Substitution of Copper - Copper Council 9 - Jacobsen.pdf · Source: Dimensions: Dubbel, Taschenbuch...

25

1 Substitution of Copper IWCC Joint Meeting 2013 Tokyo, May 13, 2013

Transcript of Substitution of Copper - Copper Council 9 - Jacobsen.pdf · Source: Dimensions: Dubbel, Taschenbuch...

1

Substitution

of Copper

IWCC Joint Meeting 2013

Tokyo, May 13, 2013

2

Legal Disclaimer IWCC Joint Meeting 2013

The purpose of this presentation is to guide programs

benefiting the copper industry and to provide attendees

with information to make independent business decisions.

3

Substitution of Copper

1. Dimensions of substitution

2. Drivers of substitution

3. Quantitative effects of

substitution

4. Applications under

substitution

5. Options for copper

4 Source: Altrogge: Investition; Wöhe; Betriebswirtschaftslehre

On an industrial scale, most substitutes or services are imperfect

A substitute

What exactly is a substitute?

» is a product or service that satisfies the need that another product or service

already fulfills

» must share at least one particular relationship with the good or service to be

substituted

» can be perfect or imperfect depending on the customer’s satisfaction

» will often stay, even if the driver of substitution has lost importance in the

meantime

5

Complementary goods:

Perfect substitute goods:

Cobb-Douglas function

Leontief function

Imperfect substitute goods:

Asymptote

Due to its unique properties, copper does not have a perfect substitute

Substitute goods or complementary goods?

6

Change in

environment

Stakeholders see substitution differently and position themselves individually

Change in

environment

Realizing Evaluating

and analyzing

Identifying

solutions Commissioning

Improving and

developing

Mines and

captive smelters

Custom

smelters

Fabricators OEMs Manufac-

turers

Consumers

In our industry, substitution takes some time

7

… by which material/system?

» Aluminum

» Plastic

» Superconductors

» Composites

» UCC/Nano composites

» Zinc

» Steel

» Silver

» Gold

» Miniaturization

… in which product group?

» Wires and cables

» Strips and foils

» Sheets and plates

» Sections and bars

» Industrial tubes

» Sanitary tubes

… for which reason?

» Price level

» Price volatility

» Physical properties

» System integration

» Regulations and

standards

» Short-term availability

» Strategic long-term

availability

» Recycling

» Image

But copper could also benefit from new applications to a certain extent

Substitution of copper

Substitution of copper is the result of many trends

8

Substitution of Copper

1. Dimensions of substitution

2. Drivers of substitution

3. Quantitative effects of

substitution

4. Applications under

substitution

5. Options for copper

9

The technical line of defense for copper is

strong, but not invincible

Cu Al Δ

Melting point tsm °C 1083 660 +64 %

Melting heat q kJ/kg 205 397 -48 %

Thermal conductivity λ W/m K 384 220 +75 %

Thermal expansion α 10-6/K 16.8 23.8 -29 %

Thermic capacity c kJ/kg K 0.383 0.896 -57 %

Electrical conductivity κ MS/m 59.1 36.7 +61 %

Density ρ kg/dm³ 8.92 2.7 +330 %

Young’s modulus E GPa 123 71 +73 %

Tensile strength Rm MPa ~235 ~75 +313 %

Elongation A % ~45 ~25 +80 %

Bending fatigue cycles - 500 300 +66 %

Creep modulus Ec GPa high low ~ 80 %

From the technical side, “only” its high density puts pressure on copper

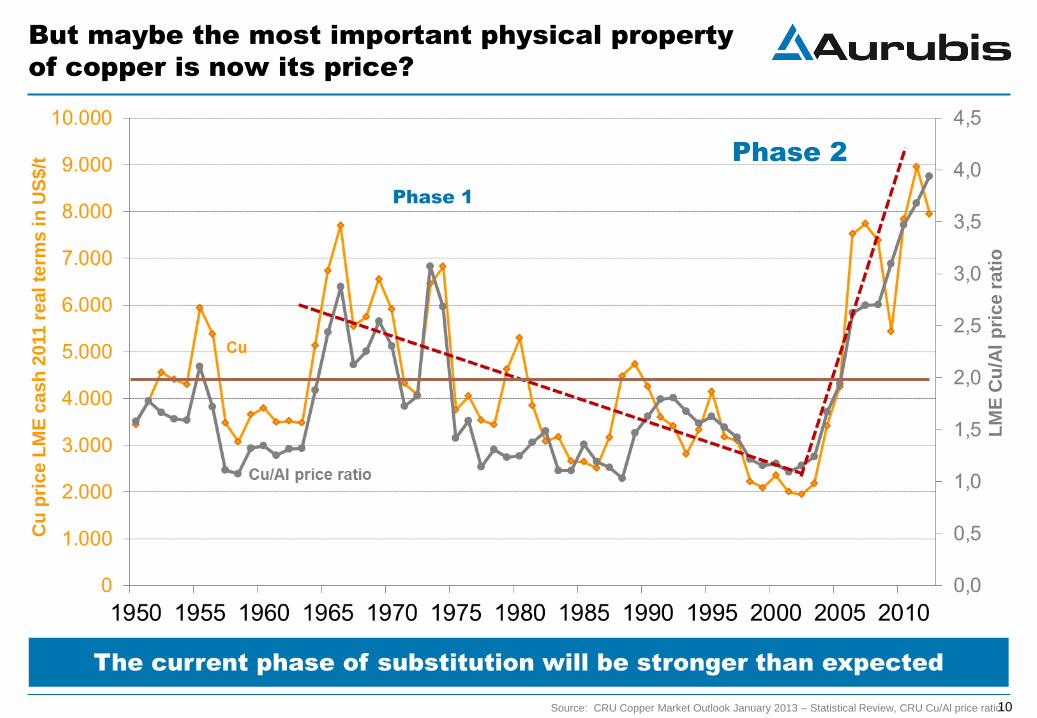

But maybe the most important physical property

of copper is now its price?

10 Source: CRU Copper Market Outlook January 2013 – Statistical Review, CRU Cu/Al price ratio

LM

E C

u/A

l p

ric

e r

ati

o

Cu

pri

ce

LM

E c

as

h 2

011

re

al te

rms

in

US

$/t

The current phase of substitution will be stronger than expected

Phase 1

Phase 2

11

Combination of price, density and conductivity pushes

the current substitution of copper by aluminum

Conductors made of copper are seven times more expensive today. Higher

costs for processing and insulating of aluminum wire do not fully compensate

Source: Dimensions: Dubbel, Taschenbuch für den Maschinenbau; Cu/Al prices: Fast Markets, March 27, 2013

Price Premium

$ 7,590/t + $ 86/t = $ 7,676/t

Value of Cu conductor: $ 10.30

Price Premium

$ 1,904/t + $ 300/t = $ 2,204/t

Value of Al conductor: $ 1.49

A = 2.5 mm²

l = 100 m

mCond = 0.675 kg

A = 1.5 mm²

l = 100 m

mCond = 1.34 kg

Example: Constant load at a current of I = 16 A, ambient temperature: T = 25 °C

Cu Al

12 Source: Scandinavian Copper Development Association, 2013

Moreover, the community is paying more attention:

Is copper antimicrobial or toxic?

» The ecolabel “Nordic Swan” defined “house criteria”: Copper roofs are not approved for

houses, apartment buildings and preschool buildings

» The new environmental program of Stockholm (Sweden, 0.9 mill. residents) does not

allow the installation of copper roofs, facades and tubes if viable alternatives exist.

» The major European landmark project “Royal Seaport” in Stockholm with

10,000 homes and 32,000 workplaces does not allow copper tubes or roofs either.

» Gothenburg (Sweden, 0.5 mill. residents) has set up a similar program setting the

standards for environmentally friendly buildings.

» Malmö (Sweden, 0.3 mill. residents) follows with programs for ecological buildings,

which do not allow the participants to install copper roofs, facades or tubes.

Even if all existing legislative limits are met, copper is facing a ban

13

Substitution of Copper

1. Dimensions of substitution

2. Drivers of substitution

3. Quantitative effects of

substitution

4. Applications under

substitution

5. Options for copper

Global refined copper output has not been

able to follow global GDP growth since 2005

14

Global production (in mill. t/y)

Copper wire rod as a dominant “first use” has developed even more weakly

Source: CRU Copper Market Outlook January 2013 World copper refinery production, CRU Wire and Cable Quarterly – Production of Copper Wire Rod 2008, 2010, 2012

CAGR refined copper: 2.9 %

CAGR copper wire rod: 2.3 % CAGR GDP growth: 3.7 %

In contrast, global refined aluminum output has

grown much more strongly

15

Since 2005 aluminum wire rod has grown five times faster than copper wire rod

Source: CRU World Primary Aluminum Production , CRU Wire and Cable Quarterly Oct 12 and Jan 13 – Production of Aluminum wirerod

CAGR refined aluminum: 5.5 %

CAGR aluminum wire rod: 10.9 % CAGR GDP growth: 3.7 %

Global production (in mill. t/y)

The cumulated substitution effect is significant

In the last 10 years the netted annual losses have added up to 4.3 mill. t/y

Source: Aurubis Intelligence, International Copper Association, Brook Hunt /Wood Mackenzie, CRU 16

Volume (in kt)

17

Asia is going to be the center of gravity; Western markets are stagnating

Copper wire rod demand (in mill. t/y)

Source: CRU Wire and Cable Quarterly, Industry Market Outlook, Jan 2013; Aurubis estimation - Asia = Japan, S. Korea, Taiwan, China, ASEAN

CAGR World Asia

2008 – 2012 1.5 % 5.0 %

2008 – 2015e 2.6 % 4.5 %

2008 – 2018e 2.8 % 4.5 %

2008 – 2025e 3.0 % 4.5 %

Stable growth of copper wire rod markets expected

18

Aluminum wire rod will probably catch up to copper around 2022

Aluminum wire rod demand (in mill. t/y)

Aluminum wire rod demand is speeding up and

moving to the Far East at the same time

Source: CRU Wire and Cable Quarterly, Industry Market Outlook, Jan 2013, Cu/Al price ratio; Aurubis estimation, Asia = Japan, S. Korea, Taiwan, China, ASEAN

CAGR World Asia

2008 – 2012 11.9 % 19.5 %

2008 – 2015e 9.7 % 14.0 %

2008 – 2018e 9.9 % 14.0 %

2008 – 2025e 10.4 % 14.0 %

19

Substitution of Copper

1. Dimensions of substitution

2. Drivers of substitution

3. Quantitative effects of

substitution

4. Applications under

substitution

5. Options for copper

20

Application Risk of substitution Trend

Energy cable LV (< 1 kV) very high nearly saturated

MV (1-66 kV) very high increasing

HV (66-220 kV) high increasing

XHV (220-380 kV) medium starting

Building wire low to medium increasing

Heat/flame-resistant cable very low -

Submarine energy cable low flat

Magnet wire medium increasing

Transformers high increasing

Motors and generators high increasing

Cable for vehicle harnesses high increasing

Civil aviation harnesses medium increasing

Cables/harnesses for military applications low flat

Telecommunications/network cable very high nearly saturated

Local Area Network cable low slowly increasing

Other special cable low flat

Cablemakers are working on substitutes to fulfill their customers’ demand

Many copper wire rod applications are at risk

» The German energy supplier RWE is installing a 10 kV HTSC cable in Essen

(Germany) to replace a 110 kV copper cable. With a length of more than 1 km, this is

the largest HTSC project worldwide.

» This new 10 kV HTSC cable transports five times as much energy (P= 40 MW) than the

substituted 110 kV copper cable using the same cable ducts. Energy losses are

negligible.

» The accompanying current limiters also utilize HTSC.

» Cooling by liquid nitrogen to -200 °C.

» Improved connections to conventional cables.

» 110kV/10kV relay stations not necessary any more.

» Total CAPEX ~ € 13.5 mill.

» HTSC cables are still 2.5 times more expensive than copper cables; break-even

expected 2020 at the latest.

21

10-15 % lower total HTSC system costs in comparison to copper cables

AmpaCity superconductor replacing copper cables

22

Substitution of Copper

1. Dimensions of substitution

2. Drivers of substitution

3. Quantitative effects of

substitution

4. Applications under

substitution

5. Options for copper

23

Copper industry has to reinvent its industrial logic along the whole value chain

“Duck and cover” Arrange

and start to defend

Actively search for

and develop new

applications

» No integrated approach

in a “fragmented

industry”

» Stand-alone measures

to survive, e.g. cost

saving programs

» Waiting for better times,

which will not come

again

» Reduce working capital

» Consolidate portfolio and

footprint, M+A activities

» Coordinate steps to look for

new applications

» Join and align forces,

strengthen associations

» Avoid perception of scarcity

» Understand the logics of

OEMs and manufacturers

in buyer’s markets

» Structured and integrated

product development in

long-term approach

» Increase R&D efforts

» Offer sustainable solutions

featuring strong USP and

societal benefit

Sulking and complaining is not a solution

24

...but if copper does not actively join these trends, its substitution will continue

2012 2025

Growing Energy Scarcity

Changes in Energy Transfer and Distribution

Decentralization of Energy Production

New Propulsion Technologies

Continuing Urbanization

Backshoring

Rebalancing of Global Financial Markets

Growing Global Middle Class

»World population continues to grow:

1950: 2.6 billion

2013: 7.1 billion

2035: 8.5 billion

2050: 9.3 billion (=> stagnation)

»Urbanization will proceed: In 2035

65 % of population will live in cities

»Townspeople need more

infrastructure and especially

conductivity per capita

»Growing middle class means rising

living standards

»Recycling and sustainability will

become more important

Global megatrends offer opportunities …

25

Thank you!

Questions welcome

IWCC Joint Meeting 2013