SUIVI DES RECOMMANDATIONS DU PE DANS LE CADRE DE … · SUIVI DES RECOMMANDATIONS DU PE DANS LE...

25

SUIVI DES RECOMMANDATIONS DU PE DANS LE CADRE DE LA DÉCHARGE 2006 TABLEAU DE BORD § SUJET POSITIONS DE LA COMMISSION PLAN D'ACTION CHEF DE FILE ET SERVICES ASSOCIÉS ÉCHÉANCE COMMENTAIRES / UPDATE 27.05.2008 1 Welcomes the progress made by the Commission towards a more efficient use of EU funds and in the overall control environment, which is reflected by the ECA's statement of assurance (DAS); welcomes in this light the statement of the ECA on the financial impact of errors; invites it to apply this to all chapters of its annual report in the future This seems contrary to the normal practice of the Court but will be decided by the Court. The Commission has set up an Action Plan "Towards an Integrated Internal Control Framework" which addresses the main gaps identified in the control framework. This includes formalisation and harmonisation of the presentation of the internal control strategies, the aim of which is to provide an overall view of the internal control flow and related accountability chain and to document how associated risks are addressed. Internal Control Templates have been included in AAR 2007. AIDCO G2 DONE 9 3 Welcomes the commitment by the Commission to report on a monthly basis to its Committee on Budgetary Control on the implementation of the follow-up to the 2006 discharge procedure, whereby every month one Member of the Commission presents developments in his or her area of responsibility, covering national declarations and annual summaries, external actions and the implementation of the action plan to strengthen the Commission's supervisory role under shared management of structural actions; -See Vice-President reply to Mr Bösch (17/4/08) Report on a monthly basis to the Committee on Budgetary Control on the implementation of the follow-up to the 2006 discharge procedure. DG BUDG Chef de File + AIDCO G2 associated ON GOING Monthly reporting AIDCO will transmit to DG BUDG the requested information by end of may and following months. 16 Considers that following the discharge procedure in respect of the financial year 2006, the Commission has become increasingly aware The Joint Visibility Guidelines have been approved and adopted in the 5 th FAFA AIDCO G8 DONE

Transcript of SUIVI DES RECOMMANDATIONS DU PE DANS LE CADRE DE … · SUIVI DES RECOMMANDATIONS DU PE DANS LE...

SUIVI DES RECOMMANDATIONS DU PE DANS LE CADRE DE LA DÉCHARGE 2006

TABLEAU DE BORD

§ SUJET

POSITIONS DE LA COMMISSION PLAN D'ACTION CHEF DE FILE ET SERVICES

ASSOCIÉS

ÉCHÉANCE COMMENTAIRES / UPDATE 27.05.2008

1 Welcomes the progress made by the Commission towards a more efficient use of EU funds and in the overall control environment, which is reflected by the ECA's statement of assurance (DAS); welcomes in this light the statement of the ECA on the financial impact of errors; invites it to apply this to all chapters of its annual report in the future

This seems contrary to the normal practice of the Court but will be decided by the Court.

The Commission has set up an Action Plan "Towards an Integrated Internal Control Framework" which addresses the main gaps identified in the control framework. This includes formalisation and harmonisation of the presentation of the internal control strategies, the aim of which is to provide an overall view of the internal control flow and related accountability chain and to document how associated risks are addressed. Internal Control Templates have been included in AAR 2007.

AIDCO G2

DONE

3

Welcomes the commitment by the Commission to report on a monthly basis to its Committee on Budgetary Control on the implementation of the follow-up to the 2006 discharge procedure, whereby every month one Member of the Commission presents developments in his or her area of responsibility, covering national declarations and annual summaries, external actions and the implementation of the action plan to strengthen the Commission's supervisory role under shared management of structural actions;

-See Vice-President reply to Mr Bösch (17/4/08)

Report on a monthly basis to the Committee on Budgetary Control on the implementation of the follow-up to the 2006 discharge procedure.

DG BUDG Chef de File

+ AIDCO G2 associated

ON GOING

Monthly reporting

AIDCO will transmit to DG BUDG the requested information by end of may and following months.

16 Considers that following the discharge procedure in respect of the financial year 2006, the Commission has become increasingly aware

The Joint Visibility Guidelines have been approved and adopted in the 5th FAFA

AIDCO G8

DONE

2

of the importance of transparency, visibility and political guidance for all EU funds implemented in the area of external actions, be it directly by the Commission or via decentralised management or international trust funds;

working group meeting (10-11 April 2008)

17 Welcomes the commitment of the UN representative to Iraq to improve real time information to the Commission, and considers that the 13 months of close research into the use of EU funds via international trust funds has contributed to increased awareness of the need for accountability regarding the use of EU taxpayers' money; invites the Commission to cooperate closely with it in the revision of the Financial and Administrative Framework Agreement between the European Community and the United Nations (FAFA);

As for Iraq, the Commission confirms its commitment to provide up dated information on EU aid to Iraq by producing and distributing to the EP a monthly state of play. As for the revision of the FAFA, the Commission has expressed its intention to cooperate closely with the Parliament in this respect. An informal meeting was organised on 9 April 2008 with a group of MEPs from AFET, DEVE, BUDG and CONT to ensure that Parliament's concerns were taken duly account ahead of the annual FAFA meeting with the UN.

Iraq : production and diffusion of a monthly state of play

FAFA: A letter was sent on 6 May to Mr Gahler to inform the Parliament of the outcome of the Vienna meeting.

The Commission will inform the Parliament on improvements in the operation of the FAFA in the future.

AIDCO, RELEX

+ AIDCO A2 for

Iraq +

AIDCO G8 for FAFA

+ AIDCO G2 Associated

Monthly report

ON GOING

In view of the progress made at the meeting in Vienna on 10-11 April on the key issues of visibility and verification it does not seem necessary at this stage to push for changes in the FAFA agreement itself.

AIDCO A2 will update the Iraq State of Play monthly. Next one on 31/05/2008 . Expected to be distributed before the next COCOBU meeting (2/3 June) which will discuss the MEP CASACA field Mission Report.

18 Welcomes the fact that the Commission included information on verification missions under FAFA, as well as the relevant conclusions, in the annual activity reports signed by the competent Directors-General at the end of March 2008, and that this allowed Parliament to take that information into account during its vote on this report

In line with conclusion 17 of the Parliament's discharge resolution, the AAR 2007, signed in March 2008 by Director General Koos Richelle, includes information on verification missions under FAFA, as well as the relevant conclusions. The AAR 2007 includes reporting on missions to all international organisations, including the UN.

The AAR 2007 includes reporting on missions to all international organisations, including the UN.

AIDCO G8 +

AIDCO G2 associated

DONE

19 Accepts the Commission's proposal to discuss the question of a definition of nongovernmental organisation (NGO) after the results of the ECA's ongoing audit of NGOs have been made available;

See point 13 of Vice-President Kallas letter of 17 March 2008.

Considering these legal issues, the Commission proposes to discuss this matter with members of the EP

The Commission proposes to discuss this matter with members of the EP coming from the different competent Committees following the

AIDCO F 1 +

AIDCO G2

31/03/2009 In the meanwhile, AIDCO will start looking at the issue of a definition of NGO.

3

coming from the different competent Committees following the results of the Court of Auditors' ongoing audit on NGOs.

results of the Court of Auditors' ongoing audit on NGOs.

See 181

20 Calls on the Commission to:

a) provide it with regular information on EU financing of multi-donor trust funds, both on its own initiative and at Parliament's request;

b) present measures on how to improve the visibility of EU funds when implementing external aid via other organisations;

c) present measures aimed at allowing better access for EU auditors (ECA, Commission or private audit firms) to carry out audits of projects under joint management, especially joint management with the UN

a) The Commission has provided a list of EU financing of multi-donor trust funds. The Commission also agrees to provide Parliament with regular up-dated information on EU financing of multi-donor trust funds, and has proposed ways of keeping Parliament better informed on a regular basis in future;

b) the Commission agrees to present measures to achieve improved visibility. Letters were co-signed in 2006 and 2008 by Commissioner Ferrero Waldner with the UN and the World Bank to this effect, copies of which have been provided to Parliament, and detailed operational guidelines are being agreed with these organisations;

c) Current FAFA agreements with the UN already provide for access of EC officials, including the Court of Auditors, to UN project documentation for control purposes. The Commission is further discussing this issue with the UN in the framework of the FAFA and will report results to the EP.

• The Commission will provide information on multi-donor trust funds annually and at Parliament's request. For Iraq and Afghanistan, the Commission will provide a monthly state of play (see points 17 and 209).

• The Joint Visibility Guidelines have been approved and adopted in the 5th FAFA working group meeting (10-11 April 2008)

• The need for access for EU representants to carry out verification missions for projects under joint management has been reiterated during the 5th FAFA WG. Common ToR for verifications are being developed by EC / UN, which aim at facilitating the performance of such verification missions.

AIDCO G8 +

AIDCO G2 +

Iraq: A2 +

Afghanistan: D1

01/07/2008

ON GOING

AIDCO A2 will update Iraq the State of Play monthly. Next one on 31/05/2008 (See also pt 17)

Work on going in Aidco D1 for the production of a similar document on Afghanistan.

The Commission has proposed organising a meeting with members of COCOBU, AFET, DEVE and trust fund managers (dates to be confirmed)

21 Welcomes the Commission's commitment to further inform it of beneficiaries of funds, as referred to in Article 30(3) of the Financial Regulation, as well as to further increase political steering, visibility and control over

The Commission intends to fulfil the requirements of the Financial Regulation (FR) (under Art. 30.3) applicable as from 1/5/07 for all operations related to external

- Note of information sent by Aidco DG to all EC delegations

AIDCO F4 +

AIDCO G7 +

As from June 2008

and following

The instruction Note (D (2008) D/9337) was signed on 21.05.08. With this note all concerned services were requested to

4

these funds, in particular over funds managed via international trust funds

assistance and programmes starting after this date. The Commission confirms its commitments of increasing visibility and control over funds managed via international trust funds.

- PRAG is updated according to schedule.

AIDCO 04 +

Directorates A B C D F

+ Delegations

years take the required measures to meet the legal requirements for all modes of implementation by end of June 2008. Consolidated information to the EP will be made available before 15 July 2008.

Discussion are on going as for operations with International Organisations.

Commission (DG Budg) expected to provide a communication of the definition of Beneficiaries in July 2008.

22 Insists on public access to information concerning all members of expert and working groups working with the Commission, as well as full disclosure of beneficiaries of EU funding;

As to meeting the obligations of full disclosure of beneficiaries of EU funding under Article 30(3) of the Financial Regulation by AIDCO, see reply to point 21.

SG +

BUDG

See pt 21 as for beneficiaries of EU funding.

181 Urges the Commission to present its definition of a non-governmental organisation, focussing not only on legal aspects but also on the way the non-governmental financing of these organisations is ensured; 19 -Accepts the Commission's proposal to discuss the question of a definition of nongovernmental organisation (NGO) after the results of the ECA's ongoing audit of NGOs have been made available;

See point 13 of Vice-President Kallas letter of 17 March 2008.

Considering these legal issues, the Commission proposes to discuss this matter with members of the EP coming from the different competent Committees following the results of the Court of Auditors' ongoing audit on NGOs.

The Commission proposes to discuss this matter with members of the EP coming from the different competent Committees following the results of the Court of Auditors' ongoing audit on NGOs.

AIDCO F 1 +

AIDCO G2

31/03/2009

To be further discussed. There is no single comprehensive legal definition of an NGO. The Development and Cooperation Instrument, as of January 2007, therefore provides the typology of reference with regard to non state actors eligible for co-financing.

5

See also point 19

182 Recalls that funds spent on external actions in 2006 totalled EUR 5,867 billion and payments EUR 5,186 billion; notes with concern the following findings in the ECA's Annual Report: – a high incidence of error in the sample tested at the level of project-implementing organisations; – weaknesses in the supervisory and control systems designed to ensure the legality and regularity at the level of project-implementing organisations; – that the highest risk areas were again the contracting procedures, the eligibility of expenditure at project level and the insufficiency of supporting documentation;

Certain errors concerned current contracts for which the final payment had not yet been made in relation to which corrective action should therefore have been taken at the time of closure under the Commission control. Implementing organisations are not part of the Commission's internal control system. They are linked to the Commission by a contractual relation for the implementation of a specific action. The fact that a weakness is identified at implementing organisation level implies neither a weakness of the Commission control system nor that this weakness will go undetected by the Commission.

- Tendering procedures, the eligibility of expenditures and supporting documentation are the main bulk of verifications made by the auditors when assessing the projects in the external field system.

• Standard ToR for audits (financial and systems) are mandatory since October 2007;

• Expenditure verifications for grants and services fee based contracts are mandatory since February 2006;

• The 4 pillars exercise has been completed for the WB and more than 97% of the UN family;

• Organisations entitled to manage projects under indirect centralised management have been submitted to the previous assessment;

• Standard ToR for program estimates will be finalised before the entry into force of the 10th EDF

AIDCO G2 Chef de File

+ AIDCO G8 associated

DONE This set of tools will progressively allow to better identify and correct errors detected at the level of implementing organisations.

See also points 198 and 207

183 Regrets the ECA's finding that, as concerns the annual activity report of DG AIDCO, "the material incidence of error and the weaknesses in the supervisory and control systems designed to ensure the legality and regularity of the transactions at the level of project implementing organisations in the area of external actions found by the ECA are not sufficiently reflected in the annual activity report and declaration of Europe Aid Cooperation Office" (point 2.17 and Table 2.1 of the Annual Report);

The Commission is aware that there is always room for improvement but considers that the systems currently in place provide reasonable assurance concerning the legality and regularity of external action expenditure as a whole

The material incidence of error and the weaknesses in the supervisory and control systems designed to ensure the legality and regularity of the transactions at the level of project implementing organisations in the area of external actions found by the ECA are reflected in the 2007 AAR and declaration of AIDCO.

AIDCO G2

DONE In the context of the 2007 AAR, the Commission explained in a explicit way the difference of appreciation between the Commission and the Court of Auditors.

6

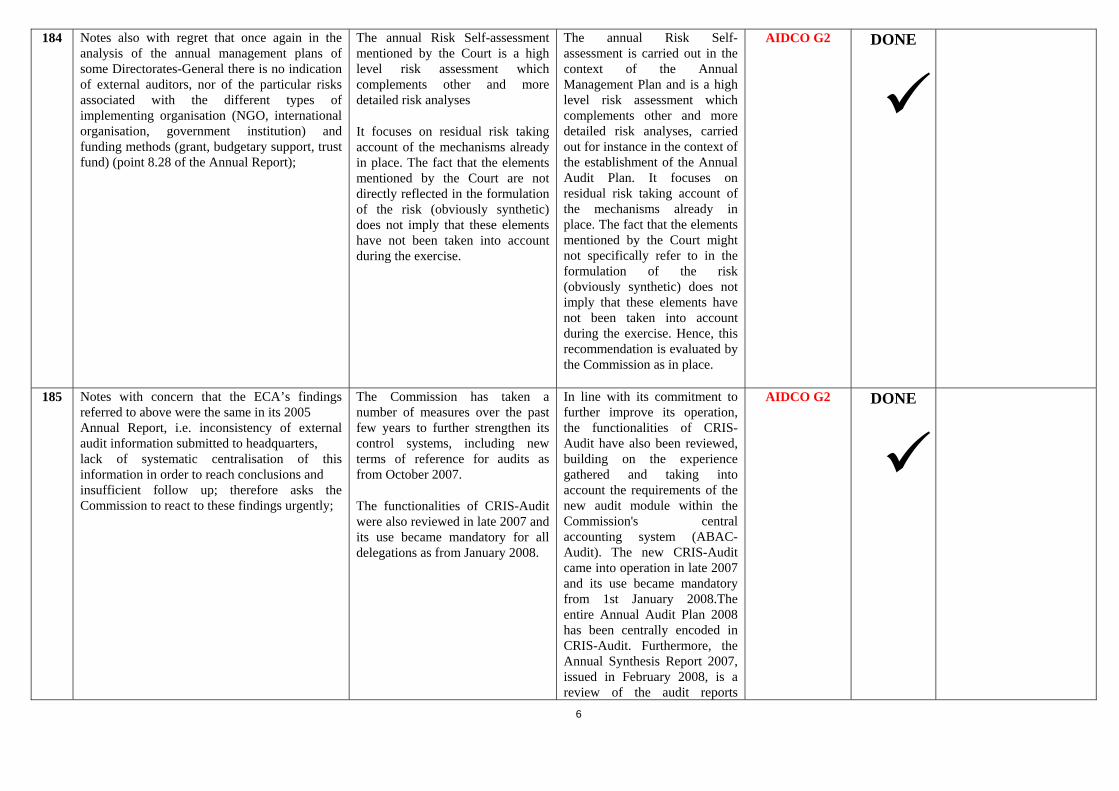

184 Notes also with regret that once again in the analysis of the annual management plans of some Directorates-General there is no indication of external auditors, nor of the particular risks associated with the different types of implementing organisation (NGO, international organisation, government institution) and funding methods (grant, budgetary support, trust fund) (point 8.28 of the Annual Report);

The annual Risk Self-assessment mentioned by the Court is a high level risk assessment which complements other and more detailed risk analyses

It focuses on residual risk taking account of the mechanisms already in place. The fact that the elements mentioned by the Court are not directly reflected in the formulation of the risk (obviously synthetic) does not imply that these elements have not been taken into account during the exercise.

The annual Risk Self-assessment is carried out in the context of the Annual Management Plan and is a high level risk assessment which complements other and more detailed risk analyses, carried out for instance in the context of the establishment of the Annual Audit Plan. It focuses on residual risk taking account of the mechanisms already in place. The fact that the elements mentioned by the Court might not specifically refer to in the formulation of the risk (obviously synthetic) does not imply that these elements have not been taken into account during the exercise. Hence, this recommendation is evaluated by the Commission as in place.

AIDCO G2

DONE

185 Notes with concern that the ECA’s findings referred to above were the same in its 2005 Annual Report, i.e. inconsistency of external audit information submitted to headquarters, lack of systematic centralisation of this information in order to reach conclusions and insufficient follow up; therefore asks the Commission to react to these findings urgently;

The Commission has taken a number of measures over the past few years to further strengthen its control systems, including new terms of reference for audits as from October 2007.

The functionalities of CRIS-Audit were also reviewed in late 2007 and its use became mandatory for all delegations as from January 2008.

In line with its commitment to further improve its operation, the functionalities of CRIS-Audit have also been reviewed, building on the experience gathered and taking into account the requirements of the new audit module within the Commission's central accounting system (ABAC-Audit). The new CRIS-Audit came into operation in late 2007 and its use became mandatory from 1st January 2008.The entire Annual Audit Plan 2008 has been centrally encoded in CRIS-Audit. Furthermore, the Annual Synthesis Report 2007, issued in February 2008, is a review of the audit reports

AIDCO G2

DONE

7

received in 2007 by Headquarters and Delegations, and aims at giving AIDCO Headquarters an overview of the main audit findings related to its activities.

186 Regrets also that according to the ECA's Annual Report "the Internal Audit Capability (IAC) does not at present provide an annual overall assessment of the state of internal control in Europe-Aid and DG ECHO ... Despite the creation during 2006 of two additional posts in the IAC, it does not seem feasible with the present staff complement to carry out, within the three-year cycle proposed, the full audit coverage identified in the Europe-Aid Audit Needs Assessment" (point 8.30 of the Annual Report);

The IAC's work programme for 2007-2009 is on track. Following the single audit approach, the work of the IAC together with the audits performed by the IAS will enable the coverage of the most significant risks identified in DG AIDCO by the end of 2009.

AIDCO 02 +

AIDCO G2 associated

DONE

187 Asks the Commission to carry out an annual overall assessment of the state of play of internal control in DG AIDCO and to evaluate whether additional posts are necessary in the IAC service;

Currently, the IAC charter does not refer to an overall assurance but rather to an opinion in specific assurance audit engagements. The IAC audit capacity is assessed on an annual basis when preparing the audit plan. This is done in a coordinated way with the IAS.

IAC has been reinforced by two new posts.

AIDCO DONE

188 Notes the situation criticised by the ECA as regards the Commission's ex post control activities (points 8.23 and 8.33 of the Annual Report), and calls on the Commission to regularly inform its Committee on Budgetary Control of the steps taken to remedy the situation;

Ex-post transactional controls provide an additional layer of assurance for the appreciation of payments, recoveries and clearance of pre-financing transactions carried out by the Commission. Transactions at implementing organisation level fall within the scope of other controls, notably audits. More than 90% of the total amounts of grants are covered by audits.

The transactional ex post control function was first set up in EuropeAid in May 2004, and the function has largely been carried out in the operational directorates since 2005, with the necessary safeguards to ensure homogeneity across these different services.

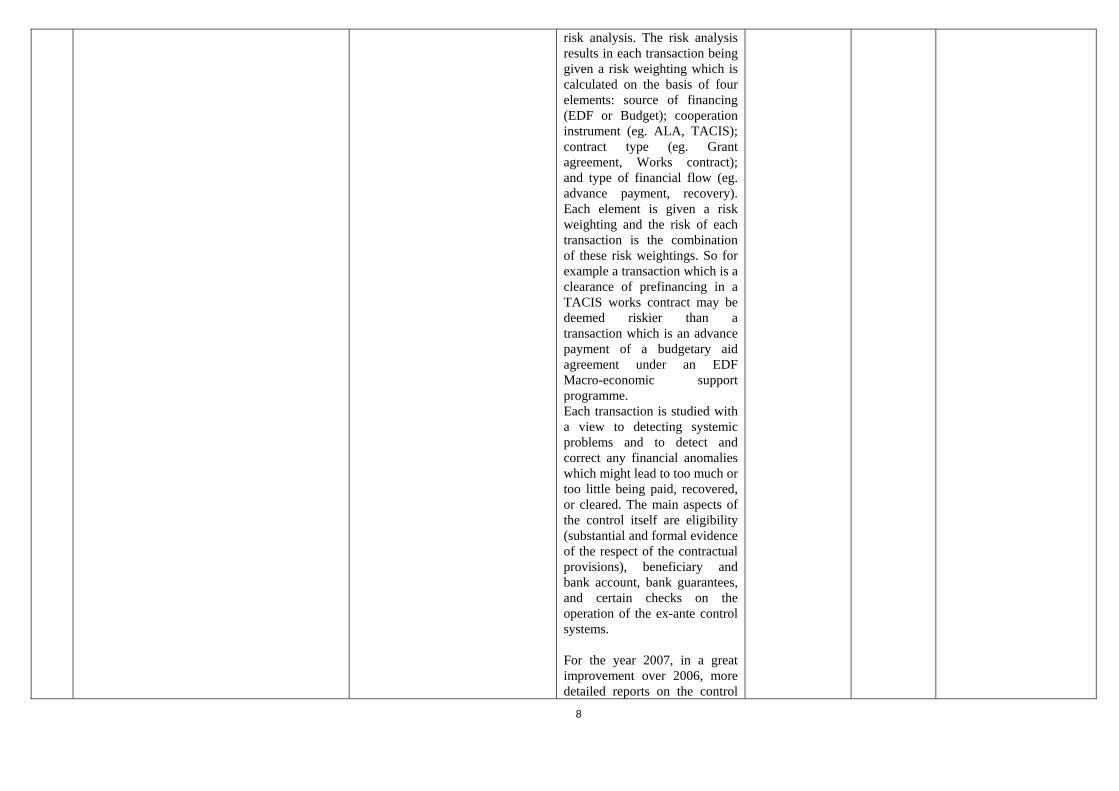

The control is based on a monetary unit sampling (MUS) of transactions which have been pre-selected on the basis of a

AIDCO DONE

8

risk analysis. The risk analysis results in each transaction being given a risk weighting which is calculated on the basis of four elements: source of financing (EDF or Budget); cooperation instrument (eg. ALA, TACIS); contract type (eg. Grant agreement, Works contract); and type of financial flow (eg. advance payment, recovery). Each element is given a risk weighting and the risk of each transaction is the combination of these risk weightings. So for example a transaction which is a clearance of prefinancing in a TACIS works contract may be deemed riskier than a transaction which is an advance payment of a budgetary aid agreement under an EDF Macro-economic support programme. Each transaction is studied with a view to detecting systemic problems and to detect and correct any financial anomalies which might lead to too much or too little being paid, recovered, or cleared. The main aspects of the control itself are eligibility (substantial and formal evidence of the respect of the contractual provisions), beneficiary and bank account, bank guarantees, and certain checks on the operation of the ex-ante control systems. For the year 2007, in a great improvement over 2006, more detailed reports on the control

9

activity by directorate have been taken into consideration. The rate of sampling was 1 % of transactions. The main conclusions of the report are:

• the level of anomalies detected by the ex post control is again extremely low: errors giving rise to an overpayment totalled only 11,146 euro which is a tiny fraction of the value of those transactions tested, which totalled 1,271 million euro

• the great majority of errors detected relate to procedural errors

189 Invites the Commission to further improve DG AIDCO's risk assessment by making reference to the findings of auditors at project level and by making a distinction according to the different types of implementing organisation and funding method;

Done in the context of AAR 2007 The annual Risk Self-assessment is carried out in the context of the Annual Management Plan and is a high level risk assessment which complements other and more detailed risk analyses, carried out for instance in the context of the establishment of the Annual Audit Plan. It focuses on residual risk taking account of the mechanisms already in place. The fact that the elements mentioned by the Court might not specifically refer to in the formulation of the risk (obviously synthetic) does not imply that these elements have not been taken into account during the exercise. Hence, this

AIDCO G2

DONE

10

recommendation is evaluated by the Commission as in place.

190 Invites DG AIDCO to improve the terms of reference of its external audits to cover all known risk areas, including the verification of compliance with the Commission's requirements regarding contracting procedures and the eligibility of expenditure;

New terms of reference for financial and systems audits have been introduced since July 2007. They include, in an explicit way, the verification of compliance with the Commission's requirements regarding the contracting procedure and the eligibility of expenditure.

In early 2006 the standard grant and fee-based service contracts have been revised. They now include standard terms of reference (ToR) for auditors to perform expenditure verifications to be submitted by the beneficiaries of Community funds prior to final payments. Furthermore, AIDCO adopted new standard ToR for financial and systems audits and for compliance assessments on 16.07.2007

AIDCO G2

DONE

191 Underlines that in the period 2000 to 2006, EU contributions to the UN have increased by 700% (from EUR 200 million in 2000 to EUR 1,4 billion in 2007); cannot understand the lack of follow up of funds transferred to international trust funds by the Commission;

The Commission believes that adequate control systems are in place to ensure that the money entrusted to the UN is wisely and properly used.

Firstly, a major analysis of UN partners has been carried out to verify that they meet the highest international standards in accounting, audit, internal control and procurement

Secondly, the Commission and the Court of Auditors have the right to carry out checks on those operations financed by the Community Budget – the so-called verification clause of the FAFA.

Considering the increasing level of funding being channelled through the UN, the number of controls has increased substantially from 6 in

• Common ToR are being developed for facilitating the conduct of verification missions;

• Standard ToR for verification missions are used by the Commission since 2006. These ToR are being discussed with the UN in order to adopt "Common ToR for verification missions";

• The compliance analysis of UN organisations' procedures with internationally accepted standards in terms of audit, accounting internal control and procurement (the "four pillars" exercise) has been performed for 11 UN Organisation, covering 97% of AIDCO

AIDCO G2 +

AIDCO G7

ON GOING

Status "on going" justified by the fact that common ToR UN verification mission are on process.

See also point 196.

11

2006 to more than 40 in 2007

Thirdly, the Commission has launched a global evaluation to assess to what extent Commission interventions through the UN system have been relevant, efficient and effective, and visible in supporting sustainable impact for the development of partner countries.

contributions to the FAFA family;

The Commission and the UN have signed joint guidelines on reporting to improve the reporting practises;

• The Commission has signed an action plan on visibility in 2006, followed by the approval of joint guidelines indicating how this should be implemented;

• The signature of the FAFA with the UN in 2003 and the use of the Standard Contribution Agreement since that year (updated pursuant to the modification of the Financial Regulation in May 2003) contains specific rules on verification, visibility, reporting, monitoring, eligibility of costs, limitation of the management fee to a maximum of 7%;

• Commission services take part, as much as possible, to the meetings of governing bodies.

• Where the Commission contributes predominantly to a Trust Fund it would expect to have an appropriate role in the

12

Technical and Steering Committees, where contributors participate.

192 In this context, expresses its concern at the lack of information necessary for the discharge authority to proceed to a meaningful discharge in respect of the funds implemented under the external action heading;

The Commission is aware that there is always room for improvement but considers that the systems currently in place provide reasonable assurance concerning the legality and regularity of external action expenditure as a whole.

AIDCO This is not a recommendation.

193 Insists that a harmonised information system should be developed in order to provide the discharge authority in particular, and the public in general, with a fully transparent database containing a full overview of projects financed with EU funds in the world, and the final recipients of these funds; is of the opinion that, preferably, the Common Relex Information System (CRIS) database should be enabled to deliver this kind of information;

The Commission is committed to making available to the Parliament in the first half of 2008 consolidated information on grants awarded during 2007 including inter alia: an identification of the name and nationality of the grant beneficiary, all implementing partners, the location of the action and other contributors of financing. The use of CRIS to generate this information is being examined.

Improve CRIS functionalities. AIDCO 01 Chef de File

+ AIDCO G5 associated

31/12/2008

194 Recalls that, under the Financial Regulation, the Commission should have been able since May 2007 to immediately identify the final beneficiaries and implementing actors of any project financed or co-financed with EU funds;

The Commission intends to fulfil the requirements of the Financial Regulation (FR) (under Art 30.3), applicable as from 01/05/07 for all operations related to external assistance and programmes starting after this date.

ON GOING

The instruction Note (D (2008) D/9337) was signed on 21.05.08. With this note all concerned services were requested to take the required measures to meet the legal requirements for all modes of implementation before end of June 2008. Consolidated information to the EP will be made available before 15 July 2008.

13

See also pt 21

195 Considers that the visibility, political guidance and possibility of control by the Commission of international trust funds (where the EU is a major donor) should be strengthened, without compromising the effectiveness of action in this field;

Addressed by Vice-President Siim Kallas in his letter of 17/3/08.

The Commission still intends to improve the traceability of EU funds that are channelled through the UN and other multilateral donor trust funds, as well as the available information on final beneficiaries of such projects.

The Joint Visibility Guidelines have been approved and adopted in the 5th FAFA working group meeting (10-11 April 2008)

AIDCO G8 +

Geographic Directorates

DONE

The World Bank will provide its comments on the Joint Visibility Guidelines by 6 June.

It was also suggested to organise on a yearly basis a meeting between EP and UN and WB managers of EU co funded MDTF. The Commission has proposed organising such a meeting with the members of COCOBU, AFET, DEVE and trust fund managers(dates tbc).

See also 210

196 Invites the Commission to present to it a plan to further increase EU ownership of external actions;

The choice of delivery channels is made on a case by case basis and the Commission cannot, and would not, always decide to undertake actions directly. This is the reason for the provision in the Financial Regulation for joint management and for more co-financing. The Commission has proposed ways of keeping Parliament better informed on a regular basis in future.

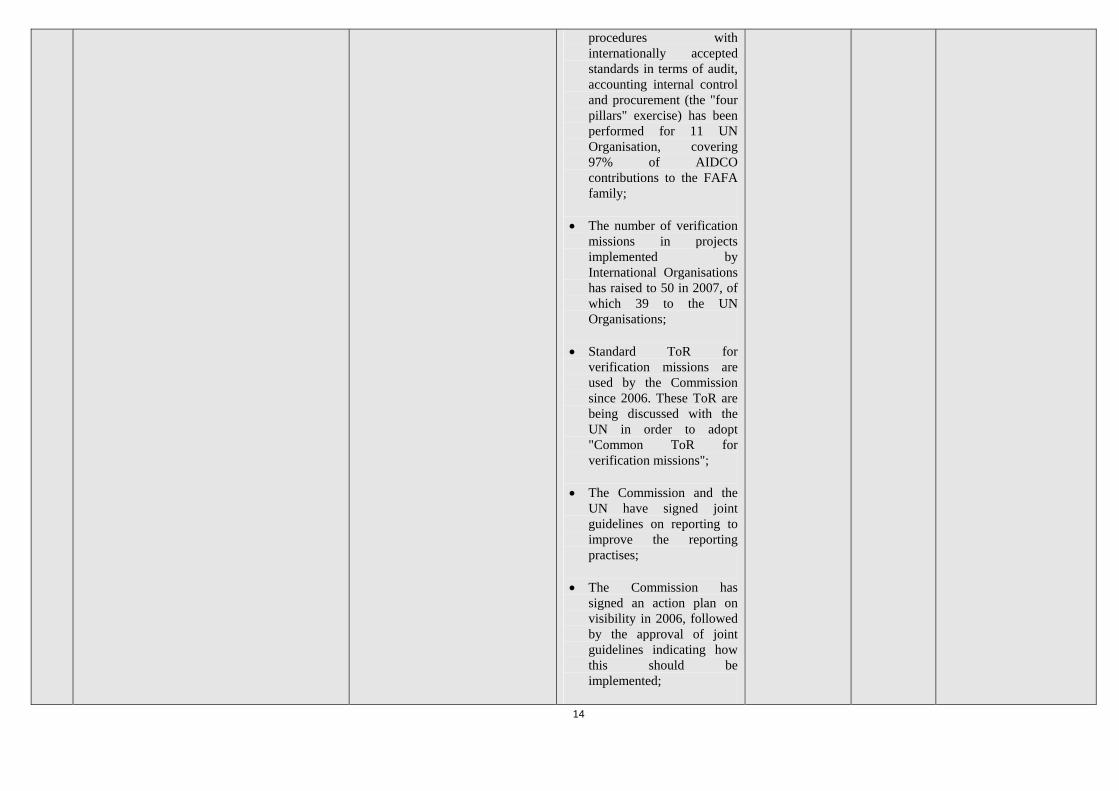

The European Commission has put in place over the last few years several actions that will increase EU ownership of external actions:

• ToR for expenditure verifications are mandatory since 2006 and cover 97% of the amount of the grants;

• Since October 2007, standard ToR for audits (financial and systems) are mandatory for all kind of projects financed by the external headings of the Budget and managed by AIDCO

• The compliance analysis of UN organisations'

AIDCO DONE The Action plan described under the item is part of the reporting to be transmitted by DG BUDG to the EP (see pt 83)

14

procedures with internationally accepted standards in terms of audit, accounting internal control and procurement (the "four pillars" exercise) has been performed for 11 UN Organisation, covering 97% of AIDCO contributions to the FAFA family;

• The number of verification missions in projects implemented by International Organisations has raised to 50 in 2007, of which 39 to the UN Organisations;

• Standard ToR for verification missions are used by the Commission since 2006. These ToR are being discussed with the UN in order to adopt "Common ToR for verification missions";

• The Commission and the UN have signed joint guidelines on reporting to improve the reporting practises;

• The Commission has signed an action plan on visibility in 2006, followed by the approval of joint guidelines indicating how this should be implemented;

15

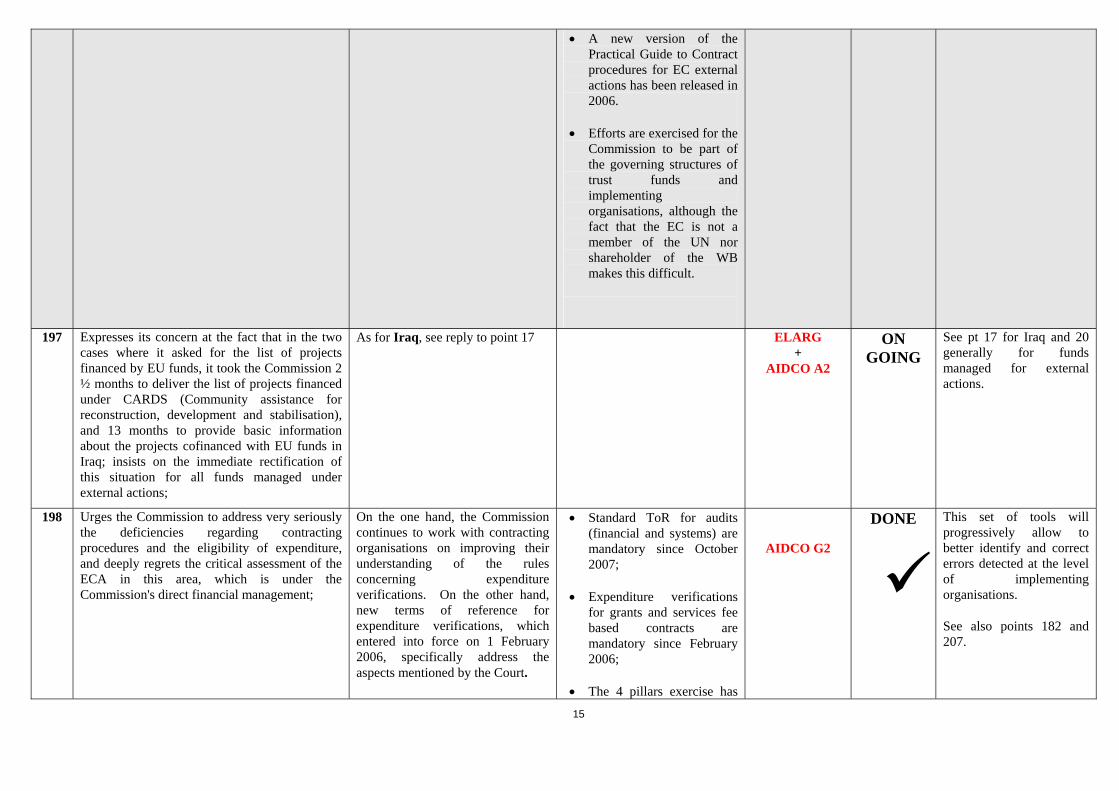

• A new version of the Practical Guide to Contract procedures for EC external actions has been released in 2006.

• Efforts are exercised for the Commission to be part of the governing structures of trust funds and implementing organisations, although the fact that the EC is not a member of the UN nor shareholder of the WB makes this difficult.

197 Expresses its concern at the fact that in the two cases where it asked for the list of projects financed by EU funds, it took the Commission 2 ½ months to deliver the list of projects financed under CARDS (Community assistance for reconstruction, development and stabilisation), and 13 months to provide basic information about the projects cofinanced with EU funds in Iraq; insists on the immediate rectification of this situation for all funds managed under external actions;

As for Iraq, see reply to point 17 ELARG +

AIDCO A2

ON GOING

See pt 17 for Iraq and 20 generally for funds managed for external actions.

198 Urges the Commission to address very seriously the deficiencies regarding contracting procedures and the eligibility of expenditure, and deeply regrets the critical assessment of the ECA in this area, which is under the Commission's direct financial management;

On the one hand, the Commission continues to work with contracting organisations on improving their understanding of the rules concerning expenditure verifications. On the other hand, new terms of reference for expenditure verifications, which entered into force on 1 February 2006, specifically address the aspects mentioned by the Court.

• Standard ToR for audits (financial and systems) are mandatory since October 2007;

• Expenditure verifications for grants and services fee based contracts are mandatory since February 2006;

• The 4 pillars exercise has

AIDCO G2

DONE This set of tools will progressively allow to better identify and correct errors detected at the level of implementing organisations.

See also points 182 and 207.

16

been completed for the WB and more than 97% of the UN family;

• Organisations entitled to manage projects under indirect centralised management have been submitted to the previous assessment;

• Standard ToR for program estimates will be finalised before the entry into force of the 10th EDF

199 Agrees with the ECA that the Commission should include information on all audits of projects in the CRIS and should better link this information to project management information; also asks the Commission's EuropeAid headquarters to review the financial information provided by delegations in order to ensure its completeness and consistency;

Further improvements have been introduced in CRIS-Audit since 1 January 2008 addressing the aspects mentioned by the Court.

In line with its commitment to further improve its operation, the functionalities of CRIS-Audit have also been reviewed, building on the experience gathered and taking into account the requirements of the new audit module within the Commission's central accounting system (ABAC-Audit). The new CRIS-Audit came into operation in late 2007 and its use became mandatory from 1st January 2008.The entire Annual Audit Plan 2008 has been centrally encoded in CRIS-Audit. Furthermore, the Annual Synthesis Report 2007, issued in February 2008, is a review of the audit reports received in 2007 by Headquarters and Delegations, and aims at giving AIDCO Headquarters an overview of the main audit findings related to its activities.

AIDCO G2

DONE

17

200 Invites the Commission to improve transparency and access to documentation relating to projects managed by UN agencies, and to continue to develop clear guidelines and procedures within FAFA, setting out the framework for managing the financial contributions made by the Commission to the UN;

Addressed by Vice-President Siim Kallas in his letter of 17/3/08.

The Commission still intends to improve the traceability of EU funds that are channelled through the UN and other multilateral donor trust funds, as well as the available information on final beneficiaries of such projects.

• The FAFA and the model of contribution-specific agreement signed with UN (and other international organisations) declare that all EC institutions are entitled to on-spot checks (verifications). Since May 2007, the specific-contribution agreement further explicitly mentions the Court of Auditors. The Commission draws the attention of the UN agencies on a regular basis on the concerns of the Court of Auditors to have access to the documentation they need.

• ToR for verification into projects managed by international organisations are being developed

AIDCO G2 +

AIDCO G8

01/07/2008

201 Invites the Commission to report to it on controls undertaken under FAFA;

The Commission will present on an annual basis the list of controls on actions undertaken under the FAFA agreement, as well as a synthesis of the main conclusions.

The reporting on controls undertaken under FAFA is foreseen in the context of the AAR

AIDCO G2

DONE

18

206 Is pleased with the ECA's assessment that several remedial measures were introduced by the Commission in the follow-up to the ECA's special report on twinning from 2003; invites the Commission to motivate beneficiary governments more strongly to make use of the outputs of projects carried out in the context of their reform efforts; supports the ECA's recommendation to the Commission that the Commission reduce the level of detail of the twinning contracts in order to allow greater flexibility of project management;

The Commission will continue to ensure that the beneficiary administrations ensure the sustainability of twinning project results. If that condition is not met, the Commission can interrupt the implementation of the project. Moreover, the Commission is committed to further streamline the rules governing budgetary modifications so as to increase clarity and simplicity in the management of twinning projects.

ELARG +

AIDCO A6

31/12/08 To be discussed between DG Elarg and DG Aidco in consultation with MS

207 Notes the ECA's findings as to the legality and regularity of transactions in the field of external actions and of the related supervisory and control systems; invites the Commission to undertake all necessary system improvements so as to ensure that irregularities identified at the level of project-implementing organisations in third countries are removed;

The Commission has accepted all recommendations made by the Court in the field of external actions in the context of the Annual Report, and important improvements have already been introduced in order to improve the quality of audits, the operationalities provided by CRIS –Audit and the use of information provided by the delegations.

• Standard ToR for audits (financial and systems) are mandatory since October 2007;

• Expenditure verifications for grants and services fee based contracts are mandatory since February 2006;

• The 4 pillars exercise has been completed for the WB and more than 97% of the UN family;

• Organisations entitled to manage projects under indirect centralised management have been submitted to the previous assessment;

• Standard ToR for program estimates will be finalised before the entry into force of the 10th EDF

AIDCO G2

DONE This set of tools will progressively allow to better identify and correct errors detected at the level of implementing organisations.

See point 182.

19

208 Invites the Commission to present to it a report on what exactly has been done to alleviate the situation of Iraqi refugees and displaced persons;

The Commission can provide such a report before autumn 2008.

Report drafting

AIDCO A2

01/09/08

X 31/12/2008 would be more appropriate. EC would have more information on its 10 million € contribution to IRFFI Cluster F which was committed late 2006.

209 Emphasises its interest regarding assistance provided to Afghanistan, and invites the Commission to present to it a report on the state of play of the implementation of EU funds in Afghanistan, and to comment on the expulsion from that country of the acting EU representative on a charge of having communicated with the Afghan Taliban;

The Commission continues to report regularly to the Parliament on the implementation of funds for Afghanistan.

NO, for the second part. The question on the expulsion of the acting EU representative should be addressed to the Council

State of play and dedicated website is been developed on the same line as for Iraq

AIDCO D1

01/07/08 State of Play and website under preparation.

210 Expects to receive annual reports on budget implementation contracts, an annual list of projects and their location and lists of final beneficiaries; considers that its rapporteur for the discharge should have access to information declared confidential for security reasons; welcomes the Commission's commitment to re-negotiate relevant agreements on trust funds with the UN in order to achieve joint reporting guidelines and disclosure of final beneficiaries; welcomes the Commission's commitment to organise annual meetings between Parliament and senior UN staff responsible for the management of multi-donor trust funds, and is of the opinion that this would provide a framework for the provision by the UN of additional information regarding EU funds;

Addressed by Vice-President Siim Kallas in his letter of 17/3/08.

The Commission intends to fulfil the requirements of the Financial Regulation (FR) (under Art 30.3), applicable as from 01/05/07 for all operations related to external assistance and programmes starting after this date.

If publication is not possible (for personal data protection and security reasons), the information will be made available on request for the EP Members, under the usual rules of confidentiality agreed between the two Institutions.

The Commission still intends to improve the traceability of EU funds that are channelled through

See 21 and 195 AIDCO F4 +

AIDCO 04 +

AIDCO G8

Link with 21 and 195

20

the UN and other multilateral donor trust funds, as well as the available information on final beneficiaries of such projects

215 Notes with satisfaction that, according to the ECA Special Report No 5/2006 concerning the MEDA programme, "the Commission’s management of the MEDA programme has clearly improved since the early years and can be considered as satisfactory";

This is not a recommendation.

216 Notes furthermore, as concluded by the ECA, that, as a result of devolution, Commission delegations have played an important role in the implementation of the programme by helping partner countries to deal with the procedural aspects of procurement;

This is not a recommendation.

217 Asks the Commission to regularly inform it of the carrying out of on-the-spot checks and inspections, identifying notable cases of suspected fraud or other financial irregularities during the last year of implementation of the MEDA programme;

EuropeAid has created a system for audits of external operations that provides assurance on the basis of a two-layer approach: Mandatory audits (audits that are required by financing agreements and external aid contracts) and Audits planned and managed by Headquarters and Delegations, which provide a second layer of assurance that is complementary to the previous one.

The Annual Audit Plan constitutes the basis for launching comprehensive audits managed by Headquarters and Delegations. The term audit is to be intended in its wider meaning that is full-scale audits, direct controls/on-the-spot checks, verifications of international organisations each of one provides a different level of assurance.

Further to the execution of its audit

OLAF DONE Commission Inform regularly the EP and Cocobu on all fraud cases

21

plans and other control activities EuropeAid/Directorate A has since 2002 identified and transmitted to OLAF about 30 MEDA programme-related cases of suspected irregularities / fraud as defined by the Council Regulation (EC, Euratom) n° 2988/95 of 18 December 1995 on the protection of the European Communities financial interests and the EU Convention of 26 July 1995 on the protection of the financial interests of the European Communities. As of the end December 2007, about 1/3 of these cases are still under assessment/investigation.

The Commission informs Parliament regularly of all cases of suspected irregularities and fraud transmitted to OLAF.

218 Looks forward to an increase in the visibility of actions financed by the EU via international trust funds, in particular in the context of the sums totalling more than EUR 1 billion which have been transferred from the EU budget to UN and World Bank funds; urges the Commission to ensure that political guidance, visibility and control of the funds are improved;

The Joint Visibility Guidelines have been approved and adopted in the 5th FAFA working group meeting (10-11 April 2008)

See point 196

AIDCO G8

DONE The World Bank will provide its comments on the Joint Visibility Guidelines by 6 June.

219 Invites the Commission regularly to present to it specific measures to further increase EU ownership of its external actions in their geographical contexts, in accordance with the principles of efficiency, accountability and visibility;

See point 196 AIDCO ON GOING

The action Plan described under pt 196 will be updated if necessary.

220 Calls on the Commission to inform it efficiently and rapidly about the use of EU funds via international trust funds in Iraq; invites the

As for Iraq see pt 17.

As for others MDTF see also

AIDCO ON GOING

Covered under other points 20 – 195 - 210

22

Commission to update and give substance to this information, and to propose a system which enables Parliament to see in a clear and readable way what exactly has been co-financed by EU funds via international trust funds anywhere in the world;

20, 195 and 210

221 Welcomes the significant increase in the implementation rate of commitment and payment appropriations for pre-accession strategy in 2006, as compared to 2005;

This is not a recommendation.

223 Draws attention to the benchmark, agreed by the Commission, of 20% of funding under the Development Cooperation Instrument being allocated to basic and secondary education and basic health; looks forward to receiving details of the implementation of this benchmark in 2007;

RELEX DEV

AIDCO

DONE The Commission has already included in its 2008 Annual Report on EC External Assistance the follow-up of this benchmark: figures with the relevant detail of sector allocation in 2007 of the DCI country programs are provided in a table. The Commission has concluded the following as stated in the report

Aid directly targeting the basic health and education sectors (1) reached some 17% (2) of total commitments under the relevant DCI geographical programmes (Asia, Latin America and South Africa), even without including general budget support with conditionality linked to these sectors. The

23

Commission is thus well on track to reach, by 2009, the 20% goal agreed with the adoption of the DCI regulation for assistance to these sectors under the DCI country programmes.

224 Welcomes the Commission's initiative to develop a structured approach to support supreme audit institutions in countries receiving budget support; notes however that democratic accountability at the level of partner countries cannot be achieved without strengthening parliamentary budget control bodies, as required by Article 25(1)(b) of Regulation (EC) No 1905/2006 of the European Parliament and of the Council of 18 December 2006 establishing a financing instrument for development cooperation.

Addressed in the replies sent on 18/2/2008 by Commissioners Ferrero-Waldner and Michel to DEVE committee.

AIDCO E1

ON GOING

Actions à poursuivre:

- contacts avec autres bdf en particulier BM, FMI et BAD

- contacts avec INTOSAI

- actualisation "mapping" des activités d'appui aux SAI, Parlements, Institution de contrôle des fonds publics

225 Notes that in 2006, 91% of budget support from the Community budget was delivered in the form of sector budget support, which is better targeted than general budget support and therefore leads to lower risks; questions the Commission's "dynamic interpretation" of the eligibility criteria for budget support, which, according to the ECA, increases risk; believes that budget support should only be undertaken in countries that already meet a minimum standard of credible management of public finances;

The ECA did not express doubts about the 'Commission's 'dynamic interpretation' but stated that in view of its 'dynamic interpretation' the Commission was not able to demonstrate in the case of Budget support (BS) disbursements to Sierra Leone that it has complied with the provisions of the Cotonou Agreement. In its answer the Commission demonstrated that the respective disbursements were carried out in full respect with the relevant provisions of the Cotonou Agreement and in line with its 'dynamic approach'

La Commission applique cette recommendation de manière permanente et régulière dans la cadre de l'activité de contrôle de qualité et du contrôle des dossiers de décaissements.

AIDCO E1

DONE Il n'existe pas au niveau international de minimum standard.

La Commission a pris des dispositions pour

- effectuer les diagnostics en matière de GFP

- suivre la mise en œuvre des programmes de réforme de GFP (et le cas échéant les appuyer)

- formaliser et structurer mieux ses décisions en

24

matière d'éligibilité (critère PFM) et de décaissement

226 Invites the Commission to improve transparency and access to documentation relating to budget support actions, particularly by establishing agreements with beneficiary countries analogous to FAFA and setting out a framework for managing the financial contributions made by the Commission to the UN;

The Commission agrees that as external aid granted through BS become part of the national budget, any follow-up by EC institutions is undertaken in accordance with the mandate of the authorities of the partner countries which are responsible for the supervision, control and auditing of public funds. It is therefore indeed important for the Commission to cooperate with the respective national authorities

AIDCO E1

ON GOING

Commission and Delegations

La Commission prend des initiatives pour utiliser les rapports des Cdc, Commissions Parlementaires, Institutions de Contrôle externe et de contrôle des fonds publics (lutte anti-fraude)

- favoriser et développer les appuis aux institutions de Contrôle

- Développer les arrangements administratifs pour la lutte contre la fraude

227 Congratulates the Commission on reducing the level of reste à liquider (RAL) dating from commitments made by EuropeAid before 2001 by 39% in 2006; requests that it receive regular updates of changes in levels of normal and abnormal RAL;

Addressed in the replies sent on 18/2/2008 by Commissioners Ferrero-Waldner and Michel to DEVE committee.

Send regular updates of changes in levels of normal and abnormal RAL to the EP

AIDCO G1

31/12/2008

228 Notes the criticisms of Commission Technical Assistance projects made by the ECA in its Special Report No 6/2007; notes further that the Commission will address these questions in its Strategy to meet EU aid effectiveness targets on Technical Cooperation and Project Implementation Units, due by June 2008; looks forward to receiving, in due course, an assessment of the results of the implementation of this strategy;

Cf Action Plan of the Commission Technical Assistance ECA report

AIDCO E5 Chef de File

+ AIDCO 01

ON GOING

June 2008 and

following months

The preparation of the strategy is on track. The strategy will include a monitoring system which will provide regular feedback on the results of its implementation. The work plan attached to the strategy will include regular internal reviews. In 2009 an external evaluation on Technical

25

Assistance will be launched within the annual evaluation programme.

229 Welcomes the measures implemented by the Commission to promote donor coordination in the area of Technical Assistance; emphasises the importance of a coordinated approach, not only at EU level but among all donors, and looks forward to receiving details of the progress of this initiative;

Addressed in the replies sent on 18/2/2008 by Commissioners Ferrero-Waldner and Michel to DEVE committee.

Cf Action Plan of the Commission Technical Assistance ECA report

AIDCO E5 +

AIDCO 01

ON GOING

June 2008 and

following months

The work plan to be attached to the strategy will include measures to support dialogue and coordination on Technical Cooperation at various level n (HQ, Country level, programme level). Members States have been invited to comment the draft strategy and the workplan, particular attention will be given on concrete actions enhancing joint work in this area. The strategy it self and the Guidelines who will complete it represent concrete working tools to support coordinated approach among donors and will be broadly shared through the donor community.

![Le cadre de suivi et d’évaluation relatif à la politique ... · ® Le règlement horizontal [règlement (UE) n° 1306/2013, article 110], établit un cadre commun de suivi et](https://static.fdocuments.in/doc/165x107/60725fc5b5216900ee6b2ce1/le-cadre-de-suivi-et-davaluation-relatif-la-politique-le-rglement.jpg)