Styleguide ProSiebenSat.1 Media AG · Continued increase of TV share in media mix1) Continued...

35

| Page 1 | October 29, 2015 | October 29, 2015 Q3 2015 Press Presentation

Transcript of Styleguide ProSiebenSat.1 Media AG · Continued increase of TV share in media mix1) Continued...

| Page 1| October 29, 2015 |

October 29, 2015

Q3 2015Press Presentation

| Page 2| October 29, 2015 |

October 29, 2015

Thomas Ebeling

Chief Executive Officer

Q3 2015At a Glance

| Page 3| October 29, 2015 | | Page 3| October 29, 2015 |

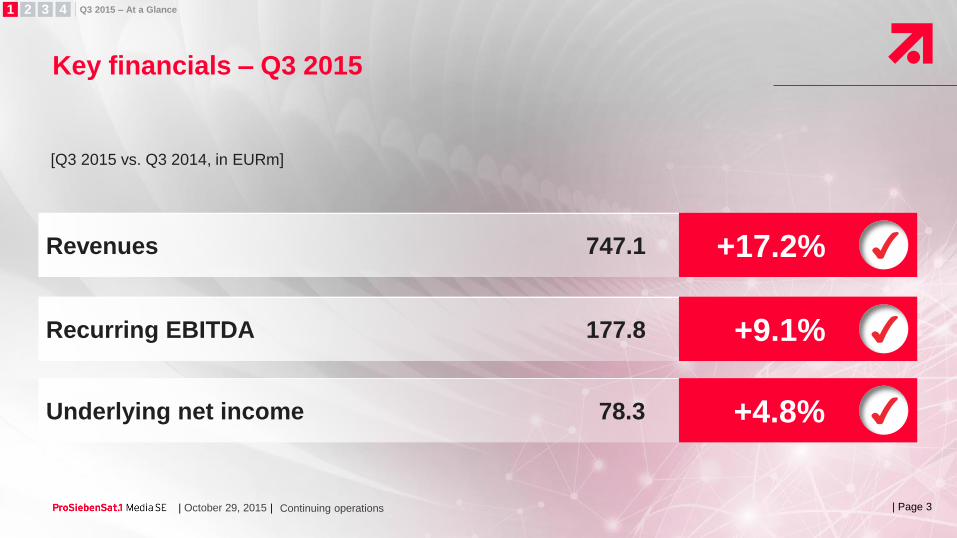

Key financials – Q3 2015

Continuing operations

1 2 3 4 Q3 2015 – At a Glance

[Q3 2015 vs. Q3 2014, in EURm]

Revenues

Recurring EBITDA

Underlying net income

✔

✔

✔747.1

177.8

78.3

+17.2%

+9.1%

+4.8%

| Page 4| October 29, 2015 | | Page 4| October 29, 2015 |

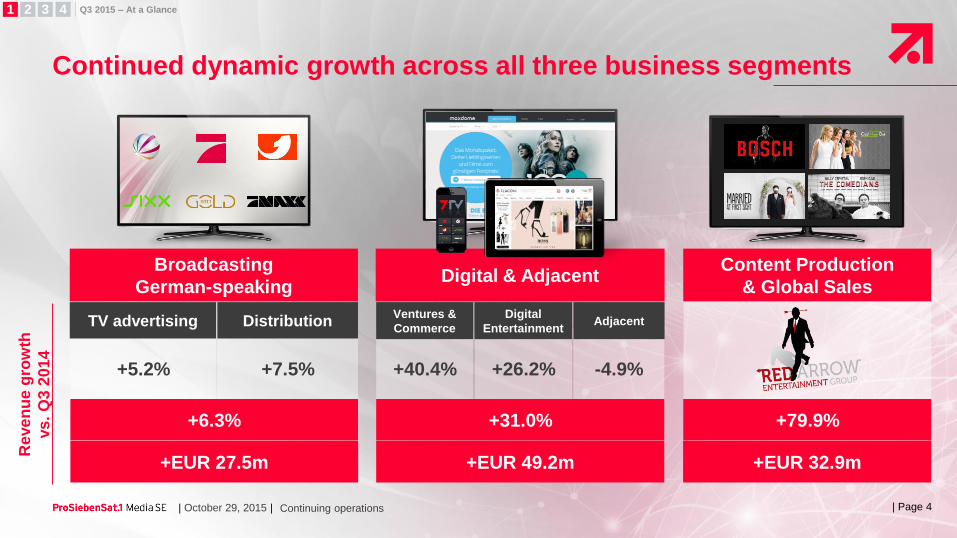

Continued dynamic growth across all three business segments

Continuing operations

1 2 3 4 Q3 2015 – At a Glance

Content Production

& Global Sales

+EUR 32.9m

Reve

nu

e g

row

th

vs

. Q

3 2

01

4

Broadcasting

German-speaking

DistributionTV advertising

+5.2% +7.5%

+EUR 27.5m

+6.3%

Digital & Adjacent

Ventures &

Commerce

Digital

EntertainmentAdjacent

+40.4% +26.2% -4.9%

+EUR 49.2m

+31.0% +79.9%

| Page 5| October 29, 2015 | | Page 5| October 29, 2015 |

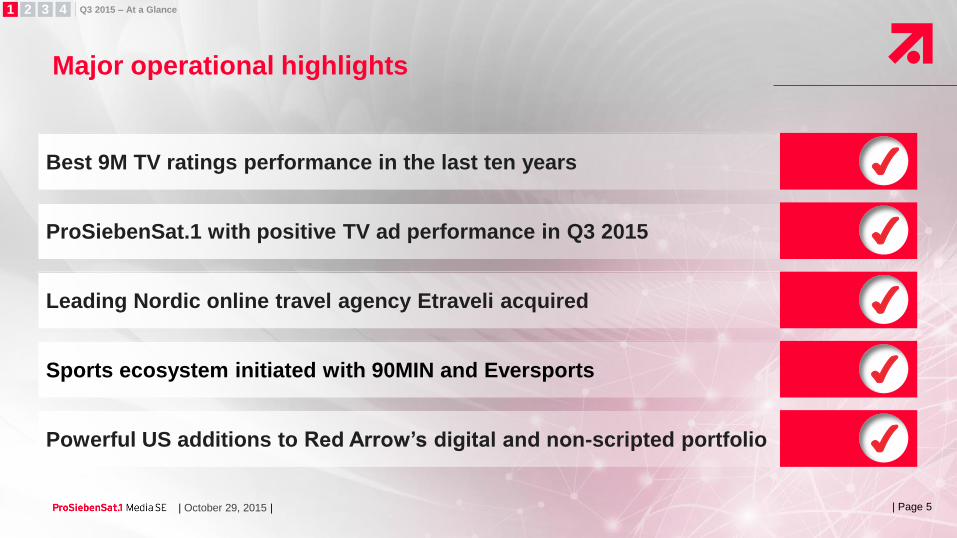

Major operational highlights

1 2 3 4 Q3 2015 – At a Glance

Sports ecosystem initiated with 90MIN and Eversports ✔

Powerful US additions to Red Arrow’s digital and non-scripted portfolio ✔

ProSiebenSat.1 with positive TV ad performance in Q3 2015 ✔

Leading Nordic online travel agency Etraveli acquired ✔

Best 9M TV ratings performance in the last ten years ✔

| Page 6| October 29, 2015 | | Page 6| October 29, 2015 |

Degree of achievement of new 2018 targets

Continuing operations

2012-18 revenue growth target, degree of achievement[achievement based on 9M 2015, in EUR m]

209392

183

784

Broadcasting

German-speaking

Digital & Adjacent

1,200

375

Content Production

& Global Sales

1,850

67%

Achievement by 9M 2015

Current CMD 2018 target

33%56% 42%X% Target achievement in %

275

1 2 3 4 Q3 2015 – At a Glance

46%Linear extrapolation

of new 2018 target

| Page 7| October 29, 2015 | | Page 7| October 29, 2015 |

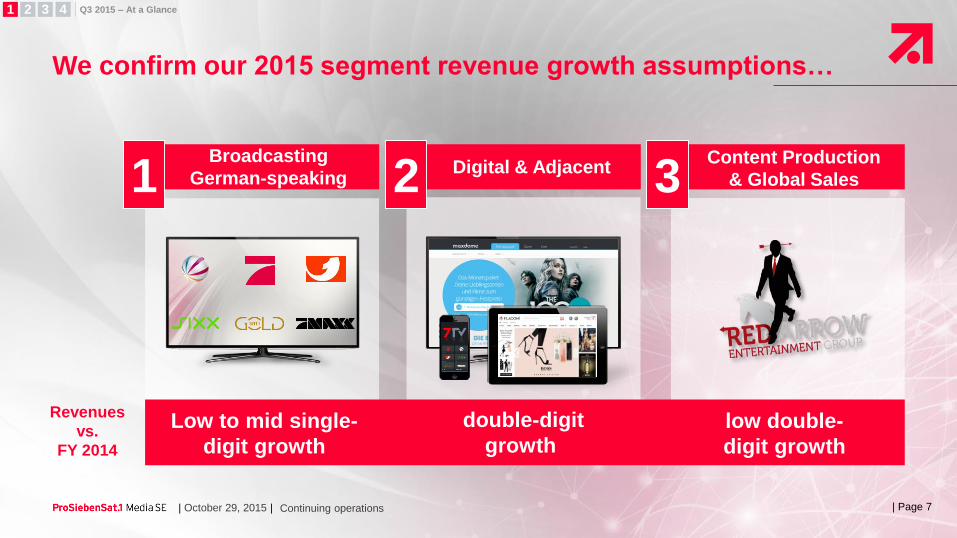

We confirm our 2015 segment revenue growth assumptions…

Continuing operations

1 2 3 4 Q3 2015 – At a Glance

Digital & Adjacent Content Production

& Global Sales 1 2 3Broadcasting

German-speaking

Revenues

vs.

FY 2014

Low to mid single-

digit growth

double-digit

growthlow double-

digit growth

| Page 8| October 29, 2015 | | Page 8| October 29, 2015 |

… and raise our positive full-year guidance

Continuing operations

1 2 3 4 Q3 2015 – At a Glance

Recurring EBITDA and underlying net income above prior year ✔

Ad performance at least in line with positive net TV ad market ✔

Digital & Adjacent with double-digit revenue growth ✔

Low double-digit Group revenue growth ✔

| Page 9| October 29, 2015 |

October 29, 2015

Dr. Gunnar Wiedenfels

Chief Financial Officer

Q3/9M 2015Financial Performance Review

| Page 10| October 29, 2015 | | Page 10| October 29, 2015 |

Q3 2015: continued high single-digit recurring EBITDA increase

Continuing operations

1 2 3 4 Q3/9M 2015 – Financial Performance Review

0

200

400

600

800

0

100

200

300

177.8162.9

+17.2%

Q3 2015

637.5

747.1

Q3 2014

Consolidated revenues

[in EUR m]

Recurring EBITDA

[in EUR m]

Q3 2015Q3 2014

Recurring EBITDA margin:

23.8% (-1.8%pts)

+9.1%

| Page 11| October 29, 2015 | | Page 11| October 29, 2015 |

9M 2015: strong revenue and recurring EBITDA improvement

Continuing operations

0

500

1,000

1,500

2,000

2,500

0

200

400

600

800

568.1522.2

+13.8%

9M 2015

1,909.72,174.2

9M 2014

Consolidated revenues

[in EUR m]

Recurring EBITDA

[in EUR m]

9M 20159M 2014

Recurring EBITDA margin:

26.1% (-1.2%pts)

+8.8%

1 2 3 4 Q3/9M 2015 – Financial Performance Review

| Page 12| October 29, 2015 | | Page 12| October 29, 2015 |

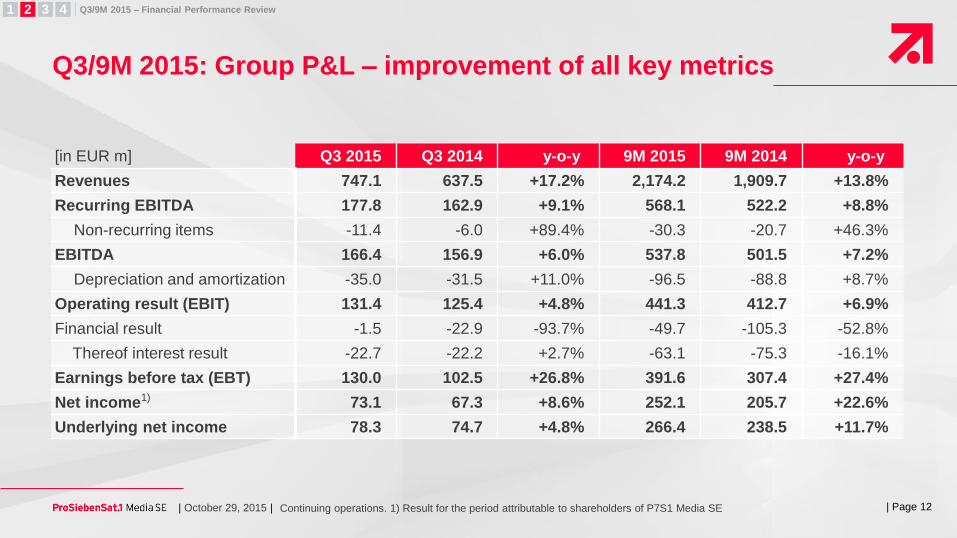

Q3/9M 2015: Group P&L – improvement of all key metrics

Continuing operations. 1) Result for the period attributable to shareholders of P7S1 Media SE

[in EUR m] Q3 2015 Q3 2014 y-o-y 9M 2015 9M 2014 y-o-y

Revenues 747.1 637.5 +17.2% 2,174.2 1,909.7 +13.8%

Recurring EBITDA 177.8 162.9 +9.1% 568.1 522.2 +8.8%

Non-recurring items -11.4 -6.0 +89.4% -30.3 -20.7 +46.3%

EBITDA 166.4 156.9 +6.0% 537.8 501.5 +7.2%

Depreciation and amortization -35.0 -31.5 +11.0% -96.5 -88.8 +8.7%

Operating result (EBIT) 131.4 125.4 +4.8% 441.3 412.7 +6.9%

Financial result -1.5 -22.9 -93.7% -49.7 -105.3 -52.8%

Thereof interest result -22.7 -22.2 +2.7% -63.1 -75.3 -16.1%

Earnings before tax (EBT) 130.0 102.5 +26.8% 391.6 307.4 +27.4%

Net income1) 73.1 67.3 +8.6% 252.1 205.7 +22.6%

Underlying net income 78.3 74.7 +4.8% 266.4 238.5 +11.7%

1 2 3 4 Q3/9M 2015 – Financial Performance Review

| Page 13| October 29, 2015 | | Page 13| October 29, 2015 |

Updated financial targets for 2015

Continuing operations 1) previously “high single-digit”

Financial leverage 1.5x – 2.5x

Recurring EBITDA above prior year

Underlying net income above prior year

Group revenue growth low double-digit1)

1 2 3 4 Q3/9M 2015 – Financial Performance Review

| Page 14| October 29, 2015 |

October 29, 2015

Thomas Ebeling

Chief Executive Officer

Broadcasting German-speakingTV Performance

| Page 15| October 29, 2015 | | Page 15| October 29, 2015 |

Strong ratings growth across German-speaking markets

Basis for GER: All German TV households (Germany + EU), A 14-49 years; Mon-Sun, full day 3-3h. Source: AGF in

cooperation with GfK / TV Scope / ProSiebenSat.1 TV Deutschland. Basis for CH: D-CH; A 15-49; Mon-Sun, full day.

Source: Mediapulse TV-Panel. Basis for A: A 12-49; Mon-Sun, full day 3-3h, P7 MAXX Austria and S1 Gold Austria (both

from Jul 15, 2014, onward). Source: AGTT / GfK: Fernsehforschung / Evogenius Reporting.

Q3 2014

Germany 29.3%

Austria 22.1%

Switzerland 17.7%

Q3 2015

30.1%

23.5%

17.9%

Audience share (A14-49)[in %]

1 2 3 4 Broadcasting German-speaking / TV Performance

| Page 16| October 29, 2015 | | Page 16| October 29, 2015 |

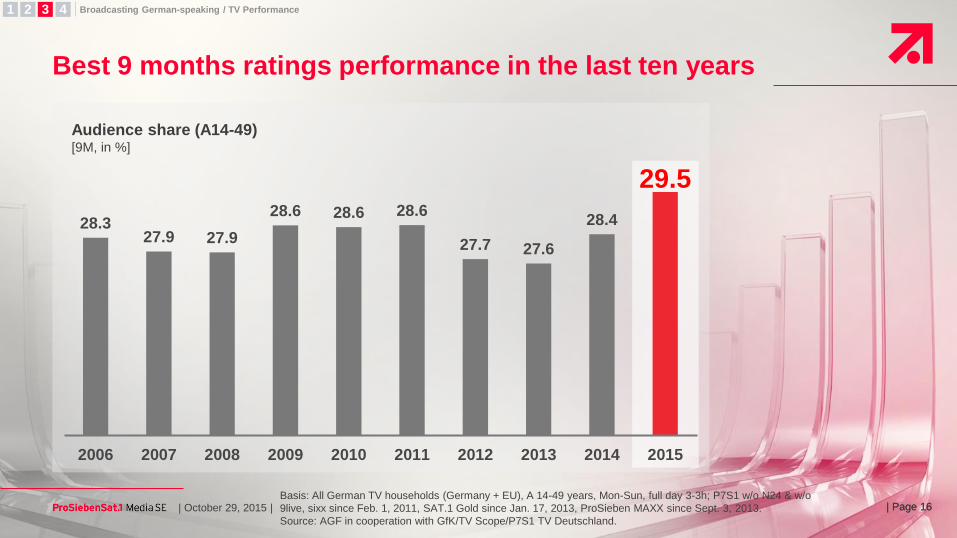

Audience share (A14-49)[9M, in %]

Best 9 months ratings performance in the last ten years

28.327.9 27.9

28.6 28.6 28.6

27.7 27.6

28.4

29.5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

| Page 16Basis: All German TV households (Germany + EU), A 14-49 years, Mon-Sun, full day 3-3h; P7S1 w/o N24 & w/o

9live, sixx since Feb. 1, 2011, SAT.1 Gold since Jan. 17, 2013, ProSieben MAXX since Sept. 3, 2013.

Source: AGF in cooperation with GfK/TV Scope/P7S1 TV Deutschland.

1 2 3 4 Broadcasting German-speaking / TV Performance

| Page 17| October 29, 2015 | | Page 17| October 29, 2015 |

New Disney volume deal fortifies access to top license supplyExamples

Multi-year volume deals with 6 out of 8 US major studios with key TV program

secured well beyond 2019

1 2 3 4 Broadcasting German-speaking / TV Performance

Features

Series

NEW

(sitcoms)

| Page 18| October 29, 2015 |

October 29, 2015

Thomas Ebeling

Chief Executive Officer

Broadcasting German-speakingAd Market Performance

| Page 19| October 29, 2015 | | Page 19| October 29, 2015 |

Positive development 9M 2015

1) Source: Nielsen; gross figures excluding YouTube and Facebook.

1 2 3 4 Broadcasting German-speaking / Ad Market Performance

Continued increase of TV share in media mix1) ✔

Continued positive net pricing development ✔

German-speaking TV advertising revenue growth of 3.9% y-o-y with

Q3 accelerated growth of 5.2% y-o-y ✔

P7S1 gained advertising share in Q3. This trend is expected to

continue in Q4 ✔

9M German net TV ad market growth in line with full year expectation

of 2-3% ✔

| Page 20| October 29, 2015 | | Page 20| October 29, 2015 | Q3: Jul-Sep | Source: Nielsen Media Research (Germany), Media Focus (Austria, Switzerland). | Page 20

1 2 3 4 Broadcasting German-speaking / Ad Market Performance

Switzerland

Austria

Germany

ProSiebenSat.1 gross TV advertising market share

[in %]

Advertising share gains in all German-speaking markets

Q3 2014 Q3 2015

24.4%

43.8%

36.7%

28.1%

45.5%

37.5%

| Page 21| October 29, 2015 | | Page 21| October 29, 2015 |

Sales outlook 2015

1 2 3 4 Broadcasting German-speaking / Ad Market Performance

3

1

2

4

German net TV advertising market growth of 2-3%

P7S1 to grow above market

Net CPTs to further increase due to increased value of reach

Continued increase of TV share in media mix

| Page 22| October 29, 2015 |

October 29, 2015

Digital & Adjacent

Thomas Ebeling

Chief Executive Officer

| Page 23| October 29, 2015 | | Page 23| October 29, 2015 |

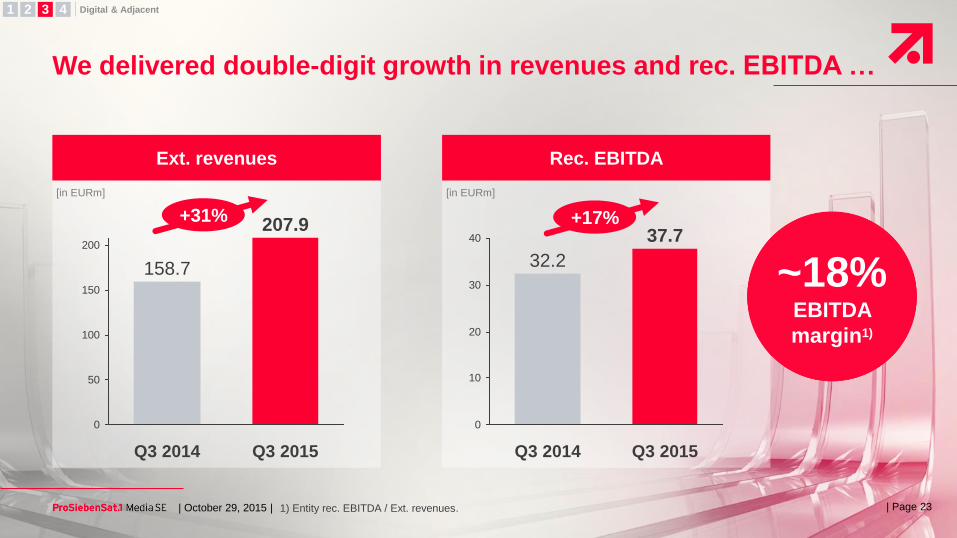

We delivered double-digit growth in revenues and rec. EBITDA …

1) Entity rec. EBITDA / Ext. revenues.

Ext. revenues Rec. EBITDA

[in EURm] [in EURm]

0

50

100

150

200

Q3 2015

207.9

Q3 2014

158.7

0

10

20

30

40

Q3 2014

32.2

Q3 2015

37.7

~18%EBITDA

margin1)

+31% +17%

1 2 3 4 Digital & Adjacent

| Page 24| October 29, 2015 | | Page 24| October 29, 2015 |

… driven by strong performance of Commerce and Entertainment

Revenues

[Q3 2015]

Revenue growth

[Q3 2015 vs.

Q3 2014]

Digital

Entertainment

EUR

67.3m

+26%

Adjacent

EUR

15.4m

-5%

Ventures &

Commerce

EUR

125.2m

+40%

1 2 3 4 Digital & Adjacent

| Page 54

| Page 25| October 29, 2015 | | Page 25| October 29, 2015 |

We have leading market positions across all our D&A pillars

1) Studio71 is #1 MCN in Germany, together with CDS top 5 globally. 2) Yieldlab is #1 Premium SSP in DACH. 3) SVoD

market Germany, according to Forsa. 4) Mobile and PC games publishers in Europe, excluding direct publishing by

developers, P7S1 estimates. 5) Etraveli and Vitafy signed with envisaged closing in Q4; Vitafy is a minority investment only

| Page 25

Market position

PayVoD GamesAdVoDTravel

vertical

New

verticalsVentures

AdjacentDigital EntertainmentVentures & Commerce

Music, Artist Mgmt.,

Live, Licensing

#4#1

Top

5

#2

Top

5

#1

#1

#2

#1

Beauty & Accessories

#1

#1

#1

Online Comparison

Other assets

Top

5

Top

33)

Top

34)

#1

Top

3

#2

#1

#11)

Leading German

VC investor

#1(M4R/E)

60.2% 32.4% 7.4%Q3 2015

revenue

split

A B C

#12)

1 2 3 4 Digital & Adjacent

Top

5

Video innovation hub New5)

#1

#1New5)

| Page 26| October 29, 2015 | | Page 26| October 29, 2015 |

In Travel, we acquired the leading Nordics online travel agency

1) P7S1 stake. 2) FY 2014 figures. Note: Signed with envisaged closing in Q4.

A

1 2 3 4 Digital & Adjacent

100%1)

40countries

1.6mtrips

per year

~1bnEUR gross

bookings2)

~70mEUR

revenues2)

What Etraveli is

Etraveli is a leading online travel

agency for flights in the Nordics

with 12 brands in 40 countries

Services include airline ticketing

and hotel bookings

| Page 27| October 29, 2015 | | Page 27| October 29, 2015 |

Etraveli closes the blank spot ‘flights’ in our 7Travel value chain

1 2 3 4 Digital & Adjacent

A

Why we acquired

We complement our online travel

vertical and close the blank spot

“flight search” in our customer journey

Etraveli enables a profitable, low risk

internationalization of Travel based

on a cost efficient platform strategy

Build new brand for Etraveli meta

business in Germany leveraging TV

Inspiration

Search

Booking

In Destination

NEW

Customer journey

| Page 28| October 29, 2015 | | Page 28| October 29, 2015 |

In Digital Entertainment, we have seen great achievements B

Maxdome with strong

growth in all dimensions

New ad tech

profit center

Market leading in

Premium Video

Building knowledge in

video innovation

#1

1 2 3 4 Digital & Adjacent

#1 MCN in Germany

#1

| Page 29| October 29, 2015 | | Page 29| October 29, 2015 |

maxdome has grown strongly in all dimensions

1) End of period Q3 2015 vs. PY. 2) Q3 2015 vs. PY. 3) Ø of period Q3 2015 vs. PY.

Total

video views2)

Total

user base3)

+35%

B

SVoD

subscribers1)

1 2 3 4 Digital & Adjacent

+65%+95%

| Page 30| October 29, 2015 | | Page 30| October 29, 2015 |

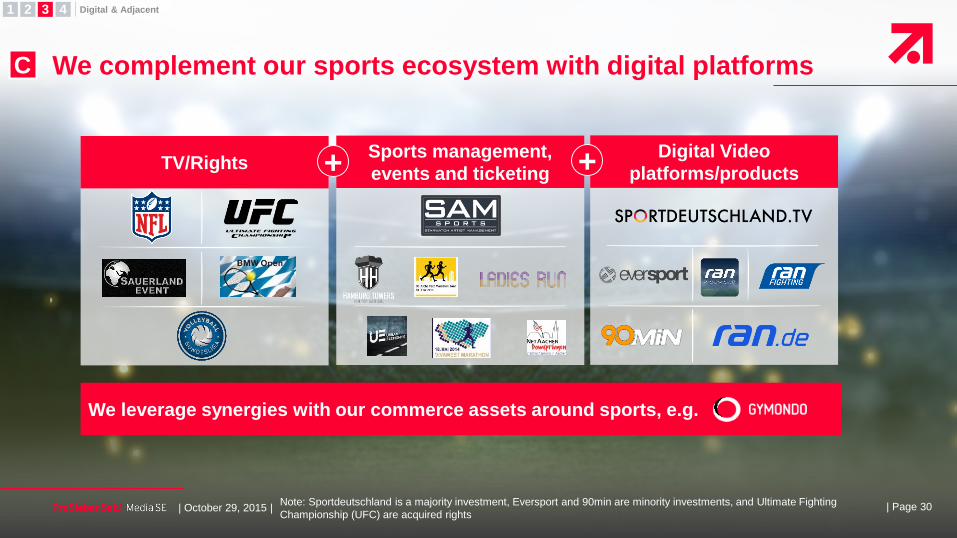

We complement our sports ecosystem with digital platforms

Note: Sportdeutschland is a majority investment, Eversport and 90min are minority investments, and Ultimate Fighting

Championship (UFC) are acquired rights

C

1 2 3 4 Digital & Adjacent

Sports management,

events and ticketing

We leverage synergies with our commerce assets around sports, e.g.

Digital Video

platforms/productsTV/Rights + +

| Page 31| October 29, 2015 | | Page 31| October 29, 2015 |

Digital & Adjacent – outlook

Deliver double-digit revenue growth in FY 2015

Build new digital verticals

Further internationalize with innovative imports and exports

1

2

3

1 2 3 4 Digital & Adjacent

| Page 32| October 29, 2015 |

October 29, 2015

Thomas Ebeling

Chief Executive Officer

Q3 2015Summary & Outlook

| Page 33| October 29, 2015 | | Page 33| October 29, 2015 |

We raise our positive full-year guidance

Continuing operations.

Recurring EBITDA and underlying net income above prior year ✔

Ad performance at least in line with positive net TV ad market ✔

Digital & Adjacent with double-digit revenue growth ✔

Low double-digit Group revenue growth ✔

1 2 3 4 Summary & Outlook

| Page 34| October 29, 2015 | | Page 34| October 29, 2015 |

Disclaimer

This presentation contains "forward-looking statements" regarding ProSiebenSat.1 Media SE ("ProSiebenSat.1")or ProSiebenSat.1 Group, including opinions, estimates and projections regarding ProSiebenSat.1's orProSiebenSat.1 Group's financial position, business strategy, plans and objectives of management and futureoperations. Such forward-looking statements involve known and unknown risks, uncertainties and other importantfactors that could cause the actual results, performance or achievements of ProSiebenSat.1 or ProSiebenSat.1Group to be materially different from future results, performance or achievements expressed or implied by suchforward-looking statements. These forward-looking statements speak only as of the date of this presentation andare based on numerous assumptions which may or may not prove to be correct.

No representation or warranty, expressed or implied, is made by ProSiebenSat.1 with respect to the fairness,completeness, correctness, reasonableness or accuracy of any information and opinions contained herein. Theinformation in this presentation is subject to change without notice, it may be incomplete or condensed, and itmay not contain all material information concerning ProSiebenSat.1 or ProSiebenSat.1 Group. ProSiebenSat.1undertakes no obligation to publicly update or revise any forward-looking statements or other information statedherein, whether as a result of new information, future events or otherwise.

| Page 35| October 29, 2015 |