Submission 37 - Regional Banks (AMP | Bendigo Bank | Bank ...

69

LEVELLING THE PLAYING FIELD IN RETAIL BANKING SUBMISSION TO THE PRODUCTIVITY COMMISSION REGIONAL BANKS SEPTEMBER 2017 COMPETITION

Transcript of Submission 37 - Regional Banks (AMP | Bendigo Bank | Bank ...

1 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

LEVELLING THE PLAYING FIELD IN RETAIL BANKINGSUBMISSION TO THE PRODUCTIVITY COMMISSION

REGIONAL BANKSSEPTEMBER 2017COMPETITION

2 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

22 September 2017

Hello Peter

Regional Banks - Submission to the Productivity Commission We are pleased to provide this submission to the Productivity Commission’s Inquiry into Competition in the Australian Financial System. Our submission reflects the collective views of Australia’s regional banking sector, represented by Bendigo Bank, Bank of Queensland, Suncorp, AMP Bank and ME Bank.

This inquiry provides the right forum to develop reforms that will support a productive, competitive and sustainable banking sector in this country. Smaller banks bring vital competition and choice to the market, and drive innovation which ultimately produces better customer outcomes.

While the Financial System Inquiry (FSI) made a number of positive recommendations, which have improved the competitive neutrality of the banking sector, the playing field is still tilted in favour of the major banks and more needs to be done. Our submission highlights our assessment of five key structural failings that are stifling competitive neutrality, and fair and sustainable competition:

The artificial funding cost advantages which the major banks continue to enjoy, even after accounting for the introduction of the new Major Bank Levy;

The risk weight disparity that remains between the major banks (that use the internal ratings based approach to risk weighting) and smaller banks (that use the standardised approach to risk weighting), which is particularly pronounced in the case of low risk lending;

Macroprudential rules which have effectively ‘locked-in’ market share at current levels, leaving smaller banks no room to challenge the already dominant position of major banks;

Limited transparency and disclosure around mortgage aggregators which limits the capacity for consumers to make informed decisions; and

The unprecedented pace and volume of new regulation and compliance which is having a disproportionate impact on smaller banks.

As you will see, we have made five recommendations for addressing these structural failings. The underlying premise of our submission is to align the needs of consumers, the community, and shareholders, and make recommendations that are based on realistic and sound policy principles that seek to level the playing field and to

Mr Peter Harris AO Chairman Productivity Commission e-mail: [email protected]

2

ensure competitive tension, while preserving the stability of the system. Reforms in these areas will help support a sustainable, competitive and diverse banking sector in Australia, which will undoubtedly deliver better outcomes for customers.

We are also strongly supportive of the ABA’s calls for closer scrutiny of the shadow banking sector, which continues to compete free of many regulations and APRA oversight. We believe this issue is fundamental to ensuring all market players are able to compete more fairly.

We look forward to working with the Productivity Commission to further explore the issues raised in this submission.

[Signoff]

Sally Bruce Group Executive AMP

Mike Hirst Managing Director Bendigo Bank

Jon Sutton MD & CEO BOQ

Jamie McPhee CEO ME Bank

David Carter CEO, Banking and Wealth Suncorp

22 September 2017

Hello Peter

Regional Banks - Submission to the Productivity Commission We are pleased to provide this submission to the Productivity Commission’s Inquiry into Competition in the Australian Financial System. Our submission reflects the collective views of Australia’s regional banking sector, represented by Bendigo Bank, Bank of Queensland, Suncorp, AMP Bank and ME Bank.

This inquiry provides the right forum to develop reforms that will support a productive, competitive and sustainable banking sector in this country. Smaller banks bring vital competition and choice to the market, and drive innovation which ultimately produces better customer outcomes.

While the Financial System Inquiry (FSI) made a number of positive recommendations, which have improved the competitive neutrality of the banking sector, the playing field is still tilted in favour of the major banks and more needs to be done. Our submission highlights our assessment of five key structural failings that are stifling competitive neutrality, and fair and sustainable competition:

The artificial funding cost advantages which the major banks continue to enjoy, even after accounting for the introduction of the new Major Bank Levy;

The risk weight disparity that remains between the major banks (that use the internal ratings based approach to risk weighting) and smaller banks (that use the standardised approach to risk weighting), which is particularly pronounced in the case of low risk lending;

Macroprudential rules which have effectively ‘locked-in’ market share at current levels, leaving smaller banks no room to challenge the already dominant position of major banks;

Limited transparency and disclosure around mortgage aggregators which limits the capacity for consumers to make informed decisions; and

The unprecedented pace and volume of new regulation and compliance which is having a disproportionate impact on smaller banks.

As you will see, we have made five recommendations for addressing these structural failings. The underlying premise of our submission is to align the needs of consumers, the community, and shareholders, and make recommendations that are based on realistic and sound policy principles that seek to level the playing field and to

Mr Peter Harris AO Chairman Productivity Commission e-mail: [email protected]

22 September 2017

Hello Peter

Regional Banks - Submission to the Productivity Commission We are pleased to provide this submission to the Productivity Commission’s Inquiry into Competition in the Australian Financial System. Our submission reflects the collective views of Australia’s regional banking sector, represented by Bendigo Bank, Bank of Queensland, Suncorp, AMP Bank and ME Bank.

This inquiry provides the right forum to develop reforms that will support a productive, competitive and sustainable banking sector in this country. Smaller banks bring vital competition and choice to the market, and drive innovation which ultimately produces better customer outcomes.

While the Financial System Inquiry (FSI) made a number of positive recommendations, which have improved the competitive neutrality of the banking sector, the playing field is still tilted in favour of the major banks and more needs to be done. Our submission highlights our assessment of five key structural failings that are stifling competitive neutrality, and fair and sustainable competition:

The artificial funding cost advantages which the major banks continue to enjoy, even after accounting for the introduction of the new Major Bank Levy;

The risk weight disparity that remains between the major banks (that use the internal ratings based approach to risk weighting) and smaller banks (that use the standardised approach to risk weighting), which is particularly pronounced in the case of low risk lending;

Macroprudential rules which have effectively ‘locked-in’ market share at current levels, leaving smaller banks no room to challenge the already dominant position of major banks;

Limited transparency and disclosure around mortgage aggregators which limits the capacity for consumers to make informed decisions; and

The unprecedented pace and volume of new regulation and compliance which is having a disproportionate impact on smaller banks.

As you will see, we have made five recommendations for addressing these structural failings. The underlying premise of our submission is to align the needs of consumers, the community, and shareholders, and make recommendations that are based on realistic and sound policy principles that seek to level the playing field and to

Mr Peter Harris AO Chairman Productivity Commission e-mail: [email protected]

2

ensure competitive tension, while preserving the stability of the system. Reforms in these areas will help support a sustainable, competitive and diverse banking sector in Australia, which will undoubtedly deliver better outcomes for customers.

We are also strongly supportive of the ABA’s calls for closer scrutiny of the shadow banking sector, which continues to compete free of many regulations and APRA oversight. We believe this issue is fundamental to ensuring all market players are able to compete more fairly.

We look forward to working with the Productivity Commission to further explore the issues raised in this submission.

Sally Bruce Group Executive AMP

Mike Hirst Managing Director Bendigo Bank

Jon Sutton MD & CEO BOQ

Jamie McPhee CEO ME Bank

David Carter CEO, Banking and Wealth Suncorp

22 September 2017

Hello Peter

Regional Banks - Submission to the Productivity Commission We are pleased to provide this submission to the Productivity Commission’s Inquiry into Competition in the Australian Financial System. Our submission reflects the collective views of Australia’s regional banking sector, represented by Bendigo Bank, Bank of Queensland, Suncorp, AMP Bank and ME Bank.

This inquiry provides the right forum to develop reforms that will support a productive, competitive and sustainable banking sector in this country. Smaller banks bring vital competition and choice to the market, and drive innovation which ultimately produces better customer outcomes.

While the Financial System Inquiry (FSI) made a number of positive recommendations, which have improved the competitive neutrality of the banking sector, the playing field is still tilted in favour of the major banks and more needs to be done. Our submission highlights our assessment of five key structural failings that are stifling competitive neutrality, and fair and sustainable competition:

The artificial funding cost advantages which the major banks continue to enjoy, even after accounting for the introduction of the new Major Bank Levy;

The risk weight disparity that remains between the major banks (that use the internal ratings based approach to risk weighting) and smaller banks (that use the standardised approach to risk weighting), which is particularly pronounced in the case of low risk lending;

Macroprudential rules which have effectively ‘locked-in’ market share at current levels, leaving smaller banks no room to challenge the already dominant position of major banks;

Limited transparency and disclosure around mortgage aggregators which limits the capacity for consumers to make informed decisions; and

The unprecedented pace and volume of new regulation and compliance which is having a disproportionate impact on smaller banks.

As you will see, we have made five recommendations for addressing these structural failings. The underlying premise of our submission is to align the needs of consumers, the community, and shareholders, and make recommendations that are based on realistic and sound policy principles that seek to level the playing field and to

Mr Peter Harris AO Chairman Productivity Commission e-mail: [email protected]

Dear Mr Harris

CONTENTSCONTENTS 4EXECUTIVE SUMMARY 5LIST OF RECOMMENDATIONS 7INTRODUCTION 81 CONTEXT 91.1 Historical overview 91.2 Summary of Murray Report Key recommendations 161.3 Reflectiononpressures/conditionsleadingtoGovernmentcallingforPCinquiry 181.4 Observations/reflectionsontermsofreference 192 COMPETITION 212.1 Definition,marketstructure,newentrants 212.2 What constitutes sustainable competition 222.3 Efficiencyandcapitalformation 232.4 Competitiveneutrality(barriers/issues) 252.5 Marketpowerandcustomer/consumerchoice/sovereignty 252.6 Innovation/technology 262.7 Regionalbankconclusiononcompetition 263 DATA: MARKET SHARE, PROFITS, MARGINS 273.1 Marketshare/trendanalysis 273.2 International comparison 323.3 Bank/non-bankmarketshare 333.4 Marketsharebysegment/product 343.5 Domestic/globaltrends 353.6 Domesticmarkets:Herfindahl–HirschmanIndexestimates 393.7 Fundingcostsandmargins 404 INDIVIDUAL REGIONAL BANK BUSINESS MODEL/S 484.1 Regionalbanksandconnectiontocustomer/community/diversity 484.2 Alignmenttocustomerinterest 524.3 Regionalbankssetthe“competitivefrontier”whilemajorsachievehigherROE’s 524.4 Growingbutcrowdedoutbyregulatoryarbitrage 525 KEY POLICY ISSUES/RECOMMENDATIONS 535.1 TBTF/Levy 535.2 Possiblelevydesignchanges 555.3 Capital/RWA 575.4 Macroprudentialcomplexity 625.5 Broker(verticalintegration) 635.6 Regulatoryburden 64CONCLUSION 65REFERENCES 66APPENDIX 1: Terms of Reference 68

5 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

EXECUTIVE SUMMARYAustralia’sfinancialservicessystemistheenvyofthedevelopedworld.Ourbankscontinuetobethebackboneofournationaleconomy,whichhasgrownfor27consecutiveyears,defyinginternationaltrends,drivingstrongemploymentandultimatelyimprovingthestandardoflivingforAustralians.AkeyingredientofAustralia’seconomicsuccesshasbeentheresilienceandstrengthofourbankingsectorwhichhaswithstoodmarketshocksanddisruption,particularlytheGlobalFinancialCrisis.However,regionalbanksbelievetheeconomyisbeingheldbackandAustralianconsumersaresubstantiallydisadvantagedbycharacteristicsofthecurrentsystem,whichareinhibitinginnovationandfaircompetitionandcreatinganunevenplayingfield.ThehighlyconcentratedAustralianbankingsystemhasdevelopedasaby-productofapolicyorthodoxythathaslargelyfavouredstabilityovercompetitionandconsumerchoice.Regionalbanksstronglycontendthatthesystemcanhaveanappropriatelevelofstabilityand,atthesametime,allowforfaircompetitioninordertoachievebalancedoutcomes.Thisisultimatelyinthe best interests of consumers and the economy. Theonlysustainablecompetitivemodelisonewhichensurescompetitiveneutrality.Thatis,asysteminwhichtherulesareneutraltothesizeandcomplexityofamarketplayer.Withalevelplayingfield,thesuccessofindividualplayerswoulddependupontheextentandqualityoftheirservicetocustomers.Incontrast,itisarguablethatthecurrentlackofcompetitiveneutralityallowssomeinstitutionstoleveragescaleadvantagesdespiterecentdemonstrableflawsin consumer outcomes.Regionalbankscompetefiercelyformarketshare,butareconstrainedinrespecttosomeproductsandservicesandthisimpactstheeasewithwhichcustomerscanswitchbetweenfinancialinstitutions.Regulatorypolicysettingshaveallowedthebankingsectortobecomeincreasinglyconcentrated,andthishashadconsequencesforcustomersandtheeconomyingeneral.Overthefiveyearsto2016,Australia’sfourmajorbankswereclosetothemostprofitableintheworld.Dependingonthedefinitionofthemarket,theyholdupto85%marketshareoftotalassetsheldbydeposit-takinginstitutions,upfrom75%just10yearsago.Infact,since2007,themajorbankshaveimprovedtheirpositioninallproductmarkets:

• Shareoftotaldomesticresidentassetshasgrownfrom64%to79%;• Totaldeposits,61%to77.3%;• Householddeposits,68%to80%;• Businessdeposits,70%to78%;• Householdcreditcards,80%to82%;• Housinginvestmentloans,77%to85%;and• Housingowner-occupied,75%to81%.

Duringapproximatelythesametime,thenumberofAuthorisedDeposit-takingInstitutions(ADIs)inAustraliahasmorethanhalvedfromover200to95.Regionalbankswillremainonthecompetitivefringewhilethemarketisdominatedbythecommercialdecisionsandthelargelyhomogenousbusinessmodelsofthebigfourbanks.WhiletheFinancialSystemInquiry(FSI)madeanumberofpositiverecommendations,whichhaveimprovedthecompetitiveneutralityofthebankingsector,theplayingfieldisstilltiltedinfavourofthemajorbanksandmoreneedstobedone.

6 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Inparticular,therearefivefundamentalareasthatrequirepolicyreformifwearetorealiseatrulycompetitivesectorandaddresswhatundoubtedlyremainsanunevenplayingfield.Theyare:

1. Further policy reform is needed to reduce the artificial funding cost advantages enjoyed by the major banks.WhiletherecentMajorBankLevyhasreducedthisadvantage,itonlyrecoupsasmallproportionoftheoverallcreditratingupliftenjoyedbythemajors,andfurtherreform should be considered.

2. Further reform of risk weights is needed, to address the significant gap that still exists between the capital requirements of the major banks and standardised banks. While there hasbeensomeriskweightnarrowingfollowingtheFSI,thegapremainssignificant,andisparticularlystarkforloanswiththelowestrisk.

3. APRA should engage with regional banks to design macroprudential rules that better balance macro outcomes such as stability, without undermining banking competition. One option would be for APRA to give greater policy weight to minimum capital requirements. MacroprudentialrulessetbyAPRAhaveeffectively‘locked-in’marketshareofloanbooksatcurrentlevels,leavingsmallerbankswithnoroomtochallengethealreadydominantpositionofmajorbanks.

4. Mortgage aggregators and brokers, owned by major banks should publicly report on the proportion of loans they direct to their owners.Whilewedonotsuggestthatmajorbanksshouldberestrictedfromowningbrokernetworks,wedobelievethatwherethisoccurs,itshouldbemanagedinanopenandtransparentwaytoensurecustomersareabletomakefullyinformed decisions.

5. Before any new regulations are introduced, greater consideration should be given to the impacts on smaller banks. Theunprecedentedpaceandvolumeofnewregulationandcompliancehasadisproportionateimpactonsmallerbankswhichstiflessustainablecompetition.

TheregionalbanksalsosupporttheABA’ssubmissiontotheProductivityCommissioncallingongreaterregulationfortheshadowbankingsector,whichwebelieveisfundamentaltoensuringallmarketplayersareabletocompetefairly.AstrongbankingsystemisgoodforallAustralians.Smallerbanksbringvitalcompetitionandchoicetothemarketanddriveinnovation,whichultimatelyproducesbettercustomeroutcomes.It is vital that competition in the sector not only be fair but productive and sustainable.Thebottom-linetestmustbe:whatisgoodforcustomersisgoodfortheeconomy.

6 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

7 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

LIST OF RECOMMENDATIONS

Recommendation:A. RegionalBankssupporttheGovernment’slevyonthemajorbanksandMacquarieasameansofpartlyaddressingthe“toobigtofail”fundingadvantage.Asthelevyonlyrecoupsaproportionofthe“toobigtofail”fundingbenefit,furtherpolicyinterventionstoreducethebenefitshouldbeconsidered. 56

Recommendation:B. Regionalbanksadvocatefurtherreformofrisk-weightsettingasperthesetofkeyprinciples. 61

Recommendation:C. APRAshouldengagewithregionalbankstodesignmacroprudential rules that better balance macro outcomes and bankingcompetition,andconsidergreaterpolicyweightbeinggiventominimumcapitalrequirements. 62

Recommendation:D. Mortgageaggregatorsandbrokersownedbymajorbanksshouldpublicly(andregularly)reportontheproportionofloansthey direct to their owners. 63

Recommendation:E. Thatbeforeanynewregulationsareintroduced,greaterconsiderationshouldbegiventotheimpactsonsmallerbanks. 64

7 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

8 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

INTRODUCTIONThissubmissionhasbeenpreparedbyBendigoandAdelaideBank,BankofQueensland(BOQ),MEBank,SuncorpBank,andAMPBank.Thefivebankscollectivelyrepresenttheperspectiveof‘regionalbanks’.TheneedforaregionalbanksubmissionstemsfromthedesireoftheseinstitutionstomakeapolicycontributionwiththeaimofensuringahealthyandsustainablefutureforAustralia’sfinancialsystem,withaparticularfocusonthebankingsector.Acompetitive,multi-tieredbankingsectoristhebestmodeltoguaranteeAustralianconsumersandbusinesseswillbeabletoaccessinnovativeandbettervaluefinancialproductsandservicesintothefuture.Amulti-tieredbankingsysteminwhicheachtierbringsadifferentperspectiveandvigorouslycompetesforcustomers,onalevelplayingfield,willensureconsumerbenefitsareprotectedandenhanced.TheregionalbankingsectorhasconsistentlydeliveredabetterserviceforallAustraliansasreflectedbysuperiorcustomersatisfactionandtrustratings.Theregionalbanksbringessentialcompetitivetensiontothemarketthroughanextensiveandcompleterangeofqualityproductsandservicesforconsumers,businessesandregionalcommunities.Regionalbanksprovidegenuineandcrediblechoiceforcustomersandthereisaclearlinkbetweenthebanks’performanceandgoodcustomer outcomes.RegionalbanksviewthislinkascriticalforAustralianconsumersandthelong-termcontributionofthebankingsystem.Ensuringgenuinecompetitiveneutralityiskeytothisoutcome.TheregionalbanksbelievetheprimaryaimofthisCompetitionInquiryistoensuretheend-usersoffinancialproductsarethecentralfocus.Bankingsystemdesignmustidentifywhatisbestforthemumsanddads,businessesandeverydayAustralianswhorelyonsafe,efficientandinnovativeservices:tosavemoney,purchaseahouse,startabusinessandcarryoutalltheothertransactionsthatpeopleneedabankingsystemtodo.Thebankingsystemhasservedthemarketovertime.Whileothersectorsofthefinancialsystem,suchassuperannuationfunds,mayplayanincreasedroleintheprovisionofcapitaltotheeconomyinthefuture,thebankingsystemwillcontinuetoplayasignificantandcriticalroleintheintermediationofcapitalandprovisionofefficientpaymentsystems.Regionalbankswillalsocontinuetocontributetothisprocessbyprovidingcompetitivetensioninthedeliveryofqualityproductsandservicestoconsumers,smallbusinessesandregionalcommunities.TheGlobalFinancialCrisis(GFC)isthemainbackdroptotheProductivityCommission’s(PC’s)CompetitionInquiry.Thecrisisisapivotaleventintheeconomicandsocialhistoryofmanycountries.WhiletheAustralianeconomyandfinancialsystemprovedrelativelyrobust,theGFChasledtosignificantchangestothemotivationsandactionsofconsumers,businesses,financialinstitutionsandGovernment.Inturn,thesehavere-shapedmuchofthecompetitiveandregulatorylandscape.UpuntiltheGFC,arelativelylevelplayingfieldexistedforlargebanks,regionalbanks,foreign-ownedbanks,creditunions,buildingsocietiesandnon-ADIs.

9 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

1 CONTEXT1.1 HISTORICAL OVERVIEWThefinancialsectorhasgrownconsistentlysincethe1970s.WhereastraditionallymanufacturinghasbeenAustralia’slargestindustry(asassessedbygrossvalueadded),financialserviceshasemergedasAustralia’smostimportantindustry.Grossvalue-added(GVA)measurestheextenttowhichanindustryusestheresourcesoflabourandcapital.Itisequivalenttothedollarvalueofthecostofwages,profitsandtaxation.Manufacturinghasdeclinedsteadilysincethe1970sascanbeseeninFigureA. This chart traces howthedeclineofmanufacturingisreplacedbytheincreasingimportanceofthefinancialsector.Financehasincreasedinrelativesizefrom4.28%oftotalGVAtothatofnearly9%today.

FIGUREA

GROSS VALUE ADDED%ofGDP

Source:UnderlyingdatafromABS.CalculationsandvisualisationbyBenchmarkAnalytics.

8.80%

5.98%

14.10%

4.28%

0.10

1977

Value

Financial and insurance serviceManufacturing

0.05

0.00

1982

Year to Date

1987 1992 1997 2002 2007 2012 2017

10 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

In1987,thefinancialservicessectorwasthesixthlargestindustrybehindconstruction,manufacturing,publicadministration,andpubliceducation.WhentheGFChitin2007,financialserviceshadgrowntobeAustralia’ssecondlargestindustry.Onmostrecentannualdata(2016),thefinancialsectorstandsasthelargestindustrybygrossvalueadded(seeFigureB).

FIGUREB

INDUSTRY GROSS VALUE ADDED$m,rankedinyear2016

Source:UnderlyingdatafromABS.CalculationsandvisualisationbyBenchmarkAnalytics.

Financial and insurance services

Construction

Mining

Health care and social assistance

Professional,scientificandtechnicalservices

Manufacturing

Publicadministrationandsafety

Educationandtraining

Transport,postalandwarehousing

Retail trade

Wholesale trade

Rental,hiringandrealestateservices

Information media and telecommunications

Administrative and support services

Electricity,gas,waterandwasteservices

Accommodation and food services

Agriculture,forestryandfishing

Other services

Arts and recreation services

37,445

40,744

26,986

32,473

27,545

77,059

42,132

40,276

30,456

26,567

25,234

17,274

9,549

17,399

25,888

17,240

19,050

14,382

5,366

109,291

97,306

66,643

75,447

75,758

109,332

70,522

65,113

65,903

57,924

53,955

33,608

35,784

44,355

38,385

35,949

29,126

25,410

10,864

146,179

134,182

114,896

112,317

103,568

99,439

90,758

78,463

78,308

72,050

66,477

49,831

46,916

44,927

42,832

39,019

36,650

29,852

13,,606

1987 2007 2016Date

0K50K100K150K200K0K50K100K150K200K0K50K100K150K200K

11 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Thegrowthinthefinancialsectorhasemergedinaderegulatoryenvironment.Whilethefinancialsectorhasalwaysbeenregulatedtosomedegree,particularlydepositorsafetyanddisclosure,theprevailingpolicyorthodoxysincethelate1970shasbeentoregulatetheindustrythroughfosteringcompetition.ThisorthodoxyisevidentintherecommendationsofthethreemajorfinancialsectorinquiriesheldinAustraliasincethe1970s.The1979CampbellInquiryrecommendedthefloatingofthedollar,andthederegulationofthebankingsector,includingthegrantingoflicencesforforeignbanks.The1997WallisInquirysimilarlyputapolicyemphasisoncompetition.Toimprovecompetitiveneutrality,itrecommendeda‘twinpeaks’regulatorymodelaimedatremovingregulatorydistortions.Underthismodel,regulatoryobjectivesarealignedwithidentifiedpotentialmarketfailures,andtheintensityofregulationistailoredtothedegreeofriskinvolved.Inthewakeofforeignbankentryinthe1980s,aperiodofintensecompetitionforcommercialpropertyloansledtounsustainablepriceincreasesand,ultimately,wasamajorfactorinthedeeprecessionoftheearly1990s.Backthen,theoverextensionofcommercialpropertylendingbyWestpacandANZledtosignificantfinanciallosses.SomeGovernment-ownedstatebanksalsocollapsed.Thisdisturbancecameagainstaperiodoffinancialstabilitythroughthe1950s,1960sand1970s.Hence,somecommentatorssawderegulationasacontributingfactortothefinancialdifficultiesofthelate1980sandearly1990s.Morerecently,thebankingsectorhasbeencriticisedfortheriseinhouseholddebt,particularlythatusedtopurchasehousing.Credittohouseholdsisnowveryhighbyhistoricalandinternationalstandards.

11 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

12 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

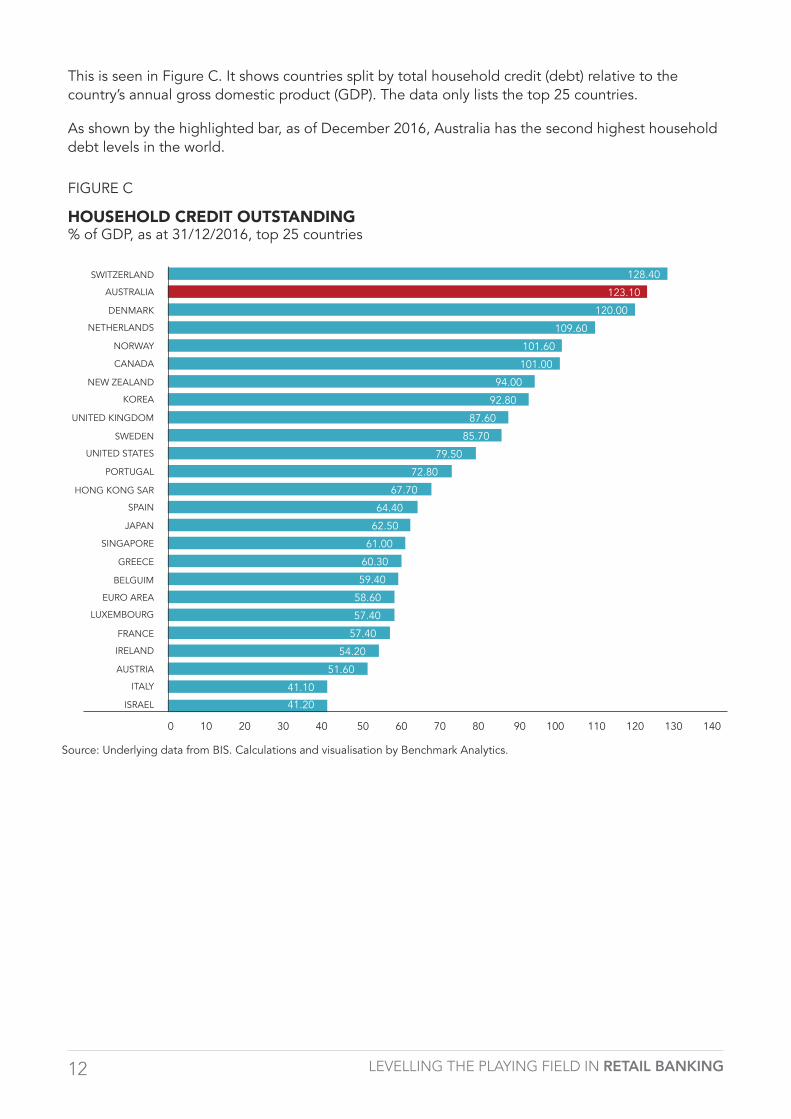

ThisisseeninFigureC.Itshowscountriessplitbytotalhouseholdcredit(debt)relativetothecountry’sannualgrossdomesticproduct(GDP).Thedataonlyliststhetop25countries.

Asshownbythehighlightedbar,asofDecember2016,Australiahasthesecondhighesthouseholddebt levels in the world.

FIGUREC

HOUSEHOLD CREDIT OUTSTANDING%ofGDP,asat31/12/2016,top25countries

Source:UnderlyingdatafromBIS.CalculationsandvisualisationbyBenchmarkAnalytics.

128.40SWITZERLAND

AUSTRALIA

DENMARK

NETHERLANDS

NORWAY

CANADA

NEWZEALAND

KOREA

UNITEDKINGDOM

SWEDEN

UNITEDSTATES

PORTUGAL

HONGKONGSAR

SPAIN

JAPAN

SINGAPORE

GREECE

BELGUIM

EURO AREA

LUXEMBOURG

FRANCE

IRELAND

AUSTRIA

ITALY

ISRAEL

123.10

120.00

109.60

101.60

101.00

94.00

92.80

87.60

85.70

79.50

72.80

67.70

64.40

62.50

61.00

60.30

59.40

58.60

57.40

57.40

54.20

51.60

41.10

41.20

0102030405060708090100110120130140

13 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Asexpected,withlargevolumesofcreditdirectedtowardshousingandconstraintsinhousingapprovalandconstruction,housepricesinAustraliahavegrownsubstantially.Sincetheyear2000,residentialpropertypriceshaveincreasedbyanaverageof237%throughoutAustralia.Thisishighbyinternationalstandards,butitisnoteworthythatothercountrieshavealsoexperiencedhighresidentialpropertypricegrowth,seeFigureD.

FIGURED

RESIDENTIAL PROPERTY PRICES%growthbetween2000and2016,averaged

Source:UnderlyingdatafromBIS.CalculationsandvisualisationbyBenchmarkAnalytics.Indexesareaveragedacrossavailabledataseries.Onlyseriesthathavedatain2000and2016areincludedintheaveragedmethodology.

346.0%LITHUANIA

FINLAND

COLUMBIA

NEWZEALAND

HONGKONGSAR

AUSTRALIA

PERU

NORWAY

SWEDEN

FRANCE

MALAYSIA

BELGIUM

MALTA

DENMARK

AUSTRIA

SPAIN

SWITZERLAND

UNITEDSTATES

EURO AREA

NETHERLANDS

SINGAPORE

ITALY

GERMANY

GREECE

315.1%

238.6%

216.2%

237.4%

217.6%

194.1%

192.0%

158.1%

148.5%

133.6%

136.7%

92.7%

77.8%

76.6%

73.4%

71.4%

59.5%

56.5%

38.7%

39.4%

31.6%

11.7%

0%50%100%150%200%250%300%350%

2016

346.2%

14 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Forsometime,analystshavepredictedthatthislevelofhouseholddebtandhousepricesareunsustainableandripeforacorrection,intheorderofpricedeclinesof25%.Sofar,thishasnotmaterialised.OnepositivefactoristheunderlyingstrengthoftheAustralia’seconomywhichhasnotexperiencedarecessionformorethan25years.

Notwithstanding,thelevelofhouseholddebtandhousepricesremainsarisktotheeconomy.Itmakestheeconomymorevulnerabletoanexternalshockasanyincreaseinunemployment,oralossofconfidencewouldresultinhouseholdsaggressivelycuttingtheirconsumptionexpenditure.Householdconsumptioncurrentlyaccountsforaround60%ofGDP1.

Highhousepricesalsomakeitdifficultforyoungpeopletosaveanadequatedeposittobuyahouse,particularlywhenpermanentworkislessavailable,andthereislesssecurityinmostemployment.Wagegrowthhasalsobeensluggishsince2007astheimpactsofglobalisationandtechnologyhavereducedthebargainingpowerofworkersinnearlyallprivatesectorindustries.

Onesignificantfactordrivinghouseholddebtandhousepricessincetheearly1990shasbeentheincreaseinlendingintotheAustralianhouseholdsectorattheexpenseofbusinesslending2. This changeinbusinessstrategywasdrivenbyaneconomicallyrationalviewthatsuperiorrisk-adjustedreturnswereavailablethroughfundingmortgagesonresidentialproperty.Thisviewwasvindicatedwith the introduction of Basel II and advanced accreditation.

1ABSAustralianNationalAccount,June2017,Cat.No.5206.02Thischangeinstrategyisevidentfromtheincreasingshareofmortgageassetsasaproportionoftotalassets.TheRBAwebsitehasbalancesheetdataonanindividualbankbasisgoingbackto1991,andAPRA’smonthlybankingstatisticsincludesbalancesheetdatafromJune2004.

14 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

15 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

FIGUREE:PERSPECTIVESONCOMPETITION

COMPETITION COMPETITIVE NEUTRALITY

1979 Financial System Inquiry (Campbell)

TheCommitteestartedfromtheviewthatthemostefficientwaytoorganiseeconomicactivityisthroughacompetitivemarketsystemwhichissubjecttominimumregulationandgovernmentintervention.(p1)

…the principle is clear –investorprotectionarrangements,includingReserveBankliquiditysupportarrangements,shouldaimto involve the minimum disturbance to competitive neutrality.(p.289)

1997 Financial System Inquiry (Wallis)

Theefficiencyofthefinancialsystemaffectsevery business and individual in the nation. Thereareverylargeefficiencygainsandcostsavingswhichcouldbereleasedfromtheexistingsystem…Marketscanonlydelivertheseoutcomes where competition is allowed to thrive andwhereconsumershaveconfidenceintheintegrityandsafetyofthesystem.(p.2)

TheprinciplesofregulationwhichhaveguidedtheInquiryarecompetitiveneutrality,costeffectiveness,transparency,flexibilityandaccountability(p.176)…Competitiveneutralityrequiresthattheregulatoryburdenapplyingtoaparticularfinancialcommitmentorpromiseapplyequallytoallwhomakesuchcommitments.(p.196)

2014 Financial System Inquiry (Murray)3

CompetitionandcompetitivemarketsareattheheartoftheInquiry’sphilosophyforthefinancialsystem.TheInquiryseesthemastheprimarymeansofsupportingthesystem’sefficiency.AlthoughtheInquiryconsiderscompetitionisgenerallyadequate,thehighconcentrationandincreasingverticalintegrationinsomepartsoftheAustralianfinancialsystemhasthepotentialtolimitthebenefitsofcompetitioninthefutureand should be proactively monitored over time.(p.xvi)

TheInquiryconsidersthatabsentotherpolicyobjectives,competitive neutrality is an importantregulatoryprinciple.(p.61)

3InadditiontotheMurrayInquiry,atthesametimeProfessorIanHarpercompletedaCompetitionPolicyReviewwherehepresenteda‘forward-looking’packageofreformstoreinvigoratecompetitioninAustralia(Harper,Anderson,McCluskey,&O’Bryan,March2015).Whilethefinancialsectorwasnotexplicitlycoveredinhisreview,theemphasisoncompetitionwasconsistentwithMurrayReportfindings.

16 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Insummary,whilecompetitionhasbeentheprevailingorthodoxyinfinancialregulationsincethe1970s,somecommentatorshavequestioneditslegitimacy.Fromaregionalbankperspective,competitiondrivesoptimaloutcomesforconsumersandthewidereconomy..Webelievethatrecentflawedoutcomesforconsumersaretheresultofshort-comingsincompetition,particularlyinadequatecompetitiveneutrality.Anotherconsiderationistheissueofsustainablecompetition.Competitionlawhaslongprohibitedpracticeswhichmayappearconsumer-friendlyintheshort-term,buthaveadverselong-termimplications.Onesuchpracticeispricingundercost.Thiscandriveoutsuppliersandcausepricestobehigherthanotherwiseinthefuture.Thisriskisheightenedwhereonesupplierhasmarketpowerand,further,wherethatsupplierhasanunwarrantedcostadvantage,suchaslowerfundingcosts(asisthecasewithbanksthataretreatedbytheGovernmentas“toobigtofail”).

1.2 SUMMARY OF MURRAY REPORT KEY RECOMMENDATIONSThe2014FinancialSystemInquiry(FSI)wasakeyeventinthepost-GFCeraforAustralianbanks.TheInquirytooktworoundsofpublicsubmissions.Thefirstroundreceived280submissionsandthesecondround6,500submissions.Thelatterbeingdominatedbysubmissionsrelatingtocreditcardsurcharging.Thefinalreportmade44recommendationstoimprovetheefficiency,resilienceandfairnessofAustralia’sfinancialsystem.Italsoprovidedsetsofprinciplestoguidepolicysettingoveranextendedtimeframe,upto20years.Itmade13observationsrelevanttobroadertaxationpolicy.TheMurrayInquiry’sTermsofReference(TOR)requiredthereviewpaneltorecommendhowAustralia’sfinancialsystemcanbepositionedtosupporteconomicgrowthandmeettheneedsofendusers.TheyalsoconsiderhowthesystemhadchangedsincetheWallisInquiry,includingtheeffectsoftheGFC.(http://fsi.gov.au/2014/12/08/address-to-ceda/)RegionalbanksmadetwosubmissionstotheFSI.Themainrecommendationoftheregionalbankswastosecurechangestothesystemofsettingrisk-weightedassetsinAustraliagiventheunjustifieddichotomythatexistedbetween‘standardised’andIRBbanks.ThisissuewasaddressedbyDavidMurray in recommendation number 2.Recommendation2waspartiallyimplementedinJune2016.Itresultedinmajorbankshavingtomateriallyincreasecapitallevels,whichhasnotonlyimprovedcompetitionbutalsoincreasedoverallsystemresilience,consistentwithDavidMurray’srecommendationnumber1whichwasforthebankingsystemtohaveunquestionablystrongcapitallevels.

1.2.1 Murray recommendations and regional bank positionRegionalbankswerepleasedthattheMurrayInquiryhighlightedthatanunevenplayingfieldthathademergedasaresultofprudentialregulationandotherinitiativessuchasthedifferentialpricingoftheGovernmentGuaranteeduringtheGFC.Afterthefinalreportwasreleased,theregionalbanksassessedeachrecommendationasperthedetailssetoutinFigureF.Note–onlyrelevantrecommendations are listed in the table.

17 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

FIGUREF:MURRAY’SRECOMMENDATIONSANDREGIONALBANKPOSITION(ONLYRELEVANTRECOMMENDATIONSLISTED)

MURRAY REC

DETAILS REGIONAL BANK POSITION

1 CapitallevelsSetcapitalstandardssuchthatAustralianauthoriseddeposit-takinginstitutioncapitalratiosareunquestionablystrong.

Supported

2 NarrowmortgageriskweightdifferencesRaisetheaverageinternalratings-based(IRB)mortgageriskweighttonarrowthedifferencebetweenaveragemortgageriskweightsforauthoriseddeposit-takinginstitutionsusingIRBrisk-weightmodelsandthoseusingstandardisedriskweights.

Stronglysupported

3 LossabsorbingandrecapitalisationcapacityImplementaframeworkforminimumlossabsorbingandrecapitalisationcapacityinlinewithemerginginternationalpractice,sufficienttofacilitatetheorderlyresolutionofAustralianauthoriseddeposit-takinginstitutionsandminimisetaxpayersupport.

Supported

4 TransparentreportingDevelopareportingtemplateforAustralianauthoriseddeposit-takinginstitutioncapitalratiosthatistransparentagainsttheminimumBaselcapitalframework.

Supported

5 CrisismanagementtoolkitCompletetheexistingprocessesforstrengtheningcrisismanagementpowersthathavebeenonholdpendingtheoutcomeoftheInquiry.

Supported

6 FinancialClaimsSchemeMaintaintheex-postfundingstructureoftheFinancialClaimsSchemeforauthoriseddeposit-takinginstitutions.

Stronglysupported

7 LeverageratioIntroducealeverageratiothatactsasabackstoptoauthoriseddeposit-takinginstitutions’risk-weightedcapitalpositions.

Supported

15 DigitalidentityDevelopanationalstrategyforafederated-stylemodeloftrusteddigitalidentities.

Supported

19 Data access and useReviewthecostsandbenefitsofincreasingaccesstoandimprovingtheuseofdata,takingintoaccountcommunityconcernsabout appropriate privacy protections.

Neutral

20 ComprehensivecreditreportingSupportindustryeffortstoexpandcreditdatasharingunderthenewvoluntarycomprehensivecreditreportingregime.If,overtime,participationisinadequate,Governmentshouldconsiderlegislatingmandatoryparticipation.

Supported

18 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

MURRAY REC

DETAILS REGIONAL BANK POSITION

22 Introduce product intervention powerIntroduce a proactive product intervention power that would enhancetheregulatorytoolkitavailablewherethereisriskofsignificantconsumerdetriment.

Neutral

23 Facilitate innovative disclosureRemoveregulatoryimpedimentstoinnovativeproductdisclosureandcommunicationwithconsumers,andimprovethewayriskandfees are communicated to consumers.

Supported

24 AligntheinterestsoffinancialfirmsandconsumersBetteraligntheinterestsoffinancialfirmswiththoseofconsumersbyraisingindustrystandards,enhancingthepowertobanindividualsfrommanagementandensuringremunerationstructuresinlifeinsuranceandstockbrokingdonotaffectthequalityoffinancialadvice.

Neutral

25 Raise the competency of advisersRaisethecompetencyoffinancialadviceprovidersandintroduceanenhancedregisterofadvisers.

Supported

1.3 REFLECTION ON PRESSURES/CONDITIONS LEADING TO GOVERNMENT CALLING FOR PC INQUIRY TheGovernmentannouncedaPCInquiryintothebankingsystemaspartofits2017Budgetannouncement.ThespecificrecommendationwasinresponsetotheColemanCommitteerecommendationforacompetitioninquiry–seeFigureG.TheColemanInquirywasitselfareflectionoftheissuesdiscussedintheprevioussection.

FIGUREG:COLEMANRECOMMENDATIONONCOMPETITIONTHATWASACCEPTEDBYTHETURNBULLGOVERNMENT

Recommendation 3 The Government agrees with this recommendation.

The committee recommends that the Australian CompetitionandConsumerCommission(ACCC),ortheproposedAustralianCouncilforCompetitionPolicy,establishasmallteamtomakerecommendationstotheTreasurereverysixmonthstoimprovecompetitioninthebankingsector.If the relevant body does not have any recommendationsinagivenperiod,itshouldexplainwhyitbelievesthatnochangestocurrentpolicysettingsarerequired.

WehavetaskedtheProductivityCommissiontoundertakeareviewofcompetitioninthefinancialsystem,commencing1July2017.TocomplementtheProductivityCommissionreview,wewillprovidetheACCC$13.2millionoverfouryearstoestablishadedicatedunittoundertakeregularin-depthinquiriesintospecificfinancialsystemcompetitionissuesfrommid-2018.

19 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

1.4 OBSERVATIONS/REFLECTIONS ON TERMS OF REFERENCERegionalbanksstronglysupportthePCreviewofthefinancialsector.WeunderstandthatthisisthefirsttimethePChasbeentaskedtoexaminecompetitioninfinancialservices.

RegionalbanksacknowledgethatthePC,asanagency,hasafocuson‘efficiency’,andthisisappropriategiventhatultimatelythepurposeofpublicpolicyistoensureacountry’sresources,includingworkersandcapital,areusedinthemostefficientmeanspossible.

1.4.1 Regional bank high-level observations on TORIn FigureH,regionalbanksdetailreflectionsontheTORthatmaybeusefulfortheinquiryinunderstandingourperspective.

20 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

FIGUREH

PC TOR NO.

DETAILS REGIONAL BANK HIGH-LEVEL COMMENT

1 Considerthelevelofcontestabilityandconcentrationinsegmentsofthefinancialsystem(includingthedegreeofverticalandhorizontalintegration,andtherelatedbusinessmodelsofmajorfirms),anditsimplications for competition and consumer outcomes

Stronglyagreewithinquiringintocontestability and concentration. RegionalBanksnotetheprimaryissuewithverticalandhorizontalintegrationiswithbanksthathaveactualmarketpower.

2 Examinethedegreeandnatureofcompetition in the provision of personal depositaccountsandmortgagesforhouseholdsandofcreditandfinancialservices for small and medium sized enterprises

Support,creditforsmallbusinessisanissueforlong-termproductivity.Majorbankshavethebalancesheetsizeandriskmanagementcapabilitytodomoresmallbusinesslending.

3 ComparethecompetitivenessandproductivityofAustralia’sfinancialsystem,andconsequentconsumeroutcomes,withthat of comparable countries

Supported.Notethatefficiencycomparisonsmustrecognisedifferencesinbusinessmodels.Forexample,banksthatdoalotofcommerciallendingwillhavehighercoststhanbankswithlargecommoditisedbusinesseslikehousingloans or credit cards.

4 Examinebarrierstoandenablersofinnovationandcompetitioninthesystem,includingpolicyandregulation

Supported.Noteinnovationwillcomefromgenuinecompetitiveneutrality.

5 Prioritiseanypotentialpolicychangeswithreferencetoexistingpro-competitionpoliciestowhichtheGovernmentisalreadycommittedorconsideringinlightofotherinquiries.

Supported.Regionalbanksarekeentoensureregulatorychangesarekeptto the minimum needed to achieve the policyobjective.

Other TheCommissionshouldhaveregardtotheGovernment’sexistingwide-rangingfinancialsystemreformagendaanditsaimsto:• strengthentheresilienceofthefinancial

system• improvetheefficiencyofthe

superannuation system• stimulateinnovationinthefinancial

system• supportconsumersoffinancialproducts

beingtreatedfairly• strengthenregulatorcapabilitiesand

accountability.

Supported.RegionalbanksunderscoretheimportanceofensuringcompetitionisgivenappropriatepolicyweightgivenAustralia’slongrecordoffinancialsecurity.

21 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

2 COMPETITION2.1 DEFINITION, MARKET STRUCTURE, NEW ENTRANTS Competitionisaprocessofrivalrybetweenfirms,eachseekingtowinacustomer’sbusiness.Theprimaryobjectiveofcompetitionpolicyistopromoteefficiencywhichinturnboostsandstimulateseconomicgrowth.Accordingtothe1993independentcommitteeofinquiryintoNationalCompetitionPolicy(Hilmer,Rayner,&Taperell,1993):

Competition policy is not about the pursuit of competition per se. Rather, it seeks to facilitate effective competition to promote efficiency and economic growth while accommodating situations where competition does not achieve efficiency or conflicts with other social objectives. (Hilmer, Rayner, & Taperell, 1993, p. xvi).

Formerchants,theretailpriceofaproducttheychargeisbroughtintosomerelationshipwithcostthroughthecompetitiveprocess(Adelman,1957,p.266).Asthe1997FinancialSystemInquiry(WallisReport)observed:

In markets where the degree of competition among suppliers is high, prices are likely to reflect the underlying cost of production. Suppliers pricing above this cost will be undercut by other suppliers, thereby losing market share. (Wallis, Beerworth, Carmichael, Harper, & Nicholls, 1997, p. 601)

Thus competition forces prices down towards the cost of production which enhances allocative efficiency.Competitionpromotesproductiveefficiencybyforcingfirmstocuttheircostsinordernottolosesalestomoreefficientrivals(Kolasky&Dick,2003,p.208). Iffirmscannotmaintainproductiveefficiencywiththeirrivals,theyrisklosingmarketshareandpossiblygoingoutofbusinessaltogether.Competitionalsoprovidesaspurfordynamicefficiency.Firmsundertakeinnovationthroughresearchanddevelopment(R&D)toimprovetheircompetitiveness.R&Dcanhelpabusinessloweritscostsofproductionand/orproducebetterproducts,givingitacompetitiveadvantageoveritsrivalsinthemarketplace.ThebenefitsfirmsseektocapturethroughR&D,namelylowercosts,higherproductivityandbetterproducts,ifrealised,willultimatelygeneratehigherratesofeconomicgrowth.Because of the demonstrated success of competitionindrivingeconomicefficiencyand,therefore,risinglivingstandards,Governmentsfrequentlychampionitsimportanceanduseitasaprimaryprincipletoguidedecision-making.ThecurrentFSIidentifiedcompetitionasa

keyobjectiveasdidthetwopreviousfinancialsysteminquiries.The1981AustralianFinancialSystemInquiry(Campbell,etal.,1981)andthe1997WallisReport (Wallis,Beerworth,Carmichael,Harper,&Nicholls,1997)placedconsiderableweighton the importance of competition as the most efficientmeansoforganisingfinancialactivity.Inadditiontothegeneralconceptofcompetition,they advocated the need to achieve competitive neutrality. These perspectives are summarised in therecommendationsofboththeCampbellandWallisreports,wheretheauthorsrecommendedpolicyinitiativestobringaboutgenuineimprovements in the competitive operation of markets.TheWallisReportledtothewholesalere-structuringoffinancialregulation,establishingadedicatedprudentialregulator,theAustralianPrudentialRegulationAuthority(APRA),andadedicatedregulatortosupervisemarketdisclosureandconduct,theAustralianSecuritiesandInvestmentsCommission(ASIC).Bothinquiriesalsorecommendedagainstallowingafinancialsystemtohaveintermediariesthatare“toobigtofail”.

22 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

2.2 WHAT CONSTITUTES SUSTAINABLE COMPETITIONRegionalbankshaveastrongpositionthattheonlysustainablecompetitivemodelisonewhichensurescompetitiveneutrality.Solongastheregulatorysettingsareneutraltosizeandcomplexity,thensuccesswilldependupontheextenttowhichcustomersaresatisfied.Atthecoreofregionalbanks’concernsisthestatusofmajorbanksasbeing“toobigtofail”.Thisdesignationbydefinitionviolatesthecompetitiveneutralityprinciple.

APRA’s December 2013 media release

InDecember2013,theAustralianPrudentialRegulatoryAuthority(APRA)issuedamediareleasedeclaringthattherewerefourbanksinAustraliaassessedasbeingdomesticallysystemicallyimportant(D-SIBs).Awidely-usedtermtodescribesystemicallyimportantinstitutionsis“toobigtofail”.APRA’sstatementconfirmedandcrystallisedwhathadbeenwellknownbutneverofficiallyrecognised,thatthelargestfourbankshadaspecialstatusinthatfailurewouldhavesevereeconomicimpacts.Ineffect,theyhadanimplicitsubsidyfromtaxpayers.RegionalbanksbelievethisAPRAmediareleasesymbolisesthecoreprobleminAustralianbanking,thatfourinstitutionshaveaspecialstatus,andthatthisgivesthematruecompetitiveadvantageoverbanksthatdonothavethisstatus.ThemostobviousmanifestationofthisbeingthedifferentialpricingoftheGovernmentGuaranteeduringtheGFC.

22 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

23 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

2.3 EFFICIENCY AND CAPITAL FORMATIONEfficiencyreferstotheoptimaluseofresources.Theissueofefficiencyiscomplexwhenconsideringfinancialservices.WeknowthatAustralia’sfinancialsectorisoneofthelargestintheworld,equatingtoaround9%oftotalgrossvalueadded.Inonerespect,thiscouldindicatewehaveaninefficientsystemgiventheamountofcapitalandlabour resources utilised in the process of intermediation and provision of payment facilities.Ontheotherhand,ourfinancialinstitutionsarerelativelyefficientregardingcost-to-incomeratios.Foreverydollarofincome,theoperatingcostsofAustralianbanksaresmallbyinternationalstandards,asperFigureI.Theefficiencyratiointhechartisdefinedastheoperatingcostsasaproportion of total income.

FIGUREI

EFFICIENCY RATIOSelectionofinternationalbanks

Source:DataprovidedbySuncorp.

88.70DZBANK

RABOBANK

ROYALBANKOFSCOTLANDGROUP

TORONTO-DOMINIONBANK

BANKOFMONTREAL

WELLSFARGO&CO

JPMORGANCHASE&CO

CITIBANKNA

BANCOSANTANDERSA

INGGROEPNV

DANSKE

NORDEABANKAB

AUSTANDNZBANKINGGROUP

NATIONALAUSTRALIABANKLTD

WESTPACBANKINGGROUP

COMMONWEALTHBANKOFAUSTRALIA

65.60

63.51

61.78

59.74

58.52

58.10

56.86

54.91

54.24

51.98

50.15

49.62

45.05

43.42

0102030405060708090100

Australian-majorbanksInternationalbanks

41.82

24 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Whencomparingfinancialinstitutionefficiencyratios,an‘applestoapples’comparisonrequiresanunderstandingofthevariousbusinessstructures.Australia’smajorbanksareveryunusualinthatthelargestcomponentoftheirassetsisresidentialmortgages.Bigbanksinmostcountrieshaveamuchhigherproportionofcommerciallending.Commerciallendingishighercostbecausetherisksassociatedwithbusinesslendingaretypicallymoreidiosyncraticandrequiremuchgreatercreditanalysisthandoesthehomogenisednatureofmortgagelending.Giventhis,itisnotsurprisingthatAustralia’smajorbanksarerelativelyefficientintermsofcost-to-income.However,thelargesizeofourfinancialsectormeansthat,asacountry,Australiaisspendingmoremoneyonfinancialservicesthanmostothercountries.Onefactoristhereturntoshareholders.Australia’smajorbanksarehighlyprofitable-seeFigureJforacomparisonofprofitmarginsacrossbankingsystems.Profitmarginisdefinedasthebeforetaxprofitdividedbytotalincome.

FIGUREJ

CautionisneededwhendrawingconclusionsabouttheefficiencyofthemajorbanksinAustralia.Thecost-to-incomeratioiscalculatedbytwovariables–incomeandcosts.Alowcosttoincomeratiowillresultifincomeishigh,costsarelow,oracombinationofboth.Bybenchmarkingcostsandincomeagainsttotalassetsandthencomparingthesebenchmarkstobanksinothercountries,theconclusionisthatAustralia’slargestbankshavelowercost-to-incomeratios due to balance sheet size and diversity. Whilecostsarenotespeciallyhighbyinternationalstandards,thiscanbepartiallyexplainedbythecommoditisednatureofmajorbank’sassets–withaheavyweightingtowardsresidentialmortgages.

PROFIT MARGINSelectionofinternationalbanks

Source:DataprovidedbySuncorp.

COMMONWEALTHBANKOFAUSTRALIA

WESTPACBANKINGGROUP

NATIONALAUSTRALIABANKLTD

DANSKE

NORDEABANKAB

AUSTANDNZBANKINGGROUP

INGGROEPNV

TORONTO-DOMINIONBANK

JPMORGANCHASE&CO

WELLSFARGO&CO

BANKOFMONTREAL

RABOBANK

CITIBANKNA

BANCOSANTANDERSA

ROYALBANKOFSCOTLANDGROUP

DZBANK

38.44

35.92

35.48

35.23

34.35

28.82

27.00

26.01

25.50

24.85

23.26

22.06

19.66

13.84

0510152025303540

Australian-majorbanksInternationalbanks8.39

5.58

25 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

2.4 COMPETITIVE NEUTRALITY (BARRIERS/ISSUES)Whilemarketconcentrationcanprovideguidanceastowhichmarketsarelikelytoraisecompetitionconcerns,otherfactorsalsowarrantconsideration.Theseotherfactorsincludetheheightofbarrierstoentryandtheextentofsunkcostsincurredbynewentrants.Aprominentindustrialorganisationeconomist(Bain,1956) considered the force of potential competitionasaregulatorofpriceandoutputisjustasimportantasactualcompetition.Bainfocussedontheheightofbarrierstoentryasthecriticaldeterminantofthepricelevel.AccordingtoBain,theextentofbarrierstoentryinanindustryindicatedtheadvantagethatexistingsellersenjoyedoverpotentialentrants.Anyentrycostthatisunrecoverableisasunkcost.Theneedtosinkcostsintoanewfirmimposesadifferencebetweentheincrementalcostandtheincrementalriskthatisfacedbyanewentrantandanincumbentfirm(Baumol&Willig,1981,p.418).Inthecaseofanincumbent,suchfundsarealreadyspent,andtheyareexposedtowhateverrisksthemarketentails.Incontrast,thenewfirmmustincuranyentrycostsonenteringthemarketthatincumbentsdon’tbear.Theentryofnewfirmsintoamarketcanprovidecompetitiveconstraintonincumbents(AustralianCompetitionandConsumerCommission,2008,p.38). If new entrants can offer customers an appropriatealternativesourceofsupplyattherighttime,anyattemptbyincumbentstoexercisemarketpowerwillbeunsustainablesincetheircustomerswillswitchtothenewentrants.Theexistenceofsunkcosts,whichincreasestherisksof,andcostsassociatedwith,failedentry,maydeternewentryaltogether.

2.5 MARKET POWER AND CUSTOMER/CONSUMER CHOICE /SOVEREIGNTYTheeconomicandlegalliteratureprovidesseveraldefinitionsofmarketpower.Acommonly-useddefinitionisthefollowing:“A firm possesses market power when it can behave persistently in a manner different from the behaviour that a competitive market would enforce on a business facing otherwise similar cost and demand conditions.” (Kaysen&Turner,1959,p.75) Anotherdefinitionofmarketpoweris“….the ability of a firm to raise price above the competitive level without losing so many sales so rapidly that the price increase is unprofitable and must be rescinded” (Landes&Posner,1981,p.937) Anoligopolyisamarketstructurecharacterisedbyafewparticipants.Itmayincludea“competitive fringe” of numerous smaller sellers who behave competitively because each is too small individually to affect prices or output (Areeda,Solow,&Hovenkamp,2002,p.9) TheprovisionoffinancialservicesinAustralia–thatisdominatedbythefourlargebanks–couldbecharacterisedasanoligopolythatissupplementedbyacompetitivefringethatincludesregionalbanksandcustomer-ownedbanks(creditunionsandbuildingsocieties).

Committeechairman,DavidColeman:“Australia’s banking sector is an oligopoly. The major banks have significant market power that they use to protect shareholders from regulatory and market developments.” (House of Representatives Standing Committee on Economics, 2016)Treasurer,ScottMorrison:“…the banking system in Australia – with a small number of large and highly profitable banks at its core – is highly concentrated… The House of Representatives Economics Committee’s ‘Review of the Four Major Banks’, commissioned by the Government last year, concluded that Australia’s banking sector is an oligopoly and that Australia’s largest banks have significant pricing power which they have used to the detriment of everyday Australians. (Morrison, 2017)

26 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Sometheoriesofoligopolypredictthatoncefirmsrecognisetheirinterdependency,theirmostrational course of action would be to behave in a manner reminiscent of a monopoly. The outcome fromthesemodelshasbeendescribedastacitcollusion,alsoknownascoordinatedeffects.Whilefirmsarenotnecessarilypartofaformalcartelarrangement,thefirmscancoordinatetheirconductso that an outcome similar to cartel or monopoly is achieved.However,justbecauseamarketischaracterisedashavinganoligopolystructuredoesnotnecessarilymeanthatitwillbepronetocoordinatedeffectsandtheabuseofmarketpower.Identifyingfirmsthathavesubstantialmarketpowerenablesonetodistinguishbetweenconductthatmightharmconsumersandconductthatcannot.(Bork&Sidak,2013,p.511)Unfortunately,thereisnodefinitivetest.Instead,onemustrelyonaseriesofpartialindicatorstodeterminewhetherfirmsparticipatinginamarketareexercisingmarketpower.AccordingtocompetitionlawexpertRobertBorkandProfessorGregorySidakofTilburgUniversity(Bork&Sidak,2013,p.512): “Courts and competition authorities around the globe typically rely on indirect evidence of market power, such as market share and barriers to entry.”

2.6 INNOVATION/TECHNOLOGYInnovationhasthepotentialtotransformthebankingandfinancialsystem.Wehavealreadyseenconsiderabledevelopmentsinmobilebanking,cloudcomputinginternetdelivery,andpaymentservices.Contactlesspayments,forexample,arequicklydisplacingcash.AsfoundbytheMurrayInquiry,innovationhasthepotentialtodeliversignificantefficiencybenefitsandimproveoutcomesforconsumersandbusinessesgenerally,butitalsoraisesfinancialrisks.Financialinnovationcanundermineregulatoryobjectivesbyshiftingrisksoutsidetheregulatoryperimeter,theso-calledproblemassociatedwith‘ShadowBanks’.Regionalbankshaveaparticularconcernovermacroprudentialrulesplacinglimitsoninvestorlendingandhowtheunevenimplementationoftheserulesisshiftingcreditsupplyintothenon-regulatedspace.Bydoingso,competitiveneutralityisunderminedasisthemacro-objective.

2.7 REGIONAL BANK CONCLUSION ON COMPETITIONRegionalbankshavebeenaroundformorethan150yearsandcompetefiercelyformarketsharebutinsomemarketshavelimitedabilitytoinfluence/compete.Thishasconsequencesforcustomersandconsumersgenerally.Regionalbanksarethecompetitivefringe,butthemarketisverymuchcontrolledbythecommercialdecisionsofthelargestinstitutions,andthebusinessmodelsofthebigfourareverysimilar.Whenregionalbankexecutivesgivebriefingsafterresultsannouncements,itiscommonforthemtorefertomarketconditionsas‘verycompetitive’.Whatthisreallymeansisthattheproductmarkets,fromtheirownbusinessperspective,areverycompetitive.Onekeyreasontheyfinditcompetitiveisthattheplayingfieldistiltedagainstthemfor the reasons discussed above. Thedominantmarketpowerofasmallnumberofplayersisaconsequenceof;

• “Toobigtofail”drivingfundingadvantages;• Risk-weightcapitaldifferences;and• Insufficientdisclosurearoundtheownershipofnon-branchdistributionnetworksandthe

proportion of loans they direct to their owners.

27 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3 DATA: MARKET SHARE, PROFITS, MARGINS3.1 MARKET SHARE/TREND ANALYSISDependingonthedefinitionofmarket,themajorbanksinAustraliahaveupto85%marketshareoftotalassetsheldbydeposit-takinginstitutions.ThisisseeninFigureKbelowwhichshowsmarketshareusingAPRA’squarterlyperformancestatistics.Thesefiguresincludedataformajorbanks,regionalbanks,creditunions,buildingsocietiesandforeign-ownedsubsidiaries.Assetsofforeignbranchesareexcluded.Thisdatasetrepresentsconsolidatedassetsofallbankingbusinesses,includingAustralian-ownedforeignoperations.In2004,themajorbanksshareoftotalassetswas78%,butthemajorbanks’marketsharesteadilydeclinedtolessthan75%beforetheGFCcommencedin2007andsubsequentmergersofCBA/BankWestandWestpac/St.George.

FIGUREK

TOTAL ASSETS%Shareoftotal(domesticandosbooks)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

21.49%

2008

MajorbanksOtherbanks

2013

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

15.07%

84.93%78.51%

28 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Themarketshareofmajorbanksintotalloansandadvancesmirrorsthatoftotalassets–see FigureL.Thisisnotsurprisingasloansandadvancesarethelargestcomponentsoftotalassets.Onceagain,majorbankssawadecliningmarketsharebetween2004and2007.Currentmarketsharestandsat84.5%.

FIGUREL

TOTAL LOANS AND ADVANCES%Shareoftotal(domesticandosbooks)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

22.01%

2008

MajorbanksOtherbanks

2013

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

15.20%

84.80%77.99%

29 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Majorbanks’shareoftotaldepositsismarginallybelowthatoftotalassetsandtotalloans.Currently,collectivemarketshareis83.7%.SincetheGFC,competitionfordepositshasintensified.Themajorbanksshareofdepositspre-GFCfelltothelow70s.

FIGUREM

24.91%

2008

MajorbanksOtherbanks

2013

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

16.24%

83.76%75.09%

TOTAL DEPOSITS%Shareoftotal(domesticandosbooks)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

30 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Themajorbankshave84%oftotalassets,andahigherproportion(over85%)ofindustrytotalprofits.In2004,theshareofprofitswas74%.Ashiftfrom74%to85%inshareofprofitsrepresentsasignificantchangeintherelativeimportanceofthesefourbanks–seeFigureN.

FIGUREN

Itshouldbestressedthatthisriseinindustryprofitshareisnottheresultoforganicgrowthbuiltonwinningcustomermarketshare.Between2004and2007,majorbankslostmarketsharetosmallerbanks.ItwasonlythemergersofBankWestandSt.George,inadditiontothepricingadvantagesinherentinBaselIIrisk-weightingmethodanddifferentialpricingoftheGovernmentGuaranteeintheGFCthathasputthebigfourbanksintothisstrongmarketposition(seepolicydiscussioninSection5).

TOTAL PROFITS%Shareoftotal(domesticandosbooks)

NOTE:Somedatachangesduetogoingfromquarterlytosmootherannualdata.Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

25.75%

2004

2005

2006

2007

2008

2010

2011

2012

2013

2014

2015

2016

MajorbanksOtherbanks

80%

60%

40%

20%

0%

14.72%

85.28%

74.25%

Date

31 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Oneofthekeydevelopmentsoverthelast13yearsinAustralia’sfinancialsystemisthedeclineinthenumberofdeposit-takinginstitutions.Ithasinfacthalved,mainlydrivenbyconsolidationinthecreditunionindustry.Australiacurrentlyhas99registereddeposit-takinginstitutions.

FIGUREO

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

NUMBER OF DEPOSIT-TAKING INSTITUTIONS

4

2004200620082010201220142016

MajorbanksOtherbanks

200

150

100

50

0 4

95

207

32 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

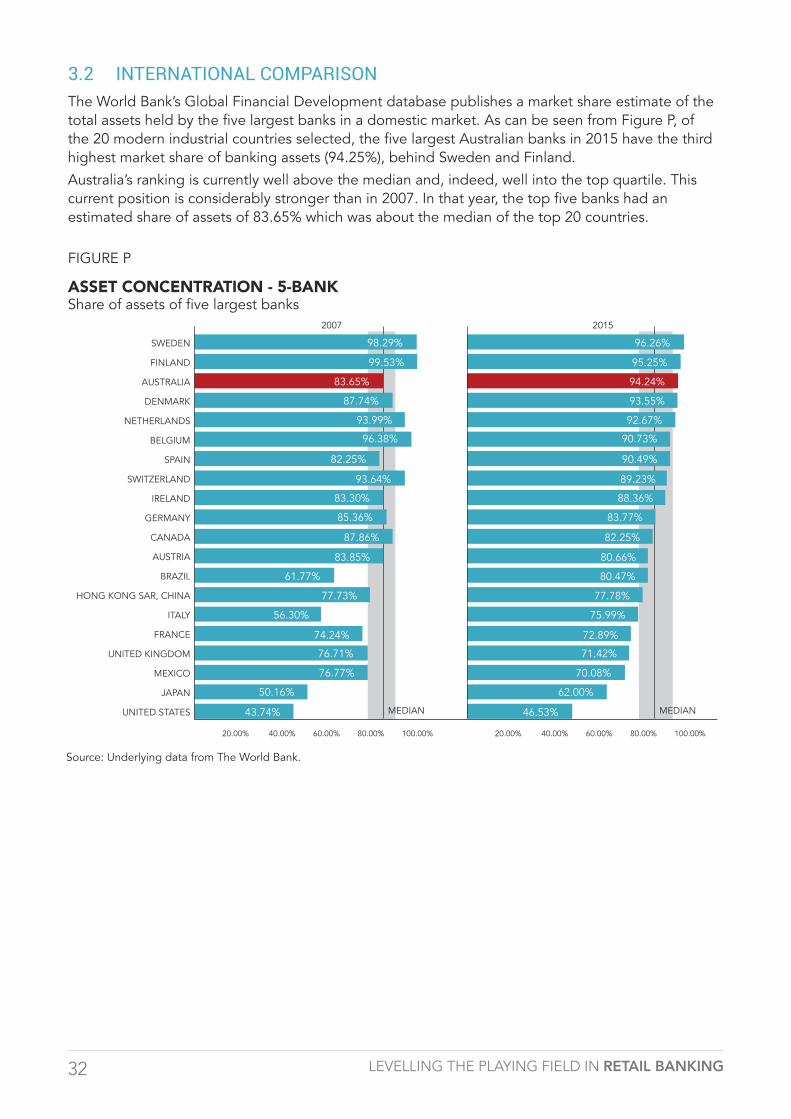

3.2 INTERNATIONAL COMPARISONTheWorldBank’sGlobalFinancialDevelopmentdatabasepublishesamarketshareestimateofthetotalassetsheldbythefivelargestbanksinadomesticmarket.AscanbeseenfromFigureP,ofthe20modernindustrialcountriesselected,thefivelargestAustralianbanksin2015havethethirdhighestmarketshareofbankingassets(94.25%),behindSwedenandFinland.Australia’srankingiscurrentlywellabovethemedianand,indeed,wellintothetopquartile.Thiscurrentpositionisconsiderablystrongerthanin2007.Inthatyear,thetopfivebankshadanestimatedshareofassetsof83.65%whichwasaboutthemedianofthetop20countries.

FIGUREP

ASSET CONCENTRATION - 5-BANKShareofassetsoffivelargestbanks

Source:UnderlyingdatafromTheWorldBank.

SWEDEN

FINLAND

AUSTRALIA

DENMARK

NETHERLANDS

BELGIUM

SPAIN

SWITZERLAND

IRELAND

GERMANY

CANADA

AUSTRIA

BRAZIL

HONGKONGSAR,CHINA

ITALY

FRANCE

UNITEDKINGDOM

MEXICO

JAPAN

UNITEDSTATES

20.00%40.00%60.00%80.00%100.00% 20.00%40.00%60.00%80.00%100.00%

98.29%

99.53%

83.65%

87.74%

93.99%

96.38%

82.25%

93.64%

83.30%

85.36%

87.86%

83.85%

61.77%

77.73%

56.30%

74.24%

76.71%

76.77%

50.16%

43.74%

96.26%

95.25%

94.24%

93.55%

92.67%

90.73%

90.49%

89.23%

88.36%

83.77%

82.25%

80.66%

80.47%

77.78%

75.99%

72.89%

71.42%

70.08%

62.00%

46.53%

2007 2015

MEDIAN MEDIAN

33 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

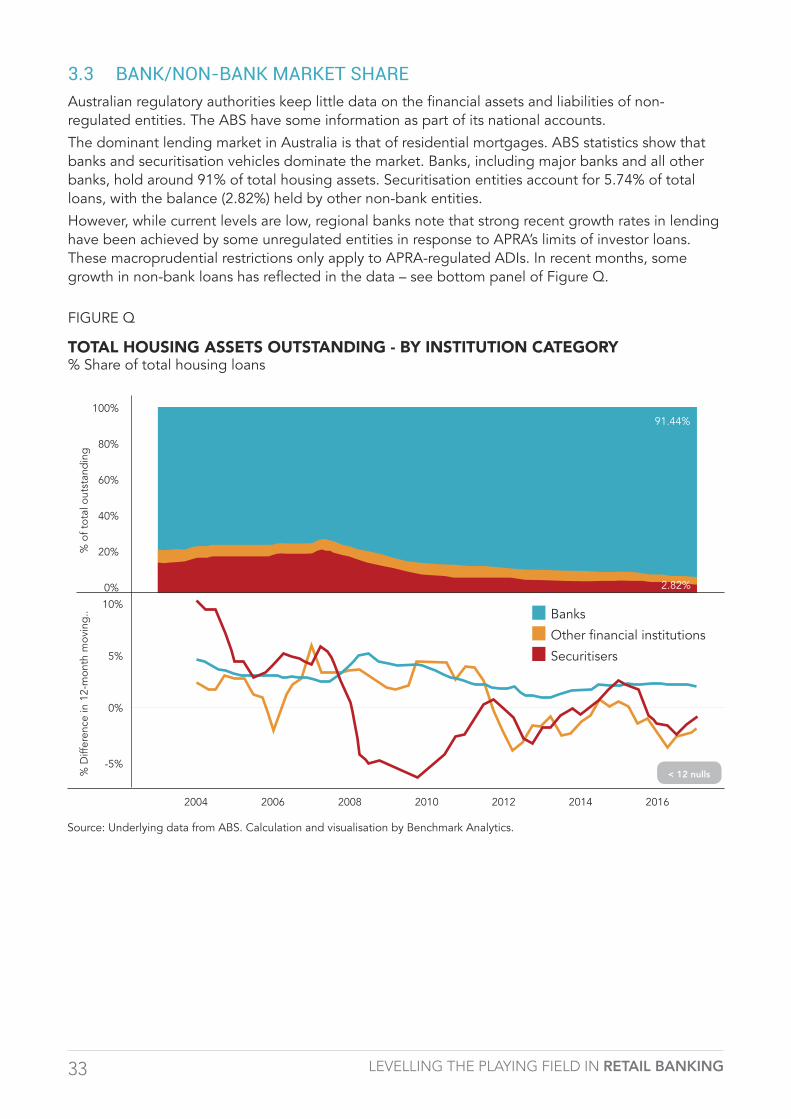

3.3 BANK/NON-BANK MARKET SHAREAustralianregulatoryauthoritieskeeplittledataonthefinancialassetsandliabilitiesofnon-regulatedentities.TheABShavesomeinformationaspartofitsnationalaccounts.ThedominantlendingmarketinAustraliaisthatofresidentialmortgages.ABSstatisticsshowthatbanksandsecuritisationvehiclesdominatethemarket.Banks,includingmajorbanksandallotherbanks,holdaround91%oftotalhousingassets.Securitisationentitiesaccountfor5.74%oftotalloans,withthebalance(2.82%)heldbyothernon-bankentities.However,whilecurrentlevelsarelow,regionalbanksnotethatstrongrecentgrowthratesinlendinghavebeenachievedbysomeunregulatedentitiesinresponsetoAPRA’slimitsofinvestorloans.ThesemacroprudentialrestrictionsonlyapplytoAPRA-regulatedADIs.Inrecentmonths,somegrowthinnon-bankloanshasreflectedinthedata–seebottompanelofFigureQ.

FIGUREQ

Source:UnderlyingdatafromABS.CalculationandvisualisationbyBenchmarkAnalytics.

TOTAL HOUSING ASSETS OUTSTANDING - BY INSTITUTION CATEGORY%Shareoftotalhousingloans

100%

80%

60%

40%

20%

0%

2004200620082010201220142016

Banks

Otherfinancialinstitutions

Securitisers

91.44%

2.82%

10%

5%

0%

-5%

%Differencein12-monthmoving..

%oftotaloutstanding

< 12 nulls

34 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3.4 MARKET SHARE BY SEGMENT/PRODUCTAPRA’smonthlybankingstatisticsenableareasonablydetailedbreakdownofmarketsharebyproductcategory.Thedataseriescommencedin2004,andthefiguresareonlyforthedomesticmarket.AscanbeseeninFigureR,thebigfourbankshavesubstantiallyimprovedmarketshareinallproductmarketssince2007:

• Shareoftotaldomesticresidentassetshasgrownfrom64%to79%;• Totaldeposits,61%to77.3%;• Householddeposits,68%to80%;• Businessdeposits,70%to78%;• Householdcreditcards,80%to82%;• Housinginvestmentloans,77%to85%;and• Housingowner-occupied,75%to81%.

FIGURER

MARKET SHARE IN KEY PRODUCT MARKETS%SHAREOFDOMESTICMARKET

2004 2007 2017Change07-17

Total depositsMajorbanks 66.7% 61.6% 77.4% 25.7%

Allotherbanks 33.3% 38.4% 22.6% -41.1%

Total deposits from householdsMajorbanks 68.8% 67.6% 79.9% 18.2%

Allotherbanks 31.2% 32.4% 20.1% -37.9%

Totaldepositsfromnon-financialcorporations

Majorbanks 73.6% 69.8% 78.2% 12.0%

Allotherbanks 26.4% 30.2% 21.8% -27.8%

Totalloanstohouseholds:Creditcards

Majorbanks 82.7% 80.1% 82.9% 3.5%

Allotherbanks 17.3% 19.9% 17.1% -14.1%

Totalloanstohouseholds:Housing:Investment

Majorbanks 77.2% 76.8% 85.4% 11.1%

Allotherbanks 22.8% 23.2% 14.6% -37.0%

Totalloanstohouseholds:Housing:Owner-occupied

Majorbanks 75.2% 75.0% 81.1% 8.2%

Allotherbanks 24.8% 25.0% 18.9% -24.5%

Total resident assetsMajorbanks 68.6% 64.0% 79.1% 23.5%

Allotherbanks 31.4% 36.0% 20.9% -41.8%Source:UnderlyingdatafromAPRAMBS.CalculationsandvisualisationbyBenchmarkAnalytics.

35 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3.5 DOMESTIC/GLOBAL TRENDSTheBankofInternationalSettlements(BIS)publishedannualdatacomparingthemajorbanksinadvancedandemergingcountriesagainstperformancemetrics(cautionisneededwhenassessingthesignificanceofinternationalcomparisonsduetodefinitionaldifferences).ThecountriescoveredaretheUnitedStates(US),Australia,Canada,Sweden,Japan,Spain,theUnitedKingdom(UK),Switzerland,GermanyandItaly.The2017annualreporthassufficientdatatoallowafive-yearaveragecalculation.Netincometoassetsisakeyprofitabilityindicator.Netincomeisnetinterestplusotheroperatingincome,minuscosts.Asaratiotototalassets,itprovidesasoundprofitabilitycomparison.Overthefiveyearsto2016,Australia’smajorbanksarethesecondmostprofitablewith1.22%.ThemostprofitableistheUSwitharatioof1.28%.Onthismeasure,Australia’slargebanksaremorethantwiceasprofitableastheaverageofadvancedcountriesinthedataset–seeFigureS.

FIGURES

NET INCOME TO ASSETS5yearaverage(2012-2016)

USA

Australia

Canada

Sweden

Japan

Spain

France

UnitedKingdom

Switzerland

Germany

Italy

1.28%

1.22%

1.00%

0.77%

0.58%

0.39%

0.38%

0.26%

0.17%

0.01%

-0.24%Average

-0.40% -0.20% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40%

Source:UnderlyingdatafromBankofInternationalSettlements(BIS).CalculationsandvisualisationbyBenchmarkAnalytics.

36 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Australia’shighprofitabilityisduetomanyfactors,includingapreferencebytheindustryformarginincomerelativetofees.ThiscanbeseeninFigureTwhichcomparesnetinterestincometototalassets.Overthelastfiveyears,Australia’smajorbankshaveaveragedamarginof2%.

FIGURET

NET INTEREST INCOME TO ASSETS5yearaverage(2012-2016)

Source:UnderlyingdatafromBankofInternationalSettlements(BIS).CalculationsandvisualisationbyBenchmarkAnalytics.

USA

Spain

Australia

Canada

Italy

UnitedKingdom

Germany

Sweden

France

Switzerland

Japan

2.25%

2.01%

1.71%

1.56%

1.42%

1.17%

0.97%

0.89%

0.84%

0.79%

0.74% Average

0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60% 1.80% 2.00% 2.20% 2.40%

37 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Incontrasttolendingmargins,Australia’smajorbanksearnarelativelysmallamountoftheirincomefromfees–seeFigureU.Thischartshowsrelativebankingsystem’sshareoffeesrelativetoassets.Lowlevelsoffeesappealtocustomersthatdonotlikepayingaccountfeesorwhoarenetsavers,butontheotherhand,alowrateofnon-interestrevenueputsagreaterburdenonhousingandbusinessborrowerstosupportbankprofitability.

FIGUREU

NET FEES AND COMMISSIONS TO ASSETS5yearaverage(2012-2016)

Source:UnderlyingdatafromBankofInternationalSettlements(BIS).CalculationsandvisualisationbyBenchmarkAnalytics.

Switzerland

USA

Italy

Canada

Germany

Spain

Sweden

UnitkedKingdom

Japan

Australia

France

1.43%

1.18%

0.84%

0.72%

0.69%

0.65%

0.51%

0.46%

0.45%

0.39%

0.37% Average

0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60%0.00%

38 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

TheBISdataalsoshowsthatAustralia’smajorbankshavenon-performingloanratesthatarewellbelowtheaverageofmajorbanksinotherindustrialisedcountries.Overthelastfiveyearsto2016,loanlossprovisionstoassetshaveaveragedjust0.13%.This,ofcourse,reflectstherelativestrengthoftheAustralianeconomyduringtheperiodoftheGFC.Itisnoteworthythatwhilealowfigure,largebanksinfiveothercountrieshaverecordedlowerlevels:UK(0.12%),Germany(0.10%),Sweden(0.07%),Japan(0.05%),Switzerland(0.01%).SeeFigureV.Australianbanksappeartohavehighmarginsdespitelowdefaults.Inotherwords,theexplanationforhighmarginsisnotahighriskenvironment,butratherlikelytobetheabilityofthesebankstoartificiallyraisethemduetopricingpower.

FIGUREV

LOAN LOSS PROVISIONS TO ASSETS5yearaverage(2012-2016)

Source:UnderlyingdatafromBankofInternationalSettlements(BIS).CalculationsandvisualisationbyBenchmarkAnalytics.

Italy

Switzerland

USA

Canada

France

Australia

UnitedKingdom

Germany

Sweden

Japan

Switzerland

0.83%

0.56%

0.26%

0.17%

0.1%

0.13%

0.12%

0.10%

0.07%

0.05%

0.01% Average

0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 0.70% 0.80%0.00% 0.90%

39 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3.6 DOMESTIC MARKETS: HERFINDAHL–HIRSCHMAN INDEX ESTIMATESTheHerfindahl-Hirschmanindex(HHI)isacommonlyacceptedmeasureofmarketconcentration.Itiscalculatedbysquaringthemarketshareofeachfirmcompetinginamarket,andthensummingtheresultingnumbers,andcanrangefromclosetozeroto10,000.TheU.S.DepartmentofJusticeusestheHHIforevaluatingpotentialmergersissues.TheU.S.DepartmentofJusticeconsidersamarketwithanHHIoflessthan1,500tobeacompetitivemarketplace,anHHIof1,500to2,500tobeamoderatelyconcentratedmarketplace,andanHHIof2,500orgreatertobeahighlyconcentratedmarketplace.(http://www.investopedia.com/terms/h/hhi.asp)FigureWshowstheHHIestimatesforthedomesticbankingmarketsinAustralia.UnderlyingdataforthesemarketsisderivedfromAPRA’smonthlystatisticspublication.Thesestatisticsdonotincludecreditunionsorbuildingsocieties,althoughincludingtheseinstitutionsisunlikelytochangetheestimatesbyanymaterialamountgiventhesmallmarketsharesofindividualcreditunions.

Thosemarketsrepresentedbya‘red’barhaveanHHIestimateabove1500,whichisthelevelwherecompetitionconcernsstarttoemerge.OneofthekeymarketsisthatofhousinginvestmentlendingwheretheHHIis1,934.Thisisanimportantdomesticmarketthatisnowsubjecttomacroprudentialruleslimitingcreditgrowthto10%andalsorestrictinginterest-onlylending.Theeffectoftheprudentialrulesistomakeitalmostimpossibleforanynon-majorbankstoincreasemarketshare.

FIGUREW

HHI ESTIMATES - BY PRODUCT CATEGORY (2017)(‘Red’=HHIabove1500)

Source:UnderlyingdatafromAPRAMBS.CalculationsandvisualisationbyBenchmarkAnalytics.

Loanstocommunityserviceorganisations

Loanstogeneralgovernment

Other deposit accounts

Depositsfromcommunityserviceorganisations

Depositsfromgeneralgovernment

Loanstohouseholds:Creditcards

Loanstohouseholds:Housinginvestment

Loanstohouseholds:Other

Deposits from households

Loanstohouseholds:Housing:Owner-oc..

Loanstofinancialcorporations

Depositsfromnon-financialcorporations

Depositsfromfinancialcorporations

Loanstonon-financialcorporations

Certificatesofdeposit

Otherborrowings

Bonds,notesandlong-termborrowings

3,151

500 1000 1500 2000 2500 3000 35000

2,742

2,400

2,390

2,140

1,934

1,803

1,800

1,798

1,947

1,560

1,386

1,365

1,318

1,279

1,472

1,683

1,500

40 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

3.7 FUNDING COSTS AND MARGINSFundingcostsandmargindataarederivedusingAPRA’squarterlyperformancestatistics.Missingdatahasbeenestimatedusingtrendsovertheprevioustwoyearsofdata.Expensestoincomeratioisastandardmeasureofoverallefficiency.Onthismeasure,itappearsthemajorAustralianbankshaveratiosmateriallybelowotherbanks(seeFigureX),buildingsocieties,and credit unions. Otherdatasuggeststhemajorbankshavelowratescomparedtointernationalbanks.Thisisprimarilydrivenbyalargevolumeofbusinessduetomarketsharedominanceandtheabilitytospreadfixedcostsacrossalargecustomerbase.

FIGUREX

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

EXPENSES TO INCOME RATIO

52.40%

200520072009201120132015

MajorbanksOtherbanks75%

70%

65%

60%

55%

50%

45%44.24%

62.42%

66.51%

41 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Interestpaidisanotherkeyindicator,itisaproxyforoverallaveragefundingcosts.TheAPRAdatadoesnotenableacurrentpricecalculation,butanaveragefundingcostcanbeestimatedfromtheincome and asset statistics.FigureYtracesaverageinterestpaid(fundingcosts)bybankssince2004.Asiswellknown,theinterestratespaidonborrowinghasbeenconsistentlylowerformajorbankssincetheGFCin2007.Combinedwithrelativelylowexpensesduetoscale,thisgivesmajorbanksadominantmarketadvantage.

FIGUREY

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

INTEREST RATE PAID

2.38%

200520072009201120132015

MajorbanksOtherbanks

7%

6%

5%

4%

3%

2% 2.20%

4.92%

5.33%

42 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Withlowerexpensesduetoscaleandlowerfundingcosts,themajorbankscanusethatcostadvantagetopricetheirproductsmarginallyundertheaverageofotherbanksinthemarket.Latestdatashowsthemajorbankschargecustomersanaverageof3.93%interestrate,comparedtootherbanksat4.17%.Thisenablesmajorbankstopartlymitigatepotentialmarketsharelossduetoreputational and service levels.FigureZshowsthatpre-GFCandpre-BaselII,themajorbanksonaveragepricedproductsabovethatofotherdeposittakinginstitutions.Note-between2004and2007themajorbankslostmarketshare to smaller rivals.CareneedstobeusedininterpretingFigureZastheaverageinterestreceivedisnotadjustedforassetcomposition.Forexample,someADIswillhaveahigherproportionofbusinessassetswhicharetypicallyriskierandhavehigherinterestratestocompensateforthatrisk.(Foramoreapplestoapplescomparisonofpricing,seehousingratecomparisonsinFigureAA.)Since2007,however,themajorbankshavebeenabletoholdaverageinterestratesbelowotherbanks.BaselII(introducedin2008)islikelytobeakeydriverofthisasitenabledthemajorbankstosimultaneouslyreducemarginsandmaintainthereturnonequity.

FIGUREZ

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

INTEREST RATE RECEIVED

4.17%

200520072009201120132015

MajorbanksOtherbanks

8%

7%

6%

5%

4% 3.93%

6.51%

6.79%

43 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Inthehousinglendingmarket,thedatashowsthemajorbanksarepricinghousingloansatroughlythesameaveragerateasotherdeposit-takinginstitutions–seeFigureAA.Indeed,thelatestdata,whichreflectschangestomortgageriskweights,showsthemajorbankshavestartedtopriceaveragemortgagesaboveotherbanks.

FIGUREAA

INTEREST RATE RECEIVED (HOUSING)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

4.34%

200520072009201120132015

MajorbanksOtherbanks

8%

7%

6%

5%

4% 4.16%

6.78%

6.90%

44 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Thestoryofthemajorbanks’relativeprofitabilitycanbeseeninFigureBB.Hereweseethatthederivednetinterestmargin(NIM)ofthemajorbankshasbeenconsistentlyaboveotherbankssince2004.ThegapwaswidestduringtheGFCasaresultofthedifferentialpricingoftheGovernmentGuarantee,andhasonlyrecentlyconverged.

FIGUREBB

INTEREST MARGIN (ALL LOANS)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

1.80%

200520072009201120132015

MajorbanksOtherbanks

2%

1%

1.74%

1.46%

1.59%

45 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Importantly,theconvergenceintheinterestmargininlendingoverallhasnotbeenseeninthehousingmarket.Themajorbanksmaintainanetinterestmargininhousingloansat2.14%,comparedotherbanksat1.79%.Thisshowstheextentofprofitabilityofmortgagelendingforthemajorbanks.

FIGURECC

INTEREST MARGIN (HOUSING LOANS)

Source:UnderlyingdatafromAPRAQADIPS.CalculationsandvisualisationbyBenchmarkAnalytics.

1.86%

200520072009201120132015

MajorbanksOtherbanks

2%

1%

2.14%

1.79%

1.57%

46 LEVELLING THE PLAYING FIELD IN RETAIL BANKING

Asaresultofthissuperiornetinterestmarginandtheincreasedleverageavailabletoadvancedaccreditedbankspursuinglowerrisk-weightedassetsi.e.housingmortgages,themajorbankshavereturnedconsiderablyhigherreturnsonequitysince2006asseeninFigureDD.(Ofcourse,analysisofNIMideallyalsotakesaccountoflendingcomposition.)

FIGUREDD

NET PROFIT TO SHAREHOLDERS EQUITY