dairy cow or monitor its body temperature and

transmit this information at regular intervals all day and night seven days a week, whilst at the same

time the amount of feed the animal has eaten in that day or part day can be assessed and at the next

milking should there be a variation from the programmed normal the cow can be separated by a

computer controlled shedding gate to ensure it is seen promptly by the stockman and its physical signs

of health assessed. The objective observer might not appreciate that the animal is less than optimally

efficient or perhaps that should be called sub-clinically unwell but the monitoring is registering the

variation from the normal. All of this is recorded and visible on a computer terminal or mobile phone

far distant from the farm and the operator can be on a different continent. The same is possible for

the slaughter process where central CCTV monitoring of the livestock handling areas of many abattoirs

can be viewed or analysed and actions or instructions fed back either in real time or after the event to

improve the welfare of the animals being presented for slaughter.

How far should society allow modern agriculture to ‘design’ the animal to fit the system?

At what level do the ‘acceptable losses’ because of the ‘efficient’ production, transport and slaughter

system that yields cheaper food become unacceptable to the industry and to the wider society?

The aim should be a good life and a good death for all production animals and transparent auditable

responsible agricultural production. Can this be done at a price that can realistically feed a nation and

maintain an industry?

20

FRAgS Report on Scale and Intensity in Livestock Production

Experiences in the UK Pig Sector

Meryl Ward

Background to changing structure of availability of supply, ownership, farm size, demand

and processing capacity (see attached slide presentation):

a) UK breeding herd shrunk from a peak of over 800,000 breeding sows 20 years ago to

just over 400,000 breeding sows. Production per sow increased from 19 to over 25

pigs sold per sow, increasing slaughter weight lifted pig meat per sow from 1345kg in

2000 to 2,062kg in 2015. Outdoor production around 220,000 sows, increased from

1998 at 180,000 sows, with significant decline in indoor breeding sow housing. Overall

pig meat production down from the peak of 1998. Self sufficiency down from over

80% to 55% (EU self sufficiency 110% 2015).

b) Changing structure with increase in small holdings (less than 5 breeding sows) but

decrease in number of other sized holdings. Removing the small holdings, average

breeding herd size continues to increase. Herd ownership changed dramatically with

ownership highly concentrated – top 16 companies own 50% of production, only 32%

in one or two site ownership. Much production physically split into 2 or 3 site pyramid

of breeding, rearing and finishing with many pigs looked after on a ‘contract rearing

arrangement’. Qu: what is the definition of a large farm – average breeding herd size

actually declining in the UK? Environmental Permitting Regulations have had an

influence on size of unit with the level at which a permit is required set at 750 breeding

sows or 2,000 pigs over 30kg. Ownership or processing has similarly concentrated

with 4 companies processing over 80% of the kill. The supply industries have

concentrated similarly with 3 major breeding companies, 2 national feed

compounders and around 20 specialist pig veterinary practices.

c) Type of housing: Since 1998, all dry sows have been grouped housed, the majority in

straw systems. Weaning age increased. Over 65% of finished pigs have access to

straw, and 80% in naturally ventilated buildings. 20% of weaners, 55 of growers and

2% of finishers are kept outdoors. A survey in 2012 put the average age of pig buildings

at 22 years, a figure which is unlikely to have changed since.

d) GB household retail purchases have shrunk driven by declines in fresh pork sales

although total pig meat consumption per head remains relatively static at 24.5 to

25kgs/head. UK exports of fresh/frozen pork are a major success story from a low

point of FMD in 2001 – over 50 countries with 19% to China in 2016.

21

e) Volatility in finished pig price and feed supply price continues to be a key feature of

the marketplace and driver of profitability. Since horsemeat gate, the mandatory

requirement for country of origin labelling on fresh pork, and the development of an

isotope database to check the origin of meat samples has led to a recognition of the

pig price premium over EU prices required for UK standard pig meat.

Qu: What do we mean by high welfare?

FAWC’s defines good welfare as skilled stockmanship, the system of husbandry and the

suitability of the genotype for the environment. The veterinary profession and producers

tend to concentrate on good physical health whereas the NGO’s consider behavioural issues

rather than aspects of physical health. FAWC’s view is that good physical health is essential

for good welfare but is not always sufficient because it does not always lead to a good mental

state. The difficulty lies in matching the triangle of advancing scientific knowledge with

imperfect public perception and farming systems that need time and capital to change. The

purchasing public has a wide choice of production systems without proper understanding of

the differences.

Qu: Do we live up to our ‘high welfare credentials’ with our current industry structure?

Our production is very different from other countries – predominantly in straw usage, natural

ventilation, group sow housing and outdoor production. Over 95% of pigs are housed on Red

Tractor assured units which are audited 5 times a year, including welfare outcome measures.

We have a comprehensive health surveillance system on farm and at abattoir with a ‘herd

health index’ currently being developed to cover on-farm mortality, post mortem health and

electronic medicine recording’. Potential electronic identification technology developments

have the potential to provide real-time data on farm and in abattoir to drive health

improvements further. There are aspects of our commercial production where there is

market failure or a lack of knowledge to encourage system change to improve welfare further

– e.g farrowing crates, some aspects of environmental enrichment in growing pigs, a reliance

on mutilations. International breeding companies do not necessarily prioritise welfare

requirements of the countries that are more advanced in their welfare developments, for

example in mothering ability of sows, social behaviour of growing pigs.

Qu: What are the benefits of increased scale and intensity? What problems can occur?

a) Stockmanship: Benefit of better training, skills development and accreditation.

Benefit of management structure and provision of expertise. Specialised veterinary

services (sometimes in-house). Expertise in nutrition and diet formulation.

b) System of husbandry: opportunity for specialisation, batching of same age groups for

health (can be separated by site). Increased opportunity for adopting technology

which is cheaper per head of animal. Exciting opportunities to take advantage of

improved ventilation systems, camera systems for detecting behavioural changes

indicating possible changes in health status, real time growth and food conversion

monitoring, more hygienic building materials, renewable energy and reduced

22

emissions whilst improving the atmosphere within the building. Health developments

– better use of preventive healthcare through regular veterinary visits, use of vaccines,

better diagnostics e.g saliva sampling and better health surveillance. Nutrition

developments – ability to match the diet to the pig age and weight, access to products

to improve gut health. Improved transport to factory with specialist livestock

trailers. All of this needs the caveat that as more choice is taken from the animal,

better controls need to be put in place.

c) Suitability of the genotype for the environment – ability to select for multiple traits

including traits which may have been incompatible under conventional breeding

programs e.g litter size and birth wt, sow appetite in lactation to enable milk production

for large litters. New molecular technologies have given the potential to screen and

eradicate individuals at risk of certain diseases and to develop robustness under

commercial conditions. However, intensive genetic selection of production traits can

result in detrimental consequences for health and welfare.

Qu: Have scale and intensity resulted in environmental damage?

In a UK context, emissions have not only reduced due to the reduction in livestock produced

but also due to improvements in production – reduced food conversion efficiencies, reduced

mortalities and better nutrient usage in pig diets. Compare other European countries, and

their pig densities – for example Denmark producing 30 million pigs compared to the UK 9.5

million. NVZ and EPR regulations have reduced the impact of emissions and new technologies

have extracted more value and better targeted value out of manures, and reduced resource

use (improved ventilation systems, LED lighting, improved cleaning methods using less water,

rain-water harvesting, manures in AD plants). The biggest issue is the speed with which

technologies are being adopted. Qu: Are Customers prepared to pay?

Qu: Are customers prepared to pay? What should they value?

Customers can’t pay if food is not labelled correctly. Cost of food is largely unrelated to the

cost of production (producer share of retail price fluctuates quite substantially at different

times and for different systems – retailers and food service operators have a major

responsibility to market products correctly). Better education is required both through the

school curriculum and at teacher training college for customers to make informed choices.

Qu: What should Govt be doing?

1. Improving education about food and food systems

2. Investing in R and D to get the balance of economics, social and environmental issues

right

3. Encourage the adoption of new technologies – the current opportunities are game

changers

4. Work with industry to establish collaborative projects where there is public good

5. Protect livestock health at our borders.

23

The Scale and Intensity in UK Livestock Production

Dairy Robert Craig

As a committed dairy farmer I’m concerned that as our numbers dwindle towards a mere

10,000 dairy farmers in the UK we’re still hearing calls for even further industry consolidation,

but towards what? My grandfather established the Sharpthorne herd (decedents of which I

still have today) in 1933 when there were around 250,000 dairy holdings in the UK. In 1933 a

dairy herd was just part of what was conventional mixed farming practice, where everyone

had a few of everything and there was little specialisation or species monoculture in

agriculture, around 10% of the work force worked on the land and so many more people had

a strong connection to farming and were closer to the production of their food. Since then in

the past 80 years there’s been massive global change to the way food is produced, transported

and consumed, with economics and politics playing an ever increasing role in the shaping and

direction of the global food system. Today like most other UK farming sectors Dairy is

becoming an increasingly marginal industry of economies of scale. Driven by the fantasy

economics of the current food system to produce cheap food, dairy farming is moving rapidly

towards two mainly intensive production systems, with herds being either housed totally or

the alternative, highly stocked grazing systems heavily reliant on the use of chemical nitrogen

fertilizer. The resulting businesses are predominantly large and to some extent would appear

to be economically robust but painting a picture completely at odds with the reality. Dairy,

which inline with most other intensive farming practice has ignored nature’s balance sheet

and has largely failed to account for the cost of the natural resource we’re consuming in

modern production systems. Along with the challenge of accounting for natural capital one of

the main issues dairy farming faces is the shortage of skilled people to operate increasingly

complex businesses and again similar to other sectors highly dependent on migrant labour

which it seems may become another casualty of BREXIT.

This restructuring of the industry is nothing new, it’s been happening as far back as you have

a mind to go, but at what point does this intensification lose sight of what we’re actually trying

to do and become just another production line with little regard for what we’re producing or

the impact we’re having on the resource we’re using to produce it. Nature aside - I think my

most pressing concern is the way in which during my career in dairy farming of three decades

I’ve seen all food becoming valued less and less by successive generations. This expectation

of low prices combined with ruthless retailer competition has unfortunately resulted in many

consumers believing food should and will always be low cost and is also limitless. Possibly this

is one of the reasons few from outside the industry chose agriculture as a career path,

although perhaps it’s unsurprising if you consider why anyone would wish to be associated

with the production of a valueless product. Unfortunately since deregulation the dairy

industry seems to gone from crisis to crisis, bankruptcy after insolvency and the disastrous

effects of EU milk quotas siphoning many millions of much needed capital from the industry

which could have been better put to use building integrated value chains which all dairy

farmers could have benefited from. But even after all that’s happened in the last twenty years

24

we still fail to learn from the mistakes of the past, today we expect a tiny amount of levy funds

gathered by the AHDB to do all the research we need, extend it effectively industry wide while

still having enough left over to promote the dietary benefits of dairy nutrition to consumers.

If we were really serious about achieving a less marginal future we’d be spending at least 10%

of our revenue on promotion annually, building value back into not just dairy products but

also into the industry. 23 years after deregulation we seem further from our customers than

we’ve ever been, some how believing it’s not our job to market what we produce, our

responsibility ending at the farm gate or when our milk is loaded on to the tanker. As

economics have dictated we adopt more intensive systems of production we seem more

reluctant to promote what we do, almost as if there’s an embarrassment that consumers may

discover the cosy image of farming is different to what they perceive it to be.

25

Scale and Intensity in UK Livestock Production

Poultry

Patrick Hook NSch

The UK poultry industry is one of the oldest in the world and the sector continues to grow at an annual rate of 2-3% and in 2015 the UK poultry meat industry contributed £4.6 billion to UK GDP. 2050 is the year being marked for a global population of 9 billion people and the UK will have to adapt and grow to meet this challenge. Farms have grown in size and genetic improvement has helped the industry produce an efficient, affordable, healthy and versatile protein. Chickens achieve FCR’s of 1.5; gain a day in growth each year and have better liveability. The challenge, is can the industry grow a 2.4kg in 30 days; whilst maintaining all the key welfare traits that farmers, customers and consumers demand? The modern day broiler is an extremely sustainable protein at a time where competition for resources will be fierce. The future chicken may be a slower growing concept; at a cost of £0.15 pence per kilo cost, with more farming space needed a 40 point increase in FCR and an increase in the carbon footprint of the chicken. Is this really sustainable? Out of 37,000 direct employees in the UK industry, 60% are migrant workers. Brexit will challenge the UK’s ability to recruit and retain a competent and reliable workforce. There will be massive implications for factories; which on average employ 90% foreign labour and the industry will have to downscale if the chickens cannot be processed. The UK, as part of the EU, has the highest welfare standards and regulation in the world, leading the way in research and development and protecting us from cheaper inferior imports. Post-Brexit trade deals could threaten our supply of clean, safe, traceable and high welfare chicken. Imported chlorinated chicken from the USA, grown in substandard conditions could be on the shelf. Current volumes of 21 million chickens a week could be reduced to 10 million. The UK is approximately 75% self-sufficient in poultry meat and 75% of our imports and exports are to the EU. European trade is vital to get value from dark meat and to get value from parts that would be otherwise disposed of. The UK poultry industry has seen consolidation and has excellent working links on issues such as antibiotics and campylobacter. The industry unites and tackles issues for the benefit of agriculture, its customers and consumers. This strength has recently driven an 80% reduction in prophylactic antibiotic use and the industry now promotes responsible use of antibiotics, prioritising the welfare of the bird. This consolidation also has massive advantages in communication of issues such as Avian Influenza and the control and spread of these outbreaks. This power to lobby and make decisions on this scale will continue to be advantageous in the future. UK consumers are demanding more, at lower prices, whilst maintaining best quality and welfare. Through the Red Tractor assurance scheme and good regulation, British chicken is grown to the highest standards in the world and has complete traceability. However the power and influence of welfare groups cannot be ignored and the industry must do a better job at communicating and demonstrating what it does to produce high welfare British Chicken, to mitigate the risk of aggressive campaigns against the sector. The growth of flexitarians and pressure to reduce meat consumption means the industry’s projected growth could reduce and there could be surplus farming space they may have to close. Avian Influenza (AI) is becoming endemic throughout the world and strategies must be consistent and robust in tackling and preventing future outbreaks. There should be mechanisms built into the planning process to ensure new poultry sites are put up in areas of minimal risk and guidance should be given to new entrants about the importance of biosecurity.

26

The UK Broiler sector has grown successfully without subsidies thanks to tight supply chains, genetic improvement, and its adaptability, whilst being customer focused. There is an opportunity to reengage with consumers to better understand their needs and ensure we clearly communicate what we do.

27

Producers, Consumers and the Government: drawing

everyone closer

Amy Jackson

We are currently experiencing one of the biggest shifts we’ve ever seen in the environment

around farming for decades. It’s not all Brexit either, although this is a factor with Government

in apparent turmoil over what role UK agriculture should play in a Britain outside the EU. Are

we just a delivery mechanism for biodiversity, landscape and ecosystem services? Is our

importance in sustaining rural communities recognised? And – the biggest ask – will our

strategic importance at the apex of the UK’s enormous food and drink industry (employing

400,000 people and contributing £28.2bn to the economy annually) be acknowledged, with

farms finally regarded as businesses?

These are valid concerns, but my bigger worry at the moment is farming’s rapidly eroding

place in the public’s wallets, minds and hearts, and the rise of movements that question the

ethics and fundamental principles of how we produce our food.

In April, The Times columnist Matt Ridley pointed out that the historical decline in acceptability

of violence and exploitation could mean that people may look back on the rearing of animals

for slaughter as barbaric. One might be tempted to assign this story to the ‘interesting but

fantastical’ shelf, alongside the time travel and colonising Mars. But it’s a very real threat.

Citizens concerned about how we produce our food have not historically impacted consumer

behaviour at the checkout. I believe this is changing – firstly because the lobbies that

traditionally criticised farming on a number of fronts are now mainstream, and secondly

because our consumers are changing. The Grey Pound is weakening and the Millennial

Bitcoin is gaining strength.

Born somewhere between the 80s and the mid-naughties, Millennials have a different

perspective on life. At a recent farm marketing conference in the US one speaker described

how Millennials find science-based information suspect when it contradicts views formed

through the self-teaching world of the internet and social media. They also demand

transparency, value brands with character and beliefs, and treat food not as a staple but as a

luxury or statement item.

The proliferation of messages online about how glyphosate is penetrating our bodies, animal

agriculture is a major contributor to climate change, and our meat-eating habit is soaking up

precious resources, are becoming fact in many eyes. And as Dr Jude Capper recently pointed

out in a paper examining how we communicate animal agriculture, it takes at least five positive

pieces of information to displace one negative.

This new citizen is waking up to all sorts of novel concepts we assumed people already knew

– that crops are sprayed, calves are separated from their mothers when hours old, and we

rely on artificial insemination of animals for reproduction. Our laziness (at best) or reluctance

(at worst) at communicating what happens on farms has given campaigners an opportunity to

present these practices as hidden and somehow subversive. As another journalist explained

recently, the change of tactics has paid off. Campaigners have stopped holding protests and

28

focus instead on showing the public what the industry would ‘rather keep hidden’. People don’t

like the idea of information being withheld from them.

We really need to wake up to this. We must reconnect with our citizens. We must proactively

occupy the space and be the ones having conversations with our consumers, not

campaigners. We have to stop trotting out science and start using common sense ways to

explain what we do. And most difficult of all, we need to take the bold step of stopping practices

that we simply cannot defend. What role does Government play in this? I’m not sure it does –

but the best we can do is make it easy for Government to support what we do. It’s a brave

new world. We no longer have a right to farm or a mandate to do it the way we feel is best.

The buffer has gone and the gloves are off. Time to start reconnecting with our consumer.