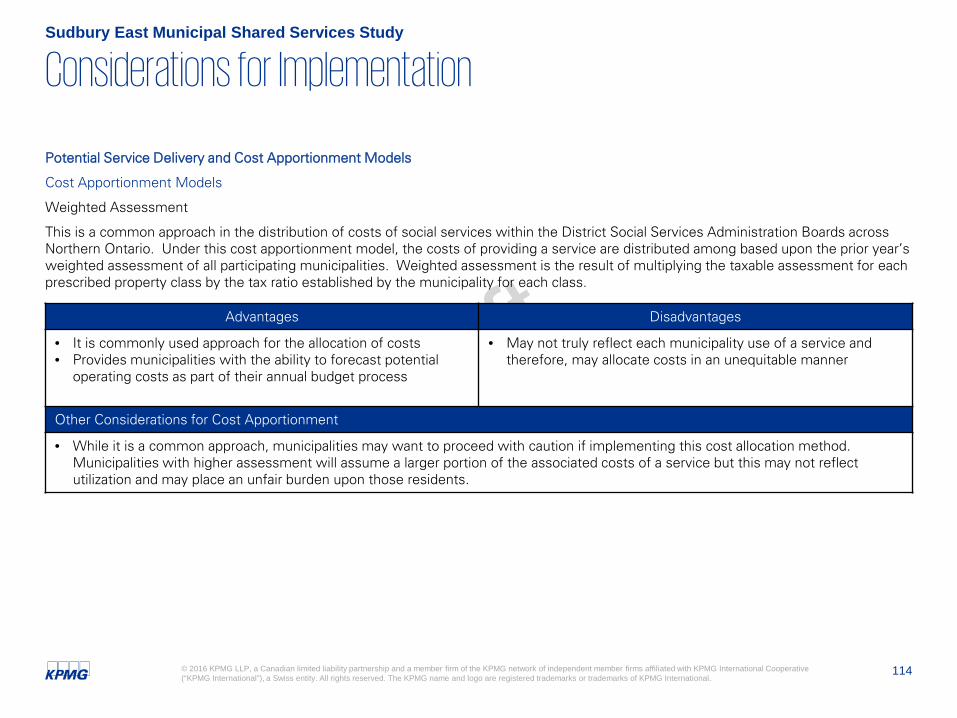

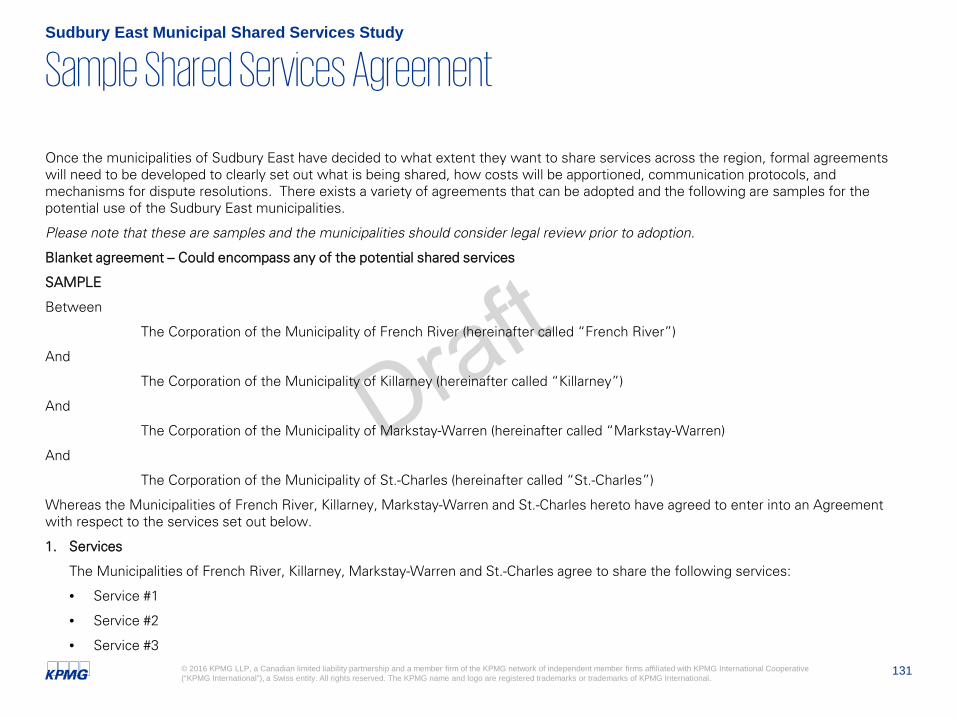

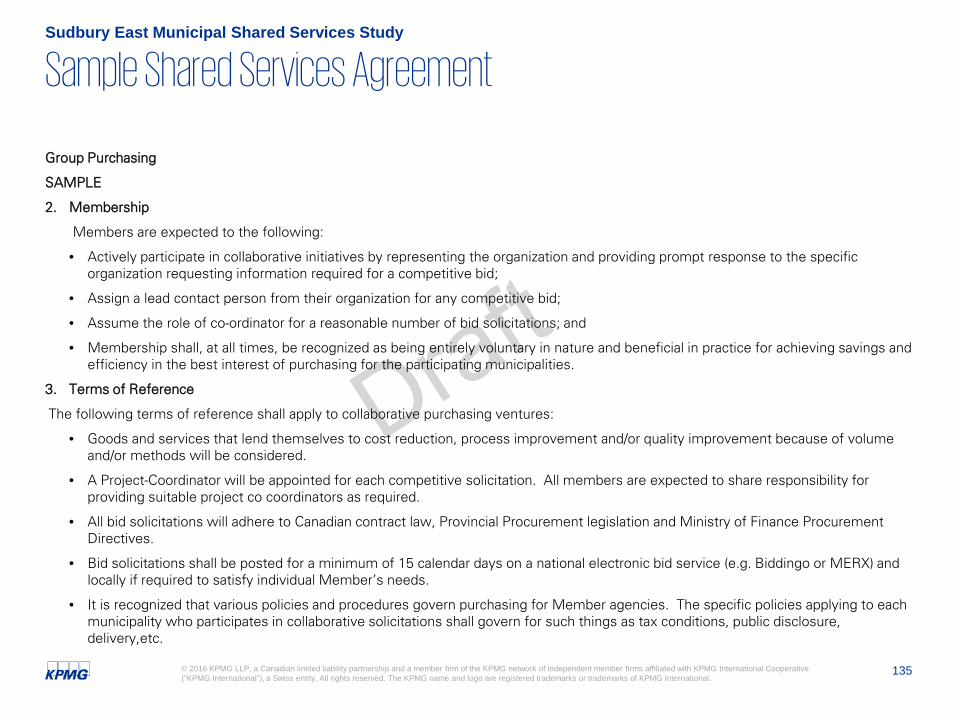

Sudbury East Municipal Shared Services Study · With a geographic area that would rival the City of...

146

Sudbury East Municipal Shared Services Study Draft Report – Third Revised Version February 17, 2017

Transcript of Sudbury East Municipal Shared Services Study · With a geographic area that would rival the City of...

Sudbury East

Municipal Shared

Services Study

Draft Report – Third

Revised Version

February 17, 2017

Mr. Denis TurcotChief Administrative Officer/ClerkCorporation of the Municipality of Markstay-WarrenPO Box 7921 Main Street South Markstay ON P0M 2G0

January 10, 2017

Dear Mr. Turcot

Shared Municipal Services Study

We are pleased to provide our report concerning KPMG’s study of potential opportunities for the sharing of municipal services in the Sudbury East region. Our study was undertaken based on the terms of reference outlined in our engagement letter with the Municipality dated September 1, 2016.

The purpose of the study was to assist the municipalities in the Sudbury East area with a review of the municipalities’ operations with the intention of identifying potential opportunities for the four municipalities in Sudbury East to share and increase the efficiency and effectiveness of those services with an additional expectation to reduce operating costs.

We trust our report is satisfactory for your purposes and appreciate the opportunity to be of service to the Municipalities of Markstay-Warren, French River, Killarney and St.-Charles. Please feel free to contact the undersigned at your convenience should you wish to discuss any aspect of our report.

Yours truly,

(signature pending finalization of report)

Per Chas Anselmo, Senior Manager705.669.2549 | [email protected]

3© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

ContentsSudbury East Municipal Shared Service Study

Page

Executive Summary 4

Study Overview 10

Municipal Profile 16

Shared Services in Ontario 35

Potential Shared Service Opportunities 42

Considerations for Implementation 108

Concluding Comments 119

Appendix A – Critical Path for Implementation 122

Appendix B – Sample Shared Service Agreements 130

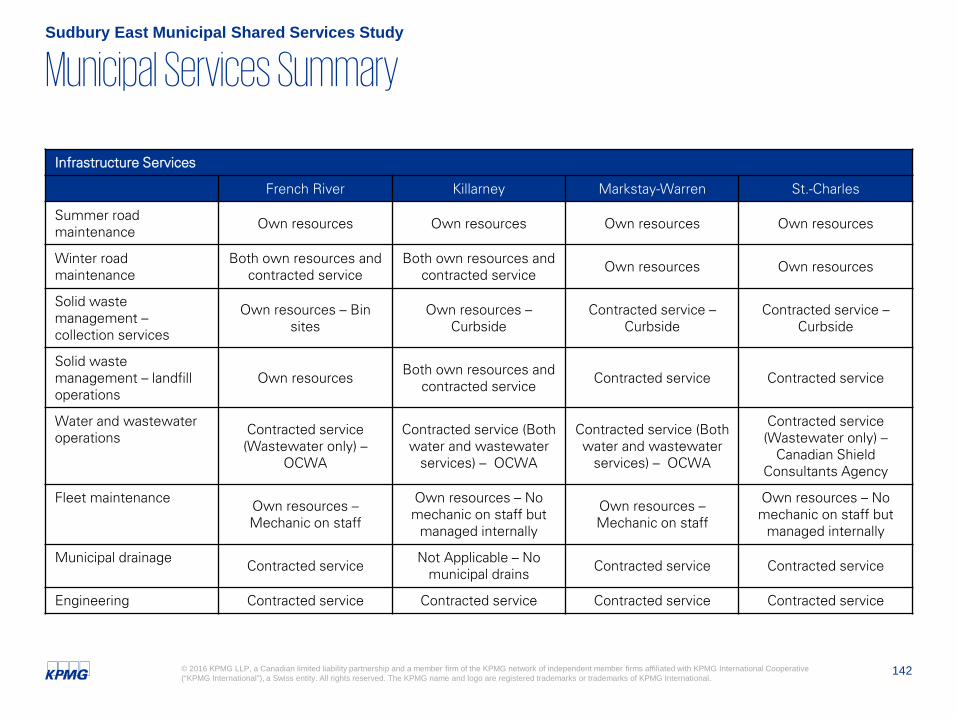

Appendix C – Municipal Services Summary 139

Sudbury East

Municipal Shared

Services Study

Executive Summary

5© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Executive Summary

KPMG was retained by the Municipality of Markstay-Warren on behalf of the municipalities of Sudbury East to provide the municipalities of Sudbury East with an objective evaluation of the operations, staffing and equipment level and service offerings currently provided by each municipality, with the view of identifying potential opportunities to share services intended to increase operating effectiveness and efficiencies while reducing operating costs.

The shared services study explored all aspects of each municipality’s operations with each service given consideration for its potential suitability for sharing among the four municipalities of Sudbury East. With a geographic area that would rival the City of Greater Sudbury as the largest municipality in Ontario, geographic barriers exist for the purposes of sharing services.

Regardless, there are factors that should encourage the municipalities of Sudbury East to pursue the opportunities contained within the report which include:

• Shared service arrangement have proven successful elsewhere, with 368 of Ontario’s 444 indicating that they participate in some form of shared service arrangement.

• All of the municipalities in the region are facing financial challenges with operating grant levels either declining or remaining constant while operating expenditures are continue to increase on an annual basis which is then resulting in a greater reliance on municipal taxation as each municipality’s main revenue source. This financial pressure is placing a greater emphasis on the realization of operating efficiencies and effectiveness.

• With the formal adoption of asset management plans and a heightened emphasis on managing capital, municipalities are seeking outways to address their respective infrastructure needs and any cost savings identified and realized have the potential of being re-invested in an attempt to begin to address this challenge.

At the beginning of the study, the membership of the Sudbury East Municipal Association (‘SEMA’) was asked what was ‘on the table.’ At that time, all matters of a municipal nature were to be explore with one exception. The membership of SEMA did not appear to support the rationalization of recreational facilities.

The shared services study initially identified several broad areas of municipal service delivery where there was the potential for shared services intended to achieve additional efficiencies and economies of scale within the region and potentially reduce operating costs. Ultimately, seven opportunities were identified for potential implementation and following additional analysis, including discussions with municipal staff, other opportunities previously identified/discussed were dropped with an explanation as to why they were not pursued.

Sudbury East Shared Services Study

6© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Executive Summary

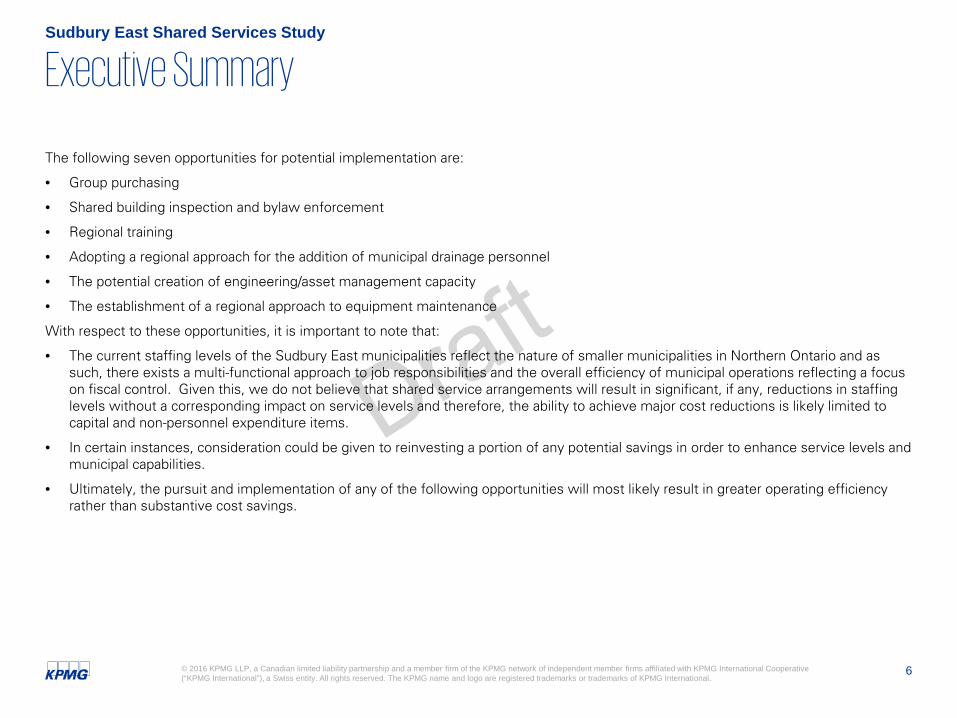

The following seven opportunities for potential implementation are:

• Group purchasing

• Shared building inspection and bylaw enforcement

• Regional training

• Adopting a regional approach for the addition of municipal drainage personnel

• The potential creation of engineering/asset management capacity

• The establishment of a regional approach to equipment maintenance

With respect to these opportunities, it is important to note that:

• The current staffing levels of the Sudbury East municipalities reflect the nature of smaller municipalities in Northern Ontario and as such, there exists a multi-functional approach to job responsibilities and the overall efficiency of municipal operations reflecting a focus on fiscal control. Given this, we do not believe that shared service arrangements will result in significant, if any, reductions in staffing levels without a corresponding impact on service levels and therefore, the ability to achieve major cost reductions is likely limited to capital and non-personnel expenditure items.

• In certain instances, consideration could be given to reinvesting a portion of any potential savings in order to enhance service levels and municipal capabilities.

• Ultimately, the pursuit and implementation of any of the following opportunities will most likely result in greater operating efficiency rather than substantive cost savings.

Sudbury East Shared Services Study

7© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Prioritization of Opportunities We have provided below a suggested implementation framework for consideration by the Sudbury East municipalities.

Sudbury East Municipal Shared Services Study

Short(<1 Year)

Medium(1 to 2 Year)

Long(2+ Years)

Timeframe

Prio

rity

Low

Med

High 2

Group Purchasing

Regional Training

4

1

Regional Equipment Maintenance

7

Regional Building Controls and Bylaw Enforcement

3

Municipal Drainage

6

Regional Asset Management and Engineering

5

8© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Executive Summary

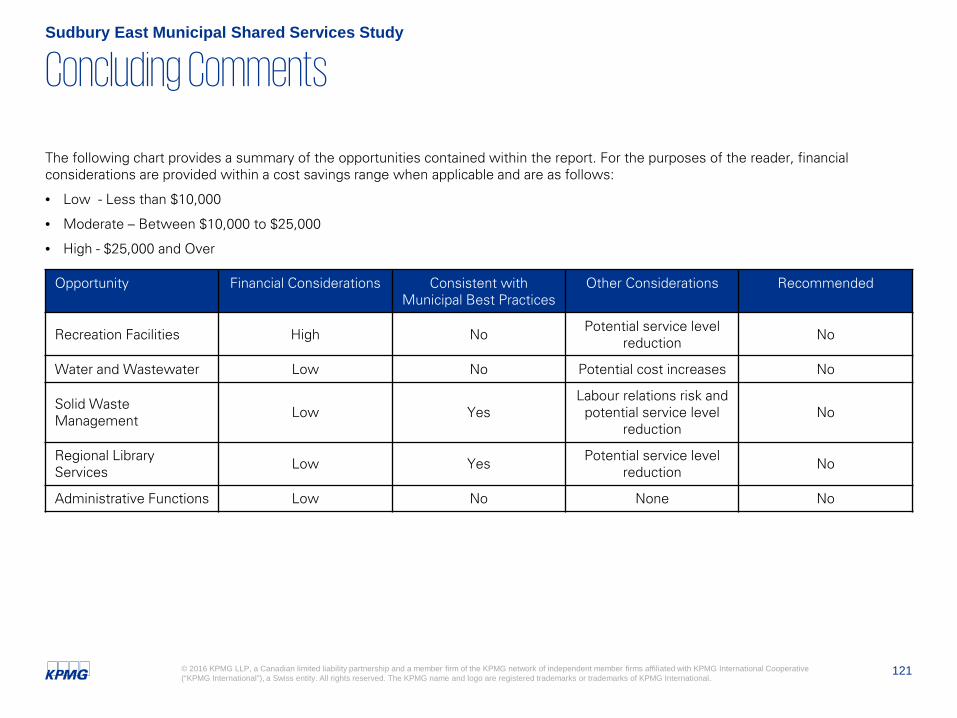

The following chart provides a summary of the opportunities contained within the report. For the purposes of the reader, financial considerations are provided within a cost savings range when applicable and are as follows:

• Low - Less than $10,000

• Moderate – Between $10,000 to $25,000

• High - $25,000 and Over

Sudbury East Municipal Shared Services Study

Opportunity Financial Considerations Consistent with Municipal Best Practices

Other Considerations Recommended

Group Purchasing High Yes None Yes

Building Controls High Yes None Yes

Bylaw Enforcement Low Yes Service enhancement Yes

Regional Training Low Yes Capacity building Yes

Regional Asset Management/Engineering

Low No Service enhancement Yes

Regional Equipment Maintenance Moderate No Capacity building Yes

Municipal Drainage Low Yes Capacity building Yes

Regional Economic Development Low Yes Service enhancement No

Regional Fire Services Low Yes Potential cost increases No

Sharing of Senior Administration Low No Potential cost increases No

9© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Executive Summary

The following chart provides a summary of the opportunities contained within the report. For the purposes of the reader, financial considerations are provided within a cost savings range when applicable and are as follows:

• Low - Less than $10,000

• Moderate – Between $10,000 to $25,000

• High - $25,000 and Over

Sudbury East Municipal Shared Services Study

Opportunity Financial Considerations Consistent with Municipal Best Practices

Other Considerations Recommended

Recreation Facilities High No Potential service level reduction No

Water and Wastewater Low No Potential cost increases No

Solid Waste Management Low Yes

Labour relations risk and potential service level

reductionNo

Regional Library Services Low Yes Potential service level

reduction No

Administrative Functions Low No None No

Sudbury East

Municipal Shared

Services Study

Study Overview

11© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Study Overview

A. Terms of Reference

The terms of reference for our engagement were established in KPMG’s engagement letter dated September 1, 2016 and consistent with KPMG’s proposal document dated July 15, 2016, the intention of our review was to provide the municipalities of Sudbury East with an objective evaluation of the operations, staffing and equipment level and service offerings currently provided by each municipality, with the view of identifying potential opportunities to share services intended to increase operating effectiveness and efficiencies while reducing operating costs. Specific outcomes outlined within the engagement letter included:

• Assisting the Municipality and the member municipalities of the Sudbury East Municipal Association (‘SEMA’) with the establishment of a methodology for the municipal shared services study;

• In conjunction with each municipality’s staff, undertaking of analysis of services, internal processes, service and equipment levels, and associated costs and funding; and

• Summarizing the results of our analysis and presenting potential opportunities in the form of business cases to the Municipality and the member municipalities of SEMA.

B. Methodology

Project Initiation

• An initial meeting was held with the Chief Administrative Officer/Clerk (the ‘CAO’) to confirm the terms of the study including the objectives, deliverables, methodology and timeframes.

• The Municipality assisted in the creation and establishment of a committee comprised of senior management to liaison with KPMG for the purposes of the study. The committee was comprised of the Chief Administrative Officers for the four municipalities as well as representation from the Province of Ontario’s Ministry of Municipal Affairs.

• A presentation was provided to SEMA on September 15, 2016 to explain the process to all of the member municipalities and discussany areas of interest and address questions regarding the study.

Sudbury East Municipal Shared Services Study

12© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Study Overview

B. Methodology

Current State Assessment

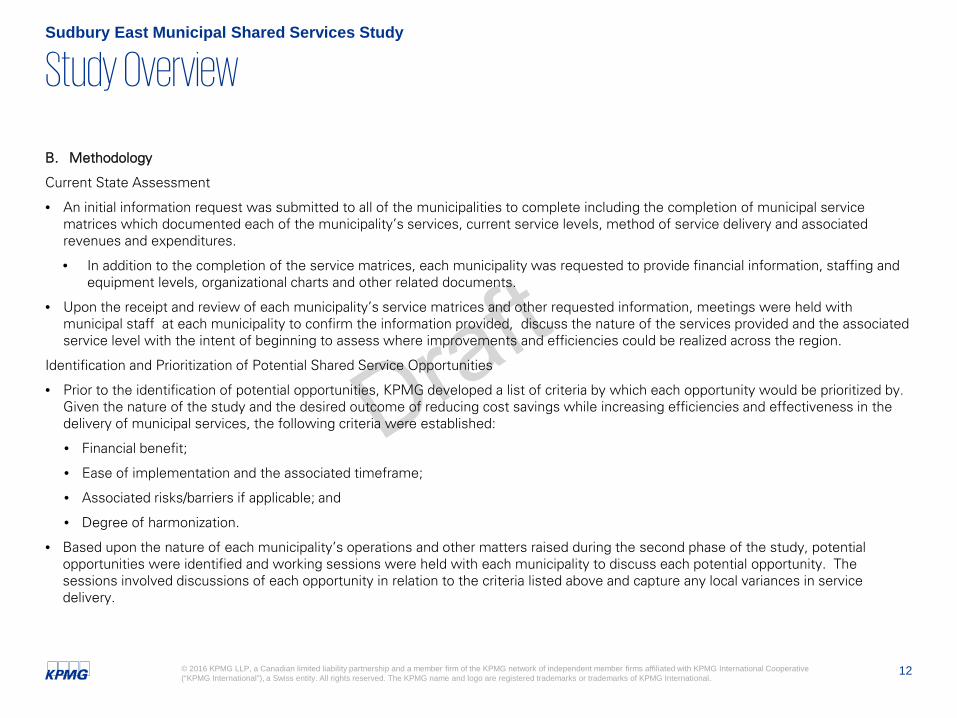

• An initial information request was submitted to all of the municipalities to complete including the completion of municipal service matrices which documented each of the municipality’s services, current service levels, method of service delivery and associatedrevenues and expenditures.

• In addition to the completion of the service matrices, each municipality was requested to provide financial information, staffing and equipment levels, organizational charts and other related documents.

• Upon the receipt and review of each municipality’s service matrices and other requested information, meetings were held with municipal staff at each municipality to confirm the information provided, discuss the nature of the services provided and the associated service level with the intent of beginning to assess where improvements and efficiencies could be realized across the region.

Identification and Prioritization of Potential Shared Service Opportunities

• Prior to the identification of potential opportunities, KPMG developed a list of criteria by which each opportunity would be prioritized by. Given the nature of the study and the desired outcome of reducing cost savings while increasing efficiencies and effectiveness in the delivery of municipal services, the following criteria were established:

• Financial benefit;

• Ease of implementation and the associated timeframe;

• Associated risks/barriers if applicable; and

• Degree of harmonization.

• Based upon the nature of each municipality’s operations and other matters raised during the second phase of the study, potentialopportunities were identified and working sessions were held with each municipality to discuss each potential opportunity. The sessions involved discussions of each opportunity in relation to the criteria listed above and capture any local variances in service delivery.

Sudbury East Municipal Shared Services Study

13© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Study Overview

B. Methodology

Business Case Development

• After the completion of the fourth phase of the study, an additional information request was sent to each municipality to assist in the further development of opportunities into more detailed business cases for the consideration of the four municipalities.

• For each business case, the following factors were explored:

• Changes to operating costs including potential cost reductions to each municipality where applicable and one-time implementationcosts;

• Identification of any infrastructure needs for the pursuit of the opportunity and the potential associated costs for each;

• Potential impact on staffing and service levels across the region; and

• Other considerations on the sharing of costs.

• To assist the municipalities, a potential critical path as well as matters pertaining to implementation were developed to assist the municipalities in the development of implementation plans.

• Potential governance and cost apportionment models were developed to assist in how each opportunity could potentially be managed if the Sudbury East municipalities pursued them.

• For those opportunities that did not meet the criteria established, the rationale as to why they did not result in a full business case was provided in the event that if conditions should change, the municipalities could potentially revisit these.

• Sample shared service agreements were developed (where applicable) to assist in the potential implementation of the opportunities.

Communication

• Throughout the study process, KPMG and the study’s working committee scheduled and participated in bi-weekly teleconference calls to discuss the progress of the study

• An interim presentation was provided to SEMA on October 27th to update the participating municipalities on the process with a preliminary list of potential opportunities as well as KPMG’s perspectives on municipal shared services.

Sudbury East Municipal Shared Services Study

14© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Study Overview

B. Methodology

Communication

• A presentation of the draft report was provided to SEMA on January 24th to review the opportunities developed as part of the study

• Following the delivery of the draft report, public consultation sessions were held in each community to share with the region’s residents and receive feedback about the potential to share services

• Upon the completion of the public consultations, the results of the consultations were incorporated into the report

• The presentation of the final report was provided to SEMA on xxxx.

Sudbury East Municipal Shared Services Study

15© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Study Overview

Restrictions

This report is based on information and documentation that was made available to KPMG at the date of this report. KPMG has not audited nor otherwise attempted to independently verify the information provided unless otherwise indicated. Should additional information be provided to KPMG after the issuance of this report, KPMG reserves the right (but will be under no obligation) to review this information and adjust its comments accordingly.

Pursuant to the terms of our engagement, it is understood and agreed that all decisions in connection with the implementation of advice and recommendations as provided by KPMG during the course of this engagement shall be the responsibility of, and made by, theMunicipality of Markstay-Warren and the member municipalities of SEMA. KPMG has not and will not perform management functions or make management decisions for the Municipality of Markstay-Warren and the member municipalities of SEMA.

This report includes or makes reference to future oriented financial information. Readers are cautioned that since these financial projections are based on assumptions regarding future events, actual results will vary from the information presented even if the hypotheses occur, and the variations may be material.

Comments in this report are not intended, nor should they be interpreted, to be legal advice or opinion.

KPMG has no present or contemplated interest in the Municipality of Markstay-Warren and the member municipalities of SEMA nor are we an insider or associate of the Municipality of Markstay-Warren or its management team nor of the other member municipalities of SEMA and their respective management teams. Our fees for this engagement are not contingent upon our findings or any other event. Accordingly, we believe we are independent of the Municipality of Markstay-Warren and the member municipalities of SEMA and are acting objectively

Sudbury East Municipal Shared Services Study

Sudbury East

Municipal Shared

Services Study

Municipal Profile

17© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Population and Households

Located outside of the City of Greater Sudbury and within the territorial Sudbury District, the four municipalities of the Sudbury East area have a combined population of just under 6,600 residents, 5,781 households and over 3,200 square kilometres. The geographic area covered by the four municipalities is just slightly smaller than the City of Greater Sudbury and as a result, these four municipalities’ collective geographic size would place them as the second largest single tier municipality in the Province of Ontario.

Sudbury East Municipal Shared Services Study

Municipality Land Area (km2)

1. Greater Sudbury 3,227.38

2. Kawartha Lakes 3,083.06

3. Timmins 2,979.15

4. Ottawa 2,790.22

5. Greenstone 2,767.76

6. Chatham-Kent 2,458.09

7. West Nipissing 1,992.08

8. Temagami 1,906.42

9. Killarney 1,654.58

10. Norfolk 1,607.60

Population Households Land Area (km2)

French River 2,547 2,550 735.47

Killarney 399 935 1654.58

Markstay-Warren

2,366 1,333 513.10

St.-Charles 1,282 963 321.54

Total 6,594 5,781 3,224.69

Population, Households and Land Area for Sudbury East Municipalities Largest Geographic Ontario Single Tier Municipalities

18© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Population and Households

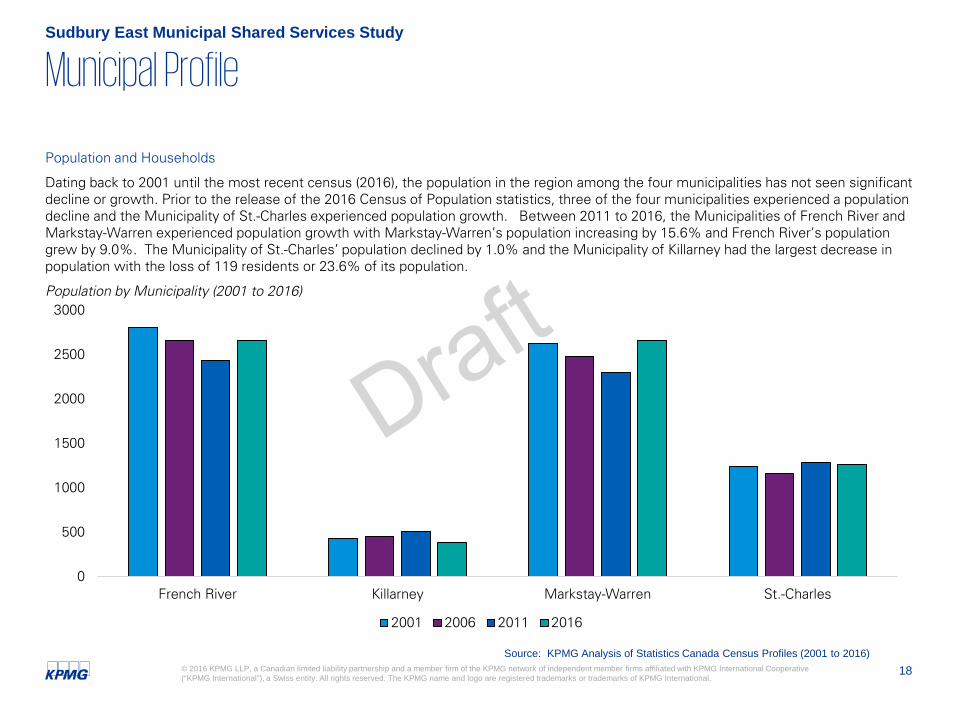

Dating back to 2001 until the most recent census (2016), the population in the region among the four municipalities has not seen significant decline or growth. Prior to the release of the 2016 Census of Population statistics, three of the four municipalities experienced a population decline and the Municipality of St.-Charles experienced population growth. Between 2011 to 2016, the Municipalities of French River and Markstay-Warren experienced population growth with Markstay-Warren’s population increasing by 15.6% and French River’s population grew by 9.0%. The Municipality of St.-Charles’ population declined by 1.0% and the Municipality of Killarney had the largest decrease in population with the loss of 119 residents or 23.6% of its population.

Population by Municipality (2001 to 2016)

Sudbury East Municipal Shared Services Study

0

500

1000

1500

2000

2500

3000

French River Killarney Markstay-Warren St.-Charles

2001 2006 2011 2016

Source: KPMG Analysis of Statistics Canada Census Profiles (2001 to 2016)

19© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Over the past five years, three of the four municipalities in Sudbury East have experience positive growth in their revenues. Only the Municipality of Killarney had a decrease in revenues between the years of 2011 to 2015 but this is attributed to a reduction in conditional grants received by the Municipality. The remaining three municipalities had increases in revenues ranging from 10% (St.-Charles) to 13% (French River) and 14% (Markstay-Warren). For the purposes of the reader, revenues listed within this chart include:

Revenues by Municipality (2011 to 2015)

Sudbury East Municipal Shared Services Study

2011 2012 2013 2014 2015 Change 2011 to 2015

French River $6.76 million $6.85 million $7.16 million $7.00 million $7.64 million +13%

Killarney $4.36 million $3.64 million $3.87 million $3.81 million $3.62 million -17%

Markstay-Warren $5.16 million $4.75 million $5.03 million $6.30 million $5.88 million +14%

St.-Charles $2.87 million $2.84 million $3.02 million $3.09 million $3.16 million +10%

Source: KPMG Analysis of Schedule 10 – Financial Information Returns (2011 to 2015)

• Property taxation • Grants (Conditional and unconditional)

• User fees and charges • Licenses, permits and rents

• Fines and penalties • Revenue from other municipalities

• Other revenues as recorded by the municipality

20© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Municipal Taxation

Municipal taxation represents the main source of revenues for the four municipalities in Sudbury East and in 2015, it accounted for at least half of each municipality’s revenues and as much as 62% of one municipality’s revenues (Municipality of French River). The fourmunicipalities generated over $11.5 million in 2015 through municipal taxation. Over the past five years, municipal taxation in each of the four municipalities has increased on an annual basis illustrated in the chart below.

Municipal Taxation by Municipality (2011 to 2015)

In Millions

Sudbury East Municipal Shared Services Study

Municipal Taxation as a Percentage of Total Revenues (2015)

French River Killarney Markstay-Warren St.-Charles

62% 57% 50% 57%

Source: KPMG Analysis of Schedule 10 – Financial Information Returns (2015)

$-

$1.00

$2.00

$3.00

$4.00

$5.00

French River Killarney Markstay-Warren St.-Charles

2011 2012

2013 2014

2015

Source: KPMG Analysis of Schedule 10 – Financial Information Returns (2011 to 2015)

21© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Municipal Taxation

The following chart illustrates median residential property taxes per household for the years of 2014 to 2016 for Sudbury East. The median represents the middle value. The Municipality of Markstay-Warren had the higher median residential property taxes within the Sudbury East group ($1,592) with the Municipality of Killarney being the lowest ($937). Over the course of the three years, residential taxes increased across the region with larger increases in the Municipalities of St.-Charles (an increase of 8.9% between the years of 2015 to 2016) and the Municipality of French River (7.1% between the years of 2015 to 2016).

Residential Property Taxes – Typical/Median Property (2014-2016)

Sudbury East Municipal Shared Services Study

$- $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 $1,800

Killarney

French River

St.-Charles

Markstay-Warren

2016

2015

2014

Source: KPMG Analysis of OPTA Analysis

22© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Taxable Assessment

Over the years of 2011 to 2015, all four of the municipalities in Sudbury East had their respective assessment grow across all properties with one exception. The Municipality of St.-Charles had a decline in their multi-residential assessment over the five year period. The growth in total assessment across the region ranged from 39.3% in the Municipality of Killarney to 56.1% in the Municipality of Markstay-Warren. The following charts on this page and the next illustrate phased in taxable assessment for the years of 2011 and 2015 and the change over that time period.

Phased In Taxable Assessment 2011 vs 2015 (In millions)

Sudbury East Municipal Shared Services Study

French River 2011 2015 Change from 2011 to 2015

Residential $294.1 $458.9 +56.0%

Multi-Residential $0.4 $0.5 +25.0%

Industrial $2.6 $3.7 +42.3%

Commercial $10.6 $13.6 +28.3%

Farmland and Managed Forest

$4.5 $5.8 +28.9%

Pipeline - - -

Total $312.2 $482.5 +54.5%

Killarney 2011 2015 Change from 2011 to 2015

Residential $113.8 $157.5 +38.5%

Multi-Residential - - -

Industrial $1.6 $1.9 +18.8%

Commercial $6.2 $9.8 +58.1%

Farmland and Managed Forest

- $0.06 -

Pipeline - - -

Total $121.6 $169.4 +39.3%

Source: KPMG Analysis of Financial Information Returns (2011 and 2015)

23© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Taxable Assessment

Phased In Taxable Assessment 2011 vs 2015 (In millions)

Sudbury East Municipal Shared Services Study

Markstay-Warren

2011 2015 Change from 2011 to 2015

Residential $112.8 $175.1 +55.3%

Multi-Residential $0.6 $0.6 -

Industrial $1.5 $7.9 +426.7%

Commercial $3.1 $3.5 +12.9%

Farmland and Managed Forest

$3.7 $4.6 +24.3%

Pipeline $4.2 $4.8 +9.5%

Total $125.9 $196.5 +56.1%

St.-Charles 2011 2015 Change from 2011 to 2015

Residential $98.1 $149.1 +52.0%

Multi-Residential $0.7 $0.6 -14.3%

Industrial - - -

Commercial $5.6 $6.1 8.9%

Farmland and Managed Forest

$2.6 $3.5 +34.6%

Pipeline $0.5 $0.5 -

Total $107.5 $159.8 +48.7%

Source: KPMG Analysis of Financial Information Returns (2011 and 2015)

24© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Taxable Assessment

Municipal assessment is determined by the Municipal Property Assessment Corporation(‘MPAC’) every four years in Ontario and represents the variable in the equation by which municipalities have no control over in setting their municipal levy. The municipal levy is driven by the desired services levels of the municipality and when increases occur, municipalities may wish to establish tax rates accordingly to potentially address affordability issues within their respective communities.

The following chart provides the typical/median current value assessment for a single family residence for the four municipalities in Sudbury East. Over the past three years, the current value assessment for this property class has increased on an annual basis for all four in the region.

Residential Current Value Assessment – Typical/Median Property (2014-2016)

Sudbury East Municipal Shared Services Study

$- $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000

St.-Charles

Killarney

French River

Markstay-Warren

2016

2015

2014

Source: KPMG Analysis of OPTA Analysis

25© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

Operating Grants

The main operating grant provided to municipalities in Ontario is the Ontario Municipal Partnership Fund (‘OMPF’) and all of themunicipalities in Northern Ontario and therefore, by extension, all four municipalities in Sudbury East receive OMPF funding on an annual basis. The Province of Ontario announced its intent to reduce the overall envelope of funding to $505 million by 2016 and in 2017, maintained this level of funding. As a result of this, the four municipalities of Sudbury have experienced a decrease in annual support from the Province with one exception where the Municipality of St.-Charles received an increase of almost $18,000 between 2016 to 2017. The following chart illustrates the level of support the four municipalities of Sudbury East have received over the past five years. In response to this challenge, municipalities are seeking out innovative ways to avoid simply passing along the decrease to their respective tax base and a study such as this is one potential strategy in assisting the four municipalities in Sudbury East.

OMPF Funding by Municipality (2013 to 2017)

Sudbury East Municipal Shared Services Study

$-

$0.50

$1.00

$1.50

$2.00

$2.50

French River Killarney Markstay-Warren St.-Charles

2013 2014 2015 2016 2017

Source: KPMG Analysis of OMPF Funding Allocation Notices (2013 to 2017)

26© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Municipal Revenues

User Fees and Service Charges

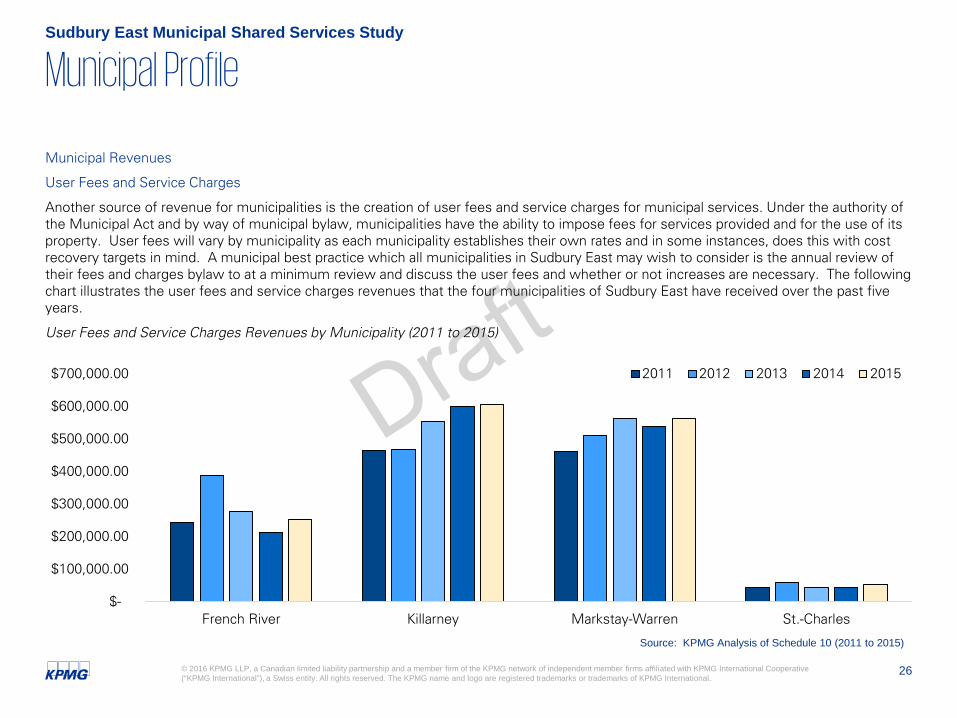

Another source of revenue for municipalities is the creation of user fees and service charges for municipal services. Under the authority of the Municipal Act and by way of municipal bylaw, municipalities have the ability to impose fees for services provided and for the use of its property. User fees will vary by municipality as each municipality establishes their own rates and in some instances, does this with cost recovery targets in mind. A municipal best practice which all municipalities in Sudbury East may wish to consider is the annual review of their fees and charges bylaw to at a minimum review and discuss the user fees and whether or not increases are necessary. The following chart illustrates the user fees and service charges revenues that the four municipalities of Sudbury East have received over the past five years.

User Fees and Service Charges Revenues by Municipality (2011 to 2015)

Sudbury East Municipal Shared Services Study

$-

$100,000.00

$200,000.00

$300,000.00

$400,000.00

$500,000.00

$600,000.00

$700,000.00

French River Killarney Markstay-Warren St.-Charles

2011 2012 2013 2014 2015

Source: KPMG Analysis of Schedule 10 (2011 to 2015)

27© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Operating Expenditures

The following chart is a summary of operating expenditures for the four municipalities of Sudbury East for the years of 2011 to 2015. While each of the municipalities may have experienced a decrease in operating expenditures from one year to the next, the consistent trend across the region is an increase in operating expenditures over the five year used for the purposes of the study.

Total Operating Expenditures by Municipality excluding amortization (2011 to 2015)

Sudbury East Municipal Shared Services Study

2011 2012 2013 2014 2015 Change 2011 to 2015

French River $5.49 million $5.37 million $5.78 million $6.01 million $5.98 million +9%

Killarney $2.85 million $3.08 million $3.17 million $3.15 million $3.31 million +16%

Markstay-Warren $4.09 million $4.38 million $4.51 million $4.36 million $4.62 million +13%

St.-Charles $2.50 million $2.66 million $3.19 million $3.13 million $2.90 million +16%

Source: KPMG Analysis of Financial Information Returns (2011 to 2015)

28© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Operating Expenditures

In 2015, the four municipalities of Sudbury East had operating expenditures ranging from $2.9 million (St.-Charles) to $6 million spent in the Municipality of French River. The level of expenditures across the region of Sudbury East is consistent with our experience in the municipal sector where it is expected that the majority of municipal operating expenditures reside within the delivery of infrastructure services and in corporate services and that is reflected in the chart below.

Operating Expenditures by Category and by Municipality excluding amortization (2015)

Sudbury East Municipal Shared Services Study

French River Killarney Markstay-Warren St.-Charles

Expenditures As of % of Total Expenditures As of % of

Total Expenditures As of % of Total Expenditures As of % of

Total

General Government $1,378,370 23.1% $705,386 21.3% $829,380 18.0% $792,925 27.3%

Protective Services $865,260 14.5% $248,349 7.5% $943,254 20.4% $476,638 16.4%

Infrastructure(Transportation and Environment)

$1,742,339 29.2% $1,183,863 35.8% $1,644,027 35.6% $807,833 27.8%

Health and Social Services

$1,191,652 19.9% $985,360 29.8% $655,094 14.2% $276,675 9.5%

Recreation $595,991 10.0% $133,170 4.0% $455,727 9.9% $442,198 15.2%

Planning and Development $202,742 3.3% $50,818 1.6% $90,492 1.9% $108,553 3.8%

Total $5,976,354 $3,306,946 $4,617,974 $2,904,822

Source: KPMG Analysis of Financial Information Returns (2015)

29© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Personnel

One of the largest expenditures that municipalities have on an annual basis relate to the salaries and benefits paid to their employees to carry out the operations of their respective municipalities. In Sudbury East, wages and benefits account for a range of almost 25% in the Municipality of Killarney to 36% in the Municipality of St.-Charles. The range in Sudbury East appears to be lower based on our experience with similarly sized municipalities where the salaries and benefits account for 30% to 40% of total operating expenditures.

Sudbury East Municipal Shared Services Study

Source: KPMG Analysis of Financial Information Returns (2015)

French River Killarney Markstay-Warren St.-Charles

Salaries and Benefits $1.89 million $0.82 million $1.38 million $1.05 million

Total OperatingExpenditures exc. Amortization

$5.98 million $3.31 million $4.62 million $2.90 million

Salaries and Benefits as a % of Total Operating Expenditures

31.6% 24.8% 29.9% 36.2%

30© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Personnel

The following chart below illustrates the staffing levels in the four municipalities of Sudbury East. The staffing levels across the four municipalities are relatively consistent and where variance occur, they are reflective of the complement of municipal services provided and the associated service levels. For example, the Municipality of French River has the largest staffing complement in the group but unlike the other municipalities, performs services such as solid waste management where the others rely on different approaches.

Municipal Staffing Levels

Sudbury East Municipal Shared Services Study

0

5

10

15

20

25

French River Killarney Markstay-Warren St.-Charles

Corporate Infrastructure Protective Community

Source: KPMG Analysis of Information Provided by Sudbury East Municipalities

31© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Personnel

The Ministry of Finance has identified the aging population as the greatest demographic trend facing Ontario and much like many of their municipal peers, the municipalities of Sudbury East will need to address an aging workforce and the need to plan for the future. Based on information shared with KPMG, the following charts illustrate the years of experience and demographics of the Sudbury East municipal staffing complement. While the majority of the municipal workforce has less than 5 years of service with their respective municipalities, 33% of the workforce is over the age of 50 with 17% over the age of 60. The potential threat and one that many municipalities currently face is when these individuals decide to retire and if plans are not in place, their knowledge and experience follows which can create operational inefficiencies in the interim until their replacements develop.

Sudbury East Municipal Shared Services Study

Source: KPMG Analysis of Information Provided by Sudbury East Municipalities

0

5

10

15

20

25

30

0 to 5 Years 6 to 10 Years 11 to 15 Years 15+ Years

50 to 59 Years

33% 40 to 49 Years

21%

30 to 39 Years

19%

20 to 29 Years

10%

60+ Years

17%

Years of Service Breakdown of Current Sudbury East Municipal Workforce

Age Breakdown of Current Sudbury East Municipal Workforce

32© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Capital Expenditures and Infrastructure

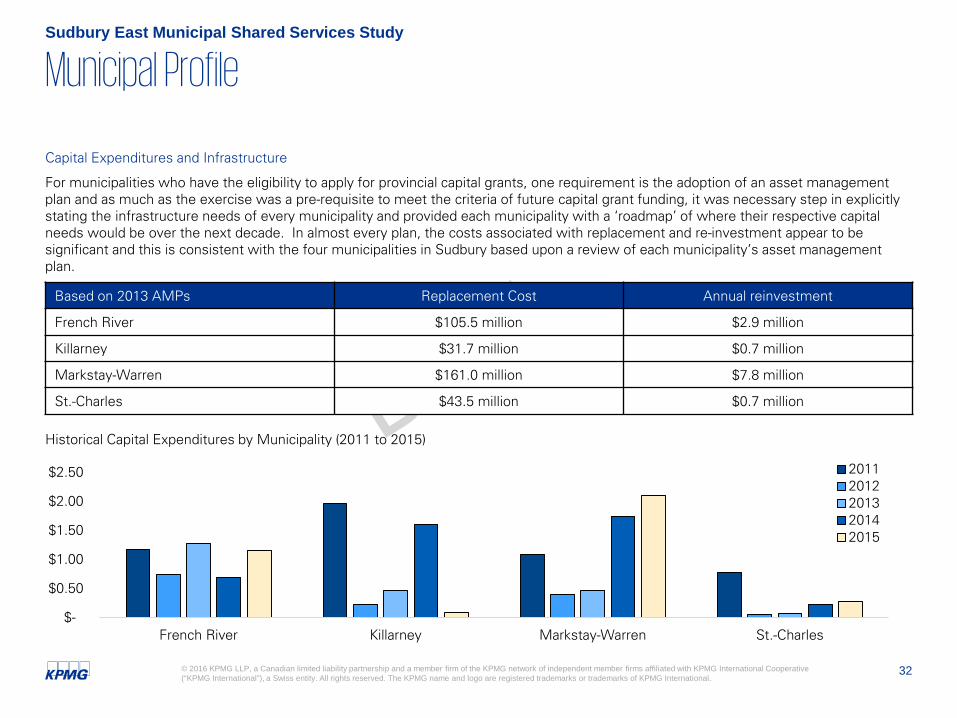

For municipalities who have the eligibility to apply for provincial capital grants, one requirement is the adoption of an asset management plan and as much as the exercise was a pre-requisite to meet the criteria of future capital grant funding, it was necessary step in explicitly stating the infrastructure needs of every municipality and provided each municipality with a ‘roadmap’ of where their respective capital needs would be over the next decade. In almost every plan, the costs associated with replacement and re-investment appear to besignificant and this is consistent with the four municipalities in Sudbury based upon a review of each municipality’s asset management plan.

Historical Capital Expenditures by Municipality (2011 to 2015)

Sudbury East Municipal Shared Services Study

$-

$0.50

$1.00

$1.50

$2.00

$2.50

French River Killarney Markstay-Warren St.-Charles

20112012201320142015

Based on 2013 AMPs Replacement Cost Annual reinvestment

French River $105.5 million $2.9 million

Killarney $31.7 million $0.7 million

Markstay-Warren $161.0 million $7.8 million

St.-Charles $43.5 million $0.7 million

33© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Capital Expenditures and Infrastructure

Asset Sustainability Ratio

The Ministry of Municipal Affairs established an asset sustainability ratio which is “an approximation of the extent to which a municipality is replacing, renewing or acquiring new assets as the existing infrastructure being managed by the municipality are reaching the end of their useful lives.” The Province sets a target ratio of 90% or greater and if a municipality is below the ratio, there may be concerns about the sufficiency of the municipality’s asset management and the potential future burden this may place upon residents. For the years of 2011 to 2015, all four municipalities in Sudbury East had at least one year that did not meet the target ratio. However, for the years of 2014 to 2015, all four municipalities exceeded the ratio and the average over the course of the five years is well above the target ratio.

Asset Sustainability for Sudbury East Municipalities (2011 to 2015)

Sudbury East Municipal Shared Services Study

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

French River Killarney Markstay-Warren St.-Charles

2011

2012

2013

2014

2015

Average

Source: KPMG Analysis of Multi-Year Financial Information Returns (2011 to 2015)

34© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Municipal Profile

Capital Expenditures and Infrastructure

Asset Consumption Ratio

The previous page examined the sufficiency of asset maintenance, renewal and replacement and the Ministry of Municipal Affairs also established a ratio which measures the consumption of a municipality’s physical assets in comparison and their cost. As part of this ratio, the Province established the following ranges: Less than 25% - relatively new infrastructure, 26% to 50% - moderately new infrastructure, 51% to 75% - moderately old infrastructure and 75% or greater – old infrastructure. All of the municipalities in Sudbury East have asset consumption ratios that either trending towards moderately old infrastructure or have a ratio within that range (Municipality of St.-Charles). This may pose a challenge for these municipalities as the need to replace assets outpaces their respective investments into their infrastructure. All municipalities appear to entering into the replacement phase for a large portion of their infrastructure and as such, thereappears to be the need for each municipality to strategize and prioritize their capital needs.

Asset Consumption for Sudbury East Municipalities (2011 to 2015)

Sudbury East Municipal Shared Services Study

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

French River Killarney Markstay-Warren St.-Charles

2011 2012 2013 2014 2015

Source: KPMG Analysis of Multi-Year Financial Information Returns (2011 to 2015)

Less than 25% - relatively new infrastructure

26% to 50% - moderately new infrastructure

51% to 75% - moderately old infrastructure

Sudbury East

Municipal Shared

Services Study

Shared Services in

Ontario

36© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Shared Services in Ontario

An Overview of Shared Services in Ontario

For the purposes of summarizing the prevalence of shared service arrangements within the municipal sector, we relied upon a survey conducted by the Ministry of Municipal Affairs and Housing in November 2012 where 400 of Ontario’s 444 municipalities participated in. In addition to the 2012 survey, we also relied upon our experiences in working with municipalities across Ontario who have participated in shared service arrangements to varying degrees.

What Do Municipalities Share?

Section 20 of the Municipal Act provides municipalities in Ontario with the legal authority to enter into shared service agreements. Section 20(1) of the Act:

Joint undertakings

20. (1) A municipality may enter into an agreement with one or more municipalities or local bodies, as defined in section 19, or a combination of both to jointly provide, for their joint benefit, any matter which all of them have the power to provide within their own boundaries. 2001, c. 25, s. 20 (1).

Ultimately, what the legislation does not place upon municipalities are explicit restrictions as to what and who a municipality can share with other municipalities or local bodies and First Nations.

Sudbury East Municipal Shared Services Study

37© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Shared Services in Ontario

An Overview of Shared Services in Ontario

What Do Municipalities Share?

Based upon a review of the survey results and our experience in working with municipalities across Ontario, the following chart illustrates the most commonly shared services in Ontario.

Sudbury East Municipal Shared Services Study

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Legal ServicesFinance – Payroll/Tax Collection/ Audit

Facilities ManagementWebsite

Clerk Or Related Administrative ResponsibilitiesMunicipal EquipmentMeeting Investigation

Community Emergency ManagementTendering Of ContractsInformation Technology

TourismWater Or Sewer

Recreation – Arenas/Parks/PoolsPurchasing

Economic DevelopmentWaste Management – Landfill Or Recycling

Planning, Building Inspection Or By-Law EnforcementLibraries

Roads – MaintenanceOther

38© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Shared Services in Ontario

An Overview of Shared Services in Ontario

Why Do Municipalities Share?

Based upon our experiences with municipalities and coupled with a review of literature on the subject, public sector entities share services for a variety of reasons:

• Reducing operating costs – The financial environment in which municipalities exist continues to challenge municipalities where they attempt to balance meeting the expectations of their residents while trying to manage operating costs. That balancing act coupled with reductions in grant revenues, municipalities are now seeking out innovative ways of reducing costs. Similar to the intended objective of the Sudbury East municipalities, municipalities seek out shared services arrangements with each other to maintain service levels while reducing the overall costs associated with delivering those services.

• Strategic approach to addressing infrastructure needs – Similar to challenges relating to operating expenditure pressures and with the adoption of municipal asset management plans in 2012, municipalities face significant challenges in maintaining and eventually replacing their assets. In response, municipalities explore the potential of sharing assets with others to spread the costs of replacement costs of the asset beyond the scope of one and this coordination of assets can also contribute to lower ongoing operating/maintenance costs.

• Increasing capacity – While reducing costs (either operating or capital) may be the main objective for municipalities seeking out shared service opportunities, municipalities may share in order to increase operational capacity and in turn, provide a higher level of service without having to bear the full cost of doing so.

Past Experience in Ontario

The overall result of the 2012 survey demonstrated that 369 municipalities in Ontario indicated that their involvement in some form of a shared service arrangement which represented 92% of the survey’s respondents. The percentage of municipalities involved in shared services was typically in excess of 90% with the exception of Northeastern Ontario (87%). The primary reason why municipalities entered into shared service arrangements was to reduce operating costs with other secondary reasons being increased goodwill between municipalities and enhancing the overall quality of service.

Despite the high degree of consistency in the prevalence and rationale for shared service arrangements, there are noticeable differences in terms of what is shared by region. While emergency medical services (land ambulance and paramedics) were cited as a shared service in all regions of Ontario, the sharing of other services will vary. For example, Western Ontario has a higher degree of sharing of so-called infrastructure-heavy services such as water, wastewater and roads, which is likely indicative of the proximity of municipalities to potential partners (as opposed to Northwestern Ontario where the major shared services are less infrastructure intensive).1

Sudbury East Municipal Shared Services Study

1 – Sharing Municipal Services in Ontario - Case Studies and Implications for Ontario Municipalities

39© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

An Overview of Shared Services in Ontario

Past Experience in Ontario

The Northern Ontario Experience

As noted earlier, there appear to be regional variances in what services are shared based upon geography. In Northern Ontario, the sharing of building, planning and bylaw related services was the most commonly shared service across the two regions. In Northwestern Ontario and beyond planning, building and bylaw related matters, municipalities west of the Algoma District share landfill operations, meeting investigations and economic development. For the 110 municipalities in Northeastern Ontario, the sharing of libraries, facility management and roads maintenance were the most commonly shared services.

Shared Services in OntarioSudbury East Municipal Shared Services Study

Northwestern Ontario

Planning, building and bylaw 41%

Landfill operations 35%

Meeting investigations 29%

Economic development 29%

Northeastern Ontario

Planning, building and bylaw 45%

Libraries 40%

Facility management 38%

Roads maintenance 29%

40© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Shared Services in Ontario

Sudbury East Municipalities and Shared Services

Consistent with their municipal peers across the Province of Ontario, the four municipalities of Sudbury East have engaged or attempted to participate in various shared service arrangements with varying levels of formality:

Sudbury East Planning Board

• The four municipalities of Sudbury East along with a number of unincorporated townships are provided with land use planning services by the Sudbury East Planning Board. The Board’s governance structure is comprised of political representation from all four municipalities as well as two provincially appointed members. The Board provides all land use planning functions to the area including but not exclusive to oversight of all Official Plans and associated zoning bylaw matters.

Building Control Services

• At the time of the study, the Municipality of St.-Charles and the Municipality of Killarney share a Chief Building Official (‘CBO’) and share costs with St.-Charles assuming 60% of the associated operating costs and Killarney assumes the remaining 40%. The Municipality of St.-Charles provides administrative support as part of the arrangement.

Boundary Road Agreements

• Based on information shared with KPMG during the study, the Municipalities of Markstay-Warren and St.-Charles have boundary roadagreements which sets out who is responsible for maintenance activities and the subsequent sharing of those costs.

Mutual Aid Agreements

• All of the municipalities participating in the study have mutual aid agreements in place with one or more of their neighbours to assist in the case of emergencies.

Public Library Services

• Another example of a current shared service arrangements exists between the Municipalities of French River and Killarney. As part of this arrangement, the Municipality of Killarney provides the Municipality of French River with an annual financial contribution through a provincial operating grant for access to library services.

Sudbury East Municipal Shared Services Study

41© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Shared Services in Ontario

Sudbury East Municipalities and Shared Services

Consistent with their municipal peers across the Province of Ontario, the four municipalities of Sudbury East have engaged or attempted to participate in various shared service arrangements with varying levels of formality:

Economic Development

• Three of the four municipalities (the Municipalities of French River, St.-Charles and Markstay-Warren) belong to Economic Partners Sudbury East/Nipissing West. In addition to the three municipalities, the Municipality of West Nipissing and two First Nations (Dokis and Nipissing) are also members. The objective of Economic Partners is dedicated “to creating opportunities for entrepreneurship and to the pursuit of economic growth in our community.”

Informal Sharing

• During the second phase of the study, instances were brought to our attention whereas municipalities would reach out to each other to share. Examples provided were where if a neighbouring municipality required a piece of equipment such as a water truck, a phone call would initiate the sharing/rental of the equipment but nothing formal was developed subsequently.

Sudbury East Municipal Shared Services Study

Sudbury East

Municipal Shared

Services Study

Potential Shared

Service Opportunities

43© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Potential Shared Service Opportunities

Based on our experience in working with municipalities and other public sector entities, any arrangement to share between two partners need to incorporate the following pillars and/or give consideration to these to enhance the likelihood of success.

Trust

When discussing any form of relationship, trust consistently ranks as probably the most fundamental element to any successfulrelationship/partnership. Without trust among the partners involved, there is the potential for an increased level of risk to the longevity of the arrangement.

Communication

Closely related to trust, communication is another essential element to a positive working relationship. Communication, as part of any partnership, needs to ongoing and honest with clearly established channels. In working with other municipalities who have long-standing shared service arrangements, one of the lessons learned is with a high level of trust and communication, discussions involving the allocation of costs take considerably less time.

Mutual Benefit

The concept of mutual benefit is crucial to the success of any shared service arrangement. At no time during the process, should one be able to clearly identify “winners” and “losers.” Each partner in the arrangement should be able to point to the benefit of the partnership. In some cases, one municipality may experience an increase in revenues as a result of sharing with another whereas the other will experience a decrease in operating costs. In the absence of mutual benefit, the relationship/arrangement is exposed to the risk of one side seeking to end it.

Data Collection

Beyond the pillars above that specifically deal with the relationship, good data can assist and facilitate the development of shared service arrangements. If any one or all of the three concepts identified above are lacking, verifiable and reliable data can reinforce and/or support the building of trust as well as the demonstration of mutual benefit to all parties. Under certain circumstances, it may be beneficial to postpone moving forward with an agreement until there is reliable data that can be then translated into pertinent information for the purposes of a shared service arrangement.

Sudbury East Municipal Shared Services Study

44© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Potential Shared Service Opportunities

Other Considerations

Within the municipal sector, there is a misconception that the potential expansion of shared service arrangements among municipalities is the first step towards amalgamation. Based upon the current language contained within the Municipal Act, municipal restructuring is a locally driven process and not one initiated by the Province of Ontario. With that in mind, an increased interest in shared service arrangements is not one of municipal restructuring but instead an attempt to reduce the cost of providing a service across two or more municipal partners and/or providing service in a more effective and efficient manner.

Sudbury East Municipal Shared Services Study

45© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

A. Overview of Group Purchasing

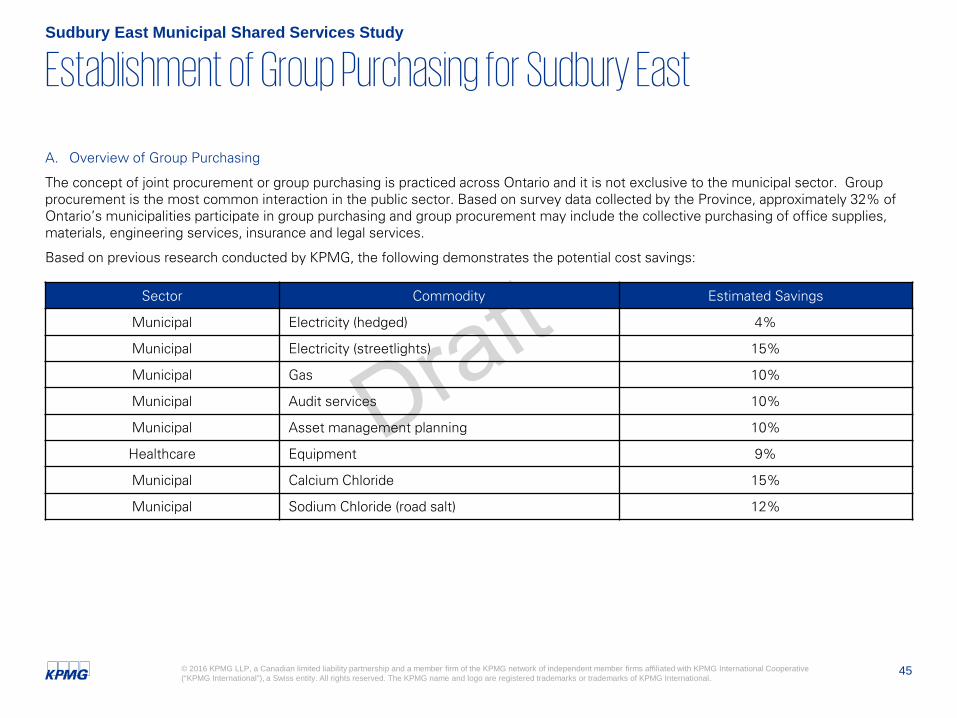

The concept of joint procurement or group purchasing is practiced across Ontario and it is not exclusive to the municipal sector. Group procurement is the most common interaction in the public sector. Based on survey data collected by the Province, approximately 32% of Ontario’s municipalities participate in group purchasing and group procurement may include the collective purchasing of office supplies, materials, engineering services, insurance and legal services.

Based on previous research conducted by KPMG, the following demonstrates the potential cost savings:

Sudbury East Municipal Shared Services Study

Sector Commodity Estimated Savings

Municipal Electricity (hedged) 4%

Municipal Electricity (streetlights) 15%

Municipal Gas 10%

Municipal Audit services 10%

Municipal Asset management planning 10%

Healthcare Equipment 9%

Municipal Calcium Chloride 15%

Municipal Sodium Chloride (road salt) 12%

46© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

A. Overview of Group Purchasing

There are no limitations as to what the municipalities of Sudbury East could purchase as a group. The following are examples of areas where group procurement can take place.

• Bulk materials

There are materials that are common across the operations of all four municipalities such as aggregate, fuel, and office supplies. Based on our experience, there exists the potential of reducing the costs of acquiring these materials as part of a larger group purchasing initiative opposed to doing so on an individual basis. With respect to the acquisition of aggregate, one consideration for the group is the Municipality of Markstay-Warren owns and operates its own pit for the purposes of providing its operations with aggregate.

• Purchasing of equipment

As part of the study, one aspect of each municipality that was examined was the suitability of its current equipment complement and as identified earlier in the report, municipalities have been sharing equipment on an informal basis. The concept of group procurement for equipment is two-fold. First, there may opportunities in the future as to when one municipality is looking to replace a common piece of equipment such as a truck that others can participate in the process and try achieve greater cost savings. Second, when a municipality is seeking out a piece of equipment that is of a more specialized nature (rubber tire excavator is an example and one raised during consultations with the participating municipalities), the opportunity to have the discussion about the needs of all can take place and potentially lead to the cost of the equipment. The majority of the municipalities indicated that their respective equipment complement meets the needs of the organization with some exceptions such as the reliance on a neighbour for access to a water truck.

• Professional services

All of the municipalities purchase various professional services from third party providers and those services may include the following professional services: external audit, information technology services, legal, human resources, banking services, and employee benefits

The proposed approach for the consideration of the municipalities of Sudbury East could involve mandatory and optional elements whereas this is not an “all or none” proposition for the four municipalities of Sudbury East. Instead and as illustrated in the implementation section of this opportunity, at the initial consultation phase, a municipality has the ability to decide to participate or not. However, if a municipality decides to participate in the group procurement process for that particular matter, it is mandatory for the municipality to award based on the group’s consensus. One cannot opt out at the end if they decide they do not like the result because it jeopardizes the credibility of the group’s purchasing power in the future. Additionally and to ensure initial buy-in, the municipalities may wish to include a component that does not allow for a municipality who opted out to try to take advantage of the result if the costs are lower than their current costs.

Sudbury East Municipal Shared Services Study

47© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

B. Current Service Delivery Model

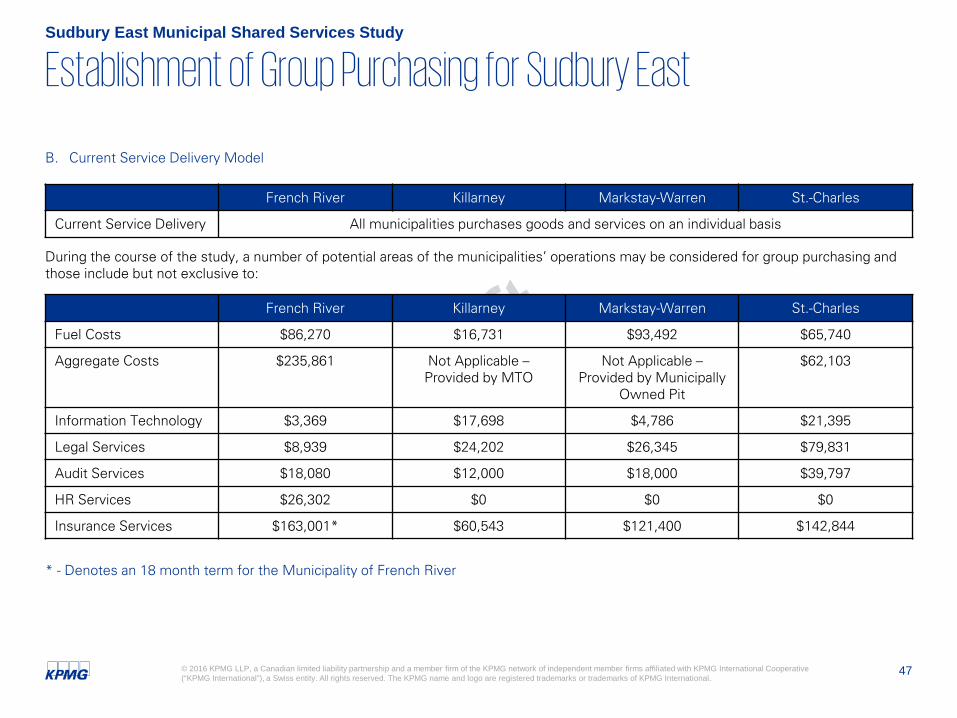

During the course of the study, a number of potential areas of the municipalities’ operations may be considered for group purchasing and those include but not exclusive to:

* - Denotes an 18 month term for the Municipality of French River

Sudbury East Municipal Shared Services Study

French River Killarney Markstay-Warren St.-Charles

Current Service Delivery All municipalities purchases goods and services on an individual basis

French River Killarney Markstay-Warren St.-Charles

Fuel Costs $86,270 $16,731 $93,492 $65,740

Aggregate Costs $235,861 Not Applicable –Provided by MTO

Not Applicable –Provided by Municipally

Owned Pit

$62,103

Information Technology $3,369 $17,698 $4,786 $21,395

Legal Services $8,939 $24,202 $26,345 $79,831

Audit Services $18,080 $12,000 $18,000 $39,797

HR Services $26,302 $0 $0 $0

Insurance Services $163,001* $60,543 $121,400 $142,844

48© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

C. Opportunity Evaluation

Financial Impact

a) Potential Cost Savings

While the potential cost savings will be dependent on nature of the purchase and the group’s ability to realize cost savings through greater volume, the following chart provides potential cost savings based on information provided to KPMG during the study:

Sudbury East Municipal Shared Services Study

Fuel

Municipality Potential Discount Cost Potential Cost Savings

French River

10%

$86,270 $8,627

Killarney $16,731 $1,673

Markstay-Warren $93,492 $9,349

St.-Charles $65,740 $6,574

Legal

French River

10%

$8,939 $894

Killarney $24,202 $2,420

Markstay-Warren

St.-Charles $79,831 $7,983

49© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

C. Opportunity Evaluation

Financial Impact

a) Potential Cost Savings

While the potential cost savings will be dependent on nature of the purchase and the group’s ability to realize cost savings through greater volume, the following chart provides potential cost savings based on information provided to KPMG during the study:

Sudbury East Municipal Shared Services Study

Audit

Municipality Potential Discount Cost Potential Cost Savings

French River

10%

$18,080 $1,808

Killarney $12,000 $1,200

Markstay-Warren $18,000 $1,800

St.-Charles $39,797 $3,980

Insurance

French River

10%

$163,001 $16,300

Killarney $60,543 $6,054

Markstay-Warren $121,400 $12,140

St.-Charles $142,844 $14,284

50© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

C. Opportunity Evaluation

Financial Impact

b) One-Time Implementation and/or Harmonization Costs

With respect to the apportionment of cost and given the nature of the opportunity, the actual costs associated with group procurement would be staff’s time participating in the process identified above and therefore, should not require any allocation of costs because the entire group benefits.

c) Capital/Infrastructure Costs

None identified given the nature of the service

Consistent with Municipal Best Practices

Yes – the potential shift to a group purchasing initiative in Sudbury East is consistent with municipal best practices. As noted earlier within this section, group purchasing is the most common shared service arrangement in the public sector. 32% of Ontario’s municipalities have participated in some form of group procurement.

Other Considerations

Additionally, there does not appear to be a need to develop a formal governance body for group procurement but a formal agreement establishing the process and procedures would be required.

Beyond the elements of the shared service identified within this opportunity, there do not appear any other non financial consideration. This opportunity is administrative in nature and therefore, group purchasing should not impact upon customer service, public health, and/or labour relations.

Provided a formal arrangement is adopted by all four municipalities, we do not believe there is any additional risk associated with the group’s participation in procurement to the four municipalities in Sudbury East. A sample agreement for the purposes of establishing a group purchasing initiative can found within Appendix B.

Sudbury East Municipal Shared Services Study

51© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Establishment of Group Purchasing for Sudbury East

D. Potential Cost Apportionment and Governance Model

With respect to the apportionment of cost and given the nature of the opportunity, the actual costs associated with group procurement would be staff’s time participating in the process identified above and therefore, should not require any allocation of costs because the entire group benefits.

Additionally, there does not appear to be a need to develop a formal governance body for group procurement but a formal agreement establishing the process and procedures would be required.

E. Recommendation

Based on the evaluation of the opportunity, it is recommended that the municipalities of Sudbury East pursue the implementation of group purchasing in Sudbury East.

Sudbury East Municipal Shared Services Study

52© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Building Controls

A. Overview of Building Controls Services

In Ontario, the Building Code Act and its regulation, the Ontario Building Code (‘OBC’) set out the rules for construction. The following describes what the two pieces of legislation deal with:

Building Code Act

• Governs the construction, renovation, change of use, and demolition of buildings;

• Provides specific powers for inspectors and rules for the inspection of buildings; and

• Allows municipalities to establish property standard by-laws.

Ontario Building Code – A Regulation of the Act