Succeeding in a challenging environment… for the … – worth £21 000 f ll li it dth £21,000...

32

Succeeding in a challenging Succeeding in a challenging environment environment environment… environment… for the next generation for the next generation Chairman Charlie Bryant Charlie Bryant Partner Brown & Co Partner, Brown & Co.

Transcript of Succeeding in a challenging environment… for the … – worth £21 000 f ll li it dth £21,000...

Succeeding in a challenging Succeeding in a challenging environmentenvironmentenvironment… environment…

for the next generationfor the next generation

Chairman

Charlie BryantCharlie BryantPartner Brown & CoPartner, Brown & Co.

Presentation by:Presentation by:

Andrew HeskinP t M ThPartner - Moore Thompson

www.moorethompson.co.uk

“Success is the ability to gofrom failure to failure without

losing your enthusiasm”losing your enthusiasm

- Sir Winston Churchill

Introduction

Agricultural Team Chris Wright, Partner - Wisbech OfficeAndrew Heskin, Partner – Spalding OfficeBill C C lt t S ldi OffiBill Creasey, Consultant – Spalding Office

M Th th ffi t S ldiMoore Thompson – three offices at Spalding, Wisbech, Market Deeping

Tax and the next ten yearsNew Government –

“The Coalition: Our programme for Government”

More competitive, simpler, greener, fairerIncrease tax burden to reduce fiscal deficitUncertain financial climate – but the tax ‘tail’ should not wag the commercial ‘dog’commercial dogi.e., do not base business decisions on tax reasons aloneTax avoidance to be targetedHMRC working together, PAYE, VAT and Business tax

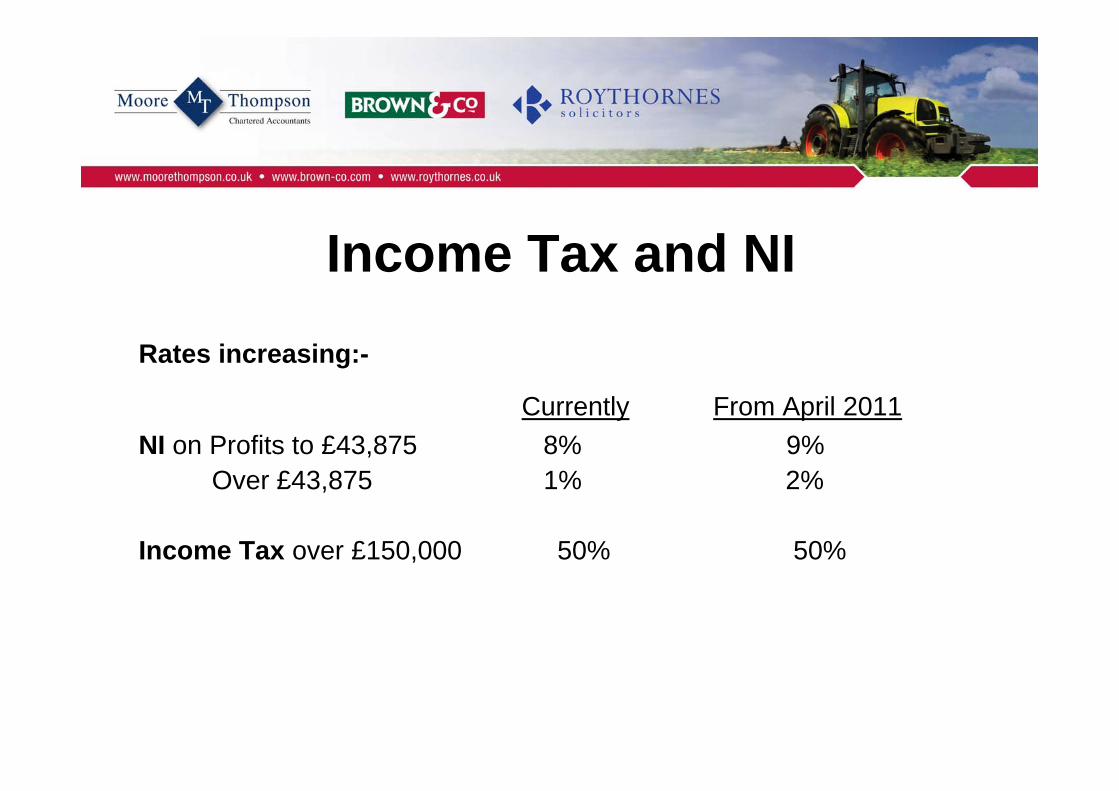

Income Tax and NIRates increasing:-

Currently From April 2011NI on Profits to £43,875 8% 9%

Over £43 875 1% 2%Over £43,875 1% 2%

Income Tax over £150,000 50% 50%

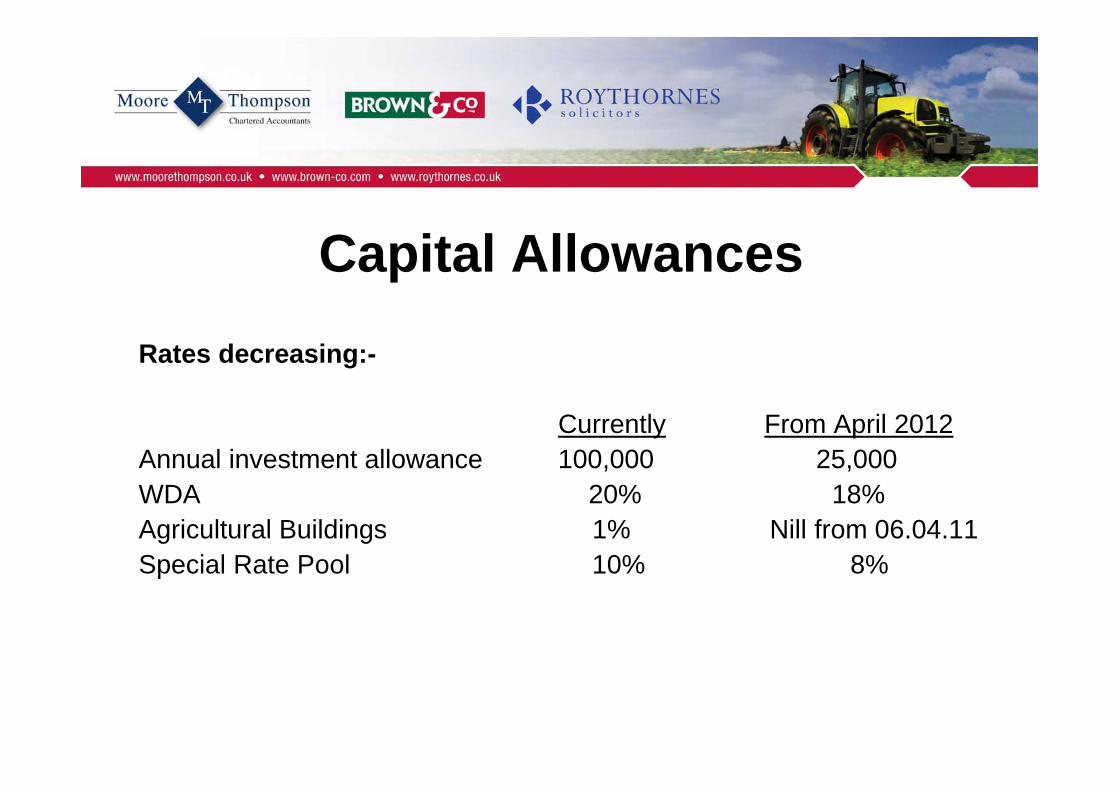

Capital AllowancesRates decreasing:-

Currently From April 2012Annual investment allowance 100,000 25,000WDA 20% 18%WDA 20% 18%Agricultural Buildings 1% Nill from 06.04.11Special Rate Pool 10% 8%p

TipsMaximise claims for allowancesAIA – worth £40,000 for higher rate tax payer (under £150,000)AIA th £21 000 f ll li it dAIA – worth £21,000 for small limited company

Consider qualifying expenditure in advanceq y g pshell of building, walls, floors, ceilings, doors, windows – not qualifyingintegral features – heating system electrical system cold waterintegral features heating system, electrical system, cold water system, thermal insulation – qualifyingrepairs – 100% allowable

% /• 100% on green assets/energy saving assetshttp://www.eca.gov.uk/etl

Corporation TaxMain rate reducing from 27% for 2011-12 to 24% for 2014-15

Small company rate reducing to 20% from April 2011p y g p

But watchattacks on benefits in kindcompany cars – taxation increasing. Consider holding outside companyand mileage claims (40p for the first 10,000 miles/25p thereafter)100% capital allowances on green cars (low CO2 emissions, i.e., less than

/ )110g/km)Farmhouse expenses

Current HMRC lines of attackDeputy PM stated on Today programme that using an Accountant was questionable!Employment status i.e. employed v self employed, onus is on the p y p y p y ,employerDrainage repairs versus capitalVAT position of shoots (private shoots run for recreation/syndicates p (p yfor cost sharing do not have to register), but watch position when landowner is member of syndicate as VAT may need to be charged on value of rights granted, even if no money changes hands.VAT f h i (70% f i t ll ti )VAT on farmhouse repairs (70% for installation).But HMRC will attack if usage predominantly private

Cash businesses – use of information for cross referrals e.g. chip h b i t t f h !shops buying potatoes for cash !

• "The most successful people in life are generally those who have the best information."

B j i Di li– Benjamin Disraeli

• “Winners never quit and quitters never win”• Winners never quit and quitters never win– Vince Lombardi

Capital Gains TaxL d l i d i d ti t li f!Land values increased, no indexation or taper relief!28% for non Entrepreneurial/non business assets (for higher rate tax

payers and trusts)

Reliefs available:• Entrepreneurs Relief

– 10% for Entrepreneurial business activities on sales of qualifying business assets– Partial sales of land without disposal of business or retirement will not qualify– First £5 million of Qualifying gains over lifetime

• Roll over relief• Roll-over relief– Buildings, land, fixed plant, goodwill, quotas, payment entitlements under the single

payment scheme• Hold-over relief• Hold-over relief

– Business assets and agricultural land including houses if ‘character appropriate’

VAT

Rate increase to 20% from 4.1.11Watch partial exemption

Rented properties e.g watch large repairs to a farm cottageI ‘O ti t T ’ l d i t ?Is ‘Option to Tax’ land appropriate?

St d d t li f i h d h lid l ttiStandard rate supplies e.g. furnished holiday lettings, fishing rights

IN SUMMARY

Increasing Income Tax and National Insurance rates will combine with falling capital allowances to cause tax bills to riseg pThere are ways to reduce this impact with careful planningCorporation Tax rates are fallingBut we are experiencing greater scrutiny of farm records as part of the drive to combat tax avoidanceCapital Gains Tax is a much more significant tax for farmers thanCapital Gains Tax is a much more significant tax for farmers than it used to beAnd VAT continues to be a complex area where it is easy to make mistakesmake mistakes.

• There are two rules to success:- Number one – never tell anyone everything

you knowyou know

Succeeding in a Challenging EnvironmentPresentation by:EnvironmentPresentation by:

Paul White Partner Brown & CoPartner, Brown & Co.

10 UK ffi

Brown & Co.10 UK offices3 Overseas offices

ActivitiesA i lt lAgricultural

Land AgencyBusiness Consultancyy

CommercialResidential es de t a170 Staff employed

CAP Reform

Single Payment

Crop Marketing (Storage)

CollaborationCollaboration

Diversification

Financial Control

CAP ReformCurrently

€3 Billion total subsidy annually y y

€2.3 Billion SFP and related Schemes

Of which,€1 9 Billi id t SFP€1.9 Billion paid out SFP

€400 Million ELS, other Schemes,

CAP Reform TimescaleEU ongoing discussions 2010

A t t t / l 2011Agreement on structure /proposals 2011

Legal papers in place 2012Legal papers in place 2012

2013 – New CAP in place

CAP ReformEU under pressure for food security

L li hi h l l f b idLess reliance on high level of subsidy

More payments into Rural DevelopmentMore payments into Rural Development

Less Red Tape – stricter penalties

Environment to remain

More even distribution of subsidy

Subsidy/Single PaymentAverage English Farmer receives £100/acre (SFP/ELS)

EU F f £35/ t £170/EU Farmers range from £35/acre to £170/acre

CAP Reform will narrow the differenceCAP Reform will narrow the difference

UK to expect lower levels of direct support

Single PaymentCross Compliance

E ll l d i t dEnsure all land registered

Have control of your landHave control of your land

Hedging Single Payment

Crop MarketingSufficient crop storage

U d t di B k MUnderstanding Bank Manager

Market knowledgeMarket knowledge

Access to Risk Management Tools

Understanding Break Even Point

Time

CollaborationKnowledge/Information

StStorage

MachineryMachinery

Labour

Machinery/LabourHelps reduce fixed costs

R d d i tiReduces depreciation

Allows for investment in larger, more efficient machinesAllows for investment in larger, more efficient machines

Bottom line benefit

DiversificationSecure non-farm income

P t t i t k t l tilitProtects against market volatility

Grant FundingGrant Funding

Renewable Energy – Solar PV, Wind, Biomass or AD

Financial ControlKnowing costs of production – break event points for selling crops

Do budget and cashflow

Financial Reporting

M it & AMonitor & Assess

Thank you

Paul WhitePaul White

07768 465 729paul white@brown-co compaul.white@brown co.com

Presentation by:Presentation by:

Jarred WrightPartner - Roythornes SolicitorsPartner - Roythornes Solicitors

th kwww.roythornes.co.uk

Presentation by:Presentation by:

John HayesMinister of State for Further Education,

Skills and Lifelong LearningSkills and Lifelong Learning

And now …. any questions?