Subnational Finance in African LDCs - United Nations · Dar es Salaam, Tanzania ... The AAAA...

45

UNCDF | FFDO/UN-DESA Informal Background Paper In preparation for the African Local Finance Expert Group Meeting on The Importance of Strengthening Subnational Finance in African LDCs Dar es Salaam, Tanzania 29 February – 1 March 2016 Implementing the Addis Ababa Action Agenda and the Sustainable Development Goals at the Local Level

Transcript of Subnational Finance in African LDCs - United Nations · Dar es Salaam, Tanzania ... The AAAA...

UNCDF | FFDO/UN-DESA

Informal Background Paper

In preparation for the African

Local Finance Expert Group Meeting on

The Importance of Strengthening

Subnational Finance in African LDCs

Dar es Salaam, Tanzania 29 February – 1 March 2016

Implementing the Addis Ababa Action Agenda and

the Sustainable Development Goals at the Local Level

CONTENTS

(I) Introduction ........................................................................................................................ 1

(II) Challenges in raising subnational revenues ........................................................ 4

(III) Challenges in municipal management ................................................................ 17

(IV) Challenges in accessing long-term finance for capital investments ...... 19

(VI) Entry points for greater international cooperation on municipal

finance ............................................................................................................................. 37

(VI) Bibliography .................................................................................................................. 41

1

(I) INTRODUCTION

With the adoption of the 2030 Agenda for Sustainable Development, the Addis Ababa

Action Agenda (AAAA) and the Paris Agreement, the international community has laid

out a clear vision and road map for achieving sustainable development in all of its three

dimensions - economic, social and environmental.1 All three documents recognize the

imperative to work with local2 authorities and communities to implement the agenda at

the subnational level. Indeed, one of the Sustainable Development Goals (SDGs) is a

subnational objective in itself, as it calls for cities and human settlements to be

“inclusive, safe, resilient and sustainable”. The local dimension permeates other SDGs,

targets and means of implementation, including those on water and sanitation

management, climate change-related planning, sustainable tourism, ecosystem and

biodiversity and the capacity of local communities to pursue sustainable livelihood

opportunities.3

The AAAA commits to fully engage local authorities in the implementation of its global

framework for financing sustainable development and its comprehensive set of policy

actions.4 The AAAA dedicates an entire paragraph to subnational finance, which

promotes greater international cooperation “to strengthen capacities of municipalities

and other local authorities”.5 Moreover, Article 7 of the Paris Agreement recognizes

that climate adaptation is a global challenge faced by all with local and subnational

dimensions.

The emphasis on the local dimension is in no small part the result of the impressive

level of engagement of local authorities at the Addis Conference, the SDG Summit as well

as COP 21 and their preparatory processes.

1 The paper was authored by Daniel Platz (FFDO, UN-DESA). Extensive substantive comments and contributions from Vito Intini, Shari Spiegel, Sam Choritz, Simona Santoro, Tim Hilger and Anisuzzaman Chowdhury are gratefully acknowledged. The views and opinions expressed in this informal background paper are those of the author and do not necessarily reflect those of the United Nations Secretariat or UNCDF. The designations and terminology employed may not conform to United Nations practice and do not imply the expression of any opinion whatsoever on the part of the organizations. All errors and omissions are the sole responsibility of the author. 2 The “local level” refers to any tier below the central government (states, cities, towns, districts, provinces etc…). For the purpose of this paper, it will be used interchangeably with the terms “subnational”, or “sub-sovereign”. “Municipal” refers to cities and towns. 3 See United Nations “Transforming our world: the 2030 Agenda for Sustainable Development” Goal 11, Goal 6.b. 8.9, Goal 12.b, Goal 13.b, Goal 15.9, Goal 15.c. 4 Addis Ababa Action Agenda, para 130. 5 Addis Ababa Action Agenda, para 34.

2

Now that subnational finance6 is firmly placed on the international policy agenda, the

question beckons as to what challenges it faces and what type of actions can be taken at

the local, national, regional and global levels to strengthen it. The financing required to

implement the 2030 Agenda is estimated to be of the order of several trillion dollars per

year.7 The new agenda’s focus on the sub-national level implies that a significant

portion of this financing will be implemented at the local level, in urban, peri-urban and

rural settings.8 Mobilizing sufficient finance for local needs represents a formidable

task.

In that context, the comprehensive approach of the AAAA translates well to the local

level. The Agenda highlights the need to draw upon all sources of finance and puts

forward a policy framework that realigns financial flows with public goals. It calls for

appropriate public policies and regulatory frameworks to help unlock the

transformative potential of people and incentivizes changes in consumption, production

and investment patterns in support of sustainable development.9 Drawing upon all

sources of finance at the local level implies the need to more effectively mobilize

internal (taxes, user fees, land value capture etc.) and external revenue streams

(intergovernmental transfers, ODA), as well as to find ways to unlock private funds in

order to finance large-scale capital investments. A policy framework that realigns

financial flows with public goals in the context of subnational finance implies a well-

coordinated decentralization effort between subnational entities and the central

government, where expenditure responsibilities to reach local development goals are

backed by reliable intergovernmental transfers and fiscal empowerment (e.g., the legal

and technical capacity to levy certain taxes). The principle is commonly referred to as

“finance follows function”, i.e. policy frameworks should empower local governments to

mobilize adequate resources.

Greater insights into the particular challenges the poorest and most vulnerable

countries face in meeting their local expenditure responsibilities remain a prerequisite

6 For the purpose of this paper subnational finance encompasses both revenue generating and borrowing activities of local authorities. 7 United Nations, Report of the Intergovernmental Committee of Experts on Sustainable Development Financing. 8 Rural development is of particular importance in African LDCs, in part because of their predominantly rural populations. Two thirds of the total population of LDCs in Africa live in rural areas, and in only 4(Djibouti, Gambia, Mauritania, Sao Tome and Principe) is the proportion below 50 per cent. Even with continued rapid urbanization, and projected rural population growth, this pattern is unlikely to change substantially by 2030 (UNCTAD, 2015, p.14). 9 United Nations, DESA-Briefing Note on the Addis Ababa Action Agenda.

3

for more effective international cooperation on subnational finance. Least Developed

Countries (LDCs) are countries that exhibit the lowest indicators of socioeconomic

development and face severe structural impediments to growth.10

African LDCs are the main focus of this paper. According to the latest «State of African

Cities» Report11, Africa is undergoing several major transitions: demographic, economic,

technological, environmental, urban and socio-political. Africa’s relative share of the

world’s urban population is also expected to nearly double between 2010 and 2050, and

more than a quarter of the world’s 100 fastest growing cities are in Africa. With the

arrival of approximately 300 million new inhabitants in African cities and towns in the

next two decades, urbanization in LDCs has become one of the critical factors of the

continent’s structural transformation.

Estimates put African cities’ annual financing needs above US$ 90 billion12. Of this

amount, US$ 45 billion could be mobilized from domestic sources of which only US$ 1

billion is estimated to come through own-source revenues from local governments. In

addition, the contribution from various donors is estimated at just US$ 10 billion per

annum.

As a result, African LDCs face a particularly urgent need for improved subnational

financial capacity that could help improve local service delivery and finance local

infrastructure development. They also face greater sets of challenges in all aspects of

national and subnational finance, compared to other country groups. Weak human and

institutional capacities, low per capita income, low productivity and shallow financial

sectors are frequently combined with political instability and high vulnerability to

terms-of trade shocks due to the reliance on a limited number of commodities for

export. At the subnational level, these characteristics may translate into small local

revenue bases, limited financial, expenditure and asset management capacities,

unpredictable and insufficient intergovernmental transfers and little to no access to

private capital. Other political constraints, e.g., insufficient local revenue authority, may

10 The identification of LDCs is currently based on three criteria: per capita gross national income (GNI), human assets and economic vulnerability to external shocks. The latter two are measured by two indices of structural impediments, namely the human assets index and the economic vulnerability index. See http://unohrlls.org/about-ldcs/ 11“Population” Division of the United Nations Department of Economic and Social Affairs (UN DESA), in State of African Cities Report 2014 – UN-Habitat 12 Urban Development Strategy of the AfDB Group, October 2011

4

pose further challenges for subnational finance. The paper argues that putting in place

effective partnerships in support of subnational finance can help overcome these

challenges and support local authorities to meet the growing demands they face to

promote sustainable development through expanded access to essential services and

climate-resilient infrastructure. The ensuing sections provide brief overviews of how

the unique vulnerabilities of LDCs may translate into specific challenges for subnational

finance in terms of revenue generation, municipal management and funding capital

investments. The paper concludes by reviewing entry points for greater international

cooperation on municipal finance.

(II) CHALLENGES IN RAISING SUBNATIONAL REVENUES

The income of local governments comprises local revenues through user fees and

charges, taxes/levies, as well as intergovernmental transfers, sometimes financed or

supplemented by foreign aid.13 These sources may be supplemented by investment

income, property sales, and licenses. User charges and fees are mostly levied where

people pay for the benefits and utilities they receive (e.g. water supply, sanitation,

energy, parking space). At the same time, the municipality typically provides a range of

public goods (police, ambulance, firefighters, streetlights etc.) whose consumption is

not exclusive and whose benefits it cannot directly assign to the individual consumers.

In such cases, taxes are the more appropriate tool as they target the entire community

that stands to benefit from the service.

User charges, fees and licenses

User charges and fees comprise service charges (water, sewerage and parking),

administrative fees (building permits, registration) and business license fees. Local

governments, when setting their tariff structures, must take social justice concerns into

consideration and facilitate access to low-income households. Cross-subsidies, where

richer segments of the population subsidize access to services for the poor, have shown

success in some countries. One popular mechanism for cross-subsidies is a pricing

system, whereby the per unit price of consuming the service rendered increases when

13 Many publications on subnational finance list borrowing as a source of income. This paper treats borrowing separately. Borrowed money is not income unless the loan or debt is forgiven. For example, a debt/income ratio, an important measurement of financial health, does not make sense if income includes debt.

5

more of it is consumed and may even be free up to a designated level. Cross-subsidies

are also possible between sectors. For example, cross-subsidies are frequently used to

reduce or eliminate user charges for health services since these tend to have a

particular detrimental effect on the poor (Lagarde and Palmer, 2008). The elimination

of user charges for health services has led to significantly higher health system

utilization rates. While greater health care is likely to pay large dividends in the future,

including through greater tax revenues, the challenge for local governments is to

replenish the lost revenue in the short and medium term through instruments like

sectoral cross-subsidies, additional taxes or donor contributions.

User charges are typically defined per unit of consumption. They can promote an

optimal level of consumption when the price equals the cost of providing an additional

unit of the service. Some have therefore argued, “(whenever) possible, local public

services should be charged for rather than given away” (Bird 2001). However, getting

prices right is easier said than done, where the infrastructure and capacity to set prices,

measure usage, and collect fees is heavily constrained and where many users live in

abject poverty. Consequently, in a number of LDCs, user charges are frequently set

below costs, infrequently revised and often inefficiently billed.

Whereas economic theory suggests that marginal cost pricing is the most efficient

pricing method, it works only in perfect market conditions where providers have

complete information on the cost of the product, as well as the opportunity cost. More

practical methods include average cost pricing, where expenditures required for

providing a service are divided by the number of consumers or the volume sold; or

average incremental pricing, which calculates how much it would cost to serve an

additional consumer based on the average cost price. Finally, there are multipart tariffs,

similar to those discussed earlier, which include fixed charges for basic consumption

and higher charges for greater consumptions and thus effectively cross- subsidize the

consumption of low-income customers. Frequently, in LDCs, prices for services, such as

water and energy are set administratively (and sometimes not at all) without a clear

pricing strategy. Where a clear pricing strategy is applied, average cost and multi-tariff

bundling are more widespread than marginal cost pricing since these are easier to

calculate and administer (World Bank, 2014).

6

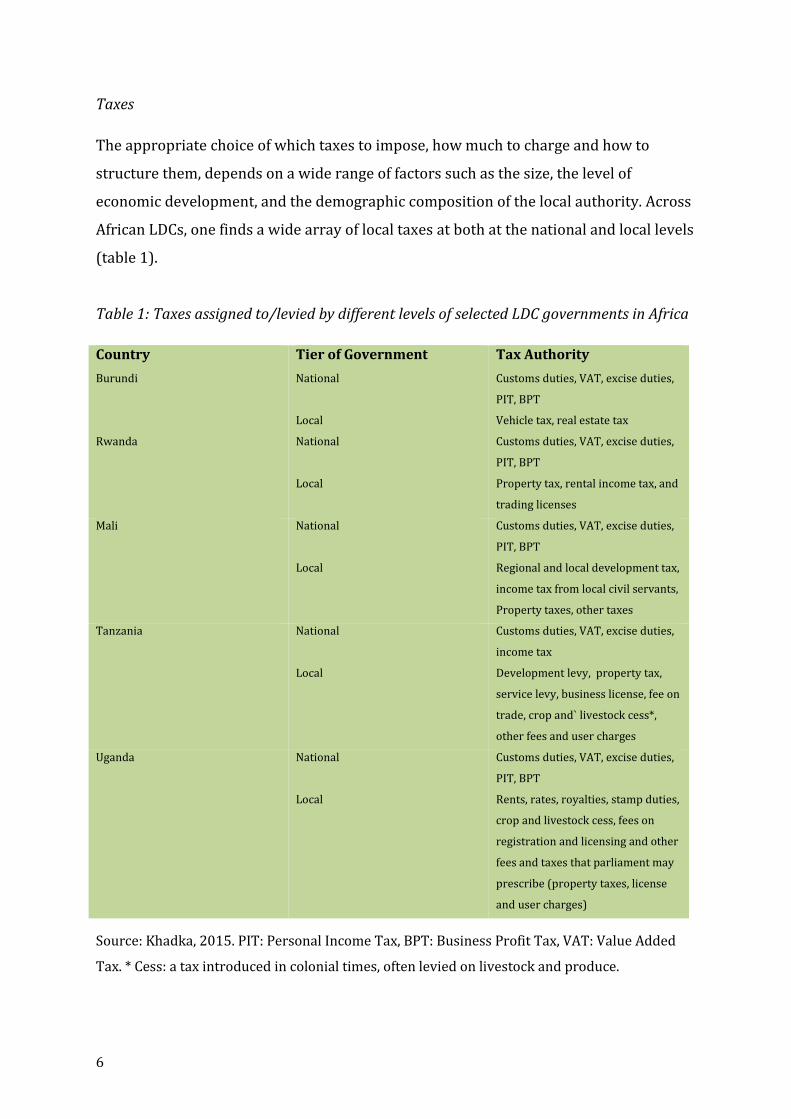

Taxes

The appropriate choice of which taxes to impose, how much to charge and how to

structure them, depends on a wide range of factors such as the size, the level of

economic development, and the demographic composition of the local authority. Across

African LDCs, one finds a wide array of local taxes at both at the national and local levels

(table 1).

Table 1: Taxes assigned to/levied by different levels of selected LDC governments in Africa

Country Tier of Government Tax Authority

Burundi National

Local

Customs duties, VAT, excise duties,

PIT, BPT

Vehicle tax, real estate tax

Rwanda National

Local

Customs duties, VAT, excise duties,

PIT, BPT

Property tax, rental income tax, and

trading licenses

Mali National

Local

Customs duties, VAT, excise duties,

PIT, BPT

Regional and local development tax,

income tax from local civil servants,

Property taxes, other taxes

Tanzania National

Local

Customs duties, VAT, excise duties,

income tax

Development levy, property tax,

service levy, business license, fee on

trade, crop and` livestock cess*,

other fees and user charges

Uganda National

Local

Customs duties, VAT, excise duties,

PIT, BPT

Rents, rates, royalties, stamp duties,

crop and livestock cess, fees on

registration and licensing and other

fees and taxes that parliament may

prescribe (property taxes, license

and user charges)

Source: Khadka, 2015. PIT: Personal Income Tax, BPT: Business Profit Tax, VAT: Value Added

Tax. * Cess: a tax introduced in colonial times, often levied on livestock and produce.

7

Evidence suggests that, in general, there is a positive correlation between the size of the

local government (in terms of its population) and the role of own-source revenues. For

example, taxes and other sources of revenue can account for as little as 9 per cent in

small Brazilian municipalities (less than 5000 people) and over 50 per cent in large

cities. The fact that larger local entities have more institutional capacity to raise revenue

is not surprising, all other things being equal, but where countries face severe

institutional constraints at all tiers of government, as is the case in most LDCs, the

positive correlation may not hold anymore. Indeed, in most large cities in LDCs in Africa,

the correlation is less pronounced, i.e. even large cities are struggling with generating

more than 10 per cent of their revenues through user fees and taxes (World Bank,

2006).

Property taxes

Property and business taxes are generally the most often levied taxes. However, while

property tax revenues can reach up to 5 percent of GDP in developed countries, they are

equivalent to only about 0.6 percent of GDP in developing countries (Bahl and Vasquez,

2007). There are little data for LDCs in Africa, but the share of property taxes to GDP in

LDCs is likely even lower. For example, even in Rwanda, a country, whose tax

administration has much improved in recent years, property tax revenues amounted to

just 0.02 per cent of GDP in 2013-14.14

One of the major challenges with levying property taxes in LDCs is the lack of proper

titles for residential premises and tax exemptions for low-value properties. It is

estimated that less than 10 per cent of African’s land is properly documented

(Byamugisha, 2013). Moreover, given the lack of suitably qualified staff and resources

for local governments in many LDCs, rising land values are not regularly assessed

leading to substantial revenue shortfalls as old property values remain on the books.

Consequently, where property taxes are levied, they often do not keep pace with

economic development. For this reason, some LDCs in Africa have refused to establish

direct property taxes and instead tax only rental income (Cameroon) or apply a

simplified occupancy tax (Burkina Faso). Property taxes also suffer from broader

14 International Centre for Tax and Development, 2014, ”Property tax in Africa: the ‘Cinderella’ of revenue instruments and why it matters for development”

8

challenges that affect other types of national taxes such as low nominal tax rates and

low collection rates.

Where title registration systems and fiscal cadasters (i.e., comprehensive and perpetual

inventories that describe and assess the value of landholdings) are not well developed,

‘street addressing’ (i.e. giving streets names and/or numbers) is a constructive first step

towards determining the tax base and increasing tax revenues. Street addressing allows

locating residents and greatly facilitates municipal service provision. It also helps

enforce the collection of user fees for water and electrical utilities. It is important to see

the building of fiscal cadasters and street addressing as complementary practices.

Indeed, the reconciling of street indices with fiscal registers can lead to substantial local

revenue increases (Habitat III, 2015).15

Business taxes

In economic theory, business taxes at the local level are often sees as inefficient

mechanisms of own source revenue generation It is argued that such taxes may

discourage business formation, have adverse effects on growth and investment and lead

to distorted capital allocation. At the same time, there can be subnational tax

competition that leads to a “race to the bottom” and erodes the tax base and revenues.

However, there is no solid empirical evidence that business taxes have implications on

growth and in practice virtually every country imposes some sort of business tax, either

at the national or local level. Bird (2006) notes there are efficiency, equity and political

arguments that support the case of the local business tax. The efficiency and equity

rationale is captured in the principle of benefit taxation. If firms receive identifiable,

cost-reducing benefits through public sector services, they should pay for the costs

incurred in the provision of such benefits, (e.g. wear and tear from large trucks on a

road or waste disposal expenditures). In this connection, business taxes are efficient in

that they ensure that someone pays for the costs related to providing a particular

service. At the same time, they are equitable and fair in that they ensure that firms pay

for a service rendered by local authorities and not just their citizens. In addition, taxing

larger domestic and foreign businesses or corporations may make political sense since

15 In the context of Sub-Saharan Africa, some non-LDCs like Botswana, Namibia and South Africa have well-developed property markets. Their experience could help African LDCs in their property market reforms.

9

negative externalities, like environmental costs may outweigh positive effects, such as

local job creation or skills transfers, as is often the case with extractive industries. Local

business taxes are also easier to administer and more elastic than property taxes and

therefore a crucial source for expanding infrastructure and local services.

In many LDCs, business taxes are widely used. In West African LDCs, the “patente”, a

differentiated set of fixed tax rates that is based on size of premises, type of business

and number of employees has made up for a sizable share of local revenues (figure 1).

In East Africa, Tanzania levies a local business tax named ‘City Service Levy’ at a fixed

percentage on the firm’s turnover. In the rest of Anglophone Africa, local business

licensing generates between 5 and 30 per cent of local government own revenues in

urban councils (Fjeldstad, and Heggstad, 2012). More research is needed on how local

business taxes should be imposed, structured and administered in order to maximize

their revenue potential and effectiveness. Such research must also acknowledge that

corporate tax evasion remains a major challenge for imposing local business taxes,

especially in the case of transnational companies that may apply methods such as

transfer or trade mispricing to deceit national local tax authorities.16

16 See Report of the High Level Panel on Illicit Financial Flows from Africa, 2015, commissioned by the

AU/ECA Conference of Ministers of Finance, Planning and Economic Development.

10

Figure 1: Composition of local tax revenue in West African LDCs (Averages for 1995-2008)

* The global tax (impôt synthétique) is levied on small business and combines taxes on commercial and industrial profits, business licenses and value added tax.

Source: IMF, 2015.

Surcharges

Surcharges are a form of subnational “piggybacking” on national or regional taxes, like

income taxes. For local surcharges a higher level of government defines the tax base,

collects both the tax and the surcharge set by subnational governments and remits the

surcharge revenue to the local government. While the national government collects the

tax, surcharges are clearly local taxes in that local governments are responsible for

imposing the tax and spending the revenues.

This approach avoids the problems that occur when subnational jurisdictions define

their tax base in conflicting ways, use different apportionment formulas, and administer

0

10

20

30

40

50

60

Benin

Senegal

Togo

Cote D'Ivoire

Mali

Niger

11

the tax in different ways. For example, two local authorities may try to impose taxes on

the same company since there are different opinions as to where and in which

subnational jurisdiction the firm operates. In such a case, it is more practical for higher

levels of governments to define the tax base and forward a share of the revenues to the

local authorities. However, surcharges are not a substitute for but rather a complement

to intergovernmental transfers, since they do not provide for vertical or horizontal

redistribution among subnational jurisdictions. Looking ahead, more data and research

is needed on how and to which extent local surcharges are used effectively in African

LDCs.

The formulation of the most welfare-enhancing combination of local and central

governments taxes is a politically difficult balancing act. Another key challenge for

central governments is to provide incentives to local governments to collect all the taxes

they are supposed to collect. While some central government fund transfers have been

linked to a reform agenda, there has been little improvement in own source revenue

collection in most cities (Habitat III, 2015). Frequently, politics get in the way of

empowering local governments to raise their own revenues (box 1).

Box 1: Local governments and revenue generation in Lesotho-Legally empowered but

politically constrained

Even where municipalities are legally empowered to raise revenues and borrow,

political inertia can stand in the way of fiscal empowerment, as was the case in Lesotho.

Lesotho is divided into ten districts, which are further subdivided into 80 constituencies

that consist of 129 local community councils. The prime agencies for collecting local

revenues at the district level are community and urban councils. The Lesotho Local

Government Act (1997) legally empowers councils to raise their own revenues. Such

revenues include taxes, rates, and charges, licenses and permits, fines and penalties and

property taxes and other commercial income generated from the sale of district

councils’ assets including natural resources. The law provides that “the Minister shall

publish in a gazette a list of items” from which councils may collect revenues by way of

tax or levy of charge. However, the ministry has never published such information.

Consequently, district councils have had no own source of revenue, which remains a

major source of frustration. The councils only act as collection agents for the central

12

government. If a new source of revenue is identified, the local authority is obliged to

notify the central government, which will provide guidance on the rates and their

application. The role of the councils is limited to recording and reporting revenue

receipts and to remit local revenues to the central government. According to local

authorities in Lesotho, the lack of power and autonomy over sources of revenues has

clearly limited their incentive to maximize revenue collections. With support from the

World Bank, UNCDF, UNDP, EU and GIZ, the Governments has formulated and passed a

new decentralization policy in February 2014. The policy proposes local fiscal

autonomy with zero tolerance for corruption and strict adherence to laws. The capital

city Maseru serves as a pilot for the new programme. In how far the new policy will be

expanded to other districts will depend on many factors, including political commitment

from the central government.

Source: expert interviews.

Intergovernmental transfers

There are no subnational governments in the world that can fully function without a

certain level of intergovernmental support. In practice, finance often does not follow

function and central governments across the globe give local authorities more

expenditure responsibilities than those can finance from their own revenue sources.

Generally, greater capacity to generate their own revenues make subnational

governments in developed countries less dependent on support from higher tiers of

governments than those in developed countries. Consequently, resource flows from

higher to lower tiers of governments average 70-72 per cent of local government

funding in developing countries and 38-39 per cent in developed countries (Alam,

2014).

The traditional rationale for intergovernmental transfers is the objective for a welfare

maximizing government to reallocate resources between richer and poorer jurisdictions

in order to reduce both horizontal (same tiers of government) and vertical (different

tiers of governments) imbalances, and to correct for externalities. The actual drivers for

intergovernmental transfer can vary, however. Public finance literature explores factors

13

that are shaped by equity and efficiency considerations such as the correction for

vertical and horizontal imbalances. Public choice theory highlights how transfers can

become tools for political influence. Frequently, electoral concerns determine the

distribution of fiscal resources to local jurisdictions (Boex and Martinez-Vazquez, 2005).

Political economy research focuses on how intergovernmental transfers are shaped by

political influence through the impact and bargaining power of political interest groups.

There is robust empirical evidence that local governments with higher political

representation per capita benefit from greater intergovernmental transfers (Wright,

1974, Porto and Sanguinetti, 2001, Khemani, 2007, Caldeira, 2011).

The impact of intergovernmental transfers on local revenue generation remains under

debate. Some have argued that large unconditional intergovernmental grants lead to

lump-sum tax reductions or lower the incentives for local governments to collect fees

and taxes, thus ‘crowding out’ own source revenue mobilization. Others argue that most

fiscal transfers are spent on the provision of public goods and services, increasing local

economic development and tax compliance, and consequently, ‘crowd in’ local tax

revenues. Studies that highlight the crowding out effect mostly focus on more developed

countries with relatively well-developed fiscal systems and significant own source

revenue generation (Kalb, 2010; Zhuravskaya, 2000).

However, such capacity is highly constrained in African LDCs. In cases where local

capacity to generate own-source revenue is weak, intergovernmental transfers are a

crucial lifeline and may further crowd in local revenue generation. For example,

evidence suggests that in Tanzania, a 1 per cent increase in intergovernmental transfers

leads to an extra 0.3-0.6 per cent increase in own source revenue generation for local

government authorities (LGAs) (Masaki, 2015). Moreover, intergovernmental transfers

are often the only regular source of local income for reasons of political interference in

own source revenue generation. In many LDCs, local governments are frequently

dependent on central government approval for taxes, fees and charges they wish to

impose. In certain cases, local governments may wait for years or even decades to get

such approvals (see Box 1).

Smoke (2015) argues that intergovernmental transfers make sense as part of smart

division of responsibilities between the central and local government based on their

14

core advantages and competencies. In this connection, the author highlights that

‘central governments have inherent advantages in generating revenues and local and

regional governments have inherent advantages in providing certain key services,

invariably necessitating intergovernmental transfers’. At the same time, LRGs must be

able to raise an adequate share of the resources to (i) reduce demands on central

budgets, (ii) create a fiscal linkage between benefits of local services and the costs of

providing them, and (iii) help repay loans on long-term capital investments (Smoke,

2015).

Intergovernmental transfers in African LDCs

Intergovernmental transfers are crucial for all African LDCs, given their low capacities

of own source revenue generation. High levels of intergovernmental transfers can be

observed in most of Anglophone LDCs in Africa. However, as shown in chart 1,

Francophone LDCs stand out for their exceptionally low level of intergovernmental

transfers. This seems to make little sense given the high average ratios for developing

countries and the fact that challenges in raising local revenues are even bigger for LDCs

than in developing countries. The low levels of transfers may be the result of sectoral

policies of the central governments that leave little resources for local authorities, thus

limiting resources and functions of local authorities and compromising the

decentralization process (UCLG, 2009).

15

Chart 1: Intergovernmental transfers in per cent of total local revenues in selected

Francophone (red) and Anglophone (blue) African LDCs

Sources: for Anglophone LDCs: Munawwar (2014) , Jibao (2009), Masaki (2015),

Caldeira (2011); for Francophone African LDCs (averages from 1995 -2008), IMF

(2015).

Overall, chart 1 illustrates widely divergent sizes of intergovernmental transfers in

LDCs in Francophone and Anglophone Africa. Most Anglophone LDCs receive the

majority of their income through intergovernmental transfers. Yet, they still face

enormous challenges in meeting their fiscal needs, as transfers are often not adequate

or reliable.

In Francophone African LDCs, the share of total local resources to total public resources

reveals some of the lowest ratios in the world (IMF, 2015).

0

10

20

30

40

50

60

70

80

90

100

16

Yet, in these cases lower central government support is not met with adequate

increases in revenue generation. For example, in the case of Senegal, revenue at the

local level has increased but remains at a mere 6 per cent of the central tax revenues.

Local resources remain insufficient to provide local basic public services and horizontal

fiscal imbalances have become a problem. The resources of the ten poorest communes

represent 1 per cent of the resources of the five richest ones (Caldeira, 2011)17. In Mali,

local taxes generate insufficient revenue and rely on a wide range of obsolete taxes,

which are particularly difficult to collect.

The fact that African LDCs with widely different transfer/total revenue ratios continue

to face similar development challenges at the local levels suggests that there is no direct

link between the level of fiscal decentralization and local development. Whether the

major source of subnational income is intergovernmental transfers or own source

revenues does not matter if the total income is inadequate .People will bear the

consequences in terms of poor quality and access of local service delivery. Fiscal

decentralization does not make sense where own-source revenue generation cannot fill

the gap. To make matters more complicated, international financial institutions have

frequently put pressure on LDCs to reduce intergovernmental transfers in an effort to

reduce central government deficits. Such a recommendation must be weighed carefully

against the adverse effects of lower transfers on access and quality of basic services,

especially where the capacity for own source revenue generation is low.

Questions for further research and discussion:

What determines the effective choice, combination and design of appropriate revenue

tools? How can local authorities improve revenue collection? What are the right policies to

ensure affordability to pay? How should local authorities take other factors into account in

the policy design when choosing the right tax and user fee revenue policies (e.g. efficiency,

equitability, impact on the distribution of income, environmental impact, and political

considerations)? How can the coordination of different government levels be improved?

How can intergovernmental transfers improve the capability of subnational governments

17 Senegal is divided into eleven regions (règions) which are subdivided into 67 communes, 43 communes d’ arrondisements which are further divided into 320 communautès Rurales (Caldeira, 2011).

17

to deliver public services and also strengthen the institutional capacity to generate

revenues?

(III) CHALLENGES IN MUNICIPAL MANAGEMENT

Municipal management is relevant for all activities related to subnational finance. In the

literature, municipal management refers to financial, expenditure and asset

management. All three types of municipal management are closely inter-related.

The four tenets of financial management include budgeting, accounting, reporting and

auditing. Expenditure management is somewhat broader in that it focuses on whether

funds are appropriately spent and monitored and whether information is available for

proper planning and budgeting. Its basic tasks are performed within a cycle that begins

with planning of resources and expenditures and moves towards allocating and

transferring funds, controlling and executing expenditures, and, eventually, evaluating

financial performance. Whereas financial management is largely the business of the

treasurer and its staff, sound expenditure management requires a broader and more

inclusive approach. For example, planning resources and expenditures and monitoring

of results requires the direct involvement of the Mayor and the council, whereas line

departments will execute expenditures in their sector.

Many developing countries are facing the challenge of relatively large shares of

administrative expenditures compared to what is spent on service delivery. This may

decrease the willingness of citizens to pay taxes since they would rather have the bulk

of the budget spent on visible service improvements. Moreover, when it comes to

capital expenditures, municipalities in LDCs often face weak local financial management

skills, a shallow financial sector and weak investor base, as well as low capacities of

implementing agencies like construction companies or construction monitoring firms.

In light of these challenges, there is a general consensus among experts and

practitioners that improved financial and expenditure management can increase the

efficiency and cost-effectiveness of municipal service delivery and functions, including

in LDCs. For example, in the case of Tanzania, there is strong evidence that councils with

better financial and expenditure management practices, generally achieve better local

financial results, even if exogenous factors like population size, the poverty rate,

18

urbanization, the level of central government support and other political and

socioeconomic factors are taken into consideration (Boex and Muga. 2009).

Municipalities can benefit from a forward-looking approach that builds on a medium-

term expenditure framework that relies on improved expenditure management systems

for accounting, internal controls, cash management, procurement, and contract

management. In addition, well-targeted tariffs can include the use of demand-side

subsidies to support the poor or other communities (World Bank, 2014).

Financial and expenditure management can further benefit strongly from participatory

and gender-sensitive approaches. Participatory budgeting processes can ensure that the

right financing priorities are set. They can help in better identifying investments of

value to poor localities and women. In addition, they can assist in forging consensus on

the appropriate distribution of costs among clients, as well as on adequate user fee and

tax levels to fund necessary investments.

Asset management refers to municipal management of both physical (land,

infrastructure, equipment) and financial assets (investments, ownership, bank

deposits). Asset management is important since it has a direct impact on the quality of

services delivered. Investments into physical capital such as water supply systems,

sewerage systems, roads and power plants require long-term maintenance. If they are

neglected the quality of services will suffer. At the same time, financial assets need to be

properly managed to help ensure long-term financial sustainability at the local level.

However, due to capacity constraints, asset management has often been neglected in the

developing world and very few municipalities have a designated focal point for this

important task.

Questions for further research and discussion:

Are the instructive examples of how local authorities in the region have ensured effective

monitoring and analysis of both operating and capital expenditures? How should they

manage subnationally owned physical assets (land, buildings, infrastructure, and vehicles

and equipment) in support of subnational finance for sustainable development? How can

they ensure long-term planning of both capital investment projects and financing? How

should they implement transparent and competitive procurement? How can they ensure

strong capacities for contract management?

19

(IV) CHALLENGES IN ACCESSING LONG-TERM FINANCE FOR CAPITAL

INVESTMENTS

Increased urbanization and political decentralization have led to enormous municipal

infrastructure financing needs around the globe. The need for capital to finance projects

targeted at implementing the SDGs, including the mitigation of or adaptation to climate

change has further promoted the idea to tap the domestic capital market for green

infrastructure investments through municipal debt issuances. However, debt issuance

by municipalities in LDCs will be challenging. Accessing long-term capital is already a

challenge for central governments in African LDCs (see table 2). Only 7 out of 48 LDCs

have raised funds (domestically and internationally) through government bonds within

the last decade.

Table 2: List of LDCs in Africa with sovereign bond issuances, 2006-2014

LDC Accumulated amount of sovereign bond

issuance 2006-2014

Angola 1.0 USD Billion

Ethiopia 1.0 USD Billion

Madagascar 0.85 USD Billion (ODI)

Rwanda 0.4 USD Billion

Senegal 1.2 USD Billion

United Rep. of Tanzania 0.6 USD Billion

Zambia 1.7 USD Billion

Sources: Sy (2015), Tyson (2015).

Raising long-terms finance poses even greater challenges at the subnational level,

especially when it comes to issuing bonds. Moreover, central government bonds provide

important pricing benchmarks and without them investors will have a more difficult

time in pricing subnational debt. Building local capital markets, where national debt can

be bought and sold by domestic investors on secondary markets, is therefore an

important policy objective for countries interested in strengthening the market for

subnational debt. Focusing on local capital markets is also crucial to prevent foreign

20

exchange rate risks. Municipalities are even less equipped to take on such risks than

central governments, as their entire revenues are generated in local currency.

A wide range of other factors influences a government’s capacity to access long term

finance, as well as the investor’s willingness to invest into local capital. This section

focuses on challenges that lend themselves to immediate and concrete policy

interventions. On the issuer (municipal) side, it emphasizes the importance of capacity

for project development, debt service and management, as well as use of credit

enhancements. On the investor side, it highlights the importance of a diversified (but

not necessarily deep) financial sector, issuer familiarity and confidence, and a suitable

regulatory and legal environment (Platz, Painter 2010).

Strengthening local capacities in support of long-term finance

Infrastructure projects need to be carefully planned, engineered, and costed to be

successfully debt financed.18 This requires up-front investment in project development

services from market demand analysis to detailed engineering design. Most

municipalities and public utilities in LDCs do not have the resources to pay for this

initial work. They may also lack the experience managing project development. The lack

of funds and management capacity means most cities cannot translate their need for

infrastructure into investible and good projects. To assist in overcoming this problem,

specialized “project development facilities” can be created. A project development

facility can take many forms and perform different roles depending on the need. In

smaller or centralized countries, the facility may be national in character. In larger or

decentralized countries, the facility may operate at a regional or state/provincial level.

For instance, in the early 2000s, bilateral donors supported the Municipal Infrastructure

Investment Unit (MIIU) in South Africa, which then successfully provided financial,

technical, and managerial support to municipalities and public utilities.19 The project

development facility may also help to carefully structure and market the loan

instruments (e.g., a sub-sovereign bond) to meet domestic investor community needs.

Greater project development capacities should be part of a national sustainable

18 This section draws heavily from Platz, Painter (2010). 19 Lessons learned from the MIIU project are summarized here - http://pdf.usaid.gov/pdf_docs/Pdacj977.pdf.

21

development strategy, which focuses on the importance of infrastructure plans, as

emphasized in the Addis Ababa Action Agenda.

The capacity to support subnational debt depends on the ability of the borrower to

maintain a reliable surplus of revenues over expenditures. As previously discussed, the

revenue potential of taxes in LDCs is often low. Consequently, strengthening the

revenue base and improving municipal management are fundamental prerequisites for

sustainable market borrowing via banks or bonds.

Once a municipality is deemed fit to take out long–term loans, it should avoid

potentially costly risk exposure to exchange rate fluctuations driven by external factors.

Local revenues are earned in local currencies. Consequently, debt issuances should be

geared towards the domestic investor community and issued in local currency. Different

forms of credit enhancements can further help sub-sovereign issuers lower default risk.

Credit enhancement mechanisms can take on the form of revenue cushions for payback

(e.g., “sinking funds” in the US, “federal tax-sharing grants” in Mexico, or “bond service

funds” in India), partial or 100 per cent external guarantees for bond repayment (e.g.,

USAID partial guarantees for repayment of the first Johannesburg bond), or the use of

pooled financing. A well-structured bank loan or bond may make use of several credit

enhancement mechanisms at the same time.

Pooled financing could be particularly promising in developing countries with

heterogeneous issuers. In this scenario, a credible intermediary, such as the national or

state government collects the borrowing needs of a group of municipalities and issues a

single debt instrument backed by a diversified pool of loans to municipal utilities and

covered by a debt service fund established before the bond is issued. This technique

offers investors access to a diversified, geographically dispersed portfolio of borrowers,

thus limiting exposure to narrowly focused credit problems. It is worthwhile to explore

whether a carefully calibrated pooled project finance approach combined with technical

assistance and credit enhancements, could help generate the municipal resources in

LDCs. In that context, some have proposed that local governments could follow a pooled

project finance approach and work with donors and private sector companies to

identify and put together investible infrastructure projects that can be financed by local

banks and capital markets on a non-recourse basis (Bond et al, 2012).

22

Strengthening the investor base

Some evidence suggests that financial sector composition matters more than relative

size for the emergence of a municipal debt market (Platz, 2009). Policy interventions

can promote further financial sector diversification. However, first and foremost, the

potential of municipal financing providers depends on the confidence in the system as a

long-term store of value. Policies that help build active government and corporate bond

markets provide critical investment opportunities that can serve as benchmarks for

investors interested in sub-sovereign bonded debt. Moreover, central governments

should consider the strengthening of national development banks. National

development banks play a crucial role as they can lend to municipalities directly under

favorable conditions (both in terms of rates and maturities) when no one else does.

Their investments into local authorities will enable those to build up their credit

histories in the long-term. When municipalities are ready to access the markets,

national development banks (as well as regional or multilateral development banks)

can also build investor confidence by underwriting, guaranteeing or investing into

municipal debt, including securities.

Another challenge relates to the lack of investor familiarity with the risk profile of local

capital investments. Rating agencies can help overcome this information gap. After the

world financial and economic crisis, rating agencies have come under increased

scrutiny. As a result, world leaders have called for increased competition, as well as

measures to avoid conflict of interest in the provision of credit ratings.20 Such measures

are certainly necessary and would strengthen the rating industry. Yet at the local level,

the major challenge is not related to how these agencies conduct their business but

their lack of engagement in the first place. Indeed, even in developed countries outside

the US (where over 12 000 municipalities are rated by S&P alone) few subnational

entities have request ratings from either of the three major rating agencies, which

together hold more than 90 per cent of the global market share. There is no rating for an

LDC from any of the three major rating agencies at the sub-national level (figure 2). The

relatively low number of subnational ratings worldwide can be explained by the fact

that most municipalities in developed countries do not access bond markets and rely on

20 Addis Ababa Action Agenda, para 110.

23

intergovernmental transfers and long-standing relationships with local banks. For

subnational entities in LDCs and low-income countries, ratings are simply not

affordable, as the major agencies are not active in these countries.

The number of subnational ratings further decreased in developing countries after the

world financial and economic crisis. That decline may be due to a loss of confidence in

the major rating agencies, less demand at the local levels due to the direct adverse

impact of the crisis on local finances as well as decreased interest of rating agencies in

emerging market and developing economies.

However, a healthy and competitive local rating industry could play a crucial role in

marketing subnational debt to investors in LDCs. Domestic investors in LDCs, where

subnational entities attempt to tap private finance for capital investments for the first

time, are typically not familiar with subnational debt issuers and ratings may be a ‘sine

qua non’ for their engagement. One of the major reasons these agencies have not rated

local authorities in LDCs is the extraordinary costs of developing a national rating scale

and adapting the rating methodology to data available in the country. As a result, initial

fees may be in the range of several hundred thousand dollars, despite relatively small

issuances. Consequently, even creditworthy local authorities in LDCs cannot afford to

pay for ratings.

Here, international development agencies can play a critical role in lowering the entry

barrier for rating agencies by paying for the first few municipal credit ratings so that the

first issuers do not have to bear the costs. Such a rating may be a confidential one that

allows municipalities to get an independent assessment of their financial marketability

without deterring potential investors (see Box 2). Indeed, it is strongly advisable to

have confidential ratings at the earlier stages as public negative ratings may do a lot of

harm in the long term for municipalities that seek to increase investor confidence.

Ideally, donors would focus their efforts on supporting the growth of local rating

agencies. Increased competition and greater issuer familiarity are important benefits of

widening the market for local rating agencies. At first, new linkages between local and

international agencies could increase the reputational capital of domestic ratings

companies. After some time and with sufficient reputational capital, local agencies can

act more independently. Once a local industry develops, fees may decrease dramatically,

24

Over recent years, a few regional rating agencies have emerged in Africa and gained

reputational capital with investors, such as the West African Ratings Agency

(established in 2005) and Bloomfield Financial (established in 2007) joining the ranks

of older agencies, such as Agusto and Co. (1992) and the Global Credit Ratings Company

(GCR). Dakar (see Box 2) and Kampala in Uganda have been among cities in African

LDCs that have received high ratings from local agencies. Kampala received an A in the

long term form GCR, its highest global rating. The high rating resulted from significant

progress the Kampala Capital City Authority (KCCA) has made in expanding its rates

and fees base, including through an improved property registry, and licensing taxis and

other businesses. Combined with improved debt collection these important steps led to

a revenue increase of 80 per cent from 2012 to 2014.21

21 Daily Monitor Uganda, “KCCA gets highest global credit rating”, 20 May 2015. The Kampala Capital City Authority was established through the Kampala City Act in 2009, which removed the authority of the city council to govern. The Kampala Capital City Authority (KCCA) is led by an Executive Director (not the Mayor) appointed directly by the President. The improvement in financial management performance came therefore with a certain trade-off in terms of citizen engagement in the election of city authorities.

25

Figure 2: Number of local authorities worldwide that have received ratings from at least one of the three major global agencies, by country and income group (2009 and 2015)

Sources: Information provided by Fitch, Moody's, S&P. Note, in the US (not included in the figure) over 12000 municipalities are rated by one of three major agencies.

0

20

40

60

80

100

120

140

160

180

200A

rgen

tin

a

Au

stra

lia

Au

stri

a

Bel

giu

m

Can

ada

Cro

atia

Cze

ch R

epu

bli

c

Est

on

ia

Fra

nce

Ger

man

y

Gre

ece

Hu

nga

ry

Ital

y

Jap

an

Sou

th K

ore

a

Lat

via

Lit

hu

ania

New

Zea

lan

d

No

rway

Po

lan

d

Po

rtu

gal

Ru

ssia

n F

eder

atio

n

Slo

vak

Rep

ub

lic

Spai

n

Swed

en

Swit

zerl

and

Un

ited

Ara

b E

mir

ates

Un

ited

Kin

gdo

m

Bel

aru

s

Bo

snia

an

d H

erze

go

vin

a

Bra

zil

Bu

lgar

ia

Co

lom

bia

Ecu

ado

r

Kaz

akh

stan

Mac

edo

nia

Mal

aysi

a

Mex

ico

Per

u

Ro

man

ia

Serb

ia

Sou

th A

fric

a

Tu

rkey

Bo

liv

ia

Mo

rocc

o

Nig

eria

Uk

rain

e

2009

2015

High Income

Upper-Middle Income

Lower-Middle Income

26

The proper legal and regulatory environment can promote the development of the

municipal debt market. Effective judicial frameworks, including a government

bankruptcy framework (chapter 9 in the US) helped sustain the municipal bond market

in the US by protecting the rights and obligations of creditors and debtors at the sub-

national level. Moreover, debt ceilings, introduced in the earlier stages of the US

municipal bond markets, have helped keep municipal debt in check. However,

important exceptions to debt limits were made for essential revenue-generating public

improvements, like water supply systems. Overly stringent credit ceilings should not

impede the development of the municipal debt market, which can channel productive

investment to providing essential local services of municipalities that would otherwise

have no access to long-term finance.

Other less market oriented type regulations may also help the development of the

municipal debt market in LDCs. For example, the Reserve Bank of India is obliged to

invest 21.5 per cent of assets into government-owned securities. Finally, in some

countries, mandatory provisions for municipal revenue cushions (“master trusts”) and

mandatory issuer ratings have promoted investor interest in municipal bonds and

increased access of municipalities to long term bank loans. Regulatory changes that

enhance the creditworthiness of the issuer and promote the local rating industry are

therefore important reform measures to deepen the market for sub-sovereign debt.

Box 2: How Dakar (almost) issued the first municipal bond in a least developed country

Dakar’s experience in (almost) getting a municipal bond to the financial market

provides invaluable lessons for other cities. The reason the bond has not yet been sold is

due to a last-minute intervention by the ministry of finance. However, getting to the

point where Dakar is technically ready to raise market resources and overcome the

long-term finance challenges discussed in this section, has been the result of a concerted

effort of a talented local municipal finance team and targeted and well-coordinated

donor support. First, through a consultative process with a wide range of stakeholders,

including district leaders and NGOs, the construction of a marketplace for more than

4,000 street vendors was identified as the bankable project the bond would fund. It was

envisaged that revenue for the bond would come from affordable fees to street vendors

relocating their business to the hall. A municipal finance management team was put in

27

place to get the city’s finances in order. The team could build on a track record of

solvency, since Dakar has been a reliable creditor to commercial banks, the French

Development Agency and the West African Development Bank since 2009. Moreover,

political stability also helped build investor confidence. Efforts by the management team

were further guided by a confidential rating from Moody’s, which provided an

independent assessment of their work and pointed to areas of further improvement.

Credit enhancements were crucial as well, including a 50 per cent partial risk guarantee

from USAID as well as the setting up of separate fund by Dakar earmarked to pay the

debt. All of these factors allowed Dakar to get a rating of BBB+, a middle-tier ranking

that qualifies as ‘investment grade’ from Bloomfield investment, a West African rating

agency. The sale of the bond would also draw on a diversified financial sector since

Dakar planned to place it on the Bourse Régionale des Valeurs Mobilières, a common

securities market that allows institutional and other investors from 14 Francophone

countries with common currencies to buy debt without foreign exchange rate risk.

However, the last minute objections from the Ministry of Finance points to the

challenges a large number of countries face in ensuring a political environment suitable

for subnational finance innovations.

Source. www.citiscope.org, expert interviews.

Should municipal bonds be on the donor agenda in African LDCs?

As of late, municipal bonds have received renewed attention in the international

development community as an effective means to mobilize additional resources for

local development (see example in box 2). However, whether they are a realistic

pursuit, is subject to debate. For an informed discussion, it is beneficial to look at how

common and successful these instruments have been how around the world.

The mechanisms of market credit for subnational governments vary widely across the

globe. The US boasts a USD 3.7 trillion municipal bond market22 where even the

smallest of towns have raised millions of dollars in bond issuances. A market of such

22 Data from Securities Industry and Financial Markets Association Website (accessed January 2016).

28

size remains unique in the world. Indeed, municipal bonds are not the predominant

source of finance in most developed countries. Outside the US, most states, cities and

towns that access the financial market for credit do so through bank loans, often from

government-owned financial institutions, and banks, such as development banks, with

which they have a long-standing relationship. In middle and low-income countries,

subnational access to capital markets is even more limited and applies to selected larger

cities at best. Many local authorities do not access private or public credit at all and rely

entirely on capital grants from the central governments to fund large-scale investments.

A cursive look at the BRICS, the group of the most advanced emerging markets, confirms

the immature stage of municipal bond markets around the developing world. The BRICS

country with the biggest potential for municipal bonds is China. After a subnational

borrowing crisis in the early 1990s, municipalities were not allowed to take out direct

credit. As a result, a plethora of semi-autonomous local government investment vehicles

emerged that borrowed on behalf of local authorities. Local government debts issued

through these financing vehicles amounted to 18 trillion yuan ($2.9 trillion) in 2014,

more than a quarter of China's GDP. Alarmed by this amount and set to bring

subnational borrowing out of the shadows, a handful of cities, including Beijing, were

authorized to issue 100 billion yuan of bonds in 2014. Some estimate that China's

municipal bond market could grow significantly, but as of now it is still small and the

major challenge is to curb local government debt.23

India has a longstanding history of municipal bonds. In 1998, Ahmedabad became the

first Indian city to sell municipal bonds to finance infrastructure improvements. Yet, in

the past decade and a half only 25 municipal additional bonds have been issued.24

In Brazil, the central governments authorized 21 states to borrow up to 60 billion ($25

billion) from 2013 through 2014, a move that ended a ban on municipal debt that dated

back to a 1997 after a subnational debt crisis required a federal bailout. However, only a

year after the ban was lifted it was reinstated after two large international banks

provoked a central governments backlash by collecting a federal government guarantee

23 Wall Street Journal, “China Places Cap on Local Government Debt”, 30 August 2015. 24 Data from Reserve Bank of India Website (accessed January 2016).

29

and charging the state of Minas Gerais more than if Brazil would have sold its own

sovereign bonds (collecting $140 million in fees in the process).25

In South Africa, municipal debt makes up less than two per cent of bonds listed on the

Johannesburg Stock Exchange, with only four metropolitan areas – Johannesburg, Cape

Town, Pretoria and eThekwini – able to access the market (albeit with government

guarantees). 26 In Russia, the volume of municipal bond market volume amounted to 0.5

trillion rubles, less than one per cent of its GDP.

As most of the economic powerhouses outside the OECD countries have only gradually

entered the municipal bond market and have done so at a deliberate pace (perhaps to

avoid pitfalls, i.e. federal bailouts, from the past) it comes as no surprise that municipal

bonds in poorer countries are far and few between. For example, there is no municipal

bond floating the market in Africa outside of South Africa, Nigeria and Cameroon.27

The experience in Dakar (box 2) shows that central government buy-in and sustained

support remains crucial when embarking on the ambitious project of a municipal bond.

The example also illustrates that with a common goal in mind and well-coordinated

donor support, even cities in the least developed countries can come a long way in

improving their finances through dedicated efforts to build fiscal responsibility and

creditworthiness. However, a more general goal of improving access of local

governments to more market based borrowing principles is perhaps more attainable in

most LDCs. For example, donors could provide incentives for local governments to

improve their capacity so that they can begin to borrow, initially through special

mechanisms like performance-based grants and subsidized lending and later on more

market-based terms. Ideally, this would help local governments develop borrowing

practices over time and empower them to fund their capital investment needed to meet

their sustainable development objectives. (Smoke 2015)

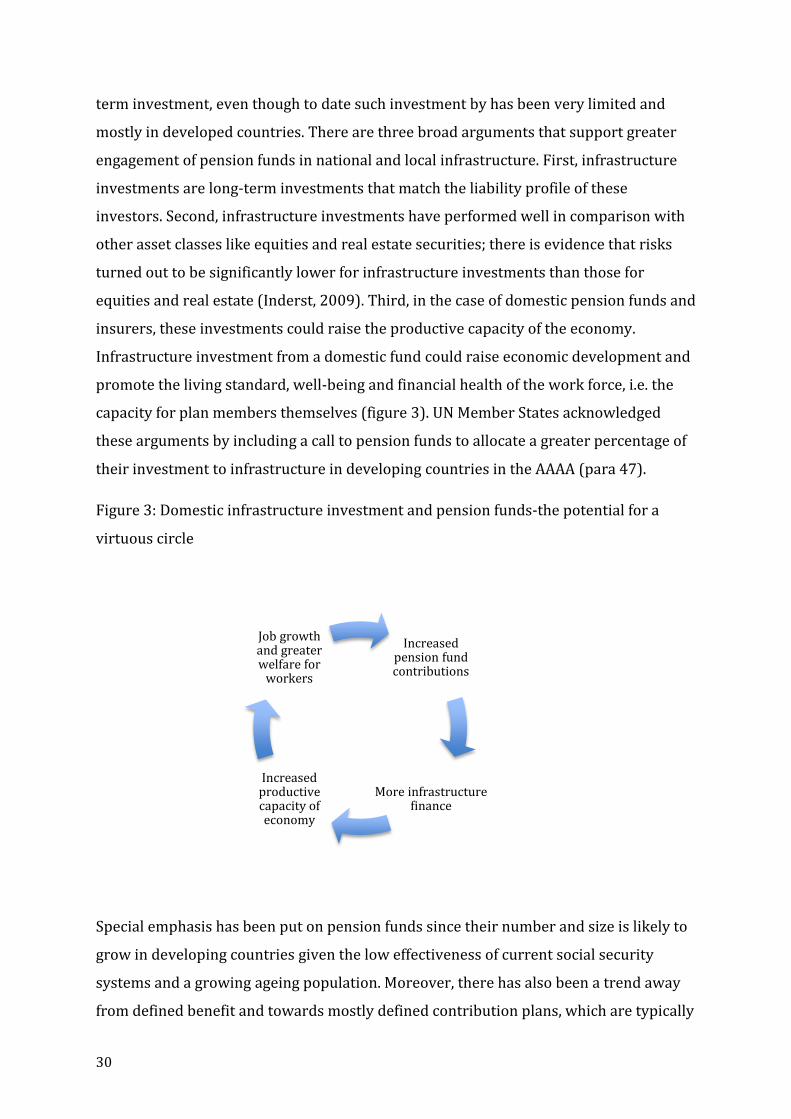

Institutional investors - an untapped source for subnational infrastructure investment?

As of late, much debate has been centered on the potential of institutional investors

(e.g., pension funds, insurers, Sovereign Wealth Funds) as potential sources for long

25 Bloomberg, “Brazil Halts Muni Market as Banks Collect $140 Mln Fees”, 21 August 2013. 26 www.africanbondmarkets.org, accessed January 201. 27 Several municipal and state bonds have been issued in Nigeria and one municipal bond was issued in Cameroon (Douala).

30

term investment, even though to date such investment by has been very limited and

mostly in developed countries. There are three broad arguments that support greater

engagement of pension funds in national and local infrastructure. First, infrastructure

investments are long-term investments that match the liability profile of these

investors. Second, infrastructure investments have performed well in comparison with

other asset classes like equities and real estate securities; there is evidence that risks

turned out to be significantly lower for infrastructure investments than those for

equities and real estate (Inderst, 2009). Third, in the case of domestic pension funds and

insurers, these investments could raise the productive capacity of the economy.

Infrastructure investment from a domestic fund could raise economic development and

promote the living standard, well-being and financial health of the work force, i.e. the

capacity for plan members themselves (figure 3). UN Member States acknowledged

these arguments by including a call to pension funds to allocate a greater percentage of

their investment to infrastructure in developing countries in the AAAA (para 47).

Figure 3: Domestic infrastructure investment and pension funds-the potential for a

virtuous circle

Special emphasis has been put on pension funds since their number and size is likely to

grow in developing countries given the low effectiveness of current social security

systems and a growing ageing population. Moreover, there has also been a trend away

from defined benefit and towards mostly defined contribution plans, which are typically

Increased pension fund contributions

More infrastructure finance

Increased productive capacity of economy

Job growth and greater welfare for

workers

31

privately managed pension funds. This trend may further raise the growth prospects for

pension fund assets. Data on the size of African pension funds is only partially available

but numbers suggest a significant gap between LDCs and non-LDCs, with the notable

exception of Tanzania (figure 4). Data on the asset allocation of pension funds is not

readily available for Sub-Saharan Africa. However, available evidence suggests that

investment practices of African pension funds traditionally favour short-term

government securities, bank deposits and real estate. Those pension funds in countries

with the shallowest financial sectors invest most of their assets in large illiquid assets.

Information on pension fund investment into different types of infrastructure projects

remains sparse since infrastructure is not listed as a separate asset class on their

balance sheets. Yet, recent information and anecdotal evidence point to a low ratio.

Global estimates suggest that pension funds invest less than 1 per cent of their deposits

into listed and unlisted infrastructure.28 That ratio is likely to be even lower in LDCs

where the risk profile of infrastructure investments is usually much higher than in

developed countries. Yet, recent years have seen some modest headway. While most

pension funds in Africa have not directly invested into infrastructure projects, half a

dozen funds have invested in Harith General Partners Ltd., a Johannesburg-based

infrastructure fund that holds $630 million and has been involved in more than 70

African projects.29

Figure 4: Pension Fund Assets under Management in African Countries

Country AUM in US$ million Botswana 6,000 Burundi 13 Ghana 2,600 Kenya 7,280 Namibia 9,960 Nigeria 25,000 Rwanda 557 South Africa 322,000 Tanzania 3,800 Uganda 1,259 Zambia 1,609

Source: Commonwealth Secretariat, 2014. Countries in italics are LDCs and are reported in Riscura, 2015.

28 OECD, Global Pension Statistics. 29 Wall Street Journal, “African Pensions Funds Invest in Infrastructure Projects”, 7 May 2015.

32

In addition to a conducive regulatory environment, more reliable data on the size, risk,

return and correlations of infrastructure investments in African LDCs would go a long

way in incentivizing pension funds and other institutional investors to allocate more of

their assets in infrastructure investments at the international, national and local levels.

PPPs and capital investments

Subnational capital investments can also be financed through public-private

partnerships (PPPs). PPPs can take on many different forms with many levels of risk

exposure. For example, in the case of management contracts, the private partners have

very limited or no capital expenditure. On the other hand, in the case of a Design, Build,

Own, Operate, Transfer (BOOT) contract, the private partners are responsible for the

design, building, operation and financing of a capital asset. In such a PPP, private

partners receive payment from either the local government (at regular intervals) or

user charges, or both for delivering the services.

Figure 4 presents variations of PPPs in terms of distribution of responsibilities between

the public and private sectors, asset ownership and the associated degree of public

sector risk. It is important to note that the chart does not say anything about the

relationship between different PPP contracts and their ultimate benefit to the public.

For example, while greater private sector responsibility will reduce public sector risk

exposure by default, a badly designed PPP of any type can carry significant risks for the

public in terms of reduced coverage, poor quality of service, or contingent fiscal

liabilities (Jomo, Chowdhurry, Sharma, Platz, 2016). Figure 4 also proposes to

distinguish between “core PPPs” and related arrangement. “Core attributes” for PPPs

have the following characteristics (World Bank, 2012):

a) A long-term agreement between a government entity and a private company, under

which the private company provides or contributes to the provision of a public

service.

b) The private company receives a revenue stream—which may be from government

budget allocations, from user charges, or a combination of the two—that is dependent

on the availability and quality of the contracted service. The agreement therefore

transfers risk from the government entity to the private company, including service

33

availability or demand risk.

c) The private company must generally make an investment in the venture, even if it is

limited, e.g., to working capital.

d) In addition to budget allocations, the government may make further contributions,

such as: providing or enabling access to land; contributing existing assets; or

providing debt or equity finance to cover capital expenditures. The government may

also provide various forms of guarantee that enable risk to be shared effectively

between the government and the private company.

e) At the end of the PPP contract the associated assets revert to government ownership.

34

Figure 4: Variations of PPPs and distribution of risk

Source: Jomo, Chowdhurry, Sharma, Platz (2016)

35

The wide range of contractual arrangements paired with the lack of clarity and

variations in definition make it difficult to generalize findings about PPPs.

Paulais (2012) notes that in Africa most PPPs in urban areas that involved local

governments were not successful. Local PPPs remain especially rare in Africa and are

concentrated in only a few countries. The example of the failed water PPP in Dar es

Salaam shows the complexities involved in ensuring a successful PPP (Box 3).

Box 3: Water supply and sewerage in Dar es Salam – A local PPP gone wrong

In 2002 most of the water produced by the public Dar es Salam water supplier DAWASA

was lost due to leaks, non-metered connections and illegal usage. Water supply was

sporadic in most areas. Moreover, less than 10 per cent of the urban population was

connected to a sewerage system. As a result, the city suffered from outbreaks of water-

borne diseases. To improve services, the city actively looked for private partners to

enter into a PPP. Following six years of negotiations with private companies and two

failed bidding processes the German/British company BGT was finally a awarded a