Study of Homeowner, Commercial Property, Liability, and Marine ...

69

Study of Homeowner, Commercial Property, Liability, and Marine Insurance Prepared for the Government of Newfoundland and Labrador MERCER OLIVER WYMAN ACTUARIAL CONSULTING, LTD. April 2004

Transcript of Study of Homeowner, Commercial Property, Liability, and Marine ...

Study of Homeowner,

Commercial Property,

Liability, and Marine

Insurance

Prepared for the Government of Newfoundland and Labrador

MERCER OLIVER WYMAN ACTUARIAL CONSULTING, LTD.

April 2004

Addendum Please note on Page 52 under the heading Oil Tanks the statement ��but that it does not require inspection and registration of oil tanks until March 2007� applies to existing oil tanks only. All new oil tanks require inspection and registration effective the date the regulations came into effect, April 2002.

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Contents

1. Introduction....................................................................................................................1

1.1 – Background.....................................................................................................1 1.2 – Study Scope, Caveats, And Limitations .........................................................4 1.3 – The Insurance Products That Are The Subject of This Study ........................6 1.4 – Affordability And Availability .......................................................................7 1.5 – Hard Market ....................................................................................................9

2. The Situation in Newfoundland and Labrador.............................................................11

2.1 – Historical Profitability of Homeowners Insurance, Commercial Property Insurance, Commercial Liability Insurance, and Marine Insurance .............11

2.2 – Newfoundland and Labrador Complaint Log ...............................................26 2.3 – Discussion with the Insurance Brokers Association of Newfoundland

(IBAN) ..........................................................................................................27 2.4 – Insurance Company Operations within the Province....................................29

3. Insurance Regulation ...................................................................................................32

3.1 – Goals of Insurance Regulation......................................................................32 3.2 – How Government Regulates Insurance ........................................................33 3.3 – Pros and Cons of Insurance Regulation ........................................................38

4. Ways to Address Availability and Affordability Problems .........................................39

4.1 – Residual Market Mechanisms.......................................................................39 4.2 – Additional Risk Spreading Mechanisms.......................................................42 4.3 – Other Ways to Deal With Affordability or Availability Problems ...............45

5. Recommendations........................................................................................................47

5.1 – Conclusions...................................................................................................47 5.2 – Recommendations as Respects Rates ...........................................................48 5.3 – Recommendations as Affordability and Availability Issues.........................50 5.4 – Recommendations Regarding Rate Regulation ............................................55 5.5 – Other Recommendations...............................................................................56

6. Appendix 1…………………………………………………………………………...57

Definition of Key Terms………………………………………………………... 57

7. Appendix 2……………………………………………………………………….…. 60

Exhibits…………………………………………………………………………. 60

i

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

CHAPTER 1

Introduction 1.1 – Background The Government of Newfoundland and Labrador (the Government) retained Mercer Oliver Wyman Actuarial Consulting, Ltd. (Mercer) for actuarial consulting assistance related to homeowner insurance, commercial property insurance, commercial liability insurance, and marine insurance. The Government is concerned about the affordability and availability of these insurance products, which are important to the financial well being of individuals and businesses in the province. Specifically, we were asked to conduct a study to address the following:

Review the history of the profitability of these insurance products in the province over the past five years.

Comment on the reasonableness of the profits realized by insurance companies, as identified

above.

Comment on whether insurance companies operate reasonably within the province in accepting risks for these insurance products, in relation to their profitability.

Recommend ways to ensure that these insurance products are available to the public,

including the feasibility of a risk sharing pool.

Make recommendations regarding the feasibility of regulating rates for these insurance products.

1

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

The principal research and findings of our analysis are contained in the following sections of this report, which should be read sequentially.

CHAPTER 1 – INTRODUCTION Section 1.1 - Background Section 1.2 - Study Scope, Caveats, and Limitations - This section contains information that

should be fully understood before taking action on any findings or recommendations contained in this report.

Section 1.3 - The Products That are the Subject of This Study - This section explains the four

insurance products that we have studied. Section 1.4 - Affordability and Availability - In this section we present and define the issues of

affordability and availability. Section 1.5 - Hard Market - In this section we discuss general reasons that lead to affordability

and availability problems.

CHAPTER 2 – THE SITUATION IN NEWFOUNDLAND AND LABRADOR Section 2.1 - Historical Profitability of Homeowners Insurance, Commercial Property

Insurance, Commercial Liability Insurance, and Marine Insurance - In this section we present the historical profitability for these insurance products in the province.

Section 2.2 - Newfoundland and Labrador Complaint Log - In this section we present

information that we compiled from a review of the insurance complaint log maintained by the Department of Government Services.

2

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Section 2.3 - Discussion With the Insurance Brokers Association of Newfoundland - In this section we present the thoughts and comments of representatives of IBAN regarding the market within the province for the four insurance products.

Section 2.4 - Insurance Company Operations Within the Province - In this section we offer our

comments, based on the information we have obtained and reviewed, as to whether insurance companies are operating reasonably within the province in accepting risks for the four insurance products, in relation to their profitability.

CHAPTER 3 – INSURANCE REGULATION Section 3.1 - Goals of Insurance Regulation - In this section we present the key reasons for

government regulation. Section 3.2 - How Insurance is Regulated - In this section we present a general overview of

insurance regulation. Section 3.3 - The Pros and Cons of Insurance Regulation - In this section we conclude our

general discussion of insurance regulation by presenting some advantages and disadvantages of government regulation of insurance.

CHAPTER 4 - WAYS TO ADDRESS AVAILABILITY AND AFFORDABILITY

PROBLEMS Section 4.1 - Residual Market Mechanisms - In this section we identify several systems that

have been established in other jurisdictions to provide insurance to risks that are not adequately serviced by the insurance industry.

Section 4.2 - Additional Risk Spreading Mechanisms - In this section we present other

alternative ways for transferring or financing insurance risk.

3

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Section 4.3 - Other Ways to Deal With Availability and Affordability Problems - In this section we discuss two other ways that government can deal with the issues of availability and affordability.

CHAPTER 5 – RECOMMENDATIONS

Section 5.1 - Recommendations - In this section we present our recommendations as to how the Government should address any availability or affordability problems that may exist.

APPENDIX 1 – DEFINITION OF KEY TERMS - This appendix is a convenient

reference for those who are not familiar with the insurance terms we use in this report.

APPENDIX 2 – EXHIBITS - In this appendix we present various exhibits and graphs that

supplement the information we present in the report.

1.2 – Study Scope, Caveats, And Limitations This section contains what we generally designate as “scope, caveats and limitations.” These are items that define the boundaries of what we do and what we don’t do in this study, and describe a number of elements and cautions that the reader should keep in mind while reading this report. The scope, caveats, and limitations listed below apply to our entire report.

4

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

General Scope The proper interpretation of this report, and the validity of any conclusions drawn from it, are highly dependent on a complete understanding of the scope of this project. The scope is defined in a number of ways, as discussed below.

Distribution This report was prepared for the Government of Newfoundland and Labrador. Permission is granted for the report to be distributed to other parties; however, the report must be distributed in its entirety.

Data Reliance This analysis is based largely on aggregate insurance industry data for Newfoundland and Labrador as compiled by the Office of the Superintendent from information presented in the P&C-1 and P&C-2 reports prepared by insurance companies. We rely on the accuracy and completeness of this information.

Insurance Products This report deals with four major insurance products. [In this report we also refer to these products as lines of insurance or insurance coverages.] The first is homeowners, which is reported as a part of the personal property line of insurance in the P&C-1 and P&C-2 reports, and not separately identified. Included in the personal property line of insurance are other insurance products such as tenants insurance and condominium insurance. The other three lines of insurance reviewed in this study are commercial property, commercial liability, and marine, each of which is reported as a separate line of insurance in the P&C-1 and P&C-2 reports.

5

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Aggregates and Averages This analysis is based, in part, on experience of all insurance companies, and our findings regarding profitability are for all insurance companies, on average. Our conclusions may not be applicable to any specific insurance company.

Provisions For Expenses, Investment Income, and Profit The assumptions that we make in this study regarding provisions for expenses, investment income, and profit are made for the purpose of measuring the historical profitability of the four insurance products. We believe our assumptions are reasonable for this purpose. The findings in this study should not be construed as recommendations for any specific level of insurance industry expenses or profits.

Input by Stakeholders In developing our findings and recommendations, we reviewed the log of complaints made by consumers as compiled by the Department of Government Services, and discussed the current market availability and affordability issues with representatives of the Insurance Brokers Association of Newfoundland and Labrador, who interact with insurers and consumers.

1.3 – The Insurance Products That Are The Subject of This Study The wording (i.e., contractual obligation between the insurance company and insured) for the insurance products that are included in this study is not subject to legislative or regulatory requirements. As such, the actual products (i.e., what is insured and what is not insured) may vary from insurance company to insurance company. Homeowners Insurance – Homeowners insurance combines real and personal property coverage with personal liability coverage. While the exact wording may vary by insurer, it generally provides insurance against damage to the home and its contents, as well as for the legal responsibility for any

6

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

injuries or property damage caused by the insured or household members to other people or property. The perils for which insurance coverage is provided are broad (e.g., fire, theft, wind, vandalism, etc.), but some perils may not be covered, such as earthquakes. There are also similar personal property policies tailored for tenants or condominium owners. Commercial Property Insurance – Commercial property insurance is designed for commercial enterprises and professionals. While the exact wording may vary by insurer, it generally provides financial protection against the loss of, or damage to, real and personal property caused by a variety of perils, such as fire, lightening, business interruption, loss of rent/income, glass breakage, windstorm, water damage, and explosion. Commercial Liability Insurance – Commercial liability insurance is also designed for commercial enterprises and professionals. While the exact wording may vary by insurer, it generally provides insurance coverage for the legal liability of the insured or insured’s business resulting from damage to the property of others or personal injury to others. Some policies are primarily for liability coverage for manufactured products, while other policies are for professional liability coverage. Marine Insurance – This insurance traditionally compensates both the owner and transportor of goods that are transported overseas (or via air) for losses due to maritime perils, which are defined as “perils consequent on or incidental to navigation, including perils of the seas, fire, acts of pirates or thieves, captures, seizures, restraints … and all other perils of a like kind …”1.

1.4 - Affordability And Availability Affordability of insurance generally refers to the financial ability, or willingness, of an individual or business to purchase desired or required insurance coverage that is otherwise available.

1 Marine Insurance Act, 1993, C. 22, Section 2.

7

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Availability of insurance generally refers to the capacity and willingness of insurance companies to offer varying forms of insurance to consumers. Affordability and availability are relative concepts. Insurance that may be affordable to one individual or business may not be affordable to another individual or business. Insurance that is affordable one year may not be affordable some other year. Insurance that may be affordable in one jurisdiction may not be affordable in another jurisdiction. Availability of insurance is a function of the willingness of insurance companies to offer insurance coverage. What coverage one insurance company may be willing to offer may not be coverage that another insurance company may be willing to offer. Coverage that insurance companies offer in one year or in one jurisdiction may not be offered in another year or in another jurisdiction. “Capacity is a function of both capital available and the extent of exposure that insurers are prepared to have, to risks that are offered to them to insure. Willingness to offer insurance is based upon the characteristics of the particular risk and whether the insurance company believes that the level of risk, as measured against the price it is charging or the reinsurance protections it may have in place, is acceptable to it.”2 Affordability and availability problems may arise independently or jointly. They may arise for an entire category of insurance coverage (e.g., property insurance, automobile insurance, medical malpractice insurance, etc.), for one particular type of risk (e.g., homes or motorcyclists), for one particular type of loss (e.g., flood, earthquake), or for a particular amount of insurance coverage (e.g., insurance on homes that exceed $500,000).

2 “Effect of State Taxes on Insurance for Small Business,” by Pete Rose and Geoff Atkins, Trowbridge Deloitte Limited, July 2003.

8

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

1.5 – Hard Market When consumers have difficulty obtaining affordable insurance, or can’t obtain insurance at all, the insurance market is generally referred to as a “hard market.” A hard market may be caused by any of a number of circumstances, including the following.

Limited Market Competition – Absent rate regulation, the existence of limited market competition provides one or a small number of insurance companies the power to charge unreasonably high premiums. Such a market condition is also characterized by a general lack of incentive for product innovation or desire to address consumer needs.

Inability of Insurance Companies to Charge the Premiums Needed to Provide for Claim

Payments, Operating Expenses, and a Reasonable Profit – This situation may be caused by either unfair competitive practices or excessive governmental regulation. This often leads to the imposition of what is referred to as restrictive underwriting, a limitation in the type and amount of insurance coverage that is offered by insurance companies. Examples include restricting the types of insurance products sold, restricting the types of perils that will be insured, or restricting the insurance coverage offered to certain types of risks. Taken to an extreme, restrictive underwriting can lead to insurance companies withdrawing from a market.

A Disconnect Between What Insurance Coverage is Desired and What Insurance Coverage is

Offered – This is often a temporary situation that is caused by a sudden demand for a type of insurance product that insurance companies have not yet fully developed. Identity theft insurance is an example of a relatively new insurance product.

Insurance Company Reduced Profitability (or fear of reduced profitability) - This can be

caused by a number of factors, many of which are inter-related, such as:

decreased investment income – A portion of an insurance company’s revenue is derived from investment returns on policyholder premiums and company surplus. When interest rates decline, or stock prices fall, the amount of investment income earned by insurance companies declines.

9

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

inadequate insurance premiums – The pricing of insurance products involves the

estimation of future costs. To the extent those estimates of future costs are too low, or to the extent that insurance companies choose to charge less than the actuarially determined premium, profits will likely suffer. Future cost estimates may be too low for a number of reasons, including new laws or court rulings that result in unanticipated increases in the number or severity of insurance claims; an unanticipated increase in the claims consciousness of those that suffer injuries; unanticipated surges in inflation rates; newly arising perils that were not contemplated, such as oil leakage liability from home heating oil tanks; or other unanticipated environmental changes. As well, companies may choose to charge less than the actuarially based premium for several reasons, including the desire to maintain or increase market share.

• Catastrophes – A single catastrophic event can significantly impair the insurance industry’s

surplus, and, hence, capacity to sell insurance. Insurance Company Insolvencies – Insurance company insolvencies, for whatever reason,

represent a financial burden on the insurance industry, and can lead to reduced profitability, and, hence, capacity to sell more insurance.

Fraudulent Claims – Fraud results in increased costs to insurance companies, which, in turn,

can lead to reduced profitability and a reduced willingness to sell insurance.

Concentration of Exposures – Insurance companies may restrict their writings in a particular market or geographical area if they feel they have written more business than their capital or reinsurance programs can support.

Unavailability of Reinsurance – The purchase of reinsurance is an important way for

insurance companies to spread their risk. Without reinsurance, insurance companies would likely decrease their writings in a market.

10

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

CHAPTER 2

The Situation in Newfoundland and Labrador 2.1 – Historical Profitability of Homeowners Insurance, Commercial Property Insurance, Commercial Liability Insurance, and Marine Insurance

Introductory Comments Determining the historical profitability of insurance products and assessing whether the earned profits are reasonable is a two-step process. First, the amount of profits must be determined, and second, the profits must be measured against a standard of reasonableness. Insurance company profits are measured as the difference between revenue and costs. Insurance companies have three sources of revenue:

• the premium they charge and collect for the insurance coverage they provide; • the investment income they earn on the premiums they collect; and

• the investment income they earn on the surplus that they carry.

Insurance companies incur two types of costs:

• the payments they make, or are expected to make, for claims filed by their insureds (hereafter we refer to these claim costs, which include both indemnification costs and claim settlement costs, as losses); and

• the operating expenses (e.g., salaries, commissions, marketing costs, etc.) that they incur.

11

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Therefore, in order to determine the historical profits of each of the four insurance products in the province, we add the three components of revenue to get total revenue, add the two components of costs to get total costs, and then subtract total costs from total revenue. We do this by year, and for each of the four insurance products. There are two basic sources of information for insurance company premium revenue and losses for the personal property, commercial property, commercial liability, and marine insurance products. One is the mandatory annual return, referred to as the P&C-1 or P&C-2, in which the premiums earned and losses incurred by insurance companies are provided by calendar year for each of these products. The second is the loss experience exhibits compiled by the Insurance Bureau of Canada (IBC) under the Personal Lines Statistical Plan, Commercial Lines Statistical Plan, and the Liability Statistical Plan. However, these IBC exhibits do not include the experience of all insurance companies, as insurance companies are not required to submit this information to IBC. Hence, the IBC reports do not provide a complete representation of premium revenue and losses in the province. For our calculation of premium revenue and losses, we rely upon the data compiled by the Office of the Superintendent from information presented in the annual returns, P&C-1 reports, prepared by each insurance company licensed (federally or provincially) in Newfoundland and Labrador. Unfortunately, there is no source of published information on the expenses of insurance companies selling these four insurance products in Newfoundland and Labrador. Therefore, we make an assumption as to the average amount of expenses incurred by insurance companies for each of the four insurance products. We state the assumed average expense cost as a percentage of the premiums earned by insurance companies, and the percentage we select is based on the following considerations and assumptions.

• that insurance companies that sell insurance through brokers pay an average commission rate of 20% of premium, plus a contingent commission that typically ranges from 1% to 3% of premium;

• that direct writer insurers (i.e., insurance companies that do not use brokers, but instead, use

salaried staff to sell their products), would have substantially lower business acquisition costs than companies that sell through brokers;

12

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

• that insurance companies pay a premium tax equal to 4% of premium;

• that costs for licenses and fees are approximately 1% of premium; and

• that other operating expense costs range from 8% to 12% of premium.

Based on these considerations, we select an average expense cost of 35% of premium for each product. That is, we assume that for every $100 of premium that an insurance company earns, $35 would be paid out in operating expenses. We believe this to be a reasonable assumption for all insurance companies, on average, but recognize that some insurance companies may have lower expense costs and some may have higher expense costs. Determining a precise standard of profit reasonableness, which will vary over time as economic conditions change, is a matter for economists to determine, and, thus, is outside the scope of this study. However, 5% of premium is a generally accepted rule of thumb standard for profit reasonableness, and we accept this as the standard against which we measure average profit reasonableness in this study. The selected expense cost of 35% of premium and the selected profit level of 5% of premium mean that 60% of premium (i.e., 100% less 35% less 5%) is the level of losses against which we measure profitability. As respects the investment income earned by insurance companies, we assume that any investment income earned on company surplus is implicitly reflected in our profit reasonableness standard. As respects the investment income earned by insurance companies on the premiums they receive (often referred to as the investment income on cash flow) we assume for the homeowners product and the commercial property product that this is relatively minimal as expenses and losses are paid relatively quickly and there is little opportunity for insurance companies to earn income on the investment of the premium.

13

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

But, unlike the property lines of business, the claims that occur under the commercial liability and marine products often take many years to settle. As a result there is a much greater opportunity for insurance companies to earn investment income on the premium that is collected until it is used to pay losses or operating expenses. While specific data for the average time period it takes to settle and fully pay commercial liability or marine losses and expenses is not available to us for Newfoundland and Labrador, based on our experience and judgement, we estimate the average time period is 5 years. Assuming insurance companies can earn investment income on their cash flow at a rate of 5% per annum, the current value of $1 in future settled claim payments is approximately $0.77. Based on these claim settlement and investment rate assumptions, a 78% loss ratio for commercial liability or marine insurance is financially equivalent to a 60% loss ratio for homeowners or commercial property insurance (.77x 78%=60%). Therefore, whereas a 60% loss ratio is the profit reasonableness standard we select for homeowners and commercial property insurance, our selected standard for commercial liability and marine insurance is 78%. Our assumed expense cost of 35% of premium, and our assumed reasonable profit level of 5% of premium, implies that if insurance companies had a level of losses that equalled 60% of premium (78% for commercial liability and marine), they would have achieved a reasonable level of profits. If insurance companies had a level of losses that exceeded 60% (or 78%) of premium, they would have achieved less than a reasonable level of profits (or possibly have incurred a loss). If insurance companies had a level of losses that was less than 60% (or 78%) of premium, they would have achieved an excessive level of profits. Note, hereafter we refer to the amount of losses as a percent of premium, as the “loss ratio.” Hence, a historical loss ratio of 60% (or 78%) implies a reasonable profit, a loss ratio in excess of 60% (or 78%) implies less than a reasonable profit, and a loss ratio less than 60% (or 78%) implies more than a reasonable profit.

14

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

We now present our findings as regards the historical profitability of these four insurance products in the province, based on the 60% and 78% loss ratio profit reasonableness standards we have selected.

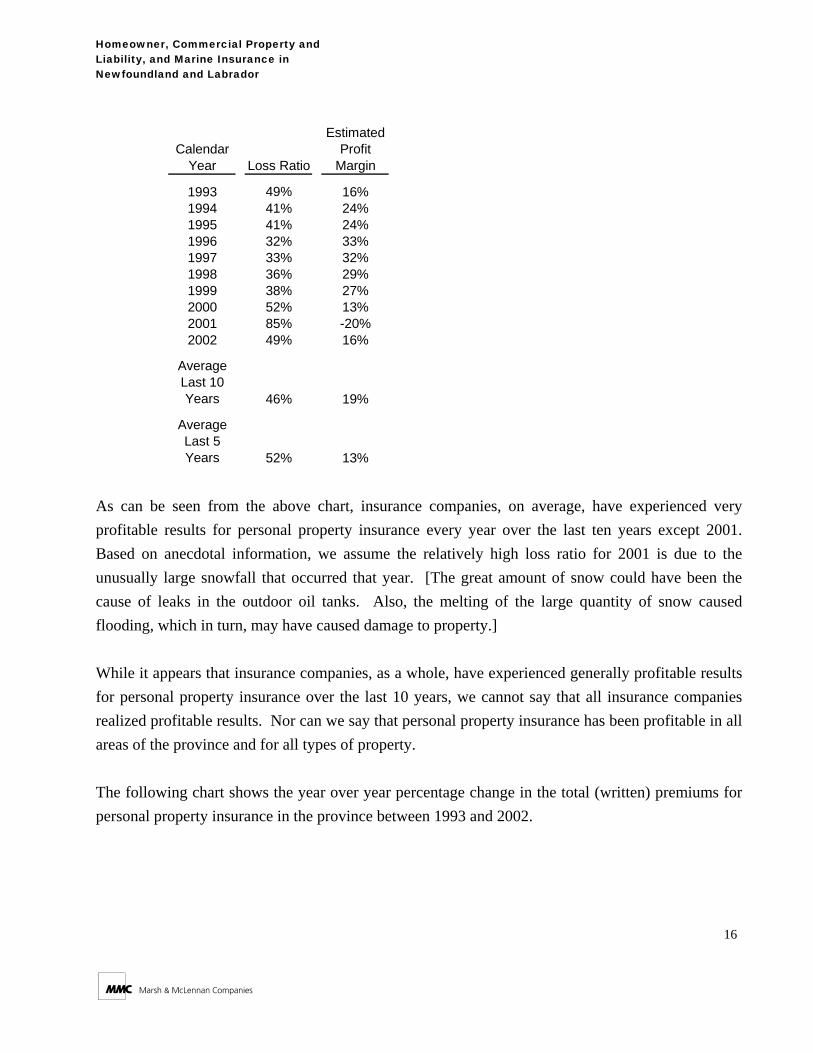

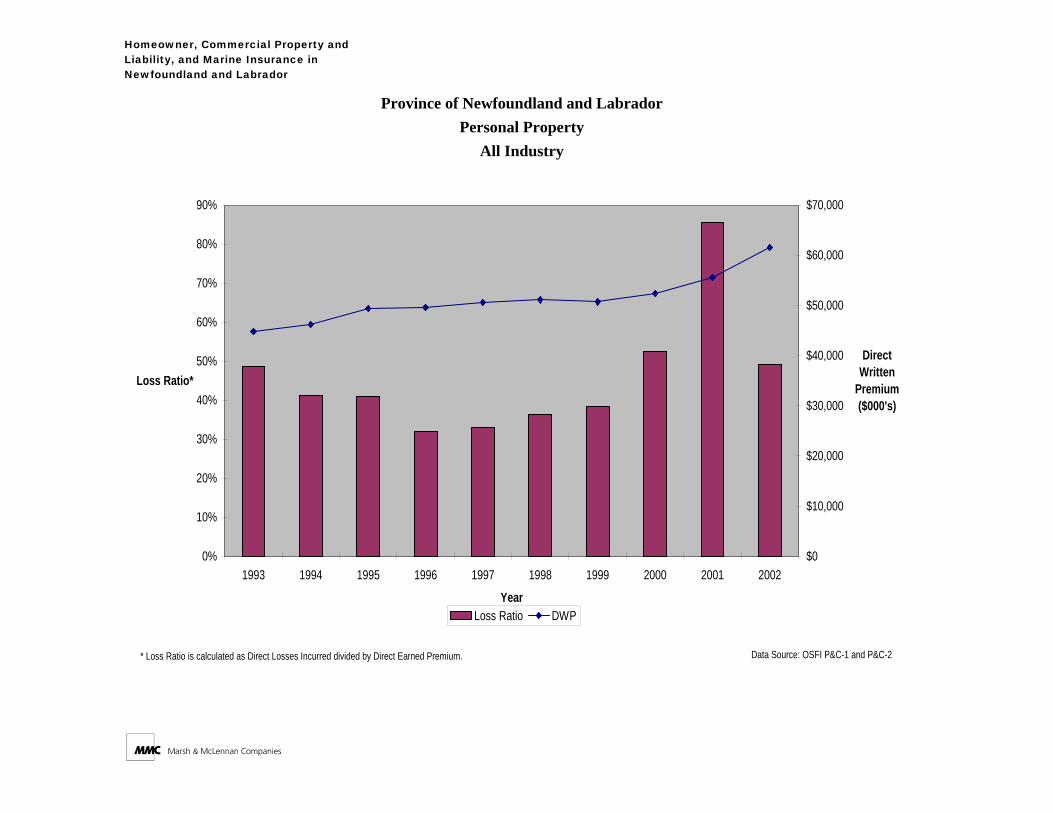

Homeowners As noted above, information for the homeowners product is not shown separately in the P&C-1 reports. Rather, the information for the homeowners product is combined with the information for other forms of personal property insurance, such as fire insurance policies. However, the homeowners product represents the majority of the personal property category of insurance. We reviewed the loss ratio history of all insurance companies that wrote personal property insurance in the province over the 10-year period, 1993-2002. The average loss ratio over the 10-year period was 46%, which is 14 percentage points less than the 60% loss ratio standard of reasonableness. This means that based on our standard, insurance companies have made, on average, a profit of 19%3 of premium over the last 10 years (100%-46%-35%). This is nearly four times our standard of profit reasonableness of 5% of premium. The loss ratio over this 10-year period was highest in 2001 at 85%, but was within the range of 33%-52% for the remaining 9 years. With the exception of 2001, the results for all years were well below the 60% loss ratio threshold target we have assumed. The following chart provides a range of estimated profit levels, based the loss ratio history and the expense ratio assumption of 35%.

3 Based on a premium to surplus ratio of 2 to 1, an investment income rate on surplus of 5%, and an income tax rate of 36%, a profit

margin of 19% implies the (after-tax) return on equity is 28%.

15

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Calendar Year Loss Ratio

Estimated Profit

Margin

1993 49% 16%1994 41% 24%1995 41% 24%1996 32% 33%1997 33% 32%1998 36% 29%1999 38% 27%2000 52% 13%2001 85% -20%2002 49% 16%

Average Last 10 Years 46% 19%

Average Last 5 Years 52% 13%

As can be seen from the above chart, insurance companies, on average, have experienced very profitable results for personal property insurance every year over the last ten years except 2001. Based on anecdotal information, we assume the relatively high loss ratio for 2001 is due to the unusually large snowfall that occurred that year. [The great amount of snow could have been the cause of leaks in the outdoor oil tanks. Also, the melting of the large quantity of snow caused flooding, which in turn, may have caused damage to property.] While it appears that insurance companies, as a whole, have experienced generally profitable results for personal property insurance over the last 10 years, we cannot say that all insurance companies realized profitable results. Nor can we say that personal property insurance has been profitable in all areas of the province and for all types of property. The following chart shows the year over year percentage change in the total (written) premiums for personal property insurance in the province between 1993 and 2002.

16

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Calendar Year

Written Premiums

in 'ooos

Annual Percentage

Change

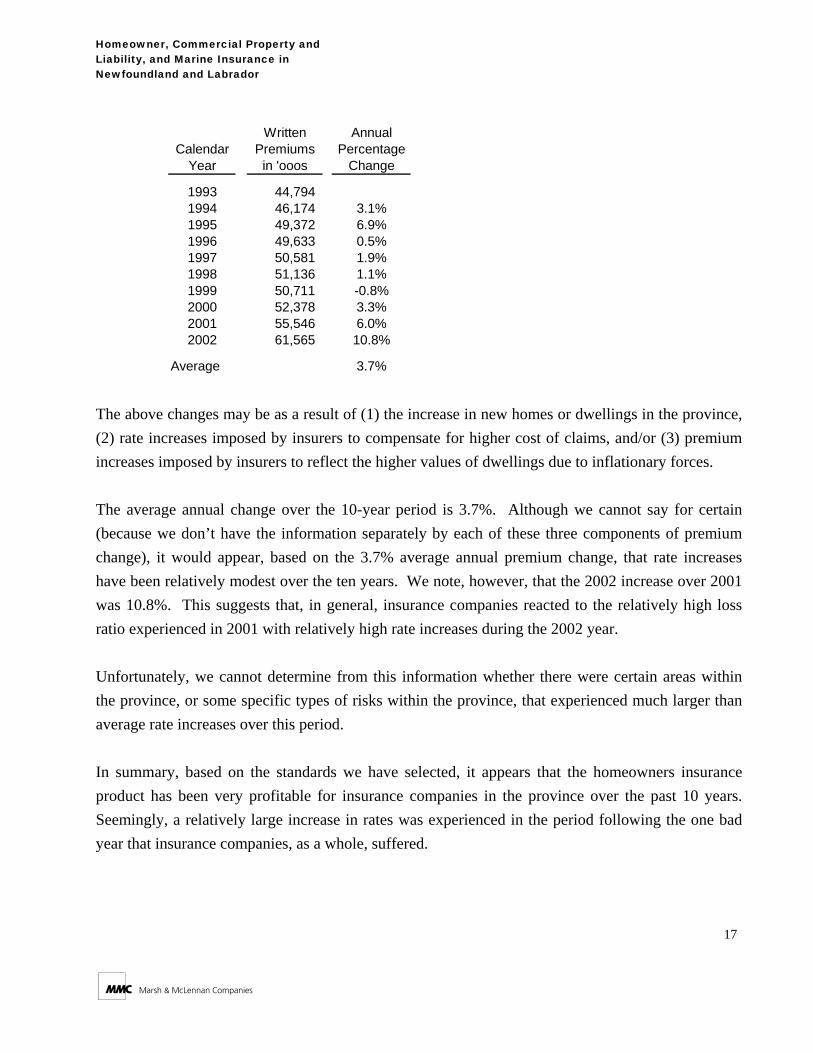

1993 44,794 1994 46,174 3.1%1995 49,372 6.9%1996 49,633 0.5%1997 50,581 1.9%1998 51,136 1.1%1999 50,711 -0.8%2000 52,378 3.3%2001 55,546 6.0%2002 61,565 10.8%

Average 3.7% The above changes may be as a result of (1) the increase in new homes or dwellings in the province, (2) rate increases imposed by insurers to compensate for higher cost of claims, and/or (3) premium increases imposed by insurers to reflect the higher values of dwellings due to inflationary forces. The average annual change over the 10-year period is 3.7%. Although we cannot say for certain (because we don’t have the information separately by each of these three components of premium change), it would appear, based on the 3.7% average annual premium change, that rate increases have been relatively modest over the ten years. We note, however, that the 2002 increase over 2001 was 10.8%. This suggests that, in general, insurance companies reacted to the relatively high loss ratio experienced in 2001 with relatively high rate increases during the 2002 year. Unfortunately, we cannot determine from this information whether there were certain areas within the province, or some specific types of risks within the province, that experienced much larger than average rate increases over this period. In summary, based on the standards we have selected, it appears that the homeowners insurance product has been very profitable for insurance companies in the province over the past 10 years. Seemingly, a relatively large increase in rates was experienced in the period following the one bad year that insurance companies, as a whole, suffered.

17

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

In Appendix 2 we present, graphically, the historical personal property loss ratios and premium for all companies combined.

Commercial Property We reviewed the loss ratio history of all insurance companies writing commercial property insurance (i.e., for retail stores, commercial buildings, etc.) in the province over the 10-year period, 1993-2002. The average loss ratio over the 10-year period was 63%, which is 3 percentage points more than the 60% loss ratio standard of reasonableness. This means that based on our standard, insurance companies, on average, have experienced somewhat less than reasonable profits over the last 10 years. The loss ratios over this 10-year period ranged from a high in 1994 at 103%, to a low of 30% in 1997. There is considerable year-to-year volatility in the loss ratio experience, with only 6 of the last 10 years at or below the 60% loss ratio standard. The following chart provides a range of estimated profit levels, based the loss ratio history and the expense ratio assumption of 35%.

18

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Calendar Year Loss Ratio

Estimated Profit

Margin

1993 71% -6%1994 103% -38%1995 63% 2%1996 47% 18%1997 30% 35%1998 47% 18%1999 103% -38%2000 56% 9%2001 59% 6%2002 52% 13%

Average Last 10 Years 63% 2%

Average Last 5 Years 63% 2%

As can be seen from the chart above, insurance companies, on average, have not experienced a reasonable level of profit over this 10-year period, and the results have fluctuated from year to year. Based on the 60% loss ratio standard, insurance companies, on average, have experienced profits in 7 of the last 10 years (1993-2002). And in 1 of those 7 years, the level of profit was less than the 5% reasonableness standard. Seemingly, however, while the insurance companies as a whole have experienced somewhat less than reasonable profits over the 10-year period, we cannot conclude that all insurance companies experienced the same financial results, or that this experience was realized for all locations or businesses within the province. There may very well have been some insurance companies, or some locations or businesses that had very different loss ratio experience. The following chart shows the year over year percentage change in the total (written) premiums for commercial property insurance in the province between 1993 and 2002.

19

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

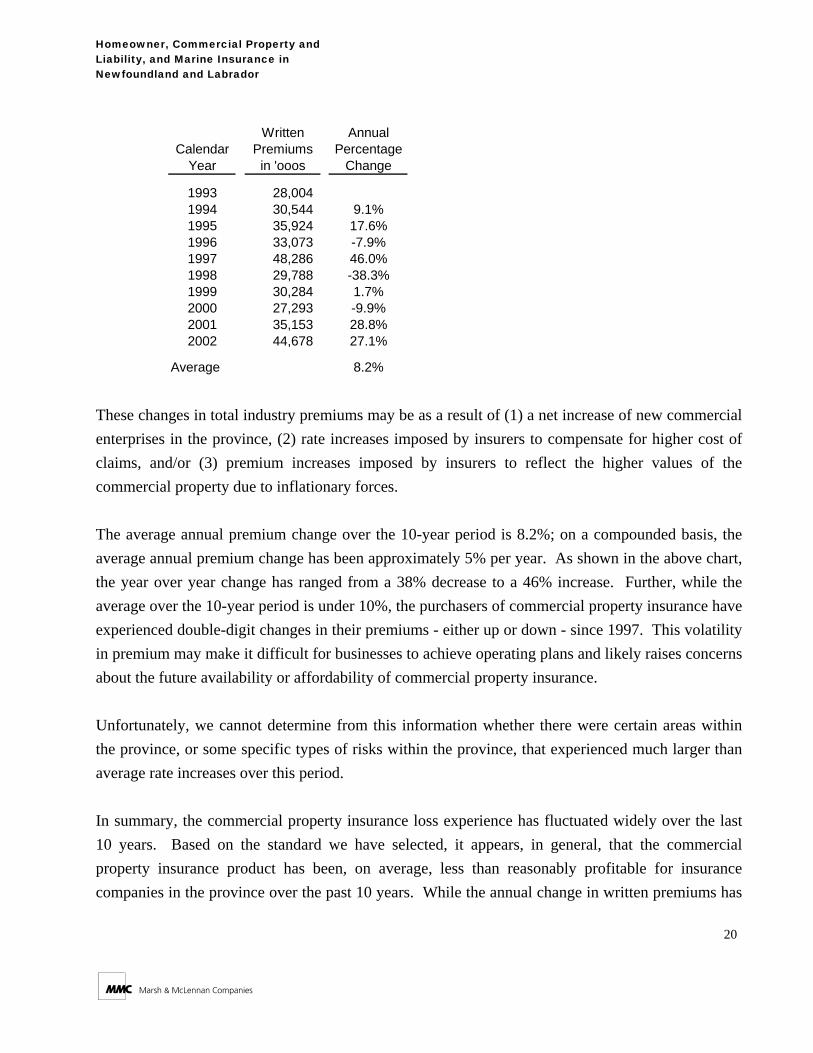

Calendar Year

Written Premiums

in 'ooos

Annual Percentage

Change

1993 28,004 1994 30,544 9.1%1995 35,924 17.6%1996 33,073 -7.9%1997 48,286 46.0%1998 29,788 -38.3%1999 30,284 1.7%2000 27,293 -9.9%2001 35,153 28.8%2002 44,678 27.1%

Average 8.2% These changes in total industry premiums may be as a result of (1) a net increase of new commercial enterprises in the province, (2) rate increases imposed by insurers to compensate for higher cost of claims, and/or (3) premium increases imposed by insurers to reflect the higher values of the commercial property due to inflationary forces. The average annual premium change over the 10-year period is 8.2%; on a compounded basis, the average annual premium change has been approximately 5% per year. As shown in the above chart, the year over year change has ranged from a 38% decrease to a 46% increase. Further, while the average over the 10-year period is under 10%, the purchasers of commercial property insurance have experienced double-digit changes in their premiums - either up or down - since 1997. This volatility in premium may make it difficult for businesses to achieve operating plans and likely raises concerns about the future availability or affordability of commercial property insurance. Unfortunately, we cannot determine from this information whether there were certain areas within the province, or some specific types of risks within the province, that experienced much larger than average rate increases over this period. In summary, the commercial property insurance loss experience has fluctuated widely over the last 10 years. Based on the standard we have selected, it appears, in general, that the commercial property insurance product has been, on average, less than reasonably profitable for insurance companies in the province over the past 10 years. While the annual change in written premiums has

20

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

been both volatile and relatively large, the compounded annual rate of change in premiums is only 5%. In Appendix 2 we present, graphically, the historical commercial property loss ratios and premium for all companies combined.

Commercial Liability We reviewed the loss ratio history of all insurance companies that wrote commercial liability insurance in the province over the 10-year period, 1993- 2002. The average loss ratio over the 10-year period was 81%, which is 3 percentage points more than the 78% loss ratio standard of reasonableness. This means that based on our standard, insurance companies, on average, have experienced somewhat less than reasonable profits over the last 10 years. The loss ratio over this period ranged from a high in 1997 at 120% to a low of 40% in 2002. There is a considerable amount of year-to-year fluctuation in the loss ratio experience. The following chart provides a range of estimated profit margins, based on the loss ratio history and the expense ratio assumption of 35%.

21

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

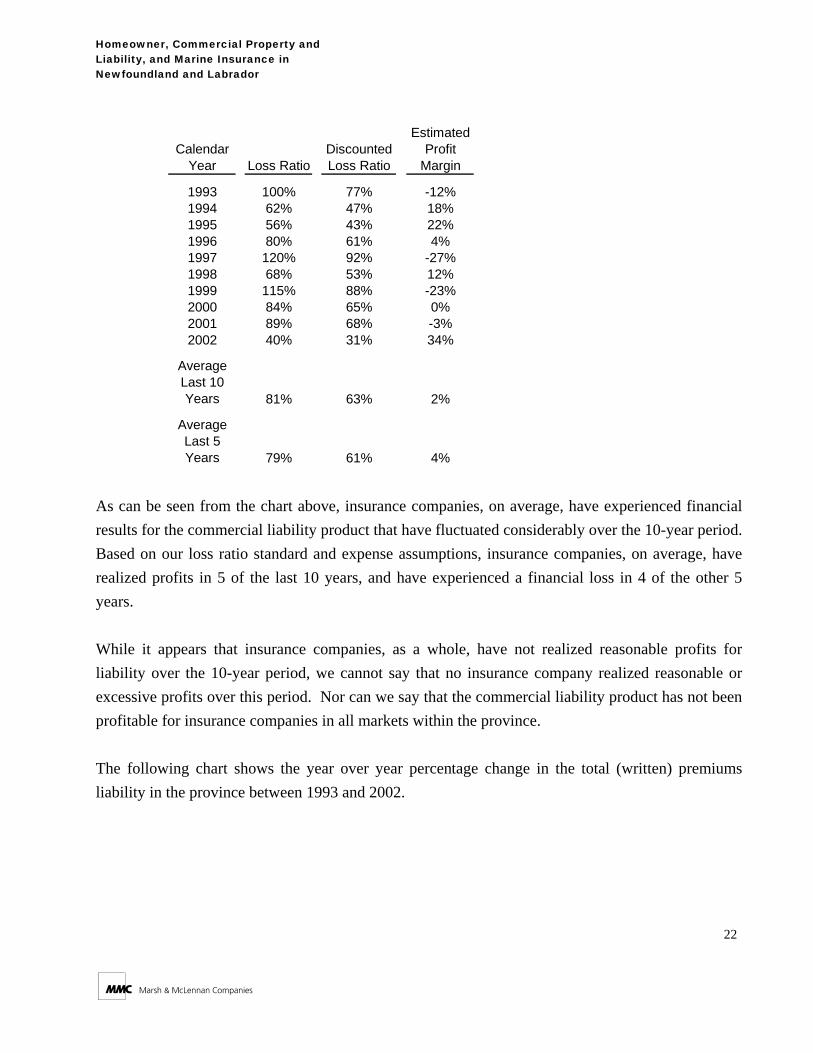

Calendar Year Loss Ratio

Discounted Loss Ratio

Estimated Profit

Margin

1993 100% 77% -12%1994 62% 47% 18%1995 56% 43% 22%1996 80% 61% 4%1997 120% 92% -27%1998 68% 53% 12%1999 115% 88% -23%2000 84% 65% 0%2001 89% 68% -3%2002 40% 31% 34%

Average Last 10 Years 81% 63% 2%

Average Last 5 Years 79% 61% 4%

As can be seen from the chart above, insurance companies, on average, have experienced financial results for the commercial liability product that have fluctuated considerably over the 10-year period. Based on our loss ratio standard and expense assumptions, insurance companies, on average, have realized profits in 5 of the last 10 years, and have experienced a financial loss in 4 of the other 5 years. While it appears that insurance companies, as a whole, have not realized reasonable profits for liability over the 10-year period, we cannot say that no insurance company realized reasonable or excessive profits over this period. Nor can we say that the commercial liability product has not been profitable for insurance companies in all markets within the province. The following chart shows the year over year percentage change in the total (written) premiums liability in the province between 1993 and 2002.

22

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Calendar Year

Written Premiums

in 'ooos

Annual Percentage

Change

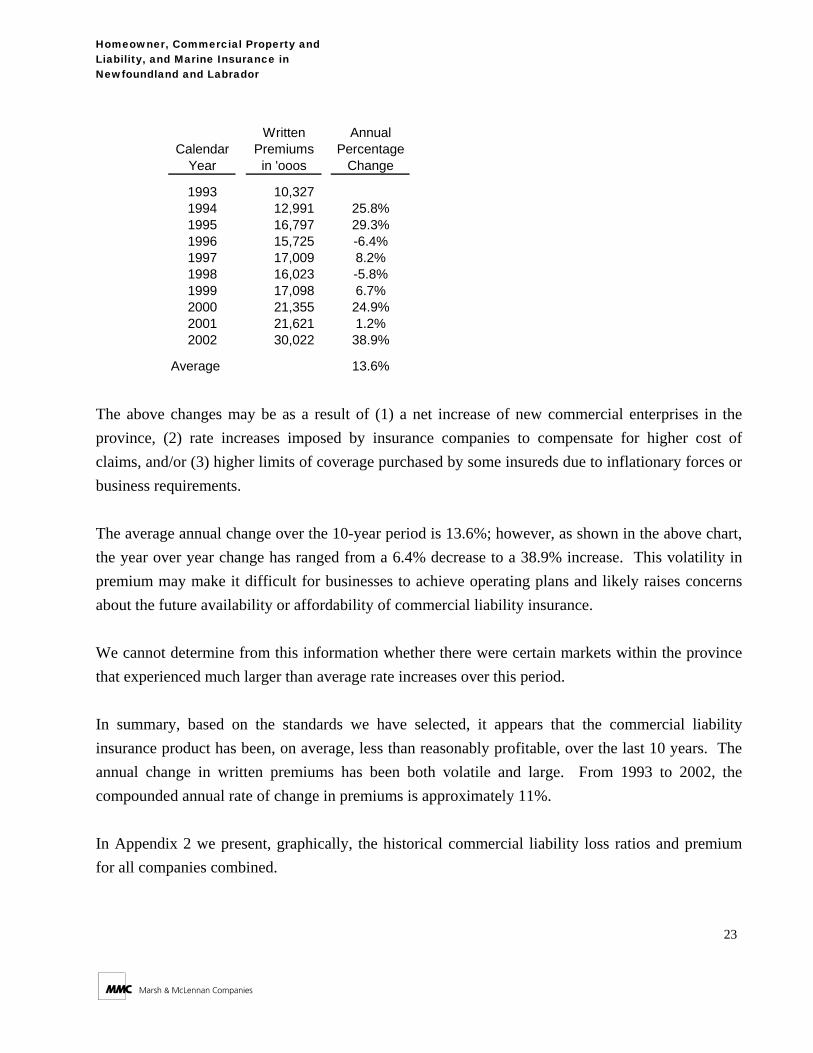

1993 10,327 1994 12,991 25.8%1995 16,797 29.3%1996 15,725 -6.4%1997 17,009 8.2%1998 16,023 -5.8%1999 17,098 6.7%2000 21,355 24.9%2001 21,621 1.2%2002 30,022 38.9%

Average 13.6% The above changes may be as a result of (1) a net increase of new commercial enterprises in the province, (2) rate increases imposed by insurance companies to compensate for higher cost of claims, and/or (3) higher limits of coverage purchased by some insureds due to inflationary forces or business requirements. The average annual change over the 10-year period is 13.6%; however, as shown in the above chart, the year over year change has ranged from a 6.4% decrease to a 38.9% increase. This volatility in premium may make it difficult for businesses to achieve operating plans and likely raises concerns about the future availability or affordability of commercial liability insurance. We cannot determine from this information whether there were certain markets within the province that experienced much larger than average rate increases over this period. In summary, based on the standards we have selected, it appears that the commercial liability insurance product has been, on average, less than reasonably profitable, over the last 10 years. The annual change in written premiums has been both volatile and large. From 1993 to 2002, the compounded annual rate of change in premiums is approximately 11%. In Appendix 2 we present, graphically, the historical commercial liability loss ratios and premium for all companies combined.

23

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Marine We reviewed the loss ratio history for marine insurance in the province over the 10-year period, 1993-2002. The average loss ratio over the 10-year period was 144%, which is 66 percentage points more than the 78% loss ratio standard of reasonableness. This means that based on our standard, insurance companies have experienced very unprofitable results over the last 10 years. The loss ratio over this period ranged from a high in 2002 at 270% to a low of 4% in 1997. There is considerable year-to-year volatility in the loss ratio experience, significantly more than the other three products. The following chart provides a range of estimated profit margins, based on the loss ratio history and the expense ratio assumption of 35%.

Calendar Year Loss Ratio

Discounted Loss Ratio

Estimated Profit

Margin

1993 192% 148% -83%1994 113% 87% -22%1995 86% 66% -1%1996 179% 138% -73%1997 4% 3% 62%1998 35% 27% 38%1999 219% 169% -104%2000 186% 143% -78%2001 160% 123% -58%2002 270% 208% -143%

Average Last 10 Years 144% 111% -46%

Average Last 5 Years 174% 134% -69%

As can be seen from the chart above, insurance companies, on average, have not experienced profitable results for the marine insurance product over the 10-year period. Based on our loss ratio

24

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

standard and expense assumptions, insurance companies, on average, have realized profits in 2 of the last 10 years, and have experienced significant financial loss in the other 8 years. The following chart shows the year over year percentage change in the total (written) premiums in the province between 1993 and 2002.

Calendar Year

Written Premiums

in 'ooos

Annual Percentage

Change

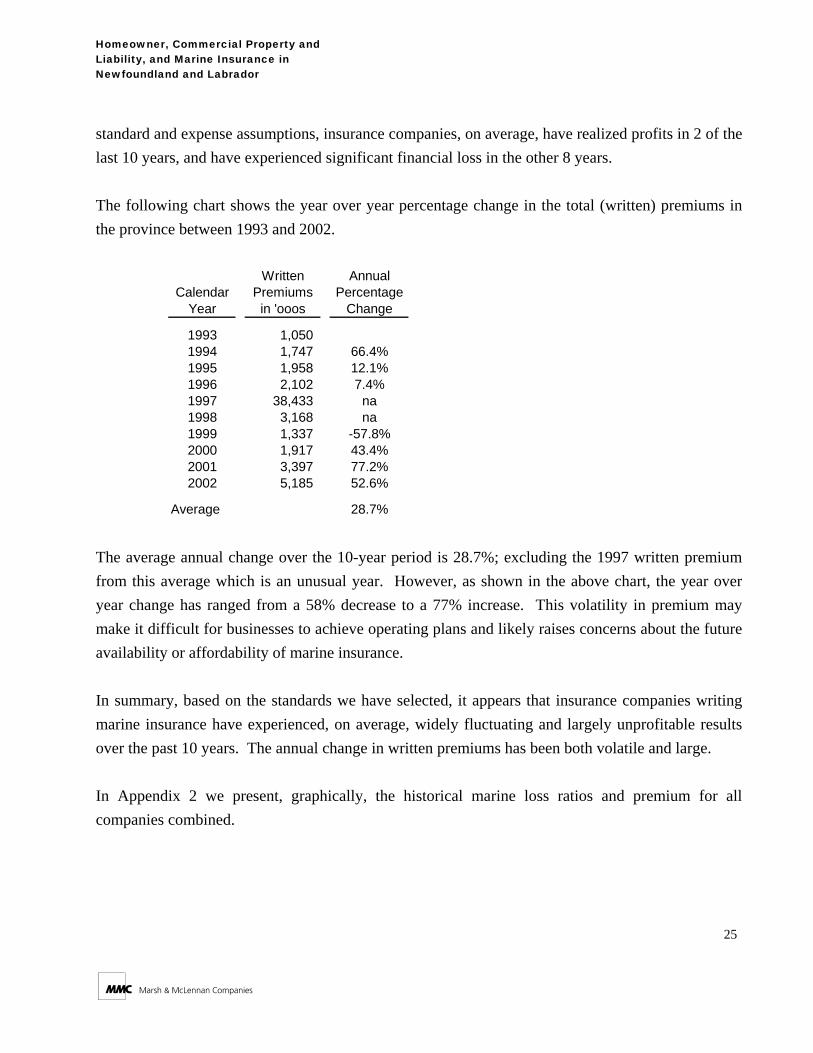

1993 1,050 1994 1,747 66.4%1995 1,958 12.1%1996 2,102 7.4%1997 38,433 na1998 3,168 na1999 1,337 -57.8%2000 1,917 43.4%2001 3,397 77.2%2002 5,185 52.6%

Average 28.7% The average annual change over the 10-year period is 28.7%; excluding the 1997 written premium from this average which is an unusual year. However, as shown in the above chart, the year over year change has ranged from a 58% decrease to a 77% increase. This volatility in premium may make it difficult for businesses to achieve operating plans and likely raises concerns about the future availability or affordability of marine insurance. In summary, based on the standards we have selected, it appears that insurance companies writing marine insurance have experienced, on average, widely fluctuating and largely unprofitable results over the past 10 years. The annual change in written premiums has been both volatile and large. In Appendix 2 we present, graphically, the historical marine loss ratios and premium for all companies combined.

25

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

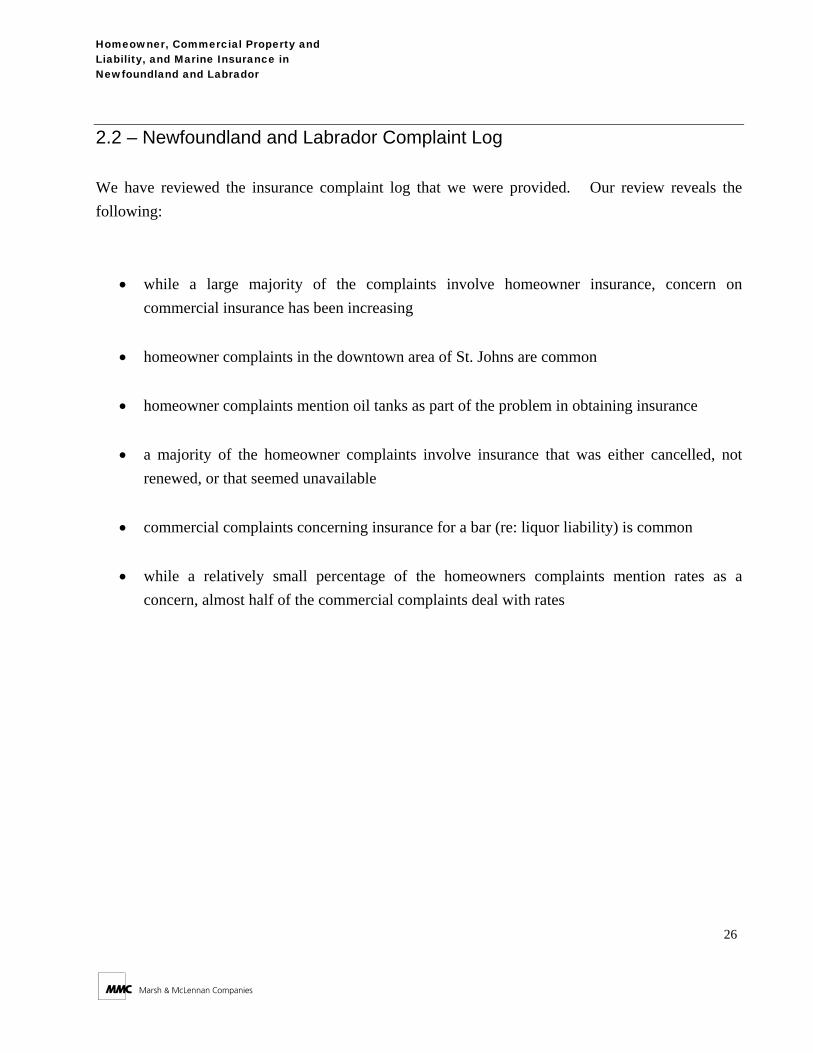

2.2 – Newfoundland and Labrador Complaint Log We have reviewed the insurance complaint log that we were provided. Our review reveals the following:

• while a large majority of the complaints involve homeowner insurance, concern on

commercial insurance has been increasing

• homeowner complaints in the downtown area of St. Johns are common

• homeowner complaints mention oil tanks as part of the problem in obtaining insurance

• a majority of the homeowner complaints involve insurance that was either cancelled, not renewed, or that seemed unavailable

• commercial complaints concerning insurance for a bar (re: liquor liability) is common

• while a relatively small percentage of the homeowners complaints mention rates as a

concern, almost half of the commercial complaints deal with rates

26

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

2.3 – Discussion with the Insurance Brokers Association of Newfoundland (IBAN) We interviewed IBAN spokespersons Mr. D. Swain and Mr. J. Legrow, who provided their perspectives of the current affordability and availability issues in the province, and who offered ways in which the brokers are helping to minimize these problems for consumers. A summary of their comments follows.

Personal Property In general, most consumers have been able to find affordable personal property insurance in the province, with annual rate increases well within the single digit range. However, for certain locations and certain types of risks, consumers have experienced problems finding insurance. In general theses risks are substandard; for example, they may lack recent updates to electrical wiring. A more common problem is the availability of insurance in the downtown areas. From IBAN’s perspective, it would appear that the downtown locations are less desirable to insurance companies for a combination of reasons: (1) insurance companies wishing to avoid an over concentration in one area, (2) proximity of adjacent sub-standard risks, and (3) substandard dwellings without recent updates. The insurance broker community has been working with the Office of the Superintendent of Insurance to find insurance for those risks unable to find insurance. Individual consumers that contacted the Office of the Superintendent were forwarded to IBAN. The broker community has been placing insurance for such orphaned risks through their insurance companies. In addition, several insurance companies have provided a “sub-standard” market for these personal property risks and have thus contributed to the solution to the personal property insurance availability issue. IBAN estimates that 30 risks were presented by the Superintendents’ Office to IBAN for special placement. Of these, only 2 were not offered insurance by the insurance companies. In one case, this was due to safety concerns, and in the other case, this was due to past claims problems.

27

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Commercial Property and Liability IBAN suggests there have been more affordability and availability problems in the commercial property and liability lines of business than in the personal property line of business. In general, IBAN estimates that annual rate increase have been in the 10% to 25% range - and often higher - making affordability an issue for many businesses. Some commercial businesses that traditionally have been difficult for insurance brokers to place, such as those with liquor liability exposure, have experienced very large rate increases. In many cases, even if the risk has very good loss control measures in place and no history of losses, large rate increase have been imposed. In some cases, certain risks have been unable to find affordable insurance to make their business enterprise feasible. Examples related to adventure tourism and snow plow operators were cited. The lack of available and/or affordable insurance has become an economic hurdle for certain businesses in the province. In the past, when the “regular” market insurers had exhausted their capacity or willingness to accept a commercial risk, the insurance broker would be able to place the risk through “specialty lines” writers. These specialty lines writers would act as the conduit between the broker and insurance companies, finding insurance markets for large or difficult commercial risks. However, for the first time, IBAN is finding even these specialty writers will not accept these “unwanted” risks at any price. Based on discussions IBAN has had with insurers, it expects the commercial insurance market to improve in 2004, with rates stabilizing and an increased acceptance of substandard risks.

28

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

2.4 – Insurance Company Operations within the Province From our analysis of the reported loss experience, our review of the complaint log, and our discussion with IBAN, we draw the following “high-level” conclusions about insurance company operations within the province.

Homeowners Homeowners (personal property) is the only insurance product where there is evidence that insurance companies, in total, may have realized excessive profits over the past ten years. Up until the 2002 year, average annual rate increases were seemingly modest. But in 2001 insurance companies suffered their first unprofitable year. The premium information and complaint log suggest that companies reacted to the 2001 experience by increasing rates more than normal, and by tightening up on underwriting – particularly in the downtown areas and homes with oil tanks. However, perhaps due to the cooperative efforts of the Superintendent’s Office, IBAN, and the insurance companies, there doesn’t appear to be a serious availability or affordability problem with this product. As respects oil tanks, we note the following:

1.) As the old tanks age, they rust (more often from the inside, which is why visual inspections are not effective) and can leak. The very major expense of environmental cleanup from this occurrence, while covered under the homeowners policy, is not contemplated in the rates, as such losses have not occurred in the past. While newer tanks are double-walled, older tanks were not. They are only now becoming old enough to rust and leak.

2.) The snowstorms of 2001, with the heavy weight of snow on unprotected tanks, and

subsequent freezing and thawing, may have weakened tanks further, causing leakage and bringing this potential loss situation to the attention of insurers.

29

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

In the Recommendations section of this report, we suggest ways in which the Government can further address issues concerning homeowners.

Commercial Property Commercial property has been less profitable than homeowners over the past 10 years, and the profits have not been excessive. Despite relatively favourable results in each of the years 2000, 2001, and 2002, there is evidence of relatively large rate increases in 2001 and 2002. We suspect that any availability or affordability problems that commercial businesses may have primarily stem from the commercial liability exposure. In the Recommendations section of this report, we suggest ways in which the Government can further address issues concerning commercial property.

Commercial Liability Commercial liability has been less than profitable for insurance companies over the past 10 years, and the experience is marked by large fluctuations. Companies suffered financial losses in 2001, and like for the homeowners product, seemingly responded by sharply increasing rates and tightening up underwriting. The risks that have been the most affected by these actions are those with a liquor liability exposure, those involved with tourism, and snow plow operators. In the Recommendations section of this report, we suggest ways in which the Government can further address issues concerning commercial liability.

Marine It is difficult for us to reach even high-level conclusions about the marine insurance product. The reported experience suggests that this has been a very unprofitable product for insurance companies, but we have no information to understand why this is the case. Premium volume has fluctuated widely over the years, but the cause is not clear. And there are no complaints that deal with this product.

30

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

We offer some comments on this product in the Recommendations section.

31

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

CHAPTER 3

Insurance Regulation

3.1 – Goals of Insurance Regulation Government has the “full power and authority to make, constitute and ordain Laws, Statutes, and Ordinances, for the public welfare and good government.”4 In the specific area of insurance, the generally recognized goals of governmental regulation are to ensure that:

• the cost of insurance is affordable for those requiring insurance • necessary insurance is available for the those requiring insurance

• insurance companies are financially able to deliver on their contractual obligations to provide

insurance coverage for future events

• insurance companies comply with insurance laws and regulations

• fraud and abuse by both insurance companies and insureds are controlled. In short, the primary goal of insurance regulation is to protect the consumer, whether the consumer is an individual or a business. There is, however, in Canada (and in other countries), an additional goal of insurance regulation: the creation and enforcement of laws and regulations (such as anti-trust laws) to “... maintain and encourage competition in Canada in order to … provide consumers with competitive prices and

4 Royal Instructions to Governor Darling, 1855.

32

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

product choices.”5 We quote from a speech made by Thomas Murin, Chairman of the Federal Trade Commission in 2002, “…faith in the market system is firmly grounded on the principle that free enterprise and competition are the best guarantors of commercial freedom, economic efficiency, and consumer welfare. Effective competition is most likely to yield the optimal mix of goods and services at the lowest cost.”6 If the premise is accepted that market competition is good and should be encouraged, then successful regulation of insurance requires achieving the goals noted above within a free enterprise and competitive market environment. We focus on the issues of affordability and availability in this report.

3.2 – How Government Regulates Insurance The goals of insurance regulation as respects the affordability and availability of insurance may be achieved through the manner in which a government chooses to regulate or monitor insurance company products (i.e., policy forms, underwriting rules, and rates), insurance company financial results, and insurance company operations.

Insurance Company Products By insurance products, we mean the policy forms, underwriting rules, and rates used by insurance companies. Policy forms set forth the contractual obligations of the insurance company as respects losses or damages suffered by the policy-owner. Who is insured, what is insured, and the perils for which insurance is provided are set forth in the policy forms. Policy forms vary by the type of insurance

5 Canadian Competition Act, R.S. 1985, C-34, Section 1.1.

6 Remarks by T.J. Muris, Chairman, Federal Trade Commission at the Milton Handler Annual Antitrust Review, December 10, 2002,

New York, NY.

33

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

coverage offered. And although each insurance company has its own policy forms, to a large degree policy wording is standardized. Underwriting rules set forth the company’s criteria for accepting risks. While underwriting rules vary from company to company, they must comply with anti-discrimination laws and public policy. Rates are the prices that insurance companies charge for the insurance coverage that they provide. Insurance rates vary by type of coverage, and by the risk characteristics of the insured. For example, in homeowners insurance, rates vary by the location of the home, by the form of fire protection that services the home, the construction material, the existence of fire and burglar alarms, and other risk variables. The insurance statutes in most jurisdictions require that rates be adequate (to ensure insurance company solvency), not excessive (to ensure insurance is affordable), and not unfairly discriminatory (to ensure that rates are fair). It is becoming more and more common, particularly as respects automobile insurance, for insurance companies to have two or more sets of rates (referred to as rating tiers). Risks that meet the most rigorous of standards, called preferred risks, are charged lower rates than risks than standard or non-standard risks. Rating tiers, as they are referred to, provide companies with greater flexibility to accept risks. There are five basic ways in which governments regulate insurance company products. They are as follows. Prior Approval – Under a prior approval system of product regulation, policy forms, underwriting rules, and/or rates must be filed with the government (i.e., insurance regulator) and approved before being used by the insurance company. Often there is a time limit within which the government must act or the filing is deemed approved. In practice, there is considerable variation in how prior approval systems operate. The following are examples of the ways that a prior approval system can vary.

Prior approval requirements may apply to forms, underwriting rules, and rates, or may apply to one or two products and not the other(s).

Prior approval requirements may only apply to certain types of insurance.

34

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

The degree to which filings are reviewed can vary considerably.

Prior approval requirements may only apply to rate changes of a certain magnitude, or to rates that fall within a certain range.

File & Use – Under a file & use system of product regulation, policy forms, underwriting rules, and/or rates must be filed with the government prior to their use, but may be used within a certain time period (prescribed by statute, and usually varying from between 30 to 75 days) following their submission. The government may, however, retroactively disapprove the filing after it has been implemented. Like prior approval systems, there is considerable variation in how file & use systems operate. Use & File - Under a use & file system of product regulation, policy forms, underwriting rules, and/or rates may be implemented by an insurance company prior to their being filed with the government, but then must be filed within a prescribed number of days following their effective date (usually from 30 to 75 days). The government may, however, retroactively disapprove the filing after it has been implemented. Like prior approval systems, there is considerable variation in how use & file systems operate. No File – Under a no file system of product regulation, policy forms, underwriting rules, and/or rates are not required to be filed with the government. Mandated – Under a mandated system of product regulation, the government dictates the policy forms, underwriting rules, and/or rates to be used. These forms of insurance product regulation are not consistently applied among the three product components, or by type of insurance. For instance, for homeowners insurance, in the U.S., it is not unusual for forms to be subject to prior approval, but for rates to be subject to file & use. And marine insurance is typically treated as no file. Typically, under the regulatory systems where product changes can be disapproved, the government will seek to have the insurance company amend its filing rather than issuing an order of disapproval. However, if a filing is disapproved, the insurance company is usually given an opportunity to justify

35

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

its request at a public hearing, run by the government in a quasi-judicial manner, with witnesses and testimony given under oath. In some jurisdictions, insurance rates are also controlled through the regulation of insurance company profits (referred to as excess profits regulation). Under excess profits regulation, insurance companies must periodically (typically every two or three years) perform a prescribed calculation showing the profit or loss made by the company for the line of business of concern. Should the calculations show a return higher than government deems acceptable, insurance companies are ordered to make refunds to policyholders. The regulation of policy forms is most generally focused on “readability.” The very legal nature of the insurance contract makes it difficult for the average consumer to understand. There is less of a need for such policy form regulation in the case of commercial insurance, where businesses are considered to be more sophisticated about insurance and have advisors (lawyers or risk managers for instance) for guidance. A few jurisdictions in the U.S. require the formal filing of selection rules. A very few must approve the rules prior to implementation. Regulatory systems requiring the filing of policy forms or rates are common in the U.S. (refer to Appendix 2), subject to variations. These systems are not as prevalent in Canada, and where filings requirements exist, they usually only apply to automobile insurance.

Insurance Company Financial Results The purpose of monitoring the financial results of insurance companies is to ensure financial health and minimize the risk of insurance company insolvencies. Governments monitor the financial results of insurance companies in two ways. Every insurance company is required to annually file with the government prescribed financial statements that present the company’s financial results for the year. In the U.S., this financial statement is referred to as the Annual Statement, and it must be filed with the company’s state of domicile. In Canada it is referred to as the P&C-1 or P&C-2. Both the Annual Statement in the U.S. and the P&C-1 or

36

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

P&C-2 in Canada must be accompanied by a statement, signed by a qualified actuary, that presents the actuary’s opinion as to the reasonableness of the loss and premium (Canada only) liabilities carried by the company. Governments also conduct periodic financial examinations (audits) of insurance companies. The Office of the Superintendent of Financial Institutions (OSFI) will audit federally licensed insurers writing insurance in Newfoundland and Labrador, whereas the Office of the Superintendent of Insurance in Newfoundland and Labrador is responsible for the financial review of the provincially licensed insurance companies.

Insurance Company Operations Governments regulate or monitor the manner in which insurance companies operate through market conduct examinations and by reviewing complaints made against insurance companies. Such examinations are performed primarily to ensure customers are treated fairly. They also serve as a means to learn of any possible availability or affordability problems. One area that is examined in a market examination is terminations. Companies terminate risks to maintain or improve their financial results. A large number of terminations over a relatively short period of time could be an indication of an availability problem. Virtually all jurisdictions in the U.S. have statutes on the books regulating when policies may or may not be cancelled or non-renewed. The concept is similar to how the Section 104 of the Newfoundland and Labrador Insurance Companies Act sets out when automobile terminations are permissible. Governments also monitor complaints files against insurance companies as a means to learn of possible availability problems.

Regulation of Homeowners, Commercial Property, Liability and Marine

Insurance In Canada, there is no rate or product related filing requirement imposed by any provincial regulator for the four lines of business under review. While most provinces regulate the rate level and legislate the coverage of automobile insurance, there is no specific legislation or regulation for

37

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

homeowners, commercial property, liability and marine. In Exhibit 1 of this report we provide a summary of the filing requirement for most of the U.S. states for commercial property & liability and homeowners insurance. With very few exceptions, most states have filing requirements for the rate levels and coverage/rules/forms. Unlike the Canadian provinces, the U.S. states do not leave these products up to the forces of competition amongst the insurers to self-regulate themselves.

3.3 – Pros and Cons of Insurance Regulation Depending upon the form of regulation and the way it is implemented, regulation of insurance company products or operations could result in suppressed insurance premiums, which could create financial difficulties for insurance companies, and which, in turn, could lead to or exacerbate availability problems, and suppressed market competition, which could lead to a stifling of creative solutions to problems. There are high costs associated with the regulation of insurance. “In some cases it is possible that action will not improve the problem, or alternatively, that the problem may solve itself (e.g., where markets are moving rapidly). Government action may only shift the problem elsewhere, or the costs of government action may be greater than the costs imposed by the problem it is designed to correct”7. Still, when the insurance market forces are not operating in a way that benefits insurance companies and consumers, and availability or affordability problems persist, and all other efforts fail, some manner of insurance regulation of insurance company products or operations may be beneficial.

7 “Alternatives to Regulation”, Regulatory Impact Unit, Cabinet Office, Government of Great Britain, http://www.cabinet-office.gov.uk/regulation/ria-guidance/content/alt-regulation/index.asp

38

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

CHAPTER 4

Ways to Address Availability and Affordability Problems 4.1 – Residual Market Mechanisms

Introduction There are a multitude of government-sponsored programs that have been tried to address the issues of availability and affordability. Some are only slight variations of others and the mechanics of each can vary. They all have at least one or more of the following characteristics:

• Government sanction/mandate • Government or quasi-government participation

• Spread of risk beyond what individual insurance companies could accomplish individually

A description of the more common programs follows.

Fair Access to Insurance Requirements (F.A.I.R Plans) F.A.I.R. Plans are common in the U.S. A F.A.I.R. Plan is a state established program that requires insurance companies who write property insurance to accept risks in economically depressed areas in the same proportion as their other business bears to the total property insurance market. In most states, the laws also provide for a facility that distributes risks among the participating insurance companies. These plans are very similar to the more widely used “Assigned Risk” or risk sharing pool plans for automobile. Increasingly, F.A.I.R plans have been expanding their offerings to

39

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

coastal risks in addition to those in urban areas. Both personal and commercial risks may be written in this manner.

Market Assistance Program (M.A.P.) A “... Market Assistance Program, is a voluntary industry program in which licensed homeowner insurance companies consider applications for insurance from residents ... that have been unsuccessful in securing coverage through the voluntary market.”8 The M.A.P. is the least intrusive of the residual market alternatives, simply assisting those in need of insurance to connect with an insurance company willing to write the risk. In the mid-1980s, M.A.P.s were used in the U.S. for many small businesses such as bars. Based upon discussion with the Insurance Brokers Association of Newfoundland (IBAN), it appears that this is already occurring on an informal basis in Newfoundland and Labrador.

Joint Underwriting Association (JUA) The JUA is a method to provide insurance to those who cannot obtain it in the voluntary market. In a JUA, there are a limited number of companies that issue and service policies at an identical rate level set by government. These “servicing carriers” are paid a set amount for expenses and claim settlements, but the ultimate costs are borne by all companies writing similar insurance in the province. Applications are submitted to the servicing carrier, who performs all operations of an insurance company. Products offered are usually standard, but with lower maximum limits and fewer miscellaneous endorsements. In some cases, deficits may be assessed to policyholders or premium taxes paid to government may be reduced, in addition to assessing all insurance companies in the jurisdiction for losses incurred by the JUA.

8 NJ Department of Banking and Insurance – Windstorm-Map Q and A. http://www.state.nj.us/dpbi/windqna.thm.

40

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Wind Pools Also called “Beach Pools” or “Coastal Pools,” these popular residual market mechanisms normally write wind-only coverage in areas vulnerable to windstorm (such as hurricane) losses. The pool may be set up to write different deductibles or coverages and for specified types of insureds, as may be needed. Coverage may be available to that government-specified geographical location where coverage cannot be purchased in the standard market. The product sold is often called a “wrap,” as it “wraps around” and coordinates with voluntary market policies. A recent trend has been for these plans to be merged into the F.A.I.R. plans.

Reinsurance Facility In the most common type of reinsurance facility, insurance companies are required to write the target class of business, but may “cede” the risk, or some part of the risk, to a single entity. This “facility” then combines the losses and spreads them over all companies writing similar business in the province. Formulas vary on how the losses are allocated to company. There are also often “incentives” in the form of lower assessments or credits for insurance companies that write more than their share of the under-served risks.

Government-Run Insurance Normally reserved as a last resort, the government could create its own “insurance company” (usually as a non-profit enterprise) to write coverage not available in the marketplace. Logically, the potential exists to reduce costs via greater efficiency in operations (due to potentially larger size of the endeavour and lack of competition), as well as the non-profit nature of the enterprise. This entity issues policies and settles claims like any other insurance company, but losses are either paid for by government revenues, assessed back to policyholders, or assessed to all insurance companies. The Newfoundland and Labrador Crop Insurance Agency, which operates with the cooperation of the Federal government under the authority of the Farm Income Protection Act, can be viewed as government-run insurance. Of course, in several provinces automobile insurance is government-run.

41

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Pros and Cons of Residual Market Mechanisms Residual market mechanisms normally run a financial loss, and, therefore, require a funding mechanism, whether it is directly from government funds or through a process of assessing insurance companies. To this extent, residual market mechanisms are a form of risk spreading. In the U.S., in the 33 years for which data is available, F.A.I.R and Beach plans alone have generated losses amounting to $2 billion dollars. While definitely a safety net for those who cannot obtain insurance, the existence of this safety net may discourage innovation in the marketplace, and insureds may end up in the residual market that might otherwise have been able to obtain insurance in the standard market. In hard markets, the residual market may become the largest insurer in the jurisdiction, placing the government squarely in the insurance business. Even if not government run, government must carefully regulate and monitor these residual market mechanisms, which have cost implications to government. F.A.I.R. Plans, Wind Pools, JUAs, Reinsurance Facilities, and Government-Owned Insurance Companies are costly to establish and maintain. In many respects their operation is similar to that of an insurance company. For example, in a F.A.I..R. Plan, underwriting, rating, claims handling, accounting, and administrative functions must be performed.

4.2 – Additional Risk Spreading Mechanisms There are a number of additional ways to spread risk should the root of an availability problem be due to catastrophe potential or the belief of insurance companies that they would be unable to charge enough premiums to cover the potential risk. Some of these mechanisms exist in North America today, but even for those already in existence, enabling legislation may be possible to make it easier for the right groups to adopt them.

42

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador

Surplus Lines Carriers When a particular insurance product is unavailable in the market from a regularly licensed insurance carrier, insurance regulations can permit the broker to place coverage with a non-admitted insurance company. There are usually protections built into the regulations to assure the quality of both the broker and company are high. One requirement is that an attempt must be made to first place the insurance with a regularly licensed company. The Newfoundland and Labrador Insurance Adjuster, Agents and Brokers Act permits such activity, and specific requirements are described in Section 24 of the Act.

Reciprocal Exchange A “Reciprocal Exchange” is “an unincorporated group of individuals, called subscribers, who mutually insure one another, each separately assuming his share of each risk.”9 In the context of this report, a reciprocal could be used by a group of businesses who might be experiencing difficulty obtaining insurance (for instance, tavern owners or doctors). The individuals band together to form a risk retention group that spreads the risk (loss and profits) amongst its members. Every reciprocal is different as they are based upon the agreement of its members and thus are very flexible. “In Canada, a number of school boards, hospitals and universities have established such reciprocal exchanges.”10 Reciprocal exchanges are permissible by the Newfoundland and Labrador Insurance Companies Act (Sections 109-129).

Captive Insurance Companies “A captive insurance company is an insurance company that has been set up to provide coverage at a lower cost than available by going through the general insurance market. The company's stock is controlled by one interest or a group of related interests so as to provide coverage for their business

9 InsWeb, http://www.insweb.com/learningcenter/glossary/general-r.htm 10 “Property and Casualty Insurance in Canada,” Department of Finance, April 1999, http://www.fin.gc.ca/toec/1999/propertye.html

43

Homeowner, Commercial Property and Liability, and Marine Insurance in Newfoundland and Labrador