Subject BUSINESS ECONOMICS Paper No and Title 9, Financial ...

15

BUSINESS ECONOMICS PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS MODULE No. :10, MORTGAGED BACKED SECURITIES Subject BUSINESS ECONOMICS Paper No and Title 9, Financial Markets and Institutions Module No and Title 10, Mortgaged Backed Securities Module Tag BSE_P9_M10

Transcript of Subject BUSINESS ECONOMICS Paper No and Title 9, Financial ...

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

Subject BUSINESS ECONOMICS

Paper No and Title 9, Financial Markets and Institutions

Module No and Title 10, Mortgaged Backed Securities

Module Tag BSE_P9_M10

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

TABLE OF CONTENTS

1. Learning Outcomes

2. Introduction

2.1 Benefits of Securitized Debt Instruments

2.2 Yield on Securitized Bonds

3. Process of Securitization

4. Types of Securitized Debt Instruments

4.1 Mortgage Backed Securities (MBS)

4.2 Collateralized Mortgage Obligation (CMO)

5. Structure of Collateralized Mortgage Obligation (CMO)

6. Difference between Fixed Coupon Bonds and Mortgage Bonds

7. Securitization in India

8. Summary

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

1. Learning Outcomes

After studying this module, you shall be able to

Understand the meaning of Securitization and its process

Describe various types of securitized debt instruments like Mortgage Backed Securities (MBS)

and Collateralized Mortgage Obligations (CMO)

Understand the structure of several types of Collateralized Mortgage Obligations

Differentiate between traditional fixed coupon bonds and Mortgage Bonds.

2. Introduction to Securitized Debt Instruments

Banks and financial institutions grant various types of loans which appear on the asset side of their

balance sheet. Securitization is a process in which loans of similar nature are bundled together and

sold to an entity known as special purpose vehicle. This process removes such loans from the balance

sheet of bank or financial institution and enhances their liquidity. Thus they can disburse further loans

with the help of funds generated from sales proceeds received from the sale of bundle of loans. Thus

it leads to availability of more funds with banks which can be further used to disburse fresh loans to

new borrowers. A specific entity, Special Purpose Vehicle (SPV) bundles the new base loans with

similar characteristics and debt securities are issued to investors against the bundle of assets. Because

the bundle of loans is securitized and those debt securities are issued to investors, therefore these debt

instruments are popularly known as securitized debt instruments. The bundle of loans may be

mortgage loans, auto loans, credit card etc. when the debt securities are issued against mortgage loans

then these debt securities are called ‘Mortgage Backed Securities (MBS)’. When the securities are

issued against other bundle of loans like car loans, credit cards and other types of loans, they are

called ‘Asset Backed Securities (ABS)’

2.1 Benefits of Securitization:

Securitization process results into several benefits, which can be described as follows:

a) When the banks or financing company sells the bundled loans to a special purpose entity then the

balance sheet of bank frees from these assets and this allows them to disburse more loans while

meeting their asset-liability matching criterion.

b) Fresh funding is received by the banks, generated from the sale of bundled loans. This infuses

more liquidity in banking system which can be used to disburse more loans to fresh borrowers.

c) Because sufficient liquidity is infused in the system therefore fresh loans may be issued at lower

rate, which benefits the borrowers.

d) The loans or assets which were lying idle on the balance sheet of banks gets converted into

tradable debt securities and thus enhances liquidity in the system.

e) Pooling the assets and distributing the securities among investors leads to diversification of risk

because all the assets in the pool will have varying degree of risk & return.

f) The investors get a new class of debt securities which are more rewarding in comparison to

traditional debt securities albeit with a higher risk.

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

g) Intermediaries benefits from the fee based income and income in the form of spread income

earned by them in this process

2.2 Yield on Securitized Bonds:

Generally the yield on the securitized bonds will be higher than the traditional fixed coupon bonds in

order to attract the investors to invest in these more complicated and risky debt instruments. However

the yield will be lower than the coupon of the bundled mortgages or pool of assets. The yield spread

may be in the form of Z spread in which a constant spread is added to spot rate. The yield spread also

depends upon the embedded options in these bonds. If there is callable or puttable option is there in

which case coupon does not depend upon the path of market interest rate movement, yield spread or

bond pricing can be calculated by using Binomial tree method. When the bond coupons are

influenced by the path of market interest rate movement then Monte-Carlo Simulation has to be used

for bond pricing.

3. Process of Securitization

Banks have several mortgage loans in their loan portfolio. These loans are backed by the property

(residential or commercial) for which these loans were disbursed to borrowers. The bank or finance

company sells these loans to another entity known as special purpose vehicle (Securitization

Company) which will bundle the loans with similar characteristics. This entity will issue the

bonds/debt securities to investors which will be backed by this bundle of mortgage loans. Such debt

securities are known as Mortgage Backed Securities. The coupon on these bonds will be similar but

less than the coupon charged by the bank on mortgage loans. The interest and principal repayment

received from borrowers of these original loans will be used to service these debt securities issued to

investors and to pay the service fee to various intermediaries involved like credit rating agency,

investment banker, trustee, guarantor etc. This can be depicted by the following diagram:

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

These securities are rated by authorized credit rating agencies. They are structured by a structure

normally an investment banker into various classes. He decides the timing and pricing of the issue

based on their rating and capital market conditions. The price of the Mortgage backed securities also

get influenced by market interest rates movement and follow an inverse relationship with the interest

rates. These bundled loans also have the risk of pre payments by the original borrowers whenever

market interest rates falls by a larger extent. Because these borrowers may prepay their costly loans

and refinance it with the prevailing lower rates in the market. Thus these debt securities are affected by

the prepayment risk by the original home buyer in addition to default risk by them and interest rate

risk caused by market interest rate movements. Because of these inherent risks involved many

investors may not have the appetite to invest in these risky securities. Therefore in order to attract the

different categories of investors these securities are structured into different types or tranches where

each tranche has unique risk-return characteristics based on its credit rating and the quality of bundled

mortgages. They are also known as collateralized mortgage obligations (CMOs)

4. Structure of Securitized Debt

4.1 Mortgage Backed Securities (MBS):

The structure of Securitized Debt may be in the form of “pass through” or “pay through”. Mortgage

Backed Securities are backed by bundles of several mortgages of similar characteristics. In US these

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

mortgages are sold to either Government backed agencies like “Fannie Mae” or “Freddie Mac”

“Ginnie Mae” (sponsored by US government)or to some private investment bank.

The majority of MBSs are issued or guaranteed by an agency of the U.S. government such as Ginnie

Mae, or by GSEs, including Fannie Mae and Freddie Mac. MBS carry the guarantee of the issuing

organization to pay interest and principal payments on their mortgage-backed securities. While Ginnie

Mae's guarantee is backed by the "full faith and credit" of the U.S. government, those issued by GSEs

are not.

A third group of MBSs is issued by private firms. These "private label" MBS are issued by subsidiaries

of investment banks, financial institutions, and homebuilders whose credit-worthiness and rating may

be much lower than that of government agencies and GSEs.

These entities securitize the packaged mortgages and sell to investor. In the pass through structure the

interest and principal repayment are periodically received from the home buyers whose mortgages are

pooled and debt securities are issued against them. The investors of mortgage backed securities have

invested in them and the funds received from them are passed to bank and in turn liquidity is created in

the system. However, these MBS have to be paid periodic interest and principal repayment. The cash

flows received from original home buyers are passed to investors of mortgage backed securities in

order to service their periodic interest & principal repayment.

The MBS may be backed by residential mortgages known as Residential Mortgage Backed Securities

(RMBS) and the type of real estate will be individual family real estates. In case of another MBS the

pool of mortgages may contain commercial real estate like offices, business parks, retail commercial

buildings or multi-family apartments. Such MBS is known as Commercial Mortgage Backed

Securities (CMBS)

In case of traditional fixed coupon bonds, investor receives periodic interest and principal is repaid at

maturity in one single instalment. In case of MBS, principal repayment takes place periodically with

every interest payment which may be monthly or quarterly payments the way amortization of home

loans takes place. Therefore the face value of these MBS will also continue to decline with each

periodic payment which has interest and principal component. Initially interest component will be

higher while in later instalments principal component will increase.

There is always a difference in the timing and amount of cash flows received from home buyers and

interest and principal repayments made to MBS investors. In addition to the debt servicing of MBS,

monthly cash flow received from original borrowers have to be used for paying servicing fee, fee to

guarantor, underwriters, structurer, credit enhancers etc. Thus pass through rate offered to MBS

investors is less than the coupon rate of packaged mortgages. Similarly home buyers make their

periodic payments at the beginning of each month while the cash flows are passed on to MBS

investors later.

The pool of mortgages against which MBS has been issued contains the mortgages with different

coupons and different maturities. Therefore the coupon rate offered on MBS is calculated by taking the

weighted average coupon of all the mortgages. To calculate the weighted average coupon following

method is used:

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

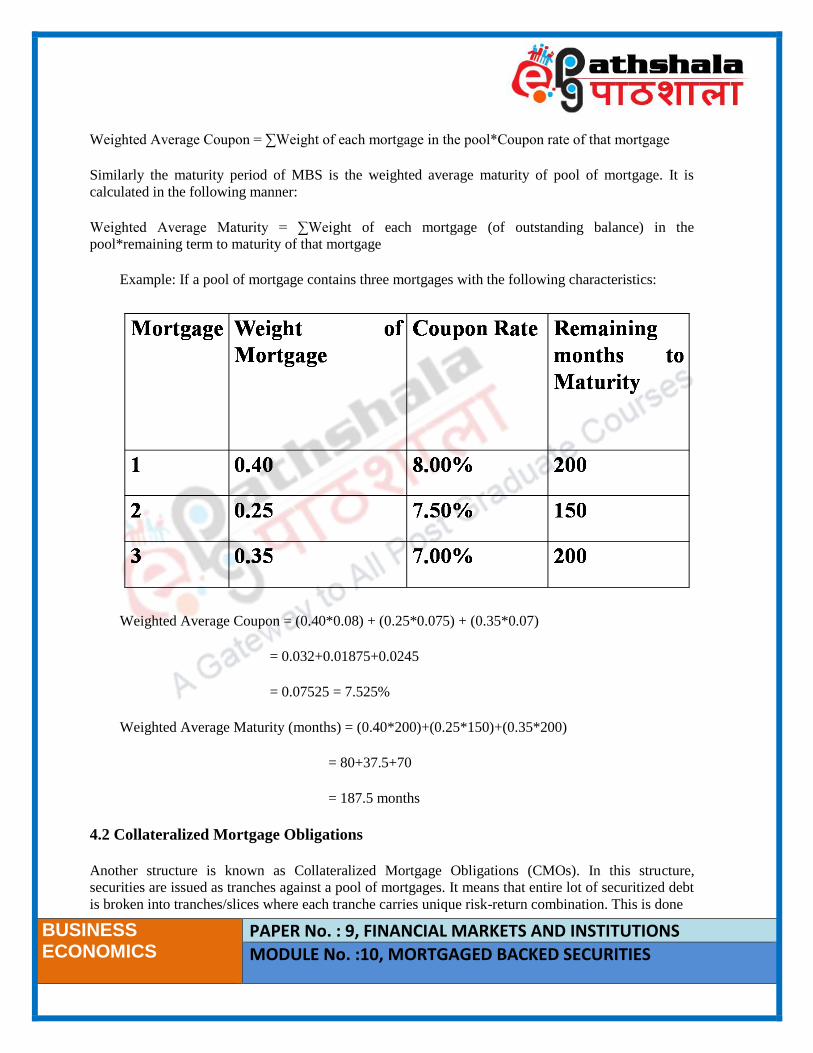

Weighted Average Coupon = ∑Weight of each mortgage in the pool*Coupon rate of that mortgage

Similarly the maturity period of MBS is the weighted average maturity of pool of mortgage. It is

calculated in the following manner:

Weighted Average Maturity = ∑Weight of each mortgage (of outstanding balance) in the

pool*remaining term to maturity of that mortgage

Example: If a pool of mortgage contains three mortgages with the following characteristics:

Weighted Average Coupon = (0.40*0.08) + (0.25*0.075) + (0.35*0.07)

= 0.032+0.01875+0.0245

= 0.07525 = 7.525%

Weighted Average Maturity (months) = (0.40*200)+(0.25*150)+(0.35*200)

= 80+37.5+70

= 187.5 months

4.2 Collateralized Mortgage Obligations

Another structure is known as Collateralized Mortgage Obligations (CMOs). In this structure,

securities are issued as tranches against a pool of mortgages. It means that entire lot of securitized debt

is broken into tranches/slices where each tranche carries unique risk-return combination. This is done

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

because in the market there are different types of investors with different investment needs in terms of

risk-return requirements and investment horizon. Some are concerned that cash flow payments may be

delayed or non-payment may take place because of default risk while some other investors are more

concerned toward the prepayment risk by original home buyer. To meet the needs of different

categories of investors, the cash-flows, payment priorities and risk-return characteristics of debt

securities are delinked from the cash flow and risk-return characteristics of pool of mortgages from

which these debt securities are created. Out of entire pool of mortgages some tranches are issued with

high risk-high return characteristics for which low priority is given for cash flow payments, while

some other offers highest safety reflected by high credit rating and commensurate return with high

priority for the payment of periodic interest & principal and therefore low prepayment or default risk.

This structure doesn’t eliminate the risk, rather it redistributes the risk among different tranches and

investors can invest in a tranche selected, as per their preferences. There is a senior-subordinate

structure to deal with credit risk called credit tranching. The subordinate or junior tranches will absorb

all of the losses, up to their value before senior tranches begin to experience losses. Subordinate

tranches typically have higher yields than senior tranches, due to the higher risk incurred. Investors can

choose which one they want to invest in, according to their risk tolerance and their outlook on the

market. Therefore these tranches attract broader classes of investors in comparison to MBS or pass

through certificates where entire lot offers single risk-return combination. These securities are also

known as Collateralized Debt Obligations (CDO).

5. Structure of Collateralized Mortgage Obligations

There are various types of structures of Collateralized Mortgage Obligations. These structures differ in

terms of distribution of interest, principal, and prepayment received on mortgages among the various

bonds or tranches. These structures are described as follows:

5.1 Sequential-Pay Tranches

In case of Sequential-Pay Tranches, CMO is structured in a manner so that each class of bond can be

repaid sequentially. Monthly coupon, principal and prepayments received on mortgages are distributed

among different tranche in the following manner:

i. All the principal payments and prepayments are first distributed among tranche I. After

tranche I is completely paid off then payment is directed to tranche II and so on.

ii. Monthly coupon received at the beginning of month, on mortgages, is distributed among all

the tranche based on the amount of principal outstanding on them at the beginning of month.

5.2 Accrual Tranches:

In case of Accrual Tranches monthly coupon, principal and prepayments received on mortgages are

distributed among different tranche in the following manner:

a) The coupon received at the beginning of month is distributed on all the tranches based on

their outstanding balance except on one tranche known as Z bonds. The coupon payment

which would have been paid on these Z bond is used to pay-off the principal

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

of other tranche. The coupon payment on these Z bond continue to accrue based on their

principal outstanding and previous months accrued coupon which is added to principal

outstanding, each month.

b) All the principal payments and prepayments are first distributed among tranche I. After

tranche I is completely paid off then payment is directed to tranche II and so on. Once all the

tranches are completely paid-off then principal and all the accrued interest on Z bond is paid

off.

5.3 Floating-Rate Tranches

Floating rate tranches carry a floating rate coupon. Their coupon moves along with the market interest

rates. As their coupon rate movement is aligned with market interest rate movement, their interest rate

risk is quite low. The mortgages from which tranche are created have fixed coupon rate, therefore it is

difficult to create floating rate tranche. In order to create floating rate tranche, a fixed rate tranche is

used and from that a floater and an inverse floater combination is created. Fixed coupon on fixed rate

mortgage is split into floater coupon and inverse floater coupon. The rate is normally linked to a

reference rate for example rate may be LIBOR+ 50 basis point. For floater rate will move along with

reference rate while for inverse floater rate will move in opposite direction of reference rate

movement.

5.4 Structured Interest-Only Tranches:

In this type of CMO structure, a specific tranche is created on which only interest is paid. They are

known as Structured IOs. In order to create Structured IOs, coupon rate of all the tranche is set below

the mortgage’s coupon rate. The excess interest received on mortgages after meeting coupons on all

the other tranches is used to pay the interest on Structure IOs.

In case of Structured Interest Only CMOS, monthly coupon, principal and prepayments received on

mortgages are distributed among different tranche in the following manner:

a) The coupon received at the beginning of month is distributed on all the tranches based on

their outstanding balance except on one tranche known as Z bonds. The coupon payment

which would have been paid on these Z bond is used to pay-off the principal of other tranche.

The coupon payment on these Z bond continue to accrue based on their principal outstanding

and previous months accrued coupon which is added to principal outstanding, each month.

The interest on the Structured IO tranche is paid at the beginning of each month on the basis

of notional amount of outstanding principal on the other tranches.

b) All the principal payments and prepayments are first distributed among tranche I. After

tranche I is completely paid off then payment is directed to tranche II and so on. Once all the

tranches are completely paid-off then principal and all the accrued interest on Z bond is paid

off. On structured IOs no principal payment takes place as they are interest only tranches.

Their notional principal outstanding continues to decline based on the principal payment to

all the other tranches.

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

5.5 Principal-Only (PO) tranches:

Some mortgage securities are created so that investors receive only principal payments generated

by the underlying collateral; the process of separating the interest payments from the principal

payments is called stripping. These Principal-Only (PO) securities may be created directly from

mortgage pass-through securities, or they may be tranches in a CMO. In purchasing a PO, investors

pay a price deeply discounted from the face value and ultimately receive the entire face value

through scheduled payments and prepayments. The market values of POs are extremely sensitive to

prepayment rates. If prepayments accelerate, the value of the PO will increase. On the other hand, if

prepayments decelerate, the value of the PO will drop. A companion tranche structured as a PO is

called a Super PO.

5.6 Planned Amortization Class Tranches

Planned amortization tranches are given highest priorities in terms of payment of periodic principal

& interest. Their cash flows follow a planned pattern and are quite predictable. They have least

exposure to pre-payment or delayed payment risk. This is so because their risk is absorbed by

support tranches. The cash flow payments to PAC tranches are as follows:

a) The periodic monthly coupon payments received form mortgage pool are disbursed to each

tranche based on the principal outstanding of that tranche at the beginning of each month.

b) When the prepayments of mortgages are very low then the principal repayment received from

the pool is first used to repay the planned principal repayment of PAC tranche and any

balance is paid to support tranches. When there are lot of prepayments on the bundled

mortgages then too PAC tranche are paid only the planned principal repayments on them and

any excess cash flow has to be transferred to support tranche. Thus PAC tranche have

minimum prepayment or extension risk as their risk is absorbed by support tranches also

sometimes known as companion tranche.

5.7 Support Tranches

The support tranche as the name implies, provide support to PAC tranche and absorbs their

prepayment and extension risk. Thus they bear maximum extension or contraction risk. In case of

delayed payments from original home buyers they sacrifice their principal repayments so that PAC

tranche planned cash flow payments can be made. In case of heavy prepayments received they

absorb all the excess cash flow payment received so that on PAC tranche only planned cash flow

payment is made. Thus they absorb the highest risk in order to support the PAC tranche and their

cash flows may be quite volatile and unpredictable.

These support tranches can be structured in the form of sequential support tranches, accrual support

tranche, floater and inverse floater tranche, support tranche etc.

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

6. Difference between Mortgage Backed Securities and Fixed-Coupon

Bonds

Traditional Fixed Coupon bonds and Mortgage Bonds can be differentiated on the basis of several

characteristics in the following manner:

7. Securitization in India and Securitization Statistics

In India, Securitization is governed by Securitization and Reconstruction of Financial Assets and

Enforcement of Security Interests Act, 2002 (SARFAESI). The Act aims to simplify the process of

recovery of bad loans from willful defaulters. The Act provides the first legal framework that

recognizes securitization, asset recovery and reconstruction. Securitization market is regulated by RBI

and the guidelines issued by RBI provide a strong regulatory and institutional framework for the

orderly development of the securitization market in the long term.

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

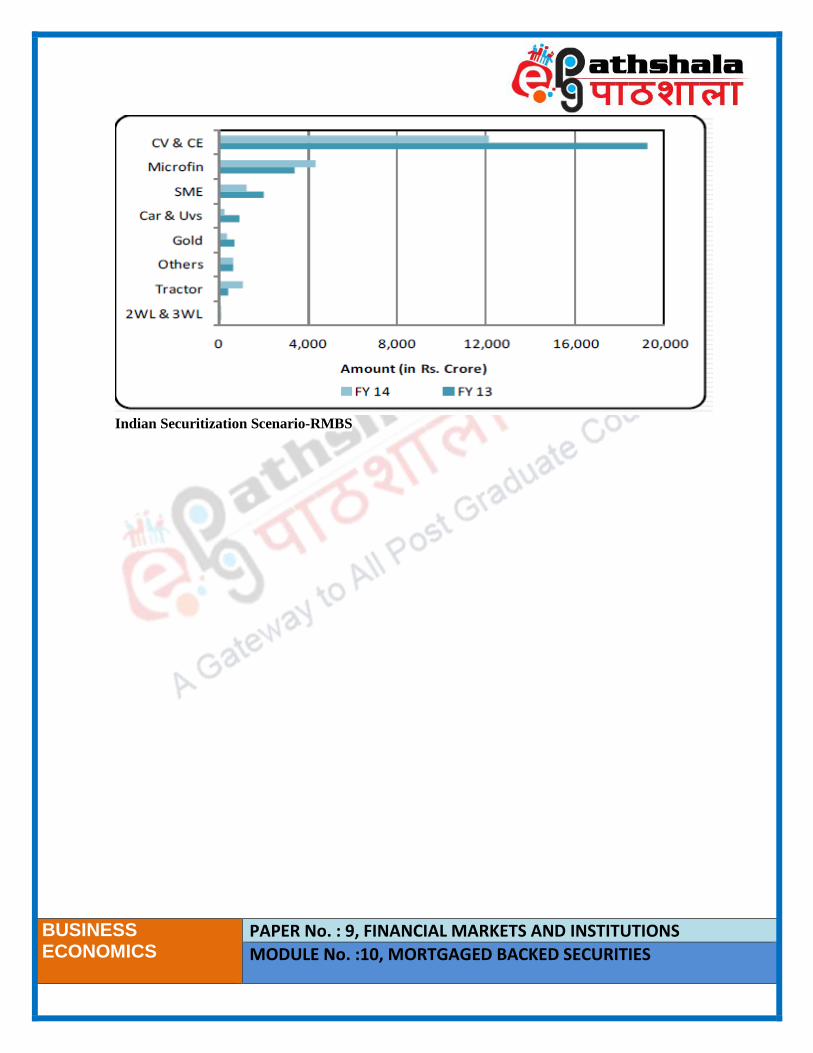

In India Securitization deals are largely dominated by Asset Backed Securitization (ABS) deals and

Residential Mortgage Based Securitization deals constitutes (RMBS) very small proportion of

securitization market in India. In India, the loans which are majorly bundled for securitization are

commercial vehicle loans issued by NBFCs which falls under ABS category. Individual commercial

vehicle loans are normally bundled by NBFCs for securitization purpose.

After the Commercial vehicle loans the next dominant category is micro-finance loans under ABS

category. In these securities the major investors are banks because the debt securities issued against

the pool of micro-finance loans also qualify for priority sector lending for banks. As per RBI

guidelines, Banks have to lend minimum 40% loan portfolio to meet the priority sector lending norms.

Where priority sectors include the agricultural loans and loans disbursed to Small Scale Enterprises. If

a bank is not able to lend 40% of loan portfolio to priority sectors then in order to fulfill the criteria

they can invest in the securitized debt issued against the pool of loans by microfinance institutions

which are qualified as priority sector lending (investments), as per RBI guidelines.

Recently RBI has widened the scope of priority sector lending (PSL) and in addition to agriculture &

Small enterprise lending the loan to medium enterprises, social infrastructure and renewable energy

are also classified as priority sector lending as per revised norms (April’2015). Now banks will be able

to fulfil the PSL requirement on their own and need not to invest in securitized debt securities issued

by microfinance institutions. Thus revised PSL guidelines may have an adverse impact on

microfinance securitized debt subscription by banks.

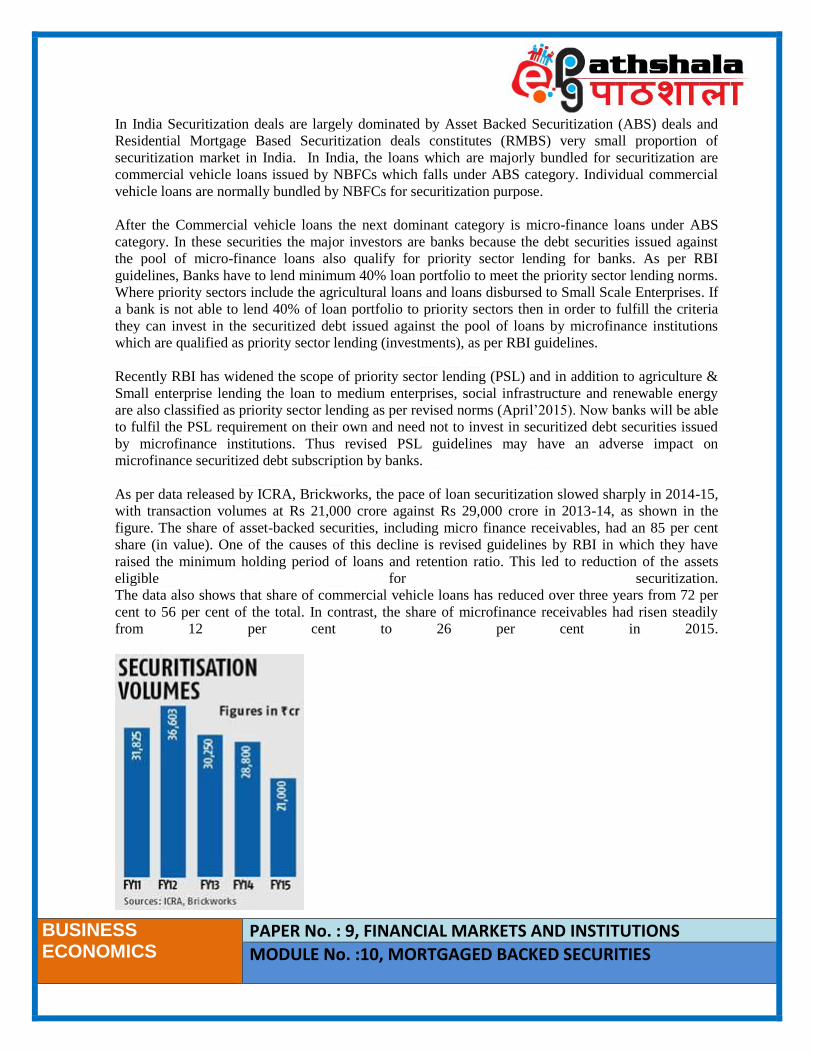

As per data released by ICRA, Brickworks, the pace of loan securitization slowed sharply in 2014-15,

with transaction volumes at Rs 21,000 crore against Rs 29,000 crore in 2013-14, as shown in the

figure. The share of asset-backed securities, including micro finance receivables, had an 85 per cent

share (in value). One of the causes of this decline is revised guidelines by RBI in which they have

raised the minimum holding period of loans and retention ratio. This led to reduction of the assets

eligible for securitization.

The data also shows that share of commercial vehicle loans has reduced over three years from 72 per

cent to 56 per cent of the total. In contrast, the share of microfinance receivables had risen steadily

from 12 per cent to 26 per cent in 2015.

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

Indian Securitization Scenario

Indian Securitization Scenario-ABS

Indian Securitization Scenario-ABS

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

Indian Securitization Scenario-RMBS

BUSINESS ECONOMICS

PAPER No. : 9, FINANCIAL MARKETS AND INSTITUTIONS

MODULE No. :10, MORTGAGED BACKED SECURITIES

8. Summary

Securitization is the process of creating securities by pooling together various cash-flow producing

financial assets. These securities are then sold to investors. Any asset may be securitized as long as it is

cash-flow producing. The terms asset-backed security (ABS) and mortgage-backed security (MBS) are

reflective of the underlying assets in the security. Securitization provides funding and liquidity for a

wide range of consumer and business credit needs. These include securitizations of residential and

commercial mortgages, automobile loans, student loans, credit card financing, equipment loans and

leases, business trade receivables, and the issuance of asset-backed commercial paper, among others.

Securitization transactions can take a variety of forms, but most shares several common characteristics.

Securitizations typically rely on cash flows generated by one or more underlying financial assets (such

as mortgage loans), which serve as the principal source of payment to investors, rather than on the

general credit/claims-paying ability of an operating entity. Securitization allows the entity that originates

or holds the assets to fund those assets efficiently, since cash flows generated by the securitized assets

can be structured, or “tranched,” in a way that can achieve targeted credit, maturity or other

characteristics desired by investors

Asset securitization began when the first mortgage pass-through security was issued in 1970, with a

guarantee by the Government National Mortgage Association (GNMA or Ginnie Mae). The most basic

mortgage securities, known as pass-through or participation certificates (PCs), represent a direct

ownership interest in a pool of mortgage loans. Shortly after this issuance, both the Federal Home Loan

Mortgage Corporation (FHMLC or Freddie Mac) and Federal National Mortgage Association (FNMA or

Fannie Mae) began issuing mortgage securities.

Mortgage pass-through securities may be pooled again to create collateral for a more complex type of

mortgage security known as collateralized mortgage obligations (CMOs). CMOs may also be referred to

as a Real Estate Mortgage Investment Conduit (REMIC). CMOs and REMICs (terms which are often

used interchangeably) are multiclass securities which allow cash flows to be directed so that different

classes of securities with different maturities and coupons can be created. They may be collateralized by

raw mortgage loans as well as already-securitized pools of loans.